Financial Decision-Making Report: Ratio Analysis and Accounting Role

VerifiedAdded on 2021/02/20

|11

|3769

|35

Report

AI Summary

This report provides a detailed analysis of financial decision-making, focusing on the application of accounting techniques and the interpretation of financial ratios. The introduction outlines the scope of the study, which includes an evaluation of the role of accounting and finance in corporate decision-making, specifically using Anglian Home Improvements as a case study. Task 1 delves into the role of management accounting techniques such as financial planning, financial statement analysis, historical cost accounting, and budgetary control within Anglian Limited. A critical analysis of these techniques is also included, highlighting their combined impact on control, planning, and decision-making. Task 2 focuses on the practical application of financial ratios using ALPHA Limited, calculating and interpreting key ratios such as Return on Capital Employed, Net Profit Margin, Current Ratio, Debtor Collection Period, and Creditor Collection Period. The analysis highlights the significance of these ratios in assessing company performance and making informed financial decisions. The report concludes with a summary of the key findings and their implications for effective financial management.

Financial

Decision Making

Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Evaluation of the role of accounting and finance:.......................................................................3

TASK 2............................................................................................................................................6

Calculation of the ratios to analyse company performance:........................................................6

Interpretation and analysis of financial ratios:.............................................................................7

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Evaluation of the role of accounting and finance:.......................................................................3

TASK 2............................................................................................................................................6

Calculation of the ratios to analyse company performance:........................................................6

Interpretation and analysis of financial ratios:.............................................................................7

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial decision-making comprises a regular and coordinated range of practices

associated with identifying a most feasible and effective choice between multiple choices fiscal-

related actions. The fundamental goal or purpose is to initiate and pick unique or revolutionary

steps to accomplish enterprise aims, mission and commitments (Bryer, 2013). The whole study is

divided in two tasks, wherein first task contains comprehensive and detailed explanation on some

key aspects such as structure of corporate financial statements along with terms and, use in

context of different key operations of like planning, decision making and control of major

method of management accounting in Anglian Home Improvements. Company is UK's uPVC

windows manufacturer and engaged in manufacture and supply of Britain made uPVC high

quality products.

Second task of study in also comprise practical workings of different ratios of ALPHA

Limited, UK's manufacturer, along with relevancy for these ratios for various users. It also

covers explantation about role of aspects: accounting and finance in corporations with regards to

decision-making and reporting.

TASK 1

Evaluation of the role of accounting and finance:

Overview of company:

Anglian Limited is UK's popular and well-known uPVC product manufacturer and

supplier. Company specially customise and feature products like uPVC windows, main doors

and other related products based on customers feedback and choices. In Norwich, United

Kingdom, Company's main headquarter is situated to control all other units of company. It lead

in providing unique and stylish designs in windows, main-entrance doors. It has accomplished

this place in industry because of approx 48 year of experience in same sector and premium

quality of products. It designs and delivers long-lasting uPVC products that also meet safety

standards. Company recently funded the recyclables of uPVC product lines and offered recycling

of their old-used products. Company providing tuff competitiveness in the uPVC sector with its

distinctive concepts and innovative thinking (Anglian Home. 2019).

Financial decision-making comprises a regular and coordinated range of practices

associated with identifying a most feasible and effective choice between multiple choices fiscal-

related actions. The fundamental goal or purpose is to initiate and pick unique or revolutionary

steps to accomplish enterprise aims, mission and commitments (Bryer, 2013). The whole study is

divided in two tasks, wherein first task contains comprehensive and detailed explanation on some

key aspects such as structure of corporate financial statements along with terms and, use in

context of different key operations of like planning, decision making and control of major

method of management accounting in Anglian Home Improvements. Company is UK's uPVC

windows manufacturer and engaged in manufacture and supply of Britain made uPVC high

quality products.

Second task of study in also comprise practical workings of different ratios of ALPHA

Limited, UK's manufacturer, along with relevancy for these ratios for various users. It also

covers explantation about role of aspects: accounting and finance in corporations with regards to

decision-making and reporting.

TASK 1

Evaluation of the role of accounting and finance:

Overview of company:

Anglian Limited is UK's popular and well-known uPVC product manufacturer and

supplier. Company specially customise and feature products like uPVC windows, main doors

and other related products based on customers feedback and choices. In Norwich, United

Kingdom, Company's main headquarter is situated to control all other units of company. It lead

in providing unique and stylish designs in windows, main-entrance doors. It has accomplished

this place in industry because of approx 48 year of experience in same sector and premium

quality of products. It designs and delivers long-lasting uPVC products that also meet safety

standards. Company recently funded the recyclables of uPVC product lines and offered recycling

of their old-used products. Company providing tuff competitiveness in the uPVC sector with its

distinctive concepts and innovative thinking (Anglian Home. 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Role of management accounting techniques:

In present time, Management accounting is crucial factor and aspect of entire operational

structure. It generally also regarded as term managerial accounting. It simply implies a specific

procedure which contributes in furnishing and supplying corporation's fiscal data and key

resources to managing officials specifically for decision-making. It contain some techniques

which are utilized by company's internal teams which makes distinguish it from process of

financial accounting. Aim of these techniques is to proper utilisation of information or data of

business and develop a assistance framework for accurate decision, managing business tasks, and

development of organisational processes (Knežević, Stanković and Tepavac, 2012). In large

corporations such as Anglian Limited bookkeepers or administrators utilizing multiple methods

to accomplish the operations and procedures with required efficiencies and objectives. It also

helps to boost and pursue accountability in the systematic distribution and distribution of

economic and fiscal resources. Corporations implement these techniques which set guidelines

and measures for performing management and business procedures. Most widely recognized

management accounting methods are cash-flow statements, financial planning, budgetary

control, fund-flow statements, financial statements analysis etc. Here are some major multi use

techniques which are needed for developing different business procedures and to achieve

targeted efficiencies.

