Tesco & Sainsbury: A Financial Performance and Ratio Analysis

VerifiedAdded on 2023/01/04

|15

|3727

|69

Report

AI Summary

This report provides a comprehensive financial analysis of Tesco and Sainsbury, two major UK retailers, using various financial ratios to assess their performance. The analysis covers key metrics such as current ratio, quick ratio, net profit margin, gross profit margin, gearing ratio, price earnings ratio, earnings per share, return on capital employed, stock turnover ratio, and dividend pay-out ratio. The report compares the financial health and investment potential of both companies, concluding that Sainsbury currently offers a better investment opportunity due to higher sales rates and dividend payouts. The report also explores the limitations of using financial ratios for performance measurement and suggests strategies for Tesco to improve its financial performance. Capital budgeting techniques and their limitations are also discussed in the context of investment decision-making. Desklib offers a wealth of similar solved assignments and resources for students.

MANAGERIAL

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

PORTFOLIO 1................................................................................................................................3

a. calculation of ratio...................................................................................................................3

b. Analysis of financial performance of Tesco & Sainsbury.......................................................6

c. Reason of poor performance of business.................................................................................8

d. Limitations of measuring financial performance by using financial ratio method..................9

PORTFOLIO 2..............................................................................................................................10

a. Use of capital budgeting technique for taking investment decision......................................10

b. Limitations of investment appraisal techniques....................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

PORTFOLIO 1................................................................................................................................3

a. calculation of ratio...................................................................................................................3

b. Analysis of financial performance of Tesco & Sainsbury.......................................................6

c. Reason of poor performance of business.................................................................................8

d. Limitations of measuring financial performance by using financial ratio method..................9

PORTFOLIO 2..............................................................................................................................10

a. Use of capital budgeting technique for taking investment decision......................................10

b. Limitations of investment appraisal techniques....................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

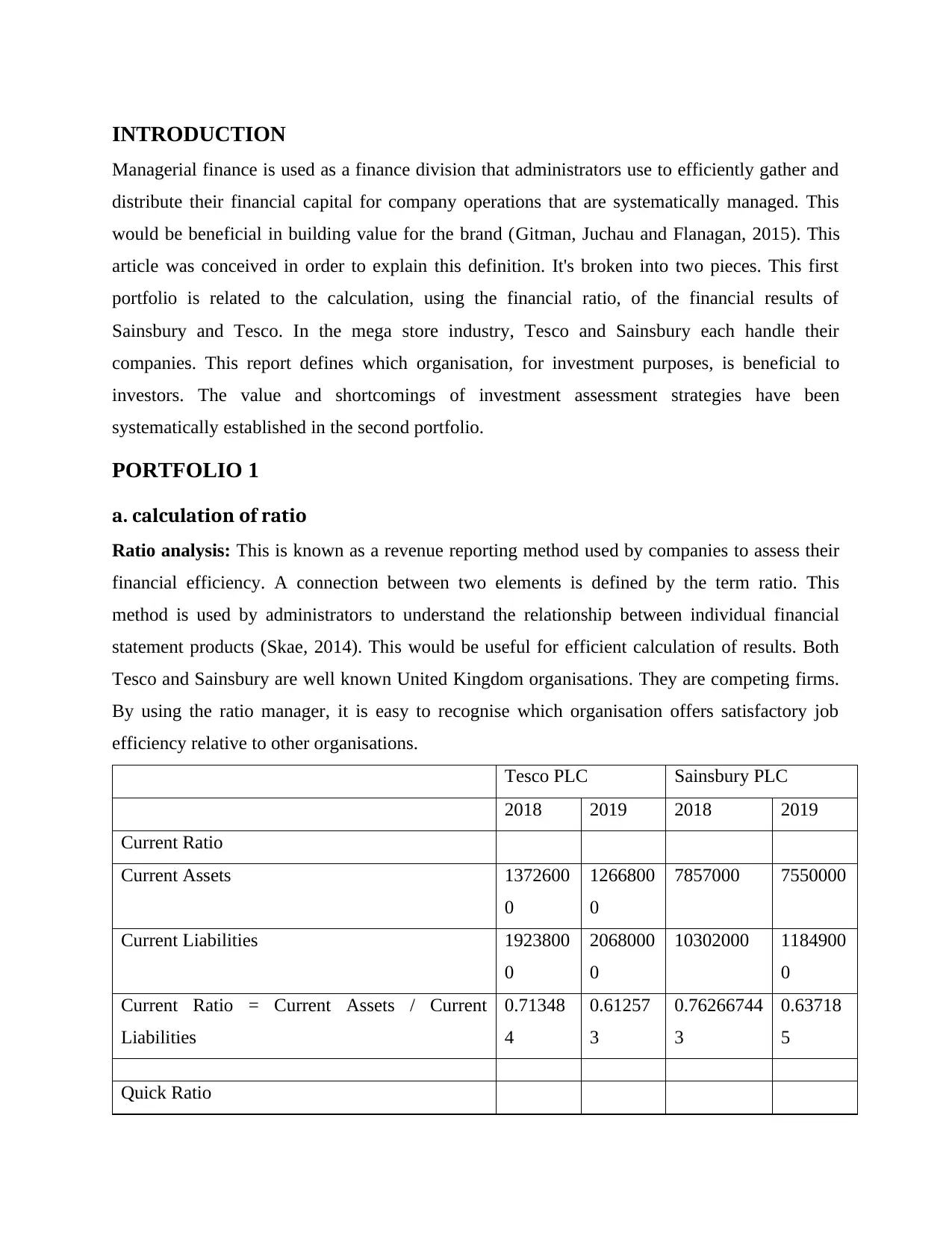

INTRODUCTION

Managerial finance is used as a finance division that administrators use to efficiently gather and

distribute their financial capital for company operations that are systematically managed. This

would be beneficial in building value for the brand (Gitman, Juchau and Flanagan, 2015). This

article was conceived in order to explain this definition. It's broken into two pieces. This first

portfolio is related to the calculation, using the financial ratio, of the financial results of

Sainsbury and Tesco. In the mega store industry, Tesco and Sainsbury each handle their

companies. This report defines which organisation, for investment purposes, is beneficial to

investors. The value and shortcomings of investment assessment strategies have been

systematically established in the second portfolio.

PORTFOLIO 1

a. calculation of ratio

Ratio analysis: This is known as a revenue reporting method used by companies to assess their

financial efficiency. A connection between two elements is defined by the term ratio. This

method is used by administrators to understand the relationship between individual financial

statement products (Skae, 2014). This would be useful for efficient calculation of results. Both

Tesco and Sainsbury are well known United Kingdom organisations. They are competing firms.

