Accounting Report: Financial Statements Analysis for Several Companies

VerifiedAdded on 2022/12/30

|14

|2932

|77

Report

AI Summary

This accounting report provides an in-depth analysis of financial statements and business transactions. It begins by exploring the need for accounting information for decision-makers at Unilever, examining both internal and external users, and discussing the advantages and disadvantages of recording accounting information. The report then delves into specific examples, including journal entries for David Wise's business, the general ledger and trial balance for Pearce and Sons, and the income statement of Airman Co. for the year ending September 30, 2020, including an analysis of the impact of COVID-19 on the company's profitability. The report highlights the effects of the pandemic on revenue, fixed costs, workforce, and customer behavior, contributing to significant losses. The report provides valuable insights into accounting practices and the effects of external factors on business performance.

RECORDING BUSINESS

TRANSACTIONS

TRANSACTIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Part 1................................................................................................................................................3

a. Need of Accounting Information For Decision Makers of Unilever Company .....................3

b. Advantages and Disadvantages of Recording Accounting Information ................................4

Part 2................................................................................................................................................7

a) Journal Entries in David wise business ..................................................................................7

Part 3................................................................................................................................................7

a) General ledger of Pearce and Sons.........................................................................................7

b) Trial balance as at 30th February 2019.................................................................................10

Part 4.........................................................................................................................................10

a) Income Statement of Airman Co. as at 30th September 2020..............................................10

b) Impact of Covid 19 on the company's Income Statement ...................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

Part 1................................................................................................................................................3

a. Need of Accounting Information For Decision Makers of Unilever Company .....................3

b. Advantages and Disadvantages of Recording Accounting Information ................................4

Part 2................................................................................................................................................7

a) Journal Entries in David wise business ..................................................................................7

Part 3................................................................................................................................................7

a) General ledger of Pearce and Sons.........................................................................................7

b) Trial balance as at 30th February 2019.................................................................................10

Part 4.........................................................................................................................................10

a) Income Statement of Airman Co. as at 30th September 2020..............................................10

b) Impact of Covid 19 on the company's Income Statement ...................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

This project shall highlight the basics of accountancy, how the transactions are recorded and

furnished to the users of financial information and how are the profitability and the position of

the company calculated. The report shall be divided into four parts each focussing on different

aspects of accounting. The first part shall be explaining the various users of the accounting

information of Unilever company. The investors, management, customers, employees etc. using

the accounting information to facilitate the decision-making process. The second part shall be

disclosing the journal entries of the David Wise who has set up a new business in January 2020

before the outbreak of coronavirus. The third part of the project shall be demonstrating the ledger

accounts and the trial balance of Pearce and Sons for the month of February 2020. Lastly it shall

be reflecting the income statement of Airman Co. for the year ending 30th September 2020 and

showing the impact of covid 19 on the profitability of the company.

Part 1

a. Need of Accounting Information For Decision Makers of Unilever Company

Unilever is Multinational company that deals in consumer products, heath and face care

and listed on stock exchange .there are several decision makers that need accounting information

of the firm (Trigo, Belfo and Estébanez, 2016.). The objective of studying this wide data by

individuals is to identify the current position of company.

Internal Decision makers of information

These users are those who are known about the company's procedure and willing to take

decisions based on calculated accounting information.

Subordinates of Unilever

Employees' are interested in accounting information of the organization as it helps them

to understand growth that firm can actually achieve as it will impact their personal growth such

as jobs security and promotion (Susanto, 2016). Employees working in finance department find

it as their duty to prepare financial statement base on this information. Subordinates of Unilever

group checks these data to measure their performance.

Management

Management includes officers, board of directors and manager of Unilever. They use

these data for several decision-making like planning, organizing, directing and controlling, and

This project shall highlight the basics of accountancy, how the transactions are recorded and

furnished to the users of financial information and how are the profitability and the position of

the company calculated. The report shall be divided into four parts each focussing on different

aspects of accounting. The first part shall be explaining the various users of the accounting

information of Unilever company. The investors, management, customers, employees etc. using

the accounting information to facilitate the decision-making process. The second part shall be

disclosing the journal entries of the David Wise who has set up a new business in January 2020

before the outbreak of coronavirus. The third part of the project shall be demonstrating the ledger

accounts and the trial balance of Pearce and Sons for the month of February 2020. Lastly it shall

be reflecting the income statement of Airman Co. for the year ending 30th September 2020 and

showing the impact of covid 19 on the profitability of the company.

Part 1

a. Need of Accounting Information For Decision Makers of Unilever Company

Unilever is Multinational company that deals in consumer products, heath and face care

and listed on stock exchange .there are several decision makers that need accounting information

of the firm (Trigo, Belfo and Estébanez, 2016.). The objective of studying this wide data by

individuals is to identify the current position of company.

Internal Decision makers of information

These users are those who are known about the company's procedure and willing to take

decisions based on calculated accounting information.

