Financial Ratio Analysis Report: Liquidity, Stability, and Performance

VerifiedAdded on 2021/02/05

|12

|5485

|52

Report

AI Summary

This report provides a comprehensive analysis of financial ratios, crucial for assessing a business's financial health and performance. Task 1 focuses on financial ratios, explaining their significance for various stakeholders such as management, competitors, and investors. It covers key financial statements like the balance sheet, cash flow statement, and profit and loss account, highlighting the importance of liquidity, inventory management, and the distinction between current and non-current assets. The report also discusses wealth monitoring using ratios and the application of spreadsheets in financial analysis. Task 2 delves into financial stability and performance, particularly liquidity ratios. It differentiates between structural and operational liquidity and explains the use of current and quick ratios in assessing a company's ability to meet short-term obligations. The report offers insights into how these ratios are calculated and interpreted, providing a valuable resource for understanding financial statements and making informed business decisions.

Task 1 – Financial ratios

SUMMARY MEMO

Financial statements are used by a business and other interested party outside the

business, as the basis for accurate decision making, planning, and controlling

purposes, parties outside the business can use them to assess competition and

investment potentials. The financial statements should also be laid out in a format

that is accessible for all parties to understand and should include every piece of

relevant information that the business has so that the financial statements are

accurate and represent the business in its true form. The users of these financial

statements are as follows:

Business management – they need this information to calculate the profitability,

cash flows and liquidity of the business every month, so they can make decision on

the business and identify the problematic areas of the business.

Competitors – this will allow competition to evaluate the business’ financial position

and condition in the market so they can alter their competitive strategies.

Employees – the statements will give employees an insight into the business

performance so the employee can assess the security of the business and also see

if the business is fairly paying the employees when compared to the financial info.

Customers – this user can look at the financial information to see if the business is

struggling and this can help the customer see if the business will be able to

undertake the customers requests. For example, a customer of a construction firm

can look at the statements and look to see if the business will be able to provide the

goods without running into cash flow problems that could halt the process.

Governments – the government will use the statements as a basis to determine the

business’ taxation, the business must complete the statements honestly with

accurate information or could be accused of ‘window dressing’ the business which

could lead to fraud investigates.

Lenders – banks will look at the information to evaluate how risky the business is

and how likely they are to receive their finance back from the business.

Investors – similar to lenders investors will want to see where and how their

investment will be spent and what is the potential return on those investments.

For all the information in the statements the stakeholders above will use parts of the

information to divide by one another to calculate different results which can be

described as the financial ratios. These ratios help with all sorts of decision making,

and also help eliminate confusion when comparing data in the statements between

different sized businesses. However, the ratios must be used in reference to the

following:

Establishing trends from past years, to provide a standard of comparison

Benchmarking against other businesses in the same industry

SUMMARY MEMO

Financial statements are used by a business and other interested party outside the

business, as the basis for accurate decision making, planning, and controlling

purposes, parties outside the business can use them to assess competition and

investment potentials. The financial statements should also be laid out in a format

that is accessible for all parties to understand and should include every piece of

relevant information that the business has so that the financial statements are

accurate and represent the business in its true form. The users of these financial

statements are as follows:

Business management – they need this information to calculate the profitability,

cash flows and liquidity of the business every month, so they can make decision on

the business and identify the problematic areas of the business.

Competitors – this will allow competition to evaluate the business’ financial position

and condition in the market so they can alter their competitive strategies.

Employees – the statements will give employees an insight into the business

performance so the employee can assess the security of the business and also see

if the business is fairly paying the employees when compared to the financial info.

Customers – this user can look at the financial information to see if the business is

struggling and this can help the customer see if the business will be able to

undertake the customers requests. For example, a customer of a construction firm

can look at the statements and look to see if the business will be able to provide the

goods without running into cash flow problems that could halt the process.

Governments – the government will use the statements as a basis to determine the

business’ taxation, the business must complete the statements honestly with

accurate information or could be accused of ‘window dressing’ the business which

could lead to fraud investigates.

Lenders – banks will look at the information to evaluate how risky the business is

and how likely they are to receive their finance back from the business.

Investors – similar to lenders investors will want to see where and how their

investment will be spent and what is the potential return on those investments.

For all the information in the statements the stakeholders above will use parts of the

information to divide by one another to calculate different results which can be

described as the financial ratios. These ratios help with all sorts of decision making,

and also help eliminate confusion when comparing data in the statements between

different sized businesses. However, the ratios must be used in reference to the

following:

Establishing trends from past years, to provide a standard of comparison

Benchmarking against other businesses in the same industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Comparing with standards assumed to be satisfactory by the interested party, e.g.

the bank

A summary of the key financial statements

1. Balance sheet – this will combine the assets, liabilities (money owed to

creditors) and the equity capital (shareholder invested and what is retained or

reserved to be reinvested back into the business) that the business holds on a

certain date. The balance sheet will also be equal on both sides.

2. Cash flow – this statement is important as it answers the questions mangers

may have about if they have enough cash to fulfil certain projects. It shows the

changes in the balance sheet and breaks it down into the operating, investing,

and financing activities. The cash flow statement will be used to make a cash flow

forecast which comprises the receipts and payments of the business. A business

will always have expenses in their operations and their may be a delay in the

payments they receive from the goods they have sold to the customers e.g. credit

sale, so the business must have a good cash flow forecast to be able to interpret

when the business will be short n cash and how they can overcome this to

prevent the operations slowing down below optimum output.

3. Profit and loss account – this provide information on the operating activities of

the business to include the business’ gross profit after marking sales, the

turnover, and the net profit after deducting the expenses the business incurred.

Gross profit is income – cost and Net profit is gross profit – expenses. The

profit loss account will also consider the depreciation of the fixed assets a

business owns.

Liquidity

This exists when the organisation has a good cash flow or has enough cash to meet

short-term requirements and commitments. Liquidity thus refers to the amount cash

available in relation to the size of its debts which are payable in the near future. A

ratio that is used to monitor the business’ performance in terms of liquidity is the

Current ratio = Current assets / current liabilities, the Quick ratio ( acid test )

can also be used which is Quick ratio = (current assets – inventories) / current

liabilities

Inventory

Another factor in the profit loss account information is the inventory which is the term

used for the value of stock, which is made up of the materials and components the

business has to buy for the product, as well as the finished goods that are currently

unsold. Inventory can be costly for a business to hold and can cause risks such a

health and safety problems and potential damaged goods so a business will always

want to keep its inventory at its optimal capacity. Having too much inventory at any

given time can always cause a business to run into cash flow problems so keep the

optimal levels can be done by using different systems that will calculate trends in the

environment for large demand and a slump in demand allowing a business to make

the bank

A summary of the key financial statements

1. Balance sheet – this will combine the assets, liabilities (money owed to

creditors) and the equity capital (shareholder invested and what is retained or

reserved to be reinvested back into the business) that the business holds on a

certain date. The balance sheet will also be equal on both sides.

2. Cash flow – this statement is important as it answers the questions mangers

may have about if they have enough cash to fulfil certain projects. It shows the

changes in the balance sheet and breaks it down into the operating, investing,

and financing activities. The cash flow statement will be used to make a cash flow

forecast which comprises the receipts and payments of the business. A business

will always have expenses in their operations and their may be a delay in the

payments they receive from the goods they have sold to the customers e.g. credit

sale, so the business must have a good cash flow forecast to be able to interpret

when the business will be short n cash and how they can overcome this to

prevent the operations slowing down below optimum output.

3. Profit and loss account – this provide information on the operating activities of

the business to include the business’ gross profit after marking sales, the

turnover, and the net profit after deducting the expenses the business incurred.

