Financial Reporting Analysis: Sainsbury Plc, IFRS, and Stakeholders

VerifiedAdded on 2020/10/23

|13

|3363

|255

Report

AI Summary

This report delves into the multifaceted world of financial reporting, examining its purpose and context, alongside the regulatory and conceptual frameworks that govern it. It analyzes the needs of key stakeholders, including managers, customers, employees, competitors, investors, and shareholders, and assesses the value of financial reporting in achieving organizational growth and objectives. The report explores international accounting standards and International Financial Reporting Standards (IFRS), evaluating their benefits and the application of relevant theories like equity and legitimacy theory. Using Sainsbury Plc as a case study, the report evaluates the degrees of compliance with IFRS across different organizations globally, highlighting the significance of financial reporting in communicating a company's overall health and facilitating informed decision-making. The analysis encompasses the differences in financial reporting practices worldwide and the factors influencing these variations.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Analysing purpose and context of financial reporting............................................................1

2. Examining regulatory and conceptual framework along with governance of financial

reporting and explaining key principles and assessing requirement and purpose......................2

3. Determining key stakeholders of organization and assessing need of financial reporting.....3

4. Analysing value of financial reporting in business to attain organizational growth and

objectives.....................................................................................................................................4

5. International accounting standard and International financial reporting Standards and their

benefits........................................................................................................................................5

6. Evaluation of financial reporting through application of theories ........................................6

7. The differences in financial reporting across world ..............................................................7

8. Degrees of compliance with IFRS by different organisation around the world.....................8

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Analysing purpose and context of financial reporting............................................................1

2. Examining regulatory and conceptual framework along with governance of financial

reporting and explaining key principles and assessing requirement and purpose......................2

3. Determining key stakeholders of organization and assessing need of financial reporting.....3

4. Analysing value of financial reporting in business to attain organizational growth and

objectives.....................................................................................................................................4

5. International accounting standard and International financial reporting Standards and their

benefits........................................................................................................................................5

6. Evaluation of financial reporting through application of theories ........................................6

7. The differences in financial reporting across world ..............................................................7

8. Degrees of compliance with IFRS by different organisation around the world.....................8

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Financial reporting is replicated as disclosure of financial outcome and related

information to external stakeholders and management. The present report will analysis context

and purpose of financial reporting and examining its regulatory and conceptual framework on

basis of Sainsbury Plc. It will articulate about key stakeholder and assessing their need of

financial reporting. In the same series, there is analysis of importance of financial reporting for

attaining organizational growth with objectives. This report would explain international

accounting standards and International financial reporting standards with evaluation of benefits.

Simultaneously, financial reporting in organization would be explained with application of

theories and differences in financial reporting would be stated across world and evaluating

factors which influence these variations. This report has formed arguments by undertaking

Sainsbury Plc as largest chain of supermarkets in the United Kingdom as it has 16.95 share of

supermarket sector. Lastly, this will evaluate degree of compliance with IFRS through different

organization throughout world.

MAIN BODY

1. Analysing purpose and context of financial reporting

Financial reporting is disclosure of financial outcome and related information to external

stakeholders and management. It helps in giving relevant and useful information to

organization's owners where is categorisation of ownership along with company's control.

Generally, it occurs in public limited companies where share capital is directly sole to public via

stock exchange and market system (Dou, Wong and Xin, 2019). In the same series, potential and

diverse geographically dispersed shareholders does not get engaged in company's management

and directors are appointed on this behalf. The purpose of financial reporting are reflected to

potential and primary investors, creditors and lenders who uses this information for purpose of

buying decision making, holding or selling equity or debt instruments and offering or setting

loans with other form of credit. The initial users require information related to resources of entity

not only to assess prospects of entity for future net cash inflows but with effective and efficient

management has discharged responsibilities with application of existing resources. In simple

words, financial reports deliver information to share owners and lenders of business. National

accounting standards includes five standards that are been published by the Financial reporting

council in the UK that states the regulations regarding the taxation and the financial relations and

1

Financial reporting is replicated as disclosure of financial outcome and related

information to external stakeholders and management. The present report will analysis context

and purpose of financial reporting and examining its regulatory and conceptual framework on

basis of Sainsbury Plc. It will articulate about key stakeholder and assessing their need of

financial reporting. In the same series, there is analysis of importance of financial reporting for

attaining organizational growth with objectives. This report would explain international

accounting standards and International financial reporting standards with evaluation of benefits.

Simultaneously, financial reporting in organization would be explained with application of

theories and differences in financial reporting would be stated across world and evaluating

factors which influence these variations. This report has formed arguments by undertaking

Sainsbury Plc as largest chain of supermarkets in the United Kingdom as it has 16.95 share of

supermarket sector. Lastly, this will evaluate degree of compliance with IFRS through different

organization throughout world.

