Financial Reporting: Analysis, Standards, and Stakeholders

VerifiedAdded on 2021/02/19

|18

|5012

|257

Report

AI Summary

This report provides a detailed analysis of financial reporting, examining its context, purpose, and importance for organizations. It begins with an introduction to financial reporting, followed by an exploration of the conceptual and regulatory frameworks, key principles, and qualitative characteristics. The report identifies and discusses the main stakeholders of companies and the benefits they derive from financial reports, highlighting the value of financial reporting in meeting organizational objectives and fostering growth. The report then delves into the preparation of financial statements and their interpretation. It also compares and contrasts International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), and discusses the advantages of an international financial reporting system. Finally, it assesses the degree of compliance with international financial reporting standards, concluding with a comprehensive overview of the subject matter.

FINANCIAL-

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1. Context and purpose of financial reporting.............................................................................3

2. Conceptual, regulatory framework, key principle and qualitative characteristics..................4

3. Main stakeholders of companies and what benefit they get from financial reports. ..............5

4. The value of financial reporting for meeting organisational objectives and growth..............7

TASK 2............................................................................................................................................8

5. Preparation of main financial statements on the basis of given information..........................8

6. Interpretation and communication of financial performance..................................................9

TASK 3. ........................................................................................................................................14

7. The difference between international Accounting Standards (lAS) and if international

Financial Reporting Standards (IFRS)......................................................................................14

8. Advantage of International financial reporting system.........................................................15

TASK 4. ........................................................................................................................................16

9. Degree of compliance with international financial-reporting standards...............................16

CONCLUSION .............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1. Context and purpose of financial reporting.............................................................................3

2. Conceptual, regulatory framework, key principle and qualitative characteristics..................4

3. Main stakeholders of companies and what benefit they get from financial reports. ..............5

4. The value of financial reporting for meeting organisational objectives and growth..............7

TASK 2............................................................................................................................................8

5. Preparation of main financial statements on the basis of given information..........................8

6. Interpretation and communication of financial performance..................................................9

TASK 3. ........................................................................................................................................14

7. The difference between international Accounting Standards (lAS) and if international

Financial Reporting Standards (IFRS)......................................................................................14

8. Advantage of International financial reporting system.........................................................15

TASK 4. ........................................................................................................................................16

9. Degree of compliance with international financial-reporting standards...............................16

CONCLUSION .............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

The financial reporting can be defined as reports which contains detailed information

about financial activities that occurs in an organisation during a particular time period

(Lail,MacGregor, Marcum and Stuebs, 2017). These reports are very crucial in the aspect of

making competitive strategies and plans effectively. In the absence of these reports, it can be

difficult to manage financial performance of companies. The aim of this project report is to build

a better understanding about financial-reporting and its importance for companies. For better

understanding of all above mentioned concepts, a large accountancy firm is selected which is

Grant Thornton. This company is located in London, UK and have about 26 offices all around

the UK. The aim of company is to provide audit, taxation and advisory services to their clients.

In the project report, purpose of financial reporting and interpretation of prepared financial

statements is done. As well as evaluation of financial reporting standards, models and concepts

are discussed. In the end of report, international difference under financial-reporting is done.

TASK 1

1. Context and purpose of financial reporting.

The term financial-reporting is very crucial in aspect of financial management of

companies (Dichev, 2017). It is so because with the help of these reports, manager of

organisations can assess the actual financial position and on the basis of it they take important

decisions. Along with under financial reports various kind of statements are included such as

income statement, balance sheet etc. Apart from it, the financial reporting is linked with

regulatory frameworks. As well as governance of this reporting contains duties and

responsibilities of responsible person of companies. Herein, the context of above Grant Thornton

company they prepare financial reports in order to evaluate the financial position. As well as for

evaluating the areas in which they need to improvement.

There are various kind of purpose of financial reporting and some of them are mentioned below:

Its main purpose is to helping companies in comply with different kind of regulations.

As well as financial reports are important in raising the capital of companies.

The financial reports provide detailed information regarding to financial position of

companies.

The financial reporting can be defined as reports which contains detailed information

about financial activities that occurs in an organisation during a particular time period

(Lail,MacGregor, Marcum and Stuebs, 2017). These reports are very crucial in the aspect of

making competitive strategies and plans effectively. In the absence of these reports, it can be

difficult to manage financial performance of companies. The aim of this project report is to build

a better understanding about financial-reporting and its importance for companies. For better

understanding of all above mentioned concepts, a large accountancy firm is selected which is

Grant Thornton. This company is located in London, UK and have about 26 offices all around

the UK. The aim of company is to provide audit, taxation and advisory services to their clients.

In the project report, purpose of financial reporting and interpretation of prepared financial

statements is done. As well as evaluation of financial reporting standards, models and concepts

are discussed. In the end of report, international difference under financial-reporting is done.

