Comprehensive Report: Funding Sources, Budgeting and Ratio Analysis

VerifiedAdded on 2021/04/21

|21

|4768

|51

Report

AI Summary

This report delves into various funding sources essential for businesses, categorizing them into short-term, medium-term, and long-term options, tailored for sole traders, partnerships, and both private and public limited companies. It includes a comprehensive financial analysis, utilizing a trial balance to illustrate the preparation and purpose of final accounts like income statements, balance sheets, and cash flow statements. The report also examines the role of budgetary control, types of financial budgets, and variance analysis to identify discrepancies between budgeted and actual figures. Furthermore, it presents a detailed ratio analysis, focusing on profitability ratios such as return on capital employed, net profit margin, and gross profit margin to evaluate the company's financial performance. Recommendations are provided based on the analysis, emphasizing the importance of effective budgetary techniques and strategic financial management.

Running Head: Finance & Funding in Travel & Tourism Sector

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance & Funding in Travel & Tourism Sector

2

Contents

Task 1.1: Short term, medium term and long term funding sources................................3

Task 1.2: Income generation opportunity.........................................................................5

Task 2: Refer to PPT file..................................................................................................6

Task 3: Budgetary report..................................................................................................6

Task 4: Ratio analysis:....................................................................................................10

Task 5: Breakeven point.................................................................................................14

References.......................................................................................................................18

2

Contents

Task 1.1: Short term, medium term and long term funding sources................................3

Task 1.2: Income generation opportunity.........................................................................5

Task 2: Refer to PPT file..................................................................................................6

Task 3: Budgetary report..................................................................................................6

Task 4: Ratio analysis:....................................................................................................10

Task 5: Breakeven point.................................................................................................14

References.......................................................................................................................18

Finance & Funding in Travel & Tourism Sector

3

Introduction:

The report explains about the various types of sources which are required by the

different business entities to manage and run the business as well as few new opportunities

which could be adopted by the hospitality industries to enhance the revenues.

