Financial Analysis Report: Business Structures, Ratios, and Payback

VerifiedAdded on 2021/11/23

|14

|3093

|153

Report

AI Summary

This report provides a comprehensive financial analysis, beginning with a comparison of business structures including sole proprietorships, corporations, and limited liability companies (LLCs), discussing their advantages, disadvantages, and tax implications. The report then delves into financial ratio analysis, calculating and interpreting key ratios such as current, quick, cash, total asset turnover, inventory turnover, receivables turnover, total debt, debt-equity, profit margin, return on assets, and return on equity. The analysis includes a comparison of these ratios with industry averages, providing insights into a company's financial health and performance. Finally, the report explains the payback period method, its advantages, disadvantages, and applications in investment decision-making, along with a discussion of its limitations, such as ignoring the time value of money and not considering cash flows beyond the payback period. The report concludes with a recommendation for an LLC, its advantages, and importance for business owners.

Table of Contents

Question 01................................................................................................................................................2

Question 02................................................................................................................................................5

Question 03................................................................................................................................................8

References................................................................................................................................................14

Question 01................................................................................................................................................2

Question 02................................................................................................................................................5

Question 03................................................................................................................................................8

References................................................................................................................................................14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 01

01.

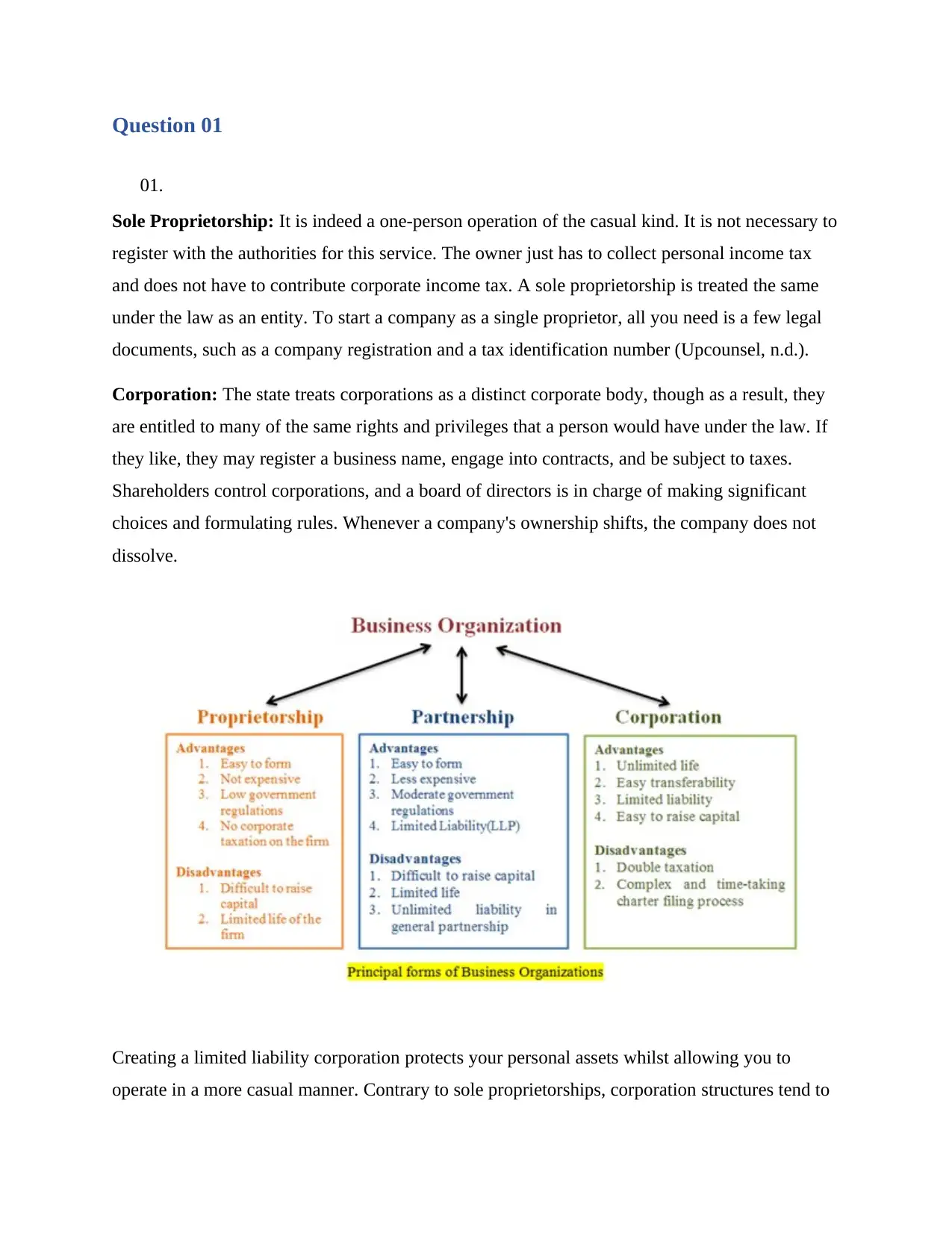

Sole Proprietorship: It is indeed a one-person operation of the casual kind. It is not necessary to

register with the authorities for this service. The owner just has to collect personal income tax

and does not have to contribute corporate income tax. A sole proprietorship is treated the same

under the law as an entity. To start a company as a single proprietor, all you need is a few legal

documents, such as a company registration and a tax identification number (Upcounsel, n.d.).

