Financial Reporting and Accounting Standards Analysis for ACC00713

VerifiedAdded on 2023/04/03

|13

|2556

|307

Report

AI Summary

This report provides an analysis of financial reporting, focusing on the application of Australian Accounting Standards (AASBs) and financial ratio analysis. The report begins with an executive summary and table of contents, followed by an introduction to financial accounting and reporting. It then discusses the AASB Conceptual Framework, AASB 15 (Revenue from Contracts with Customers), AASB 101 (Presentation of Financial Statements), and AASB 118 (Revenue). The core of the report analyzes the financial performance of Farm Pride Food Ltd. using financial ratios such as current ratio, quick ratio, operating profit, and net profit, offering insights into the company's liquidity, profitability, and financial health. The analysis considers the impact of these ratios on investors and the company's overall financial position. The report concludes with a summary of the findings and a list of references.

Running head: Accounting and Financial Reporting

Accounting and Financial Reporting

Name of the Student

Name of the University

Author Note

Accounting and Financial Reporting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Accounting and Financial Reporting

Executive Summary

The report include about the concept of financial reporting and details of the accounting

standard and also show how the company able to present their financial statement properly in

front of the stakeholders. It also shows different accounting standard and how the company

should use in regards of the financial statement. Lastly it show about the financial ratio of the

company and show they are been affected to the investors.

Accounting and Financial Reporting

Executive Summary

The report include about the concept of financial reporting and details of the accounting

standard and also show how the company able to present their financial statement properly in

front of the stakeholders. It also shows different accounting standard and how the company

should use in regards of the financial statement. Lastly it show about the financial ratio of the

company and show they are been affected to the investors.

2

Accounting and Financial Reporting

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Overview of the company......................................................................................................3

AASB Conceptual Framework..............................................................................................4

AASB 15 – Revenue from Contracts with Customers...........................................................4

AASB 101 – Presentation of Financial Statement.................................................................5

AASB 118 – Revenue............................................................................................................6

Analysis of the company with the help of Financial Ratio....................................................7

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

Accounting and Financial Reporting

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Overview of the company......................................................................................................3

AASB Conceptual Framework..............................................................................................4

AASB 15 – Revenue from Contracts with Customers...........................................................4

AASB 101 – Presentation of Financial Statement.................................................................5

AASB 118 – Revenue............................................................................................................6

Analysis of the company with the help of Financial Ratio....................................................7

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Accounting and Financial Reporting

Introduction

Financial accounting is the process from which the company disclose all the material

fact in front of the stakeholder of the company. It show the detail as how the company is been

performing in the market and also how much have increase its business as per the accounting

period (Beatty and Liao 2014). It contains different types of report and help the user to know

the value of the company. The financial reporting have many reports balance sheet, income

statement, cash flow statement and changes in equity statement. Each report so a different

aspect of the company and help the stakeholder to take necessary decision in regards of the

company (Bebbington, Unerman and O’DWYER 2014).

Accounting standard help the company to know the principle while making the

financial statement of the company. It contain all the guidelines which the company should

follow in regards of the preparation of the financial report of the company. It contain the

detail of the account and also have the principle which the company should follow in

different aspects of the account (Francis et al., 2015). It guide the company in regards how it

should record a transaction in the financial statement and how they should do the valuation of

the same. It also help them to present the information properly in the financial statement as

the user is readily available information and it able to understand it properly so it will leave a

good image in front of the financial user. It helps them to follow all the rules and regulation

about the preparation of financial statement (Glover 2014).

Discussion

Overview of the company

The report is been based upon the company name Farm Pride Food Ltd. It is been

based in Kaduna, Kaduna State and it deals with the product like fresh juices and yoghurts.

Accounting and Financial Reporting

Introduction

Financial accounting is the process from which the company disclose all the material

fact in front of the stakeholder of the company. It show the detail as how the company is been

performing in the market and also how much have increase its business as per the accounting

period (Beatty and Liao 2014). It contains different types of report and help the user to know

the value of the company. The financial reporting have many reports balance sheet, income

statement, cash flow statement and changes in equity statement. Each report so a different

aspect of the company and help the stakeholder to take necessary decision in regards of the

company (Bebbington, Unerman and O’DWYER 2014).