Financial Planning: It merely means setting particular duties and activities that

businesses carry out in order to project results, estimate capital and asses the necessity for

capital while taking into account competitive variables. It assist to develop fiscal policies

and guidance for acquisition, procurement & execution, and oversight of the sum of

funds collected within a corporate through numerous sources. Anglian Limited managing

officials also use financial planning to establish a system which informs about the level as

well as adequacy of short and long-term resources or capital to make prompt investment

options. It facilitates process scheduling and development of a managed internet to

handle financing and financing activities (Zopounidis and Doumpos, 2013). Based on the

current performance and financing framework of the corporation, managerial staff

perform assessment and assess the demand for financing. It identifies the effect of forms

of financing and controls long-term use of resources for long-term objective.

In present time, Management accounting is crucial factor and aspect of entire operational

structure. It generally also regarded as term managerial accounting. It simply implies a specific

procedure which contributes in furnishing and supplying corporation's fiscal data and key

resources to managing officials specifically for decision-making. It contain some techniques

which are utilized by company's internal teams which makes distinguish it from process of

financial accounting. Aim of these techniques is to proper utilisation of information or data of

business and develop a assistance framework for accurate decision, managing business tasks, and

development of organisational processes (Knežević, Stanković and Tepavac, 2012). In large

corporations such as Anglian Limited bookkeepers or administrators utilizing multiple methods

to accomplish the operations and procedures with required efficiencies and objectives. It also

helps to boost and pursue accountability in the systematic distribution and distribution of

economic and fiscal resources. Corporations implement these techniques which set guidelines

and measures for performing management and business procedures. Most widely recognized

management accounting methods are cash-flow statements, financial planning, budgetary

control, fund-flow statements, financial statements analysis etc. Here are some major multi use

techniques which are needed for developing different business procedures and to achieve

targeted efficiencies.

Financial Planning: It merely means setting particular duties and activities that

businesses carry out in order to project results, estimate capital and asses the necessity for

capital while taking into account competitive variables. It assist to develop fiscal policies

and guidance for acquisition, procurement & execution, and oversight of the sum of

funds collected within a corporate through numerous sources. Anglian Limited managing

officials also use financial planning to establish a system which informs about the level as

well as adequacy of short and long-term resources or capital to make prompt investment

options. It facilitates process scheduling and development of a managed internet to

handle financing and financing activities (Zopounidis and Doumpos, 2013). Based on the

current performance and financing framework of the corporation, managerial staff

perform assessment and assess the demand for financing. It identifies the effect of forms

of financing and controls long-term use of resources for long-term objective.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis of financial statements: It is also the fundamental technique that most of the

corporate organizations are using to assess outcomes and efficiency over a definite period

of time applying financial statements and associated statistics. Financial statements

generally includes balance sheet, statement of income, change in shareholder's fund

statement etc. All of them covers and presents numerous aspects of entity. Normally a

corporation's Financial statements comprises it's balance sheet, income statement,

fluctuation of shareholder's equity statement etc. all these exhibits wider aspects and

features of business enterprise. A corporation's balance sheet reflects clear position of

assets and liabilities of on year end date while company's income statement displays its

actual gross as well as net profitability status during particular period (Chiang, Nouri and

Samanta, 2014). A thorough assessment of these statements can assist executives in

making plans and taking decisions, as financial statement demonstrates real performance

statistics. Anglian Limited reports yearly financial statements and the analysis that

relevant users and managerial personnels use to take trade-decisions. Company

undergoes though such analyses to discover future opportunities, methods of financing,

considerations that influence the efficiency of the corporation and identify probable or

contingent liability commitments. Financial statement allows a comprehensive and

comparative evaluation of more-than one period's statistics and values, an

acknowledgement of corporation weakness.

Historical Cost Accounting: Here Historical cost is a notable term which simply implies

to basic initial-price which has been paid by company at acquisition date of assets. It

mainly concentrate upon concept that corporation's assets especially tangible and fixed

assets are requisite to be recorded at cost-price paid on asset's purchase along with other

related costs which essential to use such asset, instead of recording at market value. The

whole approach of this technique helps to improve financial statement credibility since it

helps to show more credible information (Ball, 2013). For instance, marketable securities

which are not registered at historical value, but not all assets are reported at assets'

historical cost. In practice life this is more biased-free concept as it facilitates easy

verification of values reported through original invoices and supportive papers. It can aid

in managing the efficient use of resources in the framework of company. Management

could also make right decisions, choices and create plans for procuring and buying assets.

corporate organizations are using to assess outcomes and efficiency over a definite period

of time applying financial statements and associated statistics. Financial statements

generally includes balance sheet, statement of income, change in shareholder's fund

statement etc. All of them covers and presents numerous aspects of entity. Normally a

corporation's Financial statements comprises it's balance sheet, income statement,

fluctuation of shareholder's equity statement etc. all these exhibits wider aspects and

features of business enterprise. A corporation's balance sheet reflects clear position of

assets and liabilities of on year end date while company's income statement displays its

actual gross as well as net profitability status during particular period (Chiang, Nouri and

Samanta, 2014). A thorough assessment of these statements can assist executives in

making plans and taking decisions, as financial statement demonstrates real performance

statistics. Anglian Limited reports yearly financial statements and the analysis that

relevant users and managerial personnels use to take trade-decisions. Company

undergoes though such analyses to discover future opportunities, methods of financing,

considerations that influence the efficiency of the corporation and identify probable or

contingent liability commitments. Financial statement allows a comprehensive and

comparative evaluation of more-than one period's statistics and values, an

acknowledgement of corporation weakness.