MAIN BODY

1. Analysing purpose and context of financial reporting

Financial reporting is disclosure of financial outcome and related information to external

stakeholders and management. It helps in giving relevant and useful information to

organization's owners where is categorisation of ownership along with company's control.

Generally, it occurs in public limited companies where share capital is directly sole to public via

stock exchange and market system (Dou, Wong and Xin, 2019). In the same series, potential and

diverse geographically dispersed shareholders does not get engaged in company's management

and directors are appointed on this behalf. The purpose of financial reporting are reflected to

potential and primary investors, creditors and lenders who uses this information for purpose of

buying decision making, holding or selling equity or debt instruments and offering or setting

loans with other form of credit. The initial users require information related to resources of entity

not only to assess prospects of entity for future net cash inflows but with effective and efficient

management has discharged responsibilities with application of existing resources. In simple

words, financial reports deliver information to share owners and lenders of business. National

accounting standards includes five standards that are been published by the Financial reporting

council in the UK that states the regulations regarding the taxation and the financial relations and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

various recommendations has been given relating to the accounting principles. In the year 2013,

the FRC committee has introduced the financial reporting standards which is been called as the

new UK generally accepted accounting principle. The regulation was made that interim reporting

will be done as per FRS 104 and reporting standards that is been applicable to micro entities.

2. Examining regulatory and conceptual framework along with governance of financial reporting

and explaining key principles and assessing requirement and purpose

The regulatory framework for purpose of preparing financial statements is mandatory for

numerous reasons such as ensuring needs of financial statement user's to accomplish with least of

basic minimum of information. All information required will be ensured in relevant economic

arena with increment in international one (Mao and Wu, 2019). This will lead to increment in

confidence of users for process of financial reporting and regulates behaviour of directors and

companies toward investors. Financial reporting standards which would be not sufficient for

attaining these objectives and there should be legal and market based regulation. In this aspect,

presence of national regulatory framework for financial reporting and its elements are stated as

national financial reporting standards, national law, market regulations and security exchange

rules.

The conceptual framework of financial reporting has underpinned preparation of financial

statements and reflects main ideas, principles and concepts upon standards of international

financial reporting and based on financial statements with discussion of objectives, qualitative

characteristics, recognition and definition of elements where financial statements are constructed.

2

the FRC committee has introduced the financial reporting standards which is been called as the

new UK generally accepted accounting principle. The regulation was made that interim reporting

will be done as per FRS 104 and reporting standards that is been applicable to micro entities.

2. Examining regulatory and conceptual framework along with governance of financial reporting

and explaining key principles and assessing requirement and purpose

The regulatory framework for purpose of preparing financial statements is mandatory for

numerous reasons such as ensuring needs of financial statement user's to accomplish with least of

basic minimum of information. All information required will be ensured in relevant economic

arena with increment in international one (Mao and Wu, 2019). This will lead to increment in

confidence of users for process of financial reporting and regulates behaviour of directors and

companies toward investors. Financial reporting standards which would be not sufficient for

attaining these objectives and there should be legal and market based regulation. In this aspect,

presence of national regulatory framework for financial reporting and its elements are stated as

national financial reporting standards, national law, market regulations and security exchange

rules.

The conceptual framework of financial reporting has underpinned preparation of financial

statements and reflects main ideas, principles and concepts upon standards of international

financial reporting and based on financial statements with discussion of objectives, qualitative

characteristics, recognition and definition of elements where financial statements are constructed.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