Accounting standard help the company to know the principle while making the

financial statement of the company. It contain all the guidelines which the company should

follow in regards of the preparation of the financial report of the company. It contain the

detail of the account and also have the principle which the company should follow in

different aspects of the account (Francis et al., 2015). It guide the company in regards how it

should record a transaction in the financial statement and how they should do the valuation of

the same. It also help them to present the information properly in the financial statement as

the user is readily available information and it able to understand it properly so it will leave a

good image in front of the financial user. It helps them to follow all the rules and regulation

about the preparation of financial statement (Glover 2014).

Discussion

Overview of the company

The report is been based upon the company name Farm Pride Food Ltd. It is been

based in Kaduna, Kaduna State and it deals with the product like fresh juices and yoghurts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Accounting and Financial Reporting

The company carry its business in Nigeria and it is a Nigerian brand which only deal

beverages from natural fruits.

AASB Conceptual Framework

It is the guideline or framework in regards of the “preparation and presentation of

financial statement”. The purpose of this to assist the AASB in regards of the coming up with

new standard and also keeping changes in the old standard, so it can be say that it check the

old standard as also it time to time come up with the new standard. It also help the AASB to

make norms and regulation in regards of the preparation and presentation of the financial

statement in regards of this standard (Henderson et al., 2015). It also help in making the

procedure in regards of the presentation and preparation of the accounting standard so that the

company can able to get more better presentation in the financial statement. It help in the

preparation of the financial statement as per the rules and regulation given by the accounting

standard as it show and guide the m in the preparation of the financial statement (Aasb.gov.au

2019). It also helps the external auditor in regards of the opinion that the company is having

true and fair view or not. As it give all the guidelines that the company should follow in

regards of the financial statement so if they do not follow the rules than the financial

statement are not showing true and fair view (Hoyle, Schaefer and Doupnik 2015). The

framework guides the user to interpret the financial statement and able to take the decision in

regards of the financial statement. As it contain all the information so it help the user to know

more about company and able to take proper decision in regards of the company.

AASB 15 – Revenue from Contracts with Customers

The standard deals about the provision related to the recognition of revenue from

contracts with customers. It state all the principle related to the amount, timing, nature and

uncertainty related to the cash flow from the contract with the customers. So it gives the

criteria when the company can able to record as when the company and other party have

Accounting and Financial Reporting

The company carry its business in Nigeria and it is a Nigerian brand which only deal

beverages from natural fruits.

AASB Conceptual Framework

It is the guideline or framework in regards of the “preparation and presentation of

financial statement”. The purpose of this to assist the AASB in regards of the coming up with

new standard and also keeping changes in the old standard, so it can be say that it check the

old standard as also it time to time come up with the new standard. It also help the AASB to

make norms and regulation in regards of the preparation and presentation of the financial

statement in regards of this standard (Henderson et al., 2015). It also help in making the

procedure in regards of the presentation and preparation of the accounting standard so that the

company can able to get more better presentation in the financial statement. It help in the

preparation of the financial statement as per the rules and regulation given by the accounting

standard as it show and guide the m in the preparation of the financial statement (Aasb.gov.au

2019). It also helps the external auditor in regards of the opinion that the company is having

true and fair view or not. As it give all the guidelines that the company should follow in

regards of the financial statement so if they do not follow the rules than the financial

statement are not showing true and fair view (Hoyle, Schaefer and Doupnik 2015). The

framework guides the user to interpret the financial statement and able to take the decision in

regards of the financial statement. As it contain all the information so it help the user to know

more about company and able to take proper decision in regards of the company.

