In-Depth Financial Analysis: Company X Ratio & Performance Report

VerifiedAdded on 2023/06/12

|21

|3291

|59

Homework Assignment

AI Summary

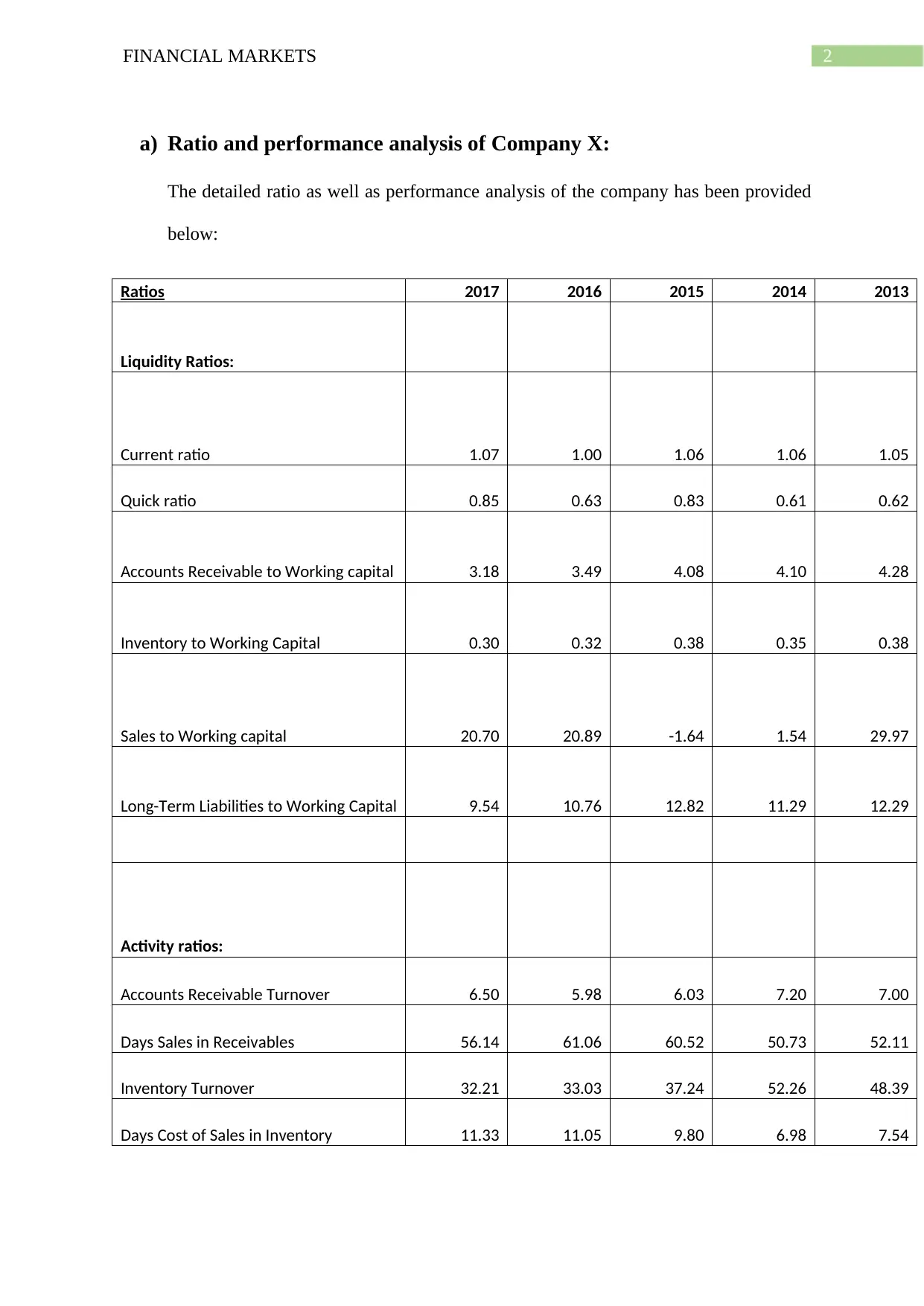

