Management Accounting Report: Agmet's Financial Analysis

VerifiedAdded on 2020/01/28

|15

|4670

|153

Report

AI Summary

This report presents a management accounting analysis of Agmet, a small chemical manufacturing company. It explores various aspects of management accounting including the importance of management accounting techniques, and essential requirements such as traditional, lean, and cost accounting systems. The report delves into job costing, batch costing, and inventory management, highlighting their significance for Agmet. It also discusses the benefits of implementing management accounting techniques, such as improved cash flow, expense reduction, and enhanced decision-making. Furthermore, the report includes financial reporting methods, such as job cost reports, inventory management reports, and sales reports. The report also includes a task involving calculations of marginal costing and absorption costing methods, providing a practical application of these techniques for Agmet's financial analysis. Finally, the report emphasizes the integration of management accounting into business activities and concludes with a summary of key findings and recommendations for Agmet.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1............................................................................................................................................1

M1...........................................................................................................................................2

P2............................................................................................................................................3

D1...........................................................................................................................................4

TASK 2............................................................................................................................................4

P3 & M2.................................................................................................................................4

D2...........................................................................................................................................7

TASK 3............................................................................................................................................7

P4............................................................................................................................................7

M3...........................................................................................................................................9

D3 & M4...............................................................................................................................10

TASK 4..........................................................................................................................................11

P5..........................................................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1............................................................................................................................................1

M1...........................................................................................................................................2

P2............................................................................................................................................3

D1...........................................................................................................................................4

TASK 2............................................................................................................................................4

P3 & M2.................................................................................................................................4

D2...........................................................................................................................................7

TASK 3............................................................................................................................................7

P4............................................................................................................................................7

M3...........................................................................................................................................9

D3 & M4...............................................................................................................................10

TASK 4..........................................................................................................................................11

P5..........................................................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting can be referred as a system through which any entity can carry

on their operations in an efficient and efficient manner so that they can achieve the

predetermined goals and objectives. In this report there are several techniques and methods have

been defined in which the concepts have been mentioned which can be utilized by an entity for

the management of cited entity. This report is based on the case study of Agmet which is a

chemical manufacturing company this company is having less than 50 employees and its annual

turnover is less than £500,000 hence it can be said that there are very less and limited financial

and non financial sources available with cited firm(Ajibolade, Arowomole and Ojikutu, 2010).

Hence it gets very important for any firm to properly utilize the available funds in a way so that

they can get the desirable returns in a specific time period.

TASK 1

P1.

Management accounting system can be defined as the type of procedure in which

concepts of both the financial accounting and management has been involved. The entity which

is adopting management accounting techniques can properly utilize its available resources.

Agmet is a chemical manufacturing company in United Kingdom which is considered as the

small business enterprise (Albelda, 2011). Because its employing less than 50 Employees in its

organisational structure and its having less than £500,000 as its annual turnover.

Hence it can be said that being a small business enterprise, Agmet is having very less

available financial and non financial resources which its management is required to make it

possible that they can utilize them in way so that they can get the best available results out of the

available sources and available techniques. Hence it can be said that management accounting

being a credible branch of accounting with its immensely credible methods which are universally

accepted and scientifically proved (Arroyo, 2012). Cited enterprise can use the methods of

forecasting and budgeting for the estimation of expenditure which is involved in any future or

present project further they can also estimate the amount and quantity of return which it can get

form such a project. There are certain essential requirements of management accounting

techniques which an user is required to maintain for the utilization of the specified techniques of

cost accounting. Such requirements can be classified in the manner of principles which are

described in financial accounting. As in financial accounting financial accounting International

1

Management accounting can be referred as a system through which any entity can carry

on their operations in an efficient and efficient manner so that they can achieve the

predetermined goals and objectives. In this report there are several techniques and methods have

been defined in which the concepts have been mentioned which can be utilized by an entity for

the management of cited entity. This report is based on the case study of Agmet which is a

chemical manufacturing company this company is having less than 50 employees and its annual

turnover is less than £500,000 hence it can be said that there are very less and limited financial

and non financial sources available with cited firm(Ajibolade, Arowomole and Ojikutu, 2010).

Hence it gets very important for any firm to properly utilize the available funds in a way so that

they can get the desirable returns in a specific time period.

TASK 1

P1.