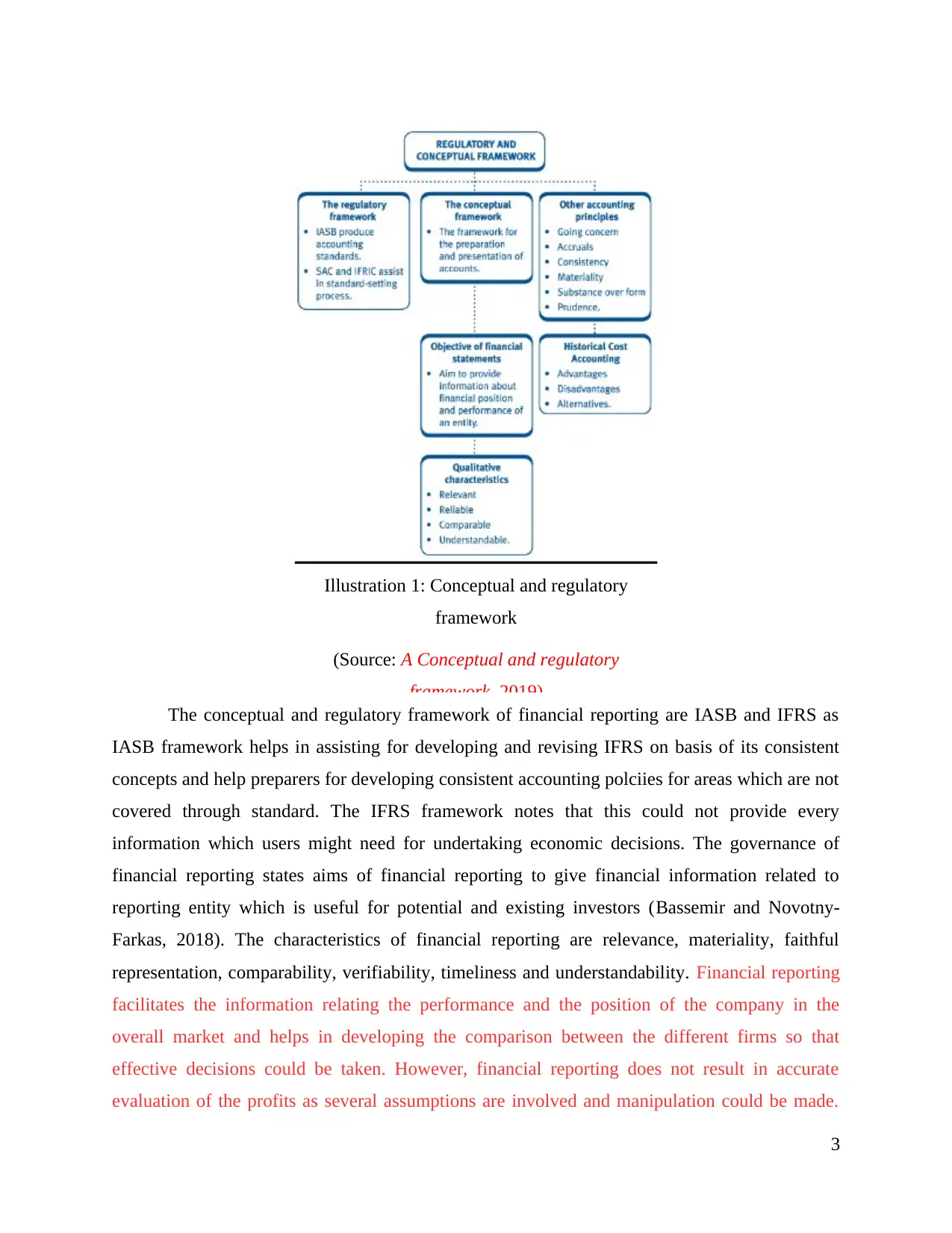

Illustration 1: Conceptual and regulatory

framework

(Source: A Conceptual and regulatory

framework, 2019)

The conceptual and regulatory framework of financial reporting are IASB and IFRS as

IASB framework helps in assisting for developing and revising IFRS on basis of its consistent

concepts and help preparers for developing consistent accounting polciies for areas which are not

covered through standard. The IFRS framework notes that this could not provide every

information which users might need for undertaking economic decisions. The governance of

financial reporting states aims of financial reporting to give financial information related to

reporting entity which is useful for potential and existing investors (Bassemir and Novotny‐

Farkas, 2018). The characteristics of financial reporting are relevance, materiality, faithful

representation, comparability, verifiability, timeliness and understandability. Financial reporting

facilitates the information relating the performance and the position of the company in the

overall market and helps in developing the comparison between the different firms so that

effective decisions could be taken. However, financial reporting does not result in accurate

evaluation of the profits as several assumptions are involved and manipulation could be made.

3

framework

(Source: A Conceptual and regulatory

framework, 2019)

The conceptual and regulatory framework of financial reporting are IASB and IFRS as

IASB framework helps in assisting for developing and revising IFRS on basis of its consistent

concepts and help preparers for developing consistent accounting polciies for areas which are not

covered through standard. The IFRS framework notes that this could not provide every

information which users might need for undertaking economic decisions. The governance of

financial reporting states aims of financial reporting to give financial information related to

reporting entity which is useful for potential and existing investors (Bassemir and Novotny‐

Farkas, 2018). The characteristics of financial reporting are relevance, materiality, faithful

representation, comparability, verifiability, timeliness and understandability. Financial reporting

facilitates the information relating the performance and the position of the company in the

overall market and helps in developing the comparison between the different firms so that

effective decisions could be taken. However, financial reporting does not result in accurate

evaluation of the profits as several assumptions are involved and manipulation could be made.

3

On the other side financial reporting based on the established concepts, rules and the standards

that are framed by the IFRS. Moreover, for complying with the set standards, highly skilled

professional are required especially in those businesses which are managed by the owners itself.

Financial auditing develops more reliability in the results that are been communicated to the

external and the internal users. Positive comments by the auditors helps in gaining the brand

image for the company in the overall market. However, auditing creates a significant disruption

at the workplace of the company which may result in the lower productivity.