Gross profit is income – cost and Net profit is gross profit – expenses. The

profit loss account will also consider the depreciation of the fixed assets a

business owns.

Liquidity

This exists when the organisation has a good cash flow or has enough cash to meet

short-term requirements and commitments. Liquidity thus refers to the amount cash

available in relation to the size of its debts which are payable in the near future. A

ratio that is used to monitor the business’ performance in terms of liquidity is the

Current ratio = Current assets / current liabilities, the Quick ratio ( acid test )

can also be used which is Quick ratio = (current assets – inventories) / current

liabilities

Inventory

Another factor in the profit loss account information is the inventory which is the term

used for the value of stock, which is made up of the materials and components the

business has to buy for the product, as well as the finished goods that are currently

unsold. Inventory can be costly for a business to hold and can cause risks such a

health and safety problems and potential damaged goods so a business will always

want to keep its inventory at its optimal capacity. Having too much inventory at any

given time can always cause a business to run into cash flow problems so keep the

optimal levels can be done by using different systems that will calculate trends in the

environment for large demand and a slump in demand allowing a business to make

its decisions based on these findings. The ratio that will help with this is called the

Inventory Turnover Ratio = Cost of goods sold / Average inventory

Non-current assets and current assets

The non-current assets (fixed assets) are the long-term assets that a business owns

which would include things like the building the business has, the equipment they

use in their operations and the land they own. Whereas the current assets include

anything the business has that can be converted into cash relatively quickly such as

the raw materials the business has, the inventory of finished products, and accounts

receivables etc. Cash can also be classified as a current asset. The business must

also evaluate the total liabilities of the business which are anything the business

owes to different parties such as, electricity bills, bank loan repayments, salaries,

accounts payable and income taxes. A ratio to assist a business to evaluate the

business’ performance with reference to liabilities and assets would be the:

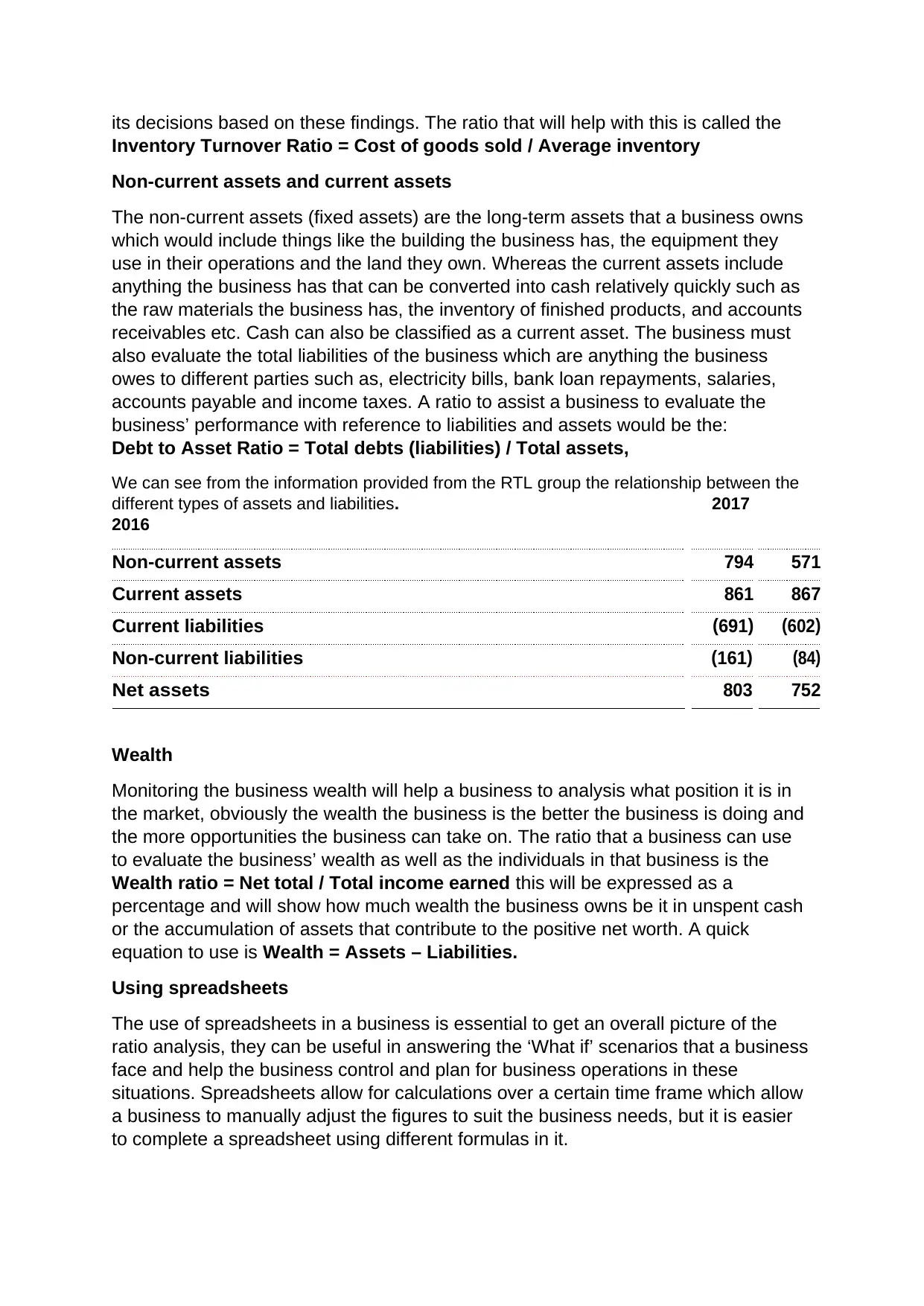

Debt to Asset Ratio = Total debts (liabilities) / Total assets,

We can see from the information provided from the RTL group the relationship between the

different types of assets and liabilities. 2017

2016

Non-current assets 794 571

Current assets 861 867

Current liabilities (691) (602)

Non-current liabilities (161) (84)

Net assets 803 752

Wealth

Monitoring the business wealth will help a business to analysis what position it is in

the market, obviously the wealth the business is the better the business is doing and

the more opportunities the business can take on. The ratio that a business can use

to evaluate the business’ wealth as well as the individuals in that business is the

Wealth ratio = Net total / Total income earned this will be expressed as a

percentage and will show how much wealth the business owns be it in unspent cash

or the accumulation of assets that contribute to the positive net worth. A quick

equation to use is Wealth = Assets – Liabilities.

Using spreadsheets

The use of spreadsheets in a business is essential to get an overall picture of the

ratio analysis, they can be useful in answering the ‘What if’ scenarios that a business

face and help the business control and plan for business operations in these

situations. Spreadsheets allow for calculations over a certain time frame which allow

a business to manually adjust the figures to suit the business needs, but it is easier

to complete a spreadsheet using different formulas in it.

Inventory Turnover Ratio = Cost of goods sold / Average inventory

Non-current assets and current assets

The non-current assets (fixed assets) are the long-term assets that a business owns

which would include things like the building the business has, the equipment they

use in their operations and the land they own. Whereas the current assets include

anything the business has that can be converted into cash relatively quickly such as

the raw materials the business has, the inventory of finished products, and accounts

receivables etc. Cash can also be classified as a current asset. The business must

also evaluate the total liabilities of the business which are anything the business

owes to different parties such as, electricity bills, bank loan repayments, salaries,

accounts payable and income taxes. A ratio to assist a business to evaluate the

business’ performance with reference to liabilities and assets would be the:

Debt to Asset Ratio = Total debts (liabilities) / Total assets,

We can see from the information provided from the RTL group the relationship between the

different types of assets and liabilities. 2017

2016

Non-current assets 794 571

Current assets 861 867

Current liabilities (691) (602)

Non-current liabilities (161) (84)

Net assets 803 752

Wealth

Monitoring the business wealth will help a business to analysis what position it is in

the market, obviously the wealth the business is the better the business is doing and

the more opportunities the business can take on. The ratio that a business can use

to evaluate the business’ wealth as well as the individuals in that business is the

Wealth ratio = Net total / Total income earned this will be expressed as a

percentage and will show how much wealth the business owns be it in unspent cash

or the accumulation of assets that contribute to the positive net worth. A quick

equation to use is Wealth = Assets – Liabilities.