AASB 15 – Revenue from Contracts with Customers

The standard deals about the provision related to the recognition of revenue from

contracts with customers. It state all the principle related to the amount, timing, nature and

uncertainty related to the cash flow from the contract with the customers. So it gives the

criteria when the company can able to record as when the company and other party have

5

Accounting and Financial Reporting

entered in to the contract and it is been approve by oral or by written method, when the

company is able to identify the right of the contract as it able to know the right in regards of

the good and services (Kieso, Weygandt and Warfield 2016). It able to know the details of

the payment and able to judge the proper amount of the contract. It should able to ascertain

all the above points and then only it will able to record the same as revenue from the contract

from the customers (Aasb.gov.au 2019). The standard also contain many details about the

contract and many other definition so that it will be able to judge by the company and help

them to correctly follow the standard. It also state about the disclosure of the company as the

company should disclose all the revenue from the contract and also should disclosure

judgements which the company have taken in regards of the account (Kimmel et al., 2016).

So it should disclose all the fact about the contract in the company financial account.

AASB 101 – Presentation of Financial Statement

This standard state about how the company should present the financial statement in

the financial reporting of the company (Libby 2017). This provide the guidelines of the

preparation of the financial statement of the company as it should be prepare in a proper

manner so that the financial statement can be easily comparable with other period of the

company and also with the other company in the industry as it show them the proper

guidance so that the financial user can easily able to compare it and able to take proper

decision in regards of the company (Aasb.gov.au 2019). It gets them an overview guide so

that it can able to prepare the financial statement properly and can make a proper financial

statement of the company (Schaltegger and Burritt 2017). So this helps the company to

provide the financial information properly in the financial statement so that the user can able

to know the details of the company. It also describe the other items of the financial statement

so that the company can able to know all the related definition and can able to easily record

the asset in the financial statement of the company (Warren Jr, Moffitt and Byrnes 2015).

Accounting and Financial Reporting

entered in to the contract and it is been approve by oral or by written method, when the

company is able to identify the right of the contract as it able to know the right in regards of

the good and services (Kieso, Weygandt and Warfield 2016). It able to know the details of

the payment and able to judge the proper amount of the contract. It should able to ascertain

all the above points and then only it will able to record the same as revenue from the contract

from the customers (Aasb.gov.au 2019). The standard also contain many details about the

contract and many other definition so that it will be able to judge by the company and help

them to correctly follow the standard. It also state about the disclosure of the company as the

company should disclose all the revenue from the contract and also should disclosure

judgements which the company have taken in regards of the account (Kimmel et al., 2016).

So it should disclose all the fact about the contract in the company financial account.

AASB 101 – Presentation of Financial Statement

This standard state about how the company should present the financial statement in

the financial reporting of the company (Libby 2017). This provide the guidelines of the

preparation of the financial statement of the company as it should be prepare in a proper

manner so that the financial statement can be easily comparable with other period of the

company and also with the other company in the industry as it show them the proper

guidance so that the financial user can easily able to compare it and able to take proper

decision in regards of the company (Aasb.gov.au 2019). It gets them an overview guide so

that it can able to prepare the financial statement properly and can make a proper financial

statement of the company (Schaltegger and Burritt 2017). So this helps the company to

provide the financial information properly in the financial statement so that the user can able

to know the details of the company. It also describe the other items of the financial statement

so that the company can able to know all the related definition and can able to easily record

the asset in the financial statement of the company (Warren Jr, Moffitt and Byrnes 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Accounting and Financial Reporting

AASB 118 – Revenue

The standard deals with the how the company should record the revenue in the

balance sheet and also the related disclosure in the notes on accounts. It state that the there

are two kind of income in the business (Aasb.gov.au 2019). One is gain and other is revenue.

Revenue is been classified as the income which the company gets in the ordinary course of

the business whereas gain stand for the other income which the company get from the

business. The standard state the answer of the problem that when the company should record

the income as revenue in the business. It state that an income is been termed as revenue

when the company is able to get some economic benefit from the revenue in future and also it

able to calculate the amount of the revenue. The circumstance which should be there in the

income so that it will be consider as a revenue, the standard state that the ownership is been

transferred to the buyer and ll the risk and reward related to the goods is been given to the

buyer, the company does not have any right upon the good which they have transferred to the

buyer, the company is able to recognise the amount of revenue which they will earn in

respect of the goods transferred to then buyer, the confirmation of the ownership transfer is

been done and all the future economic benefit from the goods should be entitled by the new

entity, it also that the company is able to know real cost which they have spend upon the

good and had record the same in the financial statement of the company.

