Financial Analysis: Ratio Calculation and Breakeven Point Analysis

VerifiedAdded on 2023/06/04

|18

|4582

|250

Homework Assignment

AI Summary

This document presents a comprehensive solution to a finance assignment. It begins with an introduction to finance, defining its core concepts and evolution. The assignment then delves into detailed financial ratio analysis, calculating and interpreting various ratios such as gross profit margin, asset usage, current ratio, acid test ratio, inventory holding period, and debt-to-equity ratio for Liverton Co. for the years ending 2019 and 2018. The importance of financial statements for both external and internal users is also discussed. Furthermore, the solution includes a cash budget for Sassy Clothing, addressing the company's financial position and strategies for improvement. The assignment proceeds to calculate breakeven points in units and sales revenue for 2019 and 2020, along with margin of safety calculations. Finally, the document covers capital budgeting techniques including payback period, accounting rate of return, and net present value, offering a complete financial analysis.

Introduction to

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1..................................................................................................................................3

QUESTION 2..................................................................................................................................6

(c) Explanation of additional expenditures.............................................................................8

QUESTION 3..................................................................................................................................8

(a) Calculate the breakeven point in units and sales revenue for the year ended 31 March

2019 and the year ended 31 March 2020.................................................................................8

(b) Calculate the margin of safety in units and sales revenue for the year 2019 and 2020.

...................................................................................................................................................10

(c) Discuss the new strategy developed by Jessica................................................................10

QUESTION 4................................................................................................................................10

(a)Payback period....................................................................................................................10

Accounting rate of return.......................................................................................................11

Net present value......................................................................................................................13

(b) Project A should be undertaken.......................................................................................14

(c) Capital appraisal technique: -...........................................................................................14

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

QUESTION 1..................................................................................................................................3

QUESTION 2..................................................................................................................................6

(c) Explanation of additional expenditures.............................................................................8

QUESTION 3..................................................................................................................................8

(a) Calculate the breakeven point in units and sales revenue for the year ended 31 March

2019 and the year ended 31 March 2020.................................................................................8

(b) Calculate the margin of safety in units and sales revenue for the year 2019 and 2020.

...................................................................................................................................................10

(c) Discuss the new strategy developed by Jessica................................................................10

QUESTION 4................................................................................................................................10

(a)Payback period....................................................................................................................10

Accounting rate of return.......................................................................................................11

Net present value......................................................................................................................13

(b) Project A should be undertaken.......................................................................................14

(c) Capital appraisal technique: -...........................................................................................14

REFERENCES..............................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance can be defined as the system of exchange amongst the various borrowers, lenders

and investors. It involves various complexities, as it operates at various levels in various

organisations globally. In finance the medium of exchange that are used can be money, credit

and finance. The concept of finance has been there in the global economy for a very long time

that is since 20th century. Earlier the financial function was more inclined towards arranging

funds from the financial institutions through shares and debentures. It transformed and changed

with an emphasis on day to day activities. It came with fund analysis in a very regularised

manner rather than casual basis. Final phase of transition of the financial function involved the

emphasis over growth of business and thus this increased the competition in the economy. In this

particular phase the economy is more inclined towards financing all that needs finance and do

not follow stereotyped financing.(Adegboye, and Iweriebor, 2018)

In the following assessment we will try to study various ratios that are used to study the

health of the business. Importance and working of various financial statements, break even point,

pay back period, various rates of return, etc.

QUESTION 1.

(a) Calculation of the financial ratios

i) Gross profit margin

Gross profit margin = ( Sales – COGS)*100 / Sales

Sales for the year ending 2019= 3,495

COGS for the year ending 2019= 2,182

Gross profit margin for the year ending 2019 = ( 3,495 – 2,182)*100 / 3,495

= 37.56%

Interpretation : Gross profit margin indicates the share of gross profit out of the total revenues

of a company and so for the purpose it considers gross profit over net. The ideal percentage for

the same is 50% - 70% . Liverton Co. is having a gross profit margin of around 37.56% which

shows that it still has the potential to improvise on its profits. This can be done probably by

increasing the selling price of the products and services or by decreasing the cost of goods sold.