Using spreadsheets

The use of spreadsheets in a business is essential to get an overall picture of the

ratio analysis, they can be useful in answering the ‘What if’ scenarios that a business

face and help the business control and plan for business operations in these

situations. Spreadsheets allow for calculations over a certain time frame which allow

a business to manually adjust the figures to suit the business needs, but it is easier

to complete a spreadsheet using different formulas in it.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ratio Analysis

In general ratio analysis is used as a quantitative method to gain an insight into the

business’ operational efficiency, its liquidity, and its profitability by management

studying and analysis the financial statements previously discussed. Ratio analysis

is used to identity the business performance with the following:

Ratio analysis will compare the line-item data in the business financial accounts

and reveal to the management of the business insights on liquidity, profitability,

solvency, and efficiency.

The analysis will evaluate how the business is performing over a specific time

period and can use this information to compare it with businesses in the same

industry.

Ratios will offer insights but when paired with other metrics they will allow a

business to see a much broader picture of the business financial position, health,

and performance.

Classifying ratios

Financial ratios can be classified into a variety of groups:

Gearing – indicates how stable the business is in the long term

Capital structure – relates to the composition and relationship which exists

between the equity (i.e. the ordinary share capital plus reserves) and the other

long-term sources of finance (i.e. preference shares, debentures, and fixed term

loans)

The main themes within the business that the ratios identity as previously discussed

are the following:

Liquidity and Working Capital

Solvency and Gearing

Profitability

Each of these will be discussed in greater detail in the next section of this report.

Financial management and the accountants of a business will use this range of

ratios to interpret the financial performance that the business is in. Management

however must understand how each ratio is calculated and what each ratio means

so that they can assess the values found in the analysis and predict any changes in

the business which they can then implement changes in the business to counter act

adverse impacts the business is facing.

In general ratio analysis is used as a quantitative method to gain an insight into the

business’ operational efficiency, its liquidity, and its profitability by management

studying and analysis the financial statements previously discussed. Ratio analysis

is used to identity the business performance with the following:

Ratio analysis will compare the line-item data in the business financial accounts

and reveal to the management of the business insights on liquidity, profitability,

solvency, and efficiency.

The analysis will evaluate how the business is performing over a specific time

period and can use this information to compare it with businesses in the same

industry.

Ratios will offer insights but when paired with other metrics they will allow a

business to see a much broader picture of the business financial position, health,

and performance.

Classifying ratios

Financial ratios can be classified into a variety of groups:

Gearing – indicates how stable the business is in the long term

Capital structure – relates to the composition and relationship which exists

between the equity (i.e. the ordinary share capital plus reserves) and the other

long-term sources of finance (i.e. preference shares, debentures, and fixed term

loans)

The main themes within the business that the ratios identity as previously discussed

are the following:

Liquidity and Working Capital

Solvency and Gearing

Profitability

Each of these will be discussed in greater detail in the next section of this report.

Financial management and the accountants of a business will use this range of

ratios to interpret the financial performance that the business is in. Management

however must understand how each ratio is calculated and what each ratio means

so that they can assess the values found in the analysis and predict any changes in

the business which they can then implement changes in the business to counter act

adverse impacts the business is facing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

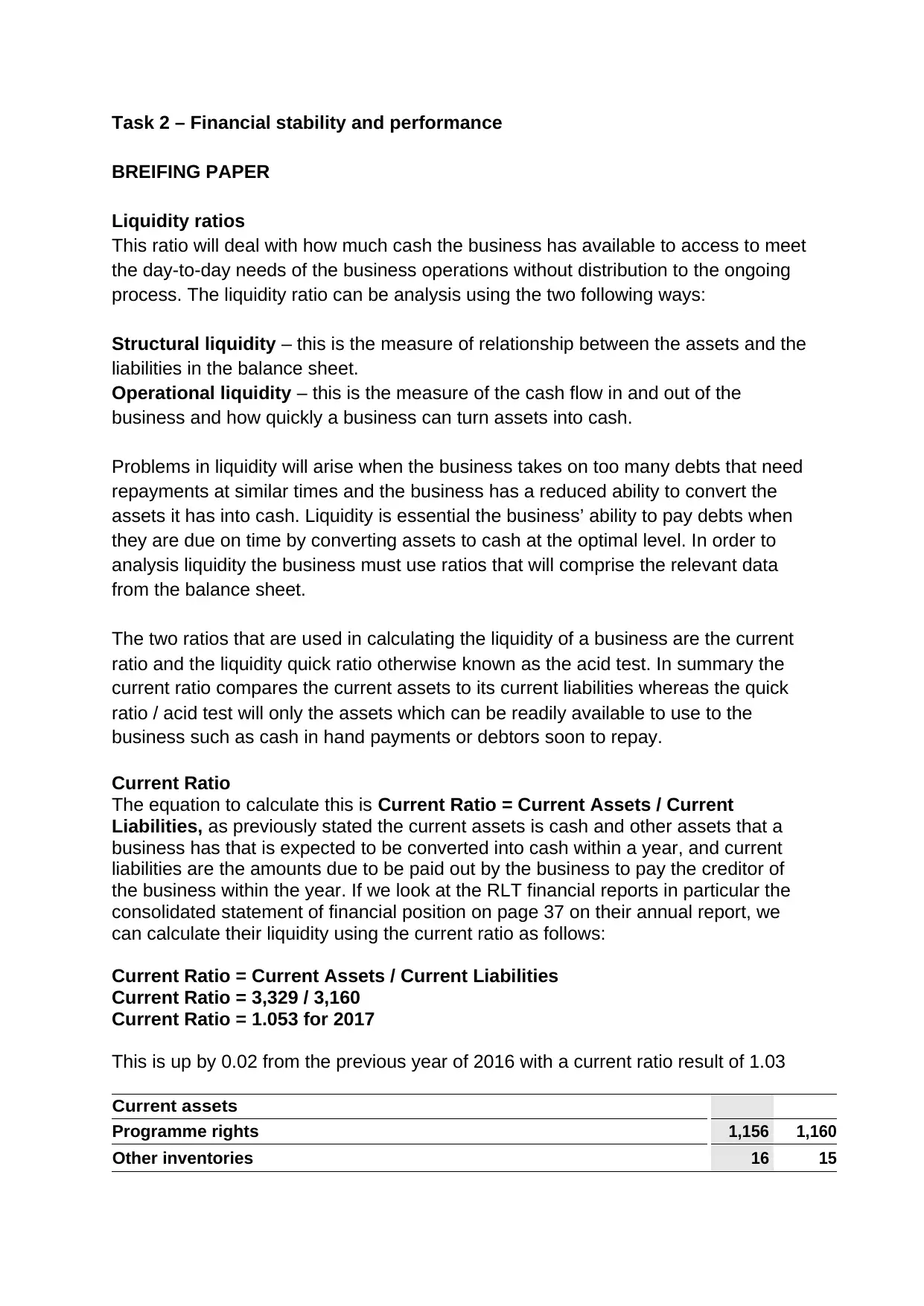

Task 2 – Financial stability and performance

BREIFING PAPER

Liquidity ratios

This ratio will deal with how much cash the business has available to access to meet

the day-to-day needs of the business operations without distribution to the ongoing

process. The liquidity ratio can be analysis using the two following ways:

Structural liquidity – this is the measure of relationship between the assets and the

liabilities in the balance sheet.

