Regulation of Financial Institutions in India: RBI, IRDA, SEBI Report

VerifiedAdded on 2021/09/18

|33

|10735

|293

Report

AI Summary

This report provides a comprehensive overview of financial regulations in India, focusing on the Reserve Bank of India (RBI), the Insurance Regulatory and Development Authority (IRDA), and the Securities and Exchange Board of India (SEBI). The report examines the RBI's role in regulating the banking sector through the RBI Act and the Banking Regulation Act, including credit control measures like reserve ratios, open market operations, and moral suasion, as well as the licensing and supervision of banks. It then delves into insurance laws and the functions of IRDA in protecting policyholders and ensuring the systematic growth of the insurance sector, covering both life and general insurance. Finally, the report explores SEBI's role as a statutory regulatory body responsible for regulating the Indian capital markets, protecting investor interests, and promoting the development of the securities market, including its functions related to issuers, traders, and financial intermediaries. The report highlights the objectives, functions, and powers of each regulatory body, providing a detailed understanding of the financial regulatory landscape in India.

1

Session 21

RBI and Banking Regulation Act

The Indian banking sector is regulated by the Reserve Bank of India Act 1934 (RBI Act) and

the Banking Regulation Act 1949 (BR Act). The Reserve Bank of India (RBI), India’s central

bank, issues various guidelines, notifications and policies from time to time to regulate the

banking sector. In addition, the Foreign Exchange Management Act 1999 (FEMA) regulates

cross-border exchange transactions by Indian entities, including banks.

India has both private sector banks (which include branches and subsidiaries of foreign banks)

and public-sector banks (ie, banks in which the government directly or indirectly holds

ownership interest). Banks in India can primarily be classified as:

scheduled commercial banks (ie, commercial banks performing all banking functions);

cooperative banks (set up by cooperative societies for providing financing to small

borrowers); and

regional rural banks (RRBs) (for providing credit to rural and agricultural areas)

Recently, the RBI has also introduced specialised banks such as payments banks and small

finance banks that perform only some banking functions.

The objectives of bank regulation, and the emphasis, vary between jurisdictions. The most

common objectives are:

Prudential - to reduce the level of risk to which bank creditors are exposed (i.e. to protect

depositors)

Systemic risk reduction - to reduce the risk of disruption resulting from adverse trading

conditions for banks causing multiple or major bank failures

To avoid misuse of banks - to reduce the risk of banks being used for criminal purposes,

e.g. laundering the proceeds of crime

To protect banking confidentiality

Credit allocation - to direct credit to favoured sectors

It may also include rules about treating customers fairly and having corporate social

responsibility.

Bank regulation is a complex process and generally consists of two components:

licensing, and

supervision.

The first component, licensing, sets certain requirements for starting a new bank. Licensing

provides the licence holders the right to own and to operate a bank. Licensing involves an

Session 21

RBI and Banking Regulation Act

The Indian banking sector is regulated by the Reserve Bank of India Act 1934 (RBI Act) and

the Banking Regulation Act 1949 (BR Act). The Reserve Bank of India (RBI), India’s central

bank, issues various guidelines, notifications and policies from time to time to regulate the

banking sector. In addition, the Foreign Exchange Management Act 1999 (FEMA) regulates

cross-border exchange transactions by Indian entities, including banks.

India has both private sector banks (which include branches and subsidiaries of foreign banks)

and public-sector banks (ie, banks in which the government directly or indirectly holds

ownership interest). Banks in India can primarily be classified as:

scheduled commercial banks (ie, commercial banks performing all banking functions);

cooperative banks (set up by cooperative societies for providing financing to small

borrowers); and

regional rural banks (RRBs) (for providing credit to rural and agricultural areas)

Recently, the RBI has also introduced specialised banks such as payments banks and small

finance banks that perform only some banking functions.

The objectives of bank regulation, and the emphasis, vary between jurisdictions. The most

common objectives are:

Prudential - to reduce the level of risk to which bank creditors are exposed (i.e. to protect

depositors)

Systemic risk reduction - to reduce the risk of disruption resulting from adverse trading

conditions for banks causing multiple or major bank failures

To avoid misuse of banks - to reduce the risk of banks being used for criminal purposes,

e.g. laundering the proceeds of crime

To protect banking confidentiality

Credit allocation - to direct credit to favoured sectors

It may also include rules about treating customers fairly and having corporate social

responsibility.

Bank regulation is a complex process and generally consists of two components:

licensing, and

supervision.

The first component, licensing, sets certain requirements for starting a new bank. Licensing

provides the licence holders the right to own and to operate a bank. Licensing involves an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

evaluation of the entity's intent and the ability to meet the regulatory guidelines governing the

bank's operations, financial soundness, and managerial actions. The regulator supervises

licensed banks for compliance with the requirements and responds to breaches of the

requirements by obtaining undertakings, giving directions, imposing penalties or (ultimately)

revoking the bank's license.