Corporation: The state treats corporations as a distinct corporate body, though as a result, they

are entitled to many of the same rights and privileges that a person would have under the law. If

they like, they may register a business name, engage into contracts, and be subject to taxes.

Shareholders control corporations, and a board of directors is in charge of making significant

choices and formulating rules. Whenever a company's ownership shifts, the company does not

dissolve.

Creating a limited liability corporation protects your personal assets whilst allowing you to

operate in a more casual manner. Contrary to sole proprietorships, corporation structures tend to

01.

Sole Proprietorship: It is indeed a one-person operation of the casual kind. It is not necessary to

register with the authorities for this service. The owner just has to collect personal income tax

and does not have to contribute corporate income tax. A sole proprietorship is treated the same

under the law as an entity. To start a company as a single proprietor, all you need is a few legal

documents, such as a company registration and a tax identification number (Upcounsel, n.d.).

Corporation: The state treats corporations as a distinct corporate body, though as a result, they

are entitled to many of the same rights and privileges that a person would have under the law. If

they like, they may register a business name, engage into contracts, and be subject to taxes.

Shareholders control corporations, and a board of directors is in charge of making significant

choices and formulating rules. Whenever a company's ownership shifts, the company does not

dissolve.

Creating a limited liability corporation protects your personal assets whilst allowing you to

operate in a more casual manner. Contrary to sole proprietorships, corporation structures tend to

give legitimacy and long-term viability. People realize that corporations must adhere to a set of

standards in order to conduct business, while sole proprietorships are not subject to governmental

control or oversight. In addition, it offers tax freedom, requires fewer paperwork, and limits your

legal responsibility. The drawback of an LLC is that, unless you want to be treated as a

corporation, you would owe self-employment taxes on your profits. Because of this, the earnings

made by the LLC will not be taxed at the corporate level, but instead would be distributed to the

LLC's members, who will report them on their individual taxable profits. Uncertainty over duties

and a finite lifespan are two more drawbacks (Hira, 2017).

Liability is minimized when operating as a corporation rather than a single proprietorship. As a

single owner, you are individually liable for any obligations or liabilities your firm accrues. As a

result, if the company is eventually sued for a significant amount of money, his personal assets

might be at risk. Corporations and Limited Liability Companies (LLCs) enable an individual to

use a corporate liability shield to safeguard their financial property against company liabilities.

Usually, assets held by the company are exposed to business liabilities in these organizations;

assets not controlled by the company normally cannot be claimed to satisfy business obligations.

Sole proprietorships, on the other hand, are firms in which there is only one owner. Associating

under an LLC or corporation makes it easier to draw in financiers and collaborators into your

company. The drawback pertains to their tax situation (Villaluz, 2019).

02.

standards in order to conduct business, while sole proprietorships are not subject to governmental

control or oversight. In addition, it offers tax freedom, requires fewer paperwork, and limits your

legal responsibility. The drawback of an LLC is that, unless you want to be treated as a

corporation, you would owe self-employment taxes on your profits. Because of this, the earnings

made by the LLC will not be taxed at the corporate level, but instead would be distributed to the

LLC's members, who will report them on their individual taxable profits. Uncertainty over duties

and a finite lifespan are two more drawbacks (Hira, 2017).

Liability is minimized when operating as a corporation rather than a single proprietorship. As a

single owner, you are individually liable for any obligations or liabilities your firm accrues. As a

result, if the company is eventually sued for a significant amount of money, his personal assets

might be at risk. Corporations and Limited Liability Companies (LLCs) enable an individual to

use a corporate liability shield to safeguard their financial property against company liabilities.

Usually, assets held by the company are exposed to business liabilities in these organizations;

assets not controlled by the company normally cannot be claimed to satisfy business obligations.

Sole proprietorships, on the other hand, are firms in which there is only one owner. Associating

under an LLC or corporation makes it easier to draw in financiers and collaborators into your

company. The drawback pertains to their tax situation (Villaluz, 2019).

02.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Would recommend to go with LLC.

A limited liability company (LLC) is regarded as a distinct statutory body than its employees or

owners. Unlike toward a corporation's stockholders, LLC owners are not personally accountable

for the debts or legal obligations of their company. Unlike investors, LLC owners risk losing

their initial financial investment in the company. Although LLCs have legal duties, personal

assets such as a house or a bank account of the LLC owner are not at danger as they would be for

a sole proprietorship or general partnership. If you personally guarantee a company debt or fail to

take reasonable care and cause injury to a third party or violate your duty to your LLC, you may

still be held personally accountable, just as in other corporate organizations.