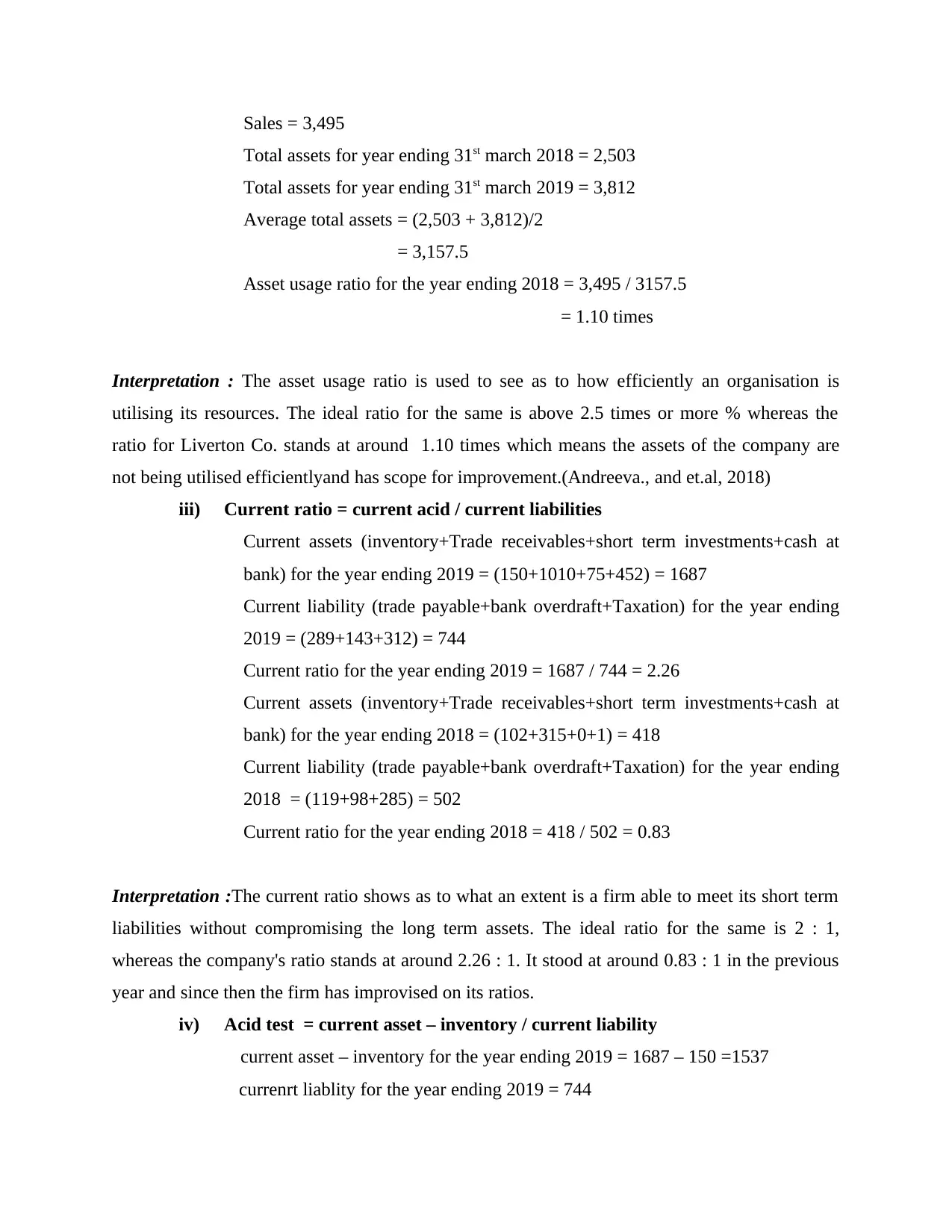

ii)Asset usage = ( net sales / average total assets)

Finance can be defined as the system of exchange amongst the various borrowers, lenders

and investors. It involves various complexities, as it operates at various levels in various

organisations globally. In finance the medium of exchange that are used can be money, credit

and finance. The concept of finance has been there in the global economy for a very long time

that is since 20th century. Earlier the financial function was more inclined towards arranging

funds from the financial institutions through shares and debentures. It transformed and changed

with an emphasis on day to day activities. It came with fund analysis in a very regularised

manner rather than casual basis. Final phase of transition of the financial function involved the

emphasis over growth of business and thus this increased the competition in the economy. In this

particular phase the economy is more inclined towards financing all that needs finance and do

not follow stereotyped financing.(Adegboye, and Iweriebor, 2018)

In the following assessment we will try to study various ratios that are used to study the

health of the business. Importance and working of various financial statements, break even point,

pay back period, various rates of return, etc.

QUESTION 1.

(a) Calculation of the financial ratios

i) Gross profit margin

Gross profit margin = ( Sales – COGS)*100 / Sales

Sales for the year ending 2019= 3,495

COGS for the year ending 2019= 2,182

Gross profit margin for the year ending 2019 = ( 3,495 – 2,182)*100 / 3,495

= 37.56%

Interpretation : Gross profit margin indicates the share of gross profit out of the total revenues

of a company and so for the purpose it considers gross profit over net. The ideal percentage for

the same is 50% - 70% . Liverton Co. is having a gross profit margin of around 37.56% which

shows that it still has the potential to improvise on its profits. This can be done probably by

increasing the selling price of the products and services or by decreasing the cost of goods sold.

ii)Asset usage = ( net sales / average total assets)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales = 3,495

Total assets for year ending 31st march 2018 = 2,503

Total assets for year ending 31st march 2019 = 3,812

Average total assets = (2,503 + 3,812)/2

= 3,157.5

Asset usage ratio for the year ending 2018 = 3,495 / 3157.5

= 1.10 times

Interpretation : The asset usage ratio is used to see as to how efficiently an organisation is

utilising its resources. The ideal ratio for the same is above 2.5 times or more % whereas the

ratio for Liverton Co. stands at around 1.10 times which means the assets of the company are

not being utilised efficientlyand has scope for improvement.(Andreeva., and et.al, 2018)

iii) Current ratio = current acid / current liabilities

Current assets (inventory+Trade receivables+short term investments+cash at

bank) for the year ending 2019 = (150+1010+75+452) = 1687

Current liability (trade payable+bank overdraft+Taxation) for the year ending

2019 = (289+143+312) = 744

Current ratio for the year ending 2019 = 1687 / 744 = 2.26

Current assets (inventory+Trade receivables+short term investments+cash at

bank) for the year ending 2018 = (102+315+0+1) = 418

Current liability (trade payable+bank overdraft+Taxation) for the year ending

2018 = (119+98+285) = 502

Current ratio for the year ending 2018 = 418 / 502 = 0.83

Interpretation :The current ratio shows as to what an extent is a firm able to meet its short term

liabilities without compromising the long term assets. The ideal ratio for the same is 2 : 1,

whereas the company's ratio stands at around 2.26 : 1. It stood at around 0.83 : 1 in the previous

year and since then the firm has improvised on its ratios.

