Business Research: Financial Ratio Analysis of Two Companies

VerifiedAdded on 2020/02/03

|11

|1795

|56

Report

AI Summary

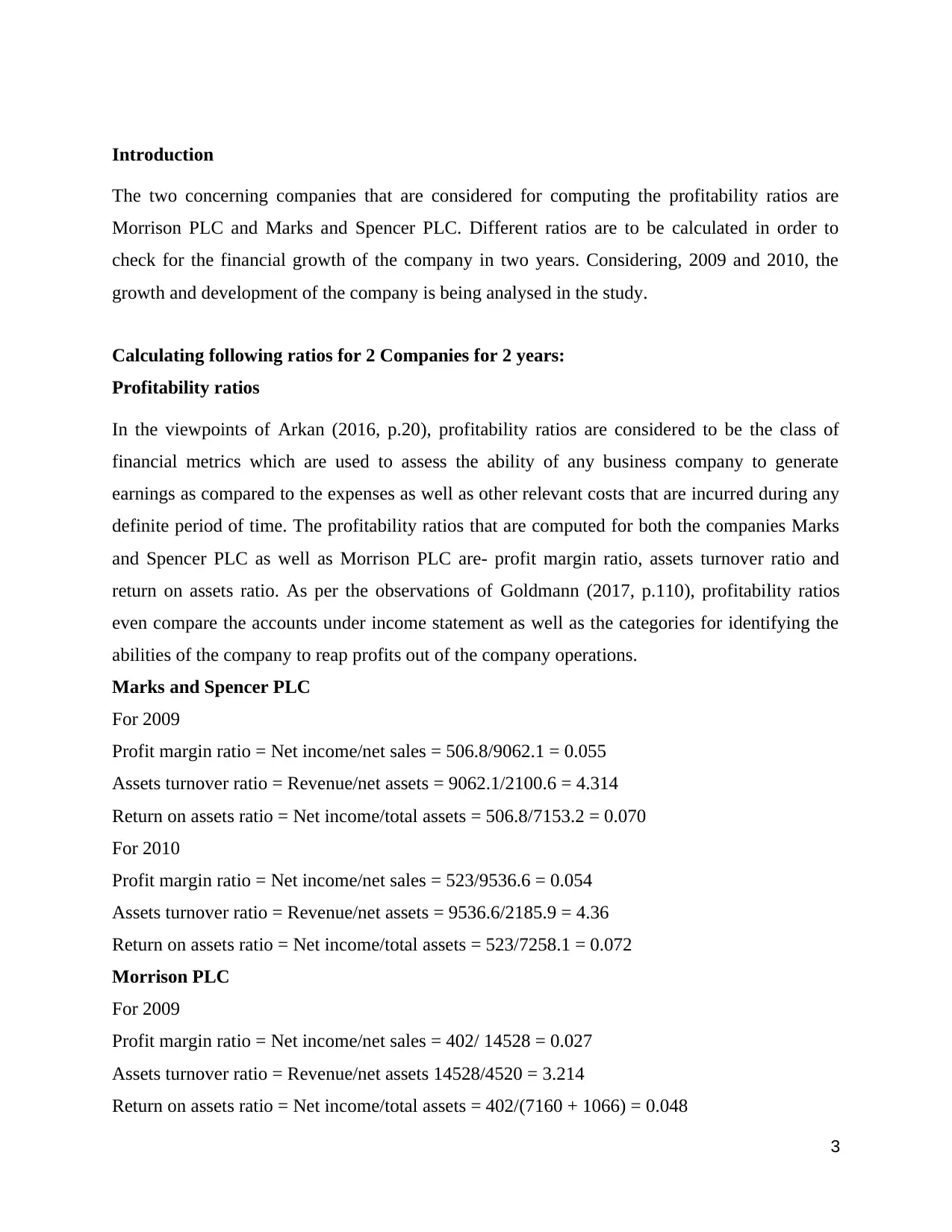

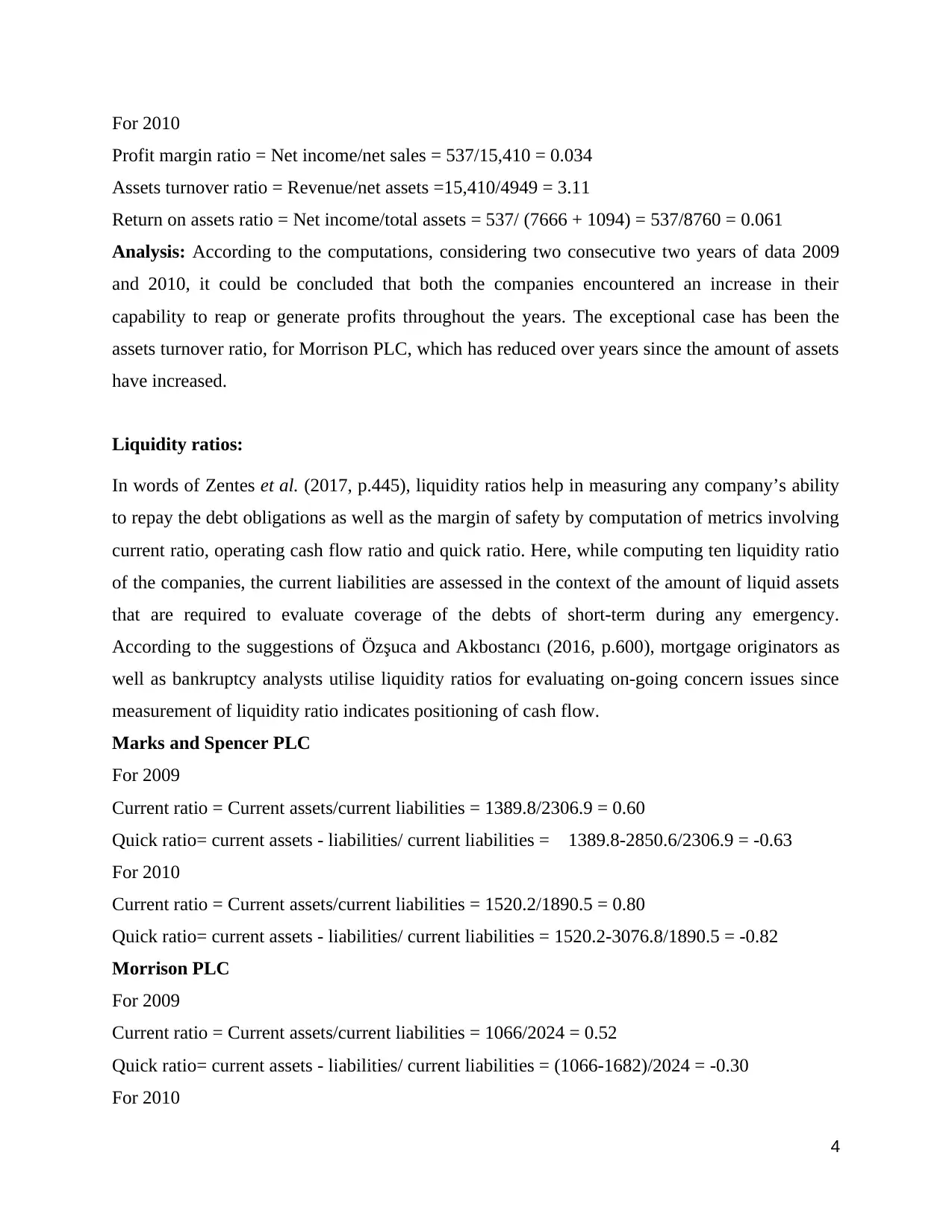

This report presents a financial ratio analysis of Morrison PLC and Marks & Spencer PLC, focusing on their performance between 2009 and 2010. The analysis encompasses profitability ratios (profit margin, asset turnover, return on assets), liquidity ratios (current and quick ratios), and working capital ratios. The report calculates these ratios, interprets the results, and discusses the companies' financial health and efficiency. Additionally, the report includes an examination of cash flow statements for both companies, providing a comprehensive overview of their financial positions and trends. The findings indicate changes in profitability, liquidity, and working capital management over the specified period, offering insights into each company's financial strategies and overall market performance.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.