Standard businesses are subject to two levels of income taxes. Profits accrued by the business are

subject to income tax, and shareholders are responsible for any dividend taxes. LLCs are given a

special tax status known as "pass through," which means that earnings allotted to LLC members

are taxed only once, on their personal income tax returns. LLCs that meet the IRS's definition of

a partnership or S corporation may benefit from the same "pass through" tax status. Additionally,

LLC owners who are pass-through company entities may be eligible to deduct 20% of their

business revenue under the new Tax Cuts and Jobs Act 20% pass-through deduction. If you're a

business owner looking for further information, take a look at the 20% Pass-Through Tax

Deduction (Fitzpatrick, 2012).

A limited liability company (LLC) is regarded as a distinct statutory body than its employees or

owners. Unlike toward a corporation's stockholders, LLC owners are not personally accountable

for the debts or legal obligations of their company. Unlike investors, LLC owners risk losing

their initial financial investment in the company. Although LLCs have legal duties, personal

assets such as a house or a bank account of the LLC owner are not at danger as they would be for

a sole proprietorship or general partnership. If you personally guarantee a company debt or fail to

take reasonable care and cause injury to a third party or violate your duty to your LLC, you may

still be held personally accountable, just as in other corporate organizations.

Standard businesses are subject to two levels of income taxes. Profits accrued by the business are

subject to income tax, and shareholders are responsible for any dividend taxes. LLCs are given a

special tax status known as "pass through," which means that earnings allotted to LLC members

are taxed only once, on their personal income tax returns. LLCs that meet the IRS's definition of

a partnership or S corporation may benefit from the same "pass through" tax status. Additionally,

LLC owners who are pass-through company entities may be eligible to deduct 20% of their

business revenue under the new Tax Cuts and Jobs Act 20% pass-through deduction. If you're a

business owner looking for further information, take a look at the 20% Pass-Through Tax

Deduction (Fitzpatrick, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 02

01.

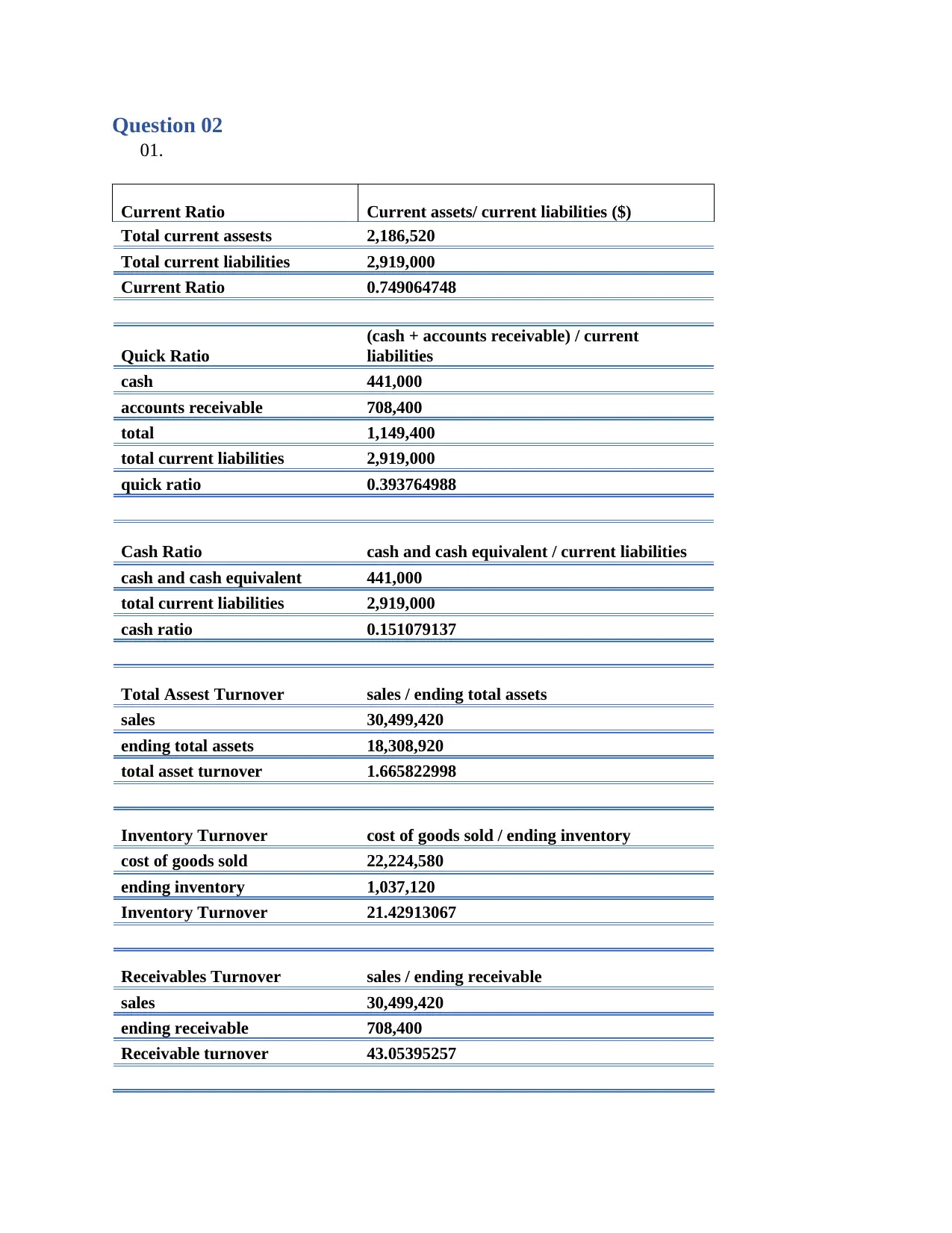

Current Ratio Current assets/ current liabilities ($)