The second component, namely, supervision, is an extension of the licence-granting process

and consists of supervision of the bank's activities by a government regulatory body i e The

RBI. Supervision ensures that the functioning of the bank complies with the regulatory

guidelines and monitors for possible deviations from regulatory standards. Supervisory

activities involve on-site inspection of the bank's records, operations and processes or

evaluation of the reports submitted by the bank.

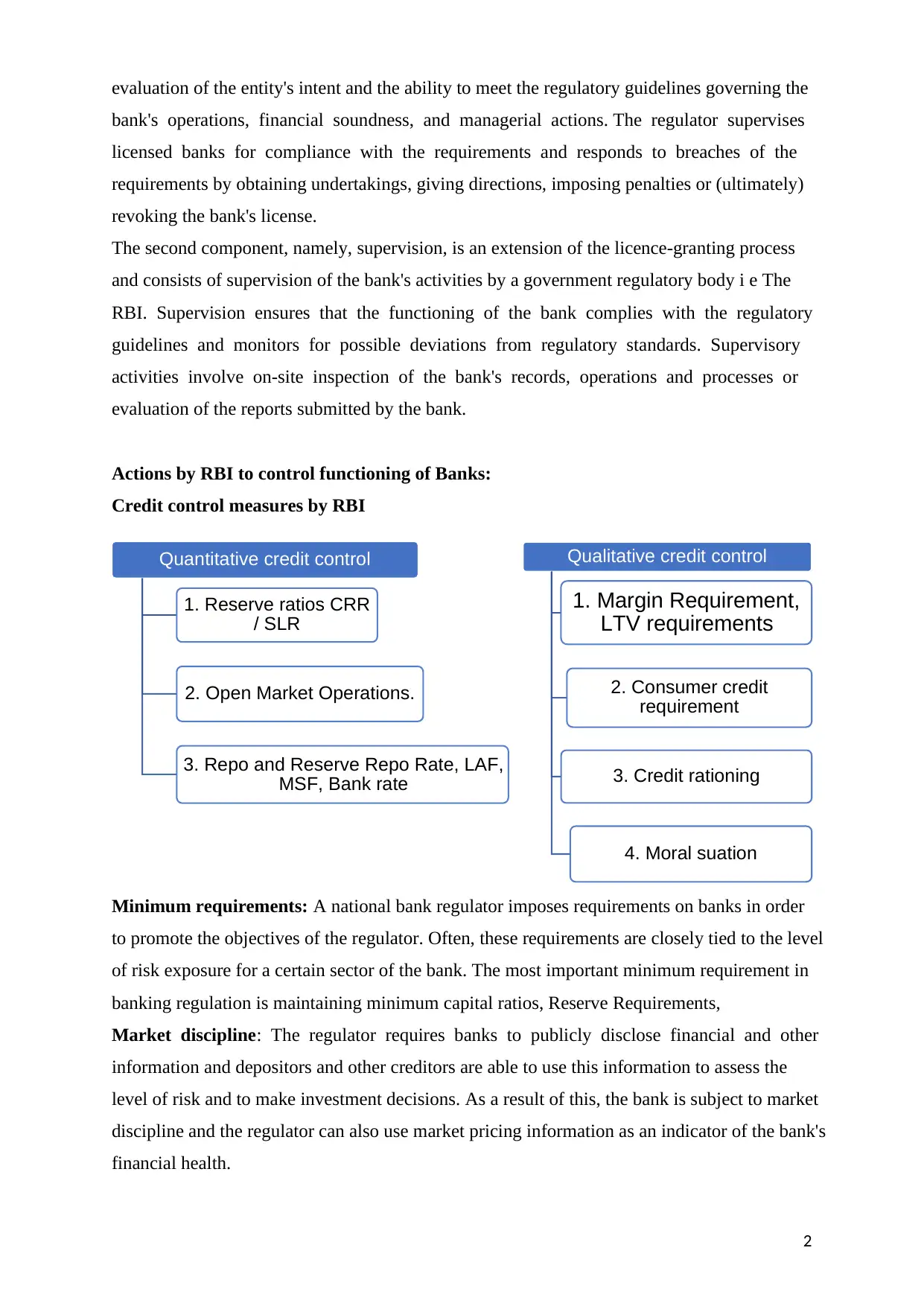

Actions by RBI to control functioning of Banks:

Credit control measures by RBI

Minimum requirements: A national bank regulator imposes requirements on banks in order

to promote the objectives of the regulator. Often, these requirements are closely tied to the level

of risk exposure for a certain sector of the bank. The most important minimum requirement in

banking regulation is maintaining minimum capital ratios, Reserve Requirements,

Market discipline: The regulator requires banks to publicly disclose financial and other

information and depositors and other creditors are able to use this information to assess the

level of risk and to make investment decisions. As a result of this, the bank is subject to market

discipline and the regulator can also use market pricing information as an indicator of the bank's

financial health.

