Financial Analysis Assessment: Elite plc Ratio Analysis Report

VerifiedAdded on 2022/12/14

|9

|1721

|319

Report

AI Summary

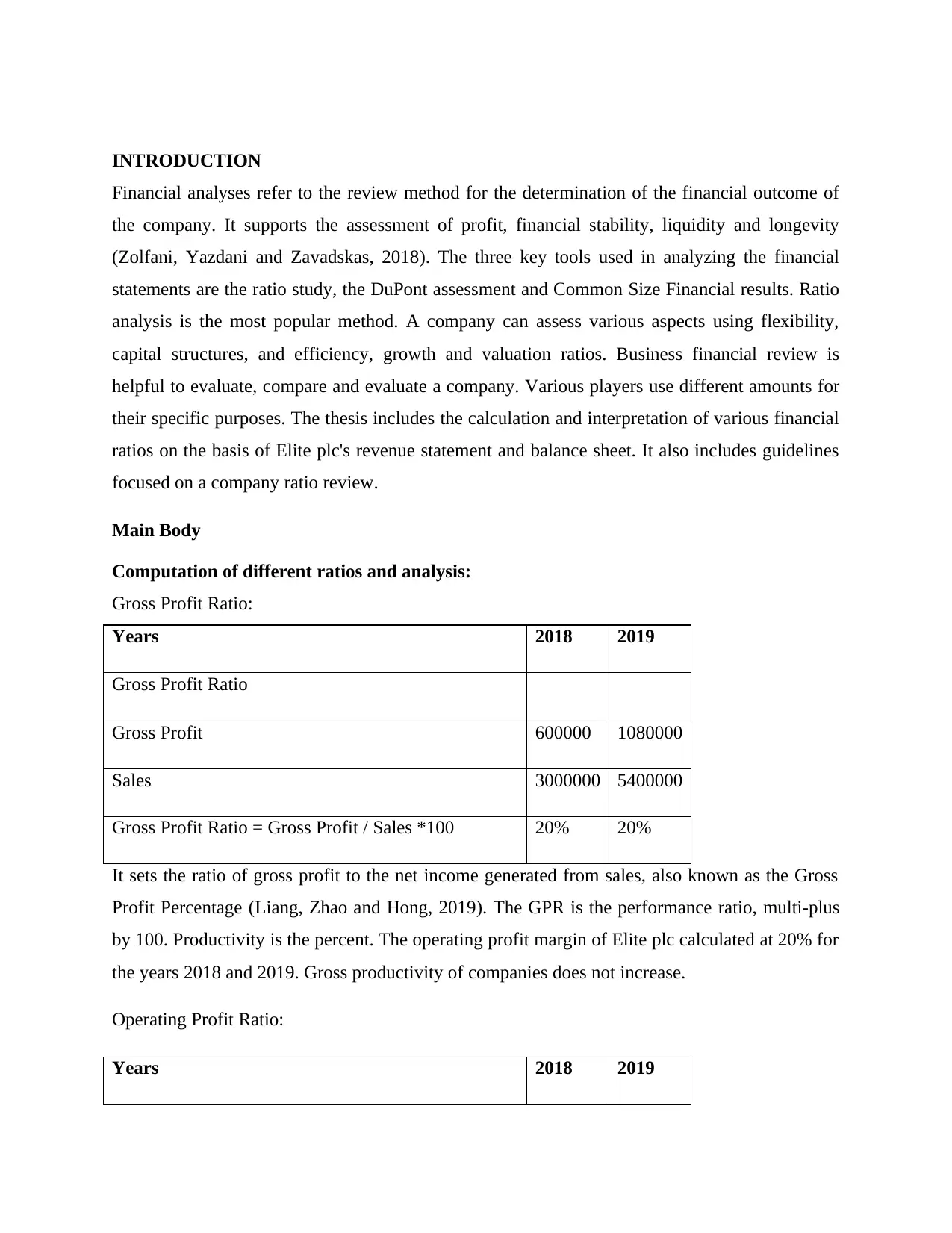

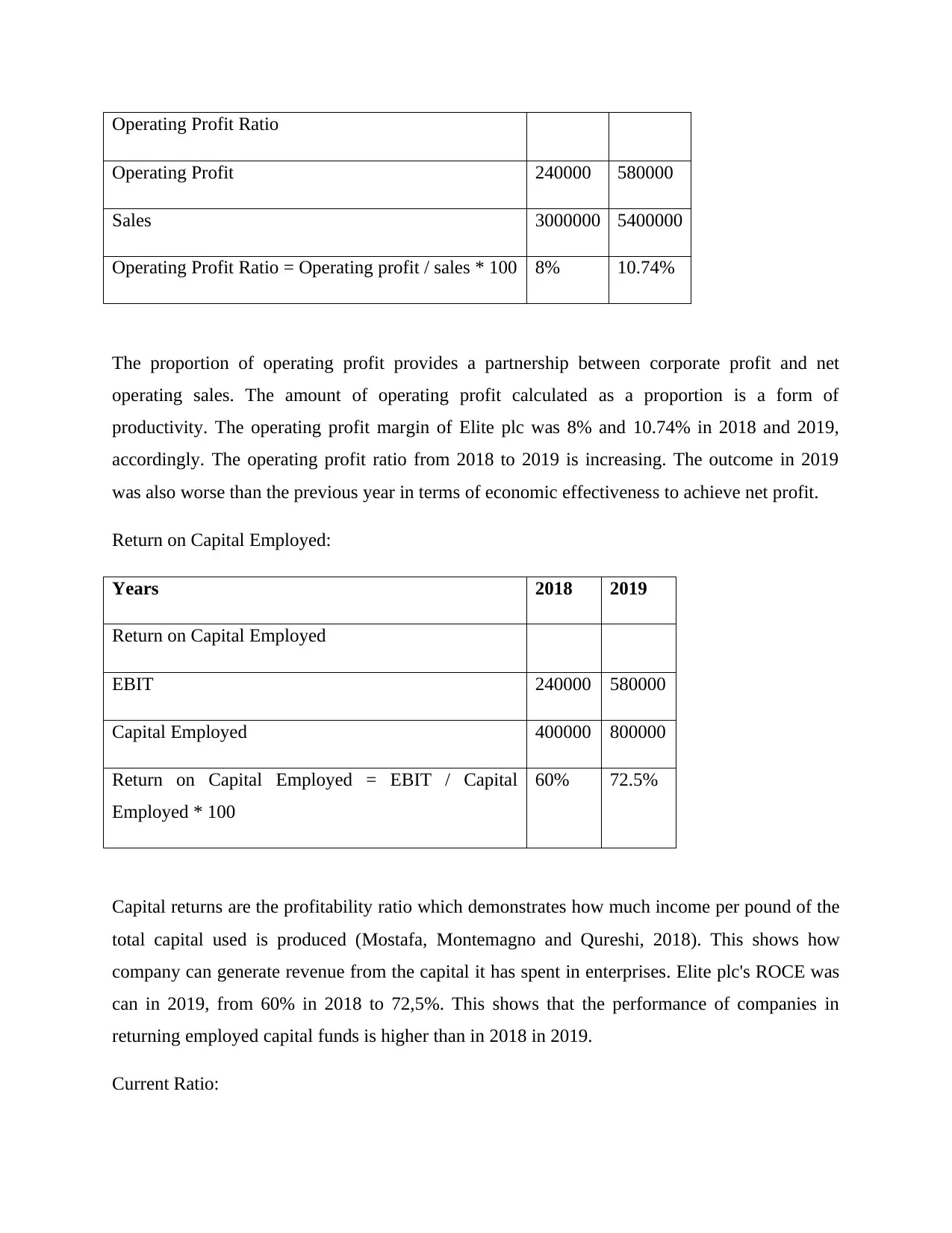

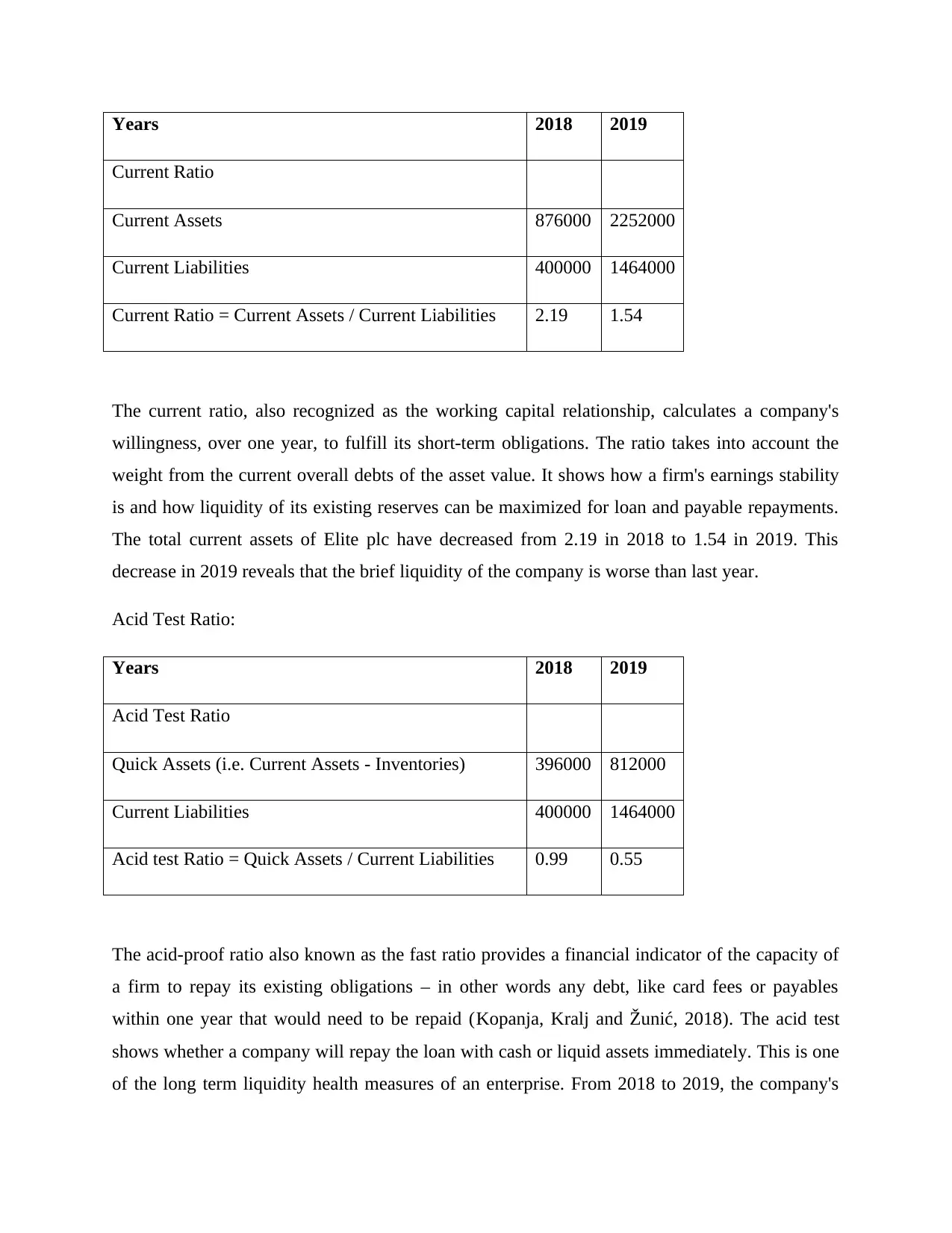

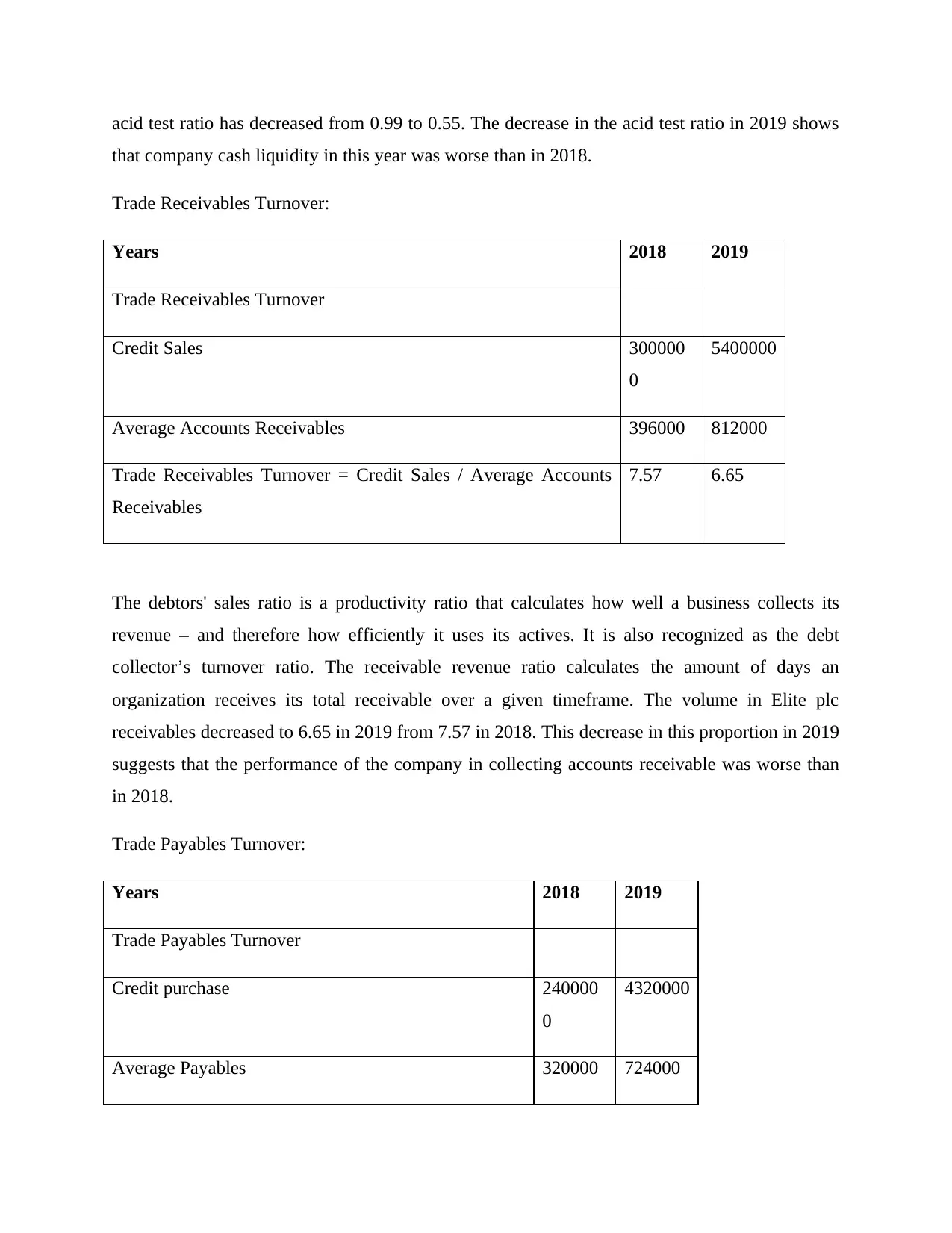

