Financial Analysis and Ratio Comparison: Tesco versus Walmart Report

VerifiedAdded on 2023/06/12

|17

|3899

|92

Report

AI Summary

This report provides a detailed financial analysis of Tesco and Walmart, focusing on ratio analysis over four years. It examines profitability, liquidity, gearing, efficiency, and investment ratios for both companies, highlighting their financial strengths and weaknesses. The report emphasizes the importance of working capital examination for decision-making, assessing the ability of each company to cover short-term debts and maintain operational solvency. Furthermore, it includes a critical evaluation of annual cash flow records, drawing conclusions about the financial health and market positioning of Tesco and Walmart. The analysis reveals Tesco's superior efficiency in debt management and overall working capacity compared to Walmart, suggesting it as a potentially more favorable investment option. The report concludes with recommendations for Walmart to improve its market performance and cash flow management. Desklib provides this and many other solved assignments for students.

FINANCIAL

ANALYSIS

MANAGEMENT AND

ENTERPRISE

ANALYSIS

MANAGEMENT AND

ENTERPRISE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.................................................................................................................................................. 3

MAIN BODY........................................................................................................................................................ 3

1. RATIO ANALYSIS OF FINANCIAL RECORDS OF TESCO AND WALMART COMPANY FOR 4 YEARS...................................................3

2. STATE THE NECESSITY AND IMPORTANCE OF EXAMINATION OF WORKING CAPITAL FOR BOTH ORGANISATIONS BEFORE TAKING ANY

DECISIONS................................................................................................................................................................ 10

3. CRITICAL EVALUATION OF ANNUAL CASH FLOW RECORD OF BOTH FIRMS...........................................................................13

CONCLUSION.................................................................................................................................................... 14

REFERENCES..................................................................................................................................................................15

INTRODUCTION.................................................................................................................................................. 3

MAIN BODY........................................................................................................................................................ 3

1. RATIO ANALYSIS OF FINANCIAL RECORDS OF TESCO AND WALMART COMPANY FOR 4 YEARS...................................................3

2. STATE THE NECESSITY AND IMPORTANCE OF EXAMINATION OF WORKING CAPITAL FOR BOTH ORGANISATIONS BEFORE TAKING ANY

DECISIONS................................................................................................................................................................ 10

3. CRITICAL EVALUATION OF ANNUAL CASH FLOW RECORD OF BOTH FIRMS...........................................................................13

CONCLUSION.................................................................................................................................................... 14

REFERENCES..................................................................................................................................................................15

INTRODUCTION

The report prepared above takes in account examination and evaluation of two companies

i.e. Tesco and Walmart. It gives a detailed description related to computation of ratios, financial

records, statements of two organisation chosen (Abdulloevich, 2021). It states necessity towards

analysing the working capital before any decision-making process. It must also include a critical

assessment of cash flow on annual basis and search for evidences that would provide support

towards the arguments expressed. It displays an quality to measure business issues that are

complicated and complex in nature. It also provides recommendation and suggestions in an

autonomous way that rely on informed examination and critical assessment. The report prepared

takes in account calculation of liquidity ratios such as current ratio, quick ratio and in case of

profitability ratios gross profit, operating ratio, operating profit ratio and net profit ratio are

computed. It helps to understand the positioning and solvency of a business in competitive

environment. Assessment of working capital ratio and finding related cash flow generated in

related companies over a period of time helps to understand whether the business is sound or not.

It further serves as a base in decision making for investors and customers that are thinking of

investing in business.

MAIN BODY

1. Ratio analysis of financial records of Tesco and Walmart company for 4 years.

Profitability ratios of Tesco

Gross profit ratio:

Year Formula Calculation Results

2017 (Gross profit/ Net sales)*100 (4098/58091)*1

00

7.05%

2018 (Gross profit/ Net sales)*100 (3352/54141)*1

00

6.19%

2019 (Gross profit/ Net sales)*100 (4144/59767)*1

00

6.93%

2020 (Gross profit/ Net sales)*100 (4889/59871)*1 8.17%

The report prepared above takes in account examination and evaluation of two companies

i.e. Tesco and Walmart. It gives a detailed description related to computation of ratios, financial

records, statements of two organisation chosen (Abdulloevich, 2021). It states necessity towards

analysing the working capital before any decision-making process. It must also include a critical

assessment of cash flow on annual basis and search for evidences that would provide support

towards the arguments expressed. It displays an quality to measure business issues that are

complicated and complex in nature. It also provides recommendation and suggestions in an

autonomous way that rely on informed examination and critical assessment. The report prepared

takes in account calculation of liquidity ratios such as current ratio, quick ratio and in case of

profitability ratios gross profit, operating ratio, operating profit ratio and net profit ratio are

computed. It helps to understand the positioning and solvency of a business in competitive

environment. Assessment of working capital ratio and finding related cash flow generated in

related companies over a period of time helps to understand whether the business is sound or not.

It further serves as a base in decision making for investors and customers that are thinking of

investing in business.

MAIN BODY

1. Ratio analysis of financial records of Tesco and Walmart company for 4 years.

Profitability ratios of Tesco

Gross profit ratio:

Year Formula Calculation Results

2017 (Gross profit/ Net sales)*100 (4098/58091)*1

00

7.05%

2018 (Gross profit/ Net sales)*100 (3352/54141)*1

00

6.19%

2019 (Gross profit/ Net sales)*100 (4144/59767)*1

00

6.93%

2020 (Gross profit/ Net sales)*100 (4889/59871)*1 8.17%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

00

Operating ratio:

Year Formula Calculation Results

2017 (Operating expense/ Net sales)*100 (1885/53015)*1

00

3.55%

2018 (Operating expense/ Net sales)*100 (1513/53015)*1

00

2.79%

2019 (Operating expense/ Net sales)*100 (2010/59215)*1

00

3.39%

2020 (Operating expense/ Net sales)*100 (1884/59871)*1

00

3.15%

Operating profit ratio:

Year Formula Calculation Results

2017 (Operating profit/ Net sales)*100 (1017/53015)*1

00

1.20%

2018 (Operating profit/ Net sales)*100 (1837/54141)*1

00

3.39%

2019 (Operating profit/ Net sales)*100 (2649/59215)*1

00

4.47%

2020 (Operating profit/ Net sales)*100 (2518/60180)*1

00

4.18%

Net profit ratio:

Year Formula Calculation Results

2017 (Net profit/Total revenue)*100 (- -0.10%

Operating ratio:

Year Formula Calculation Results

2017 (Operating expense/ Net sales)*100 (1885/53015)*1

00

3.55%

2018 (Operating expense/ Net sales)*100 (1513/53015)*1

00

2.79%

2019 (Operating expense/ Net sales)*100 (2010/59215)*1

00

3.39%

2020 (Operating expense/ Net sales)*100 (1884/59871)*1

00

3.15%

Operating profit ratio:

Year Formula Calculation Results

2017 (Operating profit/ Net sales)*100 (1017/53015)*1

00

1.20%

2018 (Operating profit/ Net sales)*100 (1837/54141)*1

00

3.39%

2019 (Operating profit/ Net sales)*100 (2649/59215)*1

00

4.47%

2020 (Operating profit/ Net sales)*100 (2518/60180)*1

00

4.18%

Net profit ratio:

Year Formula Calculation Results

2017 (Net profit/Total revenue)*100 (- -0.10%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

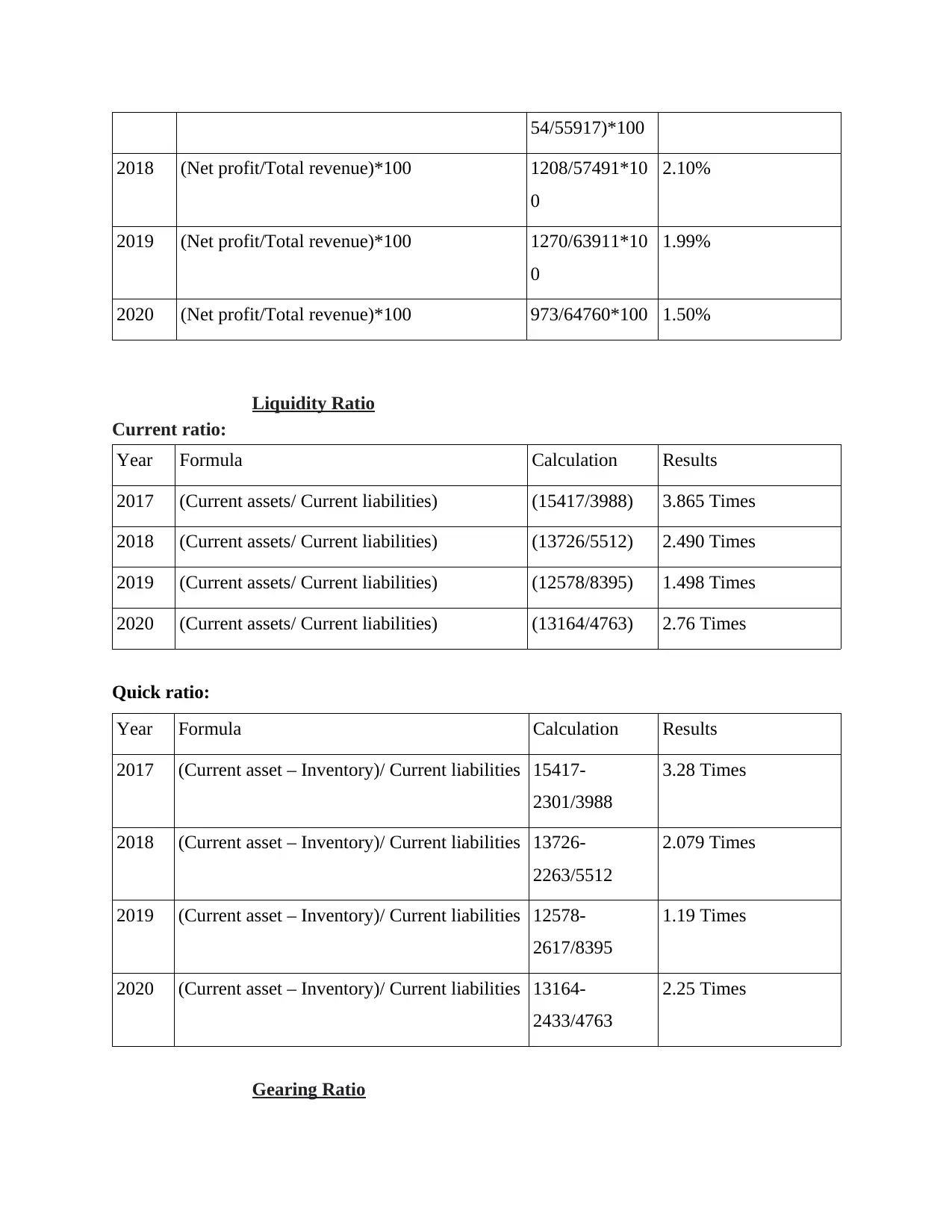

54/55917)*100

2018 (Net profit/Total revenue)*100 1208/57491*10

0

2.10%

2019 (Net profit/Total revenue)*100 1270/63911*10

0

1.99%

2020 (Net profit/Total revenue)*100 973/64760*100 1.50%

Liquidity Ratio

Current ratio:

Year Formula Calculation Results

2017 (Current assets/ Current liabilities) (15417/3988) 3.865 Times

2018 (Current assets/ Current liabilities) (13726/5512) 2.490 Times

2019 (Current assets/ Current liabilities) (12578/8395) 1.498 Times

2020 (Current assets/ Current liabilities) (13164/4763) 2.76 Times

Quick ratio:

Year Formula Calculation Results

2017 (Current asset – Inventory)/ Current liabilities 15417-

2301/3988

3.28 Times

2018 (Current asset – Inventory)/ Current liabilities 13726-

2263/5512

2.079 Times

2019 (Current asset – Inventory)/ Current liabilities 12578-

2617/8395

1.19 Times

2020 (Current asset – Inventory)/ Current liabilities 13164-

2433/4763

2.25 Times

Gearing Ratio

2018 (Net profit/Total revenue)*100 1208/57491*10

0

2.10%

2019 (Net profit/Total revenue)*100 1270/63911*10

0

1.99%

2020 (Net profit/Total revenue)*100 973/64760*100 1.50%

Liquidity Ratio

Current ratio:

Year Formula Calculation Results

2017 (Current assets/ Current liabilities) (15417/3988) 3.865 Times

2018 (Current assets/ Current liabilities) (13726/5512) 2.490 Times

2019 (Current assets/ Current liabilities) (12578/8395) 1.498 Times

2020 (Current assets/ Current liabilities) (13164/4763) 2.76 Times

Quick ratio:

Year Formula Calculation Results

2017 (Current asset – Inventory)/ Current liabilities 15417-

2301/3988

3.28 Times

2018 (Current asset – Inventory)/ Current liabilities 13726-

2263/5512

2.079 Times

2019 (Current asset – Inventory)/ Current liabilities 12578-

2617/8395

1.19 Times

2020 (Current asset – Inventory)/ Current liabilities 13164-

2433/4763

2.25 Times

Gearing Ratio

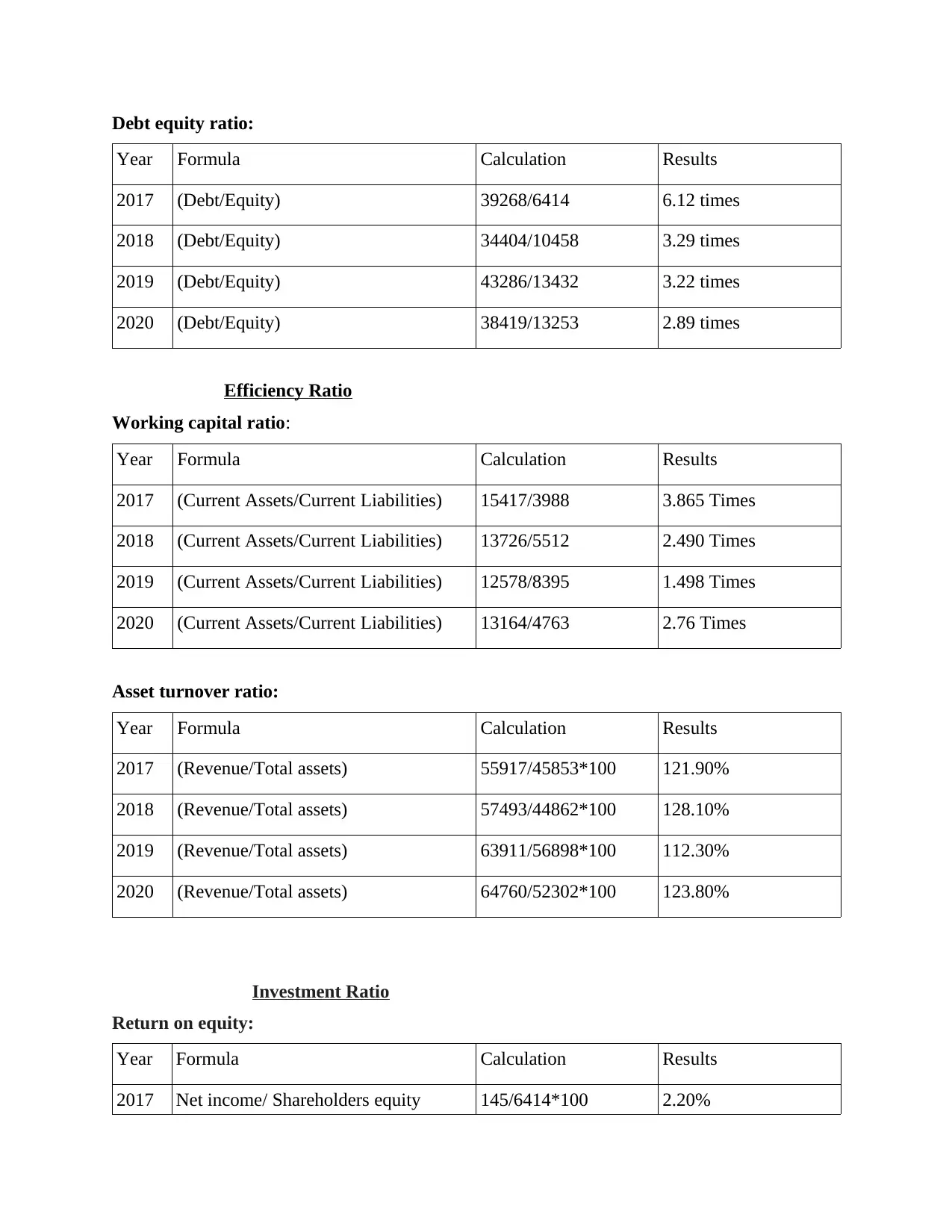

Debt equity ratio:

Year Formula Calculation Results

2017 (Debt/Equity) 39268/6414 6.12 times

2018 (Debt/Equity) 34404/10458 3.29 times

2019 (Debt/Equity) 43286/13432 3.22 times

2020 (Debt/Equity) 38419/13253 2.89 times

Efficiency Ratio

Working capital ratio:

Year Formula Calculation Results

2017 (Current Assets/Current Liabilities) 15417/3988 3.865 Times

2018 (Current Assets/Current Liabilities) 13726/5512 2.490 Times

2019 (Current Assets/Current Liabilities) 12578/8395 1.498 Times

2020 (Current Assets/Current Liabilities) 13164/4763 2.76 Times

Asset turnover ratio:

Year Formula Calculation Results

2017 (Revenue/Total assets) 55917/45853*100 121.90%

2018 (Revenue/Total assets) 57493/44862*100 128.10%

2019 (Revenue/Total assets) 63911/56898*100 112.30%

2020 (Revenue/Total assets) 64760/52302*100 123.80%

Investment Ratio

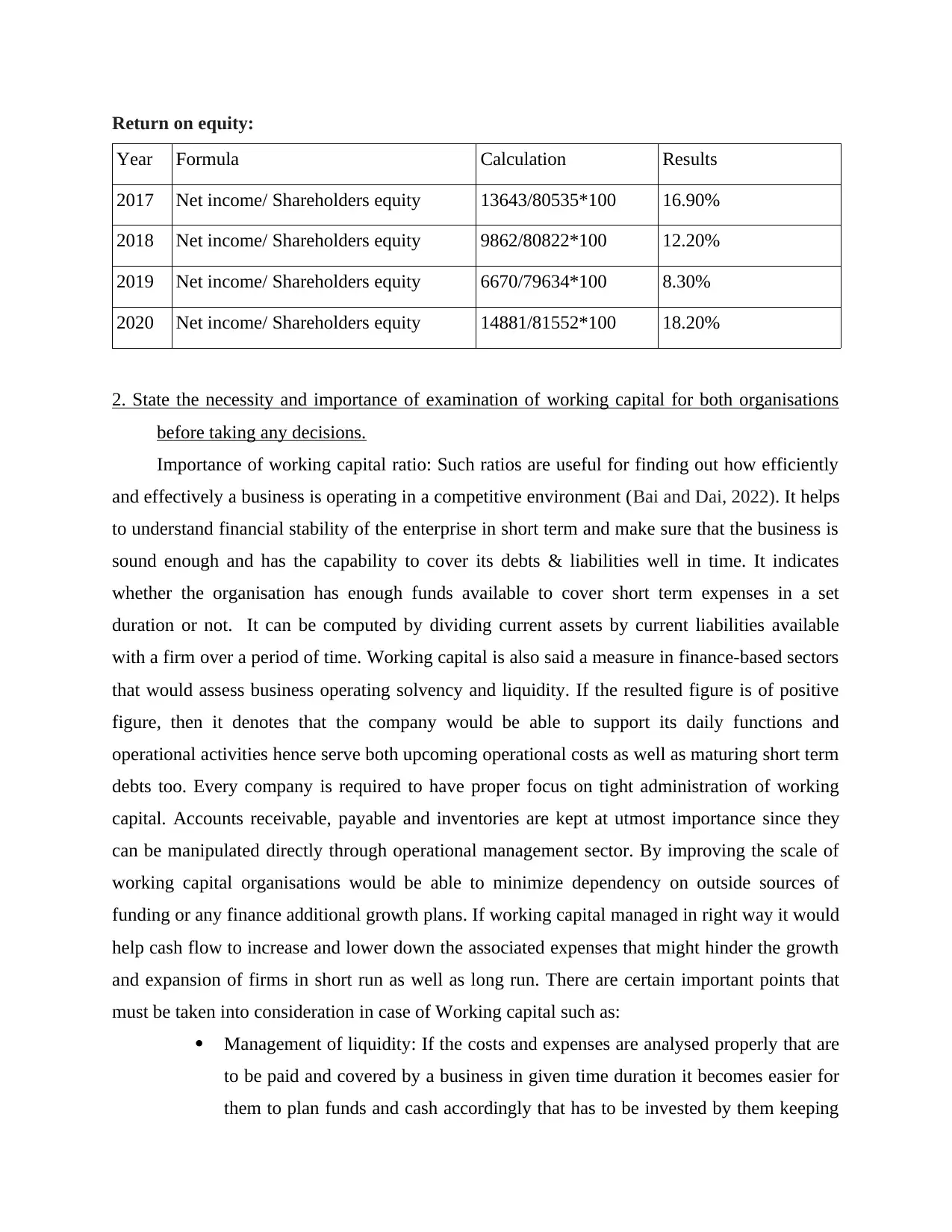

Return on equity:

Year Formula Calculation Results

2017 Net income/ Shareholders equity 145/6414*100 2.20%

Year Formula Calculation Results

2017 (Debt/Equity) 39268/6414 6.12 times

2018 (Debt/Equity) 34404/10458 3.29 times

2019 (Debt/Equity) 43286/13432 3.22 times

2020 (Debt/Equity) 38419/13253 2.89 times

Efficiency Ratio

Working capital ratio:

Year Formula Calculation Results

2017 (Current Assets/Current Liabilities) 15417/3988 3.865 Times

2018 (Current Assets/Current Liabilities) 13726/5512 2.490 Times

2019 (Current Assets/Current Liabilities) 12578/8395 1.498 Times

2020 (Current Assets/Current Liabilities) 13164/4763 2.76 Times

Asset turnover ratio:

Year Formula Calculation Results

2017 (Revenue/Total assets) 55917/45853*100 121.90%

2018 (Revenue/Total assets) 57493/44862*100 128.10%

2019 (Revenue/Total assets) 63911/56898*100 112.30%

2020 (Revenue/Total assets) 64760/52302*100 123.80%

Investment Ratio

Return on equity:

Year Formula Calculation Results

2017 Net income/ Shareholders equity 145/6414*100 2.20%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

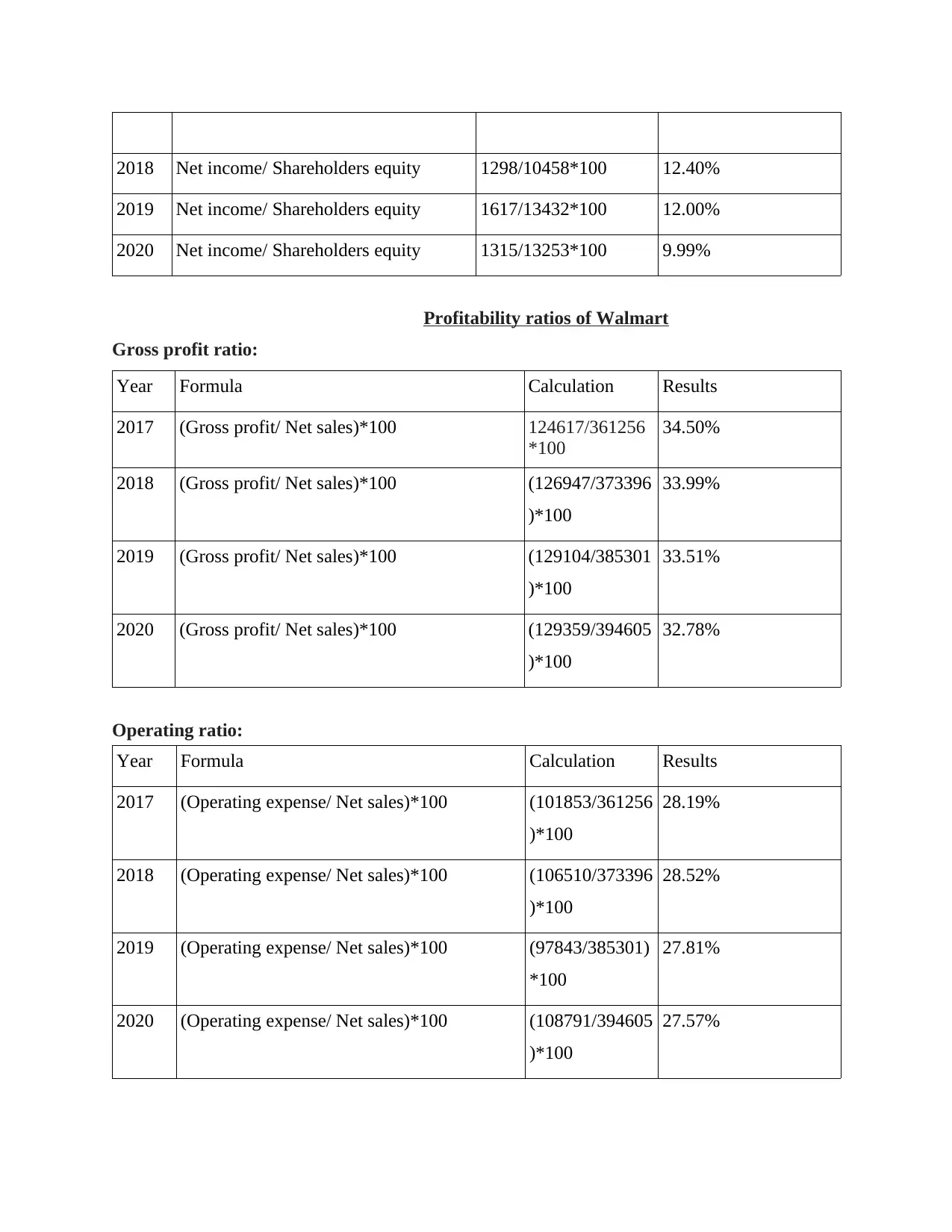

2018 Net income/ Shareholders equity 1298/10458*100 12.40%

2019 Net income/ Shareholders equity 1617/13432*100 12.00%

2020 Net income/ Shareholders equity 1315/13253*100 9.99%

Profitability ratios of Walmart

Gross profit ratio:

Year Formula Calculation Results

2017 (Gross profit/ Net sales)*100 124617/361256

*100

34.50%

2018 (Gross profit/ Net sales)*100 (126947/373396

)*100

33.99%

2019 (Gross profit/ Net sales)*100 (129104/385301

)*100

33.51%

2020 (Gross profit/ Net sales)*100 (129359/394605

)*100

32.78%

Operating ratio:

Year Formula Calculation Results

2017 (Operating expense/ Net sales)*100 (101853/361256

)*100

28.19%

2018 (Operating expense/ Net sales)*100 (106510/373396

)*100

28.52%

2019 (Operating expense/ Net sales)*100 (97843/385301)

*100

27.81%

2020 (Operating expense/ Net sales)*100 (108791/394605

)*100

27.57%

2019 Net income/ Shareholders equity 1617/13432*100 12.00%

2020 Net income/ Shareholders equity 1315/13253*100 9.99%

Profitability ratios of Walmart

Gross profit ratio:

Year Formula Calculation Results

2017 (Gross profit/ Net sales)*100 124617/361256

*100

34.50%

2018 (Gross profit/ Net sales)*100 (126947/373396

)*100

33.99%

2019 (Gross profit/ Net sales)*100 (129104/385301

)*100

33.51%

2020 (Gross profit/ Net sales)*100 (129359/394605

)*100

32.78%

Operating ratio:

Year Formula Calculation Results

2017 (Operating expense/ Net sales)*100 (101853/361256

)*100

28.19%

2018 (Operating expense/ Net sales)*100 (106510/373396

)*100

28.52%

2019 (Operating expense/ Net sales)*100 (97843/385301)