Quantitative credit control

1. Reserve ratios CRR

/ SLR

2. Open Market Operations.

3. Repo and Reserve Repo Rate, LAF,

MSF, Bank rate

Qualitative credit control

1. Margin Requirement,

LTV requirements

2. Consumer credit

requirement

3. Credit rationing

4. Moral suation

evaluation of the entity's intent and the ability to meet the regulatory guidelines governing the

bank's operations, financial soundness, and managerial actions. The regulator supervises

licensed banks for compliance with the requirements and responds to breaches of the

requirements by obtaining undertakings, giving directions, imposing penalties or (ultimately)

revoking the bank's license.

The second component, namely, supervision, is an extension of the licence-granting process

and consists of supervision of the bank's activities by a government regulatory body i e The

RBI. Supervision ensures that the functioning of the bank complies with the regulatory

guidelines and monitors for possible deviations from regulatory standards. Supervisory

activities involve on-site inspection of the bank's records, operations and processes or

evaluation of the reports submitted by the bank.

Actions by RBI to control functioning of Banks:

Credit control measures by RBI

Minimum requirements: A national bank regulator imposes requirements on banks in order

to promote the objectives of the regulator. Often, these requirements are closely tied to the level

of risk exposure for a certain sector of the bank. The most important minimum requirement in

banking regulation is maintaining minimum capital ratios, Reserve Requirements,

Market discipline: The regulator requires banks to publicly disclose financial and other

information and depositors and other creditors are able to use this information to assess the

level of risk and to make investment decisions. As a result of this, the bank is subject to market

discipline and the regulator can also use market pricing information as an indicator of the bank's

financial health.

Quantitative credit control

1. Reserve ratios CRR

/ SLR

2. Open Market Operations.

3. Repo and Reserve Repo Rate, LAF,

MSF, Bank rate

Qualitative credit control

1. Margin Requirement,

LTV requirements

2. Consumer credit

requirement

3. Credit rationing

4. Moral suation

3

Corporate governance: Corporate governance requirements are intended to encourage the

bank to be well managed, and is an indirect way of achieving other objectives. As many banks

are relatively large, and with many divisions, it is important for management to maintain a

close watch on all operations. I

Financial reporting and disclosure requirements: Among the most important regulations

that are placed on banking institutions is the requirement for disclosure of the bank's finances

Credit rating requirement: Banks may be required to obtain and maintain a current credit

rating from an approved credit rating agency, and to disclose it to investors and prospective

investors. Also, banks may be required to maintain a minimum credit rating.

Further to the above:

The RBI conducts periodic audits and also acts as a consumer disputes ombudsman for

retail banking.

RBI also supervises the Indian banking system through various methods such as on-site

inspection, surveillance and reviewing regulatory filings made by the banks.

The RBI also monitors compliance on an ongoing basis by requiring banks to submit

detailed information periodically under an off-site surveillance and monitoring system.

The RBI can conduct compulsory amalgamations:

in the public interest;

in the interests of depositors of a bank;

to secure proper management of a bank; or

in the larger interests of the banking system.

In addition, the RBI has wide powers in appropriate cases to:

require banks to make changes in their management as the RBI considers necessary;

remove any chairman, director, chief executive officer or other employee of a bank;

appoint additional directors to the board of directors of a bank; and

supersede the board of directors of a bank for a maximum period of 12 months and

instead appoint an administrator.

The RBI has the power of winding-up of a banking company. An order for the winding-up

of a banking company can be passed by a High Court:

if it is unable to pay its debts;

if an application has been made by the RBI; or

on request of the GOI.

Corporate governance: Corporate governance requirements are intended to encourage the

bank to be well managed, and is an indirect way of achieving other objectives. As many banks

are relatively large, and with many divisions, it is important for management to maintain a

close watch on all operations. I

Financial reporting and disclosure requirements: Among the most important regulations

that are placed on banking institutions is the requirement for disclosure of the bank's finances

Credit rating requirement: Banks may be required to obtain and maintain a current credit

rating from an approved credit rating agency, and to disclose it to investors and prospective

investors. Also, banks may be required to maintain a minimum credit rating.

Further to the above:

The RBI conducts periodic audits and also acts as a consumer disputes ombudsman for

retail banking.

RBI also supervises the Indian banking system through various methods such as on-site

inspection, surveillance and reviewing regulatory filings made by the banks.

The RBI also monitors compliance on an ongoing basis by requiring banks to submit

detailed information periodically under an off-site surveillance and monitoring system.

The RBI can conduct compulsory amalgamations:

in the public interest;

in the interests of depositors of a bank;

to secure proper management of a bank; or

in the larger interests of the banking system.

In addition, the RBI has wide powers in appropriate cases to:

require banks to make changes in their management as the RBI considers necessary;

remove any chairman, director, chief executive officer or other employee of a bank;

appoint additional directors to the board of directors of a bank; and

supersede the board of directors of a bank for a maximum period of 12 months and

instead appoint an administrator.