Operational liquidity – this is the measure of the cash flow in and out of the

business and how quickly a business can turn assets into cash.

Problems in liquidity will arise when the business takes on too many debts that need

repayments at similar times and the business has a reduced ability to convert the

assets it has into cash. Liquidity is essential the business’ ability to pay debts when

they are due on time by converting assets to cash at the optimal level. In order to

analysis liquidity the business must use ratios that will comprise the relevant data

from the balance sheet.

The two ratios that are used in calculating the liquidity of a business are the current

ratio and the liquidity quick ratio otherwise known as the acid test. In summary the

current ratio compares the current assets to its current liabilities whereas the quick

ratio / acid test will only the assets which can be readily available to use to the

business such as cash in hand payments or debtors soon to repay.

Current Ratio

The equation to calculate this is Current Ratio = Current Assets / Current

Liabilities, as previously stated the current assets is cash and other assets that a

business has that is expected to be converted into cash within a year, and current

liabilities are the amounts due to be paid out by the business to pay the creditor of

the business within the year. If we look at the RLT financial reports in particular the

consolidated statement of financial position on page 37 on their annual report, we

can calculate their liquidity using the current ratio as follows:

Current Ratio = Current Assets / Current Liabilities

Current Ratio = 3,329 / 3,160

Current Ratio = 1.053 for 2017

This is up by 0.02 from the previous year of 2016 with a current ratio result of 1.03

Current assets

Programme rights . 1,156 1,160

Other inventories 16 15

BREIFING PAPER

Liquidity ratios

This ratio will deal with how much cash the business has available to access to meet

the day-to-day needs of the business operations without distribution to the ongoing

process. The liquidity ratio can be analysis using the two following ways:

Structural liquidity – this is the measure of relationship between the assets and the

liabilities in the balance sheet.

Operational liquidity – this is the measure of the cash flow in and out of the

business and how quickly a business can turn assets into cash.

Problems in liquidity will arise when the business takes on too many debts that need

repayments at similar times and the business has a reduced ability to convert the

assets it has into cash. Liquidity is essential the business’ ability to pay debts when

they are due on time by converting assets to cash at the optimal level. In order to

analysis liquidity the business must use ratios that will comprise the relevant data

from the balance sheet.

The two ratios that are used in calculating the liquidity of a business are the current

ratio and the liquidity quick ratio otherwise known as the acid test. In summary the

current ratio compares the current assets to its current liabilities whereas the quick

ratio / acid test will only the assets which can be readily available to use to the

business such as cash in hand payments or debtors soon to repay.

Current Ratio

The equation to calculate this is Current Ratio = Current Assets / Current

Liabilities, as previously stated the current assets is cash and other assets that a

business has that is expected to be converted into cash within a year, and current

liabilities are the amounts due to be paid out by the business to pay the creditor of

the business within the year. If we look at the RLT financial reports in particular the

consolidated statement of financial position on page 37 on their annual report, we

can calculate their liquidity using the current ratio as follows:

Current Ratio = Current Assets / Current Liabilities

Current Ratio = 3,329 / 3,160

Current Ratio = 1.053 for 2017

This is up by 0.02 from the previous year of 2016 with a current ratio result of 1.03

Current assets

Programme rights . 1,156 1,160

Other inventories 16 15

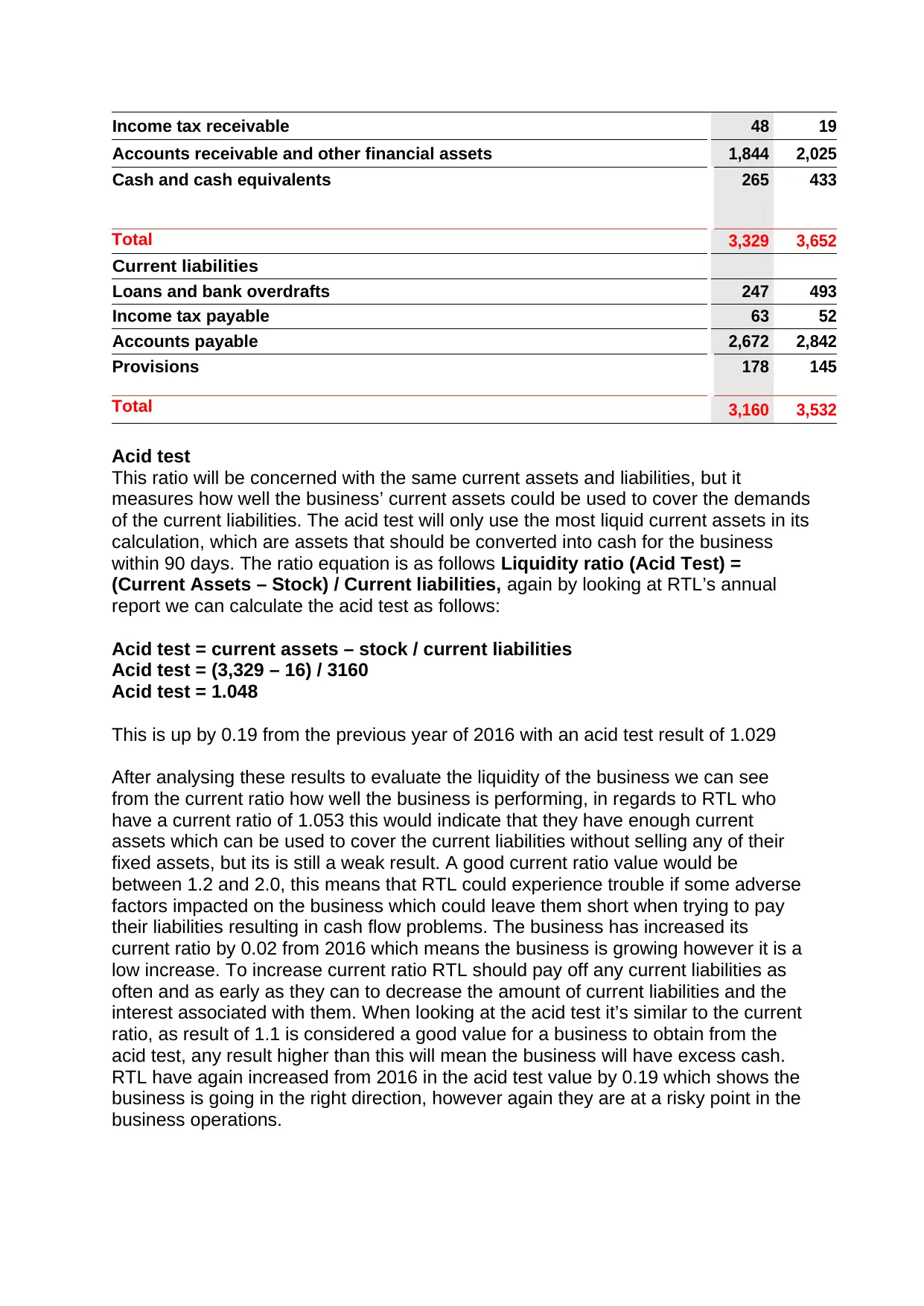

Income tax receivable 48 19

Accounts receivable and other financial assets . 1,844 2,025

Cash and cash equivalents

.

