Financial Accounting: Reconciliation and Control Accounts Analysis

VerifiedAdded on 2023/01/12

|20

|4294

|65

Homework Assignment

AI Summary

This financial accounting assignment solution covers fundamental concepts such as double-entry bookkeeping, trial balances, and the preparation of financial statements (income statement, balance sheet, and cash flow statement). It explores the differences between financial reports and financial statements and explains accounting for sole traders, partnerships, and limited companies, including their final accounts. The solution addresses the reconciliation process, including tools and techniques for checking general ledger accounts, explaining variances, and the importance of accurate figures. It includes examples and case studies demonstrating bank reconciliation statements and control accounts, concluding with an overview of the purpose of suspense accounts and their differences from control accounts. This comprehensive document is designed to enhance understanding of financial accounting principles and practices.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUTION .............................................................................................................................3

INFORMATION BOOKLET..........................................................................................................3

LO1..................................................................................................................................................3

Double entry book–keeping and trial balance and regulations....................................................3

Case Study 1................................................................................................................................4

Case Study 2................................................................................................................................4

Case Study 3................................................................................................................................5

Case Study 4................................................................................................................................5

Case Study 5................................................................................................................................8

Difference between the financial reports and financial statements. ...........................................9

LO2................................................................................................................................................10

Explanation of the accounts for sole trader, partnership and limited company and their

differences..................................................................................................................................10

Final accounts of sole trader, partnership and company............................................................11

LO3................................................................................................................................................14

Explanation of the reconciliation process and tools & techniques used for checking general

ledger accounts. Explanation on variances and importance of the correctly entered figures....14

Bank Reconciliation Statement..................................................................................................15

LO4................................................................................................................................................16

Explanation of the control accounts and their use in financial accounting................................16

Description of process for reconciling control accounts and need to reconcile the accounts....17

Explanation on purpose of suspense accounts and their difference from the control accounts.18

Control Account.........................................................................................................................19

CONCLUSION .............................................................................................................................20

REFERENCES..............................................................................................................................21

INTRODUTION .............................................................................................................................3

INFORMATION BOOKLET..........................................................................................................3

LO1..................................................................................................................................................3

Double entry book–keeping and trial balance and regulations....................................................3

Case Study 1................................................................................................................................4

Case Study 2................................................................................................................................4

Case Study 3................................................................................................................................5

Case Study 4................................................................................................................................5

Case Study 5................................................................................................................................8

Difference between the financial reports and financial statements. ...........................................9

LO2................................................................................................................................................10

Explanation of the accounts for sole trader, partnership and limited company and their

differences..................................................................................................................................10

Final accounts of sole trader, partnership and company............................................................11

LO3................................................................................................................................................14

Explanation of the reconciliation process and tools & techniques used for checking general

ledger accounts. Explanation on variances and importance of the correctly entered figures....14

Bank Reconciliation Statement..................................................................................................15

LO4................................................................................................................................................16

Explanation of the control accounts and their use in financial accounting................................16

Description of process for reconciling control accounts and need to reconcile the accounts....17

Explanation on purpose of suspense accounts and their difference from the control accounts.18

Control Account.........................................................................................................................19

CONCLUSION .............................................................................................................................20

REFERENCES..............................................................................................................................21

INTRODUTION

Financial accounting refers to process of preparing the financial statements which represents

the financial position and performance of the company. These financial information is useful for

both the internal management and stakeholders of the company such as creditors, investors,

suppliers and customers. Financial accounting is different from managerial accounting that

prepares financial records for the internal management of the company. Financial statements

prepared by the company are income statement, balance sheet and cash flow statements. They

are prepared by the company as per the applicable accounting standards. Present report will be

revealing about the concepts and methods of financial accounting. It will provide explanation on

double entry book keeping, financial reports and the financial statements. It will also provide

about the sole traders, partnership and limited company form of doing business. Report will

address the reconciliation process and techniques used for checking the balances of general

ledger and the use of control accounts in financial accounting. The concepts will be explained

with the help of examples and case studies. Study will enhance the understanding of financial

accounting concepts and techniques.

INFORMATION BOOKLET

LO1

Double entry book–keeping and trial balance and regulations.

Book keeping or double entry system

means that every transaction of the business

affects minimum two accounts. It is to be

recorded in at least two accounts.. It was

established for giving equal effects to the

debit and credit side of the balances. Double

entry requires the accounting equation to be

in balance i.e. assets = owner’s equity +

liabilities. This requires the balance in assets

side should be equal to the balance in

liabilities and equity side.

Trial balance is statement prepared in

double entry system containing the debits

and credit balances of all the ledger

accounts. Trial balance is prepared after

closing the ledger accounts for balancing the

debits and credit side of all the accounts of

business. Trial balance is prepared by the

business for ensuring that entries recorded

for the financial transactions in the ledger

accounts and are balanced at the end. The

debit and credit side of the trial balance

should be equal. In a double entry system

trial balance is used for the preparation of

financial statements. Balance of the accounts

in trial balance is transferred to the

3

Financial accounting refers to process of preparing the financial statements which represents

the financial position and performance of the company. These financial information is useful for

both the internal management and stakeholders of the company such as creditors, investors,

suppliers and customers. Financial accounting is different from managerial accounting that

prepares financial records for the internal management of the company. Financial statements

prepared by the company are income statement, balance sheet and cash flow statements. They

are prepared by the company as per the applicable accounting standards. Present report will be

revealing about the concepts and methods of financial accounting. It will provide explanation on

double entry book keeping, financial reports and the financial statements. It will also provide

about the sole traders, partnership and limited company form of doing business. Report will

address the reconciliation process and techniques used for checking the balances of general

ledger and the use of control accounts in financial accounting. The concepts will be explained

with the help of examples and case studies. Study will enhance the understanding of financial

accounting concepts and techniques.

INFORMATION BOOKLET

LO1

Double entry book–keeping and trial balance and regulations.

Book keeping or double entry system

means that every transaction of the business

affects minimum two accounts. It is to be

recorded in at least two accounts.. It was

established for giving equal effects to the

debit and credit side of the balances. Double

entry requires the accounting equation to be

in balance i.e. assets = owner’s equity +

liabilities. This requires the balance in assets

side should be equal to the balance in

liabilities and equity side.