The RBI has the power of winding-up of a banking company. An order for the winding-up

of a banking company can be passed by a High Court:

if it is unable to pay its debts;

if an application has been made by the RBI; or

on request of the GOI.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Session 22

Insurance Laws and IRDA

The word insurance means an arrangement for protection against any likely loss or damage.

Insurance contracts are based on the contingency of an event which causes a loss. Such

contracts are legal agreements which are entered into between two parties wherein, the

company promises to make good the loss as and when it occurs, in return for a regular premium

to be paid by the party.

In India, several insurance laws have been enacted to save the interest of the various

policyholders. Health insurance, fire insurance, car insurance, marine insurance, life insurance,

etc are few examples of the insurance available in India.

There are two main categories of Insurance:

1. Life insurance - Life Insurance is a legal agreement wherein financial compensation is

provided in cases of death or disability. It can be availed by paying lumpsum amount or by

making periodic instalments so as to save the vested interest of your family in your absence.

The periodic instalments are termed as premium.

Depending upon its coverage:

Life insurance can be further classified into either whole life insurance, endowment policy,

life term etc.

2. General insurance- General insurance provides protection from any loss other than life

insurance.

It includes:

Travel insurance

Health insurance

Home insurance

Motor insurance

Fire insurance

To regulate the insurance sector, several regulatory authorities have been formed:

IRDA (Insurance Regulatory and Development Authority)

Tariff Advisory Committee

Insurance Association of India, councils and committees

Ombudsman

Session 22

Insurance Laws and IRDA

The word insurance means an arrangement for protection against any likely loss or damage.

Insurance contracts are based on the contingency of an event which causes a loss. Such

contracts are legal agreements which are entered into between two parties wherein, the

company promises to make good the loss as and when it occurs, in return for a regular premium

to be paid by the party.

In India, several insurance laws have been enacted to save the interest of the various

policyholders. Health insurance, fire insurance, car insurance, marine insurance, life insurance,

etc are few examples of the insurance available in India.

There are two main categories of Insurance:

1. Life insurance - Life Insurance is a legal agreement wherein financial compensation is

provided in cases of death or disability. It can be availed by paying lumpsum amount or by

making periodic instalments so as to save the vested interest of your family in your absence.

The periodic instalments are termed as premium.

Depending upon its coverage:

Life insurance can be further classified into either whole life insurance, endowment policy,

life term etc.

2. General insurance- General insurance provides protection from any loss other than life

insurance.

It includes:

Travel insurance

Health insurance

Home insurance

Motor insurance

Fire insurance

To regulate the insurance sector, several regulatory authorities have been formed:

IRDA (Insurance Regulatory and Development Authority)

Tariff Advisory Committee

Insurance Association of India, councils and committees

Ombudsman

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Every insurer seeking to carry on the insurance business in India is required to obtain the

certificate of registration from the IRDA prior to commencement of business. However,

conditions for applying have been envisaged in various Acts.

The Acts relating to general insurance business in India are:

I. Insurance Act 1938

II. Marine Insurance Act 1963

III. Motor Vehicles Act, 1939

IV. Motor Vehicles Act, 1988

V. Inland Steam Vessels Act, 1917

VI. General Insurance Business (Nationalisation) Act,1972

VII. Carriers Act,1865, etc

The Indian Government however after several years, implemented the changes recommended

by the Malhotra Committee and made changes in insurance act,1938 and General insurance

business act,1972.

IRDA- Insurance Regulatory and Development Authority: It is a regulatory body which

regulates and the general insurance and life insurance in India.

IRDA functions and ensures:

To protect the interest of policyholders in all insurance contracts. It ensures smooth and

systematic transactions between the policy holders and the insurance companies. The

authority governs the conduct of the various insurance businesses.

IRDA clarifies the code of conduct for all insurance companies, surveyors, and loss

assessors. It ensures that companies do not ignore the requests of the general public. It

ensures that no misdeed happen and for this it regulates through regular audits investigation

into the working of all the insurance companies or intermediaries. It regulates the rates and

terms offered by the insurance companies to bring equality for the customers.

In cases of any dispute between the insurer and the policyholder, IRDA will ensure a

resolution.

Functions of IRDA:

1. Protecting interest of policyholders

2. Systematic growth of insurance sector

3. Amicable resolution of conflicts.

Every insurer seeking to carry on the insurance business in India is required to obtain the

certificate of registration from the IRDA prior to commencement of business. However,

conditions for applying have been envisaged in various Acts.

The Acts relating to general insurance business in India are:

I. Insurance Act 1938

II. Marine Insurance Act 1963

III. Motor Vehicles Act, 1939

IV. Motor Vehicles Act, 1988

V. Inland Steam Vessels Act, 1917

VI. General Insurance Business (Nationalisation) Act,1972

VII. Carriers Act,1865, etc

The Indian Government however after several years, implemented the changes recommended

by the Malhotra Committee and made changes in insurance act,1938 and General insurance

business act,1972.