265 433

Total 3,329 3,652

Current liabilities

Loans and bank overdrafts . 247 493

Income tax payable 63 52

Accounts payable . 2,672 2,842

Provisions 178 145

Total 3,160 3,532

Acid test

This ratio will be concerned with the same current assets and liabilities, but it

measures how well the business’ current assets could be used to cover the demands

of the current liabilities. The acid test will only use the most liquid current assets in its

calculation, which are assets that should be converted into cash for the business

within 90 days. The ratio equation is as follows Liquidity ratio (Acid Test) =

(Current Assets – Stock) / Current liabilities, again by looking at RTL’s annual

report we can calculate the acid test as follows:

Acid test = current assets – stock / current liabilities

Acid test = (3,329 – 16) / 3160

Acid test = 1.048

This is up by 0.19 from the previous year of 2016 with an acid test result of 1.029

After analysing these results to evaluate the liquidity of the business we can see

from the current ratio how well the business is performing, in regards to RTL who

have a current ratio of 1.053 this would indicate that they have enough current

assets which can be used to cover the current liabilities without selling any of their

fixed assets, but its is still a weak result. A good current ratio value would be

between 1.2 and 2.0, this means that RTL could experience trouble if some adverse

factors impacted on the business which could leave them short when trying to pay

their liabilities resulting in cash flow problems. The business has increased its

current ratio by 0.02 from 2016 which means the business is growing however it is a

low increase. To increase current ratio RTL should pay off any current liabilities as

often and as early as they can to decrease the amount of current liabilities and the

interest associated with them. When looking at the acid test it’s similar to the current

ratio, as result of 1.1 is considered a good value for a business to obtain from the

acid test, any result higher than this will mean the business will have excess cash.

RTL have again increased from 2016 in the acid test value by 0.19 which shows the

business is going in the right direction, however again they are at a risky point in the

business operations.

Accounts receivable and other financial assets . 1,844 2,025

Cash and cash equivalents

.

265 433

Total 3,329 3,652

Current liabilities

Loans and bank overdrafts . 247 493

Income tax payable 63 52

Accounts payable . 2,672 2,842

Provisions 178 145

Total 3,160 3,532

Acid test

This ratio will be concerned with the same current assets and liabilities, but it

measures how well the business’ current assets could be used to cover the demands

of the current liabilities. The acid test will only use the most liquid current assets in its

calculation, which are assets that should be converted into cash for the business

within 90 days. The ratio equation is as follows Liquidity ratio (Acid Test) =

(Current Assets – Stock) / Current liabilities, again by looking at RTL’s annual

report we can calculate the acid test as follows:

Acid test = current assets – stock / current liabilities

Acid test = (3,329 – 16) / 3160

Acid test = 1.048

This is up by 0.19 from the previous year of 2016 with an acid test result of 1.029

After analysing these results to evaluate the liquidity of the business we can see

from the current ratio how well the business is performing, in regards to RTL who

have a current ratio of 1.053 this would indicate that they have enough current

assets which can be used to cover the current liabilities without selling any of their

fixed assets, but its is still a weak result. A good current ratio value would be

between 1.2 and 2.0, this means that RTL could experience trouble if some adverse

factors impacted on the business which could leave them short when trying to pay

their liabilities resulting in cash flow problems. The business has increased its

current ratio by 0.02 from 2016 which means the business is growing however it is a

low increase. To increase current ratio RTL should pay off any current liabilities as

often and as early as they can to decrease the amount of current liabilities and the

interest associated with them. When looking at the acid test it’s similar to the current

ratio, as result of 1.1 is considered a good value for a business to obtain from the

acid test, any result higher than this will mean the business will have excess cash.

RTL have again increased from 2016 in the acid test value by 0.19 which shows the

business is going in the right direction, however again they are at a risky point in the

business operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As discussed, if a business like RTL has a low liquidity then they may be able to

raise it by the following:

Paying some debts

Increasing your current assets from loans or other borrowings with a maturity of

more than one year

Converting non-current assets into current assets

Increasing your current assets from new equity contributions

Putting profits back into the business

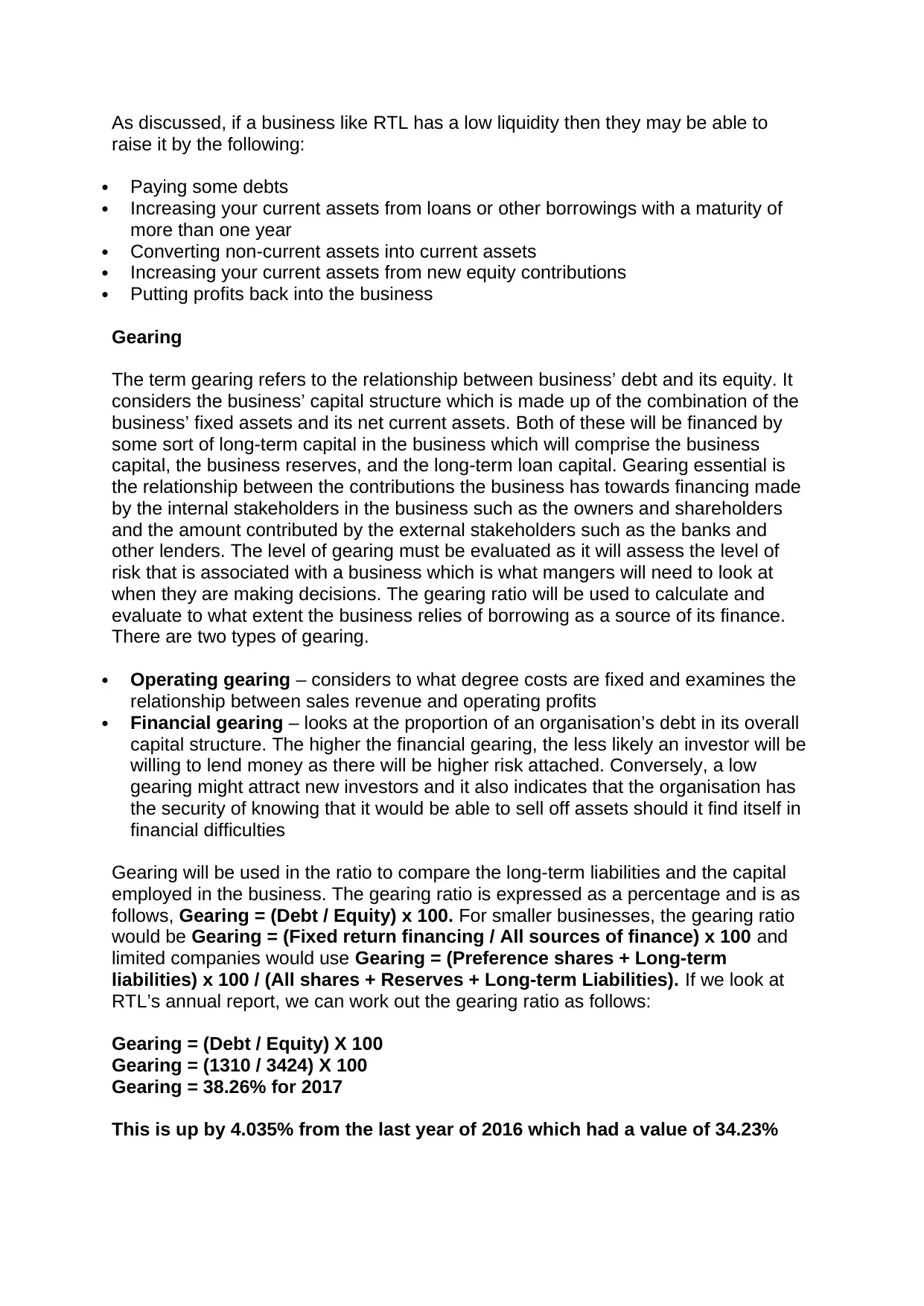

Gearing

The term gearing refers to the relationship between business’ debt and its equity. It

considers the business’ capital structure which is made up of the combination of the

business’ fixed assets and its net current assets. Both of these will be financed by

some sort of long-term capital in the business which will comprise the business

capital, the business reserves, and the long-term loan capital. Gearing essential is

the relationship between the contributions the business has towards financing made

by the internal stakeholders in the business such as the owners and shareholders

and the amount contributed by the external stakeholders such as the banks and

other lenders. The level of gearing must be evaluated as it will assess the level of

risk that is associated with a business which is what mangers will need to look at

when they are making decisions. The gearing ratio will be used to calculate and

evaluate to what extent the business relies of borrowing as a source of its finance.