Total current assests 2,186,520

Total current liabilities 2,919,000

Current Ratio 0.749064748

Quick Ratio

(cash + accounts receivable) / current

liabilities

cash 441,000

accounts receivable 708,400

total 1,149,400

total current liabilities 2,919,000

quick ratio 0.393764988

Cash Ratio cash and cash equivalent / current liabilities

cash and cash equivalent 441,000

total current liabilities 2,919,000

cash ratio 0.151079137

Total Assest Turnover sales / ending total assets

sales 30,499,420

ending total assets 18,308,920

total asset turnover 1.665822998

Inventory Turnover cost of goods sold / ending inventory

cost of goods sold 22,224,580

ending inventory 1,037,120

Inventory Turnover 21.42913067

Receivables Turnover sales / ending receivable

sales 30,499,420

ending receivable 708,400

Receivable turnover 43.05395257

01.

Current Ratio Current assets/ current liabilities ($)

Total current assests 2,186,520

Total current liabilities 2,919,000

Current Ratio 0.749064748

Quick Ratio

(cash + accounts receivable) / current

liabilities

cash 441,000

accounts receivable 708,400

total 1,149,400

total current liabilities 2,919,000

quick ratio 0.393764988

Cash Ratio cash and cash equivalent / current liabilities

cash and cash equivalent 441,000

total current liabilities 2,919,000

cash ratio 0.151079137

Total Assest Turnover sales / ending total assets

sales 30,499,420

ending total assets 18,308,920

total asset turnover 1.665822998

Inventory Turnover cost of goods sold / ending inventory

cost of goods sold 22,224,580

ending inventory 1,037,120

Inventory Turnover 21.42913067

Receivables Turnover sales / ending receivable

sales 30,499,420

ending receivable 708,400

Receivable turnover 43.05395257

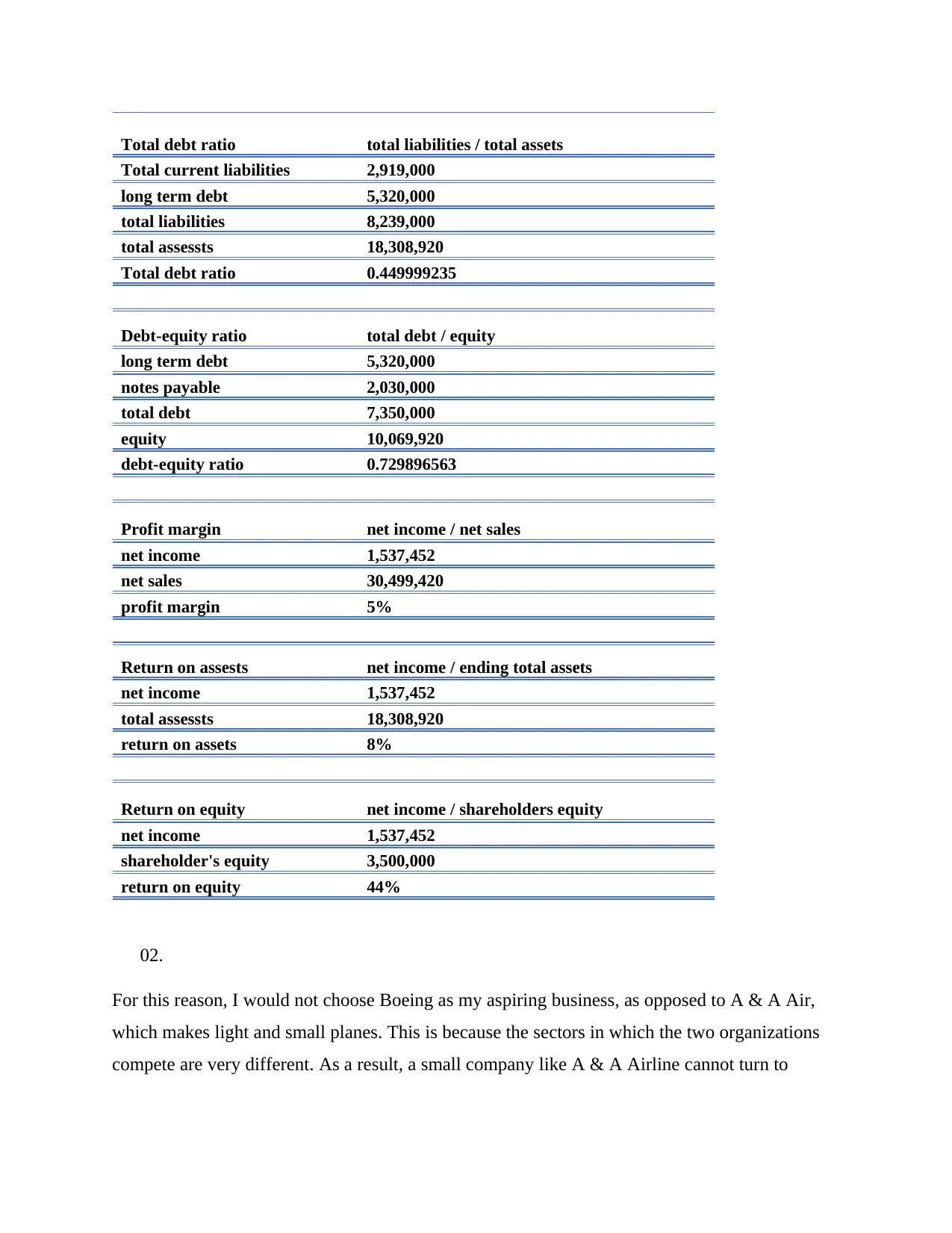

Total debt ratio total liabilities / total assets

Total current liabilities 2,919,000

long term debt 5,320,000

total liabilities 8,239,000

total assessts 18,308,920

Total debt ratio 0.449999235

Debt-equity ratio total debt / equity

long term debt 5,320,000

notes payable 2,030,000

total debt 7,350,000

equity 10,069,920

debt-equity ratio 0.729896563

Profit margin net income / net sales

net income 1,537,452

net sales 30,499,420

profit margin 5%

Return on assests net income / ending total assets

net income 1,537,452

total assessts 18,308,920

return on assets 8%

Return on equity net income / shareholders equity

net income 1,537,452

shareholder's equity 3,500,000

return on equity 44%

02.

For this reason, I would not choose Boeing as my aspiring business, as opposed to A & A Air,

which makes light and small planes. This is because the sectors in which the two organizations

compete are very different. As a result, a small company like A & A Airline cannot turn to

Total current liabilities 2,919,000

long term debt 5,320,000

total liabilities 8,239,000

total assessts 18,308,920

Total debt ratio 0.449999235

Debt-equity ratio total debt / equity

long term debt 5,320,000

notes payable 2,030,000

total debt 7,350,000

equity 10,069,920

debt-equity ratio 0.729896563

Profit margin net income / net sales

net income 1,537,452

net sales 30,499,420

profit margin 5%

Return on assests net income / ending total assets

net income 1,537,452

total assessts 18,308,920

return on assets 8%

Return on equity net income / shareholders equity

net income 1,537,452

shareholder's equity 3,500,000

return on equity 44%

02.

For this reason, I would not choose Boeing as my aspiring business, as opposed to A & A Air,