The disclosure which the company should give in respect of the revenue is that it

should show the accounting policy which the company have used in regards of the

recognition of the revenue and also should disclose the methods which is been used by the

company to know the timing of recording the revenue in the financial statement of the

company. It should also disclose any contingent asset or liabilities which are there in the

company (Aasb.gov.au 2019).

Accounting and Financial Reporting

AASB 118 – Revenue

The standard deals with the how the company should record the revenue in the

balance sheet and also the related disclosure in the notes on accounts. It state that the there

are two kind of income in the business (Aasb.gov.au 2019). One is gain and other is revenue.

Revenue is been classified as the income which the company gets in the ordinary course of

the business whereas gain stand for the other income which the company get from the

business. The standard state the answer of the problem that when the company should record

the income as revenue in the business. It state that an income is been termed as revenue

when the company is able to get some economic benefit from the revenue in future and also it

able to calculate the amount of the revenue. The circumstance which should be there in the

income so that it will be consider as a revenue, the standard state that the ownership is been

transferred to the buyer and ll the risk and reward related to the goods is been given to the

buyer, the company does not have any right upon the good which they have transferred to the

buyer, the company is able to recognise the amount of revenue which they will earn in

respect of the goods transferred to then buyer, the confirmation of the ownership transfer is

been done and all the future economic benefit from the goods should be entitled by the new

entity, it also that the company is able to know real cost which they have spend upon the

good and had record the same in the financial statement of the company.

The disclosure which the company should give in respect of the revenue is that it

should show the accounting policy which the company have used in regards of the

recognition of the revenue and also should disclose the methods which is been used by the

company to know the timing of recording the revenue in the financial statement of the

company. It should also disclose any contingent asset or liabilities which are there in the

company (Aasb.gov.au 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Accounting and Financial Reporting