By using the ratio manager, it is easy to recognise which organisation offers satisfactory job

efficiency relative to other organisations.

Tesco PLC Sainsbury PLC

2018 2019 2018 2019

Current Ratio

Current Assets 1372600

0

1266800

0

7857000 7550000

Current Liabilities 1923800

0

2068000

0

10302000 1184900

0

Current Ratio = Current Assets / Current

Liabilities

0.71348

4

0.61257

3

0.76266744

3

0.63718

5

Quick Ratio

Managerial finance is used as a finance division that administrators use to efficiently gather and

distribute their financial capital for company operations that are systematically managed. This

would be beneficial in building value for the brand (Gitman, Juchau and Flanagan, 2015). This

article was conceived in order to explain this definition. It's broken into two pieces. This first

portfolio is related to the calculation, using the financial ratio, of the financial results of

Sainsbury and Tesco. In the mega store industry, Tesco and Sainsbury each handle their

companies. This report defines which organisation, for investment purposes, is beneficial to

investors. The value and shortcomings of investment assessment strategies have been

systematically established in the second portfolio.

PORTFOLIO 1

a. calculation of ratio

Ratio analysis: This is known as a revenue reporting method used by companies to assess their

financial efficiency. A connection between two elements is defined by the term ratio. This

method is used by administrators to understand the relationship between individual financial

statement products (Skae, 2014). This would be useful for efficient calculation of results. Both

Tesco and Sainsbury are well known United Kingdom organisations. They are competing firms.

By using the ratio manager, it is easy to recognise which organisation offers satisfactory job

efficiency relative to other organisations.