which makes light and small planes. This is because the sectors in which the two organizations

compete are very different. As a result, a small company like A & A Airline cannot turn to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Boeing as a role model to emulate. It should look for a company like that if it wants to be the

market leader.

Sonex also provides services connected to the nation's military, therefore considering it would be

impractical for S & S. Choosing a niche firm in the market is essential for the company's success.

Due to its global reach and operations in commercial aviation as well as executive jets and

military security systems, Phantom Aeronautics, which focuses on the manufacturing of large

commercial aircraft, is neither practical nor desirable for A&A to follow.

Air-Tech Inc. or Aero Adventure Firm may be used as a future aspirant company for the

development of its business plan. Both companies are in the same industry and have been in

business for a long time. Therefore, they both have the potential to provide clients with

innovation, safety, and trustworthiness for their products.

03.

S&S Air is behind the industry average in terms of current and cash ratios. Assuming this is

correct, the company has less cash on hand than its competitors. The company might benefit

from stronger cash flow forecasts or easier access to short-term borrowing. The quick ratio

exceeds the industry norm. To put it another way, S&S Air's inventory to current liabilities is

around average when comparison to the whole market.

Our industry has a higher turnover ratio when compared to others. This means that the three

turnover ratios are all above average. This might mean that S&S Air offers better value than the

competition.

Despite being above the lowest quartile, all of the financial leverage ratios are lower than the

industry standard. S&S Air has less debt than comparable firms, yet it still falls within the norm.

Question 03

01.

market leader.

Sonex also provides services connected to the nation's military, therefore considering it would be

impractical for S & S. Choosing a niche firm in the market is essential for the company's success.

Due to its global reach and operations in commercial aviation as well as executive jets and

military security systems, Phantom Aeronautics, which focuses on the manufacturing of large

commercial aircraft, is neither practical nor desirable for A&A to follow.

Air-Tech Inc. or Aero Adventure Firm may be used as a future aspirant company for the

development of its business plan. Both companies are in the same industry and have been in

business for a long time. Therefore, they both have the potential to provide clients with

innovation, safety, and trustworthiness for their products.

03.

S&S Air is behind the industry average in terms of current and cash ratios. Assuming this is

correct, the company has less cash on hand than its competitors. The company might benefit

from stronger cash flow forecasts or easier access to short-term borrowing. The quick ratio

exceeds the industry norm. To put it another way, S&S Air's inventory to current liabilities is

around average when comparison to the whole market.

Our industry has a higher turnover ratio when compared to others. This means that the three

turnover ratios are all above average. This might mean that S&S Air offers better value than the

competition.

Despite being above the lowest quartile, all of the financial leverage ratios are lower than the

industry standard. S&S Air has less debt than comparable firms, yet it still falls within the norm.