Historical Cost Accounting: Here Historical cost is a notable term which simply implies

to basic initial-price which has been paid by company at acquisition date of assets. It

mainly concentrate upon concept that corporation's assets especially tangible and fixed

assets are requisite to be recorded at cost-price paid on asset's purchase along with other

related costs which essential to use such asset, instead of recording at market value. The

whole approach of this technique helps to improve financial statement credibility since it

helps to show more credible information (Ball, 2013). For instance, marketable securities

which are not registered at historical value, but not all assets are reported at assets'

historical cost. In practice life this is more biased-free concept as it facilitates easy

verification of values reported through original invoices and supportive papers. It can aid

in managing the efficient use of resources in the framework of company. Management

could also make right decisions, choices and create plans for procuring and buying assets.

Budgetary Control: Nearly all commercial enterprises are projecting costs and revenue

and preparing distinct budgets based on their distinct business goals. Core aim of framing

several budgets is developing operational procedures as well as to establish control and

regulate distinct budgetary functions of corporation, therefore budgets prepared by

accountants and budgetary-controls are significantly connected with each-other.

Budgetary control simply involves predictive value procedures and track the use and

fluctuation in company's different resources (Jetter and Walker, 2017). Anglian Limited

exercises budgetary control over resources, plans the use of resources and makes

budgetary decisions. This also offers a comprehensive comparative assessment of various

budget elements to enable rapid and convenient decision-making. It makes it easier to

identify scheduling on the grounds of efficient plans as budgets determined under it. It

controls expenses and minimizes expenses by eliminating unnecessary wastes and

unproductive processes, resulting in maximizing aggregate earnings.

Critical Analysis:

In corporation like Anglian Limited, combination of more than one above discussed

techniques are applied by managing officials with aim to establishing control, planning and

decision-making. An overall development of corporation fundamentally depends upon these

three core activities. Here among these techniques financial planning is specifically used in

company to frame blue-print of operations and future actions. While budgetary control technique

is used by company to regulate and control business tasks (Lawrence, 2013). Analysing financial

statements of corporation help to build a structure for efficient decision-making. Corporation

also adopt historical-cost based accounting technique to take quick long term decisions. These

techniques' main aim is to provide a complete and structured procedures for effective controlling,

planning and business decision-making.

TASK 2

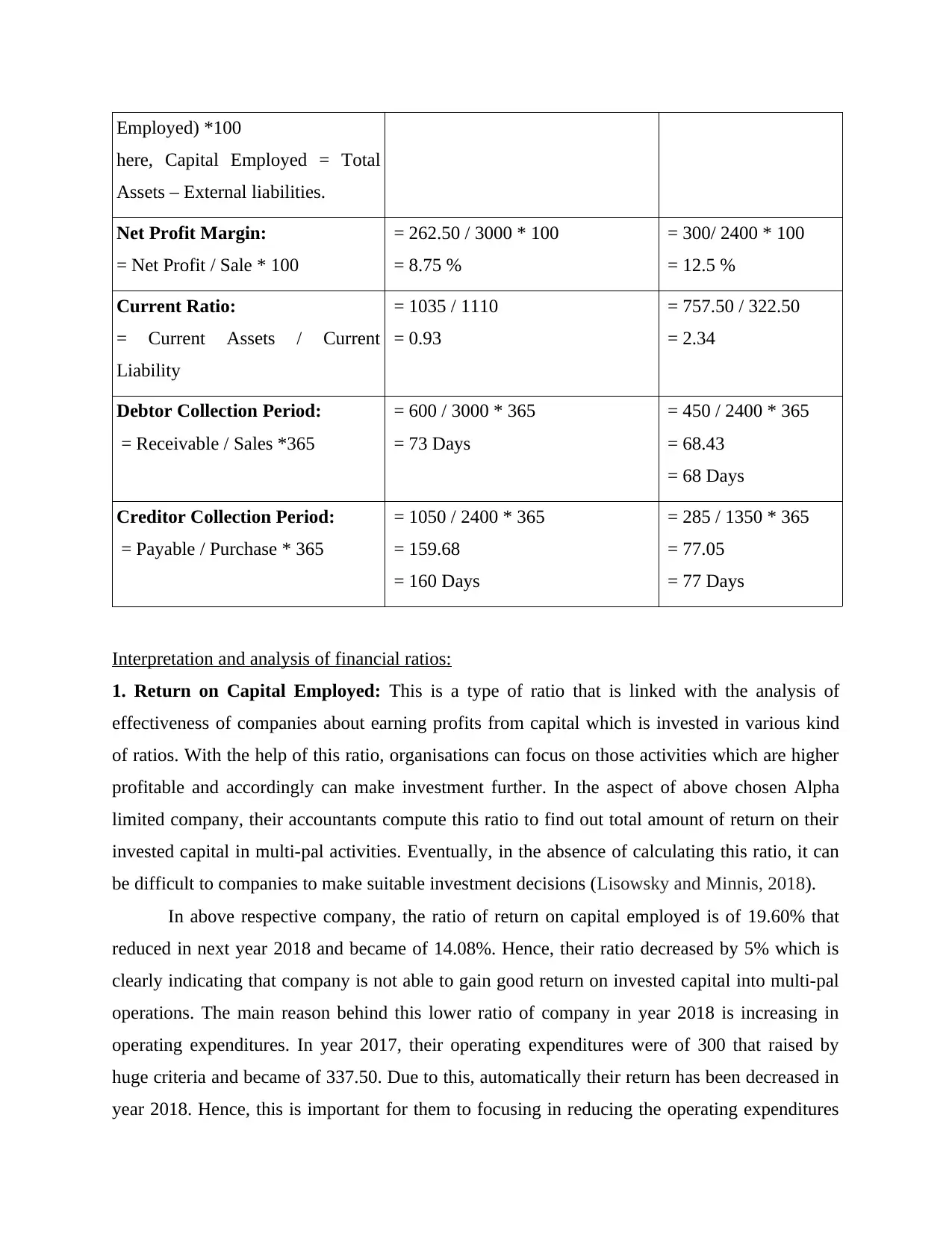

Calculation of the ratios to analyse company performance:

Ratios 2018 2017

ROCE or Return On Capital

Employed :

= (Operating Profit /Capital

= 412 / 2925 * 100

= 14.10%

= 375 / 1912.50 *100

= 19.60%

and preparing distinct budgets based on their distinct business goals. Core aim of framing

several budgets is developing operational procedures as well as to establish control and

regulate distinct budgetary functions of corporation, therefore budgets prepared by

accountants and budgetary-controls are significantly connected with each-other.