TASK 1

1. Context and purpose of financial reporting.

The term financial-reporting is very crucial in aspect of financial management of

companies (Dichev, 2017). It is so because with the help of these reports, manager of

organisations can assess the actual financial position and on the basis of it they take important

decisions. Along with under financial reports various kind of statements are included such as

income statement, balance sheet etc. Apart from it, the financial reporting is linked with

regulatory frameworks. As well as governance of this reporting contains duties and

responsibilities of responsible person of companies. Herein, the context of above Grant Thornton

company they prepare financial reports in order to evaluate the financial position. As well as for

evaluating the areas in which they need to improvement.

There are various kind of purpose of financial reporting and some of them are mentioned below:

Its main purpose is to helping companies in comply with different kind of regulations.

As well as financial reports are important in raising the capital of companies.

The financial reports provide detailed information regarding to financial position of

companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the aspect of stakeholders, financial reports play a significant role. It is so because with

help of it, they can assess the financial position and can make investment accordingly.

For managers, the financial reports become an essential framework to take important

decisions.

In addition, the financial reports inform to owner of companies about how various kind of

resources are being allocated and used.

Forecasting financial conditions and cash flows.

Satisfying stakeholders need and legislations.

As well as it helps in ensuring that all companies are using similar rules.

So these are the main purpose of financial reporting. Along with in above accountancy firm,

the financial reports play all above mentioned roles.

2. Conceptual, regulatory framework, key principle and qualitative characteristics.

Conceptual and regulatory framework- The concept of financial reporting is linked with

preparation of various kind of financial statement that become an essential framework in

decision-making and planning. The external stakeholders such as suppliers, customers are also

keep an extra site of eye on the financial performance of companies so that they can investment

accordingly.

The regulatory framework of financial reports is linked with use of all accounting

standards and principals that helps in bringing accuracy and consistency in financial statements.

Such as in the above Grant Thornton company, their accountants follow various kind of

accounting rules and principles as per international financial reporting standards which are as

follows:

Conservatism- This is one of the important principle of financial reporting that concern

about reliability of financial statements of organisations (Chand, Patel and White, 2015).

In the absence of this accounting principle, accountant cannot be able to manipulate

accounting records in which transactions are not related. Such as in the above Grant

Thornton company, their accountant follows this principal of accounting in process of

recording the transactions.

Consistency- It is a common accounting principle which is related to the follow a

common accounting methodology in the process of recording financial transaction in all

the financial year without making any change. This is important to follow because with

help of it, they can assess the financial position and can make investment accordingly.

For managers, the financial reports become an essential framework to take important

decisions.

In addition, the financial reports inform to owner of companies about how various kind of

resources are being allocated and used.

Forecasting financial conditions and cash flows.

Satisfying stakeholders need and legislations.

As well as it helps in ensuring that all companies are using similar rules.

So these are the main purpose of financial reporting. Along with in above accountancy firm,

the financial reports play all above mentioned roles.

2. Conceptual, regulatory framework, key principle and qualitative characteristics.

Conceptual and regulatory framework- The concept of financial reporting is linked with

preparation of various kind of financial statement that become an essential framework in

decision-making and planning. The external stakeholders such as suppliers, customers are also

keep an extra site of eye on the financial performance of companies so that they can investment

accordingly.

The regulatory framework of financial reports is linked with use of all accounting

standards and principals that helps in bringing accuracy and consistency in financial statements.

Such as in the above Grant Thornton company, their accountants follow various kind of

accounting rules and principles as per international financial reporting standards which are as

follows:

Conservatism- This is one of the important principle of financial reporting that concern

about reliability of financial statements of organisations (Chand, Patel and White, 2015).

In the absence of this accounting principle, accountant cannot be able to manipulate

accounting records in which transactions are not related. Such as in the above Grant

Thornton company, their accountant follows this principal of accounting in process of

recording the transactions.

Consistency- It is a common accounting principle which is related to the follow a

common accounting methodology in the process of recording financial transaction in all

the financial year without making any change. This is important to follow because with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the help of it companies can compare their financial position from previous years. Like in

the context of above accountancy firm, their accountant uses this principle so that they

can compare their past performance.

Full disclosure- As per this principle of financial- reporting, it is important for

accountants to include complete financial information in the financial statements. This is

crucial because if any information will be hidden and does not disclose under financial

reports then it may lead to error in decision-making process. Hence, it is important for

accountant of companies to mentioned each and every financial transaction in the

financial statements which occurs during a financial year. Like in the above accountancy

firm, their accountant uses this principal to make financial reports more reliable and

accurate that becomes an important framework in planning and strategies formation.

Materiality- As per this principal of financial reports, sometimes accounting standards

can be ignored if its impact is smaller on the financial statements (Nnadi and Soobaroyen,

2015). This principle can be implemented in the situation in which effect of accounting

standards is lower on financial reports.