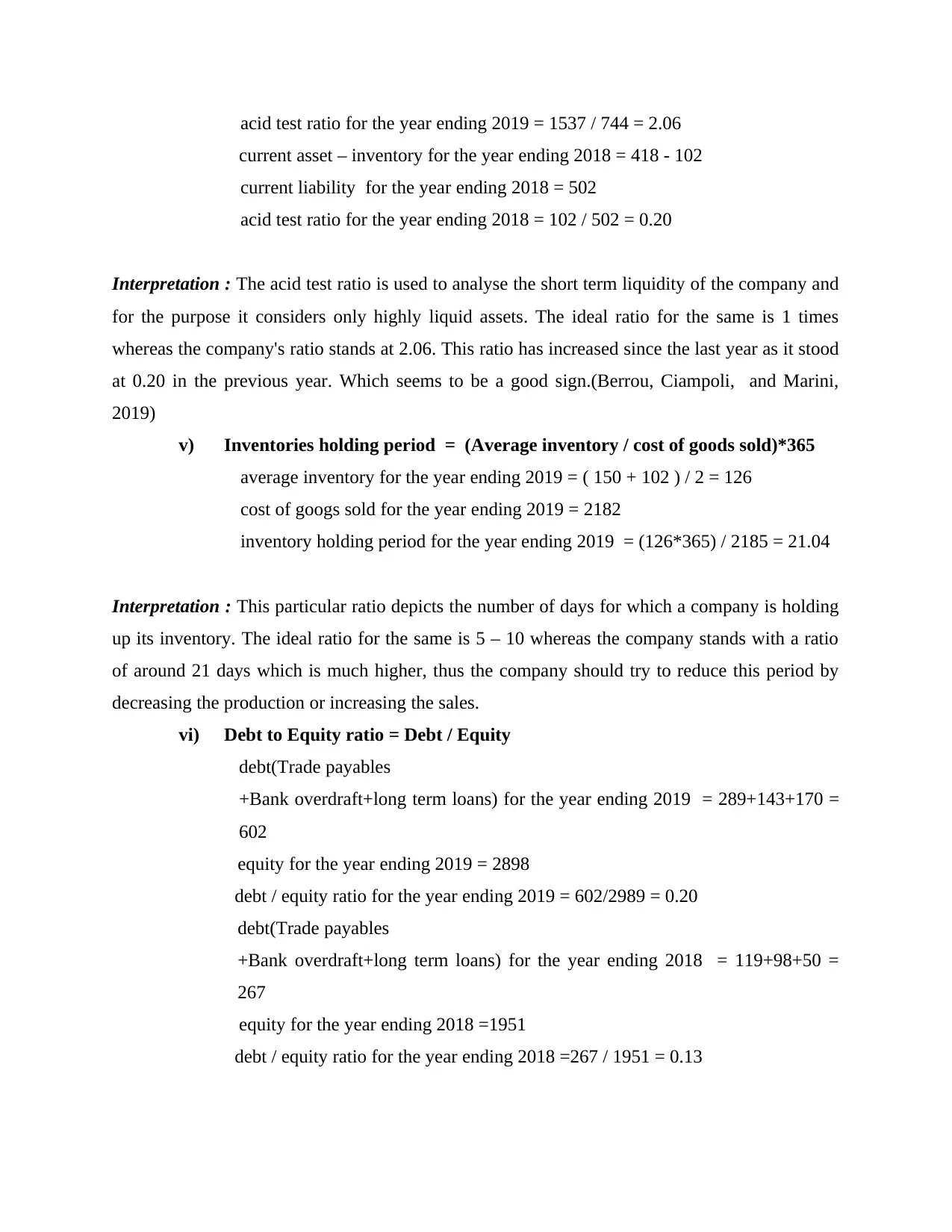

iv) Acid test = current asset – inventory / current liability

current asset – inventory for the year ending 2019 = 1687 – 150 =1537

currenrt liablity for the year ending 2019 = 744

Total assets for year ending 31st march 2018 = 2,503

Total assets for year ending 31st march 2019 = 3,812

Average total assets = (2,503 + 3,812)/2

= 3,157.5

Asset usage ratio for the year ending 2018 = 3,495 / 3157.5

= 1.10 times

Interpretation : The asset usage ratio is used to see as to how efficiently an organisation is

utilising its resources. The ideal ratio for the same is above 2.5 times or more % whereas the

ratio for Liverton Co. stands at around 1.10 times which means the assets of the company are

not being utilised efficientlyand has scope for improvement.(Andreeva., and et.al, 2018)

iii) Current ratio = current acid / current liabilities

Current assets (inventory+Trade receivables+short term investments+cash at

bank) for the year ending 2019 = (150+1010+75+452) = 1687

Current liability (trade payable+bank overdraft+Taxation) for the year ending

2019 = (289+143+312) = 744

Current ratio for the year ending 2019 = 1687 / 744 = 2.26

Current assets (inventory+Trade receivables+short term investments+cash at

bank) for the year ending 2018 = (102+315+0+1) = 418

Current liability (trade payable+bank overdraft+Taxation) for the year ending

2018 = (119+98+285) = 502

Current ratio for the year ending 2018 = 418 / 502 = 0.83

Interpretation :The current ratio shows as to what an extent is a firm able to meet its short term

liabilities without compromising the long term assets. The ideal ratio for the same is 2 : 1,

whereas the company's ratio stands at around 2.26 : 1. It stood at around 0.83 : 1 in the previous

year and since then the firm has improvised on its ratios.

iv) Acid test = current asset – inventory / current liability

current asset – inventory for the year ending 2019 = 1687 – 150 =1537

currenrt liablity for the year ending 2019 = 744

acid test ratio for the year ending 2019 = 1537 / 744 = 2.06

current asset – inventory for the year ending 2018 = 418 - 102

current liability for the year ending 2018 = 502

acid test ratio for the year ending 2018 = 102 / 502 = 0.20

Interpretation : The acid test ratio is used to analyse the short term liquidity of the company and

for the purpose it considers only highly liquid assets. The ideal ratio for the same is 1 times

whereas the company's ratio stands at 2.06. This ratio has increased since the last year as it stood

at 0.20 in the previous year. Which seems to be a good sign.(Berrou, Ciampoli, and Marini,

2019)

v) Inventories holding period = (Average inventory / cost of goods sold)*365

average inventory for the year ending 2019 = ( 150 + 102 ) / 2 = 126

cost of googs sold for the year ending 2019 = 2182

inventory holding period for the year ending 2019 = (126*365) / 2185 = 21.04

Interpretation : This particular ratio depicts the number of days for which a company is holding

up its inventory. The ideal ratio for the same is 5 – 10 whereas the company stands with a ratio

of around 21 days which is much higher, thus the company should try to reduce this period by

decreasing the production or increasing the sales.