Management accounting system can be defined as the type of procedure in which

concepts of both the financial accounting and management has been involved. The entity which

is adopting management accounting techniques can properly utilize its available resources.

Agmet is a chemical manufacturing company in United Kingdom which is considered as the

small business enterprise (Albelda, 2011). Because its employing less than 50 Employees in its

organisational structure and its having less than £500,000 as its annual turnover.

Hence it can be said that being a small business enterprise, Agmet is having very less

available financial and non financial resources which its management is required to make it

possible that they can utilize them in way so that they can get the best available results out of the

available sources and available techniques. Hence it can be said that management accounting

being a credible branch of accounting with its immensely credible methods which are universally

accepted and scientifically proved (Arroyo, 2012). Cited enterprise can use the methods of

forecasting and budgeting for the estimation of expenditure which is involved in any future or

present project further they can also estimate the amount and quantity of return which it can get

form such a project. There are certain essential requirements of management accounting

techniques which an user is required to maintain for the utilization of the specified techniques of

cost accounting. Such requirements can be classified in the manner of principles which are

described in financial accounting. As in financial accounting financial accounting International

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Reporting Standards (IFRS) are there such as essential requirements of cost and

management accounting are also there which can be helpful for the ascertainment of the right

result or outcome which is in fact estimated by the customers and management of enterprise.

Some essential requirements are described below: Traditional Accounting system: This is all about recording of cost which is incurred

during the production of any particular product and after recording it the main aim of

this system is to allocate the cost and expenditures to the department of entity which is

accountable for such cost. When any product is produced then in such product various

cost such as variable, semi variable and fixed cost are involved further these expenses

can also be categorised as direct and indirect expenses (Bodie, 2013).

Lean Accounting System: This system deals with the change in accounting estimates

and certain other facts which are related with the management accounting and its

techniques. When there is any change in the concepts which is earlier followed by the

any entity and then as per new system or it may be possible that new organisational

structure is demanding such change in the cost accounting structure. Hence lean

accounting system can have categorised as the method through which management can

cop up with the environmental changes of any business enterprise (Chenhall, 2012). Cost Accounting System: This is the system which is used to assess the cost of the

product for the making the profitability analysis, stock valuation and cost control.

Prediction of the exact cost of the product is so much critical for profitable practices.

There is need to know about which products are profitable and which are not, and this

is possible only at the time when it has forecasted the correct cost of the product. A

product costing system assist in predicting the closing value of the material stock,

work- in- progress and finished products keeping in mind ofr making the financial

statements. Job costing system: It is the costing method in which the cost of the entire product is

ascertained. Now, it has been seen that this method is used for assigning manufacturing

costs to batches of the projects. Under this method a particular costing technique is used

in order to assess the cost of a particular cost of a job.

2

management accounting are also there which can be helpful for the ascertainment of the right

result or outcome which is in fact estimated by the customers and management of enterprise.

Some essential requirements are described below: Traditional Accounting system: This is all about recording of cost which is incurred

during the production of any particular product and after recording it the main aim of

this system is to allocate the cost and expenditures to the department of entity which is

accountable for such cost. When any product is produced then in such product various

cost such as variable, semi variable and fixed cost are involved further these expenses

can also be categorised as direct and indirect expenses (Bodie, 2013).

Lean Accounting System: This system deals with the change in accounting estimates

and certain other facts which are related with the management accounting and its

techniques. When there is any change in the concepts which is earlier followed by the

any entity and then as per new system or it may be possible that new organisational

structure is demanding such change in the cost accounting structure. Hence lean

accounting system can have categorised as the method through which management can

cop up with the environmental changes of any business enterprise (Chenhall, 2012). Cost Accounting System: This is the system which is used to assess the cost of the

product for the making the profitability analysis, stock valuation and cost control.

Prediction of the exact cost of the product is so much critical for profitable practices.

There is need to know about which products are profitable and which are not, and this

is possible only at the time when it has forecasted the correct cost of the product. A

product costing system assist in predicting the closing value of the material stock,

work- in- progress and finished products keeping in mind ofr making the financial

statements. Job costing system: It is the costing method in which the cost of the entire product is

ascertained. Now, it has been seen that this method is used for assigning manufacturing

costs to batches of the projects. Under this method a particular costing technique is used

in order to assess the cost of a particular cost of a job.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Batch costing technique: It is a form of specific order costing. It is like job costing

technique. There are so many quantities within a batch so there is need to know the cost

of that particular batch. This technique is basically used in the pharma sector.