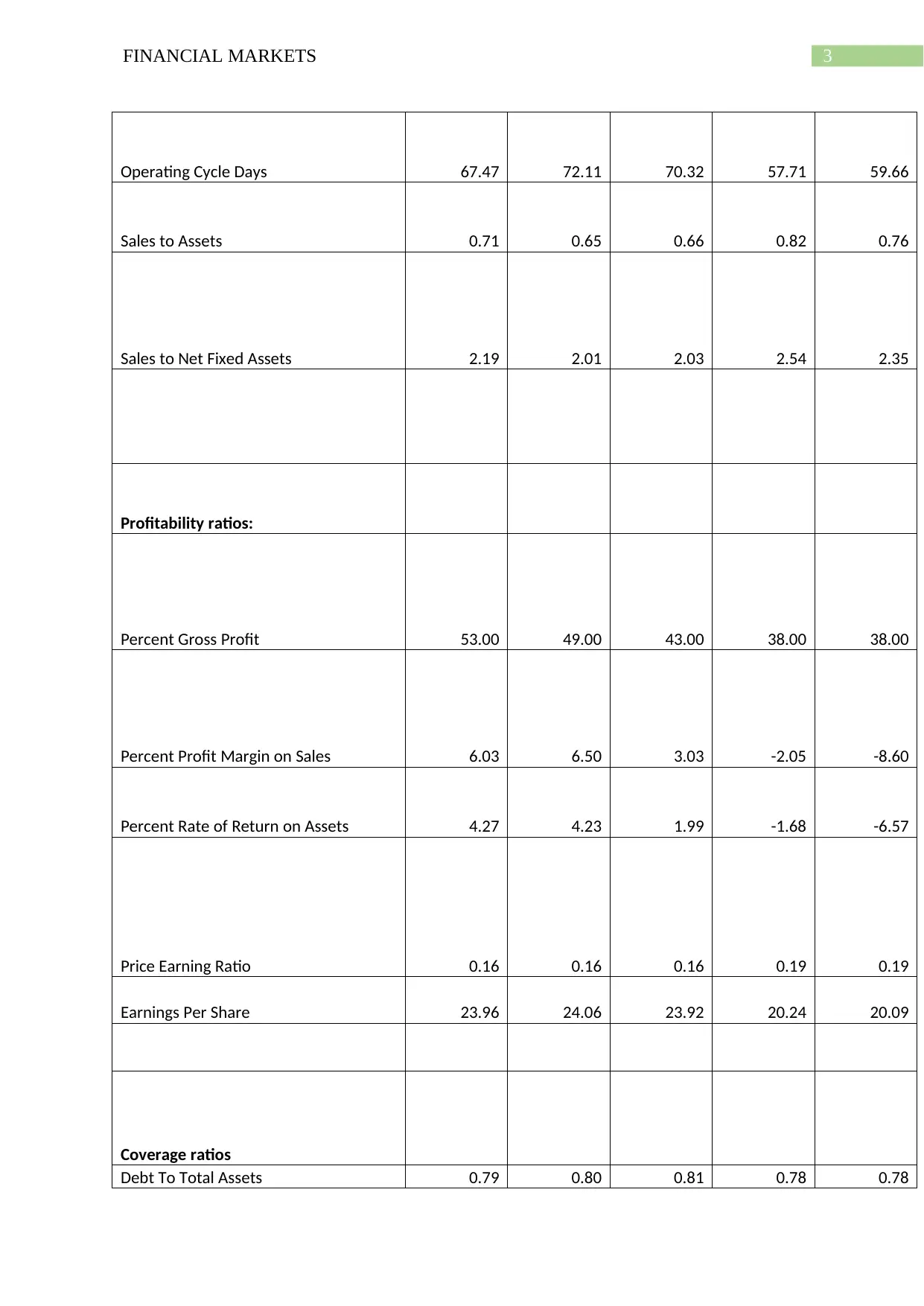

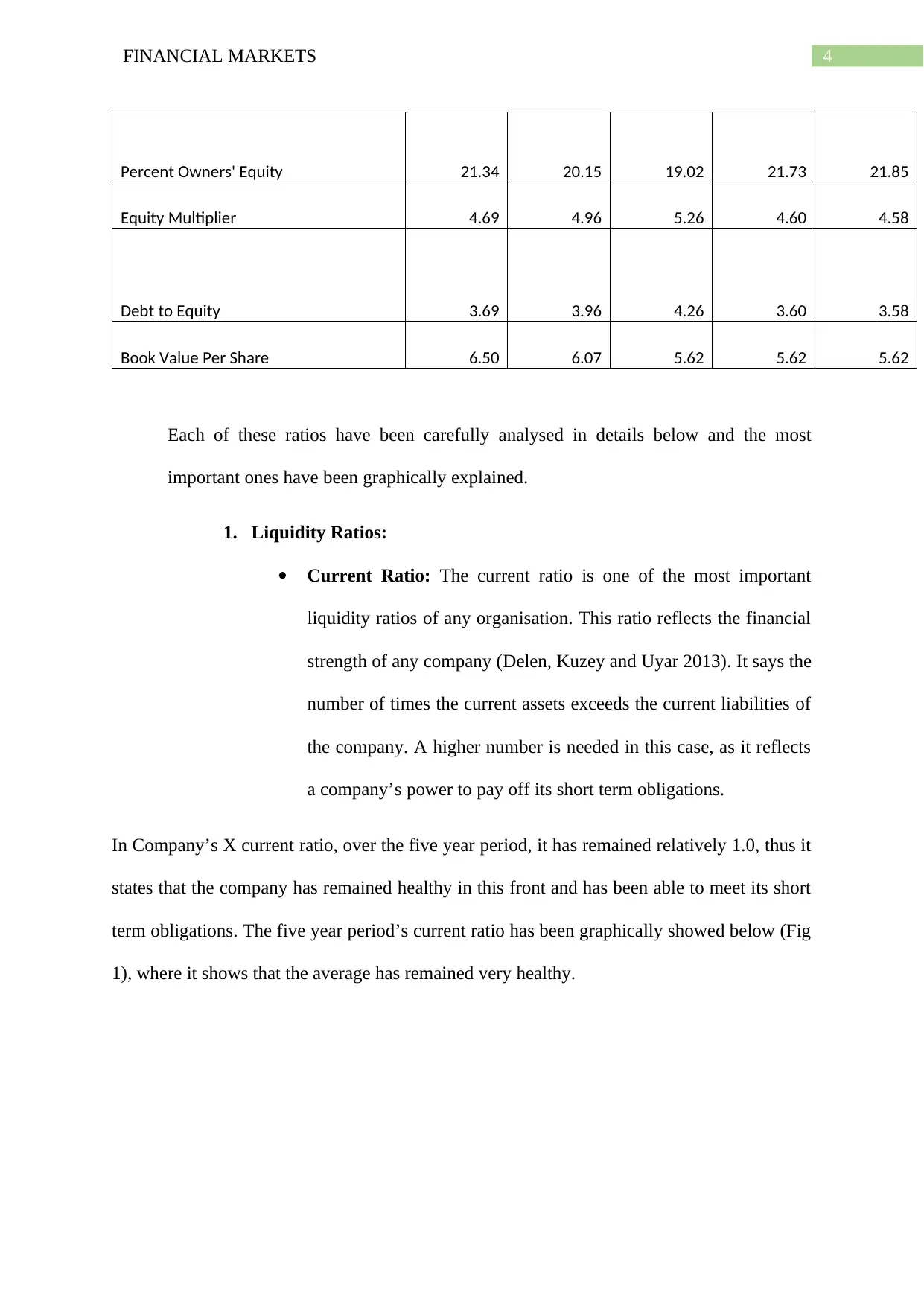

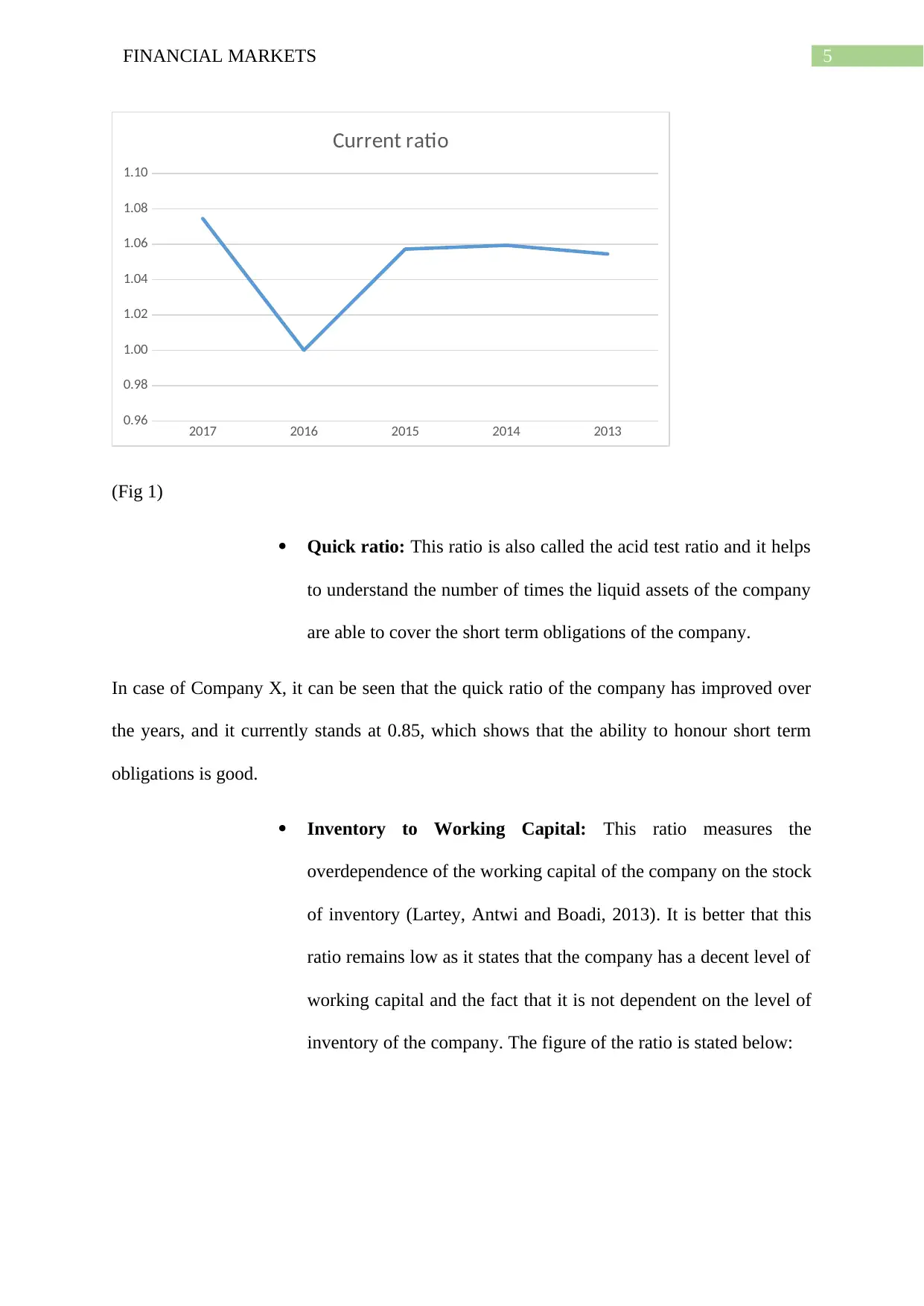

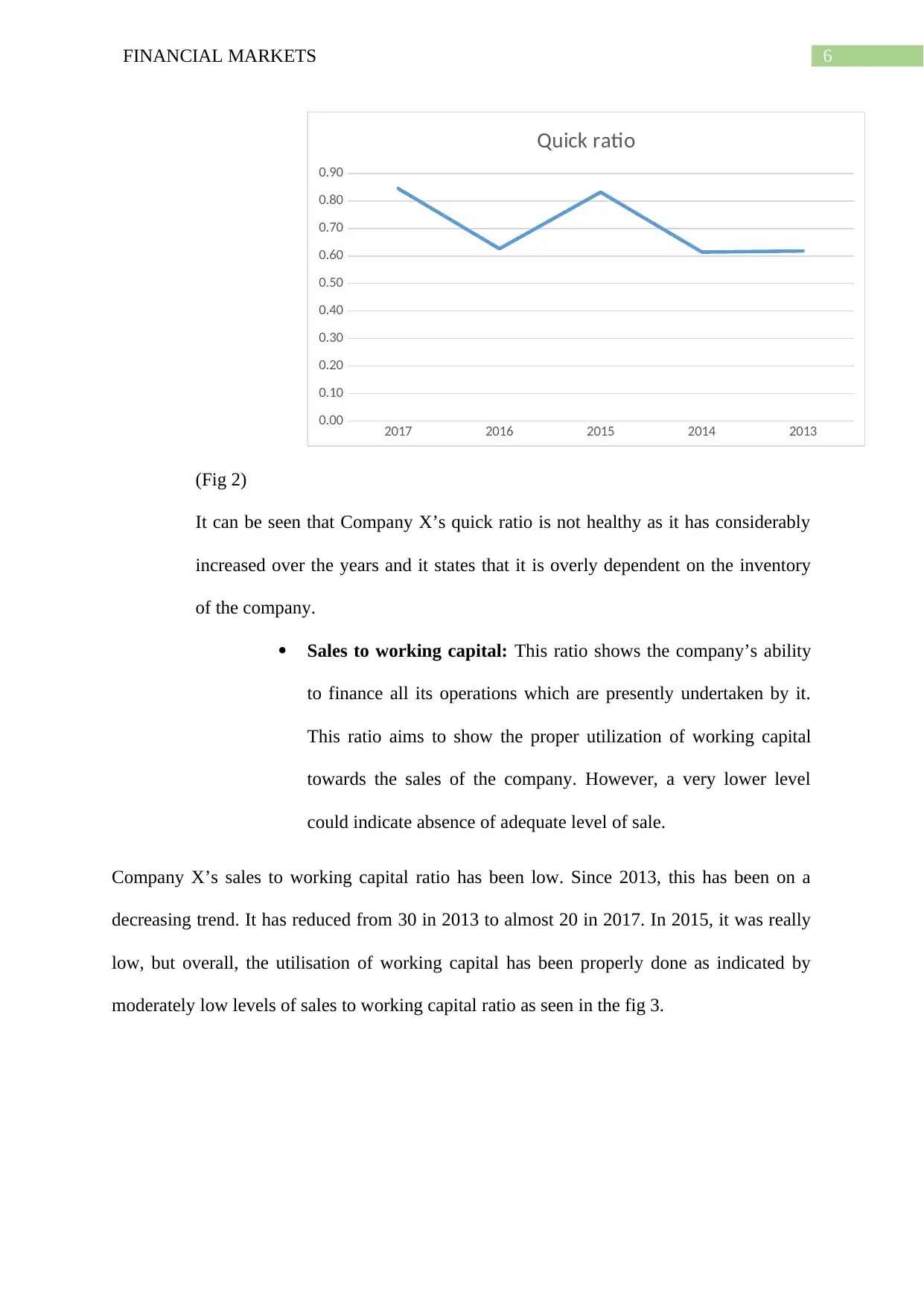