vi) Debt to Equity ratio = Debt / Equity

debt(Trade payables

+Bank overdraft+long term loans) for the year ending 2019 = 289+143+170 =

602

equity for the year ending 2019 = 2898

debt / equity ratio for the year ending 2019 = 602/2989 = 0.20

debt(Trade payables

+Bank overdraft+long term loans) for the year ending 2018 = 119+98+50 =

267

equity for the year ending 2018 =1951

debt / equity ratio for the year ending 2018 =267 / 1951 = 0.13

current asset – inventory for the year ending 2018 = 418 - 102

current liability for the year ending 2018 = 502

acid test ratio for the year ending 2018 = 102 / 502 = 0.20

Interpretation : The acid test ratio is used to analyse the short term liquidity of the company and

for the purpose it considers only highly liquid assets. The ideal ratio for the same is 1 times

whereas the company's ratio stands at 2.06. This ratio has increased since the last year as it stood

at 0.20 in the previous year. Which seems to be a good sign.(Berrou, Ciampoli, and Marini,

2019)

v) Inventories holding period = (Average inventory / cost of goods sold)*365

average inventory for the year ending 2019 = ( 150 + 102 ) / 2 = 126

cost of googs sold for the year ending 2019 = 2182

inventory holding period for the year ending 2019 = (126*365) / 2185 = 21.04

Interpretation : This particular ratio depicts the number of days for which a company is holding

up its inventory. The ideal ratio for the same is 5 – 10 whereas the company stands with a ratio

of around 21 days which is much higher, thus the company should try to reduce this period by

decreasing the production or increasing the sales.

vi) Debt to Equity ratio = Debt / Equity

debt(Trade payables

+Bank overdraft+long term loans) for the year ending 2019 = 289+143+170 =

602

equity for the year ending 2019 = 2898

debt / equity ratio for the year ending 2019 = 602/2989 = 0.20

debt(Trade payables

+Bank overdraft+long term loans) for the year ending 2018 = 119+98+50 =

267

equity for the year ending 2018 =1951

debt / equity ratio for the year ending 2018 =267 / 1951 = 0.13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

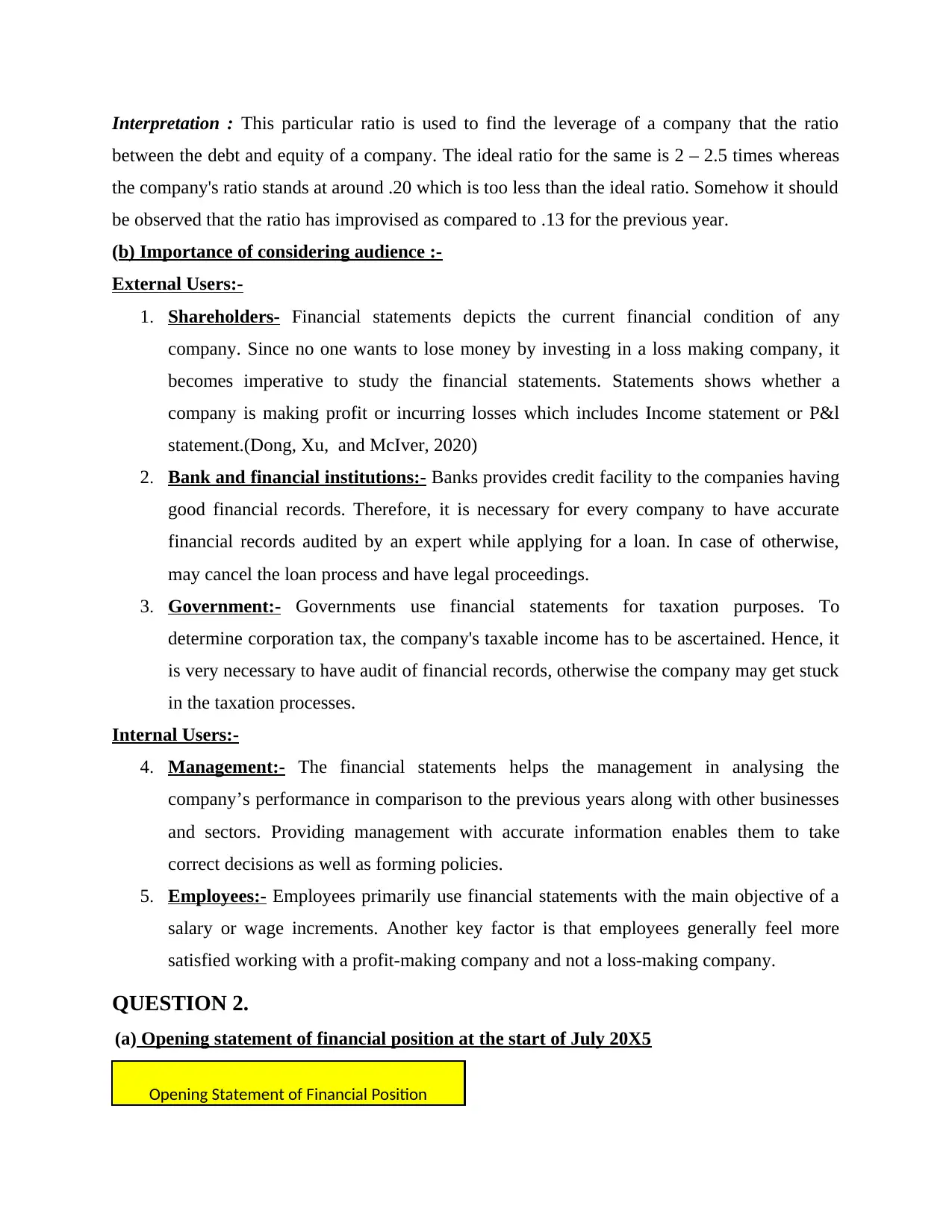

Interpretation : This particular ratio is used to find the leverage of a company that the ratio

between the debt and equity of a company. The ideal ratio for the same is 2 – 2.5 times whereas

the company's ratio stands at around .20 which is too less than the ideal ratio. Somehow it should

be observed that the ratio has improvised as compared to .13 for the previous year.