Tesco PLC Sainsbury PLC

2018 2019 2018 2019

Current Ratio

Current Assets 1372600

0

1266800

0

7857000 7550000

Current Liabilities 1923800

0

2068000

0

10302000 1184900

0

Current Ratio = Current Assets / Current

Liabilities

0.71348

4

0.61257

3

0.76266744

3

0.63718

5

Quick Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quick Asset 1146300

0

1005100

0

7857000 7550000

Current Liabilities 1923800

0

2068000

0

10302000 1184900

0

Quick Ratio = Quick Assets / Current Liabilities 0.59585

2

0.48602

5

0.76266744

3

0.63718

5

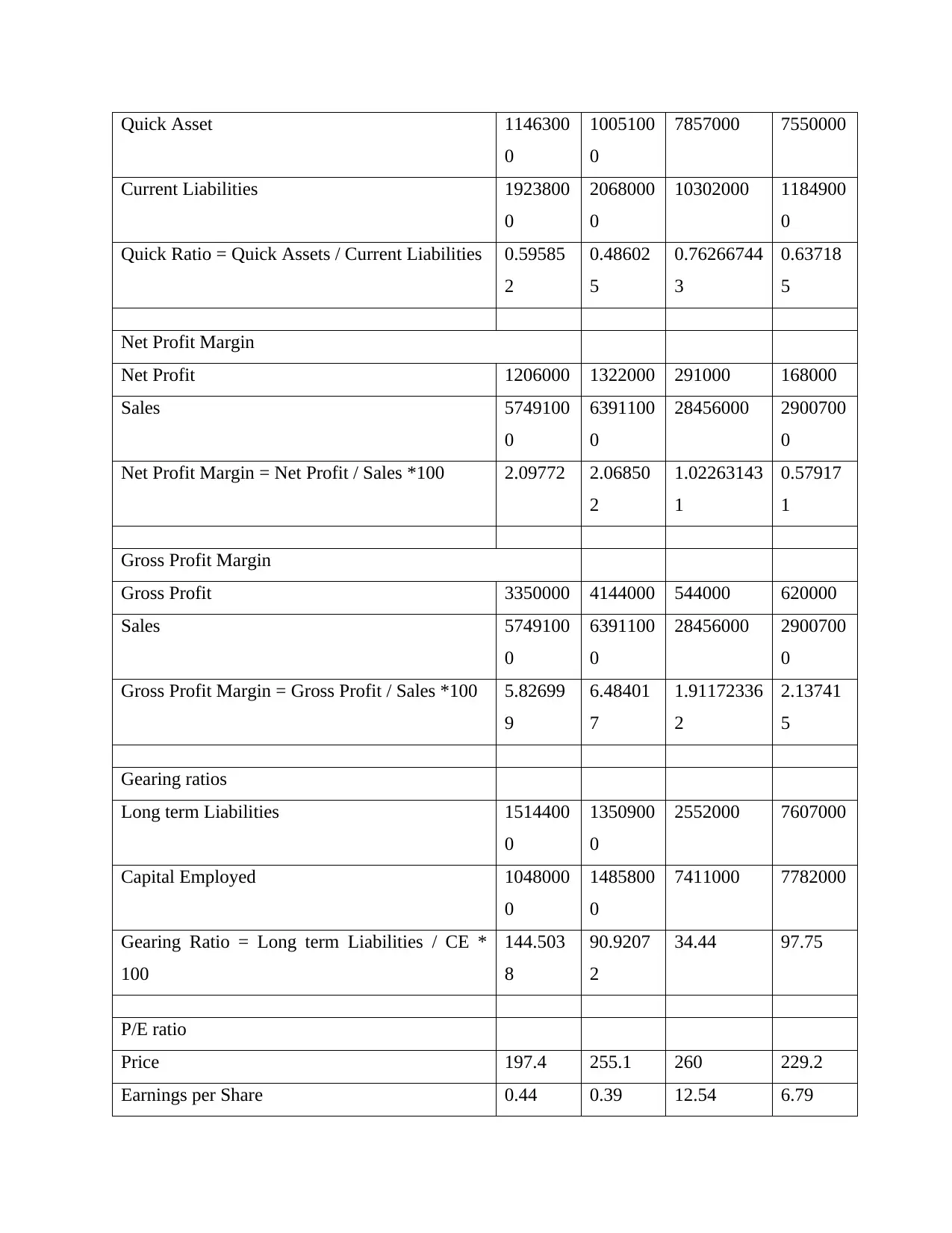

Net Profit Margin

Net Profit 1206000 1322000 291000 168000

Sales 5749100

0

6391100

0

28456000 2900700

0

Net Profit Margin = Net Profit / Sales *100 2.09772 2.06850

2

1.02263143

1

0.57917

1

Gross Profit Margin

Gross Profit 3350000 4144000 544000 620000

Sales 5749100

0

6391100

0

28456000 2900700

0

Gross Profit Margin = Gross Profit / Sales *100 5.82699

9

6.48401

7

1.91172336

2

2.13741

5

Gearing ratios

Long term Liabilities 1514400

0

1350900

0

2552000 7607000

Capital Employed 1048000

0

1485800

0

7411000 7782000

Gearing Ratio = Long term Liabilities / CE *

100

144.503

8

90.9207

2

34.44 97.75

P/E ratio

Price 197.4 255.1 260 229.2

Earnings per Share 0.44 0.39 12.54 6.79

0

1005100

0

7857000 7550000

Current Liabilities 1923800

0

2068000

0

10302000 1184900

0

Quick Ratio = Quick Assets / Current Liabilities 0.59585

2

0.48602

5

0.76266744

3

0.63718

5

Net Profit Margin

Net Profit 1206000 1322000 291000 168000

Sales 5749100

0

6391100

0

28456000 2900700

0

Net Profit Margin = Net Profit / Sales *100 2.09772 2.06850

2

1.02263143

1

0.57917

1

Gross Profit Margin

Gross Profit 3350000 4144000 544000 620000

Sales 5749100

0

6391100

0

28456000 2900700

0

Gross Profit Margin = Gross Profit / Sales *100 5.82699

9

6.48401

7

1.91172336

2

2.13741

5

Gearing ratios

Long term Liabilities 1514400

0

1350900

0

2552000 7607000

Capital Employed 1048000

0

1485800

0

7411000 7782000

Gearing Ratio = Long term Liabilities / CE *

100

144.503

8

90.9207

2

34.44 97.75

P/E ratio

Price 197.4 255.1 260 229.2

Earnings per Share 0.44 0.39 12.54 6.79

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

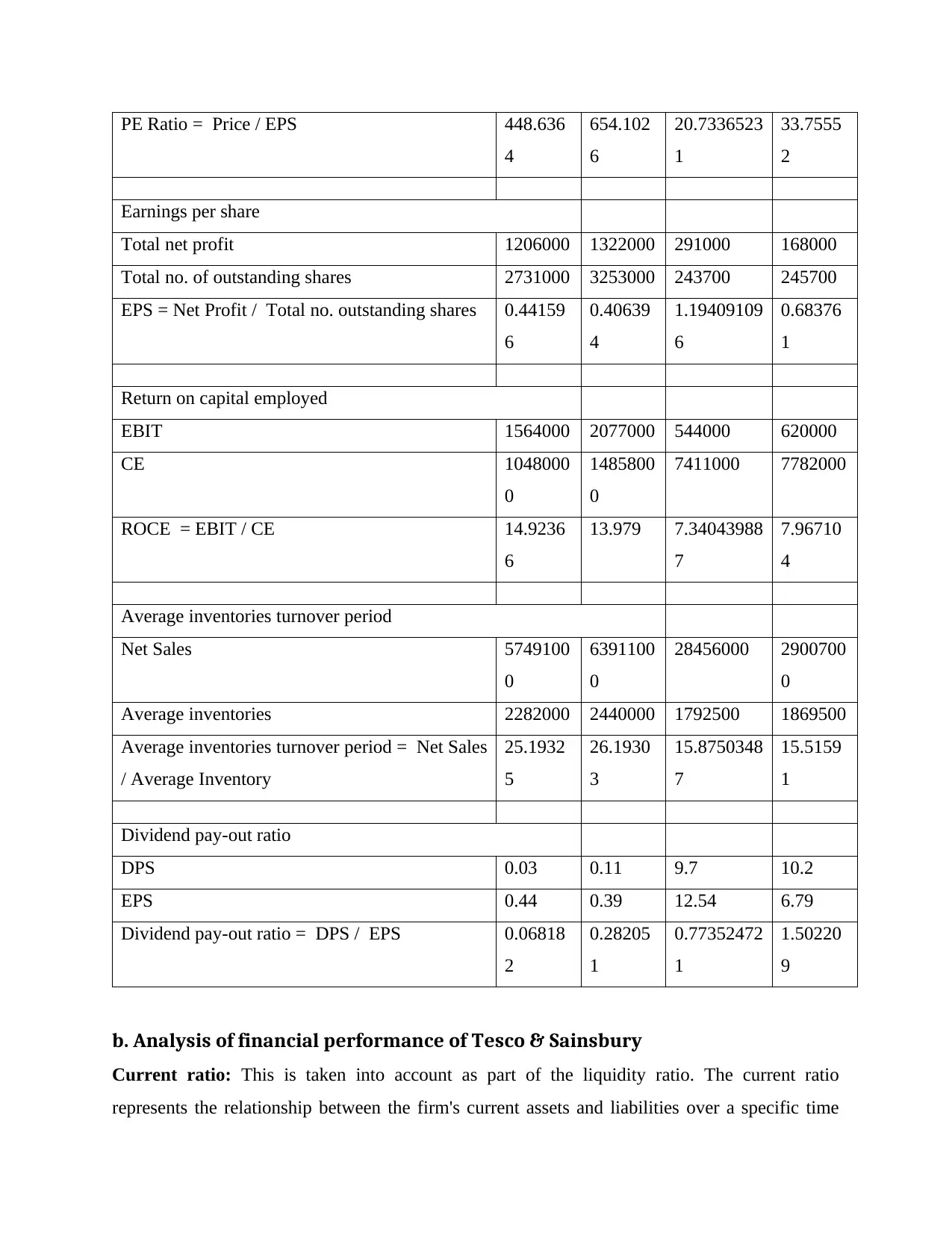

PE Ratio = Price / EPS 448.636

4

654.102

6

20.7336523

1

33.7555

2

Earnings per share

Total net profit 1206000 1322000 291000 168000

Total no. of outstanding shares 2731000 3253000 243700 245700

EPS = Net Profit / Total no. outstanding shares 0.44159

6

0.40639

4

1.19409109

6

0.68376

1

Return on capital employed

EBIT 1564000 2077000 544000 620000

CE 1048000

0

1485800

0

7411000 7782000

ROCE = EBIT / CE 14.9236

6

13.979 7.34043988

7

7.96710

4

Average inventories turnover period

Net Sales 5749100

0

6391100

0

28456000 2900700

0

Average inventories 2282000 2440000 1792500 1869500

Average inventories turnover period = Net Sales

/ Average Inventory

25.1932

5

26.1930

3

15.8750348

7

15.5159

1

Dividend pay-out ratio

DPS 0.03 0.11 9.7 10.2

EPS 0.44 0.39 12.54 6.79

Dividend pay-out ratio = DPS / EPS 0.06818

2

0.28205

1

0.77352472

1

1.50220

9

b. Analysis of financial performance of Tesco & Sainsbury

Current ratio: This is taken into account as part of the liquidity ratio. The current ratio

represents the relationship between the firm's current assets and liabilities over a specific time

