Financial Ratio Analysis: EasyJet PLC vs Ryanair - ACFI5020 Report

VerifiedAdded on 2023/04/21

|25

|5096

|190

Report

AI Summary

This report undertakes a comprehensive financial analysis of EasyJet PLC and its competitor, Ryanair, focusing on a five-year period. It begins with a comparative ratio analysis, examining profitability (operating profit, gross profit, and ROCE), liquidity (current and acid-test ratios), working capital efficiency (receivables and payables periods), and long-term financial structure (gearing ratio). The analysis uses financial data to assess each company's performance, offering insights into their strengths and weaknesses. The report then provides investment recommendations, considering the financial health of EasyJet and Ryanair, and their potential for investors. Finally, the report explores EasyJet's supply chain management system, discussing relevant models and challenges faced by the airline, concluding with a summary of findings and recommendations.

Running head: ACCOUNTING

Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING

Table of Contents

Brief Overview:..........................................................................................................................2

Task One - Ratio Analysis:........................................................................................................2

Profitability Ratios:................................................................................................................2

Liquidity Ratios:.....................................................................................................................6

Working Capital Efficiency Ratios:.......................................................................................9

Long term financial structure ratios:....................................................................................11

Investors Perspective Ratio:.................................................................................................12

Task Two: Recommendation to Buy, Sell or Hold for investors and potential Investors:......14

Task Three: Supply Chain Management System of Easy Jet..................................................15

Types of Models in Supply Chain Management......................................................................16

Issues faced by Easy Jet...........................................................................................................18

References:...............................................................................................................................19

Appendix: Workings................................................................................................................21

Table of Contents

Brief Overview:..........................................................................................................................2

Task One - Ratio Analysis:........................................................................................................2

Profitability Ratios:................................................................................................................2

Liquidity Ratios:.....................................................................................................................6

Working Capital Efficiency Ratios:.......................................................................................9

Long term financial structure ratios:....................................................................................11

Investors Perspective Ratio:.................................................................................................12

Task Two: Recommendation to Buy, Sell or Hold for investors and potential Investors:......14

Task Three: Supply Chain Management System of Easy Jet..................................................15

Types of Models in Supply Chain Management......................................................................16

Issues faced by Easy Jet...........................................................................................................18

References:...............................................................................................................................19

Appendix: Workings................................................................................................................21

2ACCOUNTING

Brief Overview:

Easy Jet Plc is one of the British low cost airline company having its headquarter in

London Luton Airport. The airline operates both in the overseas and domestic segment

having greater than 820 routes in around 30 nations. Ryanair on the other hand is Irish low-

cost airline that has its headquarter in Dublin Ireland. The company has its primary

operations at Dublin and London Stanstead airports.

The present report here provides a comparative analysis of performance between Easy

Jet Plc and its competitor Ryanair. The report would consider the five-year analysis of

financial ratio between Easy Jet Plc and benchmarking the same with its competitor Ryanair.

Later the report would also determine the rationale for making investment in the shares of

EasyJet Plc from the perspective of investors. Finally, analysis of EasyJet supply chain

management process would be considered in this report with an appropriate conclusion

supporting the analysis.

Task One - Ratio Analysis:

Profitability Ratios:

Operating Profit:

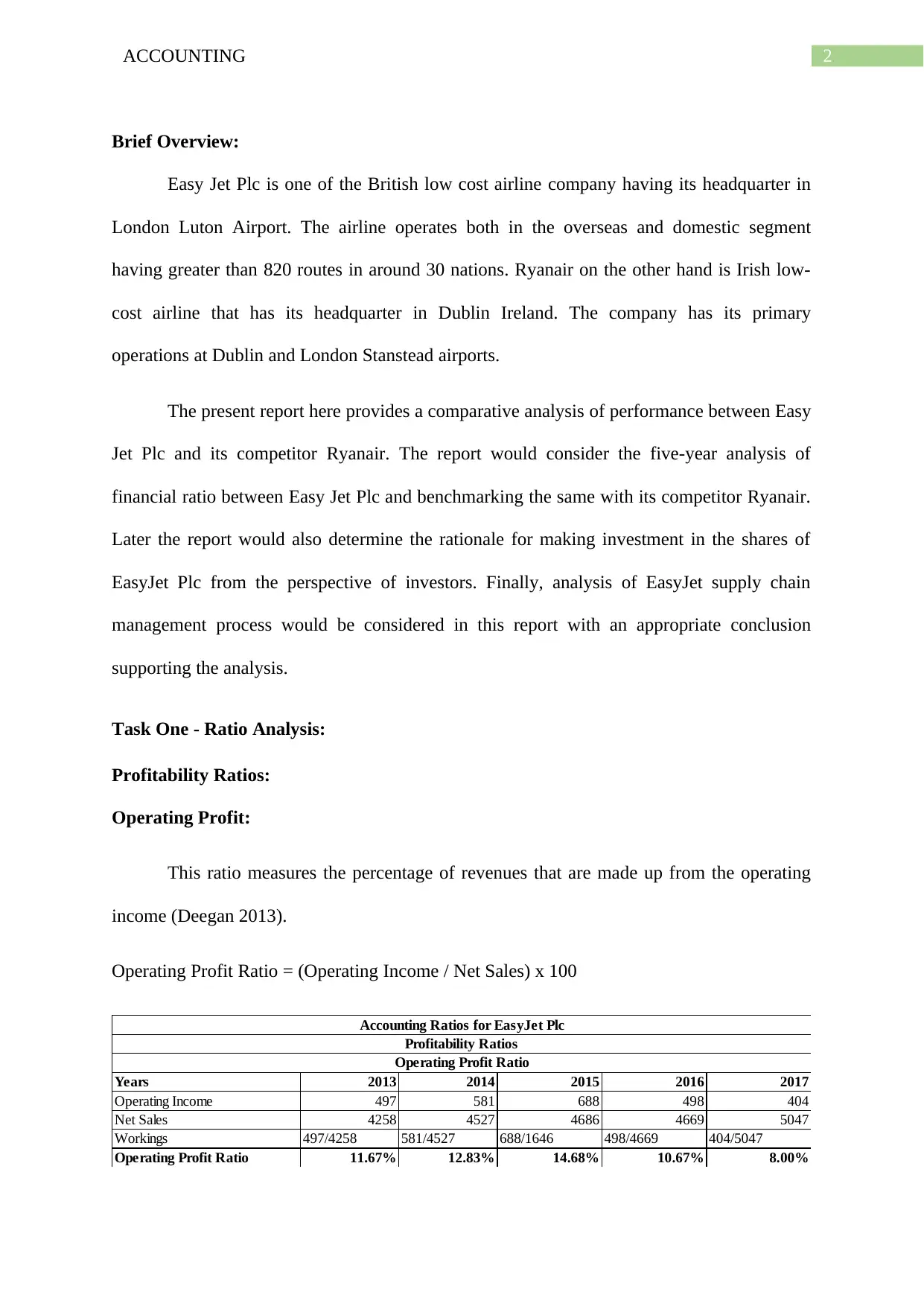

This ratio measures the percentage of revenues that are made up from the operating

income (Deegan 2013).