Trial balance is statement prepared in

double entry system containing the debits

and credit balances of all the ledger

accounts. Trial balance is prepared after

closing the ledger accounts for balancing the

debits and credit side of all the accounts of

business. Trial balance is prepared by the

business for ensuring that entries recorded

for the financial transactions in the ledger

accounts and are balanced at the end. The

debit and credit side of the trial balance

should be equal. In a double entry system

trial balance is used for the preparation of

financial statements. Balance of the accounts

in trial balance is transferred to the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

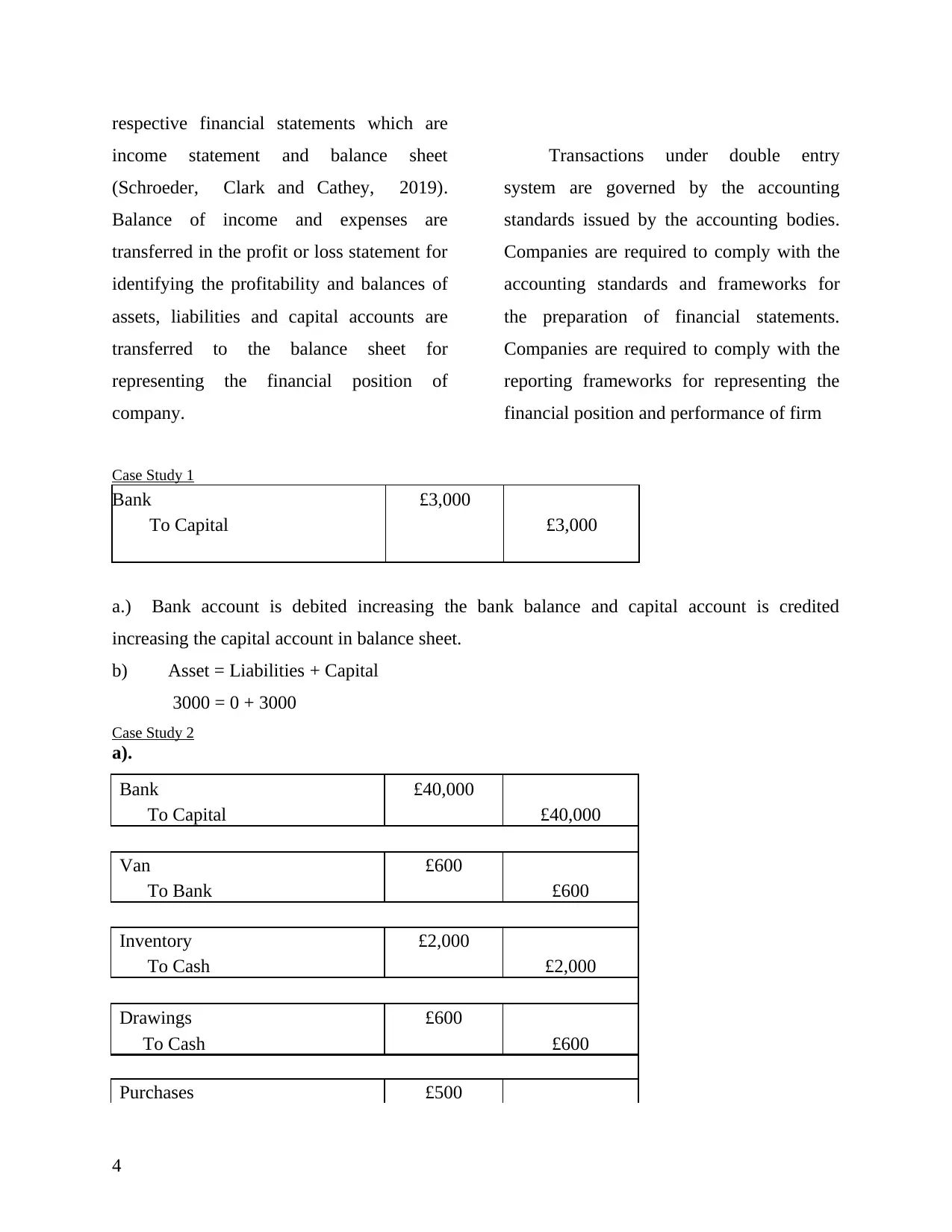

respective financial statements which are

income statement and balance sheet

(Schroeder, Clark and Cathey, 2019).

Balance of income and expenses are

transferred in the profit or loss statement for

identifying the profitability and balances of

assets, liabilities and capital accounts are

transferred to the balance sheet for

representing the financial position of

company.

Transactions under double entry

system are governed by the accounting

standards issued by the accounting bodies.

Companies are required to comply with the

accounting standards and frameworks for

the preparation of financial statements.

Companies are required to comply with the

reporting frameworks for representing the

financial position and performance of firm

Case Study 1

Bank £3,000

To Capital £3,000

a.) Bank account is debited increasing the bank balance and capital account is credited

increasing the capital account in balance sheet.

b) Asset = Liabilities + Capital

3000 = 0 + 3000

Case Study 2

a).

Bank £40,000

To Capital £40,000

Van £600

To Bank £600

Inventory £2,000

To Cash £2,000

Drawings £600

To Cash £600

Purchases £500

4

income statement and balance sheet

(Schroeder, Clark and Cathey, 2019).

Balance of income and expenses are

transferred in the profit or loss statement for

identifying the profitability and balances of

assets, liabilities and capital accounts are

transferred to the balance sheet for

representing the financial position of

company.

Transactions under double entry

system are governed by the accounting

standards issued by the accounting bodies.

Companies are required to comply with the

accounting standards and frameworks for

the preparation of financial statements.

Companies are required to comply with the

reporting frameworks for representing the

financial position and performance of firm

Case Study 1

Bank £3,000

To Capital £3,000

a.) Bank account is debited increasing the bank balance and capital account is credited

increasing the capital account in balance sheet.

b) Asset = Liabilities + Capital

3000 = 0 + 3000

Case Study 2

a).