Budgetary control simply involves predictive value procedures and track the use and

fluctuation in company's different resources (Jetter and Walker, 2017). Anglian Limited

exercises budgetary control over resources, plans the use of resources and makes

budgetary decisions. This also offers a comprehensive comparative assessment of various

budget elements to enable rapid and convenient decision-making. It makes it easier to

identify scheduling on the grounds of efficient plans as budgets determined under it. It

controls expenses and minimizes expenses by eliminating unnecessary wastes and

unproductive processes, resulting in maximizing aggregate earnings.

Critical Analysis:

In corporation like Anglian Limited, combination of more than one above discussed

techniques are applied by managing officials with aim to establishing control, planning and

decision-making. An overall development of corporation fundamentally depends upon these

three core activities. Here among these techniques financial planning is specifically used in

company to frame blue-print of operations and future actions. While budgetary control technique

is used by company to regulate and control business tasks (Lawrence, 2013). Analysing financial

statements of corporation help to build a structure for efficient decision-making. Corporation

also adopt historical-cost based accounting technique to take quick long term decisions. These

techniques' main aim is to provide a complete and structured procedures for effective controlling,

planning and business decision-making.

TASK 2

Calculation of the ratios to analyse company performance:

Ratios 2018 2017

ROCE or Return On Capital

Employed :

= (Operating Profit /Capital

= 412 / 2925 * 100

= 14.10%

= 375 / 1912.50 *100

= 19.60%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Employed) *100

here, Capital Employed = Total

Assets – External liabilities.

Net Profit Margin:

= Net Profit / Sale * 100

= 262.50 / 3000 * 100

= 8.75 %

= 300/ 2400 * 100

= 12.5 %

Current Ratio:

= Current Assets / Current

Liability

= 1035 / 1110

= 0.93

= 757.50 / 322.50

= 2.34

Debtor Collection Period:

= Receivable / Sales *365

= 600 / 3000 * 365

= 73 Days

= 450 / 2400 * 365

= 68.43

= 68 Days

Creditor Collection Period:

= Payable / Purchase * 365

= 1050 / 2400 * 365

= 159.68

= 160 Days

= 285 / 1350 * 365

= 77.05

= 77 Days

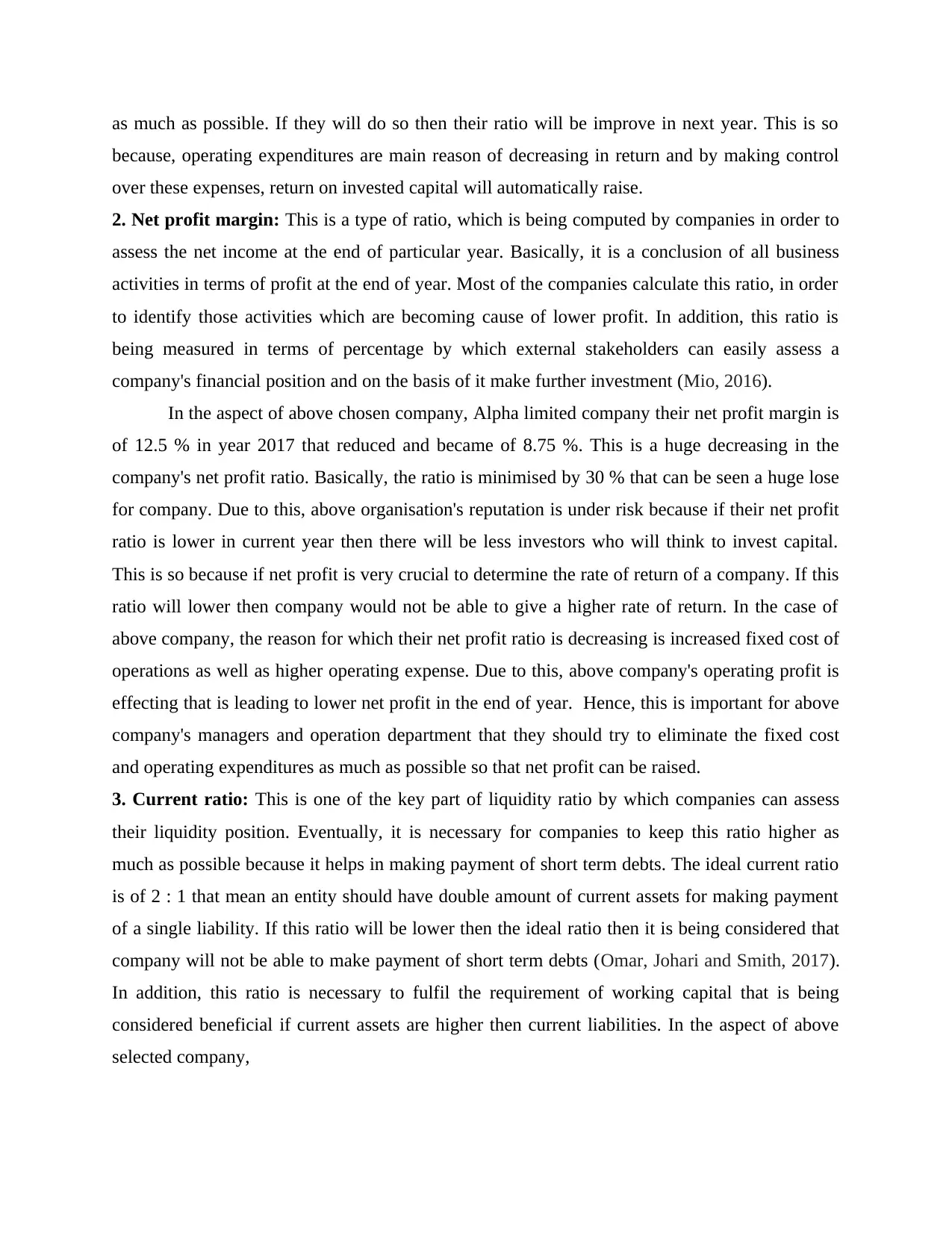

Interpretation and analysis of financial ratios:

1. Return on Capital Employed: This is a type of ratio that is linked with the analysis of

effectiveness of companies about earning profits from capital which is invested in various kind

of ratios. With the help of this ratio, organisations can focus on those activities which are higher

profitable and accordingly can make investment further. In the aspect of above chosen Alpha

limited company, their accountants compute this ratio to find out total amount of return on their

invested capital in multi-pal activities. Eventually, in the absence of calculating this ratio, it can

be difficult to companies to make suitable investment decisions (Lisowsky and Minnis, 2018).

In above respective company, the ratio of return on capital employed is of 19.60% that

reduced in next year 2018 and became of 14.08%. Hence, their ratio decreased by 5% which is

clearly indicating that company is not able to gain good return on invested capital into multi-pal

operations. The main reason behind this lower ratio of company in year 2018 is increasing in

operating expenditures. In year 2017, their operating expenditures were of 300 that raised by

huge criteria and became of 337.50. Due to this, automatically their return has been decreased in

year 2018. Hence, this is important for them to focusing in reducing the operating expenditures

here, Capital Employed = Total

Assets – External liabilities.

Net Profit Margin:

= Net Profit / Sale * 100

= 262.50 / 3000 * 100

= 8.75 %

= 300/ 2400 * 100

= 12.5 %

Current Ratio:

= Current Assets / Current

Liability

= 1035 / 1110

= 0.93

= 757.50 / 322.50

= 2.34

Debtor Collection Period:

= Receivable / Sales *365

= 600 / 3000 * 365

= 73 Days

= 450 / 2400 * 365

= 68.43

= 68 Days

Creditor Collection Period:

= Payable / Purchase * 365

= 1050 / 2400 * 365

= 159.68

= 160 Days

= 285 / 1350 * 365

= 77.05

= 77 Days

Interpretation and analysis of financial ratios:

1. Return on Capital Employed: This is a type of ratio that is linked with the analysis of

effectiveness of companies about earning profits from capital which is invested in various kind

of ratios. With the help of this ratio, organisations can focus on those activities which are higher

profitable and accordingly can make investment further. In the aspect of above chosen Alpha

limited company, their accountants compute this ratio to find out total amount of return on their

invested capital in multi-pal activities. Eventually, in the absence of calculating this ratio, it can

be difficult to companies to make suitable investment decisions (Lisowsky and Minnis, 2018).

In above respective company, the ratio of return on capital employed is of 19.60% that

reduced in next year 2018 and became of 14.08%. Hence, their ratio decreased by 5% which is

clearly indicating that company is not able to gain good return on invested capital into multi-pal

operations. The main reason behind this lower ratio of company in year 2018 is increasing in

operating expenditures. In year 2017, their operating expenditures were of 300 that raised by

huge criteria and became of 337.50. Due to this, automatically their return has been decreased in

year 2018. Hence, this is important for them to focusing in reducing the operating expenditures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

as much as possible. If they will do so then their ratio will be improve in next year. This is so

because, operating expenditures are main reason of decreasing in return and by making control

over these expenses, return on invested capital will automatically raise.

2. Net profit margin: This is a type of ratio, which is being computed by companies in order to

assess the net income at the end of particular year. Basically, it is a conclusion of all business

activities in terms of profit at the end of year. Most of the companies calculate this ratio, in order

to identify those activities which are becoming cause of lower profit. In addition, this ratio is

being measured in terms of percentage by which external stakeholders can easily assess a

company's financial position and on the basis of it make further investment (Mio, 2016).

In the aspect of above chosen company, Alpha limited company their net profit margin is

of 12.5 % in year 2017 that reduced and became of 8.75 %. This is a huge decreasing in the

company's net profit ratio. Basically, the ratio is minimised by 30 % that can be seen a huge lose

for company. Due to this, above organisation's reputation is under risk because if their net profit

ratio is lower in current year then there will be less investors who will think to invest capital.

This is so because if net profit is very crucial to determine the rate of return of a company. If this

ratio will lower then company would not be able to give a higher rate of return. In the case of

above company, the reason for which their net profit ratio is decreasing is increased fixed cost of

operations as well as higher operating expense. Due to this, above company's operating profit is

effecting that is leading to lower net profit in the end of year. Hence, this is important for above

company's managers and operation department that they should try to eliminate the fixed cost

and operating expenditures as much as possible so that net profit can be raised.

3. Current ratio: This is one of the key part of liquidity ratio by which companies can assess

their liquidity position. Eventually, it is necessary for companies to keep this ratio higher as

much as possible because it helps in making payment of short term debts. The ideal current ratio

is of 2 : 1 that mean an entity should have double amount of current assets for making payment

of a single liability. If this ratio will be lower then the ideal ratio then it is being considered that

company will not be able to make payment of short term debts (Omar, Johari and Smith, 2017).

