Comparative Financial Ratio Analysis of Boral and CSR Limited

VerifiedAdded on 2020/02/24

|10

|1161

|40

Report

AI Summary

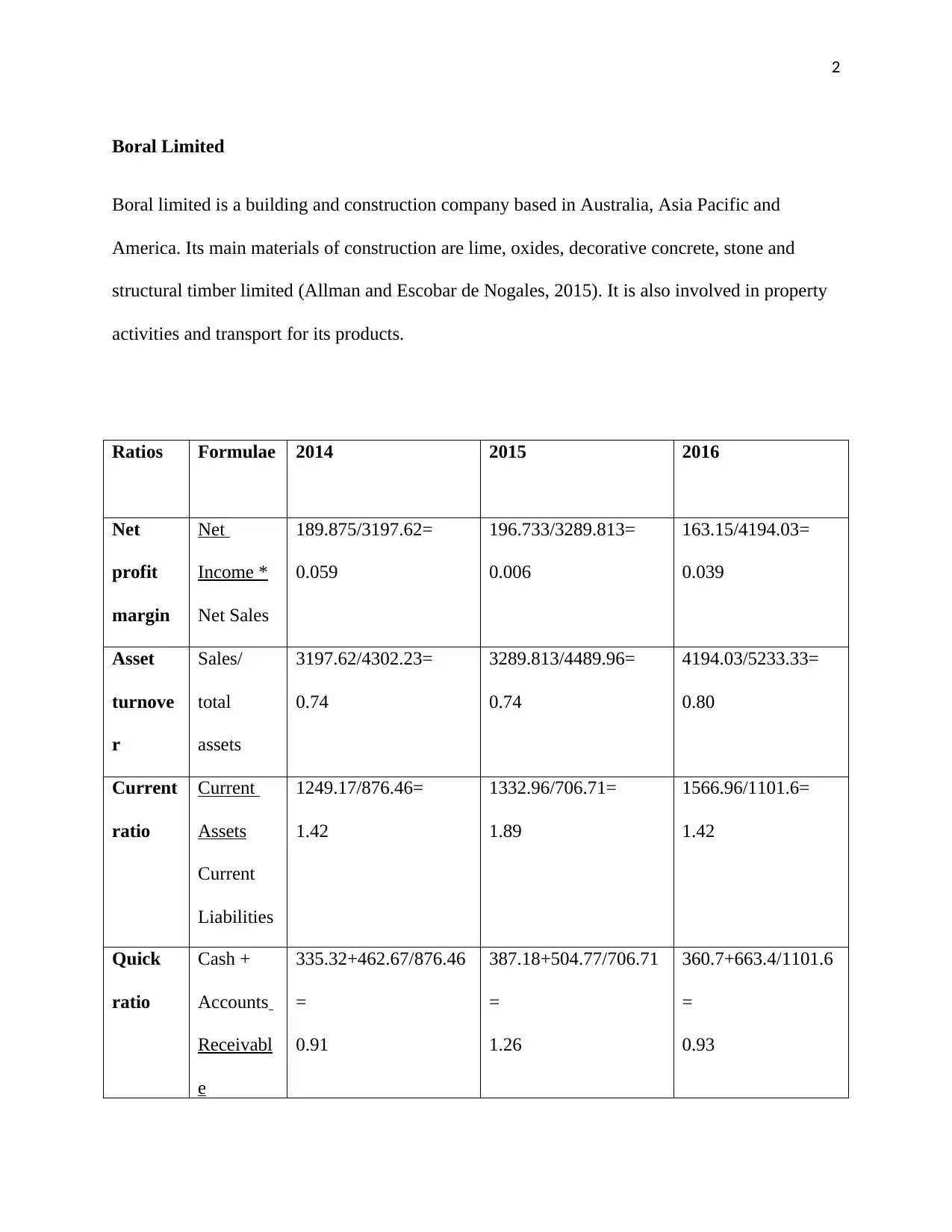

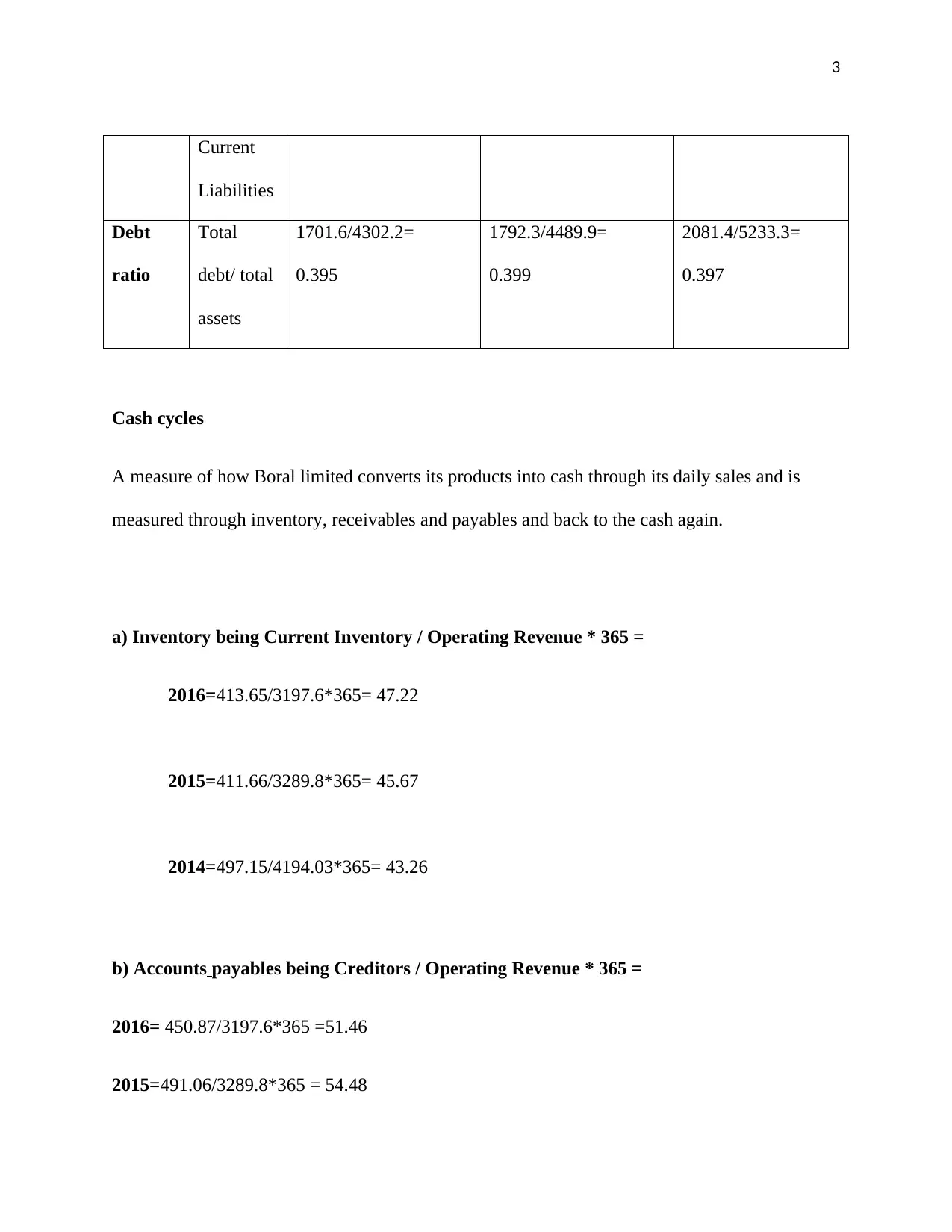