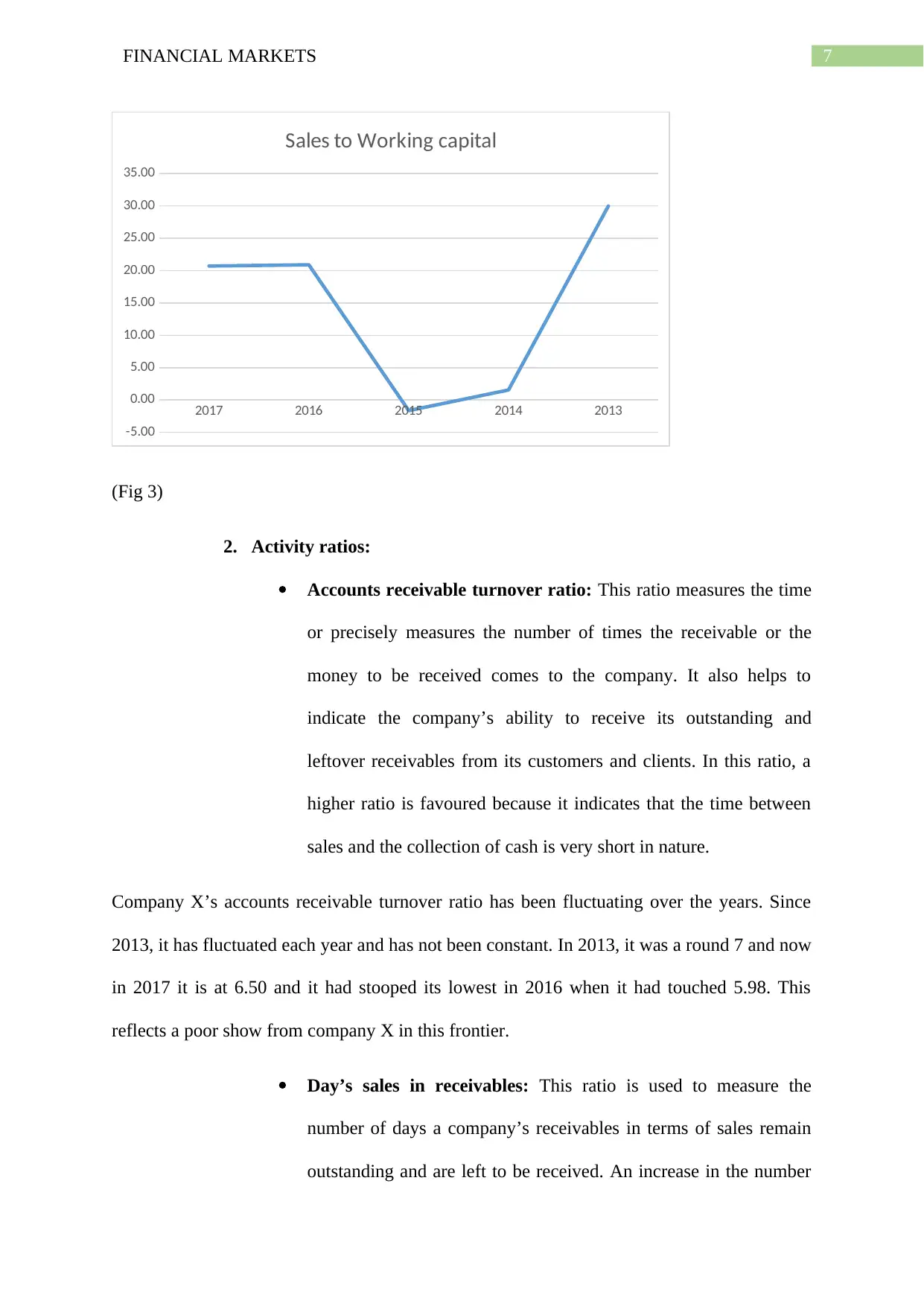

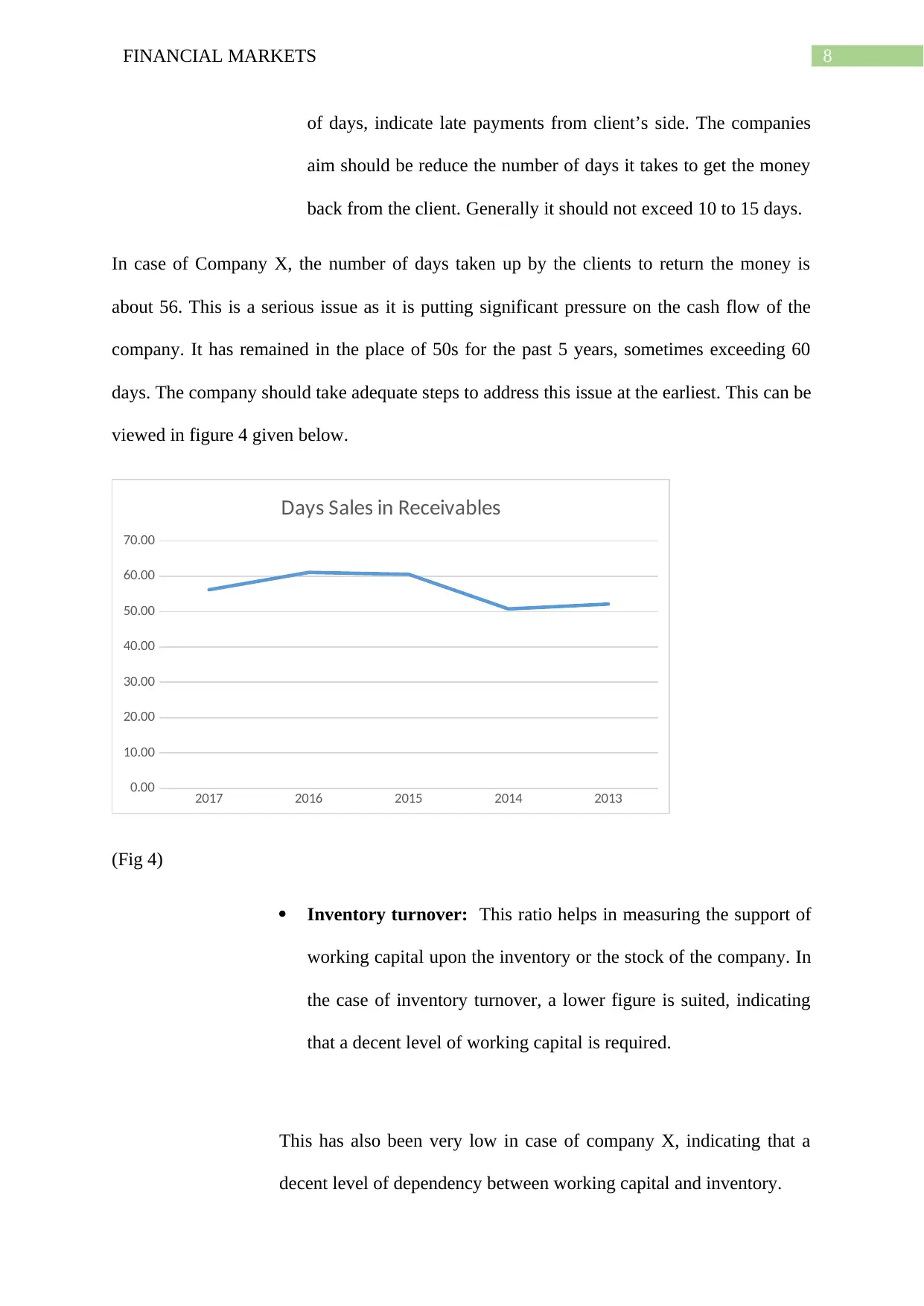

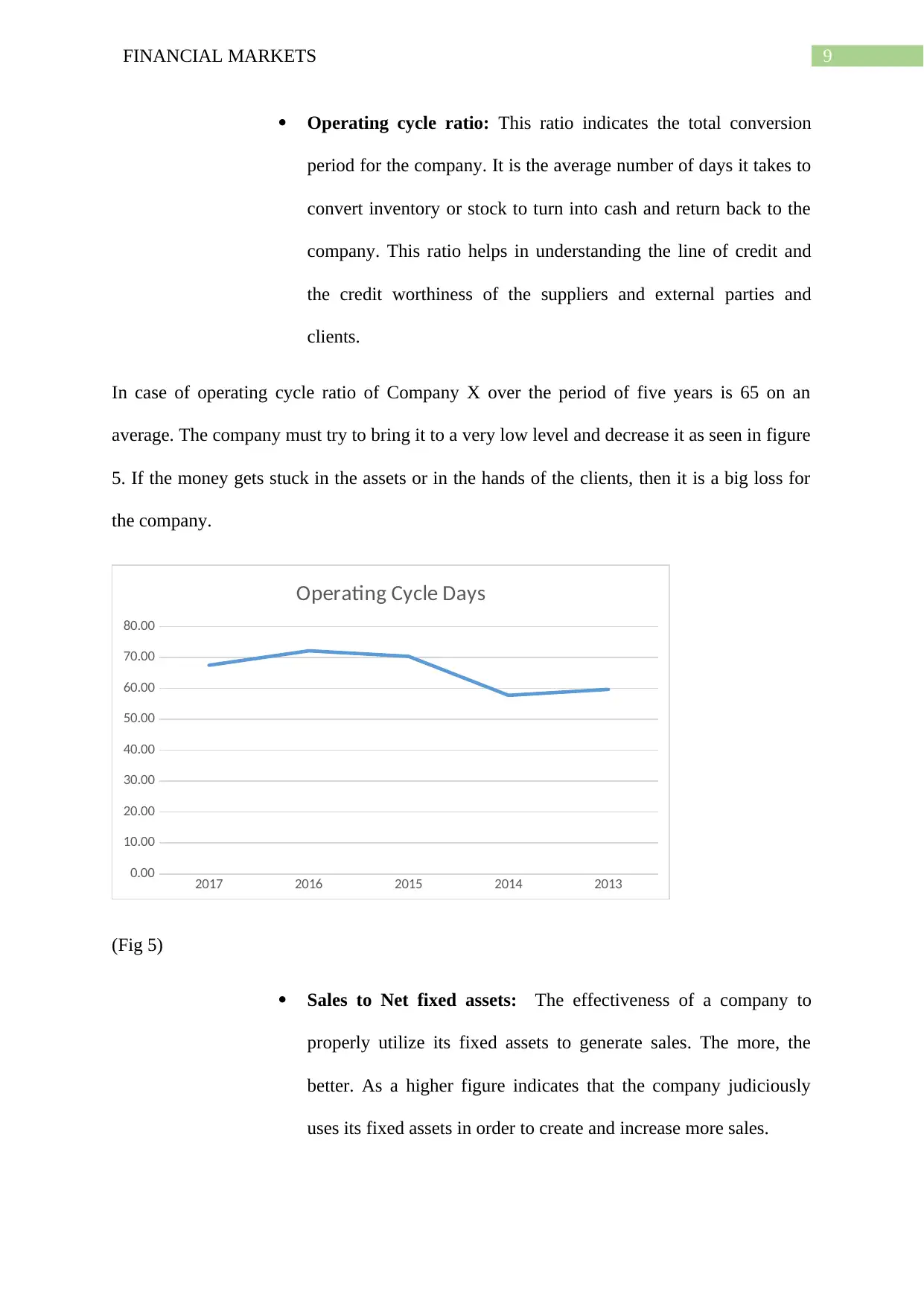

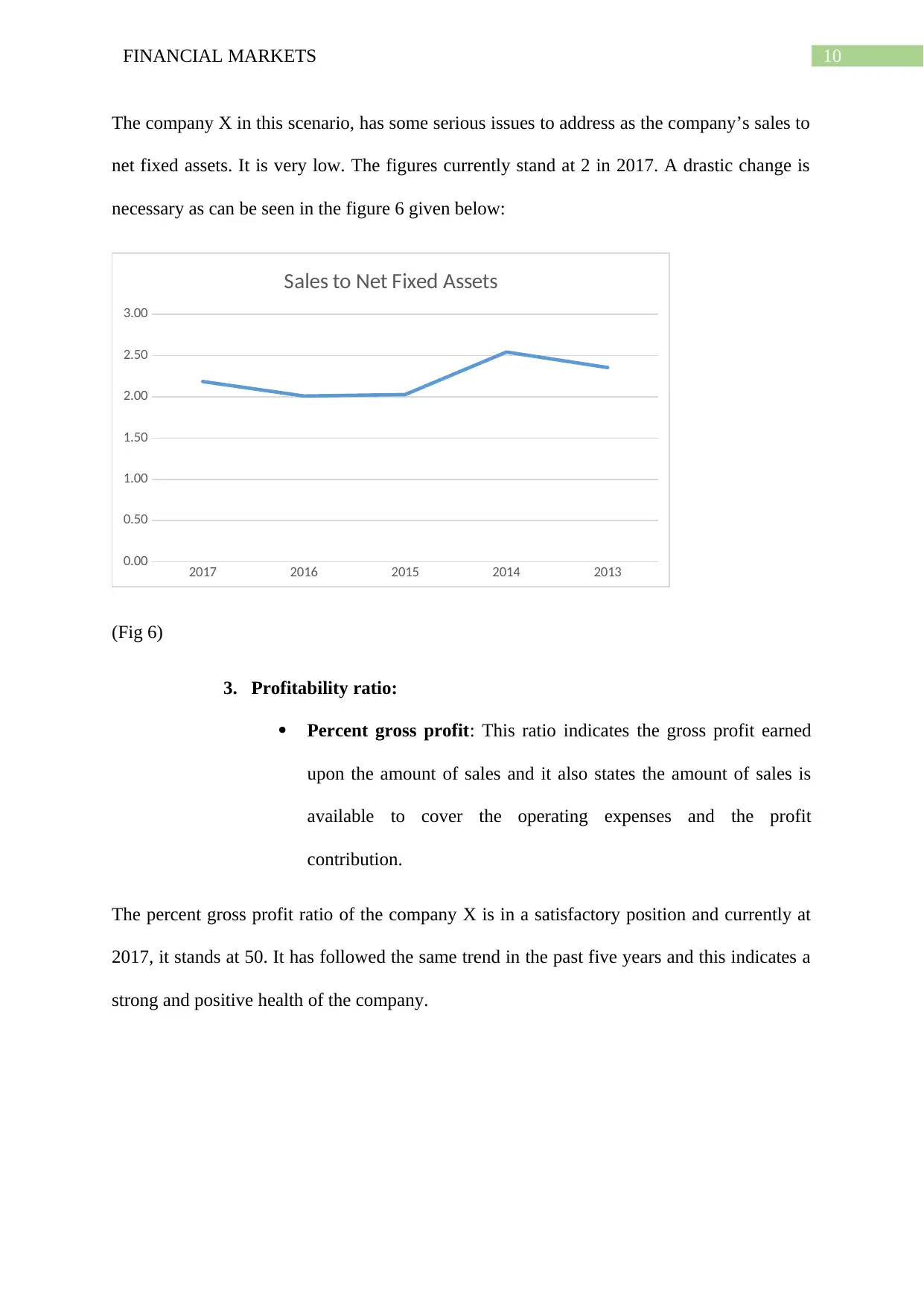