In addition, this ratio is necessary to fulfil the requirement of working capital that is being

considered beneficial if current assets are higher then current liabilities. In the aspect of above

selected company,

because, operating expenditures are main reason of decreasing in return and by making control

over these expenses, return on invested capital will automatically raise.

2. Net profit margin: This is a type of ratio, which is being computed by companies in order to

assess the net income at the end of particular year. Basically, it is a conclusion of all business

activities in terms of profit at the end of year. Most of the companies calculate this ratio, in order

to identify those activities which are becoming cause of lower profit. In addition, this ratio is

being measured in terms of percentage by which external stakeholders can easily assess a

company's financial position and on the basis of it make further investment (Mio, 2016).

In the aspect of above chosen company, Alpha limited company their net profit margin is

of 12.5 % in year 2017 that reduced and became of 8.75 %. This is a huge decreasing in the

company's net profit ratio. Basically, the ratio is minimised by 30 % that can be seen a huge lose

for company. Due to this, above organisation's reputation is under risk because if their net profit

ratio is lower in current year then there will be less investors who will think to invest capital.

This is so because if net profit is very crucial to determine the rate of return of a company. If this

ratio will lower then company would not be able to give a higher rate of return. In the case of

above company, the reason for which their net profit ratio is decreasing is increased fixed cost of

operations as well as higher operating expense. Due to this, above company's operating profit is

effecting that is leading to lower net profit in the end of year. Hence, this is important for above

company's managers and operation department that they should try to eliminate the fixed cost

and operating expenditures as much as possible so that net profit can be raised.

3. Current ratio: This is one of the key part of liquidity ratio by which companies can assess

their liquidity position. Eventually, it is necessary for companies to keep this ratio higher as

much as possible because it helps in making payment of short term debts. The ideal current ratio

is of 2 : 1 that mean an entity should have double amount of current assets for making payment

of a single liability. If this ratio will be lower then the ideal ratio then it is being considered that

company will not be able to make payment of short term debts (Omar, Johari and Smith, 2017).

In addition, this ratio is necessary to fulfil the requirement of working capital that is being

considered beneficial if current assets are higher then current liabilities. In the aspect of above

selected company,

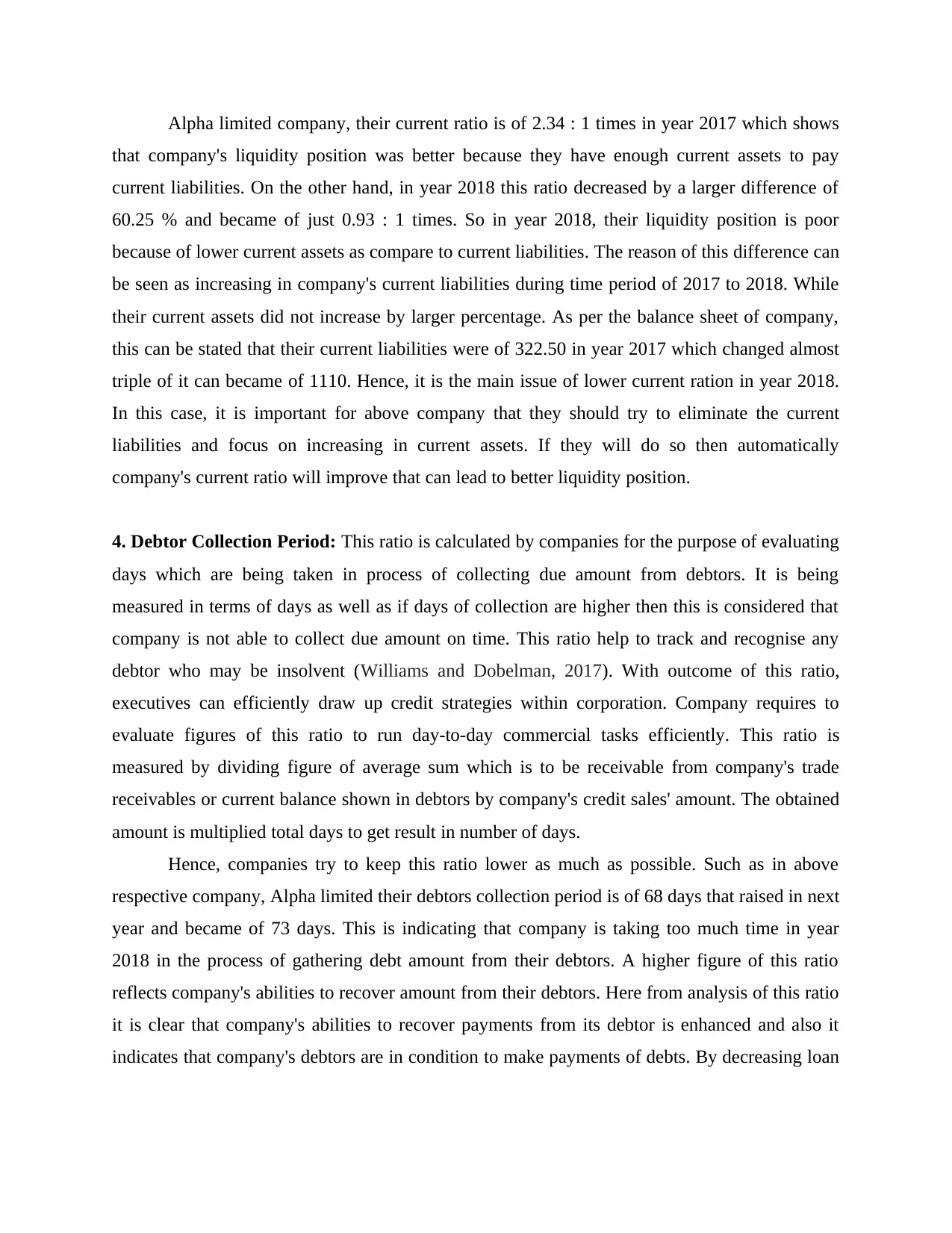

Alpha limited company, their current ratio is of 2.34 : 1 times in year 2017 which shows

that company's liquidity position was better because they have enough current assets to pay

current liabilities. On the other hand, in year 2018 this ratio decreased by a larger difference of