There are two types of gearing.

Operating gearing – considers to what degree costs are fixed and examines the

relationship between sales revenue and operating profits

Financial gearing – looks at the proportion of an organisation’s debt in its overall

capital structure. The higher the financial gearing, the less likely an investor will be

willing to lend money as there will be higher risk attached. Conversely, a low

gearing might attract new investors and it also indicates that the organisation has

the security of knowing that it would be able to sell off assets should it find itself in

financial difficulties

Gearing will be used in the ratio to compare the long-term liabilities and the capital

employed in the business. The gearing ratio is expressed as a percentage and is as

follows, Gearing = (Debt / Equity) x 100. For smaller businesses, the gearing ratio

would be Gearing = (Fixed return financing / All sources of finance) x 100 and

limited companies would use Gearing = (Preference shares + Long-term

liabilities) x 100 / (All shares + Reserves + Long-term Liabilities). If we look at

RTL’s annual report, we can work out the gearing ratio as follows:

Gearing = (Debt / Equity) X 100

Gearing = (1310 / 3424) X 100

Gearing = 38.26% for 2017

This is up by 4.035% from the last year of 2016 which had a value of 34.23%

raise it by the following:

Paying some debts

Increasing your current assets from loans or other borrowings with a maturity of

more than one year

Converting non-current assets into current assets

Increasing your current assets from new equity contributions

Putting profits back into the business

Gearing

The term gearing refers to the relationship between business’ debt and its equity. It

considers the business’ capital structure which is made up of the combination of the

business’ fixed assets and its net current assets. Both of these will be financed by

some sort of long-term capital in the business which will comprise the business

capital, the business reserves, and the long-term loan capital. Gearing essential is

the relationship between the contributions the business has towards financing made

by the internal stakeholders in the business such as the owners and shareholders

and the amount contributed by the external stakeholders such as the banks and

other lenders. The level of gearing must be evaluated as it will assess the level of

risk that is associated with a business which is what mangers will need to look at

when they are making decisions. The gearing ratio will be used to calculate and

evaluate to what extent the business relies of borrowing as a source of its finance.

There are two types of gearing.

Operating gearing – considers to what degree costs are fixed and examines the

relationship between sales revenue and operating profits

Financial gearing – looks at the proportion of an organisation’s debt in its overall

capital structure. The higher the financial gearing, the less likely an investor will be

willing to lend money as there will be higher risk attached. Conversely, a low

gearing might attract new investors and it also indicates that the organisation has

the security of knowing that it would be able to sell off assets should it find itself in

financial difficulties

Gearing will be used in the ratio to compare the long-term liabilities and the capital

employed in the business. The gearing ratio is expressed as a percentage and is as

follows, Gearing = (Debt / Equity) x 100. For smaller businesses, the gearing ratio

would be Gearing = (Fixed return financing / All sources of finance) x 100 and

limited companies would use Gearing = (Preference shares + Long-term

liabilities) x 100 / (All shares + Reserves + Long-term Liabilities). If we look at

RTL’s annual report, we can work out the gearing ratio as follows:

Gearing = (Debt / Equity) X 100

Gearing = (1310 / 3424) X 100

Gearing = 38.26% for 2017

This is up by 4.035% from the last year of 2016 which had a value of 34.23%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Non-current liabilities

Loans 568 517

Accounts payable . 475 405

Provisions . 242 249

Deferred tax liabilities

.

25 45

Total Debt 1,310 1,216

Equity

Equity attributable to RTL Group shareholders 2,957 3,077

Equity attributable to non-controlling interests 467 475

Total Equity 3,424 3,552

By analysing these results, we can see that RTL are in a strong gearing position as

the optimal gearing ratio is around 25% - 50%, which means the business has a

good balance of equity and debts meaning they will be able to operate at full

capacity without the risk of being having to slow down or halt operations due to cash

flow problems. This gearing value will allow RTL to obtain finance easier from

lenders as they can present themselves as a low risk investment, this also means

lenders will offer them lower interest rates and more favourable terms and

conditions. However, RTL have increased their gearing ratio by 4.035% since 2016

which is a significant jump which means RTL having had a higher degree of financial

leverage in 2017 which could mean they are now more susceptible to downturns in

the business cycle and economy. In general the higher the gearing the more debt the

business is in which means the business will be a high risk investment to investors

and the lower the gearing ratio is the lower debt the business is and the more

likelihood that the business will be able to settle their debts meaning it’s a lower risk

to the investor.

Solvency

This is the measure of all the capital borrowed and utilised by a business compared

the amount of the owners’ equity capital invested, the solvency therefore gives

measurements relating to how able to business is at paying all its debts if all the

assets of that business were sold. Solvency calculations provide information about

what would happen if all the assets were sold and converted into cash and all

liabilities were paid. Thus, solvency and liquidity consider the stability of the

business on both a short-term and long-term basis. The fundamental measure of

solvency is owner equity, which uses the market value of assets and deducts

liabilities and any other payments due, such as deferred taxes. Like working capital,

the adequacy of owner equity depends on the size of the business and so

comparisons are made through the use of ratios. Solvency differs from liquidity in

that it is concerned with long-term, as well as short-term, assets and liabilities. One

of the solvency ratios used for in business is as follows Solvency = Net profit +

Depreciation / All liabilities x100. After looking are RTL’s financial statement we

Loans 568 517

Accounts payable . 475 405

Provisions . 242 249

Deferred tax liabilities

.

25 45

Total Debt 1,310 1,216

Equity

Equity attributable to RTL Group shareholders 2,957 3,077

Equity attributable to non-controlling interests 467 475

Total Equity 3,424 3,552

By analysing these results, we can see that RTL are in a strong gearing position as

the optimal gearing ratio is around 25% - 50%, which means the business has a

good balance of equity and debts meaning they will be able to operate at full

capacity without the risk of being having to slow down or halt operations due to cash

flow problems. This gearing value will allow RTL to obtain finance easier from

lenders as they can present themselves as a low risk investment, this also means

lenders will offer them lower interest rates and more favourable terms and

conditions. However, RTL have increased their gearing ratio by 4.035% since 2016

which is a significant jump which means RTL having had a higher degree of financial

leverage in 2017 which could mean they are now more susceptible to downturns in

the business cycle and economy. In general the higher the gearing the more debt the

business is in which means the business will be a high risk investment to investors

and the lower the gearing ratio is the lower debt the business is and the more

likelihood that the business will be able to settle their debts meaning it’s a lower risk

to the investor.