IRDA- Insurance Regulatory and Development Authority: It is a regulatory body which

regulates and the general insurance and life insurance in India.

IRDA functions and ensures:

To protect the interest of policyholders in all insurance contracts. It ensures smooth and

systematic transactions between the policy holders and the insurance companies. The

authority governs the conduct of the various insurance businesses.

IRDA clarifies the code of conduct for all insurance companies, surveyors, and loss

assessors. It ensures that companies do not ignore the requests of the general public. It

ensures that no misdeed happen and for this it regulates through regular audits investigation

into the working of all the insurance companies or intermediaries. It regulates the rates and

terms offered by the insurance companies to bring equality for the customers.

In cases of any dispute between the insurer and the policyholder, IRDA will ensure a

resolution.

Functions of IRDA:

1. Protecting interest of policyholders

2. Systematic growth of insurance sector

3. Amicable resolution of conflicts.

6

4. Regular monitoring so as to check any discrepancies /frauds etc.

5. Fair dealings in the market.

For the systematic growth of the economy, it is imperative that government should establish

authorities who govern the working of the companies, ex- insurance companies. An

investor must be protected from any fraudulent activities and his money must be utilised

and put to judicious use. Like Banking sector, is governed by RBI and the later regulates

the entire functioning of the banks, similarly, IRDA regulates all insurance companies

managing different insurance operations.

4. Regular monitoring so as to check any discrepancies /frauds etc.

5. Fair dealings in the market.

For the systematic growth of the economy, it is imperative that government should establish

authorities who govern the working of the companies, ex- insurance companies. An

investor must be protected from any fraudulent activities and his money must be utilised

and put to judicious use. Like Banking sector, is governed by RBI and the later regulates

the entire functioning of the banks, similarly, IRDA regulates all insurance companies

managing different insurance operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Session 23

SEBI as a regulator:

Securities and Exchange Board of India (SEBI) is a statutory regulatory body entrusted with

the responsibility to regulate the Indian capital markets. It monitors and regulates the securities

market and protects the interests of the investors by enforcing certain rules and regulations.

The SEBI is the regulatory authority in India established under Section 3 of SEBI Act to protect

the interests of the investors in securities and to promote the development of, and to regulate,

the securities market and for matters connected therewith and incidental thereto. Main

objectives of SEBI are as follows:

Protecting the interests of investors in securities and promoting and regulating the

development of the securities market

Regulating the business in stock exchanges

Registering and regulating the working of stock brokers, sub–brokers, share transfer agent

etc.

Registering and regulating the working of venture capital funds, collective investment

schemes (like mutual funds) etc

Promoting investor’s education and training intermediaries

Promoting and regulating self-regulatory organizations

Prohibiting fraudulent and unfair trade practices

Calling for information from, undertaking inspection, conducting inquiries and audits of

the stock exchanges, intermediaries, self – regulatory organizations, mutual funds and other

persons associated with the securities market

SEBI, just like any corporate firm has a hierarchical structure and consists of numerous

departments headed by their respective heads. Following is a list of some of the departments:

Foreign Portfolio Investors and Custodians

Human Resources Department

Information Technology

Investment Management Department

Office of International Affairs

Commodity and Derivative Market Regulation Department

National Institute of Securities Market

Session 23

SEBI as a regulator:

Securities and Exchange Board of India (SEBI) is a statutory regulatory body entrusted with

the responsibility to regulate the Indian capital markets. It monitors and regulates the securities

market and protects the interests of the investors by enforcing certain rules and regulations.

The SEBI is the regulatory authority in India established under Section 3 of SEBI Act to protect

the interests of the investors in securities and to promote the development of, and to regulate,

the securities market and for matters connected therewith and incidental thereto. Main

objectives of SEBI are as follows:

Protecting the interests of investors in securities and promoting and regulating the

development of the securities market

Regulating the business in stock exchanges

Registering and regulating the working of stock brokers, sub–brokers, share transfer agent

etc.

Registering and regulating the working of venture capital funds, collective investment

schemes (like mutual funds) etc

Promoting investor’s education and training intermediaries

Promoting and regulating self-regulatory organizations

Prohibiting fraudulent and unfair trade practices

Calling for information from, undertaking inspection, conducting inquiries and audits of

the stock exchanges, intermediaries, self – regulatory organizations, mutual funds and other

persons associated with the securities market

SEBI, just like any corporate firm has a hierarchical structure and consists of numerous

departments headed by their respective heads. Following is a list of some of the departments:

Foreign Portfolio Investors and Custodians

Human Resources Department

Information Technology

Investment Management Department

Office of International Affairs

Commodity and Derivative Market Regulation Department

National Institute of Securities Market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

The functions and powers of SEBI have been listed in the SEBI Act,1992. SEBI caters to the

needs of three parties operating in the Indian Capital Market. These three participants are

mentioned below:

Issuers of the Securities: Companies that issue securities are listed on the stock

exchange. They issue shares to raise funds. SEBI ensures that the issuance of Initial

Public Offerings (IPOs) and Follow-up Public Offers (FPOs) can take place in a healthy

and transparent way.