Operating Profit Ratio = (Operating Income / Net Sales) x 100

Years 2013 2014 2015 2016 2017

Operating Income 497 581 688 498 404

Net Sales 4258 4527 4686 4669 5047

Workings 497/4258 581/4527 688/1646 498/4669 404/5047

Operating Profit Ratio 11.67% 12.83% 14.68% 10.67% 8.00%

Accounting Ratios for EasyJet Plc

Profitability Ratios

Operating Profit Ratio

Brief Overview:

Easy Jet Plc is one of the British low cost airline company having its headquarter in

London Luton Airport. The airline operates both in the overseas and domestic segment

having greater than 820 routes in around 30 nations. Ryanair on the other hand is Irish low-

cost airline that has its headquarter in Dublin Ireland. The company has its primary

operations at Dublin and London Stanstead airports.

The present report here provides a comparative analysis of performance between Easy

Jet Plc and its competitor Ryanair. The report would consider the five-year analysis of

financial ratio between Easy Jet Plc and benchmarking the same with its competitor Ryanair.

Later the report would also determine the rationale for making investment in the shares of

EasyJet Plc from the perspective of investors. Finally, analysis of EasyJet supply chain

management process would be considered in this report with an appropriate conclusion

supporting the analysis.

Task One - Ratio Analysis:

Profitability Ratios:

Operating Profit:

This ratio measures the percentage of revenues that are made up from the operating

income (Deegan 2013).

Operating Profit Ratio = (Operating Income / Net Sales) x 100

Years 2013 2014 2015 2016 2017

Operating Income 497 581 688 498 404

Net Sales 4258 4527 4686 4669 5047

Workings 497/4258 581/4527 688/1646 498/4669 404/5047

Operating Profit Ratio 11.67% 12.83% 14.68% 10.67% 8.00%

Accounting Ratios for EasyJet Plc

Profitability Ratios

Operating Profit Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING

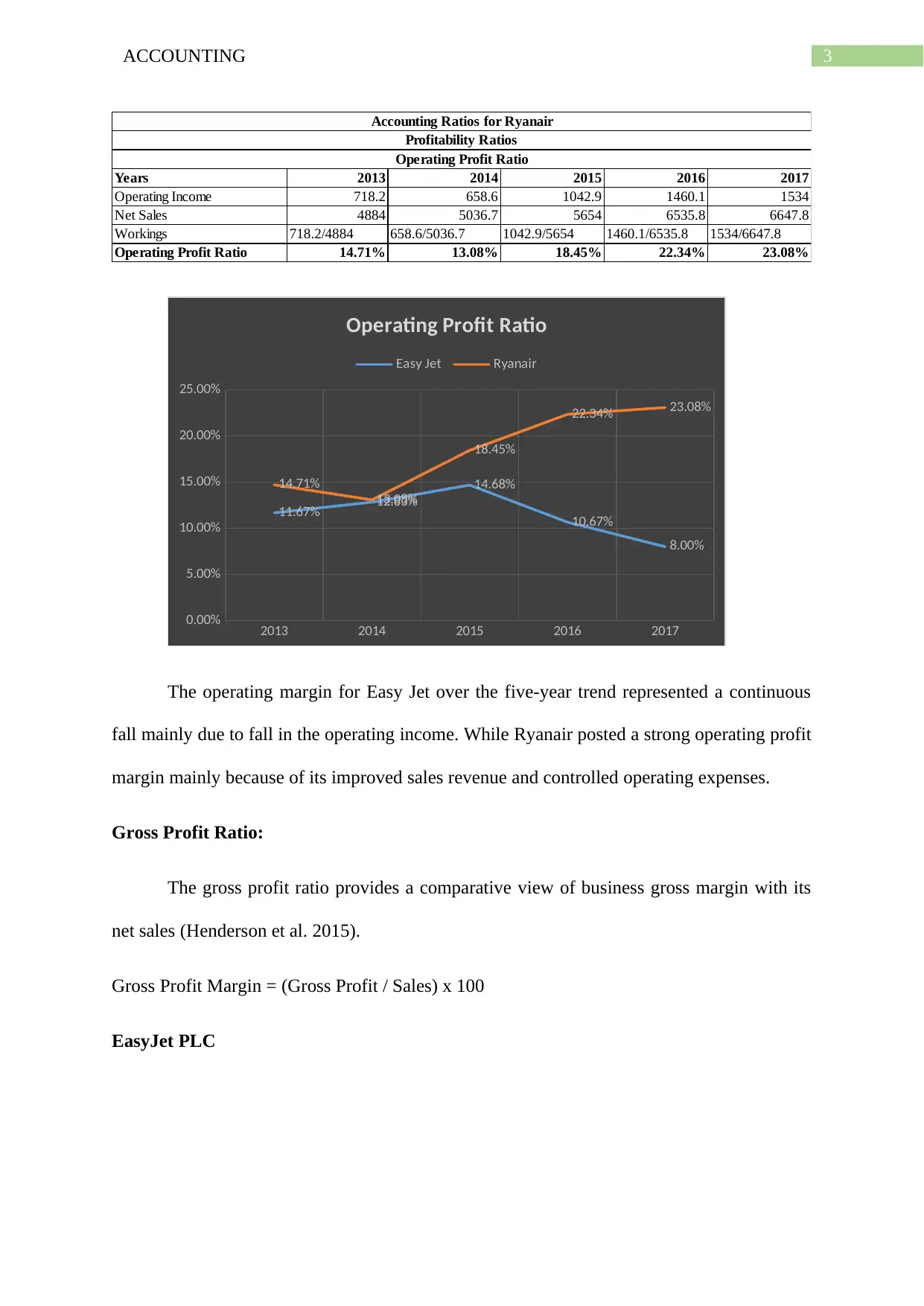

Years 2013 2014 2015 2016 2017

Operating Income 718.2 658.6 1042.9 1460.1 1534

Net Sales 4884 5036.7 5654 6535.8 6647.8

Workings 718.2/4884 658.6/5036.7 1042.9/5654 1460.1/6535.8 1534/6647.8

Operating Profit Ratio 14.71% 13.08% 18.45% 22.34% 23.08%

Accounting Ratios for Ryanair

Profitability Ratios

Operating Profit Ratio

2013 2014 2015 2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

11.67% 12.83%

14.68%

10.67%

8.00%

14.71%

13.08%

18.45%

22.34% 23.08%

Operating Profit Ratio

Easy Jet Ryanair

The operating margin for Easy Jet over the five-year trend represented a continuous

fall mainly due to fall in the operating income. While Ryanair posted a strong operating profit

margin mainly because of its improved sales revenue and controlled operating expenses.

Gross Profit Ratio:

The gross profit ratio provides a comparative view of business gross margin with its

net sales (Henderson et al. 2015).

Gross Profit Margin = (Gross Profit / Sales) x 100

EasyJet PLC

Years 2013 2014 2015 2016 2017

Operating Income 718.2 658.6 1042.9 1460.1 1534

Net Sales 4884 5036.7 5654 6535.8 6647.8

Workings 718.2/4884 658.6/5036.7 1042.9/5654 1460.1/6535.8 1534/6647.8

Operating Profit Ratio 14.71% 13.08% 18.45% 22.34% 23.08%

Accounting Ratios for Ryanair

Profitability Ratios

Operating Profit Ratio

2013 2014 2015 2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

11.67% 12.83%

14.68%

10.67%

8.00%

14.71%

13.08%

18.45%

22.34% 23.08%

Operating Profit Ratio

Easy Jet Ryanair

The operating margin for Easy Jet over the five-year trend represented a continuous

fall mainly due to fall in the operating income. While Ryanair posted a strong operating profit

margin mainly because of its improved sales revenue and controlled operating expenses.

Gross Profit Ratio:

The gross profit ratio provides a comparative view of business gross margin with its

net sales (Henderson et al. 2015).