4

654.102

6

20.7336523

1

33.7555

2

Earnings per share

Total net profit 1206000 1322000 291000 168000

Total no. of outstanding shares 2731000 3253000 243700 245700

EPS = Net Profit / Total no. outstanding shares 0.44159

6

0.40639

4

1.19409109

6

0.68376

1

Return on capital employed

EBIT 1564000 2077000 544000 620000

CE 1048000

0

1485800

0

7411000 7782000

ROCE = EBIT / CE 14.9236

6

13.979 7.34043988

7

7.96710

4

Average inventories turnover period

Net Sales 5749100

0

6391100

0

28456000 2900700

0

Average inventories 2282000 2440000 1792500 1869500

Average inventories turnover period = Net Sales

/ Average Inventory

25.1932

5

26.1930

3

15.8750348

7

15.5159

1

Dividend pay-out ratio

DPS 0.03 0.11 9.7 10.2

EPS 0.44 0.39 12.54 6.79

Dividend pay-out ratio = DPS / EPS 0.06818

2

0.28205

1

0.77352472

1

1.50220

9

b. Analysis of financial performance of Tesco & Sainsbury

Current ratio: This is taken into account as part of the liquidity ratio. The current ratio

represents the relationship between the firm's current assets and liabilities over a specific time

frame. Consider 2:1 as the desired current ratio (Schlegel, 2015). This shows that any

corporation has more money to meet their existing responsibilities. This demonstrates the firm's

willingness to satisfy its short-term obligations. The map was created to calculate Tesco and

Sainsbury's financial results.

Sainsbury's current ratio is far greater than Tesco's as per this above value, since the current

value obtained was 0.71 and 0.61 in 2019 and the Sainsbury value obtained was 0.76 and 066,

this defines that Sainsbury has far more current assets to meet its short-term debt obligations.

Quick ratio- This is also part of the ratio for calculating liquidity. To use quick ratio managers

to figure out the location of the company of liquid resources within a given amount of time. This

ratio demonstrates the connection between current liabilities and expedited properties. The

higher fast ratio suggests that the company has enough cash reserves. The cash availability of the

operational map is used for estimation.

This reveals that Sainsbury's fast asset ratio will be much better than Tesco in contrast with

Tesco's valuation. The rapid value of Sainsbury's proportion was determined at .60 in 2018

and .5 in 2019. In the case of Tesco, the fast ratio value was estimated at 0.59 and it declined in

2019. While both companies have lowered the valuation of the fast ratio, they have ample cash

or liquidity management buffer relative to Tesco Sainsbury that they use for the day-to-day daily

operations.

Net profit ratio- To figure out the organization's likelihood amount, this ratio is determined.

This is viewed as an important ratio as the ownership group considers their place within the

sector on the basis of calculating the net profit ratio (Hull and Dawar, 2014). This shows the

organization's potential to achieve profit from its revenue by deducting all the necessary costs.

This above value indicates that the total benefit ratio quality of Tesco was greater than

Sainsbury, since the net benefit level rate was estimated at 2.1 and improved in 2019 and that

level of Sainsbury fell from 1.09 to 0.75.

Gross profit margin- This percentage shows the measure of profitability and revenue,

describing the overall potential to produce sales profit from trading. When comparing the value

of gross profit with revenue, the Gross Profit Ratio is determined.

corporation has more money to meet their existing responsibilities. This demonstrates the firm's

willingness to satisfy its short-term obligations. The map was created to calculate Tesco and

Sainsbury's financial results.

Sainsbury's current ratio is far greater than Tesco's as per this above value, since the current

value obtained was 0.71 and 0.61 in 2019 and the Sainsbury value obtained was 0.76 and 066,

this defines that Sainsbury has far more current assets to meet its short-term debt obligations.

Quick ratio- This is also part of the ratio for calculating liquidity. To use quick ratio managers

to figure out the location of the company of liquid resources within a given amount of time. This

ratio demonstrates the connection between current liabilities and expedited properties. The

higher fast ratio suggests that the company has enough cash reserves. The cash availability of the

operational map is used for estimation.

This reveals that Sainsbury's fast asset ratio will be much better than Tesco in contrast with

Tesco's valuation. The rapid value of Sainsbury's proportion was determined at .60 in 2018

and .5 in 2019. In the case of Tesco, the fast ratio value was estimated at 0.59 and it declined in

2019. While both companies have lowered the valuation of the fast ratio, they have ample cash

or liquidity management buffer relative to Tesco Sainsbury that they use for the day-to-day daily

operations.

Net profit ratio- To figure out the organization's likelihood amount, this ratio is determined.

This is viewed as an important ratio as the ownership group considers their place within the

sector on the basis of calculating the net profit ratio (Hull and Dawar, 2014). This shows the

organization's potential to achieve profit from its revenue by deducting all the necessary costs.

This above value indicates that the total benefit ratio quality of Tesco was greater than

Sainsbury, since the net benefit level rate was estimated at 2.1 and improved in 2019 and that

level of Sainsbury fell from 1.09 to 0.75.

Gross profit margin- This percentage shows the measure of profitability and revenue,

describing the overall potential to produce sales profit from trading. When comparing the value

of gross profit with revenue, the Gross Profit Ratio is determined.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The magnitude of Sainsbury's gross profit margin is much higher than Tesco's. When compared

to Tesco, this means that Sainsbury earns more operating profit.

Gearing ratio- This measure is measured in order to analyse the importance of an organisation's

financial leverage. It is measured to equate equity with obligation for debt. This ratio defines the

extent at which a company needs to comply with its long-term commitments relative to the

valuation of its shareholder. Compared to their internal capital, corporate companies need to

provide ample external funds that help offer them tax advantages. Research will be achieved

through the use of Tesco and Sainsbury total equity for graphical map analysis calculation.

This graph reveals that Tesco is in a strong spot relative to Sainsbury, which suggests that

Tesco's top management conducts efficient policies about its internally and externally assets,

while systematically retaining these funds.

Price earnings ratio- In order to evaluate the relationship between stocks and net sales produced

from company operations, managers use relative valuation ratios (Asongu, 2015). This ratio is

used to assess the firm's potential to attract or not attract business buyers. The price earnings

ratio map was developed using rise in average ratio to assess the value.

It can be calculated from this map that the valuation of Sainsbury's stock values is relatively very

high meaning that buying in Sainsbury is valuable to customers because the value of the stock is

large.

Earnings per share- This ratio is determined in order to determine the profits of each share over

a given period of time. It also is calculated as the market benefit assigned to the assets (Lee and

Isa, 2015).