Bank £40,000

To Capital £40,000

Van £600

To Bank £600

Inventory £2,000

To Cash £2,000

Drawings £600

To Cash £600

Purchases £500

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

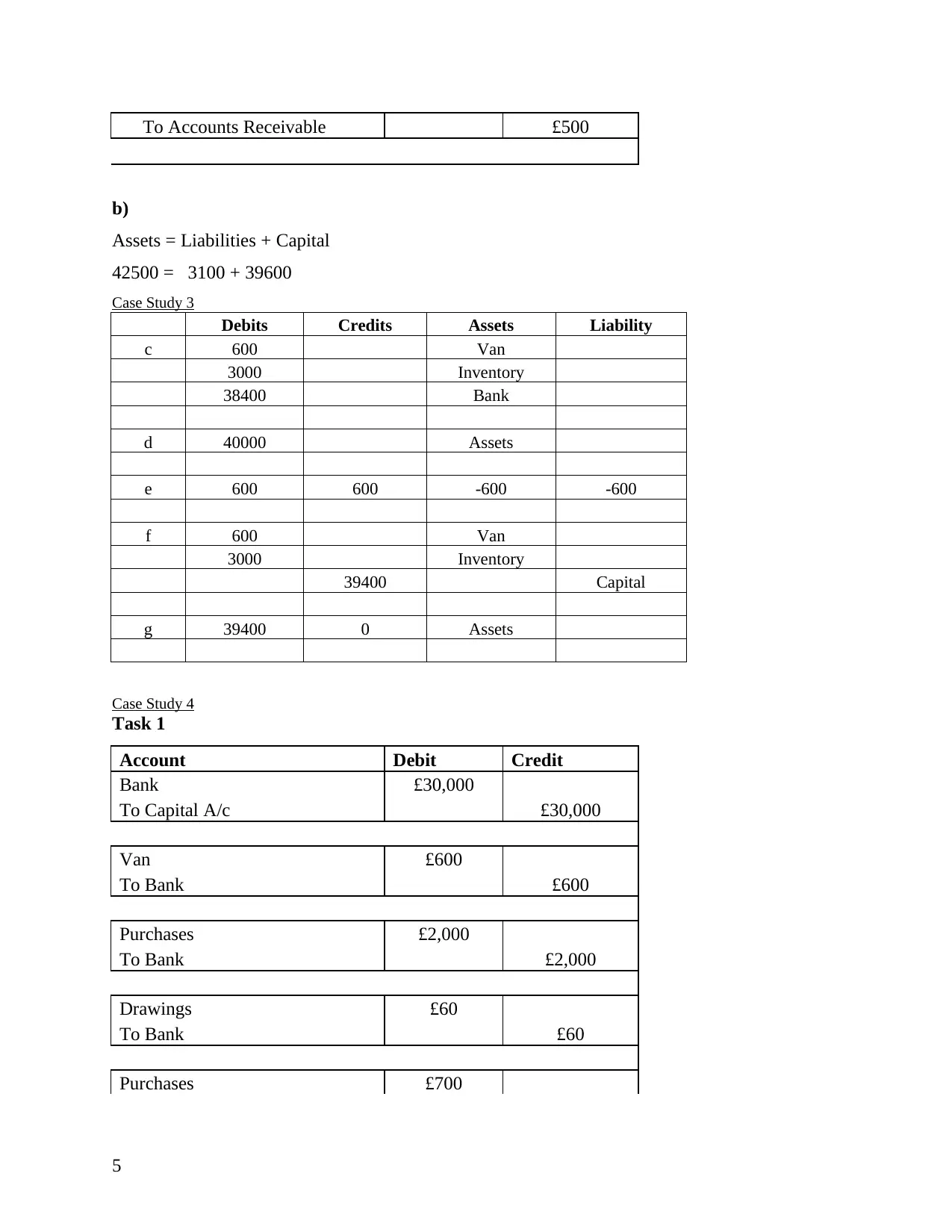

To Accounts Receivable £500

b)

Assets = Liabilities + Capital

42500 = 3100 + 39600

Case Study 3

Debits Credits Assets Liability

c 600 Van

3000 Inventory

38400 Bank

d 40000 Assets

e 600 600 -600 -600

f 600 Van

3000 Inventory

39400 Capital

g 39400 0 Assets

Case Study 4

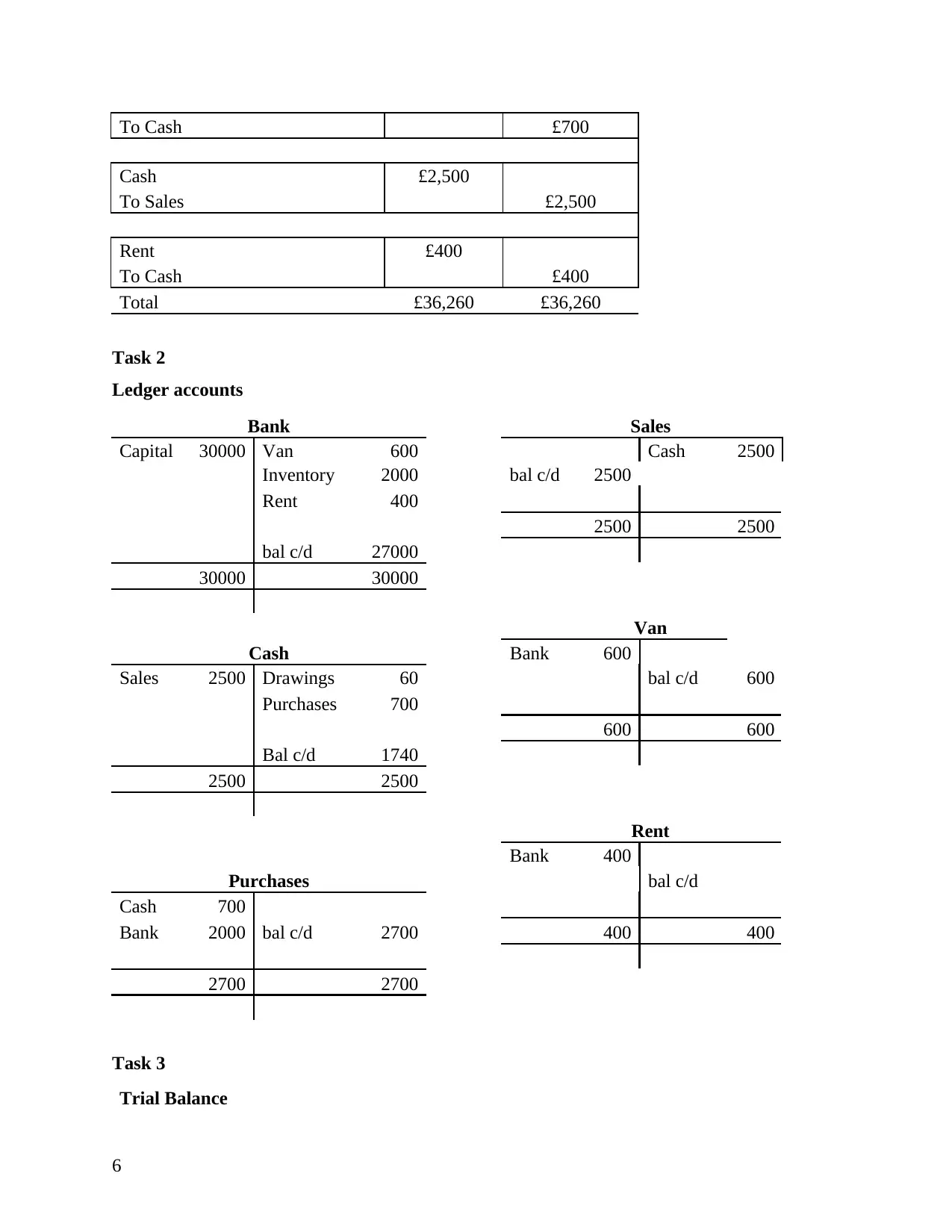

Task 1

Account Debit Credit

Bank £30,000

To Capital A/c £30,000

Van £600

To Bank £600

Purchases £2,000

To Bank £2,000

Drawings £60

To Bank £60

Purchases £700

5

b)