Subordinates of Unilever

Employees' are interested in accounting information of the organization as it helps them

to understand growth that firm can actually achieve as it will impact their personal growth such

as jobs security and promotion (Susanto, 2016). Employees working in finance department find

it as their duty to prepare financial statement base on this information. Subordinates of Unilever

group checks these data to measure their performance.

Management

Management includes officers, board of directors and manager of Unilever. They use

these data for several decision-making like planning, organizing, directing and controlling, and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

they also access accounting information to know ability of company to generate profits in future.

In financial information the management uses ratios like debt-equity, profitability and liquidity

ratios, income statements and balance sheet so that it can analyse its debt paying capacity of

Unilever company and requirement of funds can be identified by the top-level management so

that cash inflow and outflow can be adjusted.

Owners

They want to know the risk bearing capacity of business with the help of these data so

that they can take decision regarding allocation of their fund with the best strategies so that it can

give them optimum profit. Owners of Unilever company have shown many times though their

share prices that they are properly using data in adequate manner.

External Users of Accounting Information

Investors

Investors' decision of investing in any company is dependent on financial statement of

company. Unilever is company that have been on priority for some investors as its publish its

accurate financial data with full transparency.

Lenders

Lender's decision regarding lending fund to company is based on creditworthiness of

firm. The ability of paying debt is measured through calculating ratios (Olanrewaju and Jugu

2019). The Unilever company have good reputation due its solvency position in market.

Suppliers

Supplier gives input and final products to company on credit basis. It became essential

part to study the financial data of firm. Suppliers of Unilever company read the financial

statements to find out that giving o credit would be beneficial for them or not.

Tax Authorities

Tax Authorities need the financial information to determine that tax evasion can not be

take place by Unilever company. It a legal requirement for company to show its precise reports

to authorities.

b. Advantages and Disadvantages of Recording Accounting Information

There are several advantages and disadvantages of recording business transaction that

company get. Company deals various transaction so remembering each transaction becomes

In financial information the management uses ratios like debt-equity, profitability and liquidity

ratios, income statements and balance sheet so that it can analyse its debt paying capacity of

Unilever company and requirement of funds can be identified by the top-level management so

that cash inflow and outflow can be adjusted.

Owners

They want to know the risk bearing capacity of business with the help of these data so

that they can take decision regarding allocation of their fund with the best strategies so that it can

give them optimum profit. Owners of Unilever company have shown many times though their

share prices that they are properly using data in adequate manner.

External Users of Accounting Information

Investors

Investors' decision of investing in any company is dependent on financial statement of

company. Unilever is company that have been on priority for some investors as its publish its

accurate financial data with full transparency.

Lenders

Lender's decision regarding lending fund to company is based on creditworthiness of

firm. The ability of paying debt is measured through calculating ratios (Olanrewaju and Jugu

2019). The Unilever company have good reputation due its solvency position in market.

Suppliers

Supplier gives input and final products to company on credit basis. It became essential

part to study the financial data of firm. Suppliers of Unilever company read the financial

statements to find out that giving o credit would be beneficial for them or not.

Tax Authorities

Tax Authorities need the financial information to determine that tax evasion can not be

take place by Unilever company. It a legal requirement for company to show its precise reports

to authorities.

b. Advantages and Disadvantages of Recording Accounting Information

There are several advantages and disadvantages of recording business transaction that

company get. Company deals various transaction so remembering each transaction becomes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

difficult for company (Cunningham and et.al., 2020). And depending on these financial

statements can also adversely affect its performance.

Advantages

Prevention and detection of Fraud

Accounting helps business to avoid or omit the fraud and errors while recording business

transaction it play essential role as accounting data are used to decide and measure position of

company in market (Huerta and Jensen, 2017). Company get this advantage though recording

information as it help it to serve reports as a evidence of fair practices to investors, lenders, tax

authorities and to any other party.

Comparison of Results

Financial statements help the company to record the business transaction systematically

and fairly so it can be used by accountant to compare current position of company with previous

year position to measure the growth and sustainability of organization. It also helps to measure

the competition prevailing market and how many competitors are ahead of us.

Disadvantages

Records Only Financial Aspect

The biggest disadvantage of recording information is that it only consider monetary

transaction Accountant does not include impact of other non monetary transaction on business

that results in inaccurate position of firm. There are various factors that affect position of

businesses like economic conditions, government norms, competition in industry. All these are

also determinants of business position in industry (Nallareddy and Ogneva, 2017). So it gives

disadvantage of unfaithful position.

May be Manipulated

Information recorded by accountant may be false as the accountant is part of management

and the top-level management always wants firm to look in good stage without any errors so it

can be planned and manipulated by the management of organization.

Sole firm is type of organisation structure that is managed and owned by individual

person so remembering all the functioning would be difficult for him so recording all business

transaction can provide him benefit like all data in one place without any confusing the sole

proprietor can access to data and also it can provide its disadvantage like its time-consuming and

statements can also adversely affect its performance.

Advantages

Prevention and detection of Fraud

Accounting helps business to avoid or omit the fraud and errors while recording business

transaction it play essential role as accounting data are used to decide and measure position of

company in market (Huerta and Jensen, 2017). Company get this advantage though recording

information as it help it to serve reports as a evidence of fair practices to investors, lenders, tax

authorities and to any other party.