*100

27.81%

2020 (Operating expense/ Net sales)*100 (108791/394605

)*100

27.57%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

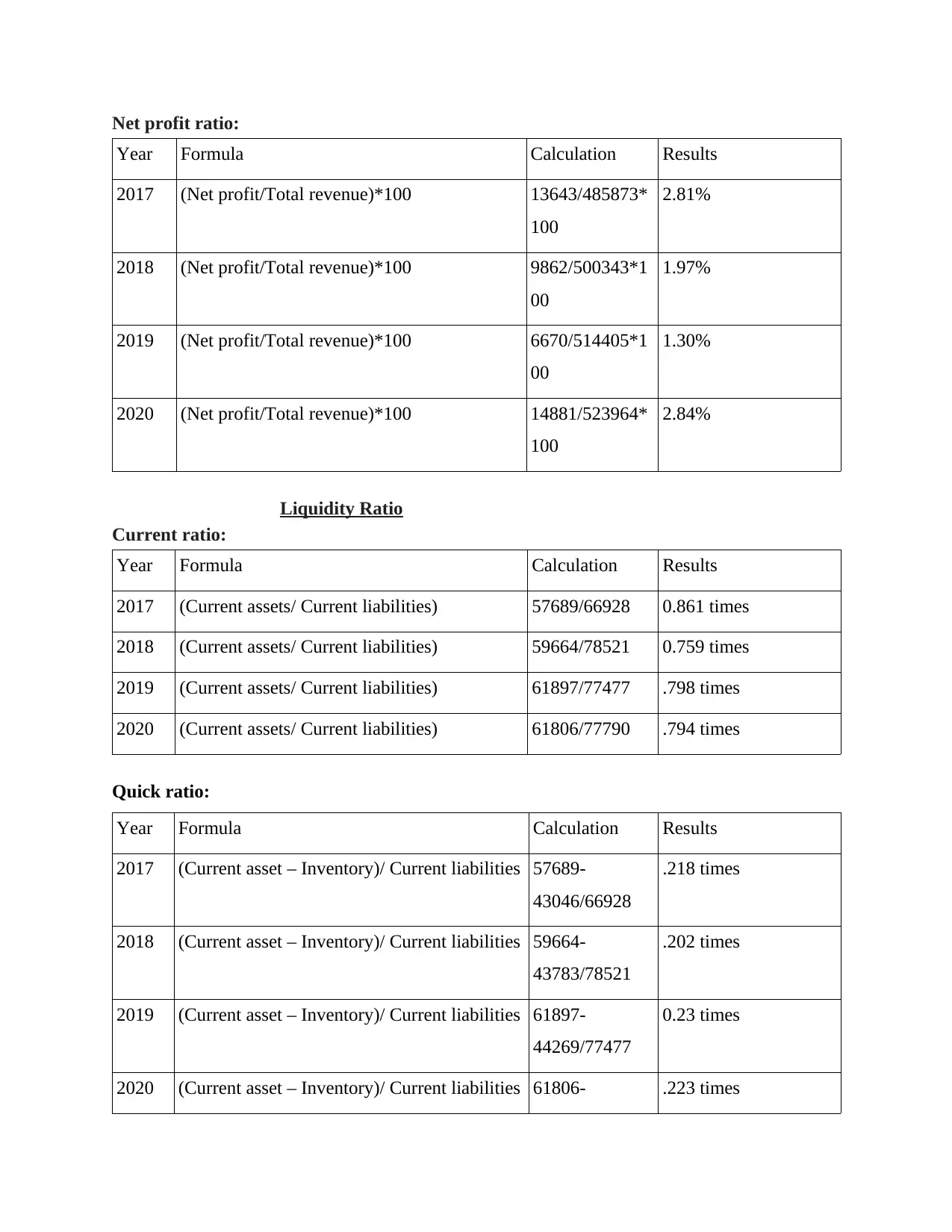

Net profit ratio:

Year Formula Calculation Results

2017 (Net profit/Total revenue)*100 13643/485873*

100

2.81%

2018 (Net profit/Total revenue)*100 9862/500343*1

00

1.97%

2019 (Net profit/Total revenue)*100 6670/514405*1

00

1.30%

2020 (Net profit/Total revenue)*100 14881/523964*

100

2.84%

Liquidity Ratio

Current ratio:

Year Formula Calculation Results

2017 (Current assets/ Current liabilities) 57689/66928 0.861 times

2018 (Current assets/ Current liabilities) 59664/78521 0.759 times

2019 (Current assets/ Current liabilities) 61897/77477 .798 times

2020 (Current assets/ Current liabilities) 61806/77790 .794 times

Quick ratio:

Year Formula Calculation Results

2017 (Current asset – Inventory)/ Current liabilities 57689-

43046/66928

.218 times

2018 (Current asset – Inventory)/ Current liabilities 59664-

43783/78521

.202 times

2019 (Current asset – Inventory)/ Current liabilities 61897-

44269/77477

0.23 times

2020 (Current asset – Inventory)/ Current liabilities 61806- .223 times

Year Formula Calculation Results

2017 (Net profit/Total revenue)*100 13643/485873*

100

2.81%

2018 (Net profit/Total revenue)*100 9862/500343*1

00

1.97%

2019 (Net profit/Total revenue)*100 6670/514405*1

00

1.30%

2020 (Net profit/Total revenue)*100 14881/523964*

100

2.84%

Liquidity Ratio

Current ratio:

Year Formula Calculation Results

2017 (Current assets/ Current liabilities) 57689/66928 0.861 times

2018 (Current assets/ Current liabilities) 59664/78521 0.759 times

2019 (Current assets/ Current liabilities) 61897/77477 .798 times

2020 (Current assets/ Current liabilities) 61806/77790 .794 times

Quick ratio:

Year Formula Calculation Results

2017 (Current asset – Inventory)/ Current liabilities 57689-

43046/66928

.218 times

2018 (Current asset – Inventory)/ Current liabilities 59664-

43783/78521

.202 times

2019 (Current asset – Inventory)/ Current liabilities 61897-

44269/77477

0.23 times

2020 (Current asset – Inventory)/ Current liabilities 61806- .223 times

44435/77790

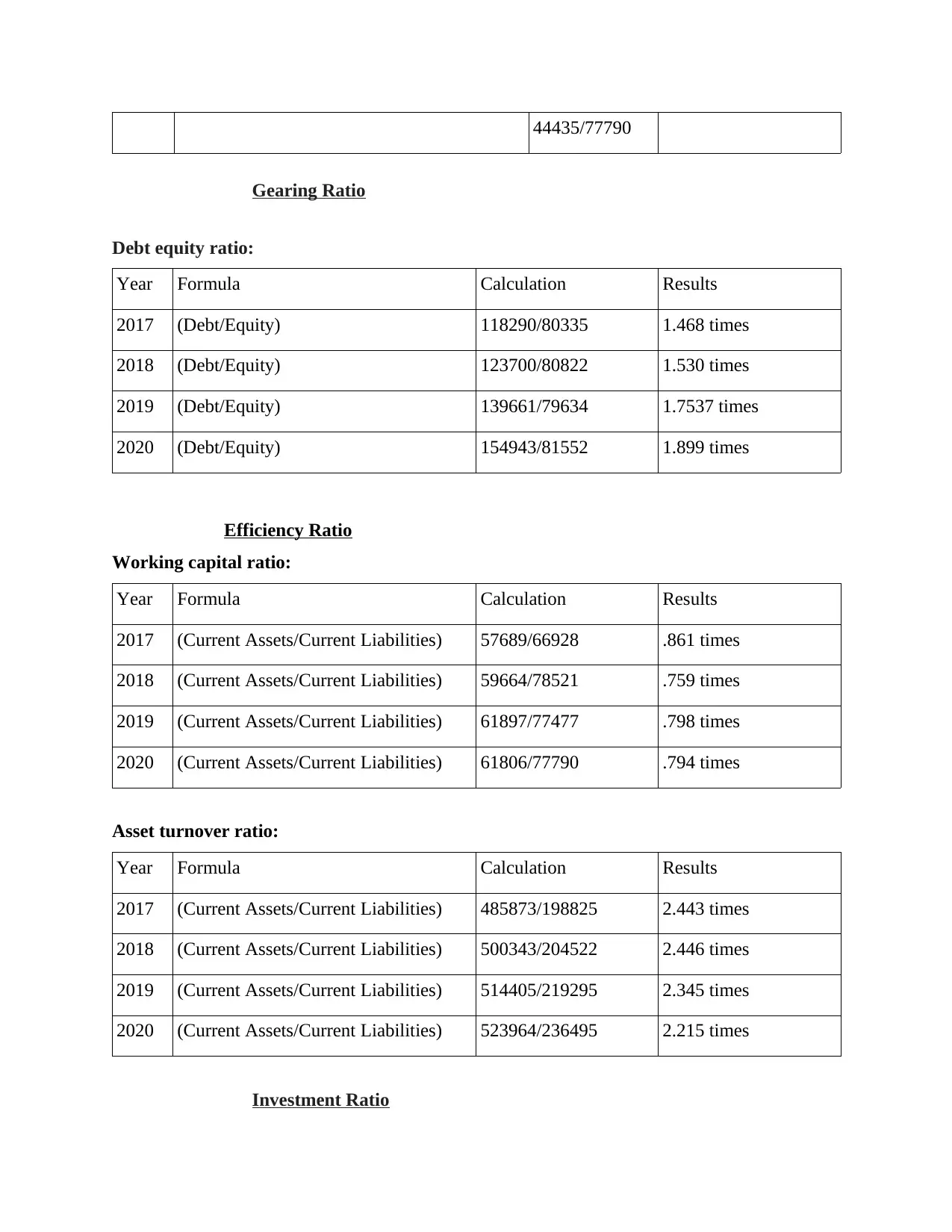

Gearing Ratio

Debt equity ratio:

Year Formula Calculation Results

2017 (Debt/Equity) 118290/80335 1.468 times

2018 (Debt/Equity) 123700/80822 1.530 times

2019 (Debt/Equity) 139661/79634 1.7537 times

2020 (Debt/Equity) 154943/81552 1.899 times

Efficiency Ratio

Working capital ratio:

Year Formula Calculation Results

2017 (Current Assets/Current Liabilities) 57689/66928 .861 times

2018 (Current Assets/Current Liabilities) 59664/78521 .759 times

2019 (Current Assets/Current Liabilities) 61897/77477 .798 times

2020 (Current Assets/Current Liabilities) 61806/77790 .794 times

Asset turnover ratio:

Year Formula Calculation Results

2017 (Current Assets/Current Liabilities) 485873/198825 2.443 times

2018 (Current Assets/Current Liabilities) 500343/204522 2.446 times

2019 (Current Assets/Current Liabilities) 514405/219295 2.345 times

2020 (Current Assets/Current Liabilities) 523964/236495 2.215 times

Investment Ratio

Gearing Ratio

Debt equity ratio:

Year Formula Calculation Results

2017 (Debt/Equity) 118290/80335 1.468 times

2018 (Debt/Equity) 123700/80822 1.530 times

2019 (Debt/Equity) 139661/79634 1.7537 times

2020 (Debt/Equity) 154943/81552 1.899 times

Efficiency Ratio

Working capital ratio:

Year Formula Calculation Results

2017 (Current Assets/Current Liabilities) 57689/66928 .861 times

2018 (Current Assets/Current Liabilities) 59664/78521 .759 times

2019 (Current Assets/Current Liabilities) 61897/77477 .798 times

2020 (Current Assets/Current Liabilities) 61806/77790 .794 times

Asset turnover ratio:

Year Formula Calculation Results

2017 (Current Assets/Current Liabilities) 485873/198825 2.443 times

2018 (Current Assets/Current Liabilities) 500343/204522 2.446 times

2019 (Current Assets/Current Liabilities) 514405/219295 2.345 times

2020 (Current Assets/Current Liabilities) 523964/236495 2.215 times

Investment Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Return on equity:

Year Formula Calculation Results

2017 Net income/ Shareholders equity 13643/80535*100 16.90%

2018 Net income/ Shareholders equity 9862/80822*100 12.20%

2019 Net income/ Shareholders equity 6670/79634*100 8.30%

2020 Net income/ Shareholders equity 14881/81552*100 18.20%

2. State the necessity and importance of examination of working capital for both organisations

before taking any decisions.

Importance of working capital ratio: Such ratios are useful for finding out how efficiently

and effectively a business is operating in a competitive environment (Bai and Dai, 2022). It helps

to understand financial stability of the enterprise in short term and make sure that the business is

sound enough and has the capability to cover its debts & liabilities well in time. It indicates

whether the organisation has enough funds available to cover short term expenses in a set

duration or not. It can be computed by dividing current assets by current liabilities available

with a firm over a period of time. Working capital is also said a measure in finance-based sectors

that would assess business operating solvency and liquidity. If the resulted figure is of positive

figure, then it denotes that the company would be able to support its daily functions and

operational activities hence serve both upcoming operational costs as well as maturing short term

debts too. Every company is required to have proper focus on tight administration of working

capital. Accounts receivable, payable and inventories are kept at utmost importance since they

can be manipulated directly through operational management sector. By improving the scale of

working capital organisations would be able to minimize dependency on outside sources of

funding or any finance additional growth plans. If working capital managed in right way it would

help cash flow to increase and lower down the associated expenses that might hinder the growth

and expansion of firms in short run as well as long run. There are certain important points that

must be taken into consideration in case of Working capital such as:

Management of liquidity: If the costs and expenses are analysed properly that are

to be paid and covered by a business in given time duration it becomes easier for

them to plan funds and cash accordingly that has to be invested by them keeping

Year Formula Calculation Results

2017 Net income/ Shareholders equity 13643/80535*100 16.90%

2018 Net income/ Shareholders equity 9862/80822*100 12.20%

2019 Net income/ Shareholders equity 6670/79634*100 8.30%

2020 Net income/ Shareholders equity 14881/81552*100 18.20%

2. State the necessity and importance of examination of working capital for both organisations

before taking any decisions.

Importance of working capital ratio: Such ratios are useful for finding out how efficiently

and effectively a business is operating in a competitive environment (Bai and Dai, 2022). It helps

to understand financial stability of the enterprise in short term and make sure that the business is

sound enough and has the capability to cover its debts & liabilities well in time. It indicates

whether the organisation has enough funds available to cover short term expenses in a set

duration or not. It can be computed by dividing current assets by current liabilities available

with a firm over a period of time. Working capital is also said a measure in finance-based sectors

that would assess business operating solvency and liquidity. If the resulted figure is of positive

figure, then it denotes that the company would be able to support its daily functions and

operational activities hence serve both upcoming operational costs as well as maturing short term

debts too. Every company is required to have proper focus on tight administration of working

capital. Accounts receivable, payable and inventories are kept at utmost importance since they

can be manipulated directly through operational management sector. By improving the scale of

working capital organisations would be able to minimize dependency on outside sources of

funding or any finance additional growth plans. If working capital managed in right way it would

help cash flow to increase and lower down the associated expenses that might hinder the growth

and expansion of firms in short run as well as long run. There are certain important points that

must be taken into consideration in case of Working capital such as:

Management of liquidity: If the costs and expenses are analysed properly that are

to be paid and covered by a business in given time duration it becomes easier for

them to plan funds and cash accordingly that has to be invested by them keeping

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

future situations in mind. Liquidity denotes the cash and funds collected by a

business over a period of time and how they can be used for better functioning of

a firm. Managing liquidity states that the firm is able to use its available funds in

such a way that it proves to be source of income and not threat (Chen and

Metawa, 2020).