Assets = Liabilities + Capital

42500 = 3100 + 39600

Case Study 3

Debits Credits Assets Liability

c 600 Van

3000 Inventory

38400 Bank

d 40000 Assets

e 600 600 -600 -600

f 600 Van

3000 Inventory

39400 Capital

g 39400 0 Assets

Case Study 4

Task 1

Account Debit Credit

Bank £30,000

To Capital A/c £30,000

Van £600

To Bank £600

Purchases £2,000

To Bank £2,000

Drawings £60

To Bank £60

Purchases £700

5

To Cash £700

Cash £2,500

To Sales £2,500

Rent £400

To Cash £400

Total £36,260 £36,260

Task 2

Ledger accounts

Bank Sales

Capital 30000 Van 600 Cash 2500

Inventory 2000 bal c/d 2500

Rent 400

2500 2500

bal c/d 27000

30000 30000

Van

Cash Bank 600

Sales 2500 Drawings 60 bal c/d 600

Purchases 700

600 600

Bal c/d 1740

2500 2500

Rent

Bank 400

Purchases bal c/d

Cash 700

Bank 2000 bal c/d 2700 400 400

2700 2700

Task 3

Trial Balance

6

Cash £2,500

To Sales £2,500

Rent £400

To Cash £400

Total £36,260 £36,260

Task 2

Ledger accounts

Bank Sales

Capital 30000 Van 600 Cash 2500

Inventory 2000 bal c/d 2500

Rent 400

2500 2500

bal c/d 27000

30000 30000

Van

Cash Bank 600

Sales 2500 Drawings 60 bal c/d 600

Purchases 700

600 600

Bal c/d 1740

2500 2500

Rent

Bank 400

Purchases bal c/d

Cash 700

Bank 2000 bal c/d 2700 400 400

2700 2700

Task 3

Trial Balance

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

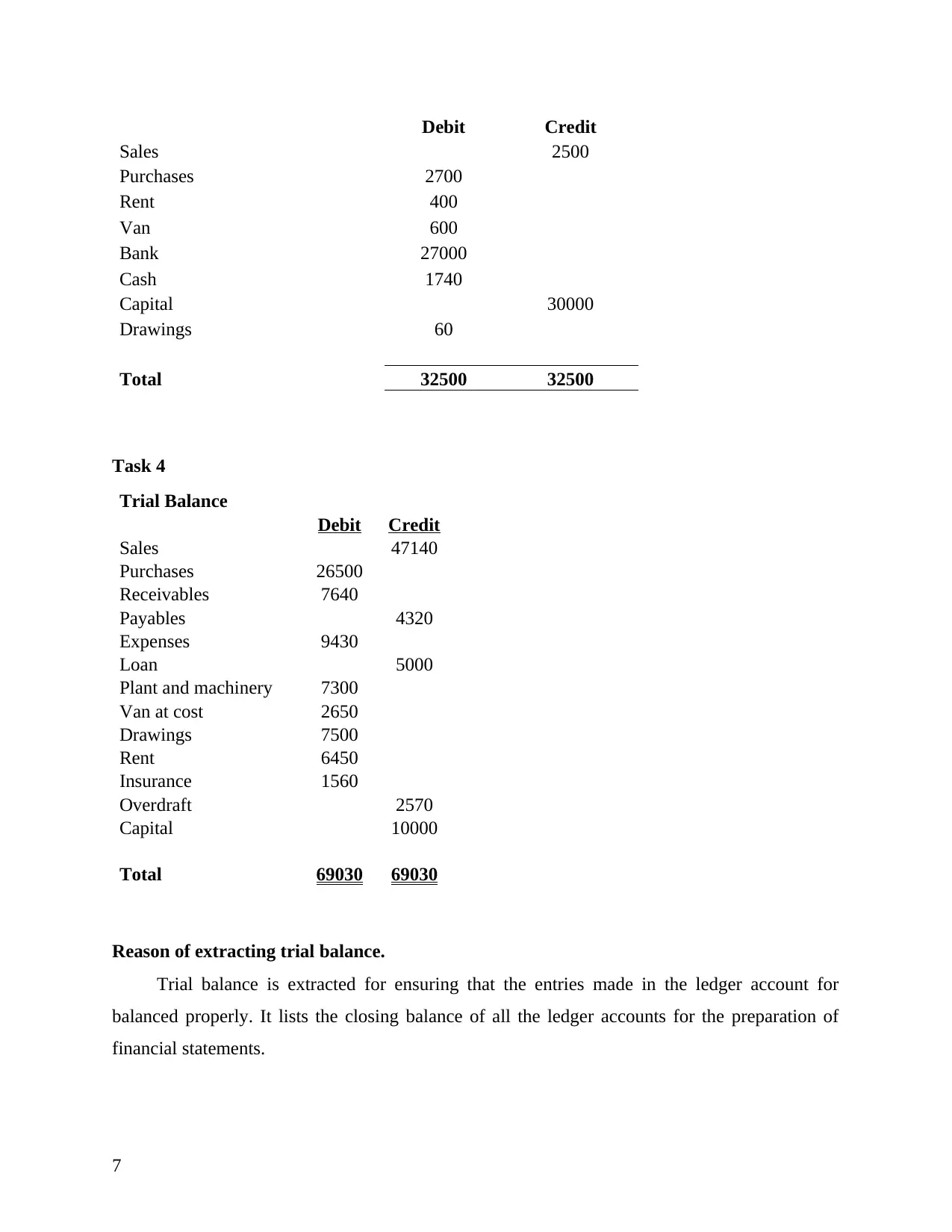

Debit Credit

Sales 2500

Purchases 2700

Rent 400

Van 600

Bank 27000

Cash 1740

Capital 30000

Drawings 60

Total 32500 32500

Task 4

Trial Balance

Debit Credit

Sales 47140

Purchases 26500

Receivables 7640

Payables 4320

Expenses 9430

Loan 5000

Plant and machinery 7300

Van at cost 2650

Drawings 7500

Rent 6450

Insurance 1560

Overdraft 2570

Capital 10000

Total 69030 69030

Reason of extracting trial balance.