Comparison of Results

Financial statements help the company to record the business transaction systematically

and fairly so it can be used by accountant to compare current position of company with previous

year position to measure the growth and sustainability of organization. It also helps to measure

the competition prevailing market and how many competitors are ahead of us.

Disadvantages

Records Only Financial Aspect

The biggest disadvantage of recording information is that it only consider monetary

transaction Accountant does not include impact of other non monetary transaction on business

that results in inaccurate position of firm. There are various factors that affect position of

businesses like economic conditions, government norms, competition in industry. All these are

also determinants of business position in industry (Nallareddy and Ogneva, 2017). So it gives

disadvantage of unfaithful position.

May be Manipulated

Information recorded by accountant may be false as the accountant is part of management

and the top-level management always wants firm to look in good stage without any errors so it

can be planned and manipulated by the management of organization.

Sole firm is type of organisation structure that is managed and owned by individual

person so remembering all the functioning would be difficult for him so recording all business

transaction can provide him benefit like all data in one place without any confusing the sole

proprietor can access to data and also it can provide its disadvantage like its time-consuming and

requires the skills of accountant so its only beneficial for large company as the sole proprietor

does not deal in large business transaction (O'Leary, 2017).

Partnership firm is that type of business structure that have two or more owners that will

to share profit or loss according to partnership deed. The biggest advantage of recording

financial information to this firm is that it can be serve as proof to other partner to ignore

disputes and misleading practices among partners of business and disadvantage of that it will

only record the monetary data not non financial data so wrong position of company is assumed

by the partners and necessary actions can be avoided to improve working of partnership firm due

to wrong information.

does not deal in large business transaction (O'Leary, 2017).

Partnership firm is that type of business structure that have two or more owners that will

to share profit or loss according to partnership deed. The biggest advantage of recording

financial information to this firm is that it can be serve as proof to other partner to ignore

disputes and misleading practices among partners of business and disadvantage of that it will

only record the monetary data not non financial data so wrong position of company is assumed

by the partners and necessary actions can be avoided to improve working of partnership firm due