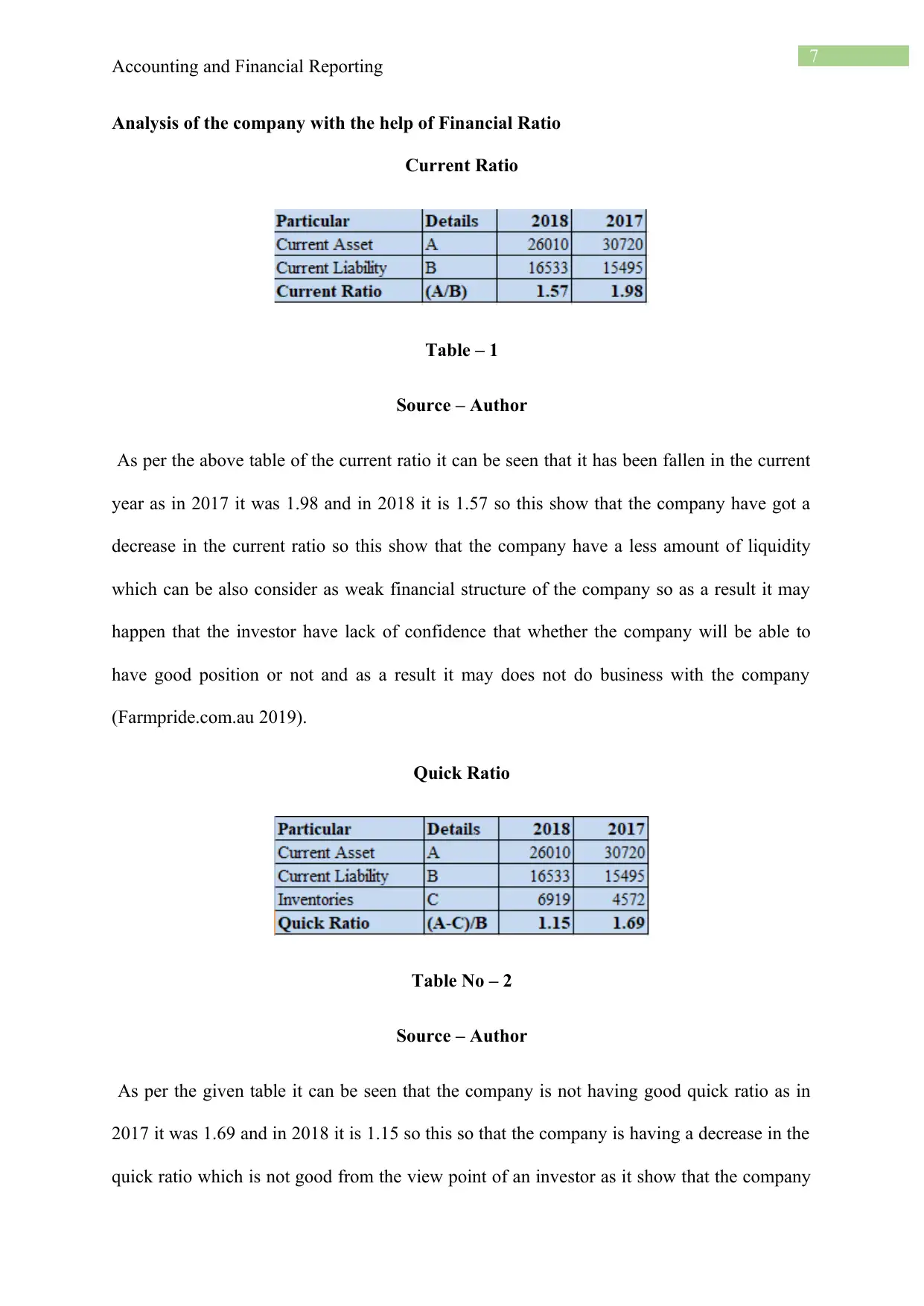

Analysis of the company with the help of Financial Ratio

Current Ratio

Table – 1

Source – Author

As per the above table of the current ratio it can be seen that it has been fallen in the current

year as in 2017 it was 1.98 and in 2018 it is 1.57 so this show that the company have got a

decrease in the current ratio so this show that the company have a less amount of liquidity

which can be also consider as weak financial structure of the company so as a result it may

happen that the investor have lack of confidence that whether the company will be able to

have good position or not and as a result it may does not do business with the company

(Farmpride.com.au 2019).

Quick Ratio

Table No – 2

Source – Author

As per the given table it can be seen that the company is not having good quick ratio as in

2017 it was 1.69 and in 2018 it is 1.15 so this so that the company is having a decrease in the

quick ratio which is not good from the view point of an investor as it show that the company

Accounting and Financial Reporting

Analysis of the company with the help of Financial Ratio

Current Ratio

Table – 1

Source – Author

As per the above table of the current ratio it can be seen that it has been fallen in the current

year as in 2017 it was 1.98 and in 2018 it is 1.57 so this show that the company have got a

decrease in the current ratio so this show that the company have a less amount of liquidity

which can be also consider as weak financial structure of the company so as a result it may

happen that the investor have lack of confidence that whether the company will be able to

have good position or not and as a result it may does not do business with the company

(Farmpride.com.au 2019).

Quick Ratio

Table No – 2

Source – Author

As per the given table it can be seen that the company is not having good quick ratio as in

2017 it was 1.69 and in 2018 it is 1.15 so this so that the company is having a decrease in the

quick ratio which is not good from the view point of an investor as it show that the company