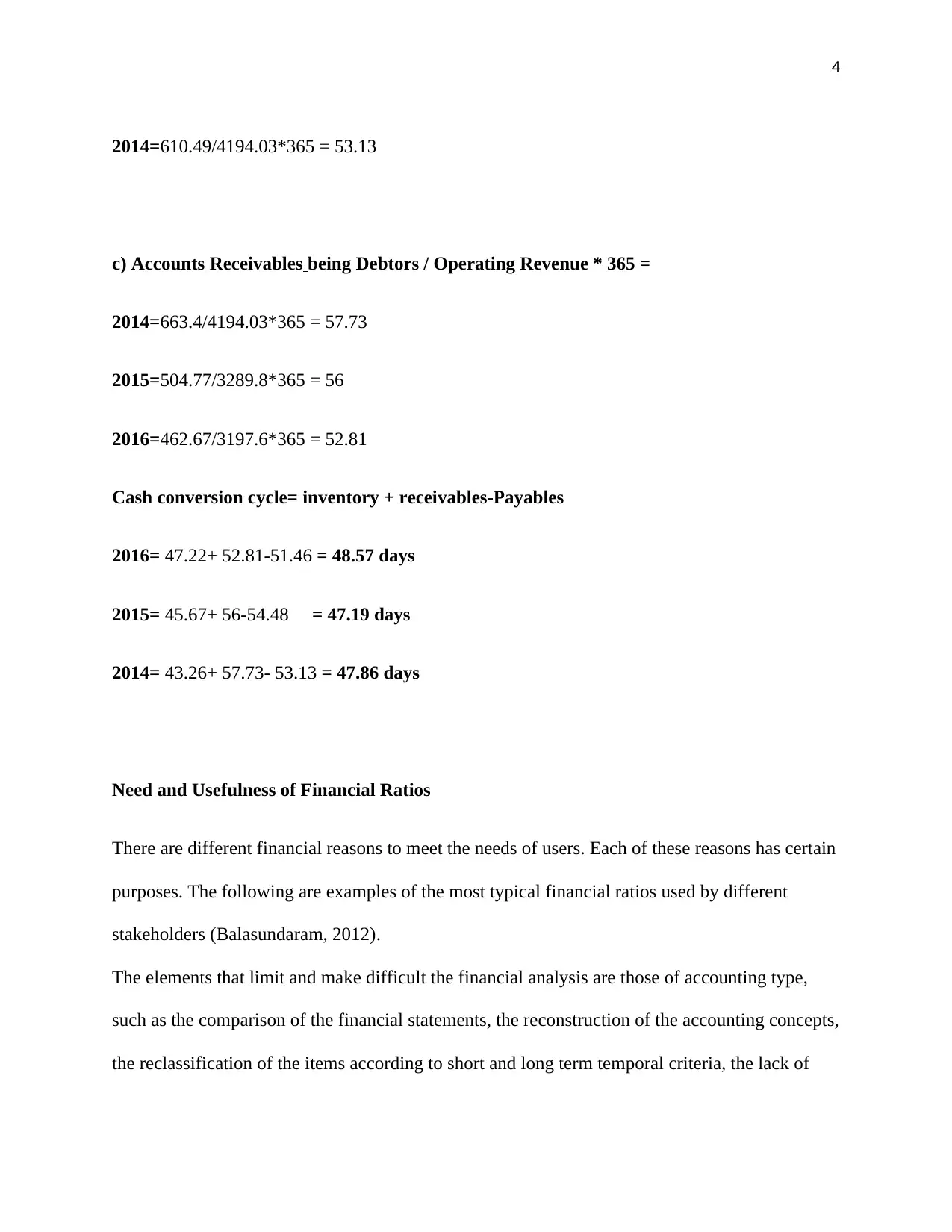

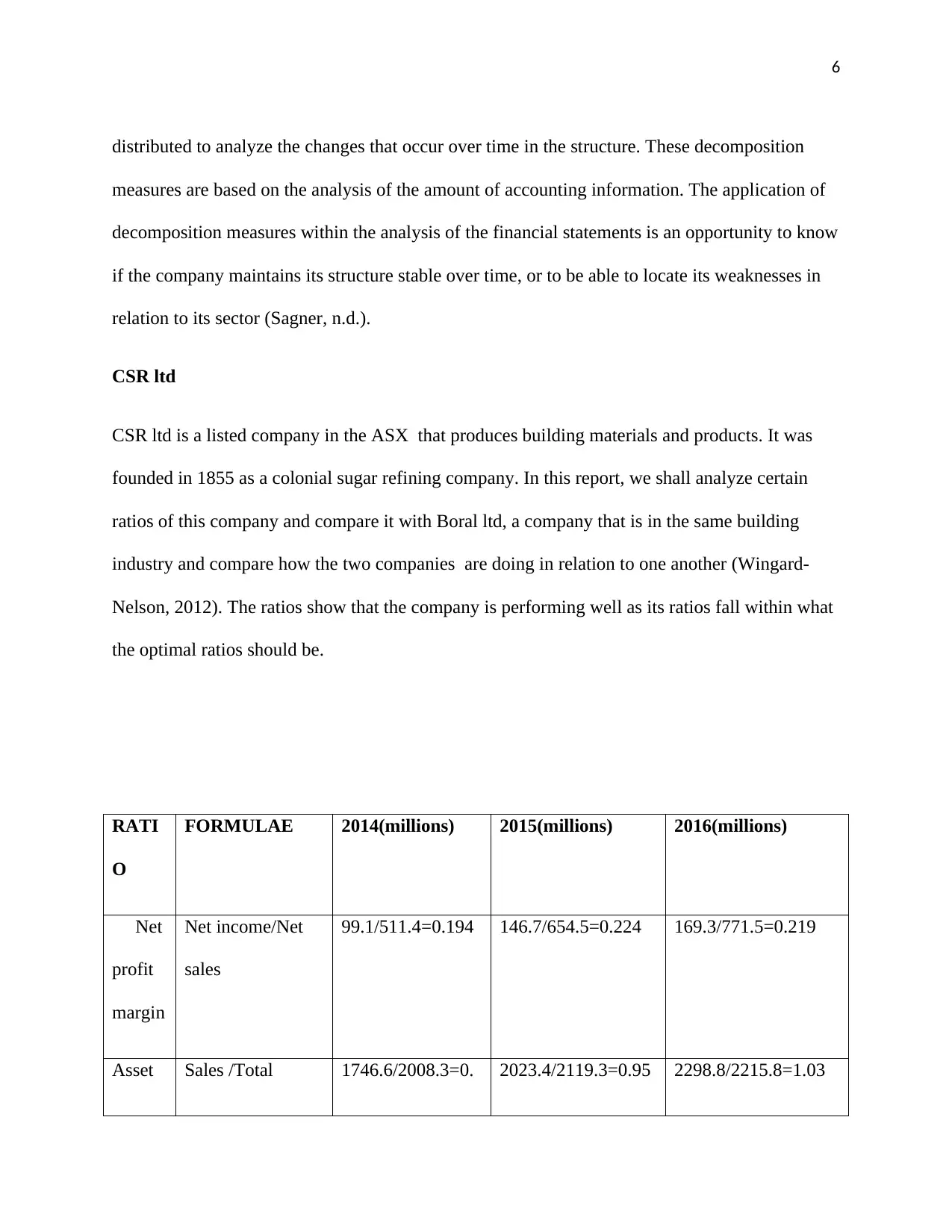

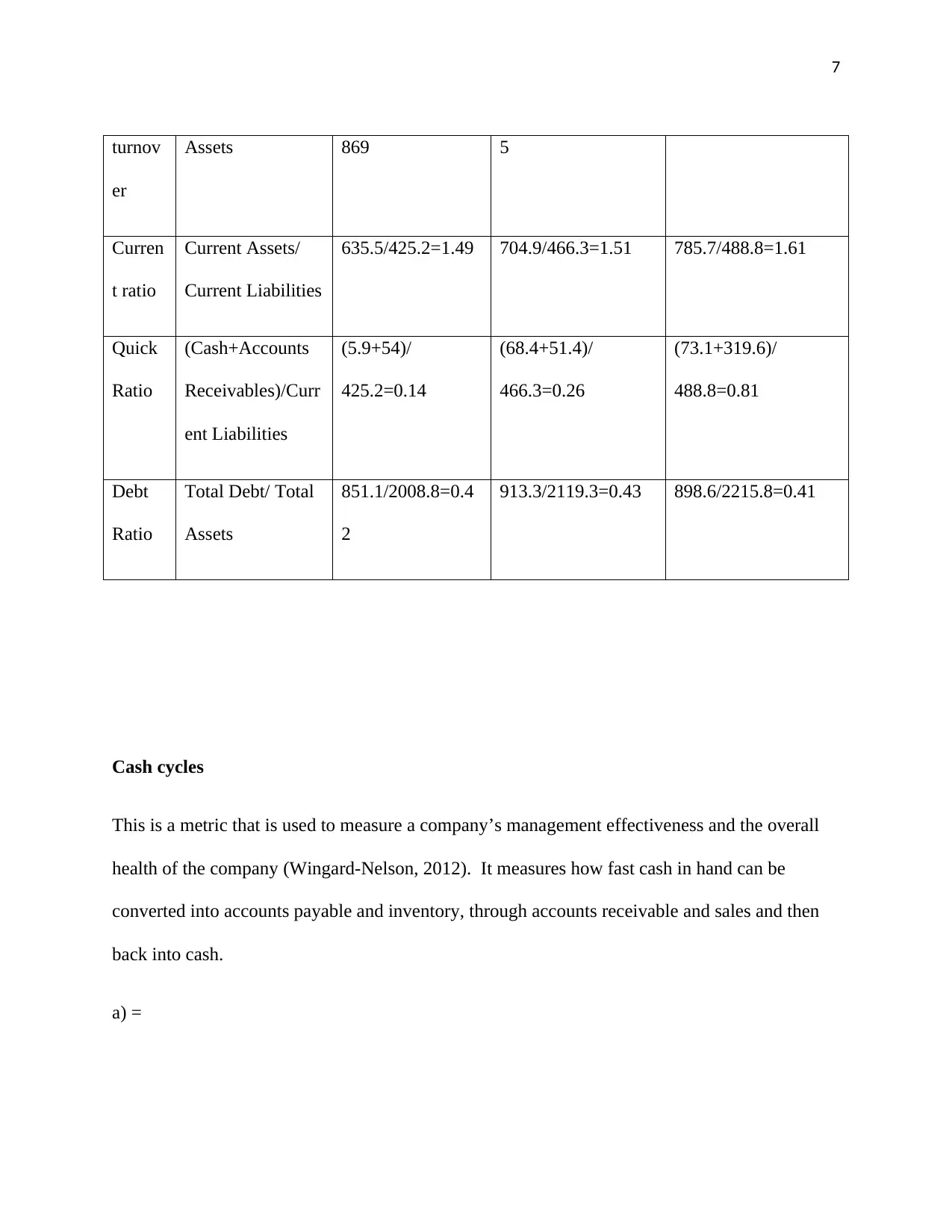

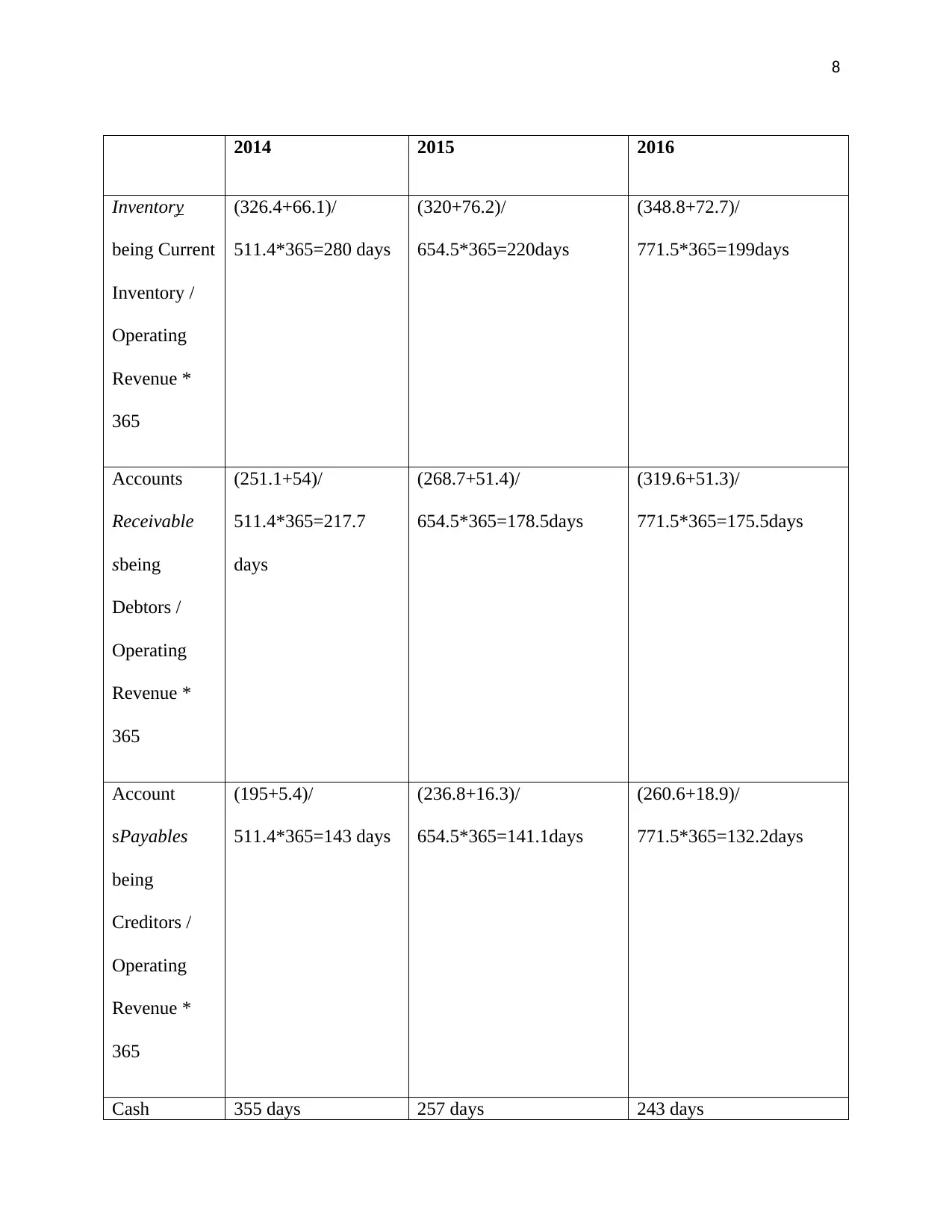

This report presents a financial ratio analysis of Boral Limited and CSR Limited, two companies in the building and construction industry. The analysis covers several years, calculating and comparing key financial ratios such as net profit margin, asset turnover, current ratio, quick ratio, and debt ratio. The report also includes a cash conversion cycle analysis for both companies, providing insights into their working capital management. Furthermore, the report discusses the need and usefulness of financial ratios, their limitations, and the importance of considering various factors when interpreting them. The findings highlight the financial performance and efficiency of both companies, offering a comparative perspective within the building materials sector. The report utilizes financial statements and industry data to provide a comprehensive understanding of the companies' financial health and operational effectiveness.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.