to wrong information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 2

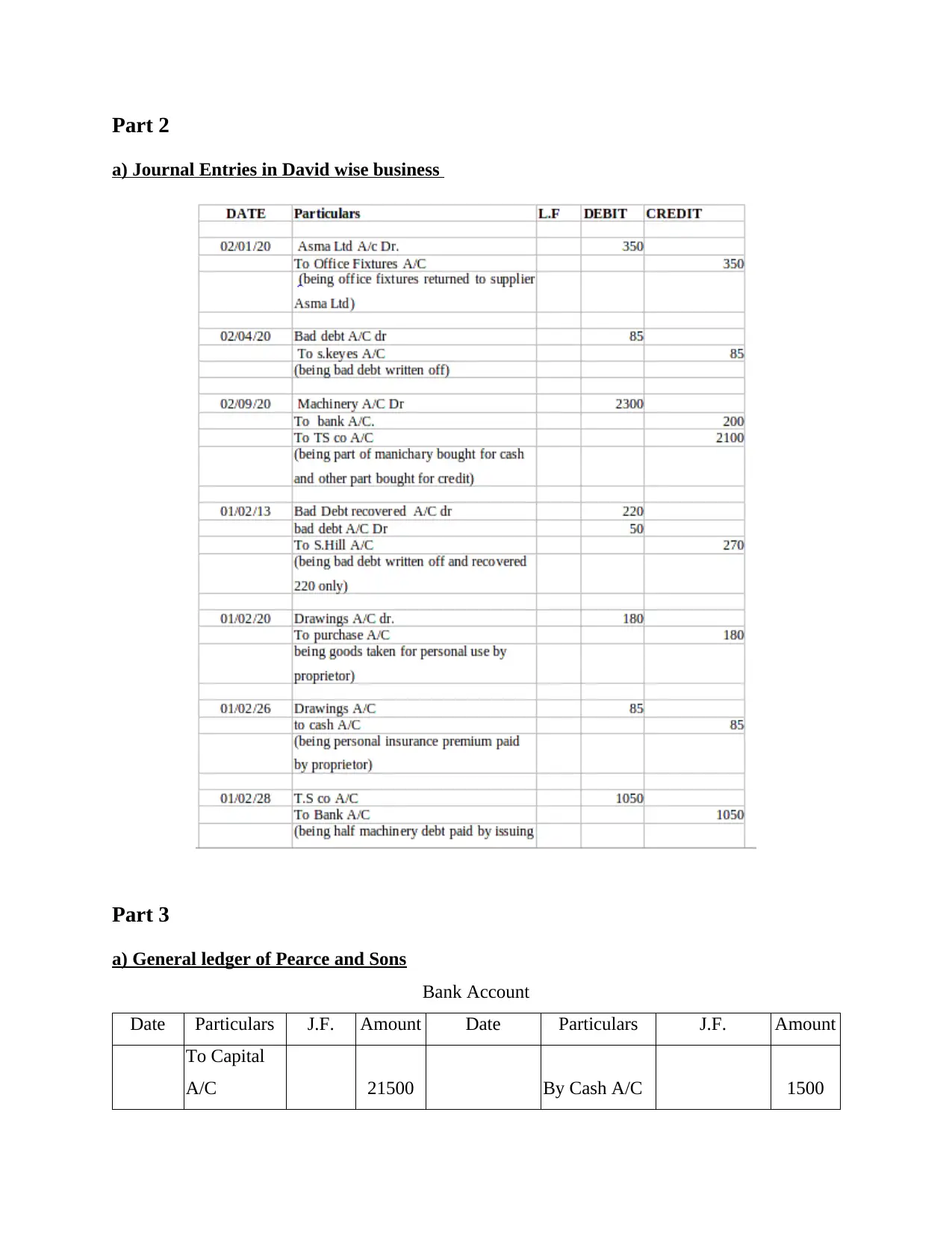

a) Journal Entries in David wise business

Part 3

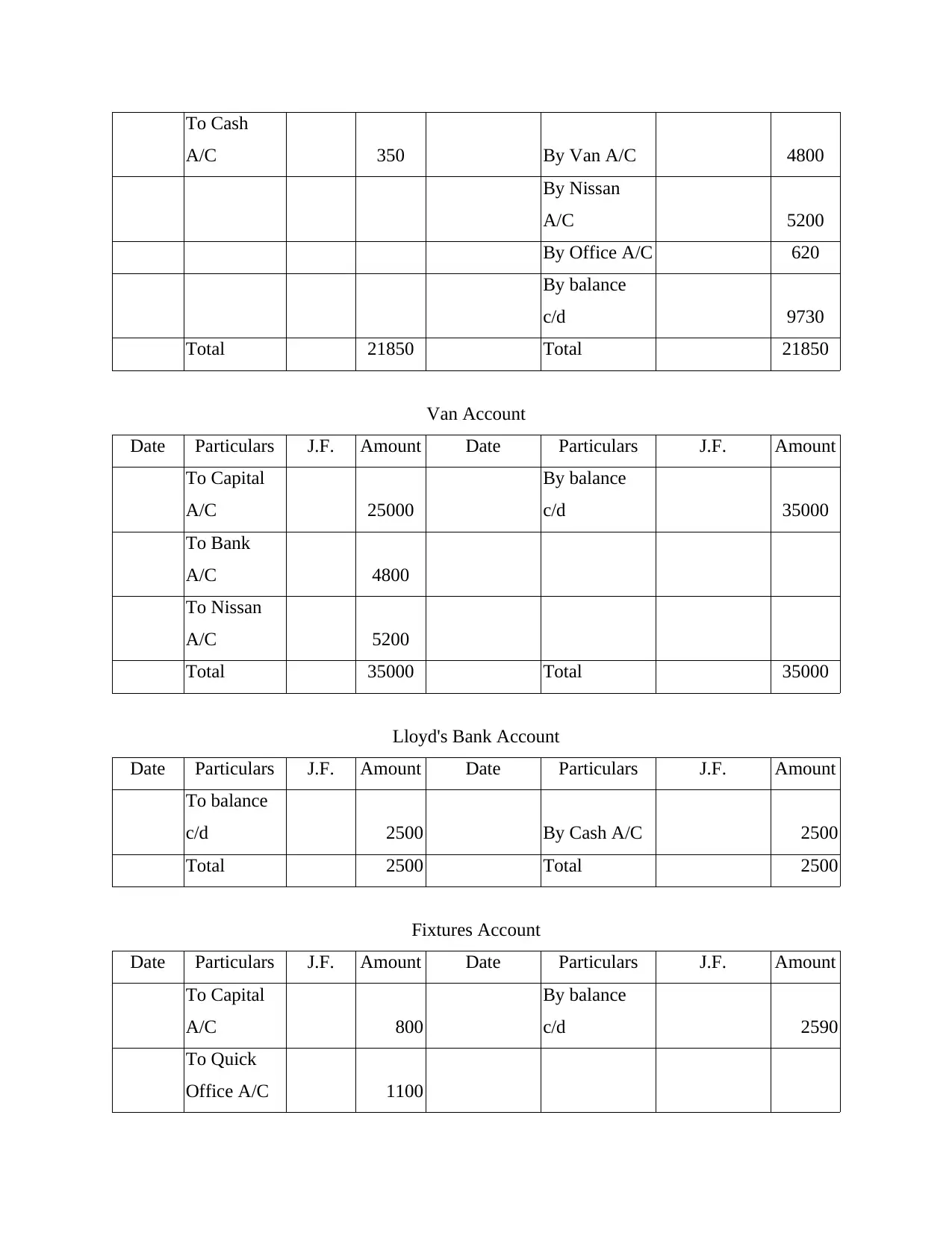

a) General ledger of Pearce and Sons

Bank Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To Capital

A/C 21500 By Cash A/C 1500

a) Journal Entries in David wise business

Part 3

a) General ledger of Pearce and Sons

Bank Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To Capital

A/C 21500 By Cash A/C 1500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To Cash