The size of Tesco's earnings per share was 4.96 in 2018 and 6.14 in 2019, and 4.75 in 2018 and

4.06 in 2019 is estimated for Sainsbury. That suggests that Tesco is in a stronger situation than

its competing organisation, and their share is more important than that.

Return on capital employed- To evaluate the capacity to use resources to produce income,

managers measured this ratio. That's also part of the financial ratios, and it shows the relationship

among capital and earnings staff. The importance of this ratio map has been developed to

calculate it.

As per this description, Tesco's amount of money invested is far greater than Sainsbury's value.

That suggests that Tesco performs its corporate processes in a relatively more structured way.

to Tesco, this means that Sainsbury earns more operating profit.

Gearing ratio- This measure is measured in order to analyse the importance of an organisation's

financial leverage. It is measured to equate equity with obligation for debt. This ratio defines the

extent at which a company needs to comply with its long-term commitments relative to the

valuation of its shareholder. Compared to their internal capital, corporate companies need to

provide ample external funds that help offer them tax advantages. Research will be achieved

through the use of Tesco and Sainsbury total equity for graphical map analysis calculation.

This graph reveals that Tesco is in a strong spot relative to Sainsbury, which suggests that

Tesco's top management conducts efficient policies about its internally and externally assets,

while systematically retaining these funds.

Price earnings ratio- In order to evaluate the relationship between stocks and net sales produced

from company operations, managers use relative valuation ratios (Asongu, 2015). This ratio is

used to assess the firm's potential to attract or not attract business buyers. The price earnings

ratio map was developed using rise in average ratio to assess the value.

It can be calculated from this map that the valuation of Sainsbury's stock values is relatively very

high meaning that buying in Sainsbury is valuable to customers because the value of the stock is

large.

Earnings per share- This ratio is determined in order to determine the profits of each share over

a given period of time. It also is calculated as the market benefit assigned to the assets (Lee and

Isa, 2015).

The size of Tesco's earnings per share was 4.96 in 2018 and 6.14 in 2019, and 4.75 in 2018 and

4.06 in 2019 is estimated for Sainsbury. That suggests that Tesco is in a stronger situation than

its competing organisation, and their share is more important than that.

Return on capital employed- To evaluate the capacity to use resources to produce income,

managers measured this ratio. That's also part of the financial ratios, and it shows the relationship

among capital and earnings staff. The importance of this ratio map has been developed to

calculate it.

As per this description, Tesco's amount of money invested is far greater than Sainsbury's value.

That suggests that Tesco performs its corporate processes in a relatively more structured way.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Although the rate of capital invested is rising in both firms, Tesco is much stronger for

comparative purposes.

Stock turnover ratio- This ratio suggests that organisations require time to turn their inputs into

outputs and sell them mostly on marketplace. It is used to determine the time inventory was sold

out. Higher proportion indicates the company require longer time to transform their stocks.

It has been established from this graph that Tesco's inventory turnover is relatively high,

indicating that it takes a lot longer for this retailers to produce its stocks.

Dividend pay-out ratio: This ratio being determined to recognise the dividend-net income ratio.

In the grounds of such a ratio measurement, administrators are able to determine the dividend

amount they are capable of paying through the net earnings (Hull, Danso and Adomako, 2014).

This ratio is helpful in finding the dividend value. Investors take their judgment to allocate the

quality of dived company to their owners on the grounds of calculation.

It should be understood by this calculation that the amount of the dividend paid out by Sainsbury

is also much greater than that of Tesco. The above calculation defines that Tesco was able to

allocate 6.78 per quarter of dividends to its investors in 2019. This level became improved by

giving their stakeholders 27.05 regular dividend. On the opposite hand, the dividend paid out

ratio level of Sainsbury was 76.05 and the level for this dividends rose from 76.05 to 112.79 in

2019. Each company have remained in a sustainable position since the magnitude of their

dividend yield has improved. That ensures that as opposed to Tesco, Sainsbury offers its owners

a high rate of dividend. While Tesco raised the size of the dividends, Sainsbury showed higher

returns to its owners in the context of a results contrast.

c. Reason of poor performance of business.

By evaluating financial results through the Tesco and Sainsbury ratio process, it was revealed

that the quality of both companies is improving, but for the sake of contrast, Sainsbury earns

high sales rates and delivers dividends, so Sainsbury is a superior choice relative to Tesco for

productive investments (Wang, Jiang and Lin, 2014).

The general manager of Tesco must apply certain market methods that help increase the rate of

sales. It would be useful for market practises that raise cash inflow.

Tesco does not use an efficient pricing policy on their commodity, but as opposed to Sainsbury,

their efficiency has decreased.

comparative purposes.

Stock turnover ratio- This ratio suggests that organisations require time to turn their inputs into

outputs and sell them mostly on marketplace. It is used to determine the time inventory was sold

out. Higher proportion indicates the company require longer time to transform their stocks.

It has been established from this graph that Tesco's inventory turnover is relatively high,

indicating that it takes a lot longer for this retailers to produce its stocks.

Dividend pay-out ratio: This ratio being determined to recognise the dividend-net income ratio.

In the grounds of such a ratio measurement, administrators are able to determine the dividend

amount they are capable of paying through the net earnings (Hull, Danso and Adomako, 2014).

This ratio is helpful in finding the dividend value. Investors take their judgment to allocate the

quality of dived company to their owners on the grounds of calculation.

It should be understood by this calculation that the amount of the dividend paid out by Sainsbury

is also much greater than that of Tesco. The above calculation defines that Tesco was able to

allocate 6.78 per quarter of dividends to its investors in 2019. This level became improved by

giving their stakeholders 27.05 regular dividend. On the opposite hand, the dividend paid out

ratio level of Sainsbury was 76.05 and the level for this dividends rose from 76.05 to 112.79 in

2019. Each company have remained in a sustainable position since the magnitude of their

dividend yield has improved. That ensures that as opposed to Tesco, Sainsbury offers its owners

a high rate of dividend. While Tesco raised the size of the dividends, Sainsbury showed higher

returns to its owners in the context of a results contrast.

c. Reason of poor performance of business.

By evaluating financial results through the Tesco and Sainsbury ratio process, it was revealed

that the quality of both companies is improving, but for the sake of contrast, Sainsbury earns

high sales rates and delivers dividends, so Sainsbury is a superior choice relative to Tesco for

productive investments (Wang, Jiang and Lin, 2014).

The general manager of Tesco must apply certain market methods that help increase the rate of

sales. It would be useful for market practises that raise cash inflow.

Tesco does not use an efficient pricing policy on their commodity, but as opposed to Sainsbury,

their efficiency has decreased.

Even in the case of other ratios, such as earnings per share, the Tesco ratio offers a reasonably

high return on invested capital. The below are few suggestions to better boost Tesco's financial

results.