3. Determining key stakeholders of organization and assessing need of financial reporting

Financial statements offer useful information to key stakeholders of Sainsbury Plc are

stated below:

Managers need financial statements for managing company affairs of organization with

context of assessing financial position and performance along with undertaking important

decisions related to business (Stubbs and Higgins, 2018).

Customers use financial statements for assessing that supplier has resources for purpose

of ensuring steady supply of goods in coming future. Especially, it is very vital that

customer is dependent with context to supplier for specialized component.

In the same series, financial statements are used by employees for assessing profitability

and consequence of organization on their future remuneration along with job security.

The performance had been compared by competitors with rival companies for

developing and learning strategies for purpose of improving competitiveness (Users of

Accounting Information, 2017).

The prospective investors require financial statements for assessing viability to invest in

particular company. The future dividends might be predicted by investors on basis of

margin disclosed in financial statements. Henceforth, associated risk with context of

investment might be gauged through financial statements.

The shareholders of Sainsbury imply financial statements for assessing return and risk of

their investment in organization and to undertake decisions related to investment on basis

of analysis.

4

that are framed by the IFRS. Moreover, for complying with the set standards, highly skilled

professional are required especially in those businesses which are managed by the owners itself.

Financial auditing develops more reliability in the results that are been communicated to the

external and the internal users. Positive comments by the auditors helps in gaining the brand

image for the company in the overall market. However, auditing creates a significant disruption

at the workplace of the company which may result in the lower productivity.

3. Determining key stakeholders of organization and assessing need of financial reporting

Financial statements offer useful information to key stakeholders of Sainsbury Plc are

stated below:

Managers need financial statements for managing company affairs of organization with

context of assessing financial position and performance along with undertaking important

decisions related to business (Stubbs and Higgins, 2018).

Customers use financial statements for assessing that supplier has resources for purpose

of ensuring steady supply of goods in coming future. Especially, it is very vital that

customer is dependent with context to supplier for specialized component.

In the same series, financial statements are used by employees for assessing profitability

and consequence of organization on their future remuneration along with job security.

The performance had been compared by competitors with rival companies for

developing and learning strategies for purpose of improving competitiveness (Users of

Accounting Information, 2017).

The prospective investors require financial statements for assessing viability to invest in

particular company. The future dividends might be predicted by investors on basis of

margin disclosed in financial statements. Henceforth, associated risk with context of

investment might be gauged through financial statements.

The shareholders of Sainsbury imply financial statements for assessing return and risk of

their investment in organization and to undertake decisions related to investment on basis

of analysis.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Analysing value of financial reporting in business to attain organizational growth and

objectives

Financial reporting is referred as method for following standard practices to give world

with accurate depiction of finances of organization which comprises revenues, profit, expenses,

cashflow and capital. These key performance indicators are significant as they reflect health of

organization. Financial reporting is important to business as it is required for tax purpose,

provides important information which could be used for taking business decisions. In the similar

aspect, it provides creditors, investors and other business as idea of financial integrity and

creditworthiness of organization.

It has high engagement for disclosing financial information to stakeholders with

reference to financial position and performance over particular duration. According to

international accounting standards it provides information of financial position and changes

which are important for wide range of users to undertake economic decisions. In order to this, it

helps business to comply with multiple statues along with regulatory requirements for purpose of

filing financial statements to government agencies (Tschopp and Huefner, 2015). On basis of

listed business, there is need of filing stock exchanges which published annual and on quarter

basis, Furthermore, it facilitates statutory audit where auditors are in need of auditing financial

statements for purpose of expressing opinion with reference to Sainsbury Plc.

In the same series, it generates confidence with favourable impact of organization's cost of

capital. This will lead to retain credibility and give society with relevant and reliable information

with context to economic events and transaction without attempting move economy in one

direction rather than another. The difference between the financial reporting in different

countries is present because of the different accounting standards are been established for

different countries like in united states US GAAP is been followed while in other countries IFRS

is adopted. US GAAP is based on the rules where the transactions are been classified by the

company on the basis of the numerical cutoffs whereas IFRS reflects the principle based rules

which includes more emphasize on the qualitative guidance and less on the bright line rules.

Financial reporting plays an important role in communicating the overall health of the company's

business and facilitates a deep insight towards the culture and the structure of the management.

5

objectives

Financial reporting is referred as method for following standard practices to give world

with accurate depiction of finances of organization which comprises revenues, profit, expenses,

cashflow and capital. These key performance indicators are significant as they reflect health of

organization. Financial reporting is important to business as it is required for tax purpose,

provides important information which could be used for taking business decisions. In the similar

aspect, it provides creditors, investors and other business as idea of financial integrity and

creditworthiness of organization.