8

Accounting and Financial Reporting

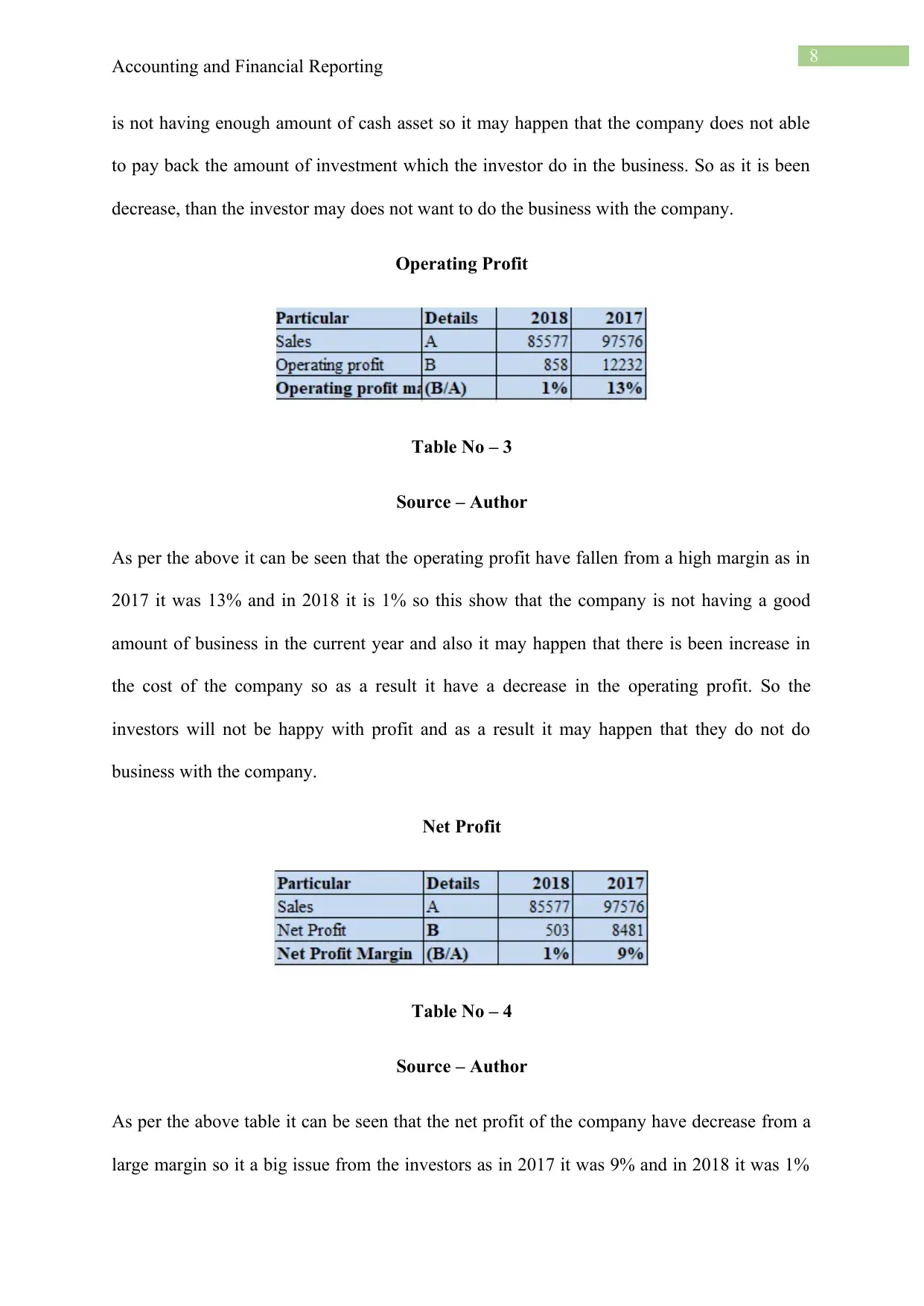

is not having enough amount of cash asset so it may happen that the company does not able

to pay back the amount of investment which the investor do in the business. So as it is been

decrease, than the investor may does not want to do the business with the company.

Operating Profit

Table No – 3

Source – Author

As per the above it can be seen that the operating profit have fallen from a high margin as in

2017 it was 13% and in 2018 it is 1% so this show that the company is not having a good

amount of business in the current year and also it may happen that there is been increase in

the cost of the company so as a result it have a decrease in the operating profit. So the

investors will not be happy with profit and as a result it may happen that they do not do

business with the company.

Net Profit

Table No – 4

Source – Author

As per the above table it can be seen that the net profit of the company have decrease from a

large margin so it a big issue from the investors as in 2017 it was 9% and in 2018 it was 1%

Accounting and Financial Reporting

is not having enough amount of cash asset so it may happen that the company does not able

to pay back the amount of investment which the investor do in the business. So as it is been

decrease, than the investor may does not want to do the business with the company.