A/C 350 By Van A/C 4800

By Nissan

A/C 5200

By Office A/C 620

By balance

c/d 9730

Total 21850 Total 21850

Van Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To Capital

A/C 25000

By balance

c/d 35000

To Bank

A/C 4800

To Nissan

A/C 5200

Total 35000 Total 35000

Lloyd's Bank Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To balance

c/d 2500 By Cash A/C 2500

Total 2500 Total 2500

Fixtures Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To Capital

A/C 800

By balance

c/d 2590

To Quick

Office A/C 1100

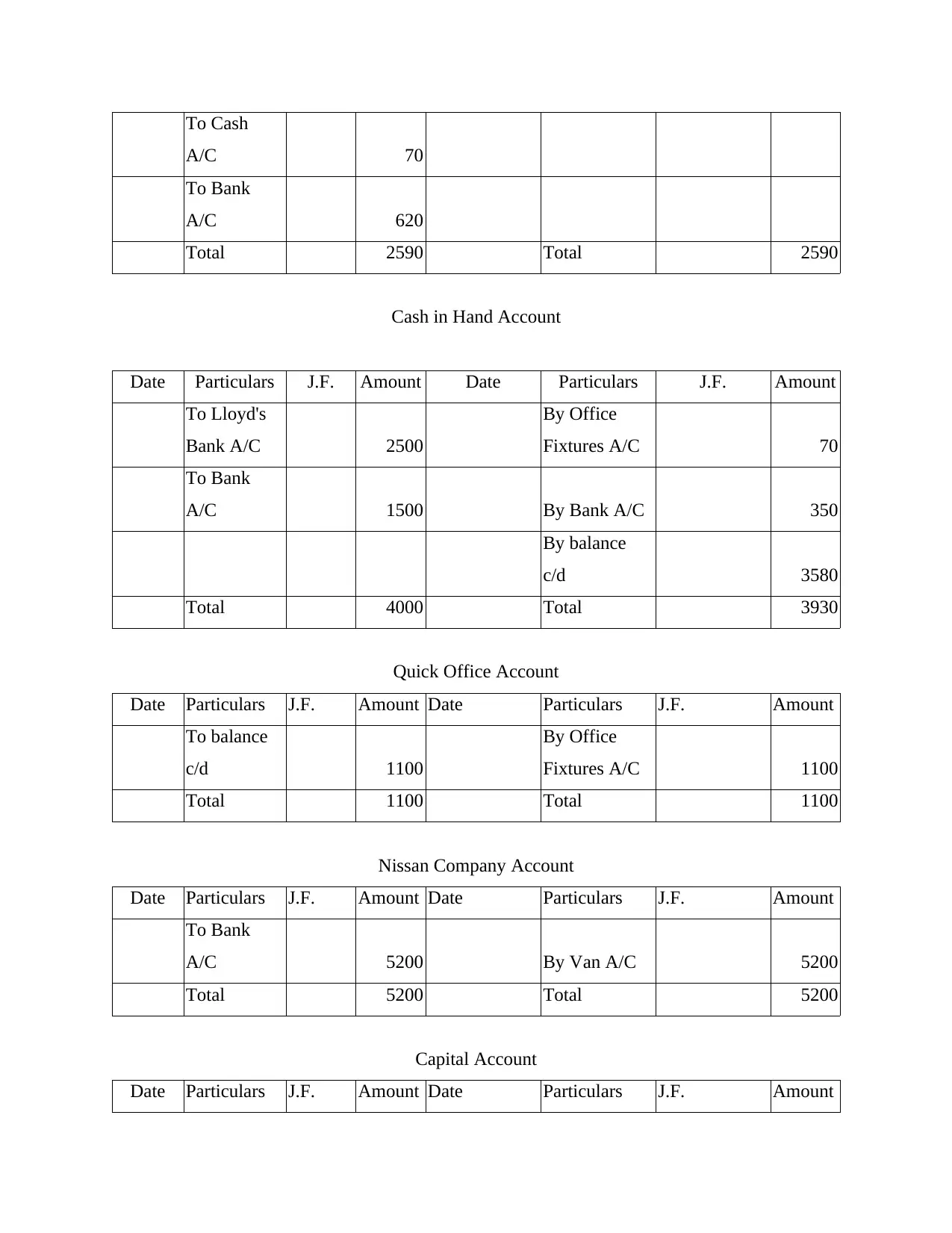

A/C 350 By Van A/C 4800

By Nissan

A/C 5200

By Office A/C 620

By balance

c/d 9730

Total 21850 Total 21850

Van Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To Capital

A/C 25000

By balance

c/d 35000

To Bank

A/C 4800

To Nissan

A/C 5200

Total 35000 Total 35000

Lloyd's Bank Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To balance

c/d 2500 By Cash A/C 2500

Total 2500 Total 2500

Fixtures Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To Capital

A/C 800

By balance

c/d 2590

To Quick

Office A/C 1100

To Cash

A/C 70

To Bank

A/C 620

Total 2590 Total 2590

Cash in Hand Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To Lloyd's

Bank A/C 2500

By Office

Fixtures A/C 70

To Bank

A/C 1500 By Bank A/C 350

By balance

c/d 3580

Total 4000 Total 3930

Quick Office Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To balance

c/d 1100

By Office

Fixtures A/C 1100

Total 1100 Total 1100

Nissan Company Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To Bank

A/C 5200 By Van A/C 5200

Total 5200 Total 5200

Capital Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

A/C 70

To Bank

A/C 620

Total 2590 Total 2590

Cash in Hand Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To Lloyd's

Bank A/C 2500

By Office

Fixtures A/C 70

To Bank

A/C 1500 By Bank A/C 350

By balance

c/d 3580

Total 4000 Total 3930

Quick Office Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To balance

c/d 1100

By Office

Fixtures A/C 1100

Total 1100 Total 1100

Nissan Company Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

To Bank

A/C 5200 By Van A/C 5200

Total 5200 Total 5200

Capital Account

Date Particulars J.F. Amount Date Particulars J.F. Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