(b) Importance of considering audience :-

External Users:-

1. Shareholders- Financial statements depicts the current financial condition of any

company. Since no one wants to lose money by investing in a loss making company, it

becomes imperative to study the financial statements. Statements shows whether a

company is making profit or incurring losses which includes Income statement or P&l

statement.(Dong, Xu, and McIver, 2020)

2. Bank and financial institutions:- Banks provides credit facility to the companies having

good financial records. Therefore, it is necessary for every company to have accurate

financial records audited by an expert while applying for a loan. In case of otherwise,

may cancel the loan process and have legal proceedings.

3. Government:- Governments use financial statements for taxation purposes. To

determine corporation tax, the company's taxable income has to be ascertained. Hence, it

is very necessary to have audit of financial records, otherwise the company may get stuck

in the taxation processes.

Internal Users:-

4. Management:- The financial statements helps the management in analysing the

company’s performance in comparison to the previous years along with other businesses

and sectors. Providing management with accurate information enables them to take

correct decisions as well as forming policies.

5. Employees:- Employees primarily use financial statements with the main objective of a

salary or wage increments. Another key factor is that employees generally feel more

satisfied working with a profit-making company and not a loss-making company.

QUESTION 2.

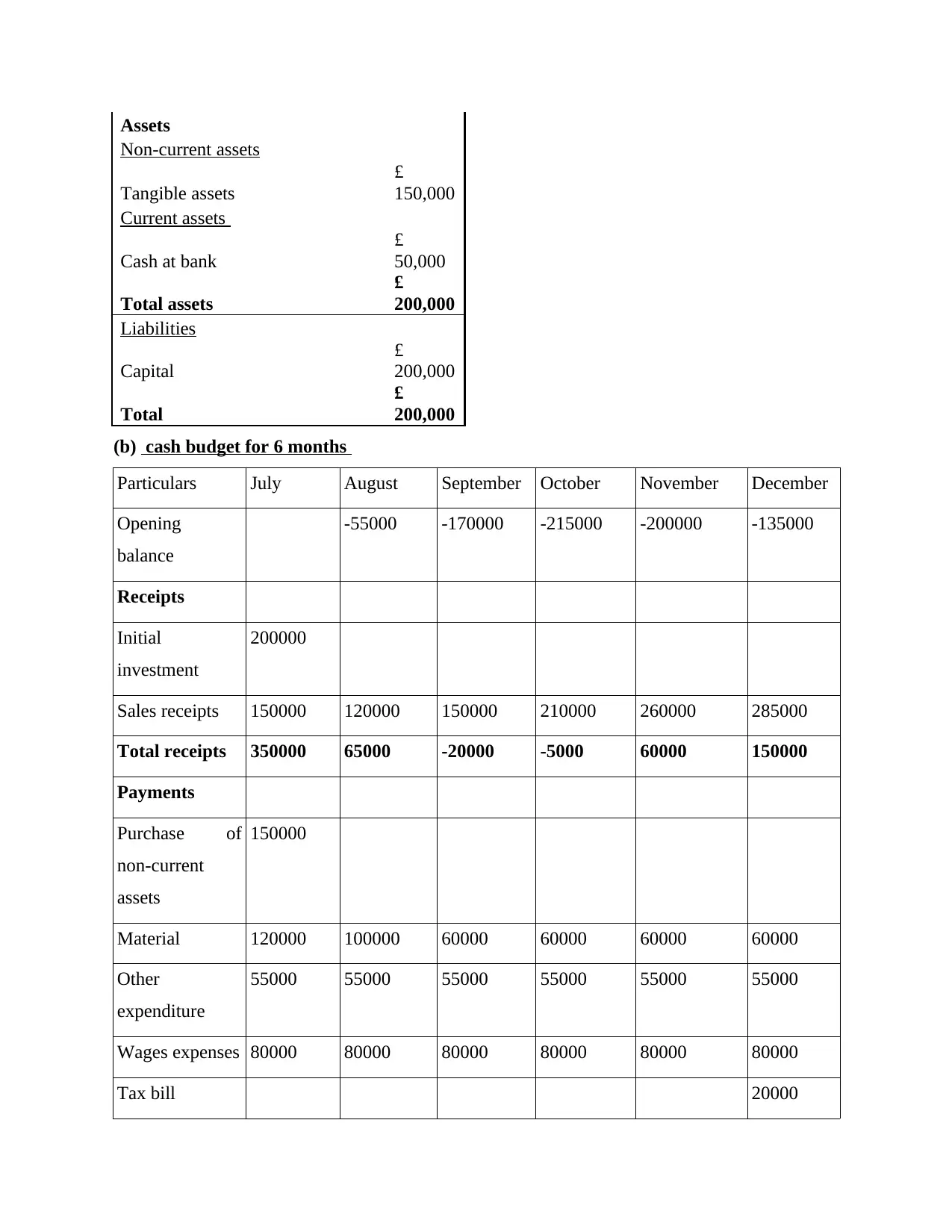

(a) Opening statement of financial position at the start of July 20X5

Opening Statement of Financial Position

between the debt and equity of a company. The ideal ratio for the same is 2 – 2.5 times whereas

the company's ratio stands at around .20 which is too less than the ideal ratio. Somehow it should

be observed that the ratio has improvised as compared to .13 for the previous year.