Serves as a tool in better decision making: By examining what are the

requirements demanded by a company on daily or frequent basis finance team can

manage related funds and search ways that would help to generate more. If any

investor or client is thinking or making its mind for investing its savings in a

certain company in a set duration then he or she must go through its financial

records and ratios before taking any decisions as it would prove to be riskier for

them in long run.

Adds value in the business: As it is evident and well known that management

focus on managing day to day requirement of funds that would be useful to cover

outstanding expenses and add goodwill towards the organisation to generate short

term revenues. Adding value depicts that it would help to increase valuation of

assets in market and rise prices of shares of company in competitive environment.

Good market image of enterprise: It is considered as the easiest and simplest

method for creating a good reputation and image in eye of people associated with

the business. It also helps companies to get contracts due to its good image and

fulfilment of commitments on time. In present scenario it is well known that

people prefer firms who possess a good and strong market position and picture.

Improvement in credit worth of company: At the time of proper planning of work-

related needs and wants working capital act as a tool and it is assumed that they

would be paying their linked vendors and suppliers that would improve their

worth and help them to get cash fund whenever needed. Credit worth states that it

is able to cover its credit or debt and process borrowings from market without any

obstacle when in need due to its goof brand image and working in marketplace

(Dokiienko, 2021).

Working capital in case of Tesco and Walmart:

business over a period of time and how they can be used for better functioning of

a firm. Managing liquidity states that the firm is able to use its available funds in

such a way that it proves to be source of income and not threat (Chen and

Metawa, 2020).

Serves as a tool in better decision making: By examining what are the

requirements demanded by a company on daily or frequent basis finance team can

manage related funds and search ways that would help to generate more. If any

investor or client is thinking or making its mind for investing its savings in a

certain company in a set duration then he or she must go through its financial

records and ratios before taking any decisions as it would prove to be riskier for

them in long run.

Adds value in the business: As it is evident and well known that management

focus on managing day to day requirement of funds that would be useful to cover

outstanding expenses and add goodwill towards the organisation to generate short

term revenues. Adding value depicts that it would help to increase valuation of

assets in market and rise prices of shares of company in competitive environment.

Good market image of enterprise: It is considered as the easiest and simplest

method for creating a good reputation and image in eye of people associated with

the business. It also helps companies to get contracts due to its good image and

fulfilment of commitments on time. In present scenario it is well known that

people prefer firms who possess a good and strong market position and picture.

Improvement in credit worth of company: At the time of proper planning of work-

related needs and wants working capital act as a tool and it is assumed that they

would be paying their linked vendors and suppliers that would improve their

worth and help them to get cash fund whenever needed. Credit worth states that it

is able to cover its credit or debt and process borrowings from market without any

obstacle when in need due to its goof brand image and working in marketplace

(Dokiienko, 2021).

Working capital in case of Tesco and Walmart:

Working capital ratio calculated for year 2019 and 2020 recorded as .798 and .794 in case

of Walmart whereas in case of Tesco it gave a result of 1.498 and 2.76. It is clear that Tesco has

more efficiency for paying back its debts and liabilities. It is also evident that it holds more assets

as compared to liabilities in own case as well as in other related company case as well. It thus

helps to understand that effectiveness and working capacity of Tesco is more than other

respective organisation. Thus, it would be beneficial in view point of investor to put its money in

carrying out better results and for generating enough cash from firm. Working capital is useful

for generating and betterment of cash flow records and statements thus in near future it would

prove to be a better option for others to get linked with the business. Tesco hold more liquidity

and profitability in competitive market and has more competitive market image when compared

to Walmart. Thus, it is recommended to Walmart that it must focus on improving its

performance in market and carry out expected results that would help it to grow and expand

(Dong, 2022).

Working capital serves as a tool in decision making:

Yes, it is true that it is a large base for facilitating decisions on the basis of

computed working capital ratio as it provides an idea about how the better

functions are being managed in a enterprise. There are times when a consumer or

investor is confused between two companies having good market value but is

unaware about real working of business in market over a period of time thus it is

required to compute related ratios that would serve as a guide for making

decisions whether to invest in a business or not.

It helps to provide an idea whether to invest or not in a company by going through

its computed ratios over a period of time.

It helps to understand profitability and liquidity positioning of a company in

market.

It also provides an idea about assets being purchased and sold. It is useful for

understanding what amount of debts are to be covered and liabilities that must be

set off.

IT helps to get an idea about revenue and income being processed by a company.

It also helps to understand its financial stability of fighting and sustaining in the

market.

of Walmart whereas in case of Tesco it gave a result of 1.498 and 2.76. It is clear that Tesco has

more efficiency for paying back its debts and liabilities. It is also evident that it holds more assets

as compared to liabilities in own case as well as in other related company case as well. It thus

helps to understand that effectiveness and working capacity of Tesco is more than other

respective organisation. Thus, it would be beneficial in view point of investor to put its money in

carrying out better results and for generating enough cash from firm. Working capital is useful

for generating and betterment of cash flow records and statements thus in near future it would

prove to be a better option for others to get linked with the business. Tesco hold more liquidity

and profitability in competitive market and has more competitive market image when compared

to Walmart. Thus, it is recommended to Walmart that it must focus on improving its

performance in market and carry out expected results that would help it to grow and expand

(Dong, 2022).

Working capital serves as a tool in decision making:

Yes, it is true that it is a large base for facilitating decisions on the basis of

computed working capital ratio as it provides an idea about how the better

functions are being managed in a enterprise. There are times when a consumer or

investor is confused between two companies having good market value but is

unaware about real working of business in market over a period of time thus it is

required to compute related ratios that would serve as a guide for making

decisions whether to invest in a business or not.

It helps to provide an idea whether to invest or not in a company by going through

its computed ratios over a period of time.

It helps to understand profitability and liquidity positioning of a company in

market.

It also provides an idea about assets being purchased and sold. It is useful for

understanding what amount of debts are to be covered and liabilities that must be

set off.

IT helps to get an idea about revenue and income being processed by a company.

It also helps to understand its financial stability of fighting and sustaining in the

market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.