It has high engagement for disclosing financial information to stakeholders with

reference to financial position and performance over particular duration. According to

international accounting standards it provides information of financial position and changes

which are important for wide range of users to undertake economic decisions. In order to this, it

helps business to comply with multiple statues along with regulatory requirements for purpose of

filing financial statements to government agencies (Tschopp and Huefner, 2015). On basis of

listed business, there is need of filing stock exchanges which published annual and on quarter

basis, Furthermore, it facilitates statutory audit where auditors are in need of auditing financial

statements for purpose of expressing opinion with reference to Sainsbury Plc.

In the same series, it generates confidence with favourable impact of organization's cost of

capital. This will lead to retain credibility and give society with relevant and reliable information

with context to economic events and transaction without attempting move economy in one

direction rather than another. The difference between the financial reporting in different

countries is present because of the different accounting standards are been established for

different countries like in united states US GAAP is been followed while in other countries IFRS

is adopted. US GAAP is based on the rules where the transactions are been classified by the

company on the basis of the numerical cutoffs whereas IFRS reflects the principle based rules

which includes more emphasize on the qualitative guidance and less on the bright line rules.

Financial reporting plays an important role in communicating the overall health of the company's

business and facilitates a deep insight towards the culture and the structure of the management.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. International accounting standard and International financial reporting Standards and their

benefits

International accounting standard are the older set of standards which were issues by the

board of international accounting standard committee. Whereas, International financial reporting

standards are the new set of standards which are issues by International accounting standard

board. International Accounting standards were published between 1973 to 2001 whereas IFRS

were Published from 2001 onwards (Chen and Li, 2015).. The benefits of adopting IFRS

includes:

Organisation by adopting IFRS standards are able to adopt global financial reporting

which assist in understanding the global market and making comparison with the

financial statement of those companies.

Moreover, it improves the financial reporting and tax planning because it produces a

standardised and consistent set of accounting and financial reports (Flower, 2016).

IFRS helps companies in setting benchmark for their performance and then can compare

their performance with the benchmark to improve their position and performance.

The benefits of IAS are stated below

It raises comparability among firms which decreases investor risk and facilitates cross

border investment and financing.

Decrease in cost of formed consolidated financial statements especially for MNCs

6. Evaluation of financial reporting through application of theories

Financial reporting is used in order to provide understanding about financial performance

and position of the company. There are various statement which are prepared for giving financial

information to the users of financial statement. There are different theories of financial reporting

which consist of equity and legitimacy theory.

Equity theory: The residual equity theory assumes that common shareholders are the

real owners of the organisation. The equity theory provides understanding about the net

incomes of the shareholders by subtracting the liabilities from it. It includes specific

equities such as claims of creditors and equities of preferred shareholders (Bonsall IV

And et.al., 2017). The residual equity approach assists in providing better information to

the shareholders which helps them in making various investment decisions.

6

benefits

International accounting standard are the older set of standards which were issues by the

board of international accounting standard committee. Whereas, International financial reporting

standards are the new set of standards which are issues by International accounting standard

board. International Accounting standards were published between 1973 to 2001 whereas IFRS

were Published from 2001 onwards (Chen and Li, 2015).. The benefits of adopting IFRS

includes:

Organisation by adopting IFRS standards are able to adopt global financial reporting

which assist in understanding the global market and making comparison with the

financial statement of those companies.

Moreover, it improves the financial reporting and tax planning because it produces a

standardised and consistent set of accounting and financial reports (Flower, 2016).

IFRS helps companies in setting benchmark for their performance and then can compare

their performance with the benchmark to improve their position and performance.

The benefits of IAS are stated below

It raises comparability among firms which decreases investor risk and facilitates cross

border investment and financing.

Decrease in cost of formed consolidated financial statements especially for MNCs

6. Evaluation of financial reporting through application of theories

Financial reporting is used in order to provide understanding about financial performance

and position of the company. There are various statement which are prepared for giving financial

information to the users of financial statement. There are different theories of financial reporting

which consist of equity and legitimacy theory.

Equity theory: The residual equity theory assumes that common shareholders are the

real owners of the organisation. The equity theory provides understanding about the net

incomes of the shareholders by subtracting the liabilities from it. It includes specific

equities such as claims of creditors and equities of preferred shareholders (Bonsall IV

And et.al., 2017). The residual equity approach assists in providing better information to

the shareholders which helps them in making various investment decisions.

6

Legitimacy theory : This theory focus on organisation operations and their social and

environmental disclosure in the financial reporting (Davidson, Dey and Smith, 2015).

Through help of this theory, company would be able to report on its various CSR

activities which will help in providing better understanding about organisation operation's

to its users.