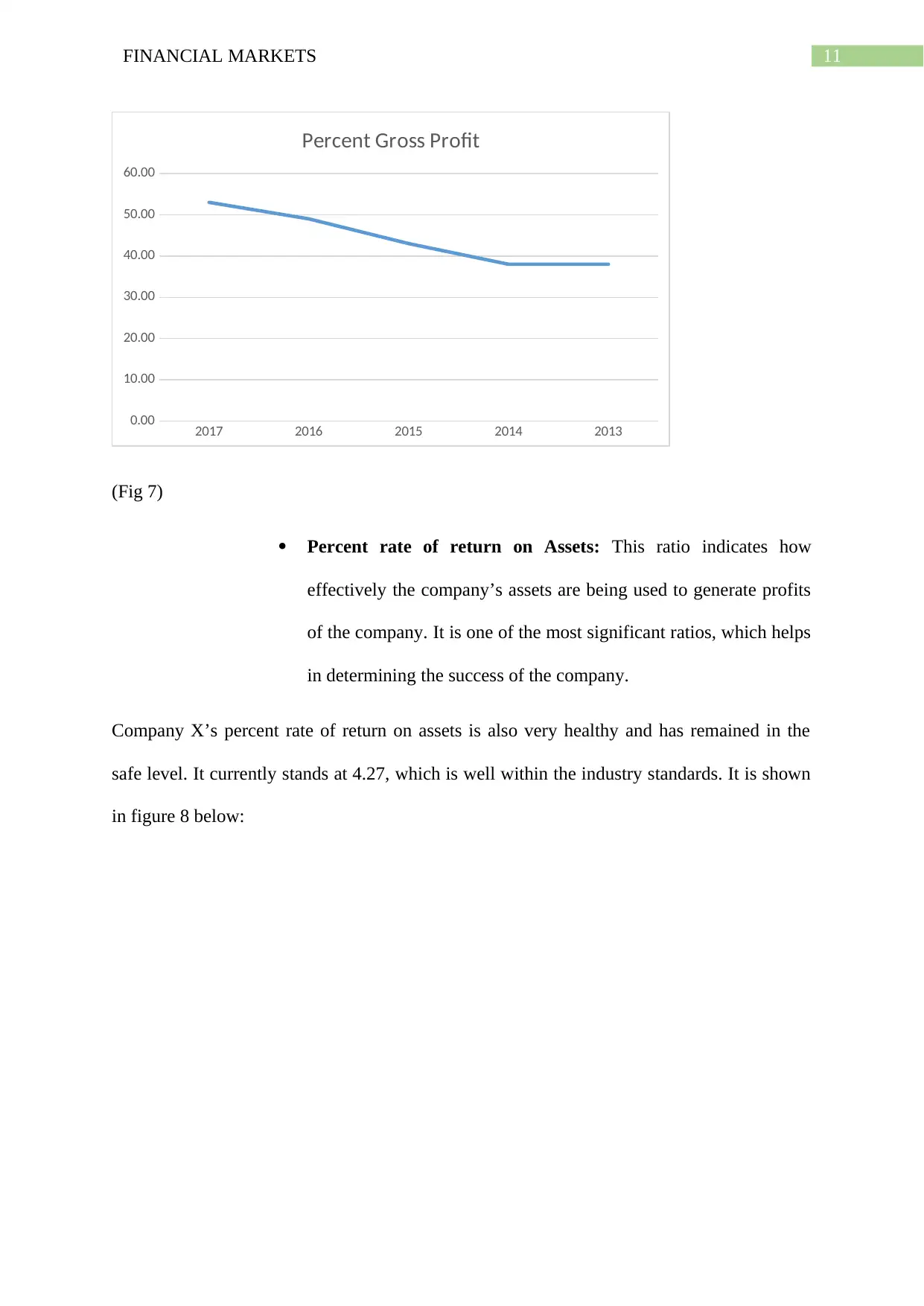

This assignment provides a comprehensive financial analysis of Company X, utilizing various financial ratios to assess the company's liquidity, activity, profitability, and coverage. The analysis spans from 2013 to 2017, examining key ratios such as current ratio, quick ratio, accounts receivable turnover, inventory turnover, debt to total assets, and debt to equity. The report includes graphical representations of these ratios to illustrate trends and performance over time. Additionally, the assignment discusses the par value and market value of the company's shares. The analysis aims to provide insights into the financial health and operational efficiency of Company X, highlighting areas of strength and potential concern. Desklib is a valuable resource for students seeking similar solved assignments and study tools.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.