Financial Analysis Report: Greencross Holdings Limited (5 Years)

VerifiedAdded on 2023/01/23

|10

|1106

|95

Report

AI Summary

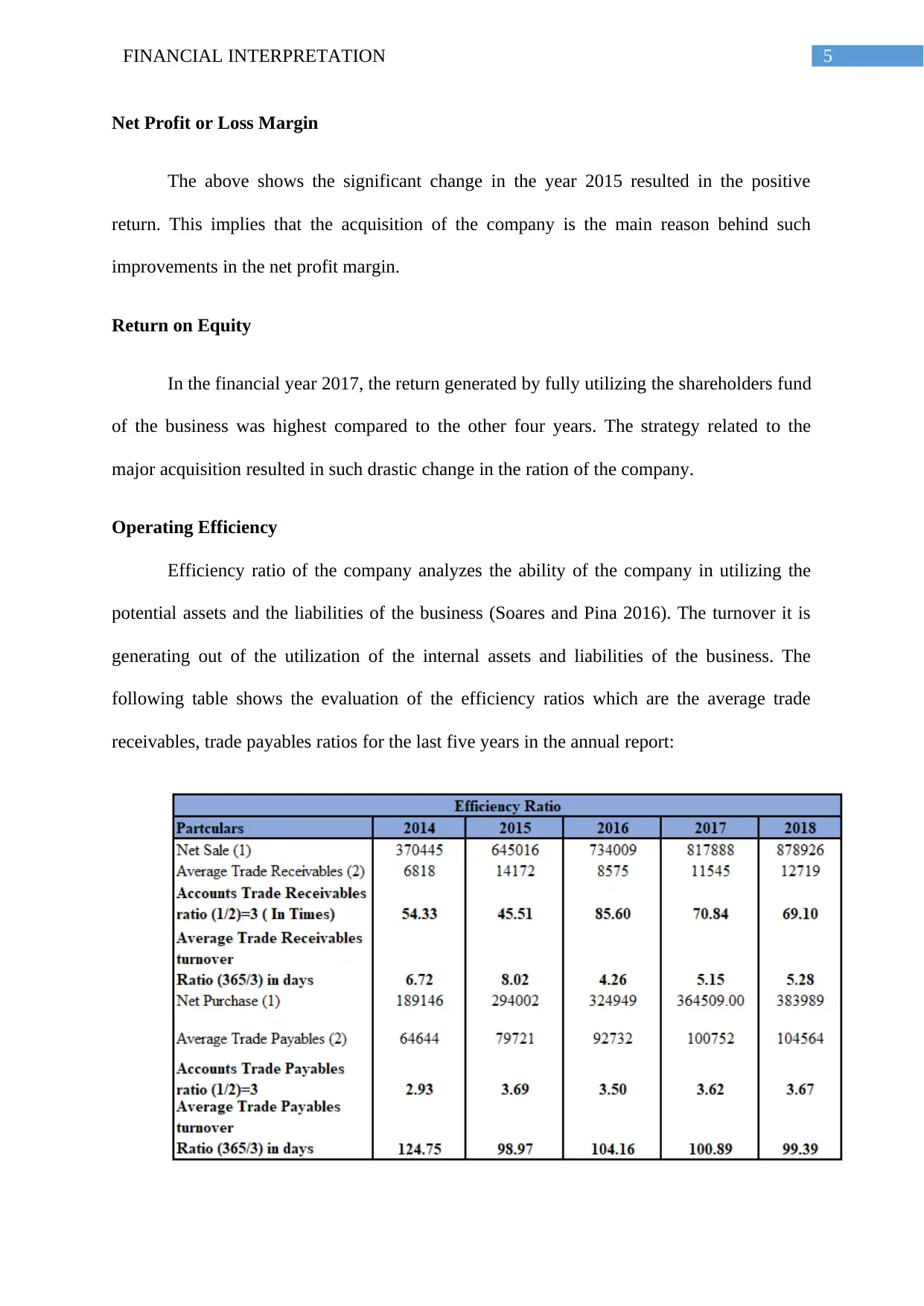

This report presents a financial analysis of Greencross Holdings Limited, evaluating its performance over five years using key financial ratios. The analysis covers profitability ratios (Return on Asset, Return on Equity, Net Profit Margin), operating efficiency ratios (Average Turnover Receivables, Average Turnover Payables), liquidity and solvency ratios (Current Ratio, Quick Ratio), and market performance ratios (Price Earnings Ratio). The report highlights the impact of the 2014 acquisition of Mammoth Pet on the company's financial position, showing improvements in profitability after the acquisition. The analysis also discusses the company's strengths and weaknesses, concluding with recommendations for enhancing financial performance and strategic decision-making.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.