Tesco management teams need to devise strategies and legislation that tend to improve their

company practises with cash inflows.

In order to minimise product turnaround time span, they need to use an inventory control strategy

that is helpful in minimising time and handling stock levels.

d. Limitations of measuring financial performance by using financial ratio

method

Business or companies use the different ratios to calculate their efficiency, although this

metric is considered the most appropriate and effective method, although there are certain

drawbacks when using this financial accounting instrument, which is described below.

It is used for calculating purposes since it becomes complicated often when many companies

use multiple accounting methods for their function (Gottardo and Moisello, 2014).

Seasons influence the valuation of financial reports explicitly. Decisions based on high or

reduce the frequency numbers are not accurate.

Only this aspect is taken into consideration, and can be true in quantitative terms and not in

measurable terms, because organisations are unable to quantify the expertise of their human

capital.

Personnel with outstanding labelling experience and expertise that have expertise of each accrual

basis need to be employed to use the financial ratio company. Although the measurement of this

ratio is difficult, all the changes need to be defined before analyse the economic equation.

PORTFOLIO 2

a. Use of capital budgeting technique for taking investment decision

Net Profits Project A

Project

B

Plant 1 Plant 2

high return on invested capital. The below are few suggestions to better boost Tesco's financial

results.

Tesco management teams need to devise strategies and legislation that tend to improve their

company practises with cash inflows.

In order to minimise product turnaround time span, they need to use an inventory control strategy

that is helpful in minimising time and handling stock levels.

d. Limitations of measuring financial performance by using financial ratio

method

Business or companies use the different ratios to calculate their efficiency, although this

metric is considered the most appropriate and effective method, although there are certain

drawbacks when using this financial accounting instrument, which is described below.

It is used for calculating purposes since it becomes complicated often when many companies

use multiple accounting methods for their function (Gottardo and Moisello, 2014).

Seasons influence the valuation of financial reports explicitly. Decisions based on high or

reduce the frequency numbers are not accurate.

Only this aspect is taken into consideration, and can be true in quantitative terms and not in

measurable terms, because organisations are unable to quantify the expertise of their human

capital.

Personnel with outstanding labelling experience and expertise that have expertise of each accrual

basis need to be employed to use the financial ratio company. Although the measurement of this

ratio is difficult, all the changes need to be defined before analyse the economic equation.

PORTFOLIO 2

a. Use of capital budgeting technique for taking investment decision

Net Profits Project A

Project

B

Plant 1 Plant 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

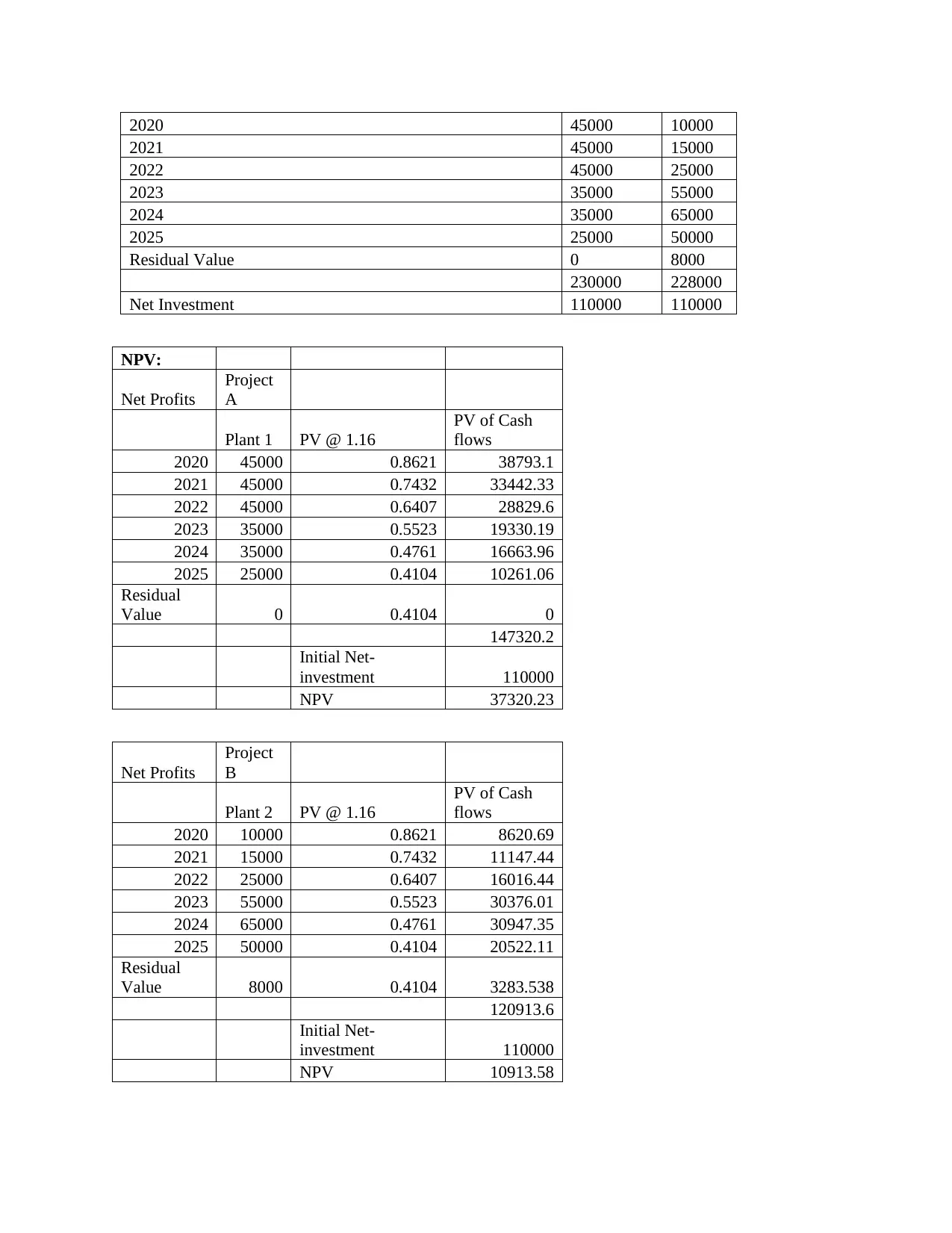

2020 45000 10000

2021 45000 15000

2022 45000 25000

2023 35000 55000

2024 35000 65000

2025 25000 50000

Residual Value 0 8000

230000 228000

Net Investment 110000 110000

NPV:

Net Profits

Project

A

Plant 1 PV @ 1.16

PV of Cash

flows

2020 45000 0.8621 38793.1

2021 45000 0.7432 33442.33

2022 45000 0.6407 28829.6

2023 35000 0.5523 19330.19

2024 35000 0.4761 16663.96

2025 25000 0.4104 10261.06

Residual

Value 0 0.4104 0

147320.2

Initial Net-

investment 110000

NPV 37320.23

Net Profits

Project

B

Plant 2 PV @ 1.16

PV of Cash

flows

2020 10000 0.8621 8620.69

2021 15000 0.7432 11147.44

2022 25000 0.6407 16016.44

2023 55000 0.5523 30376.01

2024 65000 0.4761 30947.35

2025 50000 0.4104 20522.11

Residual

Value 8000 0.4104 3283.538

120913.6

Initial Net-

investment 110000

NPV 10913.58

2021 45000 15000

2022 45000 25000

2023 35000 55000

2024 35000 65000

2025 25000 50000

Residual Value 0 8000

230000 228000

Net Investment 110000 110000

NPV:

Net Profits

Project

A

Plant 1 PV @ 1.16

PV of Cash

flows

2020 45000 0.8621 38793.1

2021 45000 0.7432 33442.33

2022 45000 0.6407 28829.6

2023 35000 0.5523 19330.19

2024 35000 0.4761 16663.96

2025 25000 0.4104 10261.06

Residual

Value 0 0.4104 0

147320.2

Initial Net-

investment 110000

NPV 37320.23

Net Profits

Project

B

Plant 2 PV @ 1.16

PV of Cash

flows

2020 10000 0.8621 8620.69

2021 15000 0.7432 11147.44

2022 25000 0.6407 16016.44

2023 55000 0.5523 30376.01

2024 65000 0.4761 30947.35

2025 50000 0.4104 20522.11

Residual

Value 8000 0.4104 3283.538

120913.6

Initial Net-

investment 110000

NPV 10913.58

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

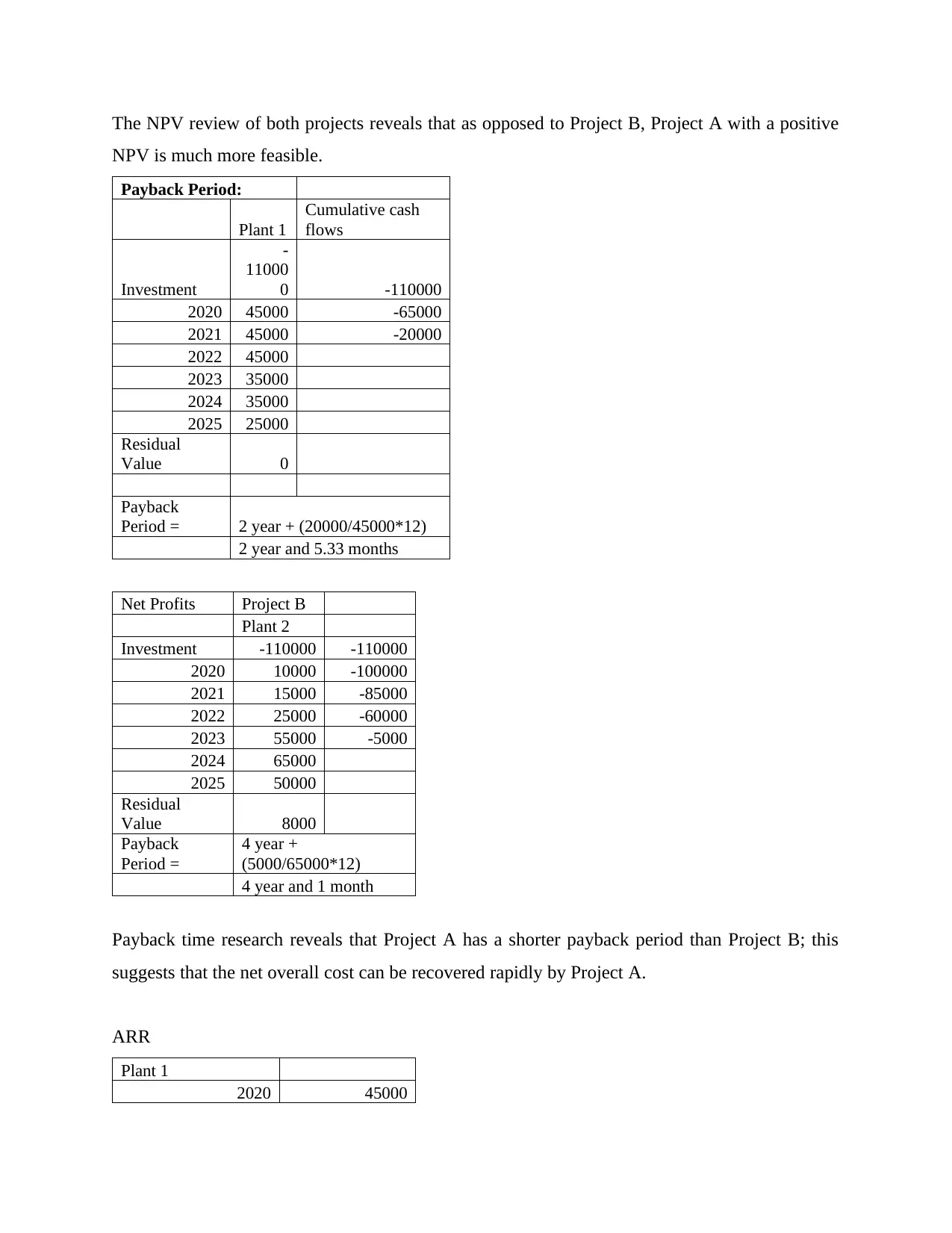

The NPV review of both projects reveals that as opposed to Project B, Project A with a positive

NPV is much more feasible.

Payback Period:

Plant 1

Cumulative cash

flows

Investment

-

11000

0 -110000

2020 45000 -65000

2021 45000 -20000

2022 45000

2023 35000

2024 35000

2025 25000

Residual

Value 0

Payback

Period = 2 year + (20000/45000*12)

2 year and 5.33 months

Net Profits Project B

Plant 2

Investment -110000 -110000

2020 10000 -100000

2021 15000 -85000

2022 25000 -60000

2023 55000 -5000

2024 65000

2025 50000

Residual

Value 8000

Payback

Period =

4 year +

(5000/65000*12)

4 year and 1 month

Payback time research reveals that Project A has a shorter payback period than Project B; this

suggests that the net overall cost can be recovered rapidly by Project A.