Inventory management system: This is the most considered tool in the business

organisation. As this is useful for managing the inventory of the business which is most

important for any business. With the help of inventory management system, the

company would able to implement their resources in a better manner.

M1.

There are certain important benefits of implementing management accounting techniques

in the organisational structure of Agmet. Such benefits and importance are mentioned and

described below in detail:

Increase and improvement in cash flow: cash flow is the movement of cash through the

movement of transactions. Cash flow can be either inflow or it can be outflow also.

Which depends on the movement of cited enterprise and transactions related to business

enterprise (France, 2010). When any payment is made to the outsiders in cash then the

movement of cash flow gets negative. But when any payment is received then the cash

flow gets positive hence through implementing better system and methods in the financial

and organisational structure of Agmet the management can improve its cash flow.

Reduction in expenses: The expenses which are associated with operating and non-

operating activities of cited enterprise can be controlled and managed in a way so that

they will not adversely affect the overall profitability of the firm (Hiebl, 2014).

Assist in decision making: This can assist the managerial personnel of any enterprise for

framing and managing any decision in reference of the future operations and process. As

the decisions should be made effectively so that employees of Agmet can easily follow

them with a view to achieve the targets which are predetermined by the top level

management of it (Hülle, Kaspar and Möller, 2011).

Assist in Financial Planning: It can be observed that budgetary control methods like

capital budgeting can allow an entity to decide the optimum capital construction for its

processes. As best capital composition is not possible in practical life because of this

3

technique. There are so many quantities within a batch so there is need to know the cost

of that particular batch. This technique is basically used in the pharma sector.

Inventory management system: This is the most considered tool in the business

organisation. As this is useful for managing the inventory of the business which is most

important for any business. With the help of inventory management system, the

company would able to implement their resources in a better manner.

M1.

There are certain important benefits of implementing management accounting techniques

in the organisational structure of Agmet. Such benefits and importance are mentioned and

described below in detail:

Increase and improvement in cash flow: cash flow is the movement of cash through the

movement of transactions. Cash flow can be either inflow or it can be outflow also.

Which depends on the movement of cited enterprise and transactions related to business

enterprise (France, 2010). When any payment is made to the outsiders in cash then the

movement of cash flow gets negative. But when any payment is received then the cash

flow gets positive hence through implementing better system and methods in the financial

and organisational structure of Agmet the management can improve its cash flow.

Reduction in expenses: The expenses which are associated with operating and non-

operating activities of cited enterprise can be controlled and managed in a way so that

they will not adversely affect the overall profitability of the firm (Hiebl, 2014).

Assist in decision making: This can assist the managerial personnel of any enterprise for

framing and managing any decision in reference of the future operations and process. As

the decisions should be made effectively so that employees of Agmet can easily follow

them with a view to achieve the targets which are predetermined by the top level

management of it (Hülle, Kaspar and Möller, 2011).

Assist in Financial Planning: It can be observed that budgetary control methods like

capital budgeting can allow an entity to decide the optimum capital construction for its

processes. As best capital composition is not possible in practical life because of this

3

manager requires to find out the sources of finance which have less obligations and

provide high returns.

P2.

There are several methods in it that can be used for financial reporting and other

processes. Such methods of management accounting reporting are mentioned below:

Job Cost Reports: It show expenses for a specific project. They are usually matched with

an estimate of revenue so the company can evaluate the job's profitability. This helps to

identify higher earning areas of the business so the company can focus its efforts. Job

cost reports are also used to analyse expenses.

Inventory Management Reports: Companies with physical inventory can use

managerial accounting reports to make their management processes more efficient. These

reports generally include items such as inventory waste and hourly labour costs. The

manager can then compare different assembly lines within the company to see where one

can improve to the best-performing departments.

Accounts Receivable Reports: The accounts receivable report is a critical tool for

managing cash flow for companies that extend credit to their customers. This report

breaks down the customer balances by total amount of time have been owed it. Sales Report: A record of calls made and products sold during a particular time frame by

a management is called a sales report. A typical sales report might incorporate data on

sales volume observed per item and how many new and current accounts were contacted

when any costs were involved in promoting and selling products

Budgetary Control: Budgetary control can be further explained as the forecasting

technique which can be used by the cited enterprise for the management of the future and

present projects through which they can make some estimates and they can also check

whether the expenditures which are made in reference of the project are as per plan or

not. Because an actual expense which is more than the budgeted one shows negativity

(Kinney, Raiborn and Poznanski, 2011).