Gross Profit Margin = (Gross Profit / Sales) x 100

EasyJet PLC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING

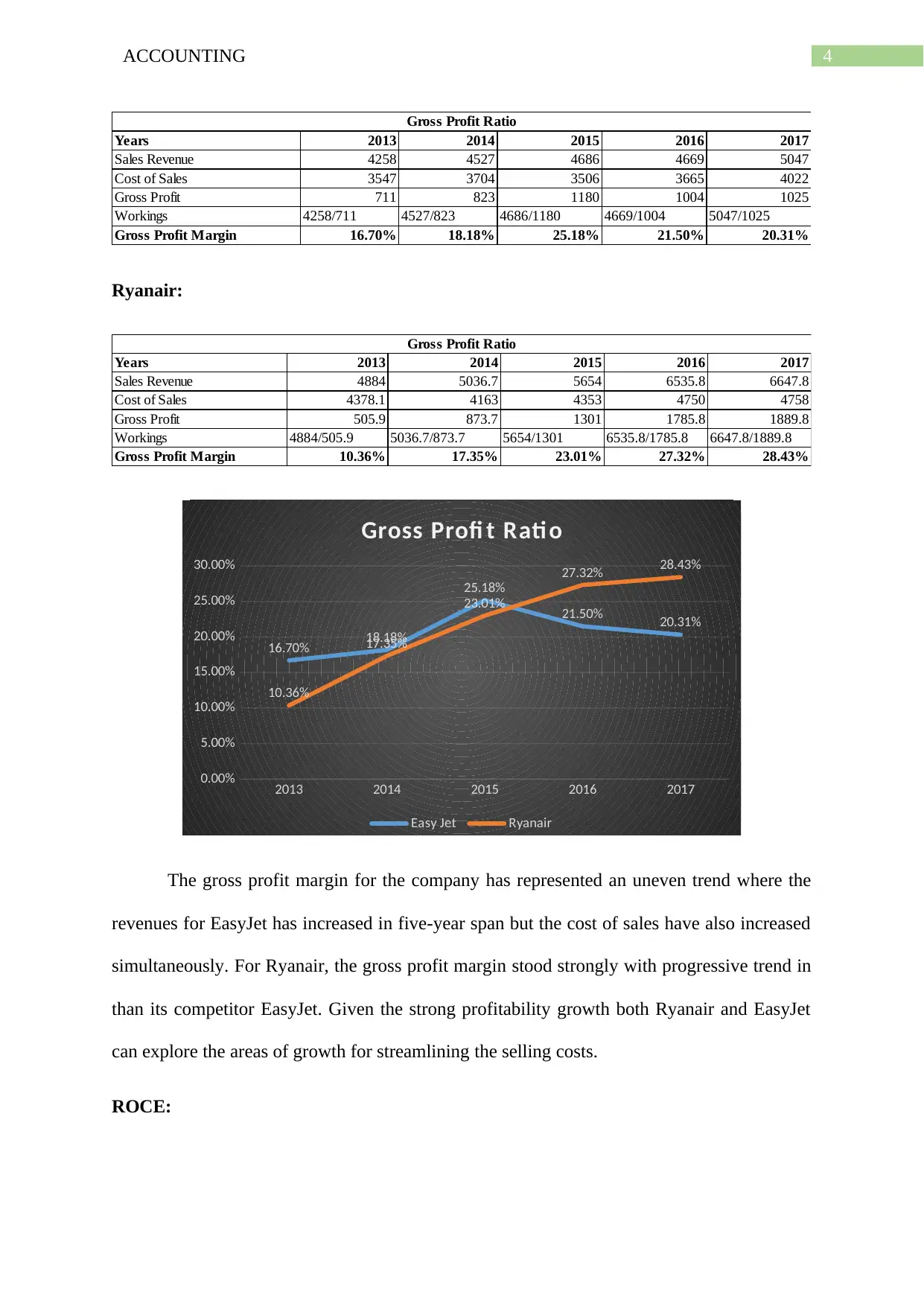

Years 2013 2014 2015 2016 2017

Sales Revenue 4258 4527 4686 4669 5047

Cost of Sales 3547 3704 3506 3665 4022

Gross Profit 711 823 1180 1004 1025

Workings 4258/711 4527/823 4686/1180 4669/1004 5047/1025

Gross Profit Margin 16.70% 18.18% 25.18% 21.50% 20.31%

Gross Profit Ratio

Ryanair:

Years 2013 2014 2015 2016 2017

Sales Revenue 4884 5036.7 5654 6535.8 6647.8

Cost of Sales 4378.1 4163 4353 4750 4758

Gross Profit 505.9 873.7 1301 1785.8 1889.8

Workings 4884/505.9 5036.7/873.7 5654/1301 6535.8/1785.8 6647.8/1889.8

Gross Profit Margin 10.36% 17.35% 23.01% 27.32% 28.43%

Gross Profit Ratio

2013 2014 2015 2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

16.70% 18.18%

25.18%

21.50% 20.31%

10.36%

17.35%

23.01%

27.32% 28.43%

Gross Profi t Rati o

Easy Jet Ryanair

The gross profit margin for the company has represented an uneven trend where the

revenues for EasyJet has increased in five-year span but the cost of sales have also increased

simultaneously. For Ryanair, the gross profit margin stood strongly with progressive trend in

than its competitor EasyJet. Given the strong profitability growth both Ryanair and EasyJet

can explore the areas of growth for streamlining the selling costs.

ROCE:

Years 2013 2014 2015 2016 2017

Sales Revenue 4258 4527 4686 4669 5047

Cost of Sales 3547 3704 3506 3665 4022

Gross Profit 711 823 1180 1004 1025

Workings 4258/711 4527/823 4686/1180 4669/1004 5047/1025

Gross Profit Margin 16.70% 18.18% 25.18% 21.50% 20.31%

Gross Profit Ratio

Ryanair:

Years 2013 2014 2015 2016 2017

Sales Revenue 4884 5036.7 5654 6535.8 6647.8

Cost of Sales 4378.1 4163 4353 4750 4758

Gross Profit 505.9 873.7 1301 1785.8 1889.8

Workings 4884/505.9 5036.7/873.7 5654/1301 6535.8/1785.8 6647.8/1889.8

Gross Profit Margin 10.36% 17.35% 23.01% 27.32% 28.43%

Gross Profit Ratio

2013 2014 2015 2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

16.70% 18.18%

25.18%

21.50% 20.31%

10.36%

17.35%

23.01%

27.32% 28.43%

Gross Profi t Rati o

Easy Jet Ryanair

The gross profit margin for the company has represented an uneven trend where the

revenues for EasyJet has increased in five-year span but the cost of sales have also increased

simultaneously. For Ryanair, the gross profit margin stood strongly with progressive trend in

than its competitor EasyJet. Given the strong profitability growth both Ryanair and EasyJet

can explore the areas of growth for streamlining the selling costs.

ROCE:

5ACCOUNTING

This ratio evaluates the profitability of an organization and the efficiency through

which a firm employs its capital (Lin et al. 2015).