So these are the main principal of financial reports.

Qualitative characteristics of financial reports- Herein, below qualitative features of financial

reports are mentioned that are as follows:

Relevance- This is one of the important feature of financial reports which defines that

information included in the financial reports is interrelated with financial transactions

of companies.

Comparability- The financial reports have feature of comparability which means

these reports can be compared by one year to another. It becomes possible only due to

using a common accounting principles in entire financial years. Due to this, financial

information become more reliable to users.

Understandability- The information included under financial reports should be

understandable and easy so that all internal and external stakeholders can aware about

company's financial performance. Eventually, this is one of the important feature that

makes financial information of companies more reliable and crucial for stakeholders.

the context of above accountancy firm, their accountant uses this principle so that they

can compare their past performance.

Full disclosure- As per this principle of financial- reporting, it is important for

accountants to include complete financial information in the financial statements. This is

crucial because if any information will be hidden and does not disclose under financial

reports then it may lead to error in decision-making process. Hence, it is important for

accountant of companies to mentioned each and every financial transaction in the

financial statements which occurs during a financial year. Like in the above accountancy

firm, their accountant uses this principal to make financial reports more reliable and

accurate that becomes an important framework in planning and strategies formation.

Materiality- As per this principal of financial reports, sometimes accounting standards

can be ignored if its impact is smaller on the financial statements (Nnadi and Soobaroyen,

2015). This principle can be implemented in the situation in which effect of accounting

standards is lower on financial reports.

So these are the main principal of financial reports.

Qualitative characteristics of financial reports- Herein, below qualitative features of financial

reports are mentioned that are as follows:

Relevance- This is one of the important feature of financial reports which defines that

information included in the financial reports is interrelated with financial transactions

of companies.

Comparability- The financial reports have feature of comparability which means

these reports can be compared by one year to another. It becomes possible only due to

using a common accounting principles in entire financial years. Due to this, financial

information become more reliable to users.

Understandability- The information included under financial reports should be

understandable and easy so that all internal and external stakeholders can aware about

company's financial performance. Eventually, this is one of the important feature that

makes financial information of companies more reliable and crucial for stakeholders.

3. Main stakeholders of companies and what benefit they get from financial reports.

The stakeholders can be defined as those who show their interest in financial

performance of companies. Herein, this is important to know that stakeholders can be impacted

by change in organisational plans and policies. All stakeholders of companies not equal because

everyone has various purpose. Such as in the above company, they have various kind of

stakeholders including internal and external. Below both kind of stakeholders are mentioned that

are as follows: Internal stakeholders- These are the stakeholders which are related with the involving

in company's day to day operational activities and in preparation of plans (Wang, Cao,

2018). Some example of these stakeholders are managers, board of director, employees

etc. These all stakeholders are very crucial in the aspect of internal management of

companies because activities and functions are performed by them. Below some types of

internal stakeholders are mentioned that are as follows:

*Managers- These stakeholders are very crucial for companies because they are linked with

the preparation of plans and policies to manage the human and financial resources in an effective

manner. Eventually, an organisation's success depends on managers that how they manage their

subordinates. The managers get benefit of financial information for preparation of various kind

of strategies because on the basis of financial position of company they prepare plans. Such as in

the above Grant Thornton company, their managers make futuristic plans and policies on the

basis of their company's financial performance and it is informed by help of financial reports.

* Employees- The employees are kind of internal stakeholders who are related with

completing organisational activities and tasks in which entity operates. These stakeholders are

very important for companies because if employees do not perform very well then this may lead

to inefficiency in task performing. The employees get benefit from financial information to

manage their individual performance. This is so because with the help of analysis of financial

performance of company they can assess their contribution in overall performance. Like in the

above Grant Thornton company, their employees check the financial information of various

activities to determine whether they should continue their job or not. External stakeholders- The external stakeholders are those who continuously evaluate

the financial position of companies to take decision regarding to investment (Cohen and

Karatzimas, 2015). These stakeholders do not effect with the change in companies' plans

The stakeholders can be defined as those who show their interest in financial

performance of companies. Herein, this is important to know that stakeholders can be impacted

by change in organisational plans and policies. All stakeholders of companies not equal because

everyone has various purpose. Such as in the above company, they have various kind of

stakeholders including internal and external. Below both kind of stakeholders are mentioned that

are as follows: Internal stakeholders- These are the stakeholders which are related with the involving

in company's day to day operational activities and in preparation of plans (Wang, Cao,

2018). Some example of these stakeholders are managers, board of director, employees

etc. These all stakeholders are very crucial in the aspect of internal management of

companies because activities and functions are performed by them. Below some types of

internal stakeholders are mentioned that are as follows:

*Managers- These stakeholders are very crucial for companies because they are linked with

the preparation of plans and policies to manage the human and financial resources in an effective

manner. Eventually, an organisation's success depends on managers that how they manage their

subordinates. The managers get benefit of financial information for preparation of various kind

of strategies because on the basis of financial position of company they prepare plans. Such as in

the above Grant Thornton company, their managers make futuristic plans and policies on the

basis of their company's financial performance and it is informed by help of financial reports.