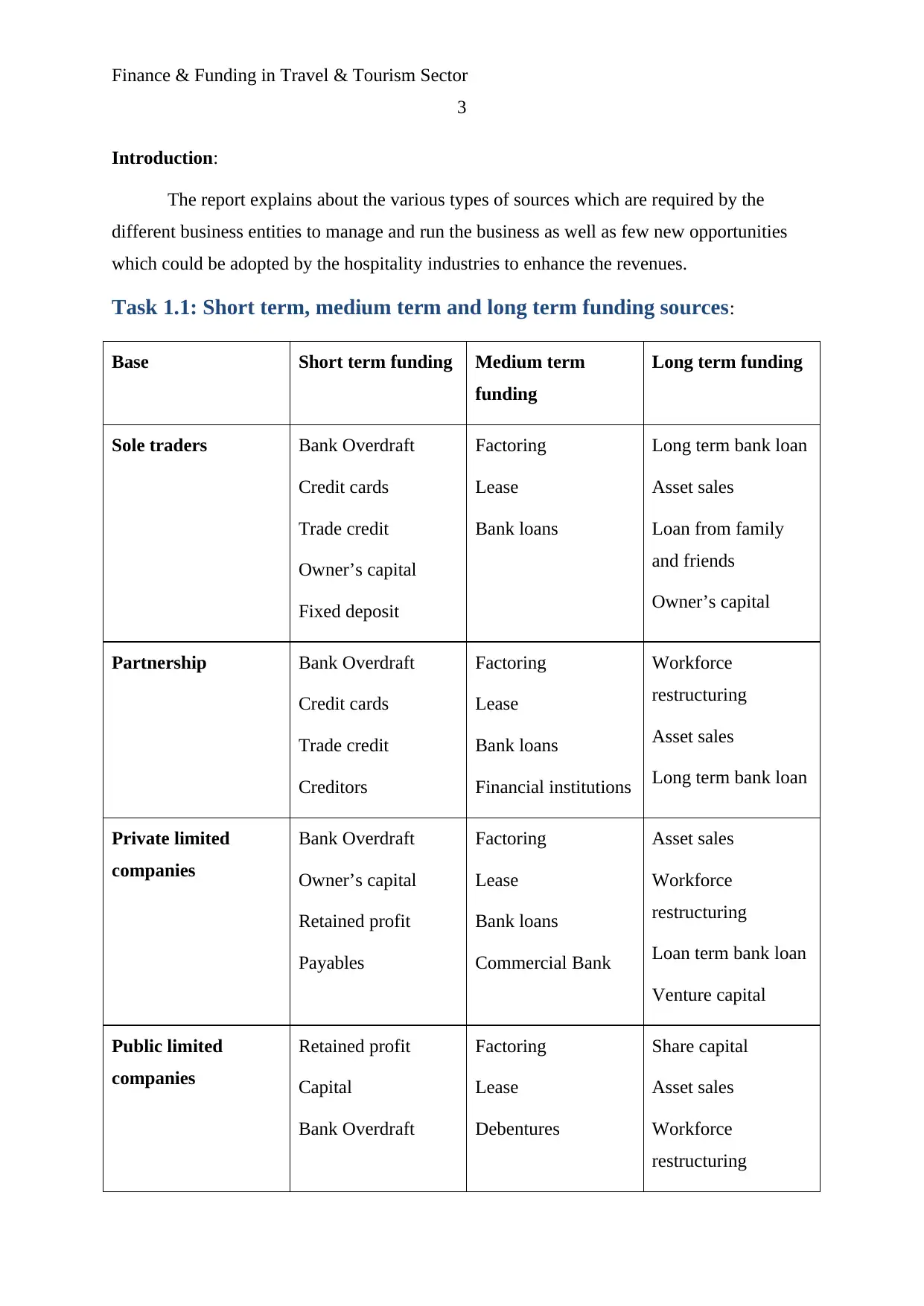

Task 1.1: Short term, medium term and long term funding sources:

Base Short term funding Medium term

funding

Long term funding

Sole traders Bank Overdraft

Credit cards

Trade credit

Owner’s capital

Fixed deposit

Factoring

Lease

Bank loans

Long term bank loan

Asset sales

Loan from family

and friends

Owner’s capital

Partnership Bank Overdraft

Credit cards

Trade credit

Creditors

Factoring

Lease

Bank loans

Financial institutions

Workforce

restructuring

Asset sales

Long term bank loan

Private limited

companies

Bank Overdraft

Owner’s capital

Retained profit

Payables

Factoring

Lease

Bank loans

Commercial Bank

Asset sales

Workforce

restructuring

Loan term bank loan

Venture capital

Public limited

companies

Retained profit

Capital

Bank Overdraft

Factoring

Lease

Debentures

Share capital

Asset sales

Workforce

restructuring

3

Introduction:

The report explains about the various types of sources which are required by the

different business entities to manage and run the business as well as few new opportunities

which could be adopted by the hospitality industries to enhance the revenues.

Task 1.1: Short term, medium term and long term funding sources:

Base Short term funding Medium term

funding

Long term funding

Sole traders Bank Overdraft

Credit cards

Trade credit

Owner’s capital

Fixed deposit

Factoring

Lease

Bank loans

Long term bank loan

Asset sales

Loan from family

and friends

Owner’s capital

Partnership Bank Overdraft

Credit cards

Trade credit

Creditors

Factoring

Lease

Bank loans

Financial institutions

Workforce

restructuring

Asset sales

Long term bank loan

Private limited

companies

Bank Overdraft

Owner’s capital

Retained profit

Payables

Factoring

Lease

Bank loans

Commercial Bank

Asset sales

Workforce

restructuring

Loan term bank loan

Venture capital

Public limited

companies

Retained profit

Capital

Bank Overdraft

Factoring

Lease

Debentures

Share capital

Asset sales

Workforce

restructuring

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance & Funding in Travel & Tourism Sector

4

Payables

Bill discounting

Bank loans

Preference capital.

Venture capital

(Ward, 2012)

Sole traders:

Sole trader is a person who executes and manages a business. A sole trader is also

known as sole proprietorship. It is a simple business structure which is run by an individual.