Trial balance is extracted for ensuring that the entries made in the ledger account for

balanced properly. It lists the closing balance of all the ledger accounts for the preparation of

financial statements.

7

Sales 2500

Purchases 2700

Rent 400

Van 600

Bank 27000

Cash 1740

Capital 30000

Drawings 60

Total 32500 32500

Task 4

Trial Balance

Debit Credit

Sales 47140

Purchases 26500

Receivables 7640

Payables 4320

Expenses 9430

Loan 5000

Plant and machinery 7300

Van at cost 2650

Drawings 7500

Rent 6450

Insurance 1560

Overdraft 2570

Capital 10000

Total 69030 69030

Reason of extracting trial balance.

Trial balance is extracted for ensuring that the entries made in the ledger account for

balanced properly. It lists the closing balance of all the ledger accounts for the preparation of

financial statements.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

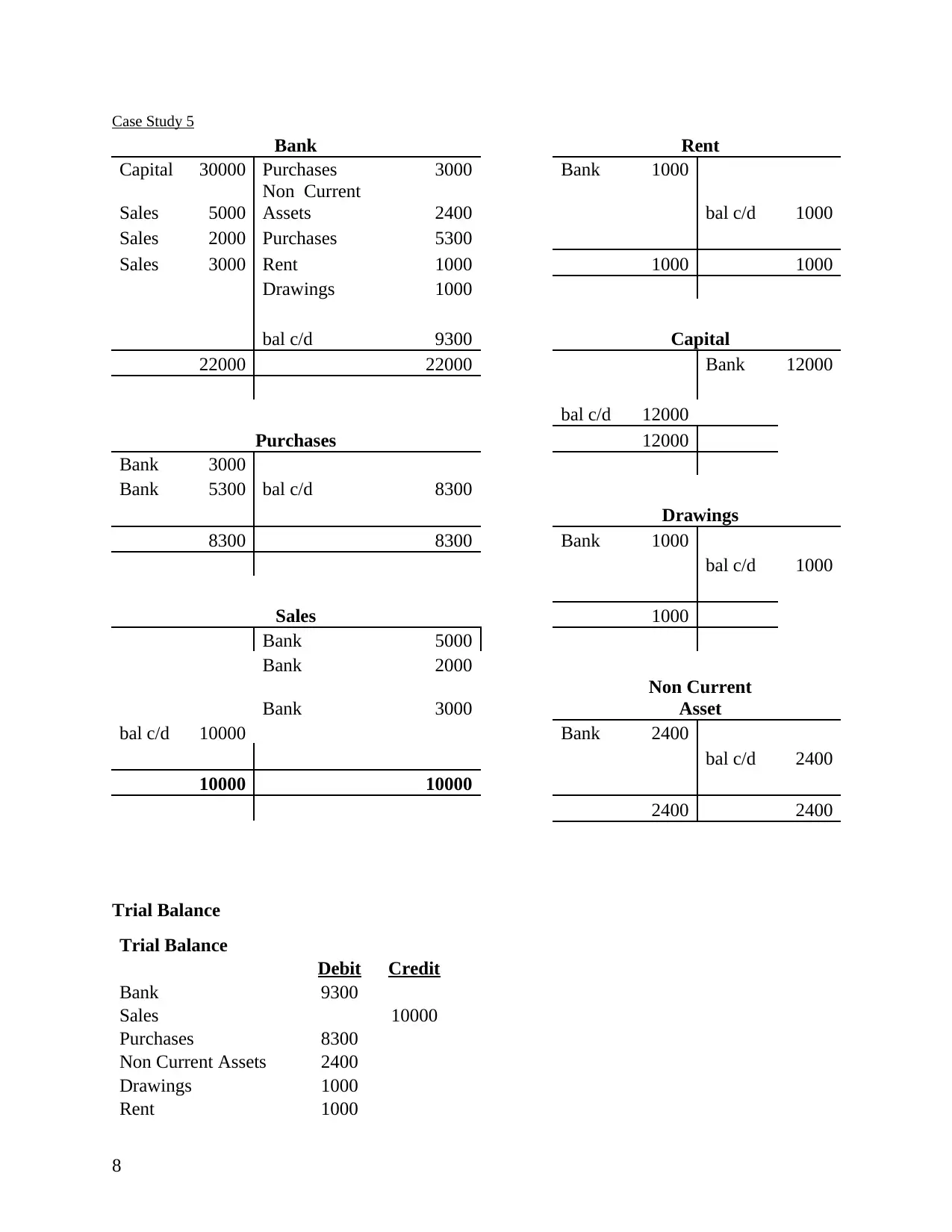

Case Study 5

Bank Rent

Capital 30000 Purchases 3000 Bank 1000

Sales 5000

Non Current

Assets 2400 bal c/d 1000

Sales 2000 Purchases 5300

Sales 3000 Rent 1000 1000 1000

Drawings 1000

bal c/d 9300 Capital

22000 22000 Bank 12000

bal c/d 12000

Purchases 12000

Bank 3000

Bank 5300 bal c/d 8300

Drawings

8300 8300 Bank 1000

bal c/d 1000

Sales 1000

Bank 5000

Bank 2000

Bank 3000

Non Current

Asset

bal c/d 10000 Bank 2400

bal c/d 2400

10000 10000

2400 2400

Trial Balance

Trial Balance

Debit Credit

Bank 9300

Sales 10000

Purchases 8300

Non Current Assets 2400

Drawings 1000

Rent 1000

8

Bank Rent

Capital 30000 Purchases 3000 Bank 1000

Sales 5000

Non Current

Assets 2400 bal c/d 1000

Sales 2000 Purchases 5300

Sales 3000 Rent 1000 1000 1000

Drawings 1000

bal c/d 9300 Capital

22000 22000 Bank 12000

bal c/d 12000

Purchases 12000

Bank 3000

Bank 5300 bal c/d 8300

Drawings

8300 8300 Bank 1000

bal c/d 1000

Sales 1000

Bank 5000

Bank 2000

Bank 3000

Non Current

Asset

bal c/d 10000 Bank 2400

bal c/d 2400

10000 10000

2400 2400

Trial Balance

Trial Balance

Debit Credit

Bank 9300

Sales 10000

Purchases 8300

Non Current Assets 2400

Drawings 1000

Rent 1000

8

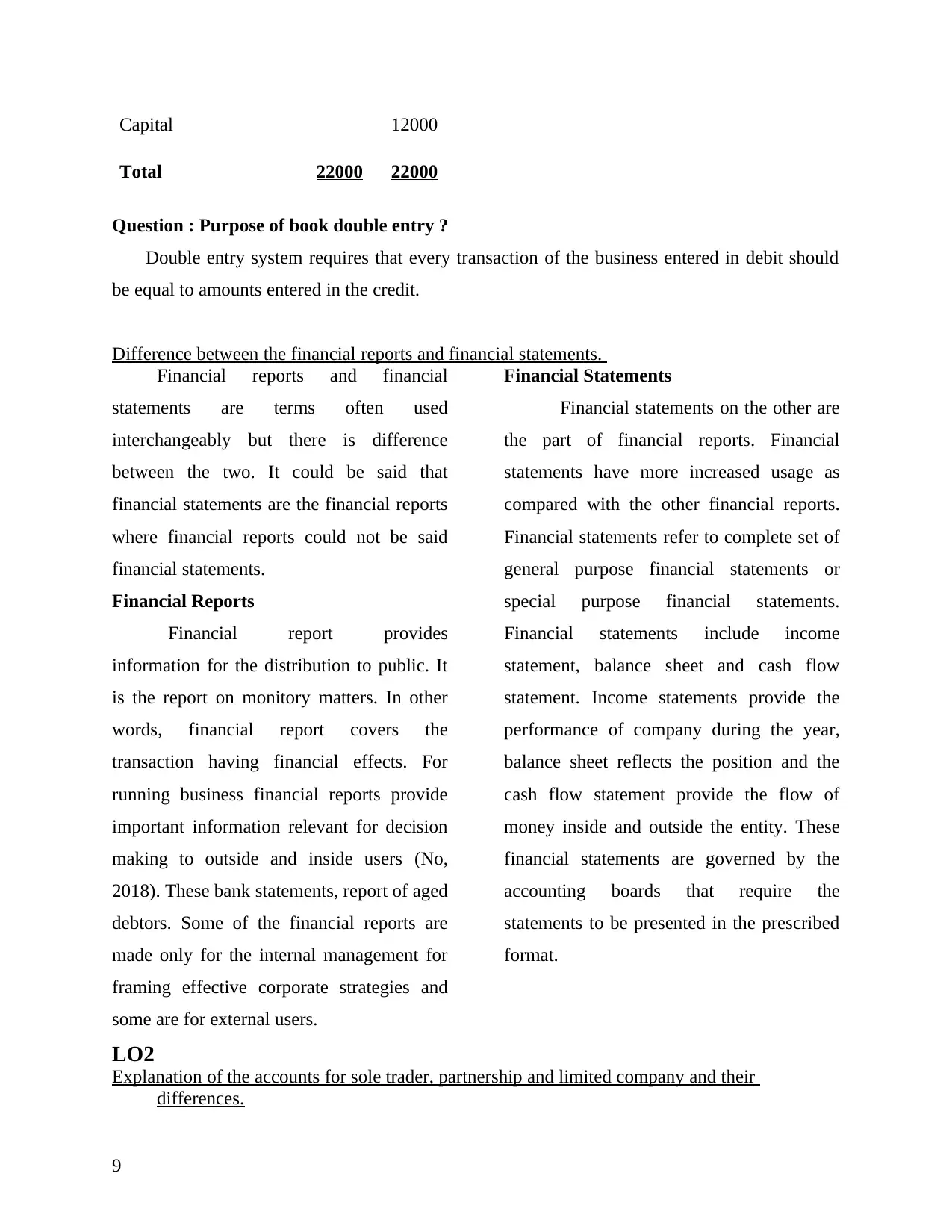

Capital 12000

Total 22000 22000

Question : Purpose of book double entry ?

Double entry system requires that every transaction of the business entered in debit should

be equal to amounts entered in the credit.

Difference between the financial reports and financial statements.

Financial reports and financial

statements are terms often used

interchangeably but there is difference

between the two. It could be said that

financial statements are the financial reports

where financial reports could not be said

financial statements.

Financial Reports

Financial report provides

information for the distribution to public. It

is the report on monitory matters. In other

words, financial report covers the

transaction having financial effects. For

running business financial reports provide

important information relevant for decision

making to outside and inside users (No,

2018). These bank statements, report of aged

debtors. Some of the financial reports are

made only for the internal management for

framing effective corporate strategies and

some are for external users.

Financial Statements

Financial statements on the other are

the part of financial reports. Financial