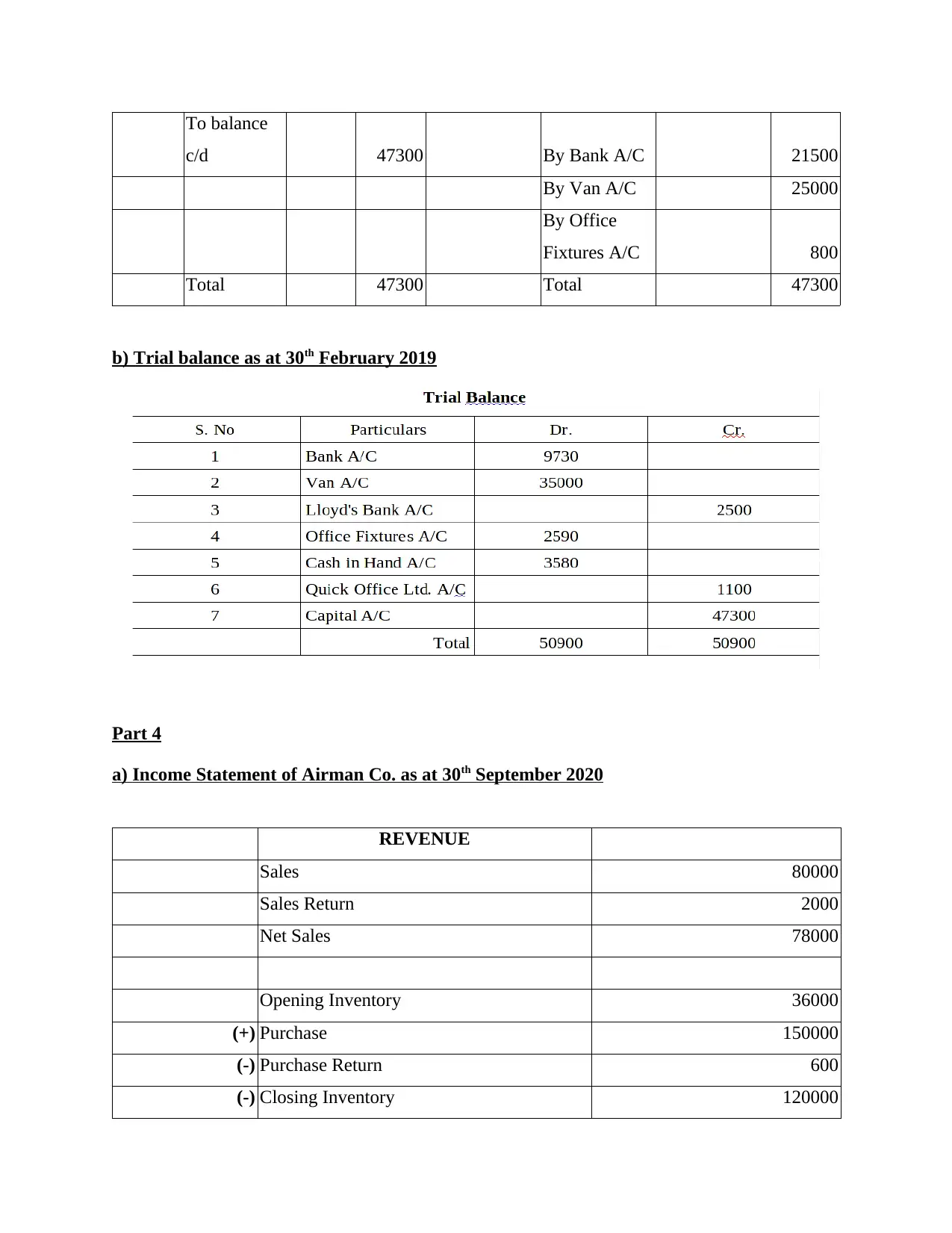

To balance

c/d 47300 By Bank A/C 21500

By Van A/C 25000

By Office

Fixtures A/C 800

Total 47300 Total 47300

b) Trial balance as at 30th February 2019

Part 4

a) Income Statement of Airman Co. as at 30th September 2020

REVENUE

Sales 80000

Sales Return 2000

Net Sales 78000

Opening Inventory 36000

(+) Purchase 150000

(-) Purchase Return 600

(-) Closing Inventory 120000

c/d 47300 By Bank A/C 21500

By Van A/C 25000

By Office

Fixtures A/C 800

Total 47300 Total 47300

b) Trial balance as at 30th February 2019

Part 4

a) Income Statement of Airman Co. as at 30th September 2020

REVENUE

Sales 80000

Sales Return 2000

Net Sales 78000

Opening Inventory 36000

(+) Purchase 150000

(-) Purchase Return 600

(-) Closing Inventory 120000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

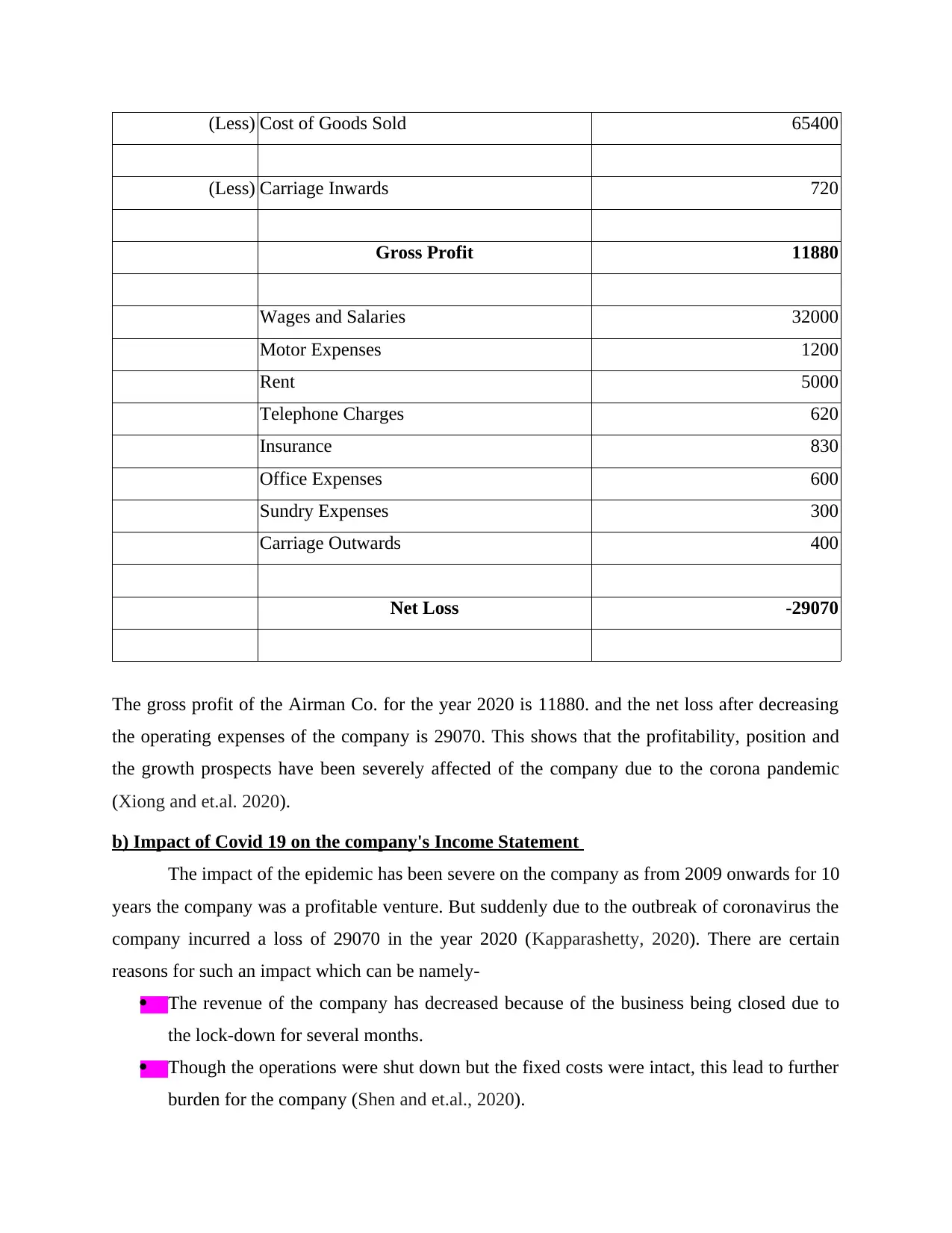

(Less) Cost of Goods Sold 65400

(Less) Carriage Inwards 720

Gross Profit 11880

Wages and Salaries 32000

Motor Expenses 1200

Rent 5000

Telephone Charges 620

Insurance 830

Office Expenses 600

Sundry Expenses 300

Carriage Outwards 400

Net Loss -29070

The gross profit of the Airman Co. for the year 2020 is 11880. and the net loss after decreasing

the operating expenses of the company is 29070. This shows that the profitability, position and

the growth prospects have been severely affected of the company due to the corona pandemic

(Xiong and et.al. 2020).

b) Impact of Covid 19 on the company's Income Statement

The impact of the epidemic has been severe on the company as from 2009 onwards for 10

years the company was a profitable venture. But suddenly due to the outbreak of coronavirus the

company incurred a loss of 29070 in the year 2020 (Kapparashetty, 2020). There are certain

reasons for such an impact which can be namely-

The revenue of the company has decreased because of the business being closed due to

the lock-down for several months.