Application

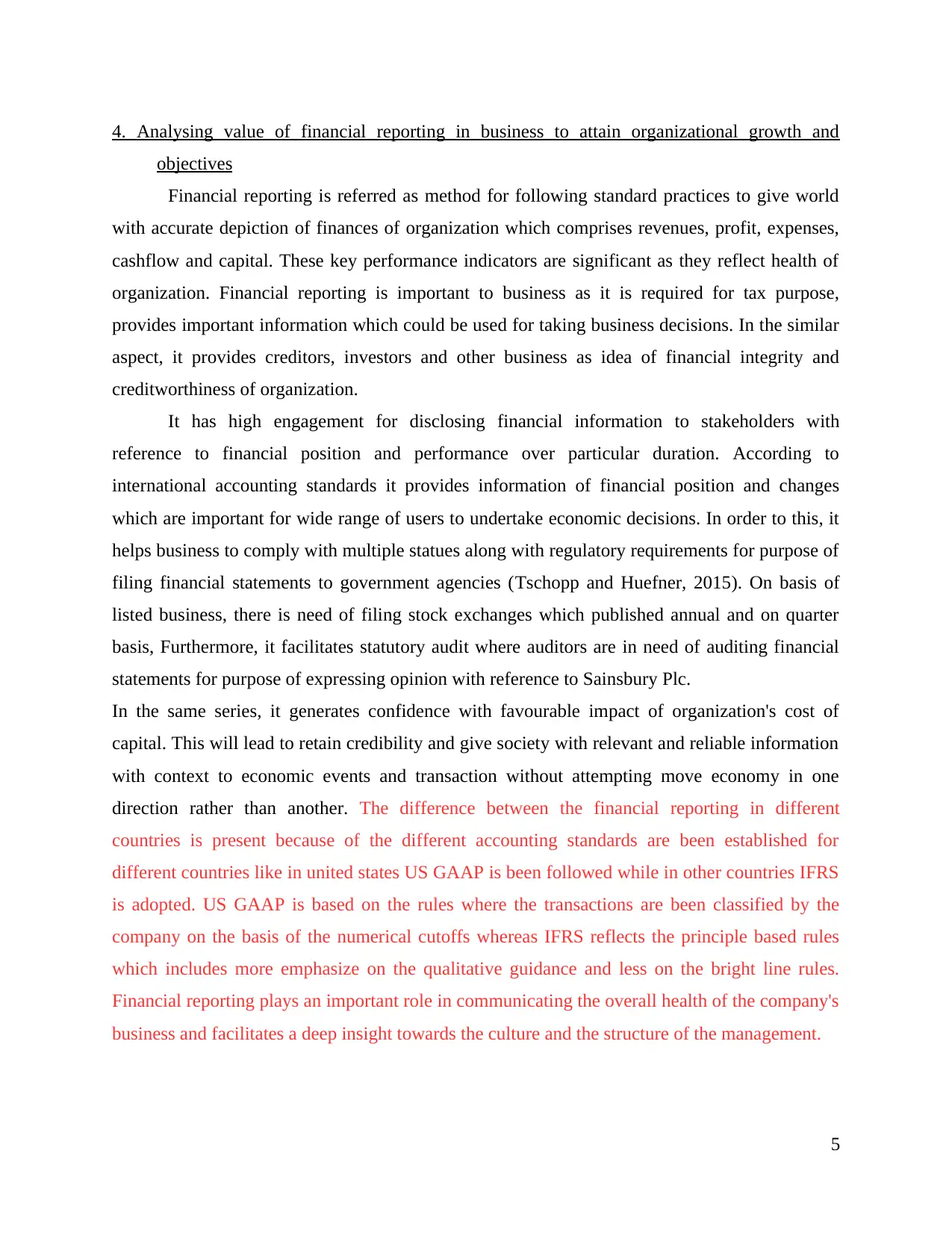

According to Equity theory, The Sainsbury provide separate column for the equity to

provide better understanding to shareholders (Annual report of Sainsbury, 2018). Sainsbury

provide separate column of equity which includes the net worth of the shareholders.

7

environmental disclosure in the financial reporting (Davidson, Dey and Smith, 2015).

Through help of this theory, company would be able to report on its various CSR

activities which will help in providing better understanding about organisation operation's

to its users.

Application

According to Equity theory, The Sainsbury provide separate column for the equity to

provide better understanding to shareholders (Annual report of Sainsbury, 2018). Sainsbury

provide separate column of equity which includes the net worth of the shareholders.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

According to Legitimacy theory, from the above it is identified that Sainsbury is applying

this theory because it maintains report for it social and corporate activities' to provide

understanding to the users regarding their operation through their corporate and sustainability

committee report (O’Riordan and Fairbrass, 2014).

7. The differences in financial reporting across world

There are different reporting standards which are being followed by different

organisation operating in different countries.. Different organisation follow different standards

such as GAAP which is generally accepted accounting principles are followed in different

countries rather than using International financial reporting standards (Abbott And et.al., 2016).

GAAP are based on rules whereas IFRS is based on principles due to this many organisations in

different countries follow the GAAP.