(b) Importance of considering audience :-

External Users:-

1. Shareholders- Financial statements depicts the current financial condition of any

company. Since no one wants to lose money by investing in a loss making company, it

becomes imperative to study the financial statements. Statements shows whether a

company is making profit or incurring losses which includes Income statement or P&l

statement.(Dong, Xu, and McIver, 2020)

2. Bank and financial institutions:- Banks provides credit facility to the companies having

good financial records. Therefore, it is necessary for every company to have accurate

financial records audited by an expert while applying for a loan. In case of otherwise,

may cancel the loan process and have legal proceedings.

3. Government:- Governments use financial statements for taxation purposes. To

determine corporation tax, the company's taxable income has to be ascertained. Hence, it

is very necessary to have audit of financial records, otherwise the company may get stuck

in the taxation processes.

Internal Users:-

4. Management:- The financial statements helps the management in analysing the

company’s performance in comparison to the previous years along with other businesses

and sectors. Providing management with accurate information enables them to take

correct decisions as well as forming policies.

5. Employees:- Employees primarily use financial statements with the main objective of a

salary or wage increments. Another key factor is that employees generally feel more

satisfied working with a profit-making company and not a loss-making company.

QUESTION 2.

(a) Opening statement of financial position at the start of July 20X5

Opening Statement of Financial Position

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assets

Non-current assets

Tangible assets

£

150,000

Current assets

Cash at bank

£

50,000

Total assets

£

200,000

Liabilities

Capital

£

200,000

Total

£

200,000

(b) cash budget for 6 months

Particulars July August September October November December

Opening

balance

-55000 -170000 -215000 -200000 -135000

Receipts

Initial

investment

200000

Sales receipts 150000 120000 150000 210000 260000 285000

Total receipts 350000 65000 -20000 -5000 60000 150000

Payments

Purchase of

non-current

assets

150000

Material 120000 100000 60000 60000 60000 60000

Other

expenditure

55000 55000 55000 55000 55000 55000

Wages expenses 80000 80000 80000 80000 80000 80000

Tax bill 20000

Non-current assets

Tangible assets

£

150,000

Current assets

Cash at bank

£

50,000

Total assets

£

200,000

Liabilities

Capital

£

200,000

Total

£

200,000

(b) cash budget for 6 months

Particulars July August September October November December

Opening

balance

-55000 -170000 -215000 -200000 -135000

Receipts

Initial

investment

200000

Sales receipts 150000 120000 150000 210000 260000 285000

Total receipts 350000 65000 -20000 -5000 60000 150000

Payments

Purchase of

non-current

assets

150000

Material 120000 100000 60000 60000 60000 60000

Other

expenditure

55000 55000 55000 55000 55000 55000

Wages expenses 80000 80000 80000 80000 80000 80000

Tax bill 20000

Total payments 405000 235000 195000 195000 195000 215000

Closing balance -55000 -170000 -215000 -200000 -135000 -65000

As per the question, the new business of Sassy Clothing which is an online clothing

business and mail order business.(Gong, and Cullinane, eds., 2018)The opening balances of cash

budgets already has a negative cash balance of months August to December. The expected sales

for upcoming six months are £1,175,000. The Sassy clothing business needs work upon its

internal as well as external resources to fully utilise the strength to increase its revenue and to

maintain surplus cash balances instead of having negative at the end of each month. This can be

effectively done by the increasing the sales and lowering the other expenses which are

responsible for the increase in manufacturing cost. (Hofmann, Strewe, and Bosia, 2018)

Instead of outsourcing the raw material the best option is in house production.

(c) Explanation of additional expenditures

There is various expenditure that need to be compressed by the Sassy Clothing business

for positive balance. The cost of the month of July and December which basically include

software bills, rent, running fees and charge to the suppliers. Overdraft mortgage is the business

enterprise on the spot admittance to more price range after they do now no longer have any

remain. It lets in dealing with the accurate mismatch of price range draft and supports in keeping

the good track record. With the support of the financial institution overdraft the Sassy business is

capable of do the bills in their costs on time.

QUESTION 3

(a) Calculate the breakeven point in units and sales revenue for the year ended 31 March

2019 and the year ended 31 March 2020.

Break Even Point = fixed cost / contribution per unit

So, Total fixed cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

And contribution per unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

So, Breakeven point of year 2019 is = £ 5,430,000 / £ 115

Closing balance -55000 -170000 -215000 -200000 -135000 -65000

As per the question, the new business of Sassy Clothing which is an online clothing

business and mail order business.(Gong, and Cullinane, eds., 2018)The opening balances of cash

budgets already has a negative cash balance of months August to December. The expected sales

for upcoming six months are £1,175,000. The Sassy clothing business needs work upon its

internal as well as external resources to fully utilise the strength to increase its revenue and to

maintain surplus cash balances instead of having negative at the end of each month. This can be

effectively done by the increasing the sales and lowering the other expenses which are

responsible for the increase in manufacturing cost. (Hofmann, Strewe, and Bosia, 2018)

Instead of outsourcing the raw material the best option is in house production.

(c) Explanation of additional expenditures

There is various expenditure that need to be compressed by the Sassy Clothing business

for positive balance. The cost of the month of July and December which basically include

software bills, rent, running fees and charge to the suppliers. Overdraft mortgage is the business

enterprise on the spot admittance to more price range after they do now no longer have any

remain. It lets in dealing with the accurate mismatch of price range draft and supports in keeping

the good track record. With the support of the financial institution overdraft the Sassy business is

capable of do the bills in their costs on time.

QUESTION 3

(a) Calculate the breakeven point in units and sales revenue for the year ended 31 March

2019 and the year ended 31 March 2020.