The entire business is owned by the single individual. Sole trader is legally responsible for all

the factors of the business and they are also required to manage and maintain the entire

finance of the business at their own. Short term finance of the company could be managed

through Bank Overdraft which could be raised by the trader through withdrawing more

amount than the balance of bank account, Credit cards, Trade credit, Owner’s capital and

fixed deposit (Ross et al, 2008). Further, medium term funds could be generated by the

company through Factoring, Lease, Bank loans. And lastly, the long term loans could be

financed by the sole traders through Long term bank loan, Asset sales, Loan from family and

friends and Owner’s capital.

Partnership:

Partnership is an arrangement in which 2 or more parties come together and executes

and manages a business. Partners share the liabilities and profits equally or according to their

contract. It is a simple business structure which is run by the 2 or more people with a

partnership agreement. Partners are legally responsible for all the factors of the business and

they are also required to manage and maintain the entire finance of the business at their own.

Short term finance of the partnership could be managed through factoring, Lease and Bank

Overdraft which could be raised by the trader through withdrawing more amount than the

balance of bank account. Further, medium term funds could be generated by the partnership

firm through Factoring, Lease, Bank loans and financial institutes (Weaver, Weston and

Weaver, 2001). And lastly, the long term loans could be financed by the partnership firm

through Workforce restructuring, Asset sales, and partner’s capital.

Private limited companies:

Private limited company is a small business entity which is privately held. In private

limited companies, the owner of the company is only responsible for the shares which are

4

Payables

Bill discounting

Bank loans

Preference capital.

Venture capital

(Ward, 2012)

Sole traders:

Sole trader is a person who executes and manages a business. A sole trader is also

known as sole proprietorship. It is a simple business structure which is run by an individual.

The entire business is owned by the single individual. Sole trader is legally responsible for all

the factors of the business and they are also required to manage and maintain the entire

finance of the business at their own. Short term finance of the company could be managed

through Bank Overdraft which could be raised by the trader through withdrawing more

amount than the balance of bank account, Credit cards, Trade credit, Owner’s capital and

fixed deposit (Ross et al, 2008). Further, medium term funds could be generated by the

company through Factoring, Lease, Bank loans. And lastly, the long term loans could be

financed by the sole traders through Long term bank loan, Asset sales, Loan from family and

friends and Owner’s capital.

Partnership:

Partnership is an arrangement in which 2 or more parties come together and executes

and manages a business. Partners share the liabilities and profits equally or according to their

contract. It is a simple business structure which is run by the 2 or more people with a

partnership agreement. Partners are legally responsible for all the factors of the business and

they are also required to manage and maintain the entire finance of the business at their own.

Short term finance of the partnership could be managed through factoring, Lease and Bank

Overdraft which could be raised by the trader through withdrawing more amount than the

balance of bank account. Further, medium term funds could be generated by the partnership

firm through Factoring, Lease, Bank loans and financial institutes (Weaver, Weston and

Weaver, 2001). And lastly, the long term loans could be financed by the partnership firm

through Workforce restructuring, Asset sales, and partner’s capital.

Private limited companies:

Private limited company is a small business entity which is privately held. In private

limited companies, the owner of the company is only responsible for the shares which are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance & Funding in Travel & Tourism Sector

5

holding by him. The total number of members in private limited company is restricted to 50

members. Firms are also eligible to enjoy various tax advantages. Short term finance of the

private limited companies could be managed through Bank Overdraft, payables, retained

earnings and owners’ capital. Further, medium term funds could be generated by the private

limited companies firm through Factoring, Lease, assets sales and commercial bank

(Schlichting, 2013). And lastly, the long term loans could be financed by the private limited

companies firm through asset sales, venture capital, loan from bank loan, restructuring etc.

Public limited companies:

Public limited company is a standard legal designation of LLC as it offers the shares

to general public and though limited liabilities are also held by the company. This business

entity is publicly held. In public limited companies, there is no owner of the company. The

total number of members in public limited company is not restricted. Firms are also eligible

to enjoy various tax advantages (Moles, Parrino and Kidwekk, 2011). Short term finance of

the public limited companies could be managed through retained profit, capital, payables, bill

discounting, Bank Overdraft, capital etc. Further, medium term funds could be generated by

the public limited companies firm through Factoring, Lease, debentures, preference share

capital, assets sales and commercial bank. And lastly, the long term loans could be financed

by the public limited companies firm through asset sales, share capital, venture capital,

restructuring etc.