Solvency

This is the measure of all the capital borrowed and utilised by a business compared

the amount of the owners’ equity capital invested, the solvency therefore gives

measurements relating to how able to business is at paying all its debts if all the

assets of that business were sold. Solvency calculations provide information about

what would happen if all the assets were sold and converted into cash and all

liabilities were paid. Thus, solvency and liquidity consider the stability of the

business on both a short-term and long-term basis. The fundamental measure of

solvency is owner equity, which uses the market value of assets and deducts

liabilities and any other payments due, such as deferred taxes. Like working capital,

the adequacy of owner equity depends on the size of the business and so

comparisons are made through the use of ratios. Solvency differs from liquidity in

that it is concerned with long-term, as well as short-term, assets and liabilities. One

of the solvency ratios used for in business is as follows Solvency = Net profit +

Depreciation / All liabilities x100. After looking are RTL’s financial statement we

can see that the net profit for the year was £837(m) and the depreciation was

valued at £230(m) and total current liabilities were £3160(m) and non-current

liabilities were £1310(m) so we can work out the solvency as follows:

Solvency = Net profit + Depreciation / All liabilities x100

Solvency = 837 + 230 (1067) / 3160 + 1310 (4470)

Solvency = 0.24 or 24% for 2017

For 2016 it is as follows:

Solvency =816 + 218 / 3532 + 1216

Solvency = 0.21 or 21%

After looking at this value we can see that RTL is in an acceptable solvency position,

a good solvency will range from anything higher than 20%, this means the that RTL

is in a healthy financial position as it means the business can repay all its debts. RTL

has had a significant favourable increase in solvency of 3% which has out them in a

healthy position. To increase this figure even further RTL could undertake various

activities such as:

Increase sales – building on sales and marketing will drastically increase

revenue in the long-term meaning kore cash will flow into the business which can

help pay debts.

Increase profitability – if revenue is high but profit is low this can impact on the

solvency of the business adversely, so building on the profit margin by increasing

prices or buying in bulk will help keep costs of operations low and profit margin

high.

Increase owner equity – the owners of the business can invest their own cash

into the business to boost the solvency but using shareholders and investors as a

source of finance will mean there is much more cash readily available which will

help the business from falling short on its debts.

Sell some assets – assets that are not central to the business operations can be

sold off which will help raise cash. If the business sells financed assets this will

increase the cash and decrease the liabilities in one.

In general, when we refer to liquidity and earing the most commonly used ratios for

assessing liquidity and gearing are:

Debt-to-asset ratio – identifies total liabilities as a proportion of total assets. The

higher the value, the greater the exposure to risk for the business

Equity-to-asset ratio – expresses the proportion of total assets financed by the

owners’ equity (percentage ownership)

Debt-to-equity ratio – reflects the capital structure of the business, and the extent

to which debt capital is being combined with equity capital (gearing ratio)

Profitability

This term can be used in business and refers to the relationship between the profit

the business is making and the total assets the business owns. In simple terms a

business with high profits and low total assets would be described as a profitability

business. Making profit is essential in business, higher profits means the business is

wealthier meaning the business will be able to undertake more potential

valued at £230(m) and total current liabilities were £3160(m) and non-current

liabilities were £1310(m) so we can work out the solvency as follows:

Solvency = Net profit + Depreciation / All liabilities x100

Solvency = 837 + 230 (1067) / 3160 + 1310 (4470)

Solvency = 0.24 or 24% for 2017

For 2016 it is as follows:

Solvency =816 + 218 / 3532 + 1216

Solvency = 0.21 or 21%

After looking at this value we can see that RTL is in an acceptable solvency position,

a good solvency will range from anything higher than 20%, this means the that RTL

is in a healthy financial position as it means the business can repay all its debts. RTL

has had a significant favourable increase in solvency of 3% which has out them in a

healthy position. To increase this figure even further RTL could undertake various

activities such as:

Increase sales – building on sales and marketing will drastically increase

revenue in the long-term meaning kore cash will flow into the business which can

help pay debts.

Increase profitability – if revenue is high but profit is low this can impact on the

solvency of the business adversely, so building on the profit margin by increasing

prices or buying in bulk will help keep costs of operations low and profit margin

high.

Increase owner equity – the owners of the business can invest their own cash

into the business to boost the solvency but using shareholders and investors as a

source of finance will mean there is much more cash readily available which will

help the business from falling short on its debts.

Sell some assets – assets that are not central to the business operations can be

sold off which will help raise cash. If the business sells financed assets this will

increase the cash and decrease the liabilities in one.

In general, when we refer to liquidity and earing the most commonly used ratios for

assessing liquidity and gearing are:

Debt-to-asset ratio – identifies total liabilities as a proportion of total assets. The

higher the value, the greater the exposure to risk for the business

Equity-to-asset ratio – expresses the proportion of total assets financed by the

owners’ equity (percentage ownership)

Debt-to-equity ratio – reflects the capital structure of the business, and the extent

to which debt capital is being combined with equity capital (gearing ratio)

Profitability

This term can be used in business and refers to the relationship between the profit

the business is making and the total assets the business owns. In simple terms a

business with high profits and low total assets would be described as a profitability

business. Making profit is essential in business, higher profits means the business is

wealthier meaning the business will be able to undertake more potential

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

opportunities and gain a larger market share. The two main ways to a business will

display profit is as follows below, these two forms of profit have a significant

difference between one another:

Gross profit – the simple difference between the income of the business and its

costs of sales

Operating profit – the gross profit less any overhead expenses

The profit margin of the business will measure how efficiency the business is running

and determine how well a business is coping when it comes to competition and

adverse market conditions such as slumps in demands. The profit margin essential

will calculate how much the business earns from each pound it makes from its

income. This ratio can be calculated as follows ad is expressed in a percentage

Profit Margin = (Net Profit / Net Sales) x 100. With reference to RTL we can work

out the Profit Margin as follows: NOTE net sales = revenue

Profit Margin = (Net Profit / Net Sales) x 100

Profit Margin = (837 / 6373) x 100

Profit Margin = 13.1% for 2017

This is an increase of 0.1% from the previous year of 2016 which a profit

margin of 13.0%

There are also a number of further ratios used to determine the profitability of a

business, one of which, which is very important to a business is the Return on

Capital Employed (ROCE), this ratio will help the business make comparisons

between the business and other businesses in different industries and economies.

The ratio equation for the ROCE is as follows (Profit before interest and tax /

Capital Employed) x 100 in addition the equation for capital employed is Capital

Employed = Total Assets – Current Liabilities. We can work out RTL ROCE as

follows:

ROCE = (Profit before interest and tax / Capital Employed) x 100

ROCE = (1246 / 4734) x 100

ROCE = 26.3% for 2017

This is an increase of 0.8% from the previous year of 2016 with a ROCE of

25.5%

The other ratio commonly used in business to measure its profitability is the Return

on Ordinary Shareholders’ Funds (ROSF), this ratio can be calculated as follows,

ROSF = (Net profit after taxation and preference dividend / Ordinary share

capital + reserves) x 100, NOTE ordinary share capital = price of share x number of

shares.

After analysing these results, we can see that RTL gained a 0.1% increase on its

profit margin although this is a small increase the overall profit margin of 13.1% is a

average but solid value in regards to profit margin, anything 10% and lower is found

to be a weak profit margin and anything 20% and higher is found to be a strong profit

margin, so if RTL continue to increase this would strength the business’ stability. The

display profit is as follows below, these two forms of profit have a significant

difference between one another:

Gross profit – the simple difference between the income of the business and its

costs of sales

Operating profit – the gross profit less any overhead expenses

The profit margin of the business will measure how efficiency the business is running

and determine how well a business is coping when it comes to competition and

adverse market conditions such as slumps in demands. The profit margin essential

will calculate how much the business earns from each pound it makes from its

income. This ratio can be calculated as follows ad is expressed in a percentage

Profit Margin = (Net Profit / Net Sales) x 100. With reference to RTL we can work

out the Profit Margin as follows: NOTE net sales = revenue

Profit Margin = (Net Profit / Net Sales) x 100

Profit Margin = (837 / 6373) x 100

Profit Margin = 13.1% for 2017

This is an increase of 0.1% from the previous year of 2016 which a profit

margin of 13.0%

There are also a number of further ratios used to determine the profitability of a

business, one of which, which is very important to a business is the Return on

Capital Employed (ROCE), this ratio will help the business make comparisons

between the business and other businesses in different industries and economies.