D1.

Management accounting system can be understanding very easily hence it gets easier to

implement it in future oriented activities. Following are some points described through which it

can be ascertained that how management accounting system can have integrated in an entity:

4

provide high returns.

P2.

There are several methods in it that can be used for financial reporting and other

processes. Such methods of management accounting reporting are mentioned below:

Job Cost Reports: It show expenses for a specific project. They are usually matched with

an estimate of revenue so the company can evaluate the job's profitability. This helps to

identify higher earning areas of the business so the company can focus its efforts. Job

cost reports are also used to analyse expenses.

Inventory Management Reports: Companies with physical inventory can use

managerial accounting reports to make their management processes more efficient. These

reports generally include items such as inventory waste and hourly labour costs. The

manager can then compare different assembly lines within the company to see where one

can improve to the best-performing departments.

Accounts Receivable Reports: The accounts receivable report is a critical tool for

managing cash flow for companies that extend credit to their customers. This report

breaks down the customer balances by total amount of time have been owed it. Sales Report: A record of calls made and products sold during a particular time frame by

a management is called a sales report. A typical sales report might incorporate data on

sales volume observed per item and how many new and current accounts were contacted

when any costs were involved in promoting and selling products

Budgetary Control: Budgetary control can be further explained as the forecasting

technique which can be used by the cited enterprise for the management of the future and

present projects through which they can make some estimates and they can also check

whether the expenditures which are made in reference of the project are as per plan or

not. Because an actual expense which is more than the budgeted one shows negativity

(Kinney, Raiborn and Poznanski, 2011).

D1.

Management accounting system can be understanding very easily hence it gets easier to

implement it in future oriented activities. Following are some points described through which it

can be ascertained that how management accounting system can have integrated in an entity:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Relevant cost analysis: This can be used for the analysis of relevant cost. Here relevant

cost means that the cost which affects the decision making procedure of any enterprise

and its management. Variable cost is always considered as the relevant cost as it changes

as per the change is quantity or volume of production (Macintosh and Quattrone, 2010).

But as fixed cost doesn't change as per the change in the production level because of this

fact fixed cost is not included in relevant cost. And through various techniques of cost

accounting it gets easier for an entity to manage its cost which can make impact over the

decision making process. Activity Based Costing Methods: This can assist an enterprise to ascertain that who will

be the customers of the enterprise and what they want or desires from them. Activity

based costing methods changes when the activity changes (Quinn, 2011).

Make or Buy Analysis: The management of cited enterprise can evaluate that what they

need to buy from outsiders and what they can produce internally. Through integrating it

the managers can think over and analyse that whether it is economical for an enterprise to

produce any article internally or it is economical to acquire it from the external sources.