It consists of different set of rules for accounting. Organisation in different countries does

not rely on principles of IFRS because these principles are not generally accepted by every

organisation and there are various problems in these principles because it does not provide

treatment of various transaction which are provided by GAAP. Moreover, The organisation in

different countries adopt their own Country's standards to provide them more importance than

other standards for reporting of the financial information (Williams and Dobelman, 2017). There

are various factors which cause difference in the financial reporting by different countries due to

difference in the treatment of various transactions. Moreover, the difference in adopting the

financial standards is due to the rules and regulation of different counties which may have

influence on the business operations. By laying emphasis on principles, aggregate volume of

legislation of IFRS is remarkable lower than GAAP. It creates flexibility of interpretation by

undertaking principle judgements and extensive disclosure in financial statements for

compensating uncertainty.

8. Degrees of compliance with IFRS by different organisation around the world

International financial reporting standards must be complied by various organisation

following these standards in order to record the financial information. Organisation by

complying with IFRS principles is able to compare the financial statements through which they

will identify the information regarding the profitability and performance of different organisation

because the same principles will be followed by different organisation in all over the world

(Leuz and Wysocki, 2016). There is varying degree of compliance with IFRS sue to lack of

8

this theory because it maintains report for it social and corporate activities' to provide

understanding to the users regarding their operation through their corporate and sustainability

committee report (O’Riordan and Fairbrass, 2014).

7. The differences in financial reporting across world

There are different reporting standards which are being followed by different

organisation operating in different countries.. Different organisation follow different standards

such as GAAP which is generally accepted accounting principles are followed in different

countries rather than using International financial reporting standards (Abbott And et.al., 2016).

GAAP are based on rules whereas IFRS is based on principles due to this many organisations in

different countries follow the GAAP.

It consists of different set of rules for accounting. Organisation in different countries does

not rely on principles of IFRS because these principles are not generally accepted by every

organisation and there are various problems in these principles because it does not provide

treatment of various transaction which are provided by GAAP. Moreover, The organisation in

different countries adopt their own Country's standards to provide them more importance than

other standards for reporting of the financial information (Williams and Dobelman, 2017). There

are various factors which cause difference in the financial reporting by different countries due to

difference in the treatment of various transactions. Moreover, the difference in adopting the

financial standards is due to the rules and regulation of different counties which may have

influence on the business operations. By laying emphasis on principles, aggregate volume of

legislation of IFRS is remarkable lower than GAAP. It creates flexibility of interpretation by

undertaking principle judgements and extensive disclosure in financial statements for

compensating uncertainty.

8. Degrees of compliance with IFRS by different organisation around the world

International financial reporting standards must be complied by various organisation

following these standards in order to record the financial information. Organisation by

complying with IFRS principles is able to compare the financial statements through which they

will identify the information regarding the profitability and performance of different organisation

because the same principles will be followed by different organisation in all over the world

(Leuz and Wysocki, 2016). There is varying degree of compliance with IFRS sue to lack of

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

standardisation is adoption of IFRS principles in different counties because various organisation

adopts their own standards for reporting of financial information.

Many organisations do not comply with IFRS principle because it requires changes in

their operation or methods of reporting financial information which will increase their cost.

Moreover, compliance with IFRS requires disclosure of all the financial information which may

affect the business profitability as more tax may be required to paid by various organisation.

There is varying degree of compliance with IFRS because of there are few standards provided by

IFRS which does not provide proper guidelines for their treatment in financial reporting.

CONCLUSION

From the above study it has concluded that financial reporting which is used by

organisation to provide the financial information in the form of statements to the users to make

effective decisions. This study has provided understanding of the purpose of Financial reporting

which is to provide better understanding to the users regarding the company's performance and

position. Moreover, it has concluded about the key stakeholders of Organisation which consist of

managers, customers, government, suppliers, lenders etc. Furthermore, It has includes the

difference between the International accounting standards and International financial reporting

standard.

9

adopts their own standards for reporting of financial information.

Many organisations do not comply with IFRS principle because it requires changes in

their operation or methods of reporting financial information which will increase their cost.

Moreover, compliance with IFRS requires disclosure of all the financial information which may

affect the business profitability as more tax may be required to paid by various organisation.

There is varying degree of compliance with IFRS because of there are few standards provided by

IFRS which does not provide proper guidelines for their treatment in financial reporting.

CONCLUSION

From the above study it has concluded that financial reporting which is used by

organisation to provide the financial information in the form of statements to the users to make

effective decisions. This study has provided understanding of the purpose of Financial reporting

which is to provide better understanding to the users regarding the company's performance and

position. Moreover, it has concluded about the key stakeholders of Organisation which consist of

managers, customers, government, suppliers, lenders etc. Furthermore, It has includes the

difference between the International accounting standards and International financial reporting

standard.