Protects the Interests of Traders & Investors: It is a fact that the capital markets are

functioning just because the traders exist. SEBI is responsible for safeguarding their

interests and ensuring that the investors do not become victims of any stock market

fraud or manipulation.

Financial Intermediaries: SEBI acts as a mediator in the stock market to ensure that

all the market transactions take place in a secure and smooth manner. It monitors every

activity of the financial intermediaries, such as broker, sub-broker, NBFCs, etc

Securities and Exchange Board of India has the following three powers:

Quasi-Judicial: With this authority, SEBI can conduct hearings and pass ruling

judgements in cases of unethical and fraudulent trade practices. This ensures

transparency, fairness, accountability and reliability in the capital market. SEBI PACL

case is an example of this power.

Quasi-Legislative: Powers under this segment allow SEBI to draft rules and

regulations for the protection of the interests of the investor. One such regulation is

SEBI LODR (Listing Obligation and Disclosure Requirements). It aims at

consolidating and streamlining the provisions of existing listing agreements for several

segments of the financial market like equity shares. This type of regulation formulated

by SEBI aims to keep any malpractice and fraudulent trading activates at bay.

Quasi-Executive: SEBI is authorised to file a case against anyone who violates its rules

and regulation. It is empowered to inspect account books and other documents as well

if it finds traces of any suspicious activity

The functions and powers of SEBI have been listed in the SEBI Act,1992. SEBI caters to the

needs of three parties operating in the Indian Capital Market. These three participants are

mentioned below:

Issuers of the Securities: Companies that issue securities are listed on the stock

exchange. They issue shares to raise funds. SEBI ensures that the issuance of Initial

Public Offerings (IPOs) and Follow-up Public Offers (FPOs) can take place in a healthy

and transparent way.

Protects the Interests of Traders & Investors: It is a fact that the capital markets are

functioning just because the traders exist. SEBI is responsible for safeguarding their

interests and ensuring that the investors do not become victims of any stock market

fraud or manipulation.

Financial Intermediaries: SEBI acts as a mediator in the stock market to ensure that

all the market transactions take place in a secure and smooth manner. It monitors every

activity of the financial intermediaries, such as broker, sub-broker, NBFCs, etc

Securities and Exchange Board of India has the following three powers:

Quasi-Judicial: With this authority, SEBI can conduct hearings and pass ruling

judgements in cases of unethical and fraudulent trade practices. This ensures

transparency, fairness, accountability and reliability in the capital market. SEBI PACL

case is an example of this power.

Quasi-Legislative: Powers under this segment allow SEBI to draft rules and

regulations for the protection of the interests of the investor. One such regulation is

SEBI LODR (Listing Obligation and Disclosure Requirements). It aims at

consolidating and streamlining the provisions of existing listing agreements for several

segments of the financial market like equity shares. This type of regulation formulated

by SEBI aims to keep any malpractice and fraudulent trading activates at bay.

Quasi-Executive: SEBI is authorised to file a case against anyone who violates its rules

and regulation. It is empowered to inspect account books and other documents as well

if it finds traces of any suspicious activity

9

Session 24

Environment laws

Government has been introducing various measure so as to preserve the environment. Various

environmental laws have been introduced to restore our natural resources and at the same time

and maintain a sustainable system with regard to the same. The ever-emerging growth of

consumerism has led to major environment issues. However, with the application of various

legislations, the govt is trying to strike a balance in the eco system. Companies have been given

moral, ethical and social responsibility to maintain the purity of the ecosystem and hence save

the environment. The Constitution of our country also contains special provisions on

environment protection. Directive principles and the fundamental duties expressly provide

measures to protect the environment.

However, there is a need for an integrated strategy at the national level, international

cooperation and plan for sustainable development for bringing out radical positive environment

change.

The various environment laws introduced in India are:

The Environmental Protection Act 1986

The Air (Prevention and Control of Pollution) Act 1981

The Water (Prevention and Control of Pollution) Act 1974

The Water (Prevention and Control of Pollution) Act 1977

The Wild Life (Protection) Act, 1972

The Public Liability Insurance Act, 1991

The National Environmental Tribunal Act, 1995

The National Environmental Appellate Authority Act, 1997

The Mines and Minerals (Regulation and Development) Act, 1957

The Indian Forest Act of 1927

The Forest (Conservation) Act of 1980

The Atomic Energy Act of 1948

The National Green Tribunal Act-2010

National Environment Policy, 2006

It the first initiative in strategy-formulation for environmental protection in a

comprehensive manner.