Question 03

01.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The payback technique aids in determining how long it will take to recoup your investment.

When a project's cash flows and earnings cover its original investment, it is said to be in the

payback phase (PBP). CFOs choose projects with shorter payback periods when given an option

(Finance Management, 2018).

Advantages of Payback Period

Ease of Use and Understanding

This is one of the payback period's most important benefits. As compared to other capital

budgeting approaches, this one requires fewer inputs and is thus simpler to compute. Payback

periods may be calculated using only the project's start-up costs and yearly cash flows. While

alternative approaches make use of the same inputs, they also need a greater number of

assumptions. Other methodologies, such as the cost of capital, need various assumptions on the

part of managers.

A Speedy Answer

Managers can rapidly compute the projects' payback periods since the payback time is simple to

calculate and requires fewer inputs. As a result, managers are better equipped to take swift

judgments, which is critical in organizations with limited resources.

Preference for Liquidity

The payback period, which is crucial information, is not shown by capital planning techniques. A

project with a shorter payback period is frequently seen as less risky. This kind of information is

crucial for startups and small businesses who may not have access to huge financing sources.

Small businesses must quickly recover their investment expenditures in order to utilise the cash

for future expansion.

If you're concerned about anything, this is a good place to start.

When dealing in industries with a high degree of uncertainty or where technology is

continuously developing, the payback strategy comes in useful. As a result, forecasting future

When a project's cash flows and earnings cover its original investment, it is said to be in the

payback phase (PBP). CFOs choose projects with shorter payback periods when given an option

(Finance Management, 2018).

Advantages of Payback Period

Ease of Use and Understanding

This is one of the payback period's most important benefits. As compared to other capital

budgeting approaches, this one requires fewer inputs and is thus simpler to compute. Payback

periods may be calculated using only the project's start-up costs and yearly cash flows. While

alternative approaches make use of the same inputs, they also need a greater number of

assumptions. Other methodologies, such as the cost of capital, need various assumptions on the

part of managers.

A Speedy Answer

Managers can rapidly compute the projects' payback periods since the payback time is simple to

calculate and requires fewer inputs. As a result, managers are better equipped to take swift

judgments, which is critical in organizations with limited resources.

Preference for Liquidity

The payback period, which is crucial information, is not shown by capital planning techniques. A

project with a shorter payback period is frequently seen as less risky. This kind of information is

crucial for startups and small businesses who may not have access to huge financing sources.

Small businesses must quickly recover their investment expenditures in order to utilise the cash

for future expansion.

If you're concerned about anything, this is a good place to start.

When dealing in industries with a high degree of uncertainty or where technology is

continuously developing, the payback strategy comes in useful. As a result, forecasting future

annual cash inflows is difficult. The usage of short PBP in projects lowers the risk due to

expiration.

Drawbacks of Payback Period

ignores the principle of compound interest

It overlooks the time worth of money, a critical business concept, which is one of the biggest

drawbacks of the payback period. Money obtained earlier has a higher value because it has the

potential to produce a higher return if it is reinvested, according to the time value of money idea.

As a result, the PBP technique overstates the underlying value of cash flows. There's a

workaround for this here. The Discounted Payback Period may be used to overcome this

drawback.

Not all cash flows have been considered.

Using the payback technique, you only assess future cash flows once you have repaid your

original investment. It does not consider future cash flows. By just considering the short-term

cash flow, you may ignore a project that generates substantial cash flow in the long term.

Unrealistic expectations

Due to the simplicity of the repayment approach, regular business circumstances are not

considered. The majority of the time, capital investments are not one-off purchases. Such

initiatives need further funding long into the future. In addition, project funding is often erratic.

Avoids focusing on the bottom line

Shorter payback periods don't mean a project will be more lucrative in the long run. What

happens if the project's cash flow stops or decreases after the payback period has passed? After

the payback time expires in either situation, the project is doomed.

Uses of Payback Period

Investors, financial experts, and companies all utilize the payback period when calculating

investment returns. You can see how long it takes to recoup your original investment fees using

expiration.

Drawbacks of Payback Period

ignores the principle of compound interest

It overlooks the time worth of money, a critical business concept, which is one of the biggest

drawbacks of the payback period. Money obtained earlier has a higher value because it has the

potential to produce a higher return if it is reinvested, according to the time value of money idea.

As a result, the PBP technique overstates the underlying value of cash flows. There's a

workaround for this here. The Discounted Payback Period may be used to overcome this

drawback.

Not all cash flows have been considered.

Using the payback technique, you only assess future cash flows once you have repaid your

original investment. It does not consider future cash flows. By just considering the short-term

cash flow, you may ignore a project that generates substantial cash flow in the long term.

Unrealistic expectations

Due to the simplicity of the repayment approach, regular business circumstances are not

considered. The majority of the time, capital investments are not one-off purchases. Such

initiatives need further funding long into the future. In addition, project funding is often erratic.

Avoids focusing on the bottom line

Shorter payback periods don't mean a project will be more lucrative in the long run. What

happens if the project's cash flow stops or decreases after the payback period has passed? After

the payback time expires in either situation, the project is doomed.