* Employees- The employees are kind of internal stakeholders who are related with

completing organisational activities and tasks in which entity operates. These stakeholders are

very important for companies because if employees do not perform very well then this may lead

to inefficiency in task performing. The employees get benefit from financial information to

manage their individual performance. This is so because with the help of analysis of financial

performance of company they can assess their contribution in overall performance. Like in the

above Grant Thornton company, their employees check the financial information of various

activities to determine whether they should continue their job or not. External stakeholders- The external stakeholders are those who continuously evaluate

the financial position of companies to take decision regarding to investment (Cohen and

Karatzimas, 2015). These stakeholders do not effect with the change in companies' plans

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and policies because their objective to gather information about financial performance

and to invest money accordingly. Herein, below some types of external stakeholders are

mentioned which are as follows:

* Creditors- These are kind of external stakeholders who are related with providing financial

assistance to companies on credit (Adams., 2017). They take benefit from financial information

of companies in the context of deciding the financial position and on the basis of it, they grant

fund. So overall with the help of financial information about companies they determine credit

score about company.

* Investors- These are kind of external stakeholders who make investment in the companies'

operations and projects on the basis of financial situation. Their objective is to get higher rate of

return on the amount which is invested by them. They get benefit from financial information of

companies to decisions about investment because if they will not aware about financial position

then it can be risky for them. Like in the above company, their investors evaluate their financial

condition and then make invest.

4. The value of financial reporting for meeting organisational objectives and growth.

The term financial reporting is very useful in the aspect of achieving organisational

objectives as well as in future growth. This is so because with the help of analysis of financial

reports companies can assess about what are the changes which are needed to be done to achieve

the objectives.

Financial reporting for meeting organisational objectives- The financial reporting is

linked with the meeting organisational objectives and goals (Whittington, 2015). It is so because

managers of companies can determine about which kind of strategy is needed to be implemented

to accomplish the objective. Such as in the above Grant Thornton company, their objectives are

achieved in an effective manner by use of financial reports. It becomes possible because

financial reports reflect the actual outcome of various kind of business activities and as per it

corrective actions are being taken by manager of above company.

Financial reporting for achieving the growth- Another purpose of financial reporting is

to help companies for future growth and success. It is so because the financial reports lead to

provide current situation of companies and on the basis of this they estimate future growth. Such

as in the above Grant Thornton company, their managers manage and sustain their growth with

and to invest money accordingly. Herein, below some types of external stakeholders are

mentioned which are as follows:

* Creditors- These are kind of external stakeholders who are related with providing financial

assistance to companies on credit (Adams., 2017). They take benefit from financial information

of companies in the context of deciding the financial position and on the basis of it, they grant

fund. So overall with the help of financial information about companies they determine credit

score about company.

* Investors- These are kind of external stakeholders who make investment in the companies'

operations and projects on the basis of financial situation. Their objective is to get higher rate of

return on the amount which is invested by them. They get benefit from financial information of

companies to decisions about investment because if they will not aware about financial position

then it can be risky for them. Like in the above company, their investors evaluate their financial

condition and then make invest.

4. The value of financial reporting for meeting organisational objectives and growth.

The term financial reporting is very useful in the aspect of achieving organisational

objectives as well as in future growth. This is so because with the help of analysis of financial

reports companies can assess about what are the changes which are needed to be done to achieve

the objectives.

Financial reporting for meeting organisational objectives- The financial reporting is

linked with the meeting organisational objectives and goals (Whittington, 2015). It is so because

managers of companies can determine about which kind of strategy is needed to be implemented

to accomplish the objective. Such as in the above Grant Thornton company, their objectives are

achieved in an effective manner by use of financial reports. It becomes possible because

financial reports reflect the actual outcome of various kind of business activities and as per it

corrective actions are being taken by manager of above company.

Financial reporting for achieving the growth- Another purpose of financial reporting is

to help companies for future growth and success. It is so because the financial reports lead to

provide current situation of companies and on the basis of this they estimate future growth. Such

as in the above Grant Thornton company, their managers manage and sustain their growth with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the help of financial reports. Hence, it can be said that financial reports are important for future

growth of companies.

TASK 2.