60.25 % and became of just 0.93 : 1 times. So in year 2018, their liquidity position is poor

because of lower current assets as compare to current liabilities. The reason of this difference can

be seen as increasing in company's current liabilities during time period of 2017 to 2018. While

their current assets did not increase by larger percentage. As per the balance sheet of company,

this can be stated that their current liabilities were of 322.50 in year 2017 which changed almost

triple of it can became of 1110. Hence, it is the main issue of lower current ration in year 2018.

In this case, it is important for above company that they should try to eliminate the current

liabilities and focus on increasing in current assets. If they will do so then automatically

company's current ratio will improve that can lead to better liquidity position.

4. Debtor Collection Period: This ratio is calculated by companies for the purpose of evaluating

days which are being taken in process of collecting due amount from debtors. It is being

measured in terms of days as well as if days of collection are higher then this is considered that

company is not able to collect due amount on time. This ratio help to track and recognise any

debtor who may be insolvent (Williams and Dobelman, 2017). With outcome of this ratio,

executives can efficiently draw up credit strategies within corporation. Company requires to

evaluate figures of this ratio to run day-to-day commercial tasks efficiently. This ratio is

measured by dividing figure of average sum which is to be receivable from company's trade

receivables or current balance shown in debtors by company's credit sales' amount. The obtained

amount is multiplied total days to get result in number of days.

Hence, companies try to keep this ratio lower as much as possible. Such as in above

respective company, Alpha limited their debtors collection period is of 68 days that raised in next

year and became of 73 days. This is indicating that company is taking too much time in year

2018 in the process of gathering debt amount from their debtors. A higher figure of this ratio

reflects company's abilities to recover amount from their debtors. Here from analysis of this ratio

it is clear that company's abilities to recover payments from its debtor is enhanced and also it

indicates that company's debtors are in condition to make payments of debts. By decreasing loan

that company's liquidity position was better because they have enough current assets to pay

current liabilities. On the other hand, in year 2018 this ratio decreased by a larger difference of

60.25 % and became of just 0.93 : 1 times. So in year 2018, their liquidity position is poor

because of lower current assets as compare to current liabilities. The reason of this difference can

be seen as increasing in company's current liabilities during time period of 2017 to 2018. While

their current assets did not increase by larger percentage. As per the balance sheet of company,

this can be stated that their current liabilities were of 322.50 in year 2017 which changed almost

triple of it can became of 1110. Hence, it is the main issue of lower current ration in year 2018.

In this case, it is important for above company that they should try to eliminate the current

liabilities and focus on increasing in current assets. If they will do so then automatically

company's current ratio will improve that can lead to better liquidity position.

4. Debtor Collection Period: This ratio is calculated by companies for the purpose of evaluating

days which are being taken in process of collecting due amount from debtors. It is being

measured in terms of days as well as if days of collection are higher then this is considered that

company is not able to collect due amount on time. This ratio help to track and recognise any

debtor who may be insolvent (Williams and Dobelman, 2017). With outcome of this ratio,

executives can efficiently draw up credit strategies within corporation. Company requires to

evaluate figures of this ratio to run day-to-day commercial tasks efficiently. This ratio is

measured by dividing figure of average sum which is to be receivable from company's trade

receivables or current balance shown in debtors by company's credit sales' amount. The obtained

amount is multiplied total days to get result in number of days.

Hence, companies try to keep this ratio lower as much as possible. Such as in above

respective company, Alpha limited their debtors collection period is of 68 days that raised in next

year and became of 73 days. This is indicating that company is taking too much time in year

2018 in the process of gathering debt amount from their debtors. A higher figure of this ratio

reflects company's abilities to recover amount from their debtors. Here from analysis of this ratio

it is clear that company's abilities to recover payments from its debtor is enhanced and also it

indicates that company's debtors are in condition to make payments of debts. By decreasing loan

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sales and optimizing the loan period provided to its debtors, the corporation can enhance this

ratio.

5. Creditors Collection Period: It's a crucial financial ratio that reflects days in number

(average) a corporation takes to make payments to its different creditors or accounts payables.

Company's creditors includes its all suppliers and vendors some other firms providing goods on

credits for short period. It is computed by companies generally on annually basis to assess how

efficiently cash outflows within company are managed (Agarwal and et.al., 2014). A company

with higher ratio or creditor-collection period generally takes more time for making payment

company's credit bills. It reflects corporation's performance and efficiencies in term of liquidity.

It simply act as an indication that company's efficiency to payout its credit liabilities. Creditors

can also use this ratio to determine credit terms for company. It also represents company's

liquidity situation as on specific date.

In 2017 and 2018, company Alpha Ltd has shown trade payable balance at amounts of

285000 and 1050000 respectively. Purchases of the company in year 2018 and 2017 are 2400000

and 1350000 respectively. Here it is presumed that all purchases are on credit basis. Company's

average payable duration is 160 days in year 2018, which was of 77 days in year 2017. Through

analysis of these outcomes it has been evaluated that there is a decline in duration of average

payable period which shows that corporation's is efficiencies to payout debts of trade payable has

decreased.

