Financial Management Report: Adfirm Gala Dinner Financial Analysis

VerifiedAdded on 2022/11/29

|9

|2335

|167

Report

AI Summary

This financial management report analyzes the impact of cost-cutting measures on the profit performance of a food outlet within a branded hotel, specifically focusing on the Adfirm Gala dinner. The report explores cost management principles, including fixed and variable costs, direct and indirect costs, and controllable versus non-controllable costs. It then delves into variance analysis, examining sales revenue variance and direct material cost variance, providing recommendations for improvement. The strategic analysis section evaluates the financial, customer, organizational process, and employee impacts of the identified variances. The report concludes by summarizing the key findings and emphasizing the importance of financial management in achieving organizational objectives. The report offers an in-depth look into the financial strategies and their impact on the business.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

PART 1.........................................................................................................................................................3

Describe how cost-cutting measures can influence the profit performance of a food outlet within a

branded hotel and potential non-financial implications resulting from it...............................................3

PART 2.........................................................................................................................................................5

Variance Analysis & Recommendations..................................................................................................5

PART 3.........................................................................................................................................................6

Strategic Analysis.....................................................................................................................................6

CONCLUSION...............................................................................................................................................7

REFERENCES................................................................................................................................................8

INTRODUCTION...........................................................................................................................................3

PART 1.........................................................................................................................................................3

Describe how cost-cutting measures can influence the profit performance of a food outlet within a

branded hotel and potential non-financial implications resulting from it...............................................3

PART 2.........................................................................................................................................................5

Variance Analysis & Recommendations..................................................................................................5

PART 3.........................................................................................................................................................6

Strategic Analysis.....................................................................................................................................6

CONCLUSION...............................................................................................................................................7

REFERENCES................................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial management entails a variety of tasks. The financial activities are planned,

organized, directed, and controlled through these operations. Administrative duties including

purchasing and usage of company money are element of capital administration in investment

companies. Any company's monetary management is faced with a critical duty. Regulating,

coordinating, and managing financial resources are all part of it. Such actions are carried out in

order to meet the aims and goals of the firm. This report based on the hotel brand Adfirm Gala

dinner which is Australia based hotel. In this report consist of financial issue that face by the

hotel and calculate different variances that related with the issues. Along with define how these

variances impact on the strategies objective of the company in direct manner.

PART 1

Describe how cost-cutting measures can influence the profit performance of a food outlet within

a branded hotel and potential non-financial implications resulting from it

Cost Management

Cost is the monetary value of all sacrifice of resources made to achieve an objective that

associates with cost management in controlling operation costs and financial management due to

production or other cost activities (Baker, Kumar & Pandey, 2020). According to Lawal (2017),

cost reduction is considered the success of real and unchanging reduction in the unit costs of

goods manufactured without impairing their suitability for the intended use. Furthermore,

Emmanuel, Otley and Merchant highlight the “five various cost classifications scheme: fixed and

variable cost, direct and indirect costs, outlays and opportunity cost, incremental costs, sunk

costs, non-controllable and controllable costs” (p. 118). Example of fixed and variable cost

include: variable cost varies in line with sales level (cost of sales and sales commissions). In

contrast, fixed cost does not change with sales levels (insurance, rent and depreciation). The

simple approach to determining the split between variable and fixed cost can be analyzed using

the high-low method to determining cost behavior. Example of direct and indirect cost include:

direct costs are traceable to “the thing being costed (the cost object). Ingredients materials would

be a direct cost in the food and beverage department (Nizam and et.al, 2019). (Barbić, Lučić &

Financial management entails a variety of tasks. The financial activities are planned,

organized, directed, and controlled through these operations. Administrative duties including

purchasing and usage of company money are element of capital administration in investment

companies. Any company's monetary management is faced with a critical duty. Regulating,

coordinating, and managing financial resources are all part of it. Such actions are carried out in

order to meet the aims and goals of the firm. This report based on the hotel brand Adfirm Gala

dinner which is Australia based hotel. In this report consist of financial issue that face by the

hotel and calculate different variances that related with the issues. Along with define how these

variances impact on the strategies objective of the company in direct manner.