TASK 2

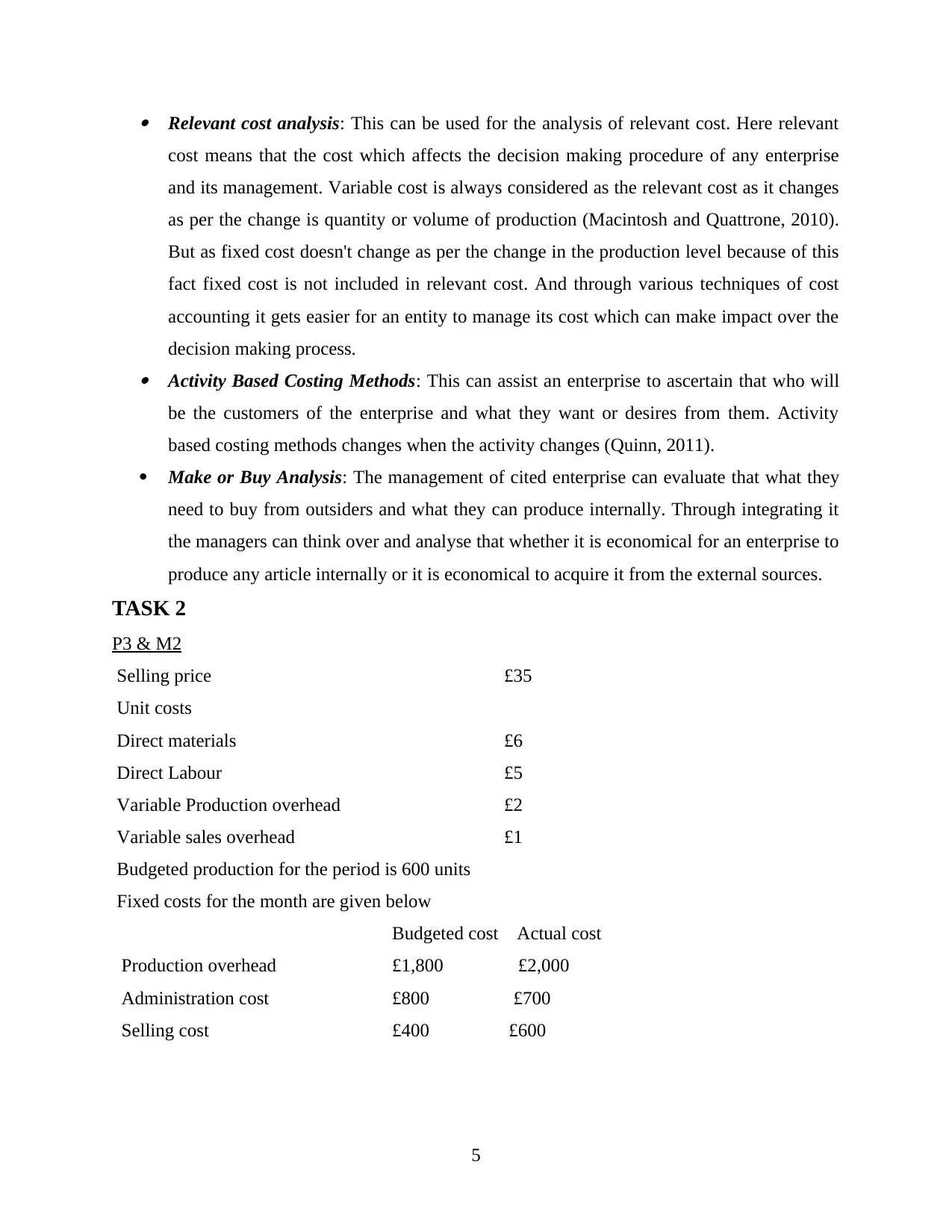

P3 & M2

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted cost Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

5

cost means that the cost which affects the decision making procedure of any enterprise

and its management. Variable cost is always considered as the relevant cost as it changes

as per the change is quantity or volume of production (Macintosh and Quattrone, 2010).

But as fixed cost doesn't change as per the change in the production level because of this

fact fixed cost is not included in relevant cost. And through various techniques of cost

accounting it gets easier for an entity to manage its cost which can make impact over the

decision making process. Activity Based Costing Methods: This can assist an enterprise to ascertain that who will

be the customers of the enterprise and what they want or desires from them. Activity

based costing methods changes when the activity changes (Quinn, 2011).

Make or Buy Analysis: The management of cited enterprise can evaluate that what they

need to buy from outsiders and what they can produce internally. Through integrating it

the managers can think over and analyse that whether it is economical for an enterprise to

produce any article internally or it is economical to acquire it from the external sources.

TASK 2

P3 & M2

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted cost Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales (35*600) 21000

less:

Cost of Production (6+5+2) -9100

closing stock (100*13) -1300

variable cost -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed overheads -2000

Admin & selling cost (700+600) -1300

-3900

NET INCOME AS PER MARGINAL COST 9300

NET INCOME AS PER ABSORPTION

COSTING:

Sales (35*600) 21000

less:

Cost of Production 9600

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

Admin & selling cost (700+600) 1300

less;over absorbed fixed production overheads -100 -1800

NET INCOME AS PER ABSORPTION

COSTING: 9600

6

less:

Cost of Production (6+5+2) -9100

closing stock (100*13) -1300

variable cost -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed overheads -2000

Admin & selling cost (700+600) -1300

-3900

NET INCOME AS PER MARGINAL COST 9300

NET INCOME AS PER ABSORPTION

COSTING:

Sales (35*600) 21000

less:

Cost of Production 9600

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

Admin & selling cost (700+600) 1300

less;over absorbed fixed production overheads -100 -1800

NET INCOME AS PER ABSORPTION

COSTING: 9600

6

D2.