9

REFERENCES

Books and Journals

Dou, Y., Wong, M. F. and Xin, B., 2019. The effect of financial reporting quality on corporate

investment efficiency: Evidence from the adoption of SFAS No. 123R. Management

Science.

Mao, C. W. and Wu, W. C., 2019. Does the government-mandated adoption of international

financial reporting standards reduce income tax revenue?. International Tax and Public

Finance, pp.1-22.

Bassemir, M. and Novotny‐Farkas, Z., 2018. IFRS adoption, reporting incentives and financial

reporting quality in private firms. Journal of Business Finance & Accounting. 45(7-8).

pp.759-796.

O’Riordan, L. and Fairbrass, J., 2014. Managing CSR stakeholder engagement: A new

conceptual framework. Journal of Business Ethics. 125(1). pp.121-145.

Stubbs, W. and Higgins, C., 2018. Stakeholders’ perspectives on the role of regulatory reform in

integrated reporting. Journal of Business Ethics. 147(3). pp.489-508.

Leuz, C. and Wysocki, P. D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research.

54(2). pp.525-622.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

Bonsall IV, S. B. And et.al., 2017. A plain English measure of financial reporting

readability. Journal of Accounting and Economics. 63(2-3). pp.329-357.

Chen, J. V. and Li, F., 2015. Discussion of “Textual analysis and international financial

reporting: Large sample evidence”. Journal of Accounting and Economics. 60(2-3).

pp.181-186.

Abbott, L. J. And et.al.,2016. Internal audit quality and financial reporting quality: The joint

importance of independence and competence. Journal of Accounting Research. 54(1).

pp.3-40.

Davidson, R., Dey, A. and Smith, A., 2015. Executives'“off-the-job” behavior, corporate culture,

and financial reporting risk. Journal of Financial Economics. 117(1). pp.5-28.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Tschopp, D. and Huefner, R. J., 2015. Comparing the evolution of CSR reporting to that of

financial reporting. Journal of Business Ethics. 127(3). pp.565-577.

Online

Annual report of Sainsbury. 2018. [Online]. Available through

<https://www.about.sainsburys.co.uk/~/media/Files/S/Sainsburys/documents/reports-and-

presentations/annual-reports/sainsburys-ar-2018-full-report.pdf>.

A Conceptual and regulatory framework. 2019. [Online]. Available through

<https://www.brainscape.com/flashcards/chapter-6-a-conceptual-and-regulatory-fra-

5514914/packs/8301421>.

10

Books and Journals

Dou, Y., Wong, M. F. and Xin, B., 2019. The effect of financial reporting quality on corporate

investment efficiency: Evidence from the adoption of SFAS No. 123R. Management

Science.

Mao, C. W. and Wu, W. C., 2019. Does the government-mandated adoption of international

financial reporting standards reduce income tax revenue?. International Tax and Public

Finance, pp.1-22.

Bassemir, M. and Novotny‐Farkas, Z., 2018. IFRS adoption, reporting incentives and financial

reporting quality in private firms. Journal of Business Finance & Accounting. 45(7-8).

pp.759-796.

O’Riordan, L. and Fairbrass, J., 2014. Managing CSR stakeholder engagement: A new

conceptual framework. Journal of Business Ethics. 125(1). pp.121-145.

Stubbs, W. and Higgins, C., 2018. Stakeholders’ perspectives on the role of regulatory reform in

integrated reporting. Journal of Business Ethics. 147(3). pp.489-508.

Leuz, C. and Wysocki, P. D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research.

54(2). pp.525-622.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

Bonsall IV, S. B. And et.al., 2017. A plain English measure of financial reporting

readability. Journal of Accounting and Economics. 63(2-3). pp.329-357.

Chen, J. V. and Li, F., 2015. Discussion of “Textual analysis and international financial

reporting: Large sample evidence”. Journal of Accounting and Economics. 60(2-3).

pp.181-186.

Abbott, L. J. And et.al.,2016. Internal audit quality and financial reporting quality: The joint

importance of independence and competence. Journal of Accounting Research. 54(1).

pp.3-40.

Davidson, R., Dey, A. and Smith, A., 2015. Executives'“off-the-job” behavior, corporate culture,

and financial reporting risk. Journal of Financial Economics. 117(1). pp.5-28.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Tschopp, D. and Huefner, R. J., 2015. Comparing the evolution of CSR reporting to that of

financial reporting. Journal of Business Ethics. 127(3). pp.565-577.

Online

Annual report of Sainsbury. 2018. [Online]. Available through

<https://www.about.sainsburys.co.uk/~/media/Files/S/Sainsburys/documents/reports-and-

presentations/annual-reports/sainsburys-ar-2018-full-report.pdf>.

A Conceptual and regulatory framework. 2019. [Online]. Available through

<https://www.brainscape.com/flashcards/chapter-6-a-conceptual-and-regulatory-fra-

5514914/packs/8301421>.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.