EasyJet PLC:

Years 2013 2014 2015 2016 2017

Operting Profit 497 581 688 498 404

Total Assets 4412 4482 4828 5505 5971

Current Liabilities 1379 1420 1768 1573 1670

Capital Employed 3033 3062 3060 3932 4301

Workings 497/3033 581/3062 688/3060 498/3932 404/4301

ROCE 16.39% 18.97% 22.48% 12.67% 9.39%

Return on Capital Employed

Ryanair:

Years 2013 2014 2015 2016 2017

Operting Profit 718.2 658.6 1042.9 1460.1 1534

Total Assets 8943 8812 12185.4 11218.3 11989.7

Current Liabilities 1911.7 2274.5 3346 3369.5 3011.8

Capital Employed 7031.3 6537.5 8839.4 7848.8 8977.9

Workings 718.2/7031.3 658.6/6537.5 1042.9/8839.4 1460.1/7848.8 1534/8977.9

ROCE 10.21% 10.07% 11.80% 18.60% 17.09%

Return on Capital Employed

2013 2014 2015 2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

16.39%

18.97%

22.48%

12.67%

9.39%

10.21% 10.07%

11.80%

18.60% 17.09%

Return on Capital Employed

Easy Jet Ryanair

The ROEC for EasyJet PLC represented a progressive decline in the ratio between

2015 to 2018 with ratio falling as low as 9.39%. The reason for this is that the operating

profit has declined leading to fall in current liabilities. While Ryanair operating in the same

This ratio evaluates the profitability of an organization and the efficiency through

which a firm employs its capital (Lin et al. 2015).

EasyJet PLC:

Years 2013 2014 2015 2016 2017

Operting Profit 497 581 688 498 404

Total Assets 4412 4482 4828 5505 5971

Current Liabilities 1379 1420 1768 1573 1670

Capital Employed 3033 3062 3060 3932 4301

Workings 497/3033 581/3062 688/3060 498/3932 404/4301

ROCE 16.39% 18.97% 22.48% 12.67% 9.39%

Return on Capital Employed

Ryanair:

Years 2013 2014 2015 2016 2017

Operting Profit 718.2 658.6 1042.9 1460.1 1534

Total Assets 8943 8812 12185.4 11218.3 11989.7

Current Liabilities 1911.7 2274.5 3346 3369.5 3011.8

Capital Employed 7031.3 6537.5 8839.4 7848.8 8977.9

Workings 718.2/7031.3 658.6/6537.5 1042.9/8839.4 1460.1/7848.8 1534/8977.9

ROCE 10.21% 10.07% 11.80% 18.60% 17.09%

Return on Capital Employed

2013 2014 2015 2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

16.39%

18.97%

22.48%

12.67%

9.39%

10.21% 10.07%

11.80%

18.60% 17.09%

Return on Capital Employed

Easy Jet Ryanair

The ROEC for EasyJet PLC represented a progressive decline in the ratio between

2015 to 2018 with ratio falling as low as 9.39%. The reason for this is that the operating

profit has declined leading to fall in current liabilities. While Ryanair operating in the same

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING

industry posted a progressive ROCE during five-year span with as high as 17.09 in 2017

mainly because of lower cost of operations.

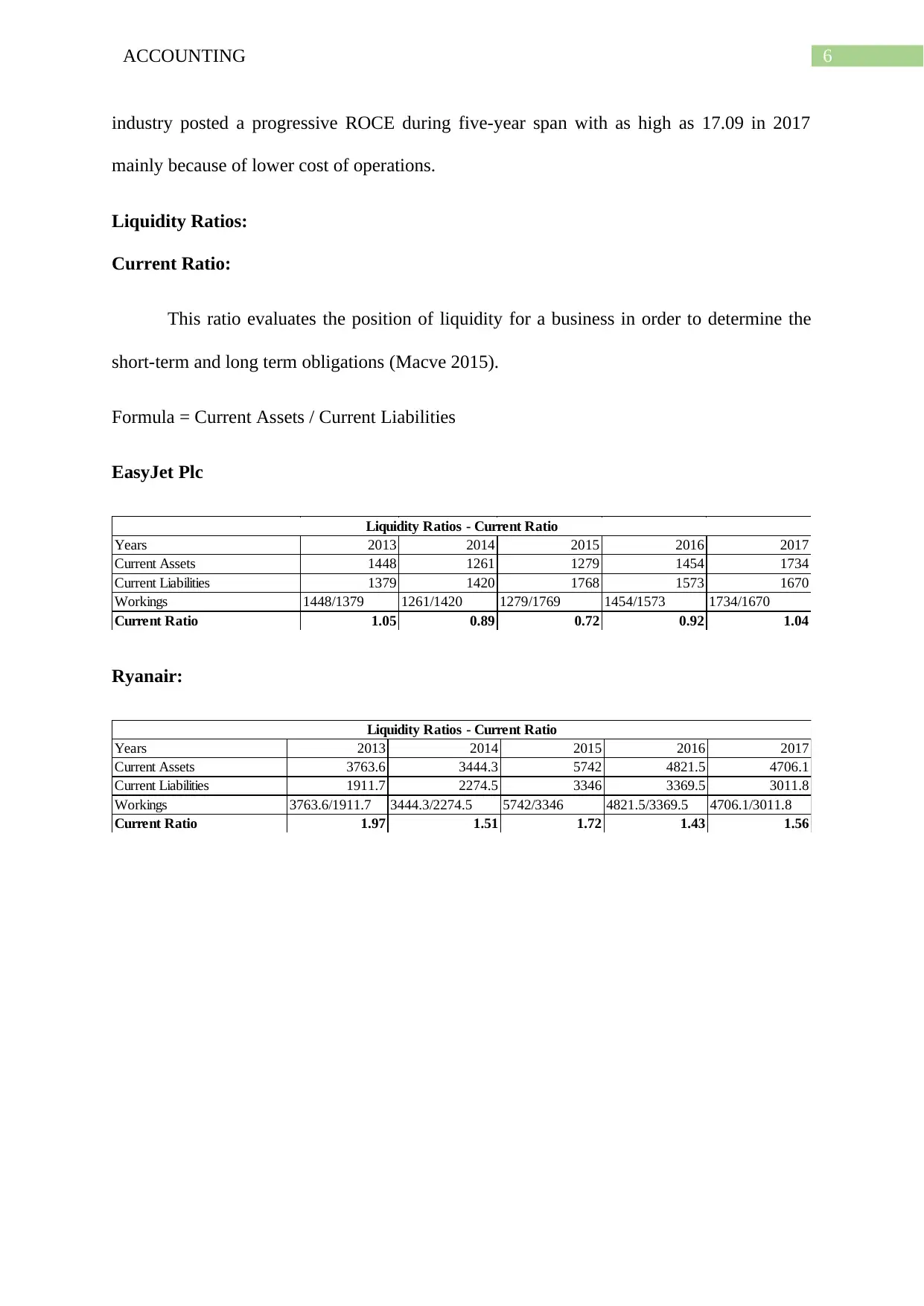

Liquidity Ratios:

Current Ratio:

This ratio evaluates the position of liquidity for a business in order to determine the

short-term and long term obligations (Macve 2015).

Formula = Current Assets / Current Liabilities

EasyJet Plc

Years 2013 2014 2015 2016 2017

Current Assets 1448 1261 1279 1454 1734

Current Liabilities 1379 1420 1768 1573 1670

Workings 1448/1379 1261/1420 1279/1769 1454/1573 1734/1670

Current Ratio 1.05 0.89 0.72 0.92 1.04

Liquidity Ratios - Current Ratio

Ryanair:

Years 2013 2014 2015 2016 2017

Current Assets 3763.6 3444.3 5742 4821.5 4706.1

Current Liabilities 1911.7 2274.5 3346 3369.5 3011.8

Workings 3763.6/1911.7 3444.3/2274.5 5742/3346 4821.5/3369.5 4706.1/3011.8

Current Ratio 1.97 1.51 1.72 1.43 1.56

Liquidity Ratios - Current Ratio

industry posted a progressive ROCE during five-year span with as high as 17.09 in 2017

mainly because of lower cost of operations.