Break Even Point = fixed cost / contribution per unit

So, Total fixed cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

And contribution per unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

So, Breakeven point of year 2019 is = £ 5,430,000 / £ 115

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

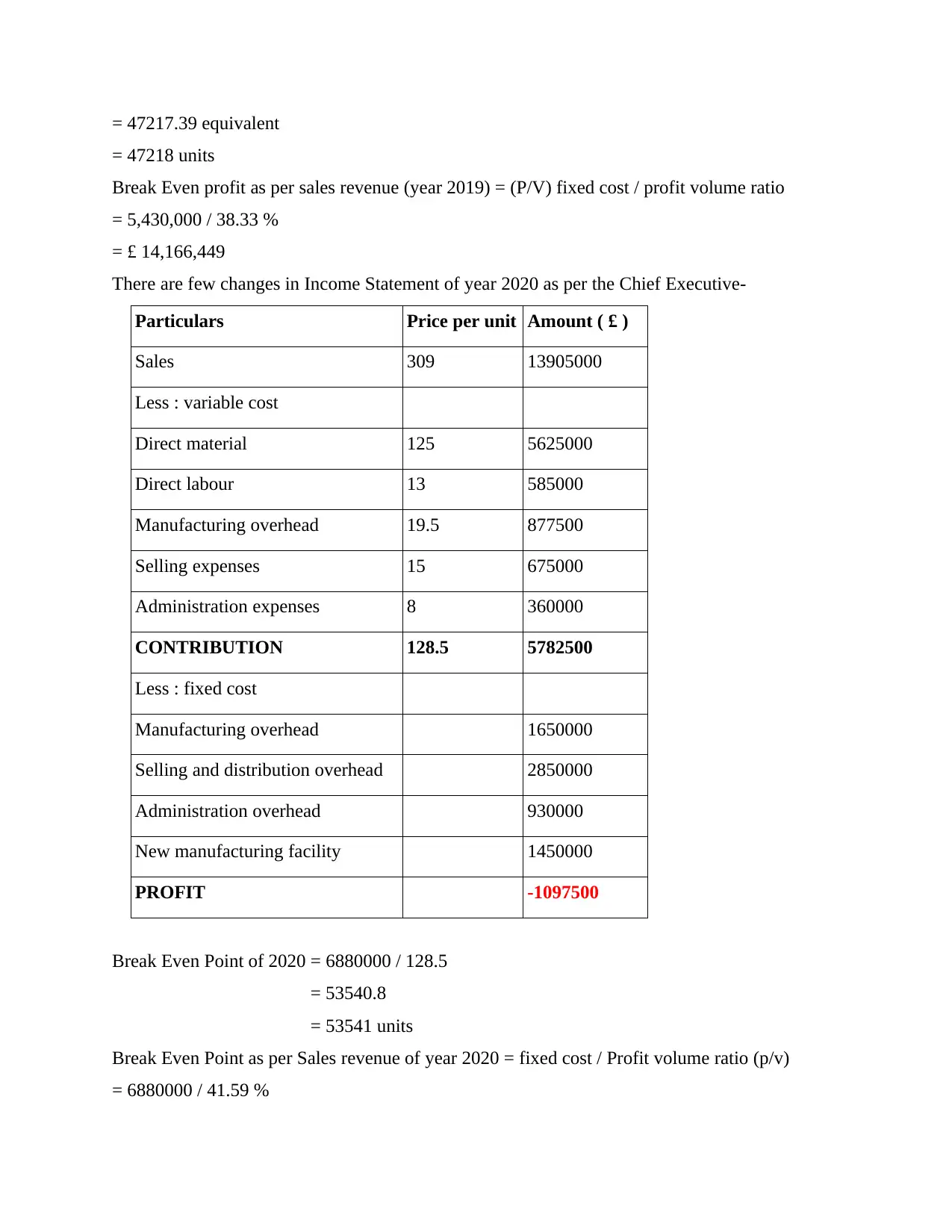

= 47217.39 equivalent

= 47218 units

Break Even profit as per sales revenue (year 2019) = (P/V) fixed cost / profit volume ratio

= 5,430,000 / 38.33 %

= £ 14,166,449

There are few changes in Income Statement of year 2020 as per the Chief Executive-

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break Even Point of 2020 = 6880000 / 128.5

= 53540.8

= 53541 units

Break Even Point as per Sales revenue of year 2020 = fixed cost / Profit volume ratio (p/v)

= 6880000 / 41.59 %

= 47218 units

Break Even profit as per sales revenue (year 2019) = (P/V) fixed cost / profit volume ratio

= 5,430,000 / 38.33 %

= £ 14,166,449

There are few changes in Income Statement of year 2020 as per the Chief Executive-

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break Even Point of 2020 = 6880000 / 128.5

= 53540.8

= 53541 units

Break Even Point as per Sales revenue of year 2020 = fixed cost / Profit volume ratio (p/v)

= 6880000 / 41.59 %

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= £ 16542438.09

(b) Calculate the margin of safety in units and sales revenue for the year 2019 and 2020.

Margin of safety in units (2019) = profit / contribution per unit (Newell, 2022)

= -255000 / 115

= -2217

For 2020 –

= -1097500 / 128.5

= -8541

Now, as per Sales revenue

Margin of Safety of year 2019 = p/v

= profit/contribution per unit

= -1097500 / 41.59 %

= £-2638855.49

(c) Discuss the new strategy developed by Jessica

The above computations were aimed at analyzing two strategies namely BEP and MOS for 2

years, that is for the year 2019 and 2020. The BEP for the old and new strategy respectively was

47218 units and 53541 units approximately(Rethel, and Thurbon, 2020). Whereas talking about

the MOS for the 2 years that is for 2019 and 2020 in terms of output was -2217 units and -8541

units respectively.

In terms of sales revenue the BEP is going to be £14,166,449.26 and £16542438.09 respectively.

Thus looking at the above calculations it can be suggested that they should try to boost their sales

by excessive sales promotion tools and by minimizing the cost.

QUESTION 4.

(a)Payback period

Payback period refers to the period in which an investment is able to realize the value of

its investment. The project with the least timing is considered to be the most suitable project.

