In-depth Financial Analysis: Ratios and Statement Preparation

VerifiedAdded on 2023/06/12

|9

|1893

|252

Report

AI Summary

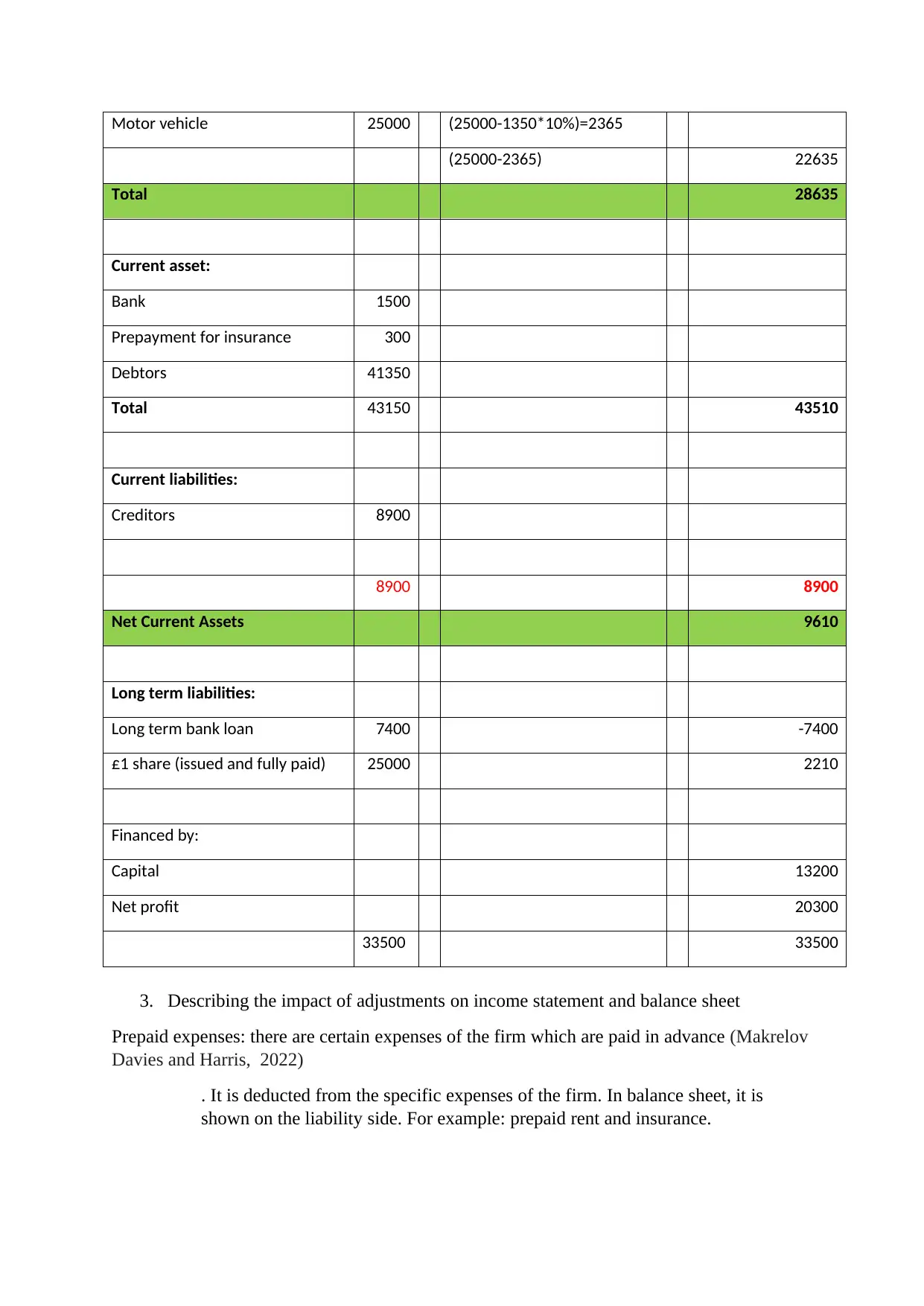

This report provides a comprehensive analysis of financial accounting, divided into two main sections. The first section interprets accounting ratios from 2018 to 2021, including profitability, efficiency, liquidity, and financial structure ratios, using ASOS plc as an example. The second section focuses on preparing an income statement and balance sheet for Ovid Ventures, explaining adjustments for items like prepaid and accrued expenses and income, and detailing the rationale for adding or subtracting items from the cash flow statement, such as depreciation and disposal of non-current assets. The report concludes that financial accounting effectively summarizes business transactions, providing a true view of an organization's financial health.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.