It explains about various sources which could be used by the different business entity

to raise the funds for short term, medium term and long term.

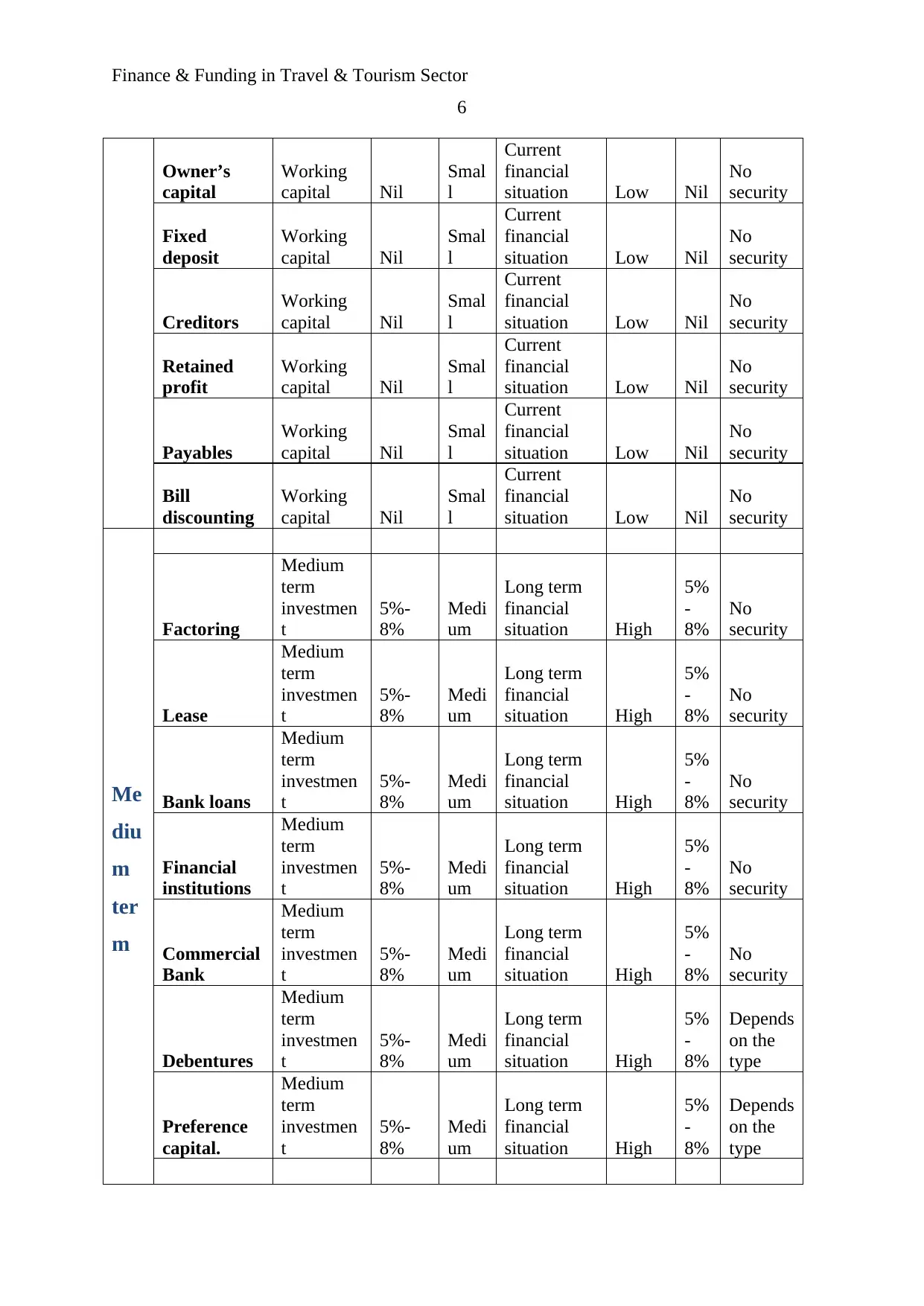

Help sheet:

Use of

funds

Cost

of

financ

e

Stat

us

and

Size

Financial

situation

Admi

nistrat

ion

charg

es

Int

ere

st

Securit

y

sho

rt

ter

m

Bank

Overdraft

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Credit cards

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Trade credit Working

capital

Nil Smal

l

Current

financial

situation

Low Nil No

security

5

holding by him. The total number of members in private limited company is restricted to 50

members. Firms are also eligible to enjoy various tax advantages. Short term finance of the

private limited companies could be managed through Bank Overdraft, payables, retained

earnings and owners’ capital. Further, medium term funds could be generated by the private

limited companies firm through Factoring, Lease, assets sales and commercial bank

(Schlichting, 2013). And lastly, the long term loans could be financed by the private limited

companies firm through asset sales, venture capital, loan from bank loan, restructuring etc.

Public limited companies:

Public limited company is a standard legal designation of LLC as it offers the shares

to general public and though limited liabilities are also held by the company. This business

entity is publicly held. In public limited companies, there is no owner of the company. The

total number of members in public limited company is not restricted. Firms are also eligible

to enjoy various tax advantages (Moles, Parrino and Kidwekk, 2011). Short term finance of

the public limited companies could be managed through retained profit, capital, payables, bill

discounting, Bank Overdraft, capital etc. Further, medium term funds could be generated by

the public limited companies firm through Factoring, Lease, debentures, preference share

capital, assets sales and commercial bank. And lastly, the long term loans could be financed

by the public limited companies firm through asset sales, share capital, venture capital,

restructuring etc.

It explains about various sources which could be used by the different business entity

to raise the funds for short term, medium term and long term.

Help sheet:

Use of

funds

Cost

of

financ

e

Stat

us

and

Size

Financial

situation

Admi

nistrat

ion

charg

es

Int

ere

st

Securit

y

sho

rt

ter

m

Bank

Overdraft

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Credit cards

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Trade credit Working

capital

Nil Smal

l

Current

financial

situation

Low Nil No

security

Finance & Funding in Travel & Tourism Sector

6

Owner’s

capital

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Fixed

deposit

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Creditors

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Retained

profit

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Payables

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Bill

discounting

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Me

diu

m

ter

m

Factoring

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

No

security

Lease

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

No

security

Bank loans

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

No

security

Financial

institutions

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

No

security

Commercial

Bank

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

No

security

Debentures

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

Depends

on the

type

Preference

capital.

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

Depends

on the

type

6

Owner’s

capital

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Fixed

deposit

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Creditors

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Retained

profit

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Payables

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Bill

discounting

Working

capital Nil

Smal

l

Current

financial

situation Low Nil

No

security

Me

diu

m

ter

m

Factoring

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

No

security

Lease

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

No

security

Bank loans

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

No

security

Financial

institutions

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

No

security

Commercial

Bank

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

No

security

Debentures

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

Depends

on the

type

Preference

capital.

Medium

term

investmen

t

5%-

8%

Medi

um

Long term

financial

situation High

5%

-

8%

Depends

on the

type

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance & Funding in Travel & Tourism Sector