Operating Profit

Table No – 3

Source – Author

As per the above it can be seen that the operating profit have fallen from a high margin as in

2017 it was 13% and in 2018 it is 1% so this show that the company is not having a good

amount of business in the current year and also it may happen that there is been increase in

the cost of the company so as a result it have a decrease in the operating profit. So the

investors will not be happy with profit and as a result it may happen that they do not do

business with the company.

Net Profit

Table No – 4

Source – Author

As per the above table it can be seen that the net profit of the company have decrease from a

large margin so it a big issue from the investors as in 2017 it was 9% and in 2018 it was 1%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Accounting and Financial Reporting

so this is a big problem as the investor may find that the company is not having good

customer business and also it can happen that market is not there in the company so it happen

that the investors does not invest in the company.

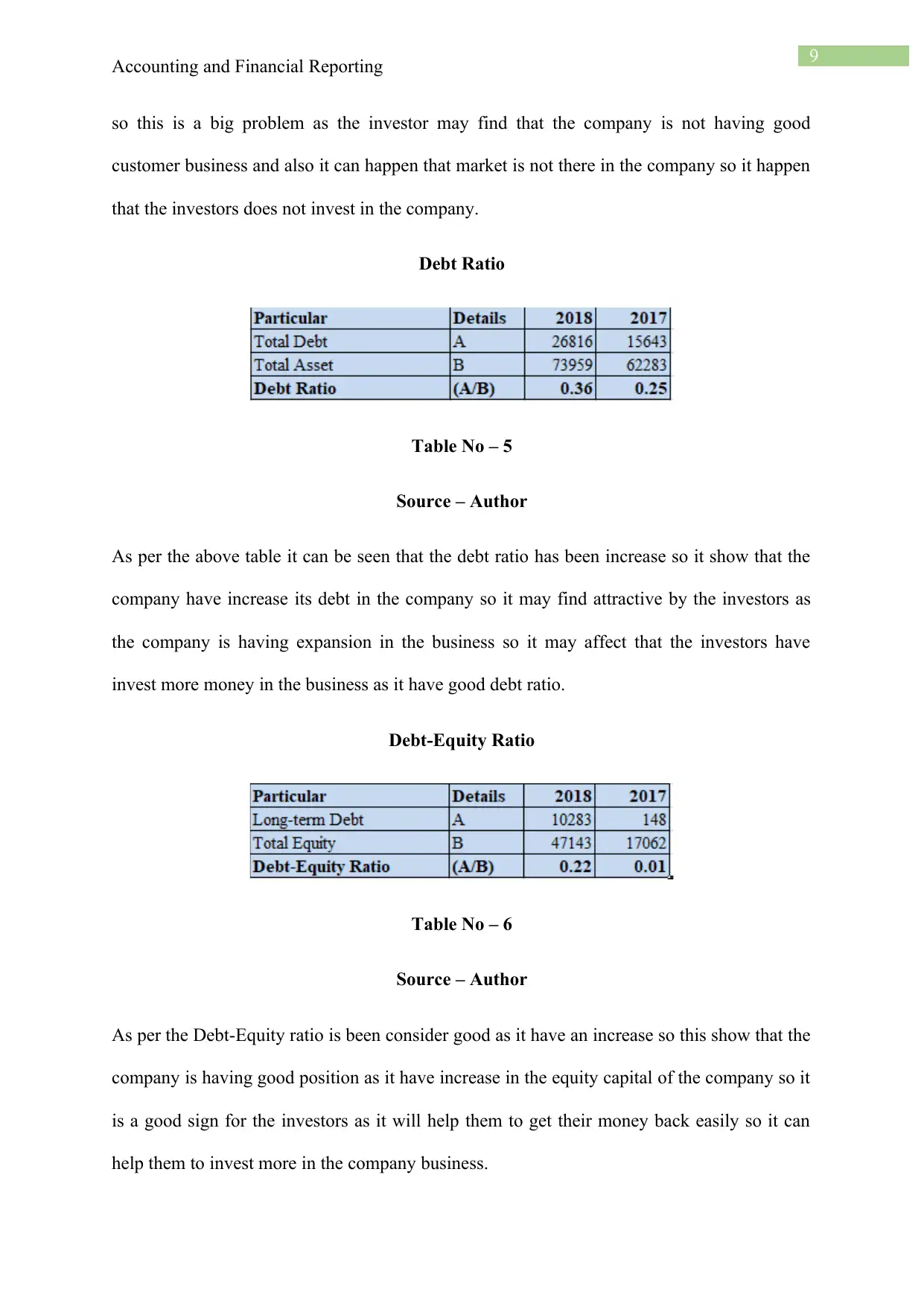

Debt Ratio

Table No – 5

Source – Author

As per the above table it can be seen that the debt ratio has been increase so it show that the