Liquidity Ratios:

Current Ratio:

This ratio evaluates the position of liquidity for a business in order to determine the

short-term and long term obligations (Macve 2015).

Formula = Current Assets / Current Liabilities

EasyJet Plc

Years 2013 2014 2015 2016 2017

Current Assets 1448 1261 1279 1454 1734

Current Liabilities 1379 1420 1768 1573 1670

Workings 1448/1379 1261/1420 1279/1769 1454/1573 1734/1670

Current Ratio 1.05 0.89 0.72 0.92 1.04

Liquidity Ratios - Current Ratio

Ryanair:

Years 2013 2014 2015 2016 2017

Current Assets 3763.6 3444.3 5742 4821.5 4706.1

Current Liabilities 1911.7 2274.5 3346 3369.5 3011.8

Workings 3763.6/1911.7 3444.3/2274.5 5742/3346 4821.5/3369.5 4706.1/3011.8

Current Ratio 1.97 1.51 1.72 1.43 1.56

Liquidity Ratios - Current Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING

2013 2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

1.05 0.89

0.72

0.92 1.04

1.97

1.51

1.72

1.43 1.56

Current Rati o

Easy Jet Ryanair

The current ratio for EasyJet during the year stood less than one while in 2017 it

marginally increased to 1.04. This signifies that there is a larger proportion of EasyJet current

liabilities than its current assets, meaning that the EasyJet has less potential of meeting short

term obligations. While the current ratio for Ryanair has been fluctuating over five-year span

but stood greater than one, meaning that Ryanair is better placed to meet its short-term debt

obligations. Ryanair is better placed than EasyJet in terms of liquidity to meet its short term

obligations.

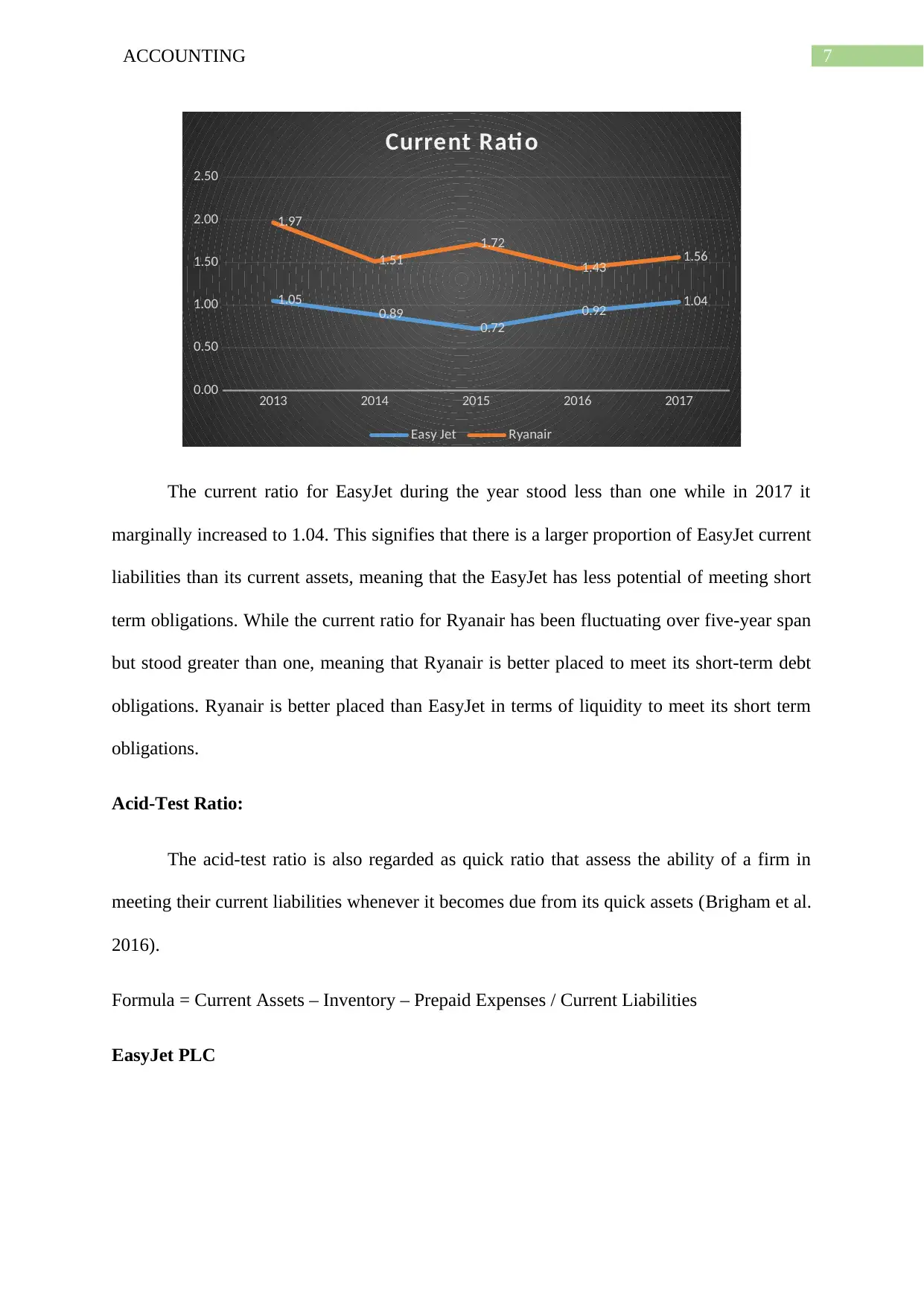

Acid-Test Ratio:

The acid-test ratio is also regarded as quick ratio that assess the ability of a firm in

meeting their current liabilities whenever it becomes due from its quick assets (Brigham et al.

2016).

Formula = Current Assets – Inventory – Prepaid Expenses / Current Liabilities

EasyJet PLC

2013 2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

1.05 0.89

0.72

0.92 1.04

1.97

1.51

1.72

1.43 1.56

Current Rati o

Easy Jet Ryanair

The current ratio for EasyJet during the year stood less than one while in 2017 it

marginally increased to 1.04. This signifies that there is a larger proportion of EasyJet current

liabilities than its current assets, meaning that the EasyJet has less potential of meeting short

term obligations. While the current ratio for Ryanair has been fluctuating over five-year span

but stood greater than one, meaning that Ryanair is better placed to meet its short-term debt

obligations. Ryanair is better placed than EasyJet in terms of liquidity to meet its short term

obligations.

Acid-Test Ratio:

The acid-test ratio is also regarded as quick ratio that assess the ability of a firm in

meeting their current liabilities whenever it becomes due from its quick assets (Brigham et al.

2016).