statements have more increased usage as

compared with the other financial reports.

Financial statements refer to complete set of

general purpose financial statements or

special purpose financial statements.

Financial statements include income

statement, balance sheet and cash flow

statement. Income statements provide the

performance of company during the year,

balance sheet reflects the position and the

cash flow statement provide the flow of

money inside and outside the entity. These

financial statements are governed by the

accounting boards that require the

statements to be presented in the prescribed

format.

LO2

Explanation of the accounts for sole trader, partnership and limited company and their

differences.

9

Total 22000 22000

Question : Purpose of book double entry ?

Double entry system requires that every transaction of the business entered in debit should

be equal to amounts entered in the credit.

Difference between the financial reports and financial statements.

Financial reports and financial

statements are terms often used

interchangeably but there is difference

between the two. It could be said that

financial statements are the financial reports

where financial reports could not be said

financial statements.

Financial Reports

Financial report provides

information for the distribution to public. It

is the report on monitory matters. In other

words, financial report covers the

transaction having financial effects. For

running business financial reports provide

important information relevant for decision

making to outside and inside users (No,

2018). These bank statements, report of aged

debtors. Some of the financial reports are

made only for the internal management for

framing effective corporate strategies and

some are for external users.

Financial Statements

Financial statements on the other are

the part of financial reports. Financial

statements have more increased usage as

compared with the other financial reports.

Financial statements refer to complete set of

general purpose financial statements or

special purpose financial statements.

Financial statements include income

statement, balance sheet and cash flow

statement. Income statements provide the

performance of company during the year,

balance sheet reflects the position and the

cash flow statement provide the flow of

money inside and outside the entity. These

financial statements are governed by the

accounting boards that require the

statements to be presented in the prescribed

format.

LO2

Explanation of the accounts for sole trader, partnership and limited company and their

differences.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sole Trader

Sole trader is a form of business

where the owner is self employed and runs

the business as individual. In sole trader

business owner is solely responsible for the

debts and obligations of the business. Sole

trader has an unlimited liability over the

business. Sole trader is not required to

prepare accounts as per the required

accounting standards. They are not required

to comply with the regulations for

preparation of financial records. There is no

prescribed format for the sole trade to

prepare its accounts. Accounts of sole trader

are prepared as per the requirement of

owners. Sole trader enjoy the whole profits

unlike the partnership and limited company.