As per the above mentioned income statements which have been prepared using

techniques of management accounting it can ascertained that there is difference in the net profit

calculated from the both methods of absorption and marginal costing. In the above given

statement it can be observed that the contribution of Agmet is 13200 out of which when Fixed

expenses gets reduced i.e. 3900 then the net profit can be calculated through these steps. Both

absorption and marginal costing techniques are appropriate and scientific but they follows

different principles because of this it can be find out that both of these statements are showing

different net profit figures (Renz, 2016). Absorption costing is showing less profit in comparison

to the other one i.e. marginal costing as in first one the amount of net profit is 9300 and in case

of later one the amount of net profit is 9600 this difference can be because the absorption method

of cost accounting considers fixed and variable cost but the marginal costing techniques

considers only variable cost associated with production of units hence due to this it might be

possible that the profit figures are different in each of the statements.

TASK 3

P4.

There are certain advantages as well as there are some disadvantages of implementing

methods of budgetary control in cited enterprise. Some planning tools of budgetary control can

be used for the analysis of situations which are there in organisational process of Agmet. Various

planning tools with their advantages and disadvantages are mentioned below:

Advantages:

The planning tools of budgetary control can be helpful in determining the goals of

business enterprise as it helps in forecasting of data which are necessary in planning and

organising or organisational process.

It can assist the management of Agmet to fix their targets. Each department of cited firm

is allotted a particular task which can be determined as their targets and they have been

provided with a certain time limit hence any particular task can be compiled in a

particular time period. Due to this targets can be achieved on time and it will bring

efficiency in entity's composition.

It provides cost consciousness between the employees so they can can easily go through

the cost composition of the products which have been produced by cited enterprise.

7

As per the above mentioned income statements which have been prepared using

techniques of management accounting it can ascertained that there is difference in the net profit

calculated from the both methods of absorption and marginal costing. In the above given

statement it can be observed that the contribution of Agmet is 13200 out of which when Fixed

expenses gets reduced i.e. 3900 then the net profit can be calculated through these steps. Both

absorption and marginal costing techniques are appropriate and scientific but they follows

different principles because of this it can be find out that both of these statements are showing

different net profit figures (Renz, 2016). Absorption costing is showing less profit in comparison

to the other one i.e. marginal costing as in first one the amount of net profit is 9300 and in case

of later one the amount of net profit is 9600 this difference can be because the absorption method

of cost accounting considers fixed and variable cost but the marginal costing techniques

considers only variable cost associated with production of units hence due to this it might be

possible that the profit figures are different in each of the statements.

TASK 3

P4.

There are certain advantages as well as there are some disadvantages of implementing

methods of budgetary control in cited enterprise. Some planning tools of budgetary control can

be used for the analysis of situations which are there in organisational process of Agmet. Various

planning tools with their advantages and disadvantages are mentioned below:

Advantages:

The planning tools of budgetary control can be helpful in determining the goals of

business enterprise as it helps in forecasting of data which are necessary in planning and

organising or organisational process.

It can assist the management of Agmet to fix their targets. Each department of cited firm

is allotted a particular task which can be determined as their targets and they have been

provided with a certain time limit hence any particular task can be compiled in a

particular time period. Due to this targets can be achieved on time and it will bring

efficiency in entity's composition.

It provides cost consciousness between the employees so they can can easily go through

the cost composition of the products which have been produced by cited enterprise.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Further it can be observed that producing articles as per the predetermined process and

estimations gives a control over the quality and price of goods and services.

Budgetary control facilitates centralized controlled which makes it possible to take

decision on the will of one single person.

Smooth running of business operations gets easy because of the predetermined planning -

Not Achieved assessment criteria- You need to

address the requirement of the task well. Examples

of management accounting reports include

a. Job cost reports

b. sales reports

c. account receivable reports

d. inventory managemeand objectives. Employees from different departments can utilize

their available financial and non financial tools in a way through which they can easily

achieve the targets that has been set by the top level management.

If any departments is performing below then the level of expectations then it gets easy to

detect the element which is responsible for such lower performances.

Disadvantages:

There are certain disadvantages of budgetary control system as there may be chances that

the responsible supervisors of departments estimate high expenses to escape out of the

situation of the case where the expenses gets higher then the estimated one (Salehi,

Rostami and Mogadam, 2010.). So in that situation the top management may ask to them

that why they haven't controlled the total expenditures so because of this they may frame

an estimated budget which have higher expenditure.