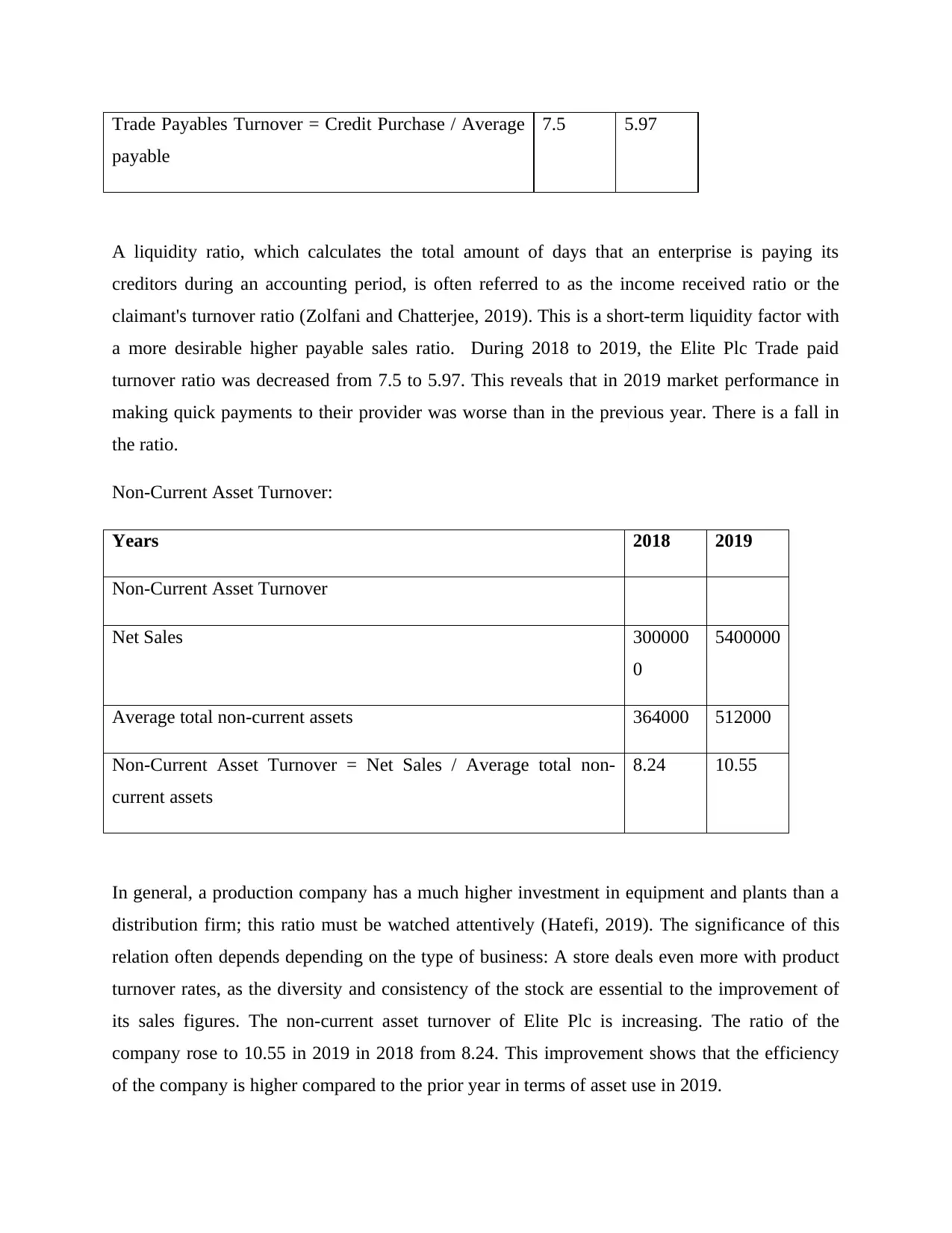

This report presents a financial analysis of Elite plc, focusing on the calculation and interpretation of various financial ratios for the years 2018 and 2019. The analysis includes the computation of gross profit ratio, operating profit ratio, return on capital employed, current ratio, acid test ratio, trade receivables turnover, trade payables turnover, and non-current asset turnover. Each ratio is calculated, and its implications on the company's performance and financial health are discussed. The report highlights trends in profitability, liquidity, and efficiency, providing insights into Elite plc's ability to manage its assets, liabilities, and overall financial standing. Based on the ratio analysis, recommendations are made to senior management, primarily focusing on improving the company's short-term liquidity, enhancing working capital management, and optimizing the collection of receivables and payment of payables. The report concludes with key suggestions for management to improve the overall economic situation of the company, including strategies for better financial control and operational efficiency.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.