Financial Accounting Report: Comprehensive Analysis of Charlie's Toys

VerifiedAdded on 2023/03/17

|12

|2085

|24

Report

AI Summary

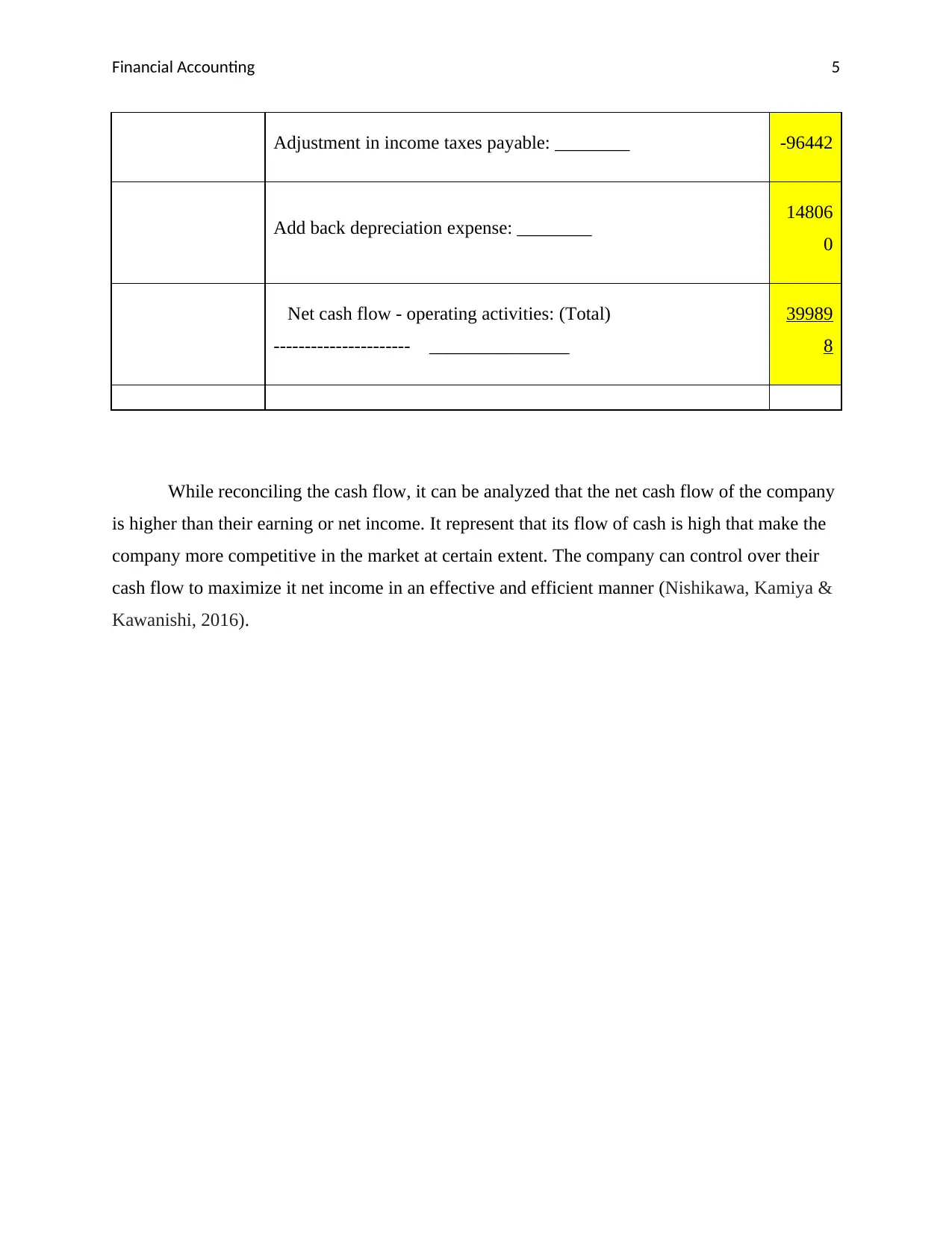

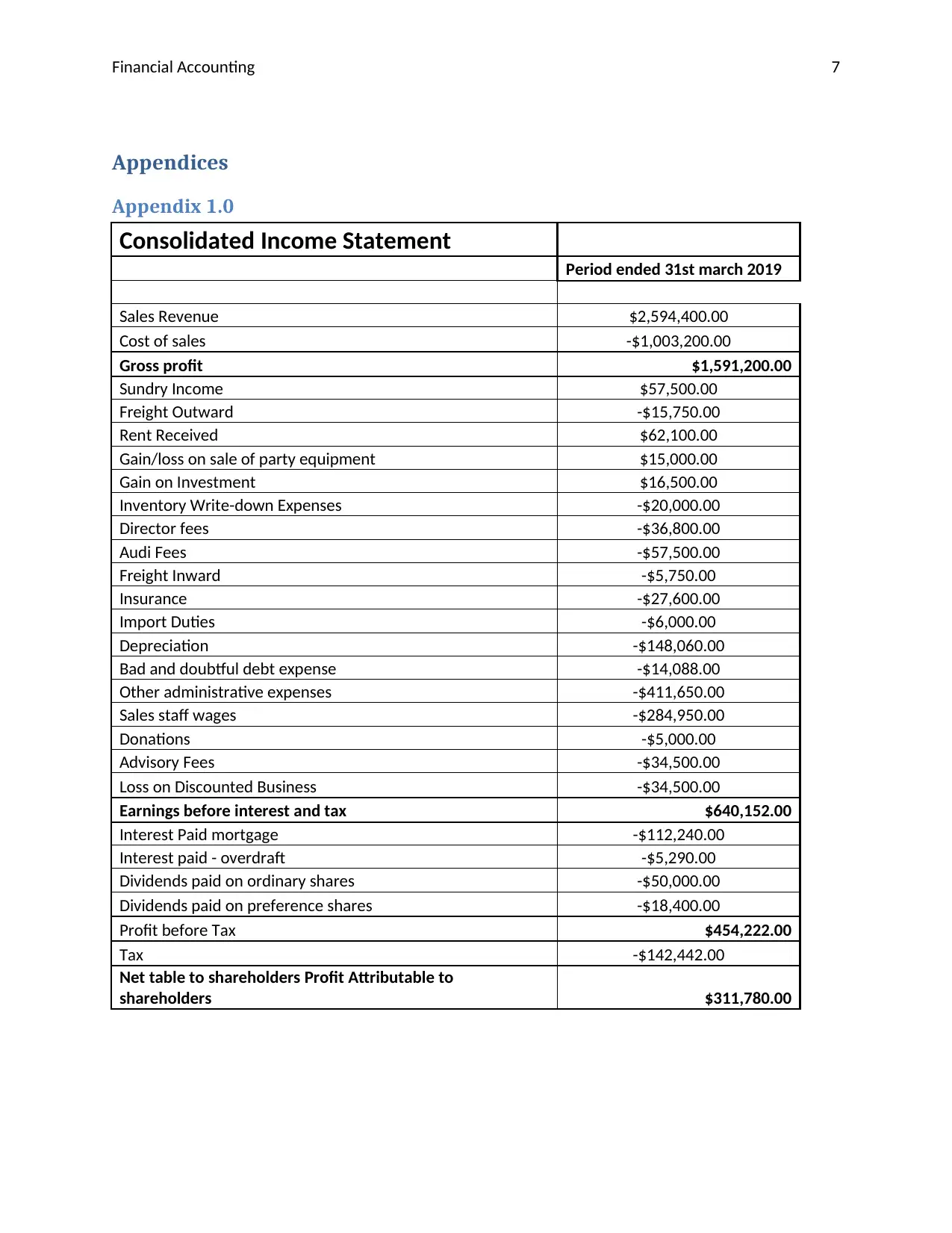

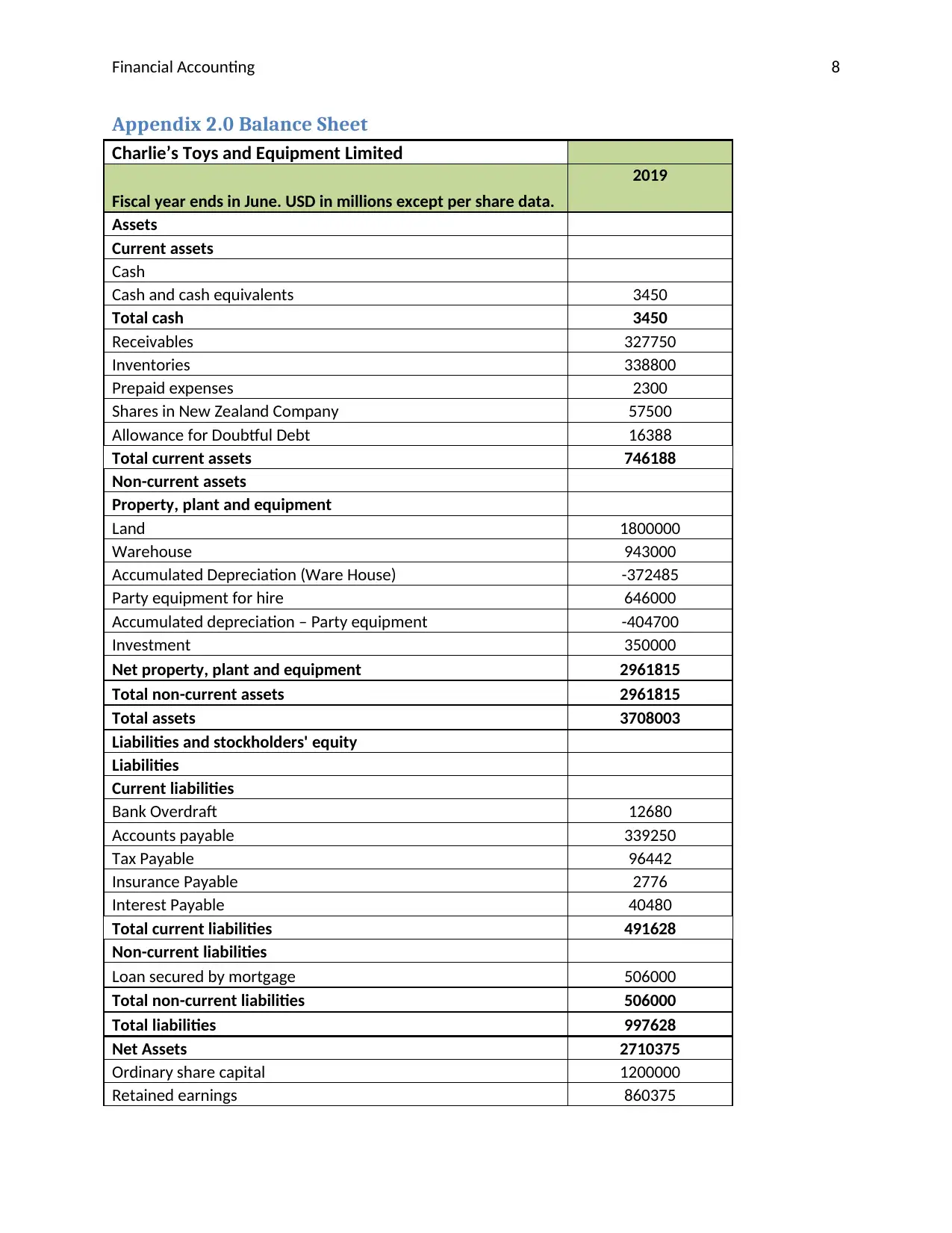

