Financial Ratio Analysis Report for Brown Electronics - Accounting

VerifiedAdded on 2022/08/25

|5

|700

|111

Homework Assignment

AI Summary

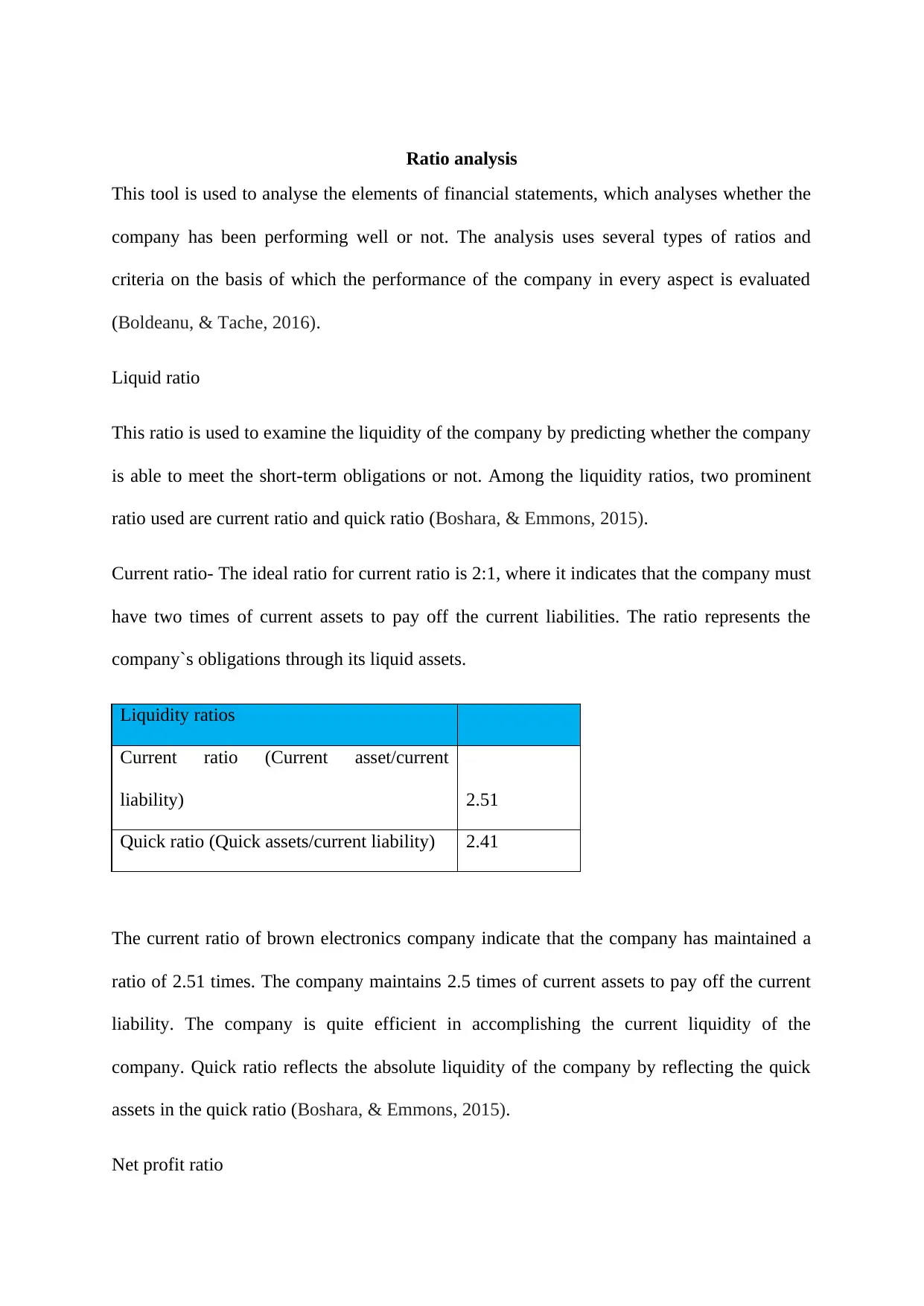

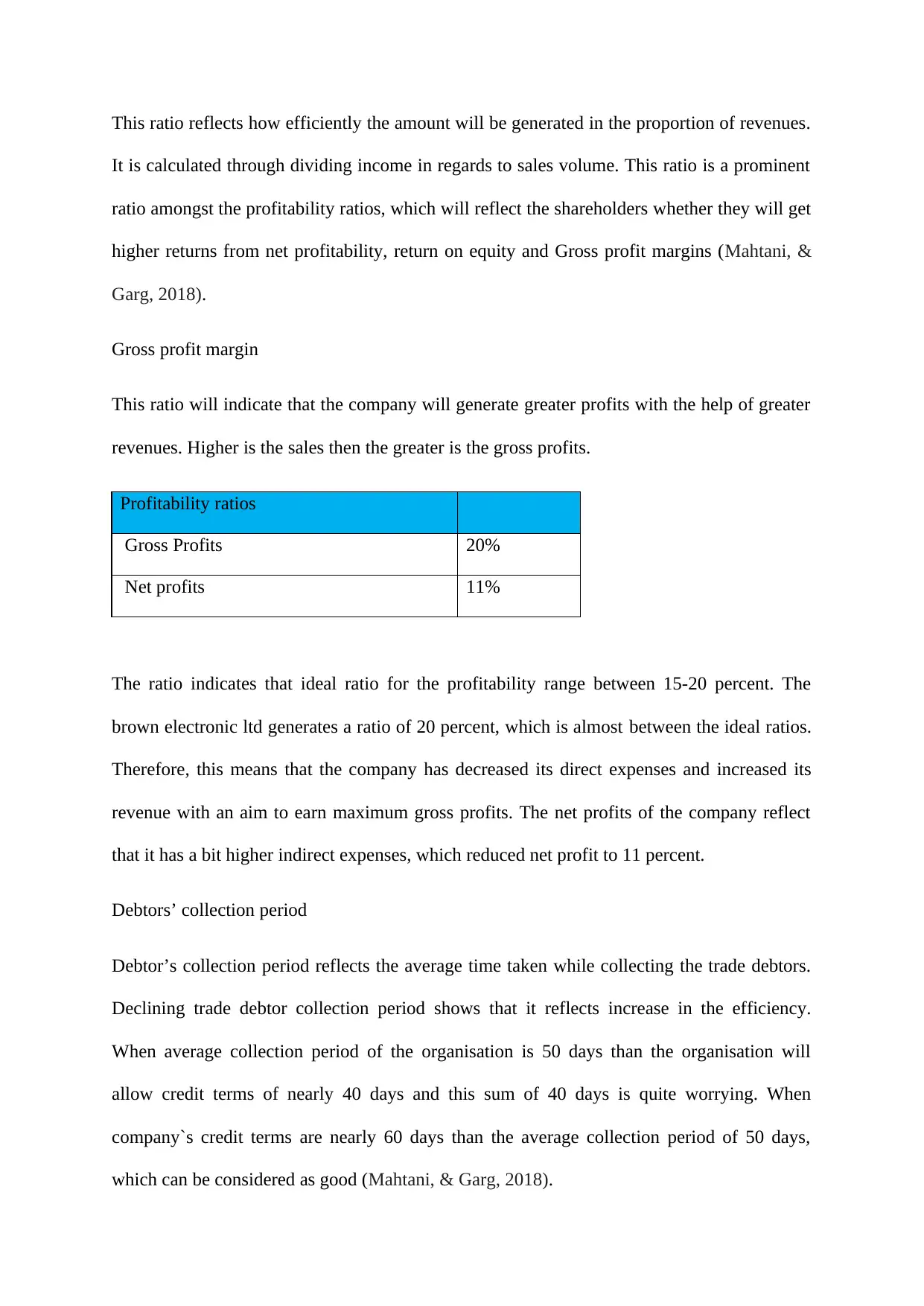

This document presents a comprehensive ratio analysis of Brown Electronics, evaluating the company's financial performance. It begins with an overview of ratio analysis as a tool for assessing financial statements, explaining the use of various ratios to determine a company's performance. The analysis includes the calculation and interpretation of liquidity ratios such as the current and quick ratios, assessing the company's ability to meet short-term obligations. Profitability ratios, including gross profit margin and net profit, are also examined to evaluate the efficiency of revenue generation. Additionally, the document discusses the debtors' collection period, providing insights into the efficiency of collecting trade debtors. The provided solution references key financial concepts and relevant literature, demonstrating a strong understanding of financial analysis techniques. The assignment also includes an incomplete records problem where transactions are recorded in relevant books.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.