Though the operations were shut down but the fixed costs were intact, this lead to further

burden for the company (Shen and et.al., 2020).

(Less) Carriage Inwards 720

Gross Profit 11880

Wages and Salaries 32000

Motor Expenses 1200

Rent 5000

Telephone Charges 620

Insurance 830

Office Expenses 600

Sundry Expenses 300

Carriage Outwards 400

Net Loss -29070

The gross profit of the Airman Co. for the year 2020 is 11880. and the net loss after decreasing

the operating expenses of the company is 29070. This shows that the profitability, position and

the growth prospects have been severely affected of the company due to the corona pandemic

(Xiong and et.al. 2020).

b) Impact of Covid 19 on the company's Income Statement

The impact of the epidemic has been severe on the company as from 2009 onwards for 10

years the company was a profitable venture. But suddenly due to the outbreak of coronavirus the

company incurred a loss of 29070 in the year 2020 (Kapparashetty, 2020). There are certain

reasons for such an impact which can be namely-

The revenue of the company has decreased because of the business being closed due to

the lock-down for several months.

Though the operations were shut down but the fixed costs were intact, this lead to further

burden for the company (Shen and et.al., 2020).

The workforce were not working for half the year in government compliance, but the

wages and salaries had to be paid. This further lead to downfall in the profits of the

company.

The fixed costs like the rent, telephone charges etc. were accrued even though the

business activities were not there. These overheads were not allocable to any of the jobs.

The sales of the company were affected due to the lack of disposable income with the

customers and change in their spending habit (Chowdhury and et.al., 2020).

The stock in hand remained idle for a period and this increased the cost of its storage and

the cost of damages.

The debtor's recovery period also increased simultaneously because of liquidity issues

with the debtors. This posed further threat on the working cycle of the company.

The liquidity crisis was also playing part in the loss of the company and this was because

of late recovery from debtors and improper management of cash.

During the year the promotional activities were also not much so the company was

ineffective in attracting new customers in the company (Babuna and et.al., 2020).

All the fixed assets of the company like van, fixtures and fittings were depreciated

without being used to generate the income. So these costs further burdened the company

without providing any simultaneous gain.

The company could not provide attractive deals like discounts, freebies, coupons etc

which impacted it with the customer loyalty.

The company had to further incur costs in respect to covid 19 like the sanitizers,

temperature machines, extra furnitures due to social distancing etc. These costs

contributed to the deepening of losses.

Drawings were also made by the sole owner which decreased the capital in use by

decreasing the operations of the company (Rapaccini and et.al., 2020).

The growth and expansion plans of the company could also not be achieved like targeting

a new market segment or launching a new product in the market.

The company also suffered because of lack of technical excellence. The competitors

during the pandemic started the operations online but the company suffered as it does not

tech savvy employees. So their market share was captured by the competitors.

wages and salaries had to be paid. This further lead to downfall in the profits of the

company.

The fixed costs like the rent, telephone charges etc. were accrued even though the

business activities were not there. These overheads were not allocable to any of the jobs.

The sales of the company were affected due to the lack of disposable income with the

customers and change in their spending habit (Chowdhury and et.al., 2020).

The stock in hand remained idle for a period and this increased the cost of its storage and

the cost of damages.

The debtor's recovery period also increased simultaneously because of liquidity issues

with the debtors. This posed further threat on the working cycle of the company.

The liquidity crisis was also playing part in the loss of the company and this was because

of late recovery from debtors and improper management of cash.

During the year the promotional activities were also not much so the company was

ineffective in attracting new customers in the company (Babuna and et.al., 2020).

All the fixed assets of the company like van, fixtures and fittings were depreciated

without being used to generate the income. So these costs further burdened the company

without providing any simultaneous gain.

The company could not provide attractive deals like discounts, freebies, coupons etc

which impacted it with the customer loyalty.

The company had to further incur costs in respect to covid 19 like the sanitizers,

temperature machines, extra furnitures due to social distancing etc. These costs

contributed to the deepening of losses.

Drawings were also made by the sole owner which decreased the capital in use by

decreasing the operations of the company (Rapaccini and et.al., 2020).

The growth and expansion plans of the company could also not be achieved like targeting

a new market segment or launching a new product in the market.

The company also suffered because of lack of technical excellence. The competitors

during the pandemic started the operations online but the company suffered as it does not

tech savvy employees. So their market share was captured by the competitors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.