Partnership

Partnership refers to form of

business in which 2 or more people come

together for carrying out the business.

Partners pool resources in partnership for

starting the business. Partnership is formed

on oral or written agreements on mutual

agreements of the partners. Profit and losses

are shared in the partnership firm in the ratio

agreed between them in agreements.

Partnership firms are required to prepare

accounts as per the partnership act (Robson,

Young and Power, 2017). They are not

required to prepare the financial statement as

per the accounting standards for reporting to

the public. Liability of the partners is

unlimited in the unlimited partnership and

limited in the limited partnership firm to the

extent of their contribution in the business.

In a partnership business tax is charged on

the individual income of partners and not

over the partnership firms.

Limited Company

Limited company is the organisation

set up for running a business. Unlike the

sole trader and partnership finance of the

business are separate from the personal

finances. A company is a separate legal

entity different from its owners. Company is

required to comply with all the regulations.

Companies are required to prepare financial

statements as per the accounting standards

given by the accounting bodies. For

preparation of financial statements all the

reporting framework and governing

principles are followed by the management.

Accounts of companies are audited for

ensuring that statements are free from errors

and misstatements before they are issued to

the public. Liabilities of company do not

extend to personal assets of owners. Also the

corporation tax is charged over the profits of

company and not like sole trader and

partnership business.

10

Sole trader is a form of business

where the owner is self employed and runs

the business as individual. In sole trader

business owner is solely responsible for the

debts and obligations of the business. Sole

trader has an unlimited liability over the

business. Sole trader is not required to

prepare accounts as per the required

accounting standards. They are not required

to comply with the regulations for

preparation of financial records. There is no

prescribed format for the sole trade to

prepare its accounts. Accounts of sole trader

are prepared as per the requirement of

owners. Sole trader enjoy the whole profits

unlike the partnership and limited company.

Partnership

Partnership refers to form of

business in which 2 or more people come

together for carrying out the business.

Partners pool resources in partnership for

starting the business. Partnership is formed

on oral or written agreements on mutual

agreements of the partners. Profit and losses

are shared in the partnership firm in the ratio

agreed between them in agreements.

Partnership firms are required to prepare

accounts as per the partnership act (Robson,

Young and Power, 2017). They are not

required to prepare the financial statement as

per the accounting standards for reporting to

the public. Liability of the partners is

unlimited in the unlimited partnership and

limited in the limited partnership firm to the

extent of their contribution in the business.

In a partnership business tax is charged on

the individual income of partners and not

over the partnership firms.

Limited Company

Limited company is the organisation

set up for running a business. Unlike the

sole trader and partnership finance of the

business are separate from the personal

finances. A company is a separate legal

entity different from its owners. Company is

required to comply with all the regulations.

Companies are required to prepare financial

statements as per the accounting standards

given by the accounting bodies. For

preparation of financial statements all the

reporting framework and governing

principles are followed by the management.