In case of budget the fixed targets are given to the supervisors of company due to which

it can be said that budgetary control tools provide rigidity and it ignores the flexibility

factors. Because of which when situation gets changed then they cant change their

procedures to cop up with the circumstances.

Preparation of budgets is really a difficult task and it gets worst in the case where the

circumstances are inflationary.

It involves huge investment as budget is a large process which is carried on by the

management of an enterprise. Due to which it involves huge investment so it gets tough

8

estimations gives a control over the quality and price of goods and services.

Budgetary control facilitates centralized controlled which makes it possible to take

decision on the will of one single person.

Smooth running of business operations gets easy because of the predetermined planning -

Not Achieved assessment criteria- You need to

address the requirement of the task well. Examples

of management accounting reports include

a. Job cost reports

b. sales reports

c. account receivable reports

d. inventory managemeand objectives. Employees from different departments can utilize

their available financial and non financial tools in a way through which they can easily

achieve the targets that has been set by the top level management.

If any departments is performing below then the level of expectations then it gets easy to

detect the element which is responsible for such lower performances.

Disadvantages:

There are certain disadvantages of budgetary control system as there may be chances that

the responsible supervisors of departments estimate high expenses to escape out of the

situation of the case where the expenses gets higher then the estimated one (Salehi,

Rostami and Mogadam, 2010.). So in that situation the top management may ask to them

that why they haven't controlled the total expenditures so because of this they may frame

an estimated budget which have higher expenditure.

In case of budget the fixed targets are given to the supervisors of company due to which

it can be said that budgetary control tools provide rigidity and it ignores the flexibility

factors. Because of which when situation gets changed then they cant change their

procedures to cop up with the circumstances.

Preparation of budgets is really a difficult task and it gets worst in the case where the

circumstances are inflationary.

It involves huge investment as budget is a large process which is carried on by the

management of an enterprise. Due to which it involves huge investment so it gets tough

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

for small business enterprise like Agmet to cop up with the procedures of budgetary

control.

Budgets are specifically prepared for the future periods which are totally unpredictable

due to which it might be possible that budgets will not give the accurate data or

information as per the scenario.

Budgets can be defined as only a tool hence it cannot abolish the management and its

importance because the decision making is the work of management. In that process

budgets can only assist the managerial personnel’s (Setthasakko, 2010).

M3.

There are various tools and techniques which can be used by the cited firm in order to make

budget and running a business in an effective manner. These are:

Operating Budget: It is related with the manufacturing companies which helps to estimate the

overall cost in advance by using various tools and techniques in an effective manner.

Cash Budget: This is another approach which associated with the cash and other related

activities. Such budget can be divided in to operating, financial and investment activities.

D3 & M4.

A sustainable success can be defined in many different way people, plan and profit. A

sustainability success is not a simple a vision to conserve natural sources. It is the thought

innovation creative to as we increase and bringing new solution to new markets to help to solve

various challenges and to cover all business operations along entire value inked to performs, task

the business with creating a sustainable success in entity. A management accounts are trusted to

a business decision and drive strong business performances. they combine expertise and

businessman to achieving sustainable success. The characteristic of management accounting

have to form a joint venture to elevate the best practices profession of the management

accounting. Financial and non financial information qualitative problems to solving all those

problems. the issue of sustainable developments has grow since its introduction in the report.

Were success to present a need of the without comprising the ability of future generations yo

own needs they change of the starting way of business thinks and react with the idea that

generate a form of competitive advantages for organisation by using development practices in

area (Ward, 2012). A management accounting has been financial reporting and taxation

9

control.

Budgets are specifically prepared for the future periods which are totally unpredictable

due to which it might be possible that budgets will not give the accurate data or

information as per the scenario.

Budgets can be defined as only a tool hence it cannot abolish the management and its

importance because the decision making is the work of management. In that process

budgets can only assist the managerial personnel’s (Setthasakko, 2010).

M3.

There are various tools and techniques which can be used by the cited firm in order to make

budget and running a business in an effective manner. These are:

Operating Budget: It is related with the manufacturing companies which helps to estimate the

overall cost in advance by using various tools and techniques in an effective manner.