PART 1

Describe how cost-cutting measures can influence the profit performance of a food outlet within

a branded hotel and potential non-financial implications resulting from it

Cost Management

Cost is the monetary value of all sacrifice of resources made to achieve an objective that

associates with cost management in controlling operation costs and financial management due to

production or other cost activities (Baker, Kumar & Pandey, 2020). According to Lawal (2017),

cost reduction is considered the success of real and unchanging reduction in the unit costs of

goods manufactured without impairing their suitability for the intended use. Furthermore,

Emmanuel, Otley and Merchant highlight the “five various cost classifications scheme: fixed and

variable cost, direct and indirect costs, outlays and opportunity cost, incremental costs, sunk

costs, non-controllable and controllable costs” (p. 118). Example of fixed and variable cost

include: variable cost varies in line with sales level (cost of sales and sales commissions). In

contrast, fixed cost does not change with sales levels (insurance, rent and depreciation). The

simple approach to determining the split between variable and fixed cost can be analyzed using

the high-low method to determining cost behavior. Example of direct and indirect cost include:

direct costs are traceable to “the thing being costed (the cost object). Ingredients materials would

be a direct cost in the food and beverage department (Nizam and et.al, 2019). (Barbić, Lučić &

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Chen, 2019). Indirect costs (overheads): are not traceable to the cost object; general advertising

for the restaurant menu fee would be an indirect cost allocation of the department based on their

relative sales levels. Example of incremental and sunk costs: incremental costs are changed when

different decisions are made whereas sunk costs are already incurred and are now irreversible

(deprecation). Example of controllable and non-controllable cost: in responsibility accounting,

managers should only be held accountable for costs that they can control (labour costs). If high

importance is attached to accounting, segment-controlled costs from non-controllable costs (rent

and insurance) should be made. Example of outlay and opportunity cost: outlay cost is “real”,

which involves a disbursement of funds (expenditures). An opportunity cost is an opportunity

forgone (annual revenue) (Kim, Kim, Pantzalis & Park, 2019). This ultimately makes it easier for

management and qualitative analysis of management decisions. The financial data provided by

the accounting system frequently plays a powerful information role as it carries an air of

‘objectivity.” This tendency should not be allowed to distract from the importance of qualitative

factors in decision making.

Non-Financial Implications

Despite the fact that nine out of ten businesses are planning, implementing, or finishing cost-

cutting activities, only around a third of them consider themselves to be cost-effective. Political

situation, a fragmented strategy, and organizational reluctance to change are seen by most CEOs

as major roadblocks to effective cost saving. Nevertheless, research reveals that many cost-

cutting strategies focus on either removing expenditure items from a cost pool (such as

discontinuing executing reduced tasks) or lowering service utilization and related expenses (such

as removing duplications and redundancies). In most situations, these haphazard, one-

dimensional actions fall short of expectations and fail to deliver the expected results.

Furthermore, the costs involved of cost cutbacks are having an increasingly negative influence

on organizations (Koochel and et.al, 2020). By "hidden costs," we indicate the frequently

unanticipated, unfavourable repercussions of cost-cutting measures. Although hidden costs

normally refer to charges that are not included in the original cost of a type of hardware or

technology (such as maintenance, support, or upgrades), in this case Adfirm Gala Dinner is

concerned about the effects of cost reductions on workplace culture, involvement, and efficiency.

for the restaurant menu fee would be an indirect cost allocation of the department based on their

relative sales levels. Example of incremental and sunk costs: incremental costs are changed when

different decisions are made whereas sunk costs are already incurred and are now irreversible

(deprecation). Example of controllable and non-controllable cost: in responsibility accounting,

managers should only be held accountable for costs that they can control (labour costs). If high

importance is attached to accounting, segment-controlled costs from non-controllable costs (rent

and insurance) should be made. Example of outlay and opportunity cost: outlay cost is “real”,

which involves a disbursement of funds (expenditures). An opportunity cost is an opportunity

forgone (annual revenue) (Kim, Kim, Pantzalis & Park, 2019). This ultimately makes it easier for

management and qualitative analysis of management decisions. The financial data provided by

the accounting system frequently plays a powerful information role as it carries an air of

‘objectivity.” This tendency should not be allowed to distract from the importance of qualitative

factors in decision making.