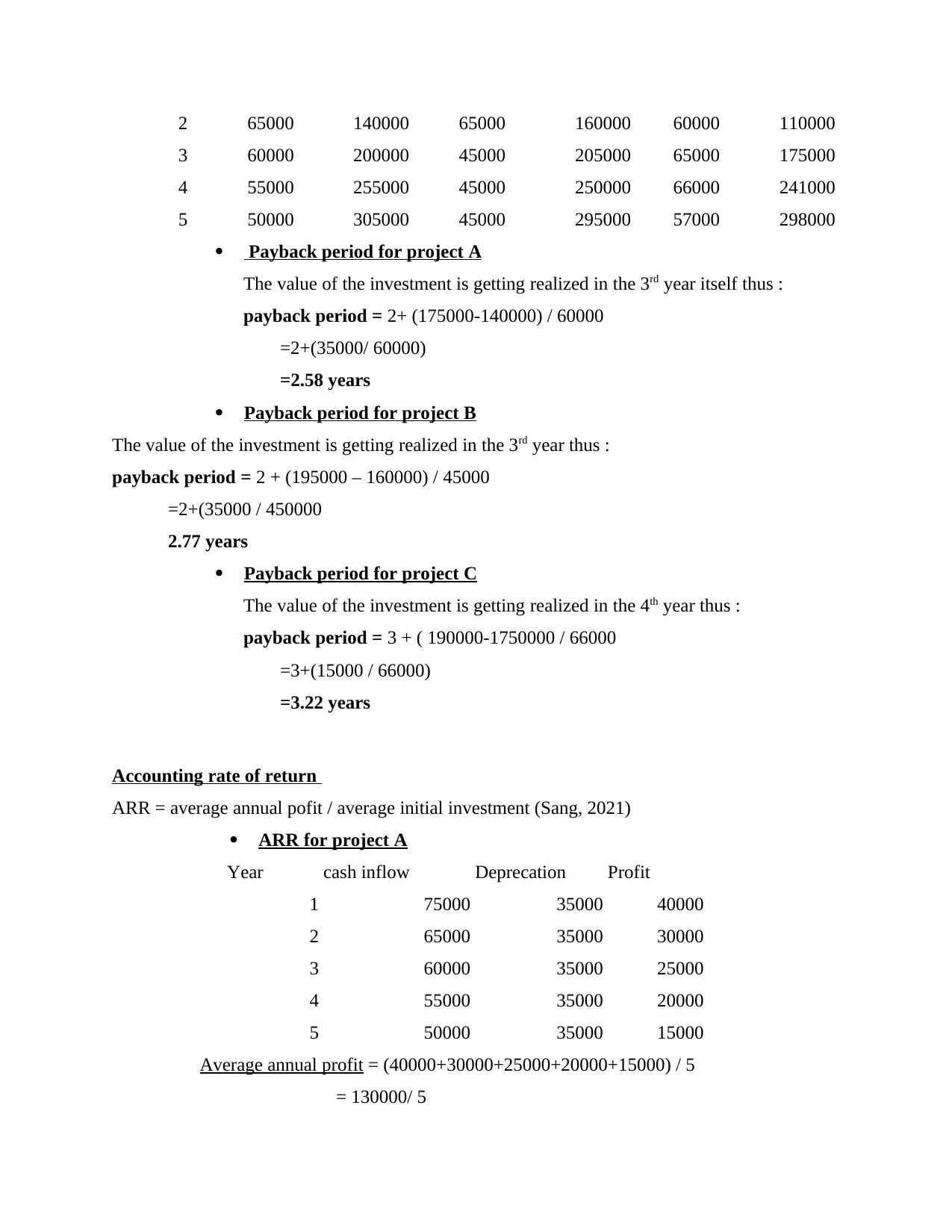

Year Appraisal A Appraisal B Appraisal C

cash inflow

cumulative

CF cash inflow cumulative CF

cash

inflow

cumulative

CF

1 75000 75000 95000 95000 50000 50000

(b) Calculate the margin of safety in units and sales revenue for the year 2019 and 2020.

Margin of safety in units (2019) = profit / contribution per unit (Newell, 2022)

= -255000 / 115

= -2217

For 2020 –

= -1097500 / 128.5

= -8541

Now, as per Sales revenue

Margin of Safety of year 2019 = p/v

= profit/contribution per unit

= -1097500 / 41.59 %

= £-2638855.49

(c) Discuss the new strategy developed by Jessica

The above computations were aimed at analyzing two strategies namely BEP and MOS for 2

years, that is for the year 2019 and 2020. The BEP for the old and new strategy respectively was

47218 units and 53541 units approximately(Rethel, and Thurbon, 2020). Whereas talking about

the MOS for the 2 years that is for 2019 and 2020 in terms of output was -2217 units and -8541

units respectively.

In terms of sales revenue the BEP is going to be £14,166,449.26 and £16542438.09 respectively.

Thus looking at the above calculations it can be suggested that they should try to boost their sales

by excessive sales promotion tools and by minimizing the cost.

QUESTION 4.

(a)Payback period

Payback period refers to the period in which an investment is able to realize the value of

its investment. The project with the least timing is considered to be the most suitable project.

Year Appraisal A Appraisal B Appraisal C

cash inflow

cumulative

CF cash inflow cumulative CF

cash

inflow

cumulative

CF

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Payback period for project A

The value of the investment is getting realized in the 3rd year itself thus :

payback period = 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Payback period for project B

The value of the investment is getting realized in the 3rd year thus :

payback period = 2 + (195000 – 160000) / 45000

=2+(35000 / 450000

2.77 years

Payback period for project C

The value of the investment is getting realized in the 4th year thus :

payback period = 3 + ( 190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Accounting rate of return

ARR = average annual pofit / average initial investment (Sang, 2021)

ARR for project A

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Payback period for project A

The value of the investment is getting realized in the 3rd year itself thus :

payback period = 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Payback period for project B

The value of the investment is getting realized in the 3rd year thus :

payback period = 2 + (195000 – 160000) / 45000

=2+(35000 / 450000

2.77 years

Payback period for project C

The value of the investment is getting realized in the 4th year thus :

payback period = 3 + ( 190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Accounting rate of return

ARR = average annual pofit / average initial investment (Sang, 2021)

ARR for project A

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.