Uses of Payback Period

Investors, financial experts, and companies all utilize the payback period when calculating

investment returns. You can see how long it takes to recoup your original investment fees using

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this tool. If you're an investor and you need to make an instant decision regarding a potential

investment, utilize this statistic (Kagan, 2021).

The payback time statistic has additional uses outside capital budgeting and financial planning,

as you'll see below. Energy-efficient solutions such as solar panels and insulation, as well as

infrastructure upgrades, may be calculated using this tool by both households and businesses.

02.

There are a certain number of years in the payback period that must pass before the money spent

in a venture is recouped. We don't consider the time worth of money when figuring up the

payback period.

The number of years after the original investment is fully recouped by the discounted cash flows

is called the discounted payback time;

Payback and discounted payback periods let us know how long it will take to recoup our initial

investment.

Due to the absence of cash flows after the recovery of the initial investment, payback and

discounted payback periods cannot be utilized as indicators of profitability. More often than not,

we utilize them to see whether we can recoup our project costs before a certain deadline. These

two metrics are helpful in determining a project's liquidity.

If the discounted repayment time for investment A is less than the discounted payback period for

investment B, we choose A over B as an investment.

Payback time is usually shorter for a typical project than discounted payback time. It's because

the discounted payback period takes future financial inflows into account when calculating the

discounted payback period. Accordingly, it will take longer to recoup the initial investment using

this criterion.

03.

NPV will be negative if discount rate > IRR

NPV will be zero if discount rate = IRR

investment, utilize this statistic (Kagan, 2021).

The payback time statistic has additional uses outside capital budgeting and financial planning,

as you'll see below. Energy-efficient solutions such as solar panels and insulation, as well as

infrastructure upgrades, may be calculated using this tool by both households and businesses.

02.

There are a certain number of years in the payback period that must pass before the money spent

in a venture is recouped. We don't consider the time worth of money when figuring up the

payback period.

The number of years after the original investment is fully recouped by the discounted cash flows

is called the discounted payback time;

Payback and discounted payback periods let us know how long it will take to recoup our initial

investment.

Due to the absence of cash flows after the recovery of the initial investment, payback and

discounted payback periods cannot be utilized as indicators of profitability. More often than not,

we utilize them to see whether we can recoup our project costs before a certain deadline. These

two metrics are helpful in determining a project's liquidity.

If the discounted repayment time for investment A is less than the discounted payback period for

investment B, we choose A over B as an investment.

Payback time is usually shorter for a typical project than discounted payback time. It's because

the discounted payback period takes future financial inflows into account when calculating the

discounted payback period. Accordingly, it will take longer to recoup the initial investment using

this criterion.

03.