Cash Budget: This is another approach which associated with the cash and other related

activities. Such budget can be divided in to operating, financial and investment activities.

D3 & M4.

A sustainable success can be defined in many different way people, plan and profit. A

sustainability success is not a simple a vision to conserve natural sources. It is the thought

innovation creative to as we increase and bringing new solution to new markets to help to solve

various challenges and to cover all business operations along entire value inked to performs, task

the business with creating a sustainable success in entity. A management accounts are trusted to

a business decision and drive strong business performances. they combine expertise and

businessman to achieving sustainable success. The characteristic of management accounting

have to form a joint venture to elevate the best practices profession of the management

accounting. Financial and non financial information qualitative problems to solving all those

problems. the issue of sustainable developments has grow since its introduction in the report.

Were success to present a need of the without comprising the ability of future generations yo

own needs they change of the starting way of business thinks and react with the idea that

generate a form of competitive advantages for organisation by using development practices in

area (Ward, 2012). A management accounting has been financial reporting and taxation

9

auditing are including to planning and control of the organisation operations. a sustainable role

of the management accounting the active part of decision making and evaluate strategies

formulation and implement. the study of the management accounting identify and understanding

of their contribution to this process. A management accounting is important role playing in the

organisation to developing several tools aid management facilitators of decision making. A

objective to the rest of the activity they will help the bards to reach its aims of leading the

company long term sustainable growth.

TASK 4

P5.

Management accounting methods can be helpful for the achievement of sustainable

success and in responding the financial problems. As the enterprise is having less financial and

non financial sources because its a small business enterprise. Due to which it gets necessary for it

to cover the entire expenditures in a definite limit of expenses. Other than this it can be said that

they can utilize their limited and available financial sources for the specified projects. Cited firm

is having less than £500,000 as their annual turnover which means they are earning less revenue

in comparison to the other big entities (Zang, 2011). Due to which they are required to make

some plans through which they can coordinate with the situations of less finance availability.

Financial resources can be utilized with proper planning so that proper and adequate returns can

be generated out of using proper resources with effective planning. If they utilize and exploit the

available business opportunities then it will gets easier for them to achieve the targets and

objectives which were previously determined by them.

There are some of the tools which have been used in order to respond the financial problems

within the organisation. Some of them have been mentioned hereunder:

Key performance indicators: They are a set of quantifiable measures that a company uses to

improve its performance. These are used to determine a company's progress in achieving

strategic and operational goals. KPI is also referred as key success indicators depending upon the

pertinent criteria. Some of the most common Key performance indicators revolve around

revenue and profit margins. The most basic profit metre is net profit . The gross profit margin,

which measures revenues after accounting for expenses directly associated with the production

of goods for sale, is a profit-based KPI.

10

of the management accounting the active part of decision making and evaluate strategies

formulation and implement. the study of the management accounting identify and understanding

of their contribution to this process. A management accounting is important role playing in the

organisation to developing several tools aid management facilitators of decision making. A

objective to the rest of the activity they will help the bards to reach its aims of leading the

company long term sustainable growth.

TASK 4

P5.

Management accounting methods can be helpful for the achievement of sustainable

success and in responding the financial problems. As the enterprise is having less financial and

non financial sources because its a small business enterprise. Due to which it gets necessary for it

to cover the entire expenditures in a definite limit of expenses. Other than this it can be said that

they can utilize their limited and available financial sources for the specified projects. Cited firm

is having less than £500,000 as their annual turnover which means they are earning less revenue

in comparison to the other big entities (Zang, 2011). Due to which they are required to make

some plans through which they can coordinate with the situations of less finance availability.

Financial resources can be utilized with proper planning so that proper and adequate returns can

be generated out of using proper resources with effective planning. If they utilize and exploit the

available business opportunities then it will gets easier for them to achieve the targets and

objectives which were previously determined by them.

There are some of the tools which have been used in order to respond the financial problems

within the organisation. Some of them have been mentioned hereunder:

Key performance indicators: They are a set of quantifiable measures that a company uses to

improve its performance. These are used to determine a company's progress in achieving

strategic and operational goals. KPI is also referred as key success indicators depending upon the

pertinent criteria. Some of the most common Key performance indicators revolve around

revenue and profit margins. The most basic profit metre is net profit . The gross profit margin,

which measures revenues after accounting for expenses directly associated with the production

of goods for sale, is a profit-based KPI.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.