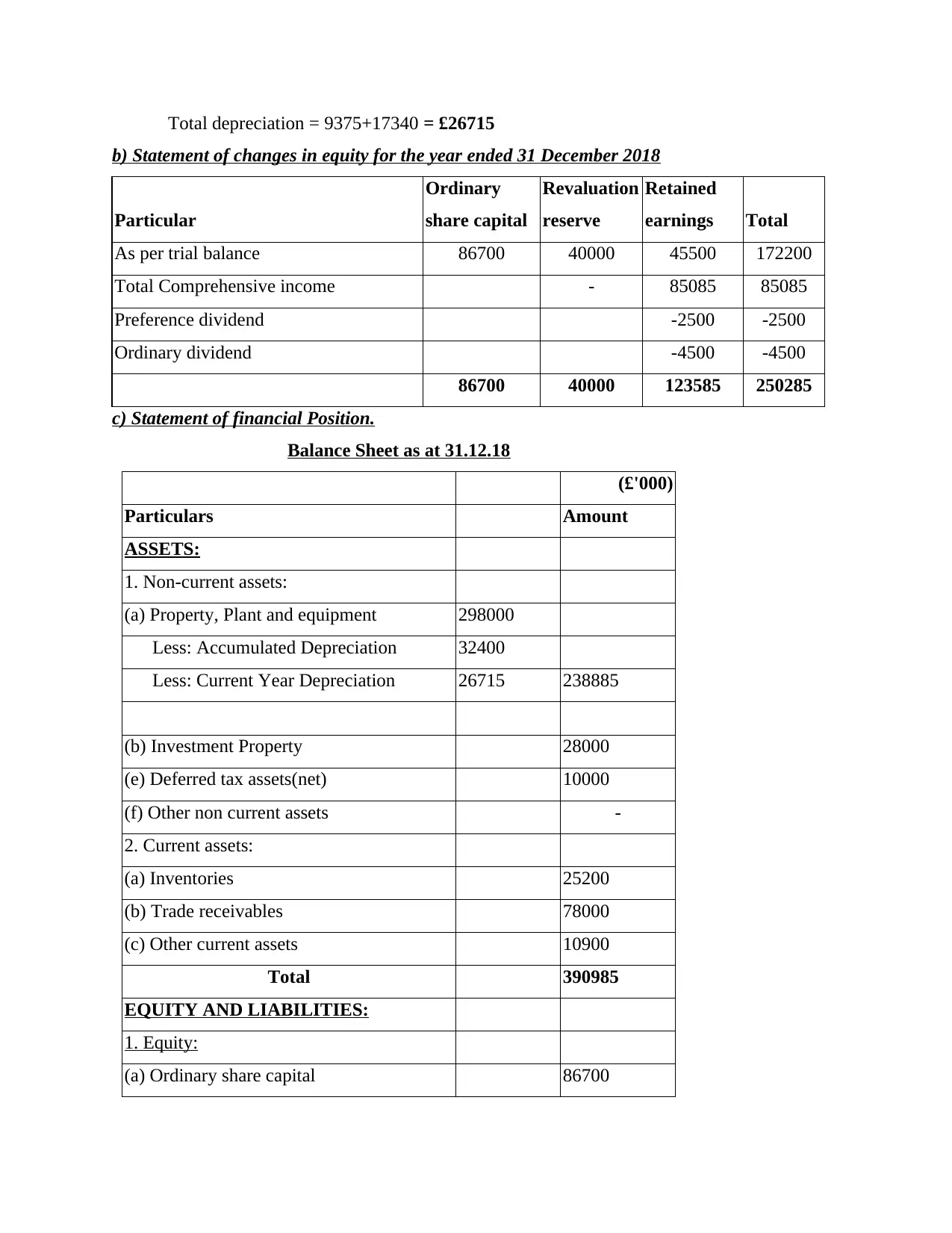

5. Preparation of main financial statements on the basis of given information.

a) Profit and Loss statement

31.12.18

(£'000)

Continuing operations

Particulars Amount

Revenue from Operations (A) 585100

Cost of goods sold (391700)

Cost of providing services -

Gross profit 193400

Less: Operating expenses 80500

Less: Depreciation (W.N. 1) 26715

Less: Other Income (9600)

Operating profit 95785

Less: Bank interest 1200

Profit before exceptional items and tax 94585

Exceptional Items Nil

Profit before tax 94585

Less: Income tax expense 9500

Profit after tax 85085

Add: Other Comprehensive income -

Total Comprehensive income 85085

Working Note:

Calculation of depreciation expenses:

Land and machinery: 150000/16 = £9375

Plant and equipment: 148000-32400 = £115600

115600*15/100 = £17340

growth of companies.

TASK 2.