Formula = Current Assets – Inventory – Prepaid Expenses / Current Liabilities

EasyJet PLC

8ACCOUNTING

Years 2013 2014 2015 2016 2017

Current Assets 1448 1261 1279 1454 1734

Derivative Financial Instrument 53 17 128 268 131

Current Liabilities 1379 1420 1768 1573 1670

Workings (1448-53)1379 (1261-17)/1420 (1279-128)/1768 (1454-268)/1573 (1734-131)/1670

Acid Test Ratio 1.01 0.88 0.65 0.75 0.96

Acid Test Ratio

Ryanair:

Years 2013 2014 2015 2016 2017

Current Assets 3763.6 3444.3 5742 4821.5 4706.1

Derivative Financial Instrument 78.1 16.7 744.4 269.1 286.3

Less: Inventories 2.1 3.3 3.1

Quick Assets 3685.5 3427.6 4995.5 4549.1 4416.7

Current Liabilities 1911.7 2274.5 3346 3369.5 3011.8

Workings 3685.5/1911.7 3427.6/2274.5 4995.5/3346 4549.1/3369.5 4416.7/3011.8

Acid Test Ratio 1.93 1.51 1.49 1.35 1.47

Acid Test Ratio

2013 2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

1.01 0.88

0.65 0.75

0.96

1.93

1.51 1.49 1.35 1.47

Quick Ratio

Easy Jet Ryanair

Unlike the current ratio the acid-test ratio for EasyJet PLC has represented a fall and

stood less than one from 2014 to 2017. This signifies that EasyJet is less liquid in satisfying

its short term debt obligations. While Ryanair has reported a declining trend of current ratio

but stood relatively greater than one, meaning that Ryanair has greater proportion of current

assets to meet its short term obligations.

Years 2013 2014 2015 2016 2017

Current Assets 1448 1261 1279 1454 1734

Derivative Financial Instrument 53 17 128 268 131

Current Liabilities 1379 1420 1768 1573 1670

Workings (1448-53)1379 (1261-17)/1420 (1279-128)/1768 (1454-268)/1573 (1734-131)/1670

Acid Test Ratio 1.01 0.88 0.65 0.75 0.96

Acid Test Ratio

Ryanair:

Years 2013 2014 2015 2016 2017

Current Assets 3763.6 3444.3 5742 4821.5 4706.1

Derivative Financial Instrument 78.1 16.7 744.4 269.1 286.3

Less: Inventories 2.1 3.3 3.1

Quick Assets 3685.5 3427.6 4995.5 4549.1 4416.7

Current Liabilities 1911.7 2274.5 3346 3369.5 3011.8

Workings 3685.5/1911.7 3427.6/2274.5 4995.5/3346 4549.1/3369.5 4416.7/3011.8

Acid Test Ratio 1.93 1.51 1.49 1.35 1.47

Acid Test Ratio

2013 2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

1.01 0.88

0.65 0.75

0.96

1.93

1.51 1.49 1.35 1.47

Quick Ratio

Easy Jet Ryanair

Unlike the current ratio the acid-test ratio for EasyJet PLC has represented a fall and

stood less than one from 2014 to 2017. This signifies that EasyJet is less liquid in satisfying

its short term debt obligations. While Ryanair has reported a declining trend of current ratio

but stood relatively greater than one, meaning that Ryanair has greater proportion of current

assets to meet its short term obligations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING

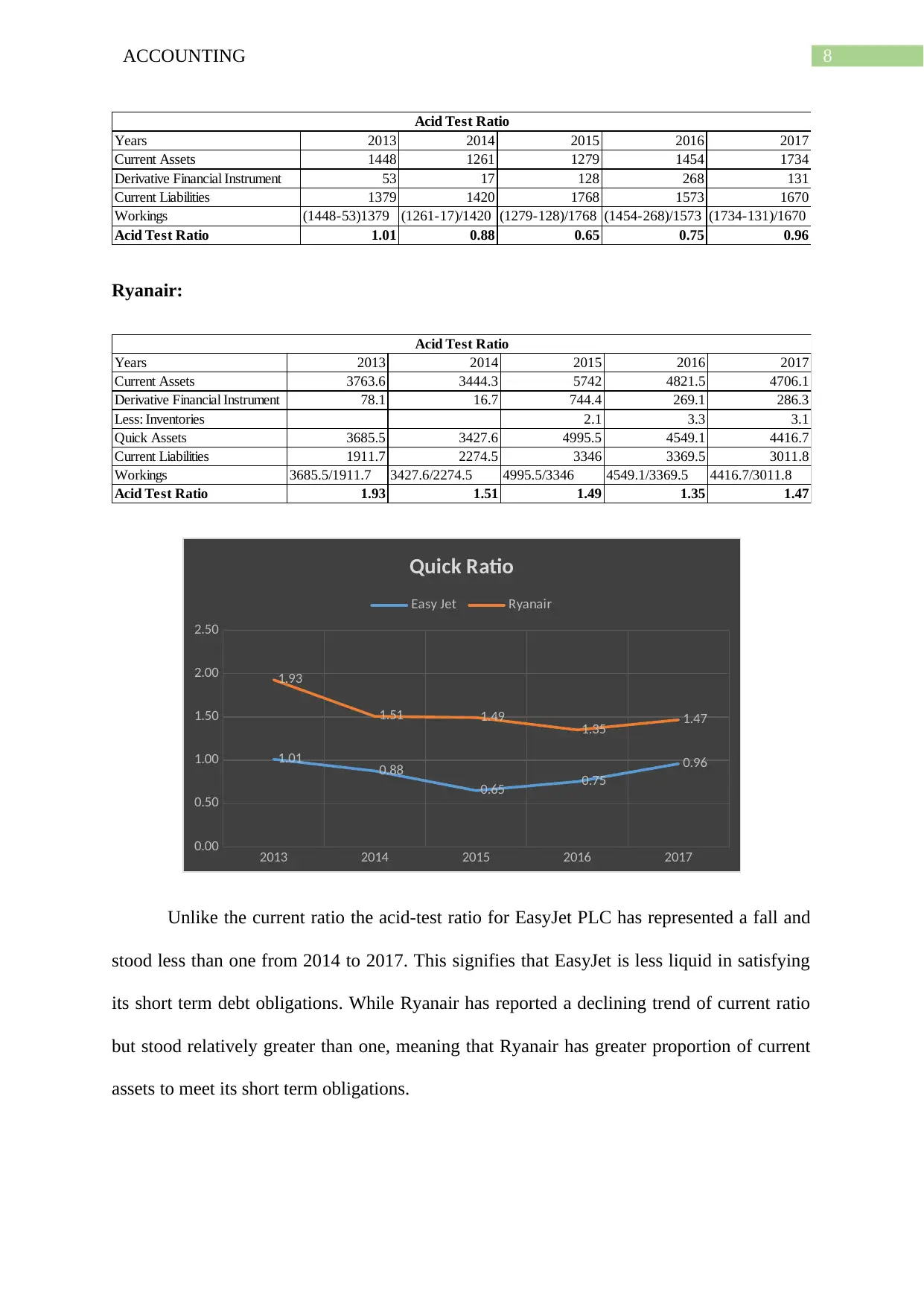

Working Capital Efficiency Ratios:

Trade Receivables Collection Period:

This ratio determines the period of trade receivables settlement period and the time

taken on average basis to receive money from the debtors (Khan 2015).

EasyJet PLC:

Years 2013 2014 2015 2016 2017

Trade Receivables 194 200 206 217 275

Total Sales 4258 4527 4686 4669 5047

Workings (194/4258)x365 (200/4527)x365 )(206/4686)x365 (217/4669)x365 (275/5047)x365

Trade Receivables Period 16.63 16.13 16.05 16.96 19.89

Trade Receivables Collection Period

Working Capital Efficiency Ratios

Ryanair:

Years 2013 2014 2015 2016 2017

Trade Receivables 56.1 58.1 60.1 66.1 54.3

Total Sales 4884 5036.7 5654 6535.8 6647.8

Workings (56.1/4884)x365 (58.1/5036.7)x365 (60.1/5654)x365 (66.1/6535.8)x365(54.3/6647.8)x365

Trade Receivables Period 4.19 4.21 3.88 3.69 2.98

Working Capital Efficiency Ratios

Trade Receivables Collection Period

2013 2014 2015 2016 2017

0.00

5.00

10.00

15.00

20.00

25.00

16.63 16.13 16.05 16.96

19.89

4.19 4.21 3.88 3.69 2.98

Trade Receivables Collecti on Period

Easy Jet Ryanair

The trade receivables period for EasyJet averages around 18 to 20 days which

signifies that business receives its outstanding dues from the debtors within a month. While

Working Capital Efficiency Ratios:

Trade Receivables Collection Period:

This ratio determines the period of trade receivables settlement period and the time

taken on average basis to receive money from the debtors (Khan 2015).