It undertakes a diagnosis of the causative factors of land degradation with a view to flagging

the remedial measures required in this direction.

Session 24

Environment laws

Government has been introducing various measure so as to preserve the environment. Various

environmental laws have been introduced to restore our natural resources and at the same time

and maintain a sustainable system with regard to the same. The ever-emerging growth of

consumerism has led to major environment issues. However, with the application of various

legislations, the govt is trying to strike a balance in the eco system. Companies have been given

moral, ethical and social responsibility to maintain the purity of the ecosystem and hence save

the environment. The Constitution of our country also contains special provisions on

environment protection. Directive principles and the fundamental duties expressly provide

measures to protect the environment.

However, there is a need for an integrated strategy at the national level, international

cooperation and plan for sustainable development for bringing out radical positive environment

change.

The various environment laws introduced in India are:

The Environmental Protection Act 1986

The Air (Prevention and Control of Pollution) Act 1981

The Water (Prevention and Control of Pollution) Act 1974

The Water (Prevention and Control of Pollution) Act 1977

The Wild Life (Protection) Act, 1972

The Public Liability Insurance Act, 1991

The National Environmental Tribunal Act, 1995

The National Environmental Appellate Authority Act, 1997

The Mines and Minerals (Regulation and Development) Act, 1957

The Indian Forest Act of 1927

The Forest (Conservation) Act of 1980

The Atomic Energy Act of 1948

The National Green Tribunal Act-2010

National Environment Policy, 2006

It the first initiative in strategy-formulation for environmental protection in a

comprehensive manner.

It undertakes a diagnosis of the causative factors of land degradation with a view to flagging

the remedial measures required in this direction.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

It recognizes that the relevant fiscal, tariffs and sectoral policies need to take explicit

account of their unintentional impacts on land degradation.

The solutions offered to tackle the problem comprise adoption of both, science-based and

traditional land-use practices, pilot-scale demonstrations, large scale dissemination,

adoption of Multi-stakeholder partnerships, promotion of agro-forestry, organic farming,

environmentally sustainable cropping patterns and adoption of efficient irrigation

techniques

As the right to pure environment is an implied right, hence any violation of this fundamental

right, can be pleaded by filling a writ petition to the Supreme Court under Art.32 and the High

Court under Art.226.

The writs of Mandamus, Certiorari and Prohibition can be invoked for such environmental

matters. A writ of mandamus would lie against a municipality which fails to construct sewers

and drains, clean street and clear garbage.

Supreme Court by virtue of various judgments for example: Oleum gas leak case, Bhopal Gas

Leak case etc has laid the rule of absolute liability and following these judgments, even The

Public Liability Insurance Act was passed, following by many other legislations.

Though the Indian Judiciary has done remarkable contribution by enacting various

environment laws but still the responsibility is on each individual to preserve the natural

resources.

It recognizes that the relevant fiscal, tariffs and sectoral policies need to take explicit

account of their unintentional impacts on land degradation.

The solutions offered to tackle the problem comprise adoption of both, science-based and

traditional land-use practices, pilot-scale demonstrations, large scale dissemination,

adoption of Multi-stakeholder partnerships, promotion of agro-forestry, organic farming,

environmentally sustainable cropping patterns and adoption of efficient irrigation

techniques

As the right to pure environment is an implied right, hence any violation of this fundamental

right, can be pleaded by filling a writ petition to the Supreme Court under Art.32 and the High

Court under Art.226.

The writs of Mandamus, Certiorari and Prohibition can be invoked for such environmental

matters. A writ of mandamus would lie against a municipality which fails to construct sewers

and drains, clean street and clear garbage.

Supreme Court by virtue of various judgments for example: Oleum gas leak case, Bhopal Gas

Leak case etc has laid the rule of absolute liability and following these judgments, even The

Public Liability Insurance Act was passed, following by many other legislations.

Though the Indian Judiciary has done remarkable contribution by enacting various

environment laws but still the responsibility is on each individual to preserve the natural

resources.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Session 25

Property Law

Property has a wide meaning in its legal sense. It means something of value and includes both

tangible and intangible assets. When a man owns a property, it means he can not only possess

and enjoy the same with an absolute right but can also derive benefit from it without violating

the law of land.

The traditional principles related to property rights include:

1. Control over the use of the property

2. Right to take any benefit from the property

3. Right to transfer or sell the property

4. Right to exclude others from the property

All properties are classified as either personal property or real property. Personal property is

movable property, anything that can be subject to ownership, except land. Real property on

the other hand, is immovable property such as land and anything attached to the land.

Though the Transfer of Property Act, 1882 does not define the term ‘Property’ the

Interpretation of the Act, says Immovable property does not includes standing timber, growing

crops or grass". Section 3(26), The General Clauses Act, 1897, defines, " immovable property"

shall include land, benefits to arise out of the land, and things attached to the earth, or

permanently fastened to anything attached to the earth.