NPV will be negative if discount rate > IRR

NPV will be zero if discount rate = IRR

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

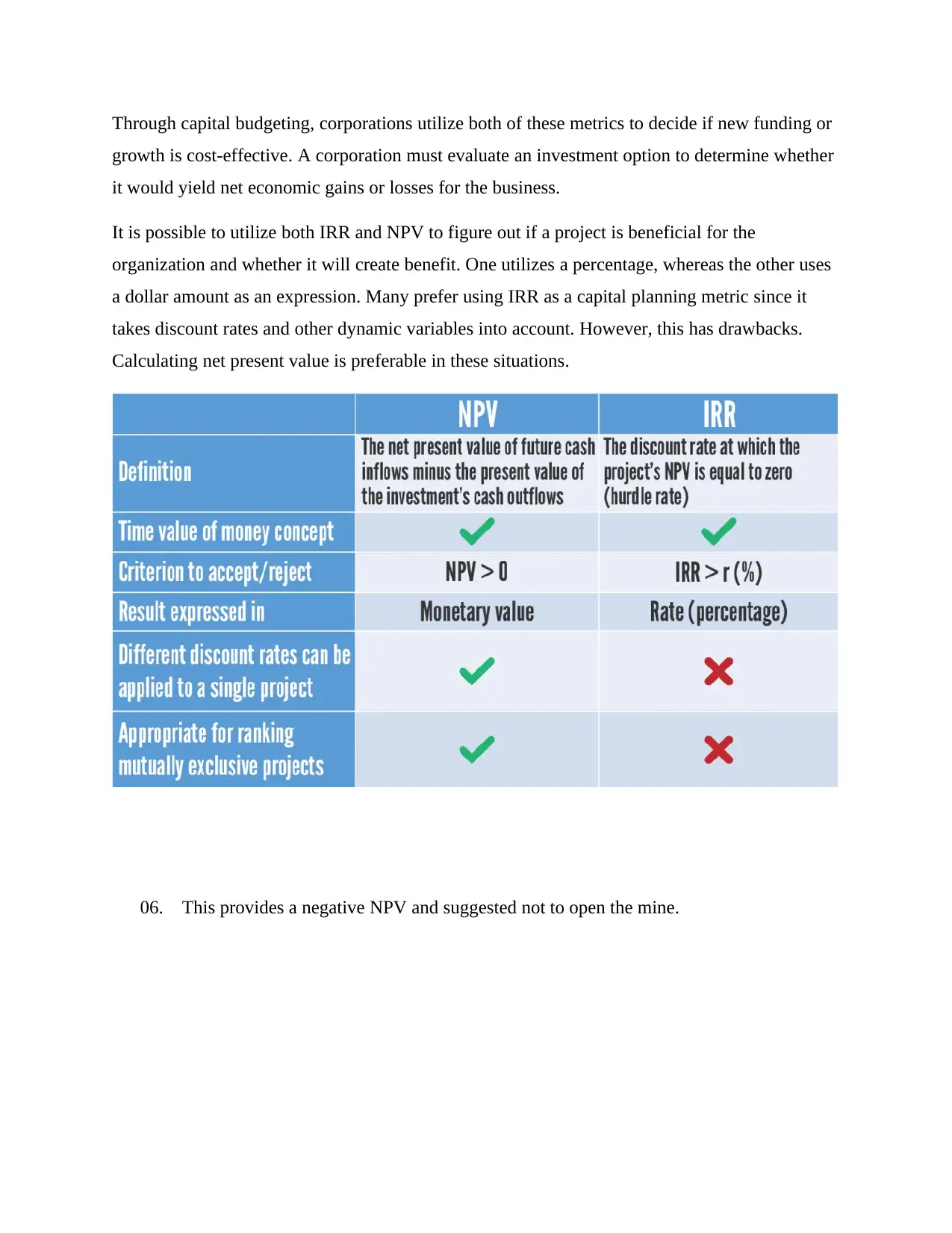

NPV will be positive if discount rate < IRR

By using the net present value approach, an organization may calculate many of the current and

prospective cash movements associated with a project, including both positive (revenue) and

unfavorable (costs). The value of future cash flows is then "discounted" to represent their current

value. With the "discount rate," it accounts for inflation, danger, and capital costs such as interest

paid on borrowed money or interest not generated on cash spent to execute the project. It

accomplishes this modification. Ultimately, the net present value (NPV) is calculated by adding

the present values of all of the project's positive and negative cash flows. Projects with a positive

net present value (NPV) should be pursued; those with a negative NPV must be discarded. When

choosing among two projects, go with the one that has the highest net present value (NPV).

04.

Because the reinvestment rate used in the NPV method is close to the current cost of capital, re-

investment estimates in the NPV method are more realistic than those in the IRR approach. The

benefit of NPV versus IRR arises when a project has non-standard cash flow patterns.

Also, what makes the profitability index superior to the net present value (NPV)? Nevertheless,

Project X is acceptable based on the Net Present Value technique due to its larger positive NPV;

nevertheless, Project Y is acceptable based on the profitability index approach due to its higher

P.I. As a result, the two mutually contradictory suggestions have a conflicting rating under the

two approaches. Since it provides a fuller view of future cash flows, NPV is preferred above IRR

and payback as other common capital planning strategies.

05.

By using the net present value approach, an organization may calculate many of the current and

prospective cash movements associated with a project, including both positive (revenue) and

unfavorable (costs). The value of future cash flows is then "discounted" to represent their current

value. With the "discount rate," it accounts for inflation, danger, and capital costs such as interest

paid on borrowed money or interest not generated on cash spent to execute the project. It

accomplishes this modification. Ultimately, the net present value (NPV) is calculated by adding

the present values of all of the project's positive and negative cash flows. Projects with a positive

net present value (NPV) should be pursued; those with a negative NPV must be discarded. When

choosing among two projects, go with the one that has the highest net present value (NPV).

04.

Because the reinvestment rate used in the NPV method is close to the current cost of capital, re-

investment estimates in the NPV method are more realistic than those in the IRR approach. The

benefit of NPV versus IRR arises when a project has non-standard cash flow patterns.

Also, what makes the profitability index superior to the net present value (NPV)? Nevertheless,

Project X is acceptable based on the Net Present Value technique due to its larger positive NPV;

nevertheless, Project Y is acceptable based on the profitability index approach due to its higher

P.I. As a result, the two mutually contradictory suggestions have a conflicting rating under the

two approaches. Since it provides a fuller view of future cash flows, NPV is preferred above IRR

and payback as other common capital planning strategies.

05.

Through capital budgeting, corporations utilize both of these metrics to decide if new funding or

growth is cost-effective. A corporation must evaluate an investment option to determine whether

it would yield net economic gains or losses for the business.

It is possible to utilize both IRR and NPV to figure out if a project is beneficial for the

organization and whether it will create benefit. One utilizes a percentage, whereas the other uses

a dollar amount as an expression. Many prefer using IRR as a capital planning metric since it

takes discount rates and other dynamic variables into account. However, this has drawbacks.

Calculating net present value is preferable in these situations.

06. This provides a negative NPV and suggested not to open the mine.

growth is cost-effective. A corporation must evaluate an investment option to determine whether

it would yield net economic gains or losses for the business.

It is possible to utilize both IRR and NPV to figure out if a project is beneficial for the

organization and whether it will create benefit. One utilizes a percentage, whereas the other uses

a dollar amount as an expression. Many prefer using IRR as a capital planning metric since it

takes discount rates and other dynamic variables into account. However, this has drawbacks.

Calculating net present value is preferable in these situations.

06. This provides a negative NPV and suggested not to open the mine.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.