EasyJet PLC:

Years 2013 2014 2015 2016 2017

Trade Receivables 194 200 206 217 275

Total Sales 4258 4527 4686 4669 5047

Workings (194/4258)x365 (200/4527)x365 )(206/4686)x365 (217/4669)x365 (275/5047)x365

Trade Receivables Period 16.63 16.13 16.05 16.96 19.89

Trade Receivables Collection Period

Working Capital Efficiency Ratios

Ryanair:

Years 2013 2014 2015 2016 2017

Trade Receivables 56.1 58.1 60.1 66.1 54.3

Total Sales 4884 5036.7 5654 6535.8 6647.8

Workings (56.1/4884)x365 (58.1/5036.7)x365 (60.1/5654)x365 (66.1/6535.8)x365(54.3/6647.8)x365

Trade Receivables Period 4.19 4.21 3.88 3.69 2.98

Working Capital Efficiency Ratios

Trade Receivables Collection Period

2013 2014 2015 2016 2017

0.00

5.00

10.00

15.00

20.00

25.00

16.63 16.13 16.05 16.96

19.89

4.19 4.21 3.88 3.69 2.98

Trade Receivables Collecti on Period

Easy Jet Ryanair

The trade receivables period for EasyJet averages around 18 to 20 days which

signifies that business receives its outstanding dues from the debtors within a month. While

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING

Ryanair reported a significantly improved trade receivables period with the ratio standing

averagely 3 to 4 days. This is advantageous for the company as its sales credit is settled

promptly within time without decrementing its cash flow from business.

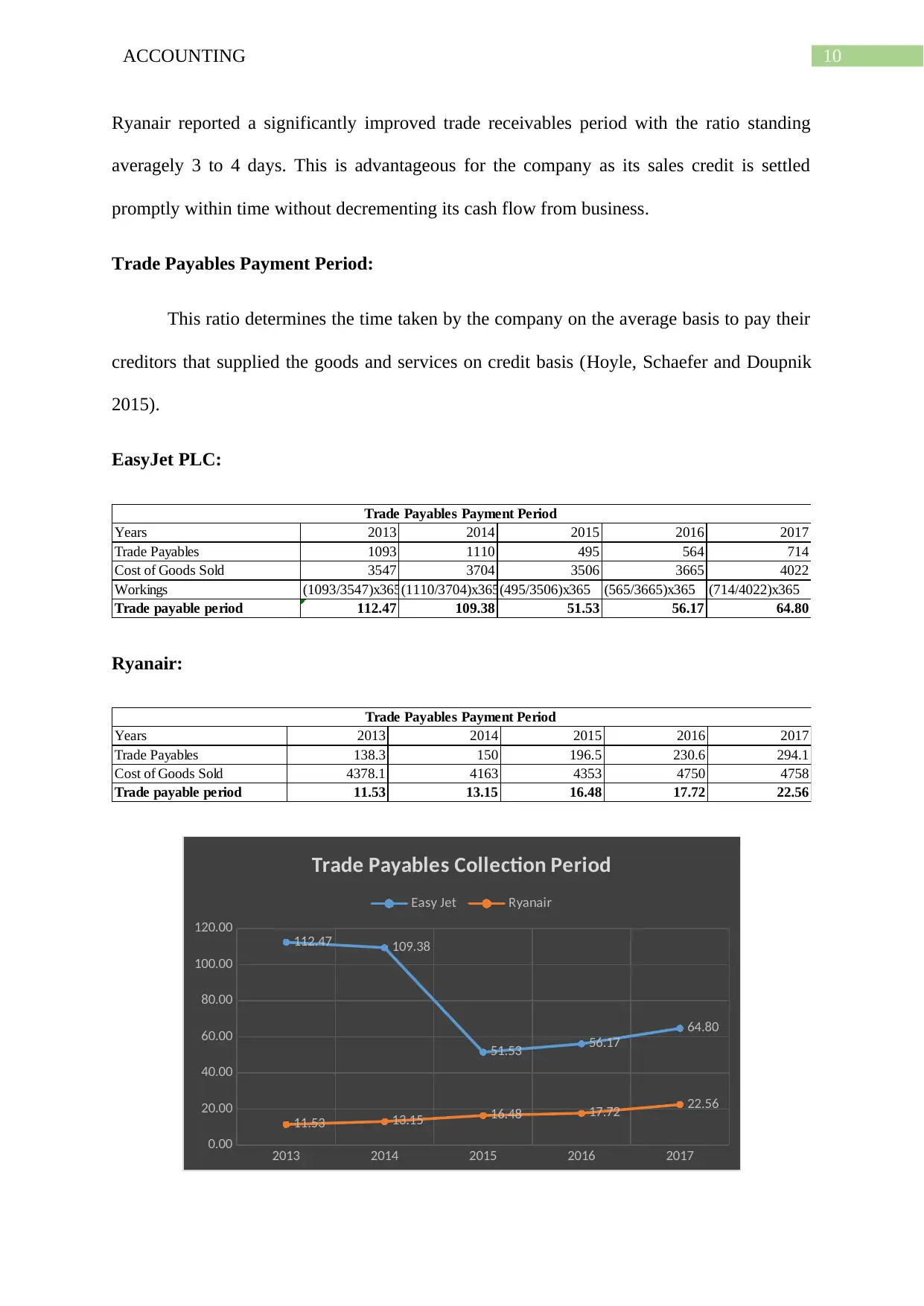

Trade Payables Payment Period:

This ratio determines the time taken by the company on the average basis to pay their

creditors that supplied the goods and services on credit basis (Hoyle, Schaefer and Doupnik

2015).

EasyJet PLC:

Years 2013 2014 2015 2016 2017

Trade Payables 1093 1110 495 564 714

Cost of Goods Sold 3547 3704 3506 3665 4022

Workings (1093/3547)x365(1110/3704)x365(495/3506)x365 (565/3665)x365 (714/4022)x365

Trade payable period 112.47 109.38 51.53 56.17 64.80

Trade Payables Payment Period

Ryanair:

Years 2013 2014 2015 2016 2017

Trade Payables 138.3 150 196.5 230.6 294.1

Cost of Goods Sold 4378.1 4163 4353 4750 4758

Trade payable period 11.53 13.15 16.48 17.72 22.56

Trade Payables Payment Period

2013 2014 2015 2016 2017

0.00

20.00

40.00

60.00

80.00

100.00

120.00 112.47 109.38

51.53 56.17

64.80

11.53 13.15 16.48 17.72 22.56

Trade Payables Collection Period

Easy Jet Ryanair

Ryanair reported a significantly improved trade receivables period with the ratio standing

averagely 3 to 4 days. This is advantageous for the company as its sales credit is settled

promptly within time without decrementing its cash flow from business.

Trade Payables Payment Period:

This ratio determines the time taken by the company on the average basis to pay their

creditors that supplied the goods and services on credit basis (Hoyle, Schaefer and Doupnik

2015).