"Immovable property" includes land, buildings, hereditary allowances, rights to ways, lights,

ferries, fisheries or any other benefit to arise out of the land, and things attached to the earth or

permanently fastened to anything which is attached to the earth, but not standing timber,

growing crops nor grass.

Under THE Securitisation And Reconstruction Of Financial

Assets And Enforcement Of Security Interest Act, 2002 "property" means--

(i) immovable property;

(ii) movable property;

(iii) any debt or any right to receive payment of money, whether secured or unsecured;

(iv) receivables, whether existing or future;

(v) intangible assets, being know-how, patent, copyright, trade mark, license, franchise or any

other business or commercial right of similar nature.

Session 25

Property Law

Property has a wide meaning in its legal sense. It means something of value and includes both

tangible and intangible assets. When a man owns a property, it means he can not only possess

and enjoy the same with an absolute right but can also derive benefit from it without violating

the law of land.

The traditional principles related to property rights include:

1. Control over the use of the property

2. Right to take any benefit from the property

3. Right to transfer or sell the property

4. Right to exclude others from the property

All properties are classified as either personal property or real property. Personal property is

movable property, anything that can be subject to ownership, except land. Real property on

the other hand, is immovable property such as land and anything attached to the land.

Though the Transfer of Property Act, 1882 does not define the term ‘Property’ the

Interpretation of the Act, says Immovable property does not includes standing timber, growing

crops or grass". Section 3(26), The General Clauses Act, 1897, defines, " immovable property"

shall include land, benefits to arise out of the land, and things attached to the earth, or

permanently fastened to anything attached to the earth.

"Immovable property" includes land, buildings, hereditary allowances, rights to ways, lights,

ferries, fisheries or any other benefit to arise out of the land, and things attached to the earth or

permanently fastened to anything which is attached to the earth, but not standing timber,

growing crops nor grass.

Under THE Securitisation And Reconstruction Of Financial

Assets And Enforcement Of Security Interest Act, 2002 "property" means--

(i) immovable property;

(ii) movable property;

(iii) any debt or any right to receive payment of money, whether secured or unsecured;

(iv) receivables, whether existing or future;

(v) intangible assets, being know-how, patent, copyright, trade mark, license, franchise or any

other business or commercial right of similar nature.

12

Movable Property

The definition of movable property is given differently under various Statutes. Some of the

definitions are as follows:

Section 3(36) of the General Clauses Act defines Movable Property as: “Movable Property

shall mean property of every description, except immovable property”.

Section 2(9) of the Registration Act, 1908 defines property as: “Moveable property’ includes

standing timber, growing crops and grass, fruit upon and juice in trees, and property of every

other description except immovable property”.

Section 22 of IPC defines property as - The words ‘Moveable property” is intended to include

corporeal property of every description except land and things attached to the earth. Things

attached to the land may become moveable property by severance from the Earth.

Tangible Property

Tangible Property refers to any type of property that can generally be moved (i.e., it is not

attached to real property or land), touched or felt.

Intangible Property

Intangible Property refers to personal property that cannot actually be moved, touched or felt

but instead represents something of value such as negotiable instruments, securities, service

(economics), and intangible assets.

Intellectual Property

Intellectual Property is a term referring to a number of distinct types of creations of the mind

for which property rights are recognized.

Under intellectual property law, owners are granted certain exclusive rights to a variety of

intangible assets, such as musical, literary and artistic works, discoveries and inventions; and

words, phrases, symbols and designs. Patents, trademarks, and copyrights, designs are the four

main categories of intellectual property.

Movable Property

The definition of movable property is given differently under various Statutes. Some of the

definitions are as follows:

Section 3(36) of the General Clauses Act defines Movable Property as: “Movable Property

shall mean property of every description, except immovable property”.

Section 2(9) of the Registration Act, 1908 defines property as: “Moveable property’ includes

standing timber, growing crops and grass, fruit upon and juice in trees, and property of every

other description except immovable property”.

Section 22 of IPC defines property as - The words ‘Moveable property” is intended to include

corporeal property of every description except land and things attached to the earth. Things

attached to the land may become moveable property by severance from the Earth.

Tangible Property

Tangible Property refers to any type of property that can generally be moved (i.e., it is not

attached to real property or land), touched or felt.

Intangible Property

Intangible Property refers to personal property that cannot actually be moved, touched or felt

but instead represents something of value such as negotiable instruments, securities, service

(economics), and intangible assets.

Intellectual Property

Intellectual Property is a term referring to a number of distinct types of creations of the mind

for which property rights are recognized.

Under intellectual property law, owners are granted certain exclusive rights to a variety of

intangible assets, such as musical, literary and artistic works, discoveries and inventions; and

words, phrases, symbols and designs. Patents, trademarks, and copyrights, designs are the four

main categories of intellectual property.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 33

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.