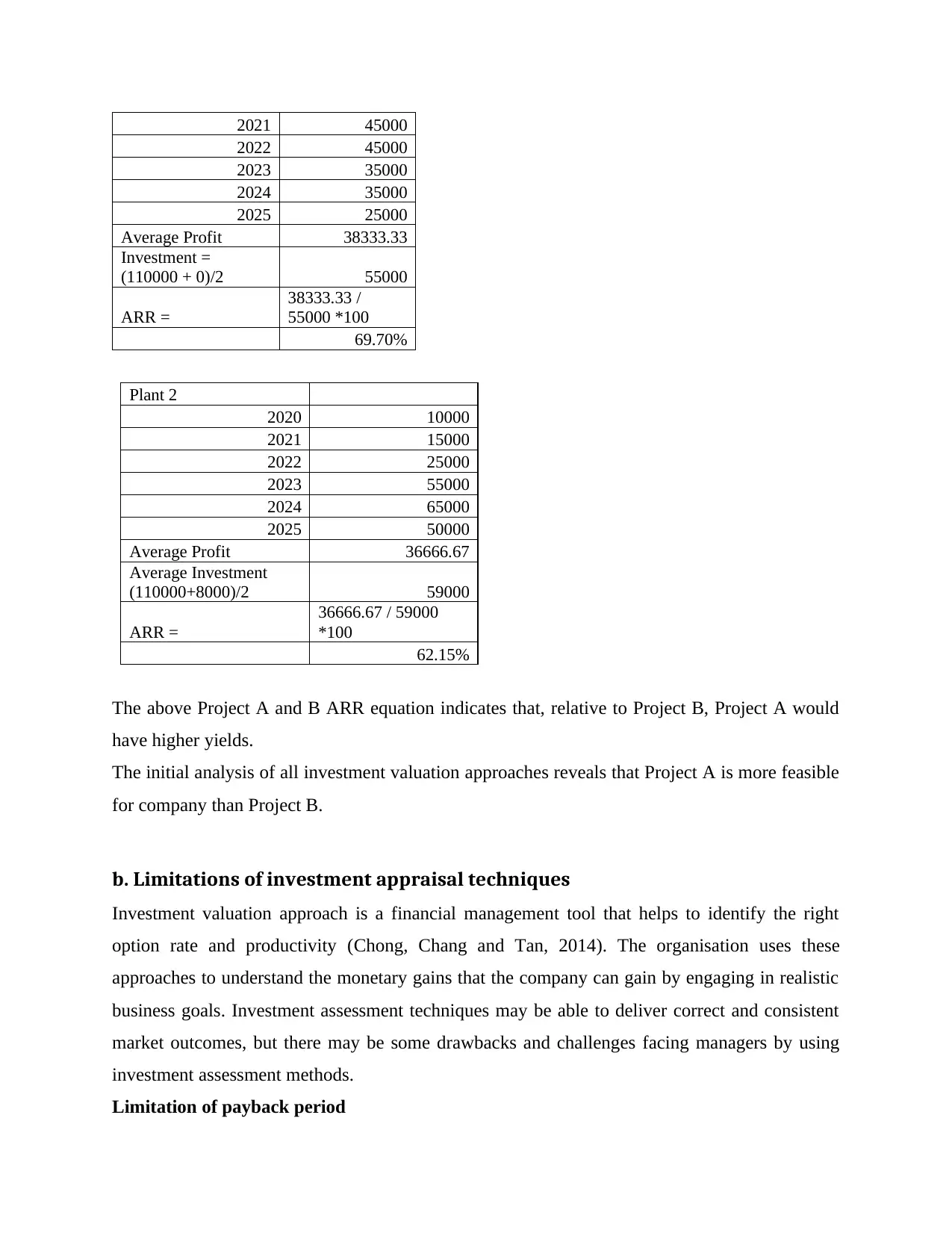

ARR

Plant 1

2020 45000

NPV is much more feasible.

Payback Period:

Plant 1

Cumulative cash

flows

Investment

-

11000

0 -110000

2020 45000 -65000

2021 45000 -20000

2022 45000

2023 35000

2024 35000

2025 25000

Residual

Value 0

Payback

Period = 2 year + (20000/45000*12)

2 year and 5.33 months

Net Profits Project B

Plant 2

Investment -110000 -110000

2020 10000 -100000

2021 15000 -85000

2022 25000 -60000

2023 55000 -5000

2024 65000

2025 50000

Residual

Value 8000

Payback

Period =

4 year +

(5000/65000*12)

4 year and 1 month

Payback time research reveals that Project A has a shorter payback period than Project B; this

suggests that the net overall cost can be recovered rapidly by Project A.

ARR

Plant 1

2020 45000

2021 45000

2022 45000

2023 35000

2024 35000

2025 25000

Average Profit 38333.33

Investment =

(110000 + 0)/2 55000

ARR =

38333.33 /

55000 *100

69.70%

Plant 2

2020 10000

2021 15000

2022 25000

2023 55000

2024 65000

2025 50000

Average Profit 36666.67

Average Investment

(110000+8000)/2 59000

ARR =

36666.67 / 59000

*100

62.15%

The above Project A and B ARR equation indicates that, relative to Project B, Project A would

have higher yields.

The initial analysis of all investment valuation approaches reveals that Project A is more feasible

for company than Project B.

b. Limitations of investment appraisal techniques

Investment valuation approach is a financial management tool that helps to identify the right

option rate and productivity (Chong, Chang and Tan, 2014). The organisation uses these

approaches to understand the monetary gains that the company can gain by engaging in realistic

business goals. Investment assessment techniques may be able to deliver correct and consistent

market outcomes, but there may be some drawbacks and challenges facing managers by using

investment assessment methods.

Limitation of payback period

2022 45000

2023 35000

2024 35000

2025 25000

Average Profit 38333.33

Investment =

(110000 + 0)/2 55000

ARR =

38333.33 /

55000 *100

69.70%

Plant 2

2020 10000

2021 15000

2022 25000

2023 55000

2024 65000

2025 50000

Average Profit 36666.67

Average Investment

(110000+8000)/2 59000

ARR =

36666.67 / 59000

*100

62.15%

The above Project A and B ARR equation indicates that, relative to Project B, Project A would

have higher yields.

The initial analysis of all investment valuation approaches reveals that Project A is more feasible

for company than Project B.

b. Limitations of investment appraisal techniques

Investment valuation approach is a financial management tool that helps to identify the right

option rate and productivity (Chong, Chang and Tan, 2014). The organisation uses these

approaches to understand the monetary gains that the company can gain by engaging in realistic

business goals. Investment assessment techniques may be able to deliver correct and consistent

market outcomes, but there may be some drawbacks and challenges facing managers by using

investment assessment methods.

Limitation of payback period

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.