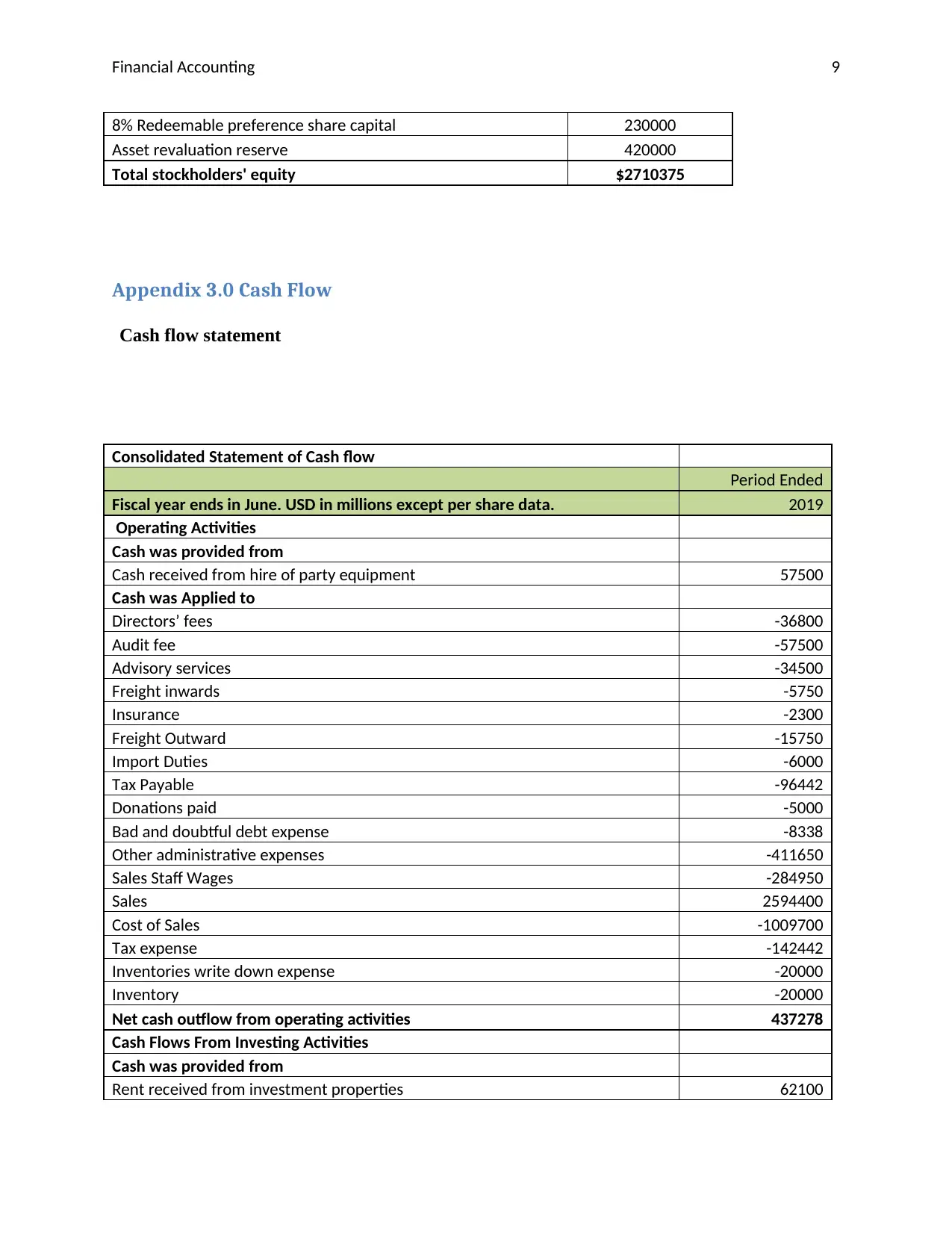

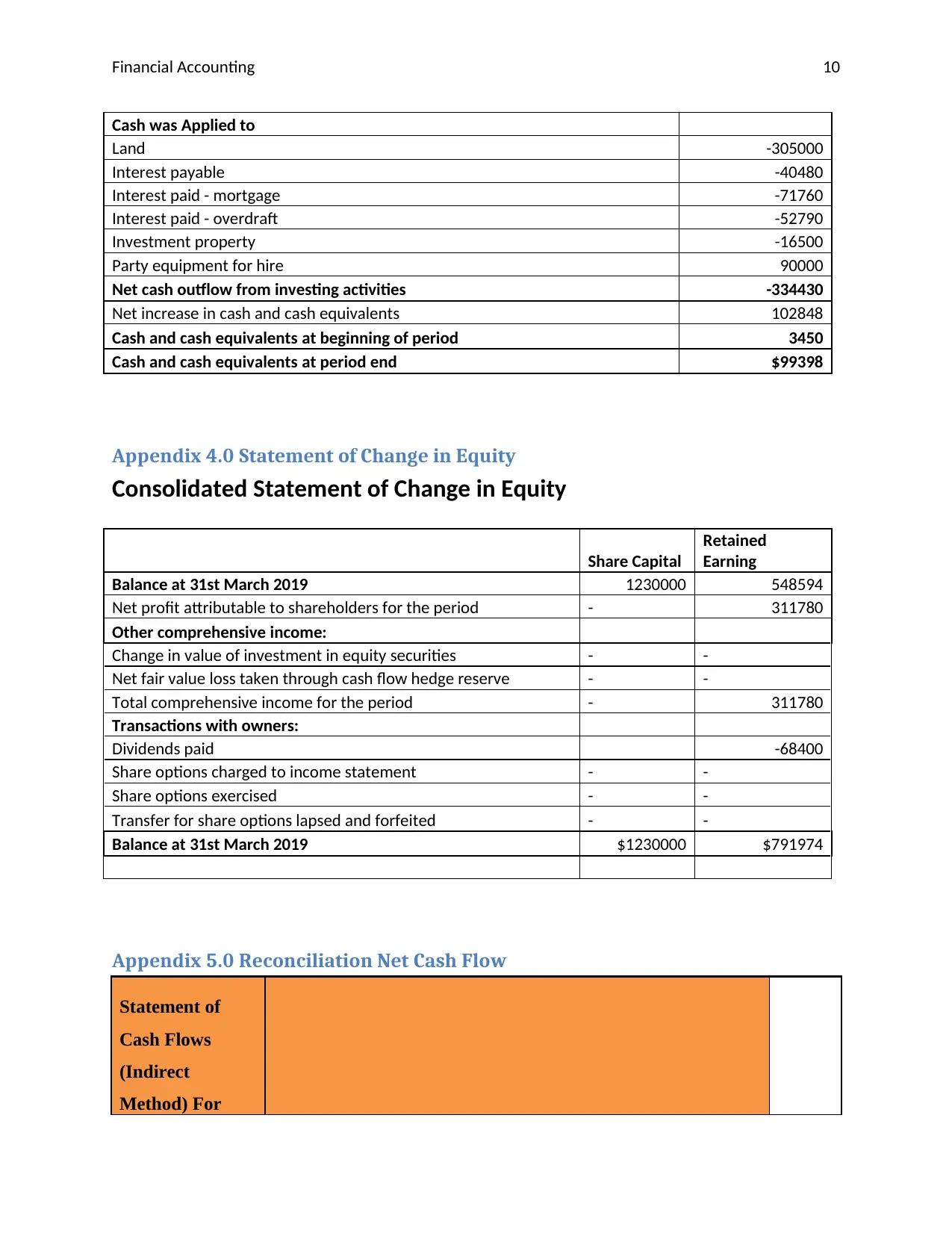

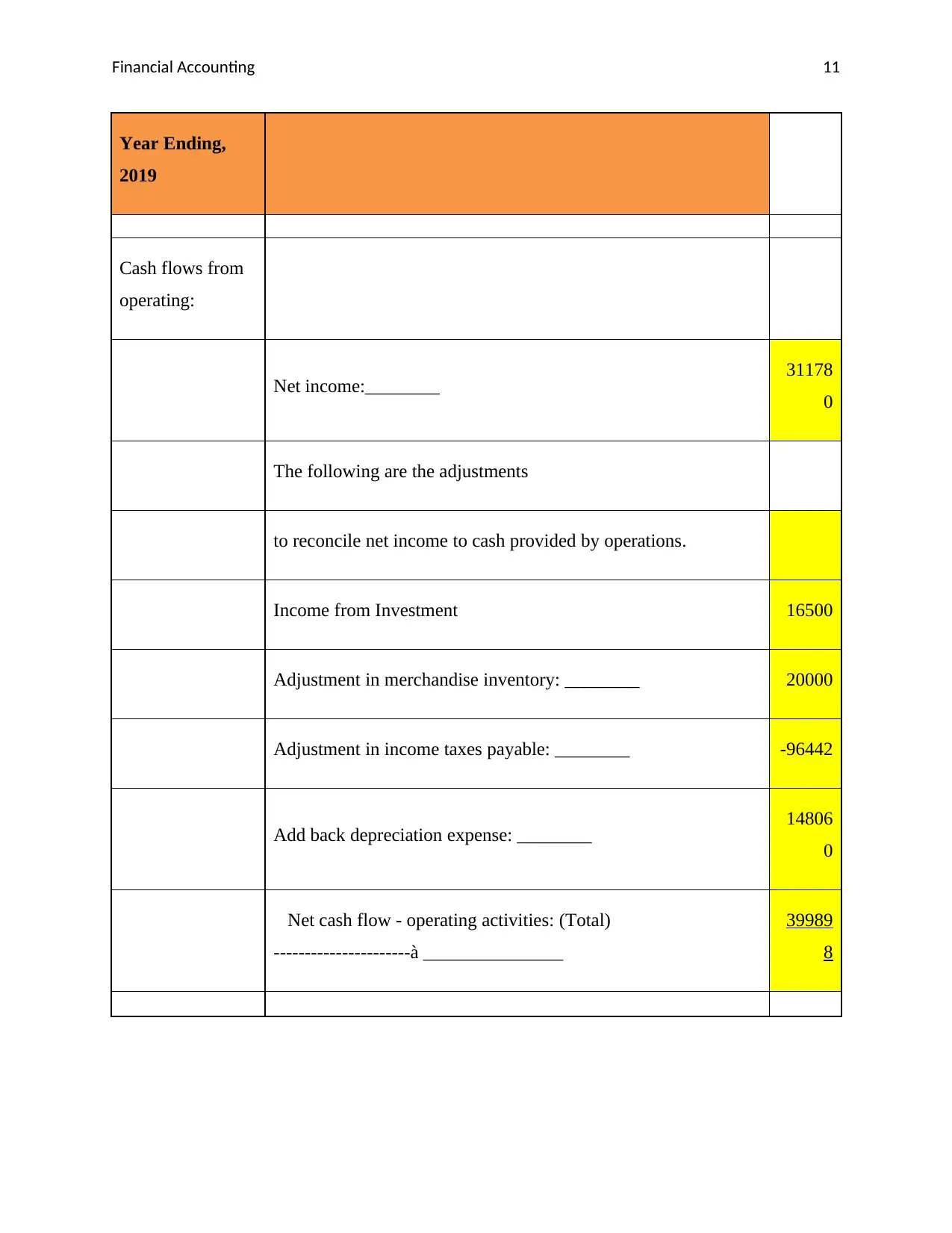

This financial accounting report provides a comprehensive analysis of Charlie's Toys and Equipment Limited. It begins with an introduction to the company, followed by a detailed examination of its significant accounting policies, including the basis of preparation, use of estimates, cash flow statement methodology, revenue recognition, and taxation. The report then delves into the operating segment disclosures, describing the types of products and services, the measurement of operating segment profit or loss, and the factors used to identify reportable segments. A key component is the reconciliation of cash flows to net profit or loss, presented using the indirect method, along with the supporting financial statements: the consolidated income statement, balance sheet, cash flow statement, and statement of changes in equity. These financial statements provide insights into the company's financial performance and position. The report concludes with a detailed analysis of the financial data, providing insights into the company's profitability, liquidity, and solvency. This report is a valuable resource for understanding the financial health and accounting practices of Charlie's Toys and Equipment Limited.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.