company have increase its debt in the company so it may find attractive by the investors as

the company is having expansion in the business so it may affect that the investors have

invest more money in the business as it have good debt ratio.

Debt-Equity Ratio

Table No – 6

Source – Author

As per the Debt-Equity ratio is been consider good as it have an increase so this show that the

company is having good position as it have increase in the equity capital of the company so it

is a good sign for the investors as it will help them to get their money back easily so it can

help them to invest more in the company business.

Accounting and Financial Reporting

so this is a big problem as the investor may find that the company is not having good

customer business and also it can happen that market is not there in the company so it happen

that the investors does not invest in the company.

Debt Ratio

Table No – 5

Source – Author

As per the above table it can be seen that the debt ratio has been increase so it show that the

company have increase its debt in the company so it may find attractive by the investors as

the company is having expansion in the business so it may affect that the investors have

invest more money in the business as it have good debt ratio.

Debt-Equity Ratio

Table No – 6

Source – Author

As per the Debt-Equity ratio is been consider good as it have an increase so this show that the

company is having good position as it have increase in the equity capital of the company so it

is a good sign for the investors as it will help them to get their money back easily so it can

help them to invest more in the company business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Accounting and Financial Reporting

Conclusion

The report is been conclude as the financial account and accounting standard details

as how it help the company to manage and present the financial statement in the company. It

also contains some details of the accounting standard and how they should be implement in

the financial statement. Lastly it show the details of the investors view with regards of the

financial ratio of the company.

Accounting and Financial Reporting

Conclusion

The report is been conclude as the financial account and accounting standard details

as how it help the company to manage and present the financial statement in the company. It

also contains some details of the accounting standard and how they should be implement in

the financial statement. Lastly it show the details of the investors view with regards of the

financial ratio of the company.

11

Accounting and Financial Reporting

Reference

Aasb.gov.au (2019). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed 25 May

2019].

Aasb.gov.au (2019). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB15_12-14_COMPsep18_01-19.pdf

[Accessed 25 May 2019].

Aasb.gov.au (2019). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 25 May

2019].

Aasb.gov.au (2019). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB118_07-04_COMPoct10_01-11.pdf

[Accessed 25 May 2019].

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Bebbington, J., Unerman, J. and O’DWYER, B.R.E.N.D.A.N., 2014. Introduction to

sustainability accounting and accountability. In Sustainability accounting and

accountability(pp. 21-32). Routledge.

Farmpride.com.au (2019). [online] Farmpride.com.au. Available at:

http://www.farmpride.com.au/wp-content/uploads/2019/02/2018-Farm-Pride-Foods-Ltd-

Annual-Report.pdf [Accessed 25 May 2019].

Accounting and Financial Reporting

Reference

Aasb.gov.au (2019). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed 25 May

2019].

Aasb.gov.au (2019). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB15_12-14_COMPsep18_01-19.pdf

[Accessed 25 May 2019].

Aasb.gov.au (2019). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 25 May

2019].

Aasb.gov.au (2019). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB118_07-04_COMPoct10_01-11.pdf

[Accessed 25 May 2019].

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Bebbington, J., Unerman, J. and O’DWYER, B.R.E.N.D.A.N., 2014. Introduction to

sustainability accounting and accountability. In Sustainability accounting and

accountability(pp. 21-32). Routledge.

Farmpride.com.au (2019). [online] Farmpride.com.au. Available at:

http://www.farmpride.com.au/wp-content/uploads/2019/02/2018-Farm-Pride-Foods-Ltd-

Annual-Report.pdf [Accessed 25 May 2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.