The ratio equation for the ROCE is as follows (Profit before interest and tax /

Capital Employed) x 100 in addition the equation for capital employed is Capital

Employed = Total Assets – Current Liabilities. We can work out RTL ROCE as

follows:

ROCE = (Profit before interest and tax / Capital Employed) x 100

ROCE = (1246 / 4734) x 100

ROCE = 26.3% for 2017

This is an increase of 0.8% from the previous year of 2016 with a ROCE of

25.5%

The other ratio commonly used in business to measure its profitability is the Return

on Ordinary Shareholders’ Funds (ROSF), this ratio can be calculated as follows,

ROSF = (Net profit after taxation and preference dividend / Ordinary share

capital + reserves) x 100, NOTE ordinary share capital = price of share x number of

shares.

After analysing these results, we can see that RTL gained a 0.1% increase on its

profit margin although this is a small increase the overall profit margin of 13.1% is a

average but solid value in regards to profit margin, anything 10% and lower is found

to be a weak profit margin and anything 20% and higher is found to be a strong profit

margin, so if RTL continue to increase this would strength the business’ stability. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit margin means that RTL can directly compare the profit and costs of each

product/service at any given time and therefore they can implement strategies to

increase particular profit margins. The various strategies to increase profit margin

are as follows:

Increase prices – this is the easiest way to increase profit margin, however this

could give your competitors a opportunity to start a price war, so doing research

on clients too see what they would pay for new products is the best way to do

this.

Evaluate and cut the costs of sales – this includes looking ay depreciation,

factory overheads, materials, wages, storage etc. by reducing these costs and

getting rid of any unnecessary expenses rom these cost then the business will

increase its overall profit margin.

Suppliers – similar to the above point, if the business can negotiate a cheaper

price with the supplier, or if this is not possible then research for new suppliers

that can offer a cheaper price for the materials. This will greatly decrease the

production price for each product sold which will drastically increase the profit

margin. If the business is in the position, then using economies of scale to their

benefit by buying in bulk is a good way to increase profit margin.

Manage inventory more efficiently – by the introduction of a up-to-date

inventory management system then the business could save on storage costs

and also will be able to predict sales patterns and trends in the market so that the

business can prepare stock for higher demands at certain times of the year.

When looking at the result from the ROCE ratio analysis we can see that the value

has increase by 0.8% from 2016 to 26.3% in 2017, even though again this is a small

increase it shows the RTL are heading in the right direction as the higher the ROCE

percentage then the higher the profits the business made on its available resources,

as long as RTL continue to have a rising ROCE then they are in a healthy position

with reference to business performance and stability. The ways RTL could improve

on their ROCE are as follows:

Improve the top line – by increasing the operating profit without increasing the

corresponding capital employed the business will increase it ROCE

Maintain operations profits – by maintaining these profits and reducing the

value of the capital employed then the business will benefit from a healthy ROCE

level.

Imitations of Ratio analysis

The ratio analysis of financial statements are useful techniques that every business

should employ as they highlight the different relationships between the elements of

the different financial statements. However even with their usefulness ratio analysis

has been found to have various limitations which are as follows:

1. Ratios are based on the accounting figures that are provided in the financial

statements – this can be subject to various approximations, deficiencies, practice

diversity and manipulation, meaning the results and values calculated can

sometimes be inaccurate and unreliable, leading to inefficient decision making.

2. Ratios have inherent problem of comparability – due to different business

employing various accounting methods, this can cause confusion in comparing

key relationships. For example, inventory turnover can be different for a company

product/service at any given time and therefore they can implement strategies to

increase particular profit margins. The various strategies to increase profit margin

are as follows:

Increase prices – this is the easiest way to increase profit margin, however this

could give your competitors a opportunity to start a price war, so doing research

on clients too see what they would pay for new products is the best way to do

this.

Evaluate and cut the costs of sales – this includes looking ay depreciation,

factory overheads, materials, wages, storage etc. by reducing these costs and

getting rid of any unnecessary expenses rom these cost then the business will

increase its overall profit margin.

Suppliers – similar to the above point, if the business can negotiate a cheaper

price with the supplier, or if this is not possible then research for new suppliers

that can offer a cheaper price for the materials. This will greatly decrease the

production price for each product sold which will drastically increase the profit

margin. If the business is in the position, then using economies of scale to their

benefit by buying in bulk is a good way to increase profit margin.

Manage inventory more efficiently – by the introduction of a up-to-date

inventory management system then the business could save on storage costs

and also will be able to predict sales patterns and trends in the market so that the

business can prepare stock for higher demands at certain times of the year.

When looking at the result from the ROCE ratio analysis we can see that the value

has increase by 0.8% from 2016 to 26.3% in 2017, even though again this is a small

increase it shows the RTL are heading in the right direction as the higher the ROCE

percentage then the higher the profits the business made on its available resources,

as long as RTL continue to have a rising ROCE then they are in a healthy position

with reference to business performance and stability. The ways RTL could improve

on their ROCE are as follows:

Improve the top line – by increasing the operating profit without increasing the

corresponding capital employed the business will increase it ROCE

Maintain operations profits – by maintaining these profits and reducing the

value of the capital employed then the business will benefit from a healthy ROCE

level.

Imitations of Ratio analysis

The ratio analysis of financial statements are useful techniques that every business

should employ as they highlight the different relationships between the elements of

the different financial statements. However even with their usefulness ratio analysis

has been found to have various limitations which are as follows:

1. Ratios are based on the accounting figures that are provided in the financial

statements – this can be subject to various approximations, deficiencies, practice

diversity and manipulation, meaning the results and values calculated can

sometimes be inaccurate and unreliable, leading to inefficient decision making.

2. Ratios have inherent problem of comparability – due to different business

employing various accounting methods, this can cause confusion in comparing

key relationships. For example, inventory turnover can be different for a company

using FIFO than for the other company using LIFO method of inventory valuation.

This thought process is the same when it comes to the methods that business

use when calculating amortisation of preliminary and intangibles expenses,

depreciation, life of asset estimates etc.

3. Inflation – inflation can cause the information of historical costs that are used in

the financial statements to become irrelevant values especially in the case of

assets purchased at different dates. Because the financial statements do not

adjust their values in relation to inflation, this can cause the ratios to be

calculated using irrelevant information which can cause distortions in their results

that can be deceptive.

4. Ratio analysis is not totally dependable – the ratios information must be used

after there is consideration given to the likes of the economic conditions, size of

firm, industry situation, diversity of the product etc. without considering these

factors the business could be ill informed and be surprised when certain factors

impacted the business that they had not accounted for.

5. The various methods of computation will also sway the use of accounting ratios.

The different concepts used for determining numerator and denominator in a

particular accounting ratio will not help in drawing reliable conclusions even in

identical situations.

This thought process is the same when it comes to the methods that business

use when calculating amortisation of preliminary and intangibles expenses,

depreciation, life of asset estimates etc.

3. Inflation – inflation can cause the information of historical costs that are used in

the financial statements to become irrelevant values especially in the case of

assets purchased at different dates. Because the financial statements do not

adjust their values in relation to inflation, this can cause the ratios to be

calculated using irrelevant information which can cause distortions in their results

that can be deceptive.

4. Ratio analysis is not totally dependable – the ratios information must be used

after there is consideration given to the likes of the economic conditions, size of

firm, industry situation, diversity of the product etc. without considering these

factors the business could be ill informed and be surprised when certain factors

impacted the business that they had not accounted for.

5. The various methods of computation will also sway the use of accounting ratios.

The different concepts used for determining numerator and denominator in a

particular accounting ratio will not help in drawing reliable conclusions even in

identical situations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.