Non-Financial Implications

Despite the fact that nine out of ten businesses are planning, implementing, or finishing cost-

cutting activities, only around a third of them consider themselves to be cost-effective. Political

situation, a fragmented strategy, and organizational reluctance to change are seen by most CEOs

as major roadblocks to effective cost saving. Nevertheless, research reveals that many cost-

cutting strategies focus on either removing expenditure items from a cost pool (such as

discontinuing executing reduced tasks) or lowering service utilization and related expenses (such

as removing duplications and redundancies). In most situations, these haphazard, one-

dimensional actions fall short of expectations and fail to deliver the expected results.

Furthermore, the costs involved of cost cutbacks are having an increasingly negative influence

on organizations (Koochel and et.al, 2020). By "hidden costs," we indicate the frequently

unanticipated, unfavourable repercussions of cost-cutting measures. Although hidden costs

normally refer to charges that are not included in the original cost of a type of hardware or

technology (such as maintenance, support, or upgrades), in this case Adfirm Gala Dinner is

concerned about the effects of cost reductions on workplace culture, involvement, and efficiency.

PART 2

Variance Analysis & Recommendations

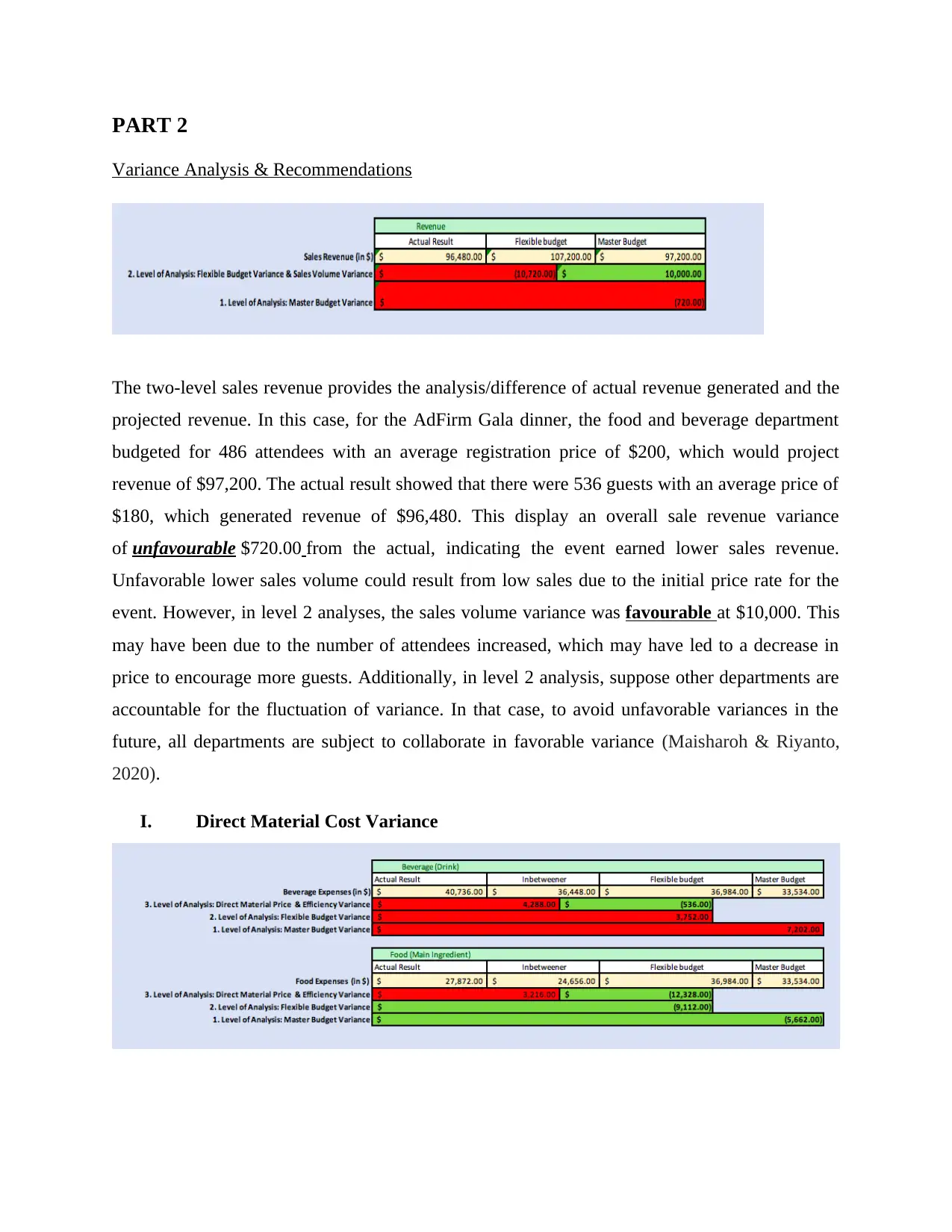

The two-level sales revenue provides the analysis/difference of actual revenue generated and the

projected revenue. In this case, for the AdFirm Gala dinner, the food and beverage department

budgeted for 486 attendees with an average registration price of $200, which would project

revenue of $97,200. The actual result showed that there were 536 guests with an average price of

$180, which generated revenue of $96,480. This display an overall sale revenue variance

of unfavourable $720.00 from the actual, indicating the event earned lower sales revenue.

Unfavorable lower sales volume could result from low sales due to the initial price rate for the

event. However, in level 2 analyses, the sales volume variance was favourable at $10,000. This

may have been due to the number of attendees increased, which may have led to a decrease in

price to encourage more guests. Additionally, in level 2 analysis, suppose other departments are

accountable for the fluctuation of variance. In that case, to avoid unfavorable variances in the

future, all departments are subject to collaborate in favorable variance (Maisharoh & Riyanto,

2020).

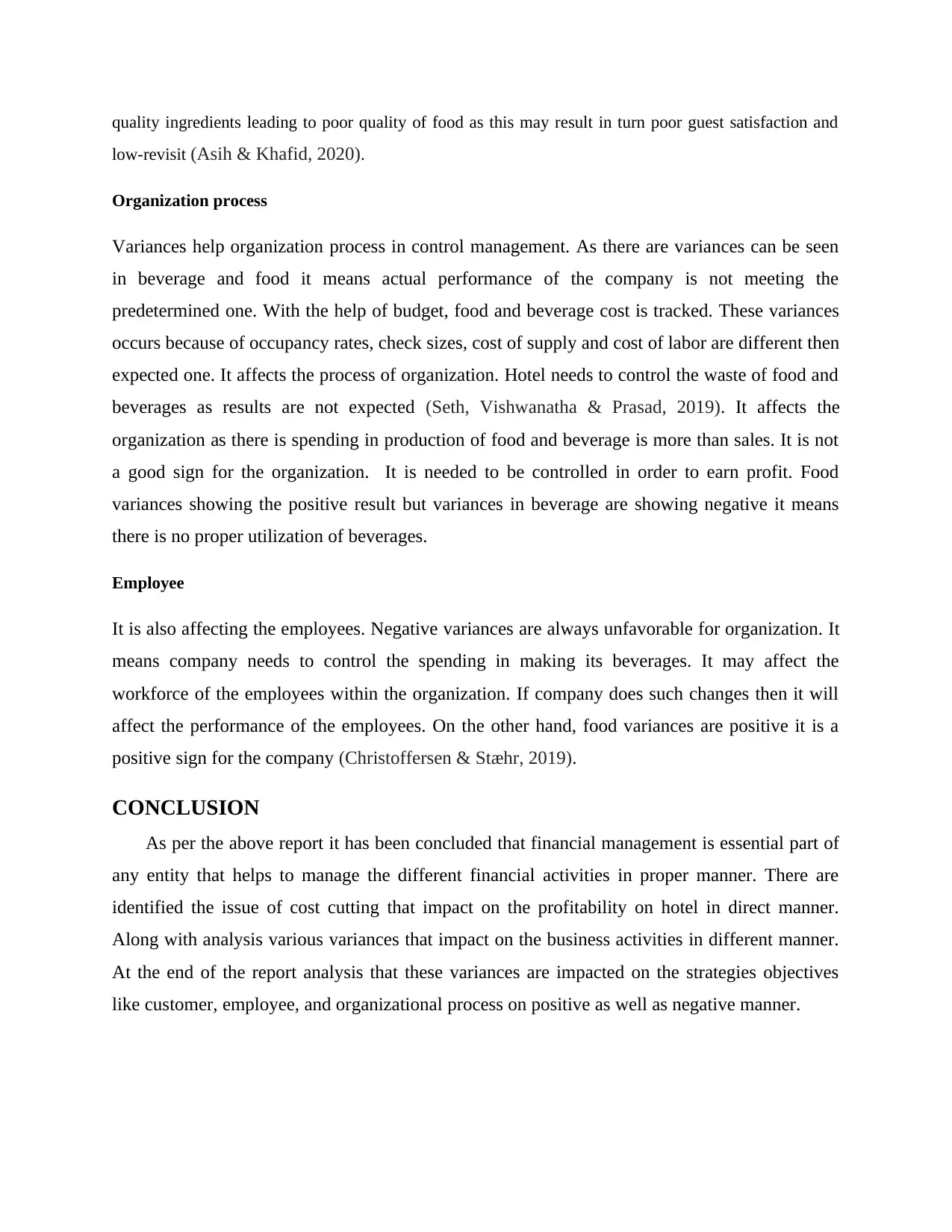

I. Direct Material Cost Variance

Variance Analysis & Recommendations

The two-level sales revenue provides the analysis/difference of actual revenue generated and the

projected revenue. In this case, for the AdFirm Gala dinner, the food and beverage department

budgeted for 486 attendees with an average registration price of $200, which would project

revenue of $97,200. The actual result showed that there were 536 guests with an average price of

$180, which generated revenue of $96,480. This display an overall sale revenue variance

of unfavourable $720.00 from the actual, indicating the event earned lower sales revenue.

Unfavorable lower sales volume could result from low sales due to the initial price rate for the

event. However, in level 2 analyses, the sales volume variance was favourable at $10,000. This

may have been due to the number of attendees increased, which may have led to a decrease in

price to encourage more guests. Additionally, in level 2 analysis, suppose other departments are

accountable for the fluctuation of variance. In that case, to avoid unfavorable variances in the

future, all departments are subject to collaborate in favorable variance (Maisharoh & Riyanto,

2020).

I. Direct Material Cost Variance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The direct material variance is the analysis/difference of the actual cost of production and the

projected cost of production. In this case, for the AdFirm Gala dinner, the food and beverage

department budgeted for 486 meals with an average ingredient cost of $230, which would project

a cost of $33,534. The actual result showed that they were 536 meals served with an actual cost

of $260. This display direct materials price variance for the beverage of $4,288 (which is the

Actual-In betweener) was unfavorable because the actual was more than the budgeted in the in

betweener. However, level 2 analysis suggests that the efficiency variances was

$536favourable, because the in betweener was below the budgeted in the flexible budget, which

could have also boosted the profit by the same amount. Level 3 food analysis suggests that the

direct material price variance for food is unfavorable $3,216. Unfavorable price variance

could’ve results from higher expenditure of ingredient cost from suppliers, higher input price and

last minutes of purchase to provide enough meals for all guest as actual guests numbers were

above the budgeted. Moreover, to avoid future unfavorable variances, `making the head chef

accountable for the quality of food outputs can be achieved. Level 3 also display a result with a

$12,328 favorable efficiency variance. This can result from under-porting the servings, which

may also lead to other key factors such as customer satisfaction.

PART 3

Strategic Analysis

Financial

The food and beverage manager and staff must prefer using meat in a controlled way and not to waste or

increase the expenditure. As seen in task 2, favourable efficiency variance has occurred mainly due to the

under-portioning of meals, directly affecting the guest. This may also have an impact on the direct

material price. Together, both variances, in turn, an unfavourable effect on the gross profit (Mayer,

2021).

Customer

The restaurant management has charged lower registration fees to what was initially budgeted and has

encouraged guests to attend the AdFirm Gala dinner to create brand awareness and loyalty among its

valued customers. This has also engaged guest in a higher number of meals served. Though the number of

attendees increased, this caused the restaurant management to experience an unfavourable price variance

in direct material cost. Hence, it would affect the guest if management decided to use cheaper and low-

projected cost of production. In this case, for the AdFirm Gala dinner, the food and beverage

department budgeted for 486 meals with an average ingredient cost of $230, which would project

a cost of $33,534. The actual result showed that they were 536 meals served with an actual cost

of $260. This display direct materials price variance for the beverage of $4,288 (which is the

Actual-In betweener) was unfavorable because the actual was more than the budgeted in the in

betweener. However, level 2 analysis suggests that the efficiency variances was

$536favourable, because the in betweener was below the budgeted in the flexible budget, which

could have also boosted the profit by the same amount. Level 3 food analysis suggests that the

direct material price variance for food is unfavorable $3,216. Unfavorable price variance

could’ve results from higher expenditure of ingredient cost from suppliers, higher input price and

last minutes of purchase to provide enough meals for all guest as actual guests numbers were

above the budgeted. Moreover, to avoid future unfavorable variances, `making the head chef

accountable for the quality of food outputs can be achieved. Level 3 also display a result with a

$12,328 favorable efficiency variance. This can result from under-porting the servings, which

may also lead to other key factors such as customer satisfaction.

PART 3

Strategic Analysis

Financial

The food and beverage manager and staff must prefer using meat in a controlled way and not to waste or

increase the expenditure. As seen in task 2, favourable efficiency variance has occurred mainly due to the

under-portioning of meals, directly affecting the guest. This may also have an impact on the direct

material price. Together, both variances, in turn, an unfavourable effect on the gross profit (Mayer,

2021).

Customer

The restaurant management has charged lower registration fees to what was initially budgeted and has

encouraged guests to attend the AdFirm Gala dinner to create brand awareness and loyalty among its

valued customers. This has also engaged guest in a higher number of meals served. Though the number of

attendees increased, this caused the restaurant management to experience an unfavourable price variance

in direct material cost. Hence, it would affect the guest if management decided to use cheaper and low-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

quality ingredients leading to poor quality of food as this may result in turn poor guest satisfaction and

low-revisit (Asih & Khafid, 2020).

Organization process

Variances help organization process in control management. As there are variances can be seen

in beverage and food it means actual performance of the company is not meeting the

predetermined one. With the help of budget, food and beverage cost is tracked. These variances

occurs because of occupancy rates, check sizes, cost of supply and cost of labor are different then

expected one. It affects the process of organization. Hotel needs to control the waste of food and

beverages as results are not expected (Seth, Vishwanatha & Prasad, 2019). It affects the

organization as there is spending in production of food and beverage is more than sales. It is not

a good sign for the organization. It is needed to be controlled in order to earn profit. Food

variances showing the positive result but variances in beverage are showing negative it means

there is no proper utilization of beverages.

Employee

It is also affecting the employees. Negative variances are always unfavorable for organization. It

means company needs to control the spending in making its beverages. It may affect the

workforce of the employees within the organization. If company does such changes then it will

affect the performance of the employees. On the other hand, food variances are positive it is a

positive sign for the company (Christoffersen & Stæhr, 2019).

CONCLUSION

As per the above report it has been concluded that financial management is essential part of

any entity that helps to manage the different financial activities in proper manner. There are

identified the issue of cost cutting that impact on the profitability on hotel in direct manner.

Along with analysis various variances that impact on the business activities in different manner.

At the end of the report analysis that these variances are impacted on the strategies objectives

like customer, employee, and organizational process on positive as well as negative manner.

low-revisit (Asih & Khafid, 2020).

Organization process

Variances help organization process in control management. As there are variances can be seen

in beverage and food it means actual performance of the company is not meeting the

predetermined one. With the help of budget, food and beverage cost is tracked. These variances

occurs because of occupancy rates, check sizes, cost of supply and cost of labor are different then

expected one. It affects the process of organization. Hotel needs to control the waste of food and

beverages as results are not expected (Seth, Vishwanatha & Prasad, 2019). It affects the

organization as there is spending in production of food and beverage is more than sales. It is not

a good sign for the organization. It is needed to be controlled in order to earn profit. Food

variances showing the positive result but variances in beverage are showing negative it means

there is no proper utilization of beverages.

Employee

It is also affecting the employees. Negative variances are always unfavorable for organization. It

means company needs to control the spending in making its beverages. It may affect the

workforce of the employees within the organization. If company does such changes then it will

affect the performance of the employees. On the other hand, food variances are positive it is a

positive sign for the company (Christoffersen & Stæhr, 2019).

CONCLUSION

As per the above report it has been concluded that financial management is essential part of

any entity that helps to manage the different financial activities in proper manner. There are

identified the issue of cost cutting that impact on the profitability on hotel in direct manner.

Along with analysis various variances that impact on the business activities in different manner.

At the end of the report analysis that these variances are impacted on the strategies objectives

like customer, employee, and organizational process on positive as well as negative manner.

REFERENCES

Books and Journal

Baker, H. K., Kumar, S., & Pandey, N. (2020). A bibliometric analysis of European Financial

Managementʼs first 25 years. European Financial Management. 26(5). 1224-1260.

Nizam, E. and et.al, (2019). The impact of social and environmental sustainability on financial

performance: A global analysis of the banking sector. Journal of Multinational Financial

Management. 49. 35-53.

Kim, C., Kim, I., Pantzalis, C., & Park, J. C. (2019). Policy uncertainty and the dual role of

corporate political strategies. Financial Management. 48(2). 473-504.

Koochel, E. E. and et.al, (2020). Financial transparency scale: Its development and potential

uses. Journal of Financial Counseling and Planning.

Maisharoh, T., & Riyanto, S. (2020). Financial Statements Analysis in Measuring Financial

Performance of the PT. Mayora Indah Tbk, Period 2014-2018. Journal of Contemporary

Information Technology, Management, and Accounting. 1(2). 63-71.

Mayer, E. J. (2021). Advertising, investor attention, and stock prices: Evidence from a natural

experiment. Financial Management. 50(1). 281-314.

Asih, S. W., & Khafid, M. (2020). Pengaruh Financial Knowledge, Financial Attitude dan

Income Terhadap Personal Financial Management behavior Melalui Locus of Control

Sebagai variabel Intervening. Economic Education Analysis Journal. 9(3). 748-767.

Seth, R., Vishwanatha, S. R., & Prasad, D. (2019). Allocation to anchor investors, underpricing,

and the after‐market performance of IPOs. Financial Management. 48(1). 159-186.

Christoffersen, J., & Stæhr, S. (2019). Individual risk tolerance and herding behaviors in

financial forecasts. European Financial Management. 25(5). 1348-1377.

Barbić, D., Lučić, A., & Chen, J. M. (2019). Measuring responsible financial consumption

behaviour. International journal of consumer studies. 43(1). 102-112.

Books and Journal

Baker, H. K., Kumar, S., & Pandey, N. (2020). A bibliometric analysis of European Financial

Managementʼs first 25 years. European Financial Management. 26(5). 1224-1260.

Nizam, E. and et.al, (2019). The impact of social and environmental sustainability on financial

performance: A global analysis of the banking sector. Journal of Multinational Financial

Management. 49. 35-53.

Kim, C., Kim, I., Pantzalis, C., & Park, J. C. (2019). Policy uncertainty and the dual role of

corporate political strategies. Financial Management. 48(2). 473-504.

Koochel, E. E. and et.al, (2020). Financial transparency scale: Its development and potential

uses. Journal of Financial Counseling and Planning.

Maisharoh, T., & Riyanto, S. (2020). Financial Statements Analysis in Measuring Financial

Performance of the PT. Mayora Indah Tbk, Period 2014-2018. Journal of Contemporary

Information Technology, Management, and Accounting. 1(2). 63-71.

Mayer, E. J. (2021). Advertising, investor attention, and stock prices: Evidence from a natural

experiment. Financial Management. 50(1). 281-314.

Asih, S. W., & Khafid, M. (2020). Pengaruh Financial Knowledge, Financial Attitude dan

Income Terhadap Personal Financial Management behavior Melalui Locus of Control

Sebagai variabel Intervening. Economic Education Analysis Journal. 9(3). 748-767.

Seth, R., Vishwanatha, S. R., & Prasad, D. (2019). Allocation to anchor investors, underpricing,

and the after‐market performance of IPOs. Financial Management. 48(1). 159-186.

Christoffersen, J., & Stæhr, S. (2019). Individual risk tolerance and herding behaviors in

financial forecasts. European Financial Management. 25(5). 1348-1377.

Barbić, D., Lučić, A., & Chen, J. M. (2019). Measuring responsible financial consumption

behaviour. International journal of consumer studies. 43(1). 102-112.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.