CONCLUSION

From above discussed report it has been articulated that financial decision-making act as

an essential framework for business enterprise to ascertain strategy for future growth and

improvement in overall operational structure. Techniques involved in managerial accoutring is

part of this framework as it allow company to develop control, planning and decision-making,

which in long run ensure company's strategic success. Ratio analysis is another major aspect of

fiscal-decision making as it enable corporation to evaluate real-time progress and performance

to take momentous business decisions.

ratio.

5. Creditors Collection Period: It's a crucial financial ratio that reflects days in number

(average) a corporation takes to make payments to its different creditors or accounts payables.

Company's creditors includes its all suppliers and vendors some other firms providing goods on

credits for short period. It is computed by companies generally on annually basis to assess how

efficiently cash outflows within company are managed (Agarwal and et.al., 2014). A company

with higher ratio or creditor-collection period generally takes more time for making payment

company's credit bills. It reflects corporation's performance and efficiencies in term of liquidity.

It simply act as an indication that company's efficiency to payout its credit liabilities. Creditors

can also use this ratio to determine credit terms for company. It also represents company's

liquidity situation as on specific date.

In 2017 and 2018, company Alpha Ltd has shown trade payable balance at amounts of

285000 and 1050000 respectively. Purchases of the company in year 2018 and 2017 are 2400000

and 1350000 respectively. Here it is presumed that all purchases are on credit basis. Company's

average payable duration is 160 days in year 2018, which was of 77 days in year 2017. Through

analysis of these outcomes it has been evaluated that there is a decline in duration of average

payable period which shows that corporation's is efficiencies to payout debts of trade payable has

decreased.

CONCLUSION

From above discussed report it has been articulated that financial decision-making act as

an essential framework for business enterprise to ascertain strategy for future growth and

improvement in overall operational structure. Techniques involved in managerial accoutring is

part of this framework as it allow company to develop control, planning and decision-making,

which in long run ensure company's strategic success. Ratio analysis is another major aspect of

fiscal-decision making as it enable corporation to evaluate real-time progress and performance

to take momentous business decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Agarwal, S. and et.al., 2014. Financial decision making when buying and owning a home.

Available at SSRN 2498111.

Ball, R., 2013. Accounting informs investors and earnings management is rife: Two

questionable beliefs. Accounting Horizons. 27(4). pp.847-853.

Bryer, R., 2013. Americanism and financial accounting theory–Part 2: The ‘modern business

enterprise’, America's transition to capitalism, and the genesis of management

accounting. Critical Perspectives on Accounting. 24(4-5). pp.273-318.

Knežević, S., Stanković, A. and Tepavac, R., 2012. Accounting Information System as a

Platform for Business and Financial Decision-Making in the Company. Management

(1820-0222). (65).

Zopounidis, C. and Doumpos, M., 2013. Multicriteria decision systems for financial problems.

Top. 21(2). pp.241-261.

Chiang, B., Nouri, H. and Samanta, S., 2014. The effects of different teaching approaches in

introductory financial accounting. Accounting Education. 23(1). pp.42-53.

Jetter, M. and Walker, J .K., 2017. Anchoring in financial decision-making: Evidence from

Jeopardy!. Journal of Economic Behavior & Organization. 141. pp.164-176.

Lawrence, A., 2013. Individual investors and financial disclosure. Journal of Accounting and

Economics. 56(1). pp.130-147.

Lisowsky, P. and Minnis, M., 2018. The Silent majority: Private US firms and financial reporting

choices. Chicago Booth Research Paper, (14-01).

Mio, C. ed., 2016. Integrated reporting: A new accounting disclosure. Springer.

Omar, N., Johari, Z. A. and Smith, M., 2017. Predicting fraudulent financial reporting using

artificial neural network. Journal of Financial Crime. 24(2). pp.362-387.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters, pp.109-169.

Online

Anglian Home. 2019 [Online] Available Through. <https://www.anglianhome.co.uk/about>

Books and Journals:

Agarwal, S. and et.al., 2014. Financial decision making when buying and owning a home.

Available at SSRN 2498111.

Ball, R., 2013. Accounting informs investors and earnings management is rife: Two

questionable beliefs. Accounting Horizons. 27(4). pp.847-853.

Bryer, R., 2013. Americanism and financial accounting theory–Part 2: The ‘modern business

enterprise’, America's transition to capitalism, and the genesis of management

accounting. Critical Perspectives on Accounting. 24(4-5). pp.273-318.

Knežević, S., Stanković, A. and Tepavac, R., 2012. Accounting Information System as a

Platform for Business and Financial Decision-Making in the Company. Management

(1820-0222). (65).

Zopounidis, C. and Doumpos, M., 2013. Multicriteria decision systems for financial problems.

Top. 21(2). pp.241-261.

Chiang, B., Nouri, H. and Samanta, S., 2014. The effects of different teaching approaches in

introductory financial accounting. Accounting Education. 23(1). pp.42-53.

Jetter, M. and Walker, J .K., 2017. Anchoring in financial decision-making: Evidence from

Jeopardy!. Journal of Economic Behavior & Organization. 141. pp.164-176.

Lawrence, A., 2013. Individual investors and financial disclosure. Journal of Accounting and

Economics. 56(1). pp.130-147.

Lisowsky, P. and Minnis, M., 2018. The Silent majority: Private US firms and financial reporting

choices. Chicago Booth Research Paper, (14-01).

Mio, C. ed., 2016. Integrated reporting: A new accounting disclosure. Springer.

Omar, N., Johari, Z. A. and Smith, M., 2017. Predicting fraudulent financial reporting using

artificial neural network. Journal of Financial Crime. 24(2). pp.362-387.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters, pp.109-169.

Online

Anglian Home. 2019 [Online] Available Through. <https://www.anglianhome.co.uk/about>

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.