5. Preparation of main financial statements on the basis of given information.

a) Profit and Loss statement

31.12.18

(£'000)

Continuing operations

Particulars Amount

Revenue from Operations (A) 585100

Cost of goods sold (391700)

Cost of providing services -

Gross profit 193400

Less: Operating expenses 80500

Less: Depreciation (W.N. 1) 26715

Less: Other Income (9600)

Operating profit 95785

Less: Bank interest 1200

Profit before exceptional items and tax 94585

Exceptional Items Nil

Profit before tax 94585

Less: Income tax expense 9500

Profit after tax 85085

Add: Other Comprehensive income -

Total Comprehensive income 85085

Working Note:

Calculation of depreciation expenses:

Land and machinery: 150000/16 = £9375

Plant and equipment: 148000-32400 = £115600

115600*15/100 = £17340

Total depreciation = 9375+17340 = £26715

b) Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluation

reserve

Retained

earnings Total

As per trial balance 86700 40000 45500 172200

Total Comprehensive income - 85085 85085

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

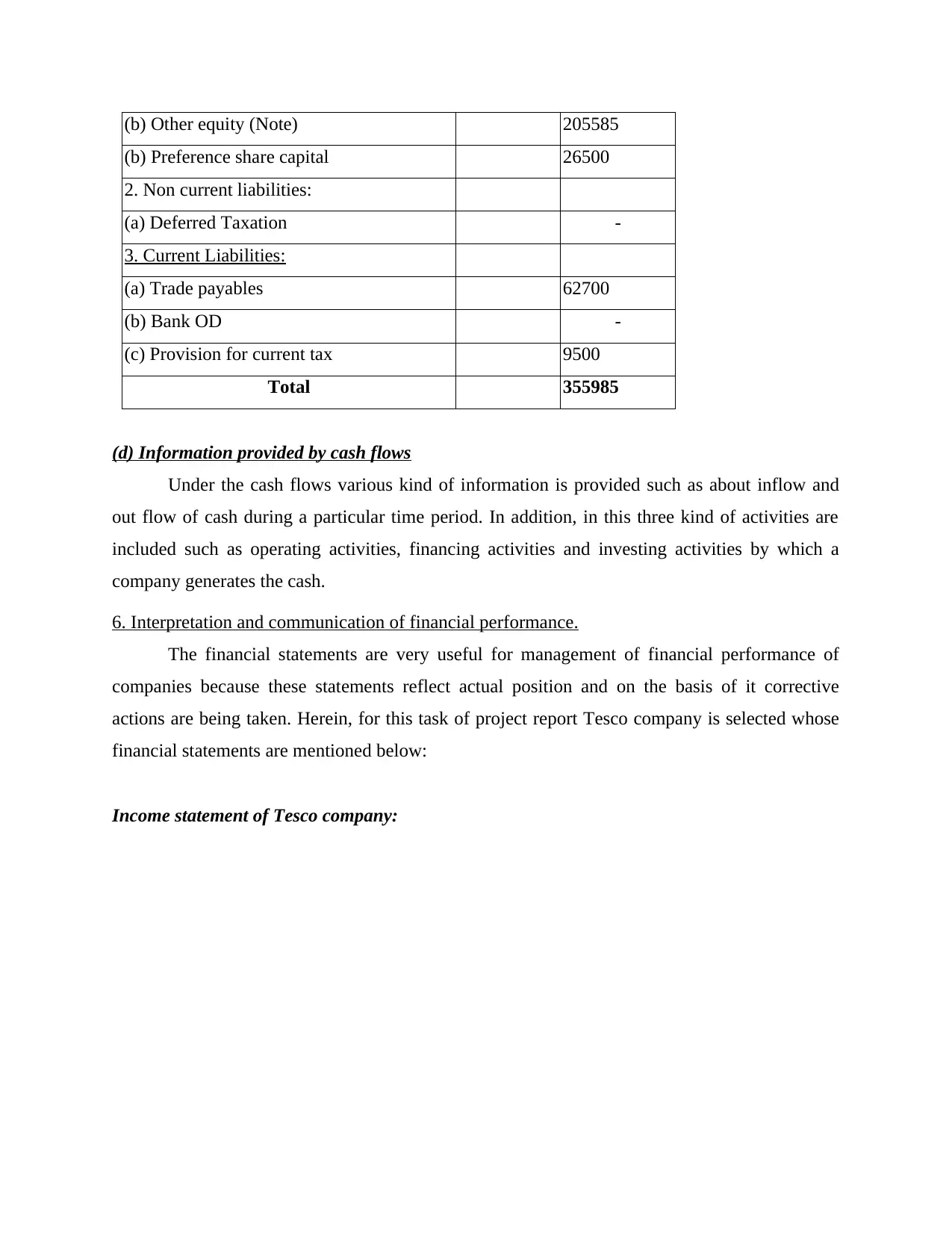

c) Statement of financial Position.

Balance Sheet as at 31.12.18

(£'000)

Particulars Amount

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

1. Equity:

(a) Ordinary share capital 86700

b) Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluation

reserve

Retained

earnings Total

As per trial balance 86700 40000 45500 172200

Total Comprehensive income - 85085 85085

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

c) Statement of financial Position.