7

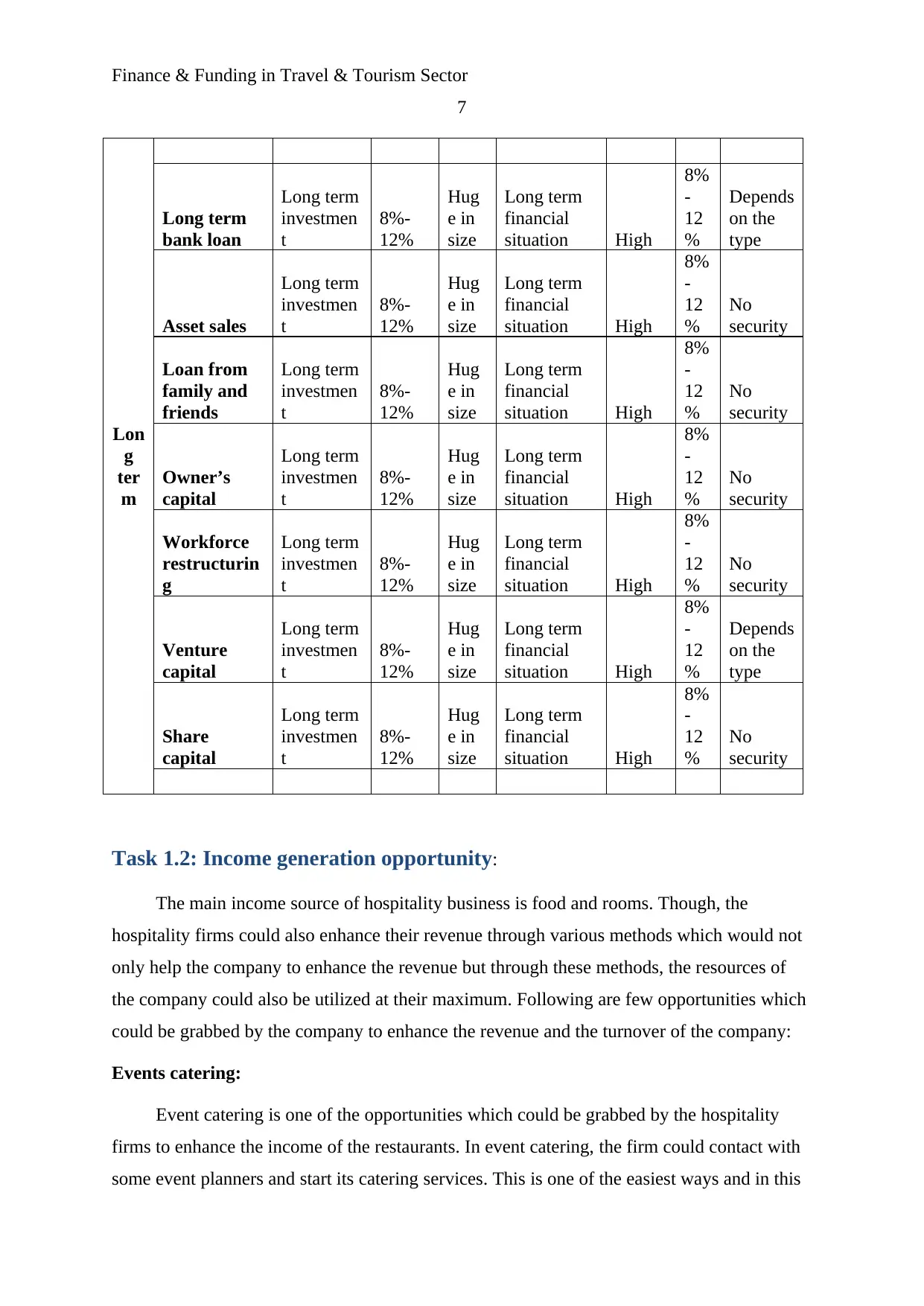

Lon

g

ter

m

Long term

bank loan

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

Depends

on the

type

Asset sales

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

No

security

Loan from

family and

friends

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

No

security

Owner’s

capital

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

No

security

Workforce

restructurin

g

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

No

security

Venture

capital

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

Depends

on the

type

Share

capital

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

No

security

Task 1.2: Income generation opportunity:

The main income source of hospitality business is food and rooms. Though, the

hospitality firms could also enhance their revenue through various methods which would not

only help the company to enhance the revenue but through these methods, the resources of

the company could also be utilized at their maximum. Following are few opportunities which

could be grabbed by the company to enhance the revenue and the turnover of the company:

Events catering:

Event catering is one of the opportunities which could be grabbed by the hospitality

firms to enhance the income of the restaurants. In event catering, the firm could contact with

some event planners and start its catering services. This is one of the easiest ways and in this