EasyJet PLC:

Years 2013 2014 2015 2016 2017

Trade Payables 1093 1110 495 564 714

Cost of Goods Sold 3547 3704 3506 3665 4022

Workings (1093/3547)x365(1110/3704)x365(495/3506)x365 (565/3665)x365 (714/4022)x365

Trade payable period 112.47 109.38 51.53 56.17 64.80

Trade Payables Payment Period

Ryanair:

Years 2013 2014 2015 2016 2017

Trade Payables 138.3 150 196.5 230.6 294.1

Cost of Goods Sold 4378.1 4163 4353 4750 4758

Trade payable period 11.53 13.15 16.48 17.72 22.56

Trade Payables Payment Period

2013 2014 2015 2016 2017

0.00

20.00

40.00

60.00

80.00

100.00

120.00 112.47 109.38

51.53 56.17

64.80

11.53 13.15 16.48 17.72 22.56

Trade Payables Collection Period

Easy Jet Ryanair

11ACCOUNTING

Computations from the above stated table for EasyJet signifies that the company

settles its trade payables in fifty to sixty days averagely. The payment period has though fell

down but because of its poor liquidity EasyJet may suffer loss of goodwill in meeting its debt

obligations. While Ryanair are settling their creditors quicker than its competitors as it

averages around twenty days. It seems that Ryanair has been consistent with its timeframe to

avoid the loss of goodwill.

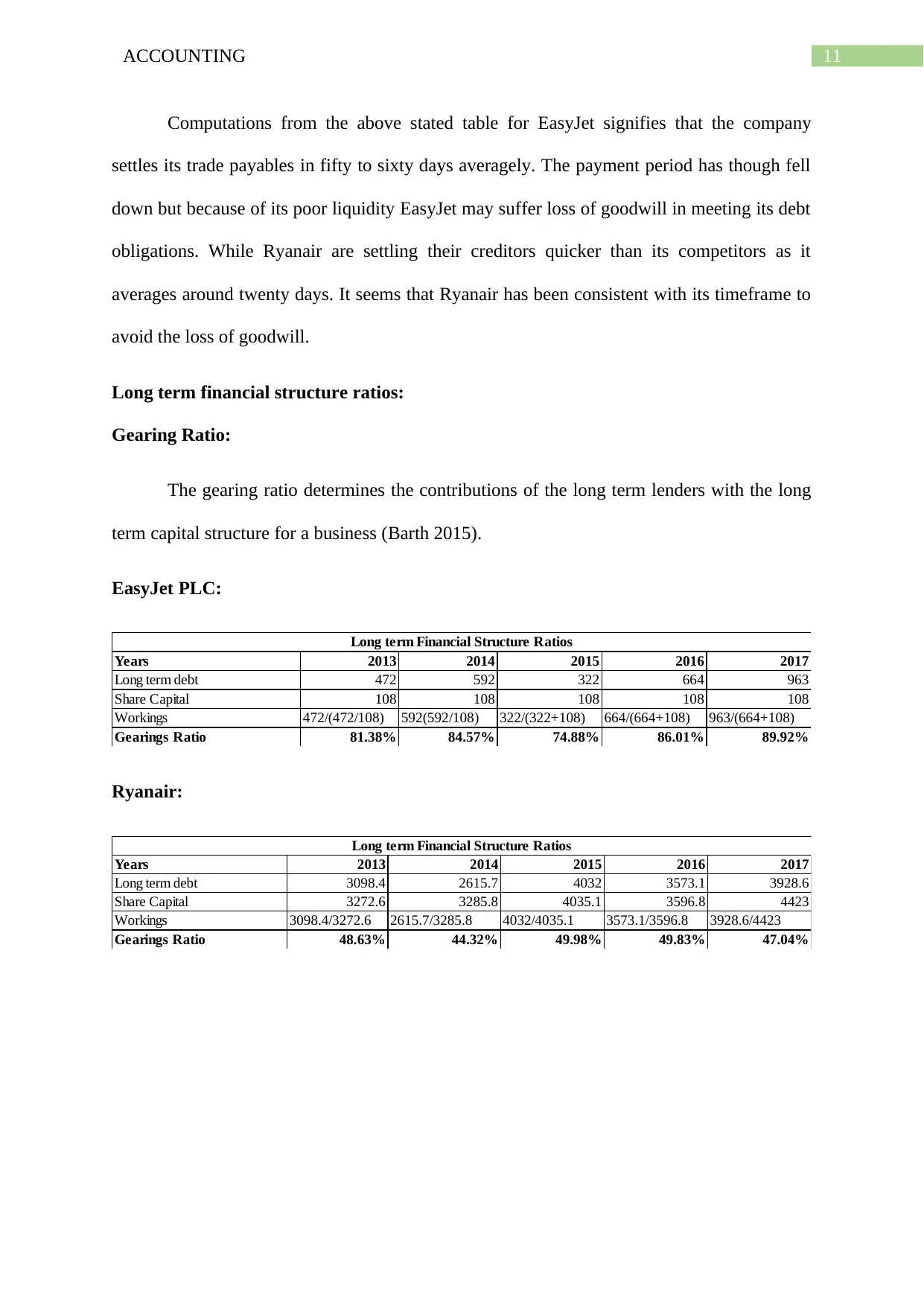

Long term financial structure ratios:

Gearing Ratio:

The gearing ratio determines the contributions of the long term lenders with the long

term capital structure for a business (Barth 2015).

EasyJet PLC:

Years 2013 2014 2015 2016 2017

Long term debt 472 592 322 664 963

Share Capital 108 108 108 108 108

Workings 472/(472/108) 592(592/108) 322/(322+108) 664/(664+108) 963/(664+108)

Gearings Ratio 81.38% 84.57% 74.88% 86.01% 89.92%

Long term Financial Structure Ratios

Ryanair:

Years 2013 2014 2015 2016 2017

Long term debt 3098.4 2615.7 4032 3573.1 3928.6

Share Capital 3272.6 3285.8 4035.1 3596.8 4423

Workings 3098.4/3272.6 2615.7/3285.8 4032/4035.1 3573.1/3596.8 3928.6/4423

Gearings Ratio 48.63% 44.32% 49.98% 49.83% 47.04%

Long term Financial Structure Ratios

Computations from the above stated table for EasyJet signifies that the company

settles its trade payables in fifty to sixty days averagely. The payment period has though fell

down but because of its poor liquidity EasyJet may suffer loss of goodwill in meeting its debt

obligations. While Ryanair are settling their creditors quicker than its competitors as it

averages around twenty days. It seems that Ryanair has been consistent with its timeframe to

avoid the loss of goodwill.

Long term financial structure ratios:

Gearing Ratio:

The gearing ratio determines the contributions of the long term lenders with the long

term capital structure for a business (Barth 2015).

EasyJet PLC:

Years 2013 2014 2015 2016 2017

Long term debt 472 592 322 664 963

Share Capital 108 108 108 108 108

Workings 472/(472/108) 592(592/108) 322/(322+108) 664/(664+108) 963/(664+108)

Gearings Ratio 81.38% 84.57% 74.88% 86.01% 89.92%

Long term Financial Structure Ratios

Ryanair:

Years 2013 2014 2015 2016 2017

Long term debt 3098.4 2615.7 4032 3573.1 3928.6

Share Capital 3272.6 3285.8 4035.1 3596.8 4423

Workings 3098.4/3272.6 2615.7/3285.8 4032/4035.1 3573.1/3596.8 3928.6/4423

Gearings Ratio 48.63% 44.32% 49.98% 49.83% 47.04%

Long term Financial Structure Ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.