Accounts of companies are audited for

ensuring that statements are free from errors

and misstatements before they are issued to

the public. Liabilities of company do not

extend to personal assets of owners. Also the

corporation tax is charged over the profits of

company and not like sole trader and

partnership business.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

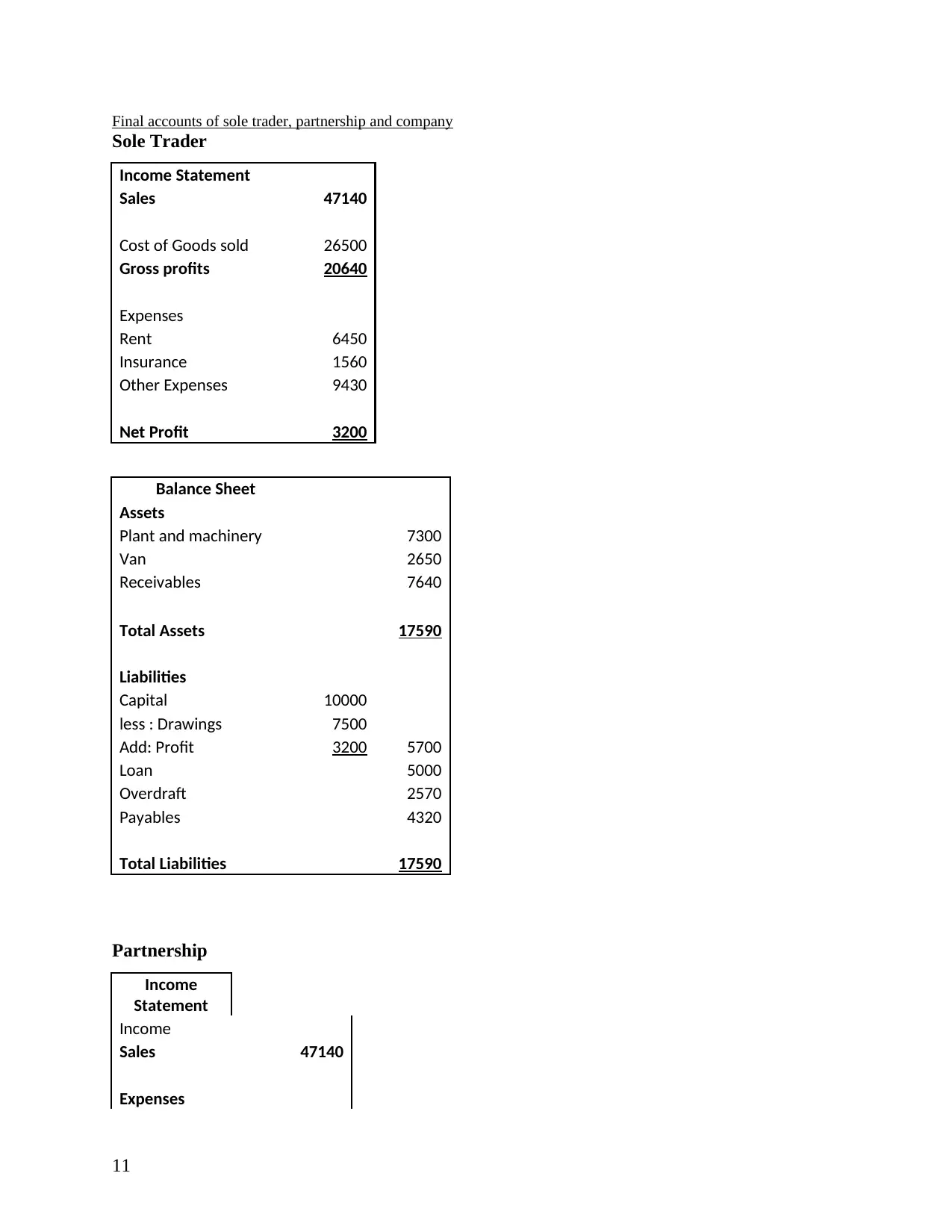

Final accounts of sole trader, partnership and company

Sole Trader

Income Statement

Sales 47140

Cost of Goods sold 26500

Gross profits 20640

Expenses

Rent 6450

Insurance 1560

Other Expenses 9430

Net Profit 3200

Balance Sheet

Assets

Plant and machinery 7300

Van 2650

Receivables 7640

Total Assets 17590

Liabilities

Capital 10000

less : Drawings 7500

Add: Profit 3200 5700

Loan 5000

Overdraft 2570

Payables 4320

Total Liabilities 17590

Partnership

Income

Statement

Income

Sales 47140

Expenses

11

Sole Trader

Income Statement

Sales 47140

Cost of Goods sold 26500

Gross profits 20640

Expenses

Rent 6450

Insurance 1560

Other Expenses 9430

Net Profit 3200

Balance Sheet

Assets

Plant and machinery 7300

Van 2650

Receivables 7640

Total Assets 17590

Liabilities

Capital 10000

less : Drawings 7500

Add: Profit 3200 5700

Loan 5000

Overdraft 2570

Payables 4320

Total Liabilities 17590

Partnership

Income

Statement

Income

Sales 47140

Expenses

11

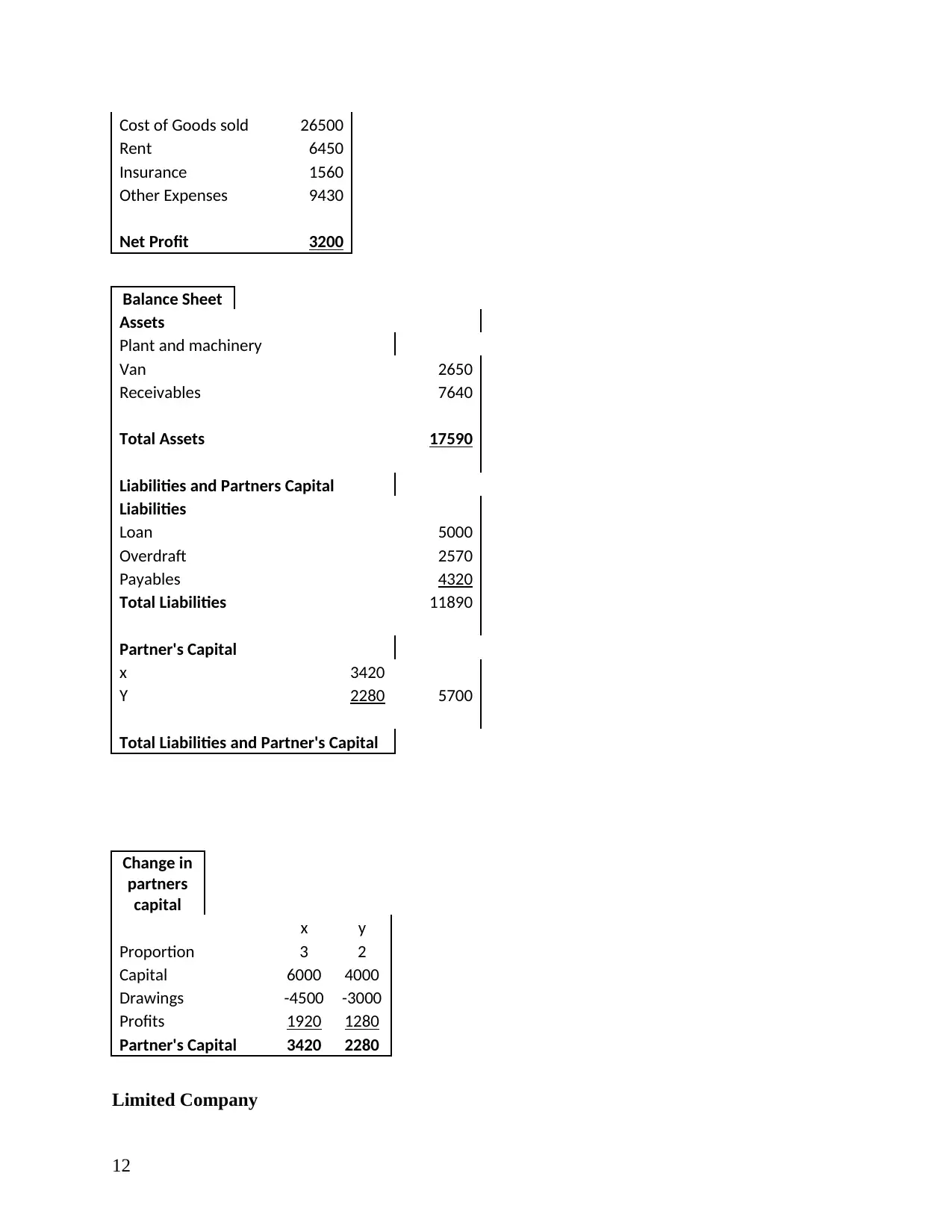

Cost of Goods sold 26500

Rent 6450

Insurance 1560

Other Expenses 9430

Net Profit 3200

Balance Sheet

Assets

Plant and machinery

Van 2650

Receivables 7640

Total Assets 17590

Liabilities and Partners Capital

Liabilities

Loan 5000

Overdraft 2570

Payables 4320

Total Liabilities 11890

Partner's Capital

x 3420

Y 2280 5700

Total Liabilities and Partner's Capital

Change in

partners

capital

x y

Proportion 3 2

Capital 6000 4000

Drawings -4500 -3000

Profits 1920 1280

Partner's Capital 3420 2280

Limited Company

12

Rent 6450

Insurance 1560

Other Expenses 9430

Net Profit 3200

Balance Sheet

Assets

Plant and machinery

Van 2650

Receivables 7640

Total Assets 17590

Liabilities and Partners Capital

Liabilities

Loan 5000

Overdraft 2570

Payables 4320

Total Liabilities 11890

Partner's Capital

x 3420

Y 2280 5700

Total Liabilities and Partner's Capital

Change in

partners

capital

x y

Proportion 3 2

Capital 6000 4000

Drawings -4500 -3000

Profits 1920 1280

Partner's Capital 3420 2280

Limited Company

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.