Balance Sheet as at 31.12.18

(£'000)

Particulars Amount

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

1. Equity:

(a) Ordinary share capital 86700

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(b) Other equity (Note) 205585

(b) Preference share capital 26500

2. Non current liabilities:

(a) Deferred Taxation -

3. Current Liabilities:

(a) Trade payables 62700

(b) Bank OD -

(c) Provision for current tax 9500

Total 355985

(d) Information provided by cash flows

Under the cash flows various kind of information is provided such as about inflow and

out flow of cash during a particular time period. In addition, in this three kind of activities are

included such as operating activities, financing activities and investing activities by which a

company generates the cash.

6. Interpretation and communication of financial performance.

The financial statements are very useful for management of financial performance of

companies because these statements reflect actual position and on the basis of it corrective

actions are being taken. Herein, for this task of project report Tesco company is selected whose

financial statements are mentioned below:

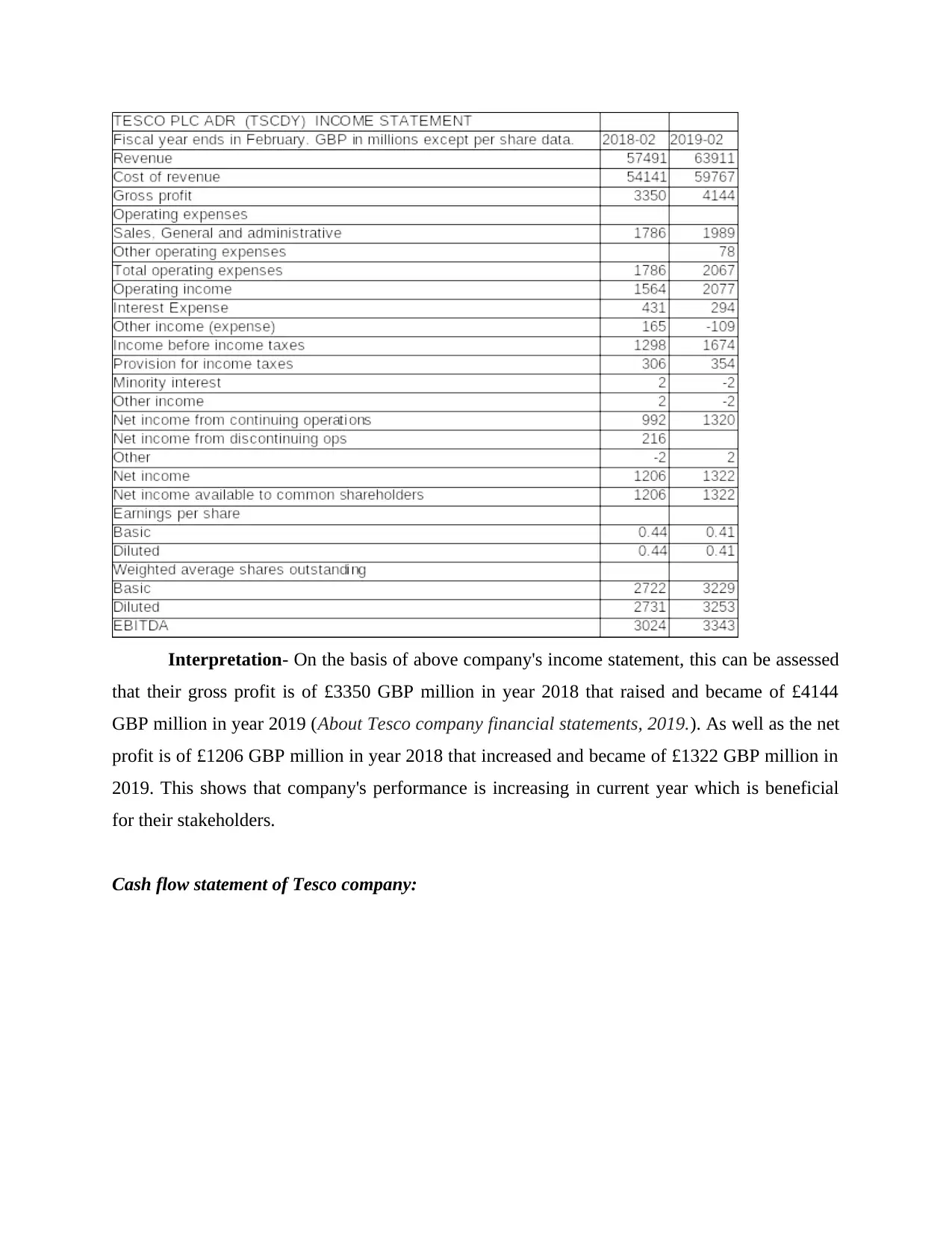

Income statement of Tesco company:

(b) Preference share capital 26500

2. Non current liabilities:

(a) Deferred Taxation -

3. Current Liabilities:

(a) Trade payables 62700

(b) Bank OD -

(c) Provision for current tax 9500

Total 355985

(d) Information provided by cash flows

Under the cash flows various kind of information is provided such as about inflow and

out flow of cash during a particular time period. In addition, in this three kind of activities are

included such as operating activities, financing activities and investing activities by which a

company generates the cash.