7

Lon

g

ter

m

Long term

bank loan

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

Depends

on the

type

Asset sales

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

No

security

Loan from

family and

friends

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

No

security

Owner’s

capital

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

No

security

Workforce

restructurin

g

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

No

security

Venture

capital

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

Depends

on the

type

Share

capital

Long term

investmen

t

8%-

12%

Hug

e in

size

Long term

financial

situation High

8%

-

12

%

No

security

Task 1.2: Income generation opportunity:

The main income source of hospitality business is food and rooms. Though, the

hospitality firms could also enhance their revenue through various methods which would not

only help the company to enhance the revenue but through these methods, the resources of

the company could also be utilized at their maximum. Following are few opportunities which

could be grabbed by the company to enhance the revenue and the turnover of the company:

Events catering:

Event catering is one of the opportunities which could be grabbed by the hospitality

firms to enhance the income of the restaurants. In event catering, the firm could contact with

some event planners and start its catering services. This is one of the easiest ways and in this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance & Funding in Travel & Tourism Sector

8

method; fixed cost of the company would also be lower. The income from the event catering

would be quite higher and it could be planned by the firms as a long term side business

(Reilly and Brown, 2011).

Cookery classes:

Cookery classes are also one of the opportunities which could be grabbed by the

hospitality firms to enhance the income of the restaurants as well as utilize the resources of

the company in a proper way. In cookery classes, the firm could offer the classes to the prime

members or some clubs. This is one of the easiest ways as in the off seasons, the hospitality

firms would be able to utilize their resources and the income could also be enhanced by the

company. And in this method; fixed cost of the company would also be lower. The income

from the cookery classes would be quite higher and it could be planned by the firms as a long

term side business as well.

Merchandising kitchen items and cookbooks:

Merchandising kitchen items and few cookbooks could also be a good opportunity for

the hospitality firms to grab and enhance the income of the restaurants. In merchandising

kitchen items and few cookbooks, the firm could provide various cuisine cook books and

imported kitchen items to its customers (Ross, Westerfield and Jaffe, 2007). This is one of the

easiest ways as the company is not required to spend some extra money on it. And in this

method; fixed cost of the company would also be lower. The income from the Merchandising

kitchen items and few cookbooks would be quite higher and it could be planned by the firms

as a long term side business as well.

Conclusion:

The above study explains about various sources which could be used by the different

business entity to raise the funds for short term, medium term and long term. And it also

explains about some opportunities which could be grabbed by the companies to enhance their

income.

8

method; fixed cost of the company would also be lower. The income from the event catering

would be quite higher and it could be planned by the firms as a long term side business

(Reilly and Brown, 2011).

Cookery classes:

Cookery classes are also one of the opportunities which could be grabbed by the

hospitality firms to enhance the income of the restaurants as well as utilize the resources of

the company in a proper way. In cookery classes, the firm could offer the classes to the prime

members or some clubs. This is one of the easiest ways as in the off seasons, the hospitality

firms would be able to utilize their resources and the income could also be enhanced by the

company. And in this method; fixed cost of the company would also be lower. The income

from the cookery classes would be quite higher and it could be planned by the firms as a long

term side business as well.

Merchandising kitchen items and cookbooks:

Merchandising kitchen items and few cookbooks could also be a good opportunity for

the hospitality firms to grab and enhance the income of the restaurants. In merchandising

kitchen items and few cookbooks, the firm could provide various cuisine cook books and

imported kitchen items to its customers (Ross, Westerfield and Jaffe, 2007). This is one of the

easiest ways as the company is not required to spend some extra money on it. And in this

method; fixed cost of the company would also be lower. The income from the Merchandising

kitchen items and few cookbooks would be quite higher and it could be planned by the firms

as a long term side business as well.

Conclusion:

The above study explains about various sources which could be used by the different

business entity to raise the funds for short term, medium term and long term. And it also

explains about some opportunities which could be grabbed by the companies to enhance their

income.

Finance & Funding in Travel & Tourism Sector

9

Task 2: Refer to PPT file

Task 3: Budgetary report

Introduction:

The report has been prepared to evaluate and analyze the purpose and structure of trial

balance, income statement, balance sheet and cash flow statement. The report explains that

why the final accounts is prepared by the different business entities. Further, it explains about

the budgetary control, variance analysis and recommendation to the entity.