6. Interpretation and communication of financial performance.

The financial statements are very useful for management of financial performance of

companies because these statements reflect actual position and on the basis of it corrective

actions are being taken. Herein, for this task of project report Tesco company is selected whose

financial statements are mentioned below:

Income statement of Tesco company:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation- On the basis of above company's income statement, this can be assessed

that their gross profit is of £3350 GBP million in year 2018 that raised and became of £4144

GBP million in year 2019 (About Tesco company financial statements, 2019.). As well as the net

profit is of £1206 GBP million in year 2018 that increased and became of £1322 GBP million in

2019. This shows that company's performance is increasing in current year which is beneficial

for their stakeholders.

Cash flow statement of Tesco company:

that their gross profit is of £3350 GBP million in year 2018 that raised and became of £4144

GBP million in year 2019 (About Tesco company financial statements, 2019.). As well as the net

profit is of £1206 GBP million in year 2018 that increased and became of £1322 GBP million in

2019. This shows that company's performance is increasing in current year which is beneficial

for their stakeholders.

Cash flow statement of Tesco company:

TESCO PLC ADR (TSCDY) Statement of CASH FLOW

Fiscal year ends in February. GBP in millions except per share data. 2018-02 2019-02

Cash Flows From Operating Activities

Investments losses (gains) 156 127

Stock based compensation 113 77

Inventory 76 9

Other working capital 516 -705

Other non-cash items 1921 2458

Net cash provided by operating activities 2782 1966

Cash Flows From Investing Activities

Investments in property, plant, and equipment -1440 -1101

Property, plant, and equipment reductions 253 286

Acquisitions, net 41 -718

Purchases of intangibles -197 -191

Other investing charges 2009 581

Net cash used for investing activities 666 -1143

Cash Flows From Financing Activities

Long-term debt issued 313 975

Long-term debt repayment -3721 -2471

Common stock issued 11 60

Repurchases of treasury stock -206

Cash dividends paid -82 -357

Other financing activities 243 18

Net cash provided by (used for) financing activities -3236 -1981

Effect of exchange rate changes 15 15

Net change in cash 227 -1143

Cash at beginning of period 3832 4059

Cash at end of period 4059 2916

Free Cash Flow

Operating cash flow 2782 1966

Capital expenditure -1637 -1292

Free cash flow 1145 674

Interpretation- On the basis of above company's cash flow statement this can be

analysed that company has free cash flow of £1145 GBP million in year 2018 that decreased and

became of £674 GBP million. In broad sense, under operating activities there is cash inflow of

£2782 GBP million that decreased in year 2019 and became of £1966 GBP million. While in

financing activities, there is cash outflow of £ (3236) in year 2018 and in year 2019 it is of £

(1981). In the end, cash flow from investing activities there is cash inflow of £666 GBP million

in year 2018 while in year 2019, there is cash outflow of £ (1143).

Balance sheet of Tesco plc:

Fiscal year ends in February. GBP in millions except per share data. 2018-02 2019-02

Cash Flows From Operating Activities

Investments losses (gains) 156 127

Stock based compensation 113 77

Inventory 76 9

Other working capital 516 -705

Other non-cash items 1921 2458

Net cash provided by operating activities 2782 1966

Cash Flows From Investing Activities

Investments in property, plant, and equipment -1440 -1101

Property, plant, and equipment reductions 253 286

Acquisitions, net 41 -718

Purchases of intangibles -197 -191

Other investing charges 2009 581

Net cash used for investing activities 666 -1143

Cash Flows From Financing Activities

Long-term debt issued 313 975

Long-term debt repayment -3721 -2471

Common stock issued 11 60

Repurchases of treasury stock -206

Cash dividends paid -82 -357

Other financing activities 243 18

Net cash provided by (used for) financing activities -3236 -1981

Effect of exchange rate changes 15 15

Net change in cash 227 -1143

Cash at beginning of period 3832 4059

Cash at end of period 4059 2916

Free Cash Flow

Operating cash flow 2782 1966

Capital expenditure -1637 -1292

Free cash flow 1145 674

Interpretation- On the basis of above company's cash flow statement this can be

analysed that company has free cash flow of £1145 GBP million in year 2018 that decreased and

became of £674 GBP million. In broad sense, under operating activities there is cash inflow of

£2782 GBP million that decreased in year 2019 and became of £1966 GBP million. While in

financing activities, there is cash outflow of £ (3236) in year 2018 and in year 2019 it is of £

(1981). In the end, cash flow from investing activities there is cash inflow of £666 GBP million

in year 2018 while in year 2019, there is cash outflow of £ (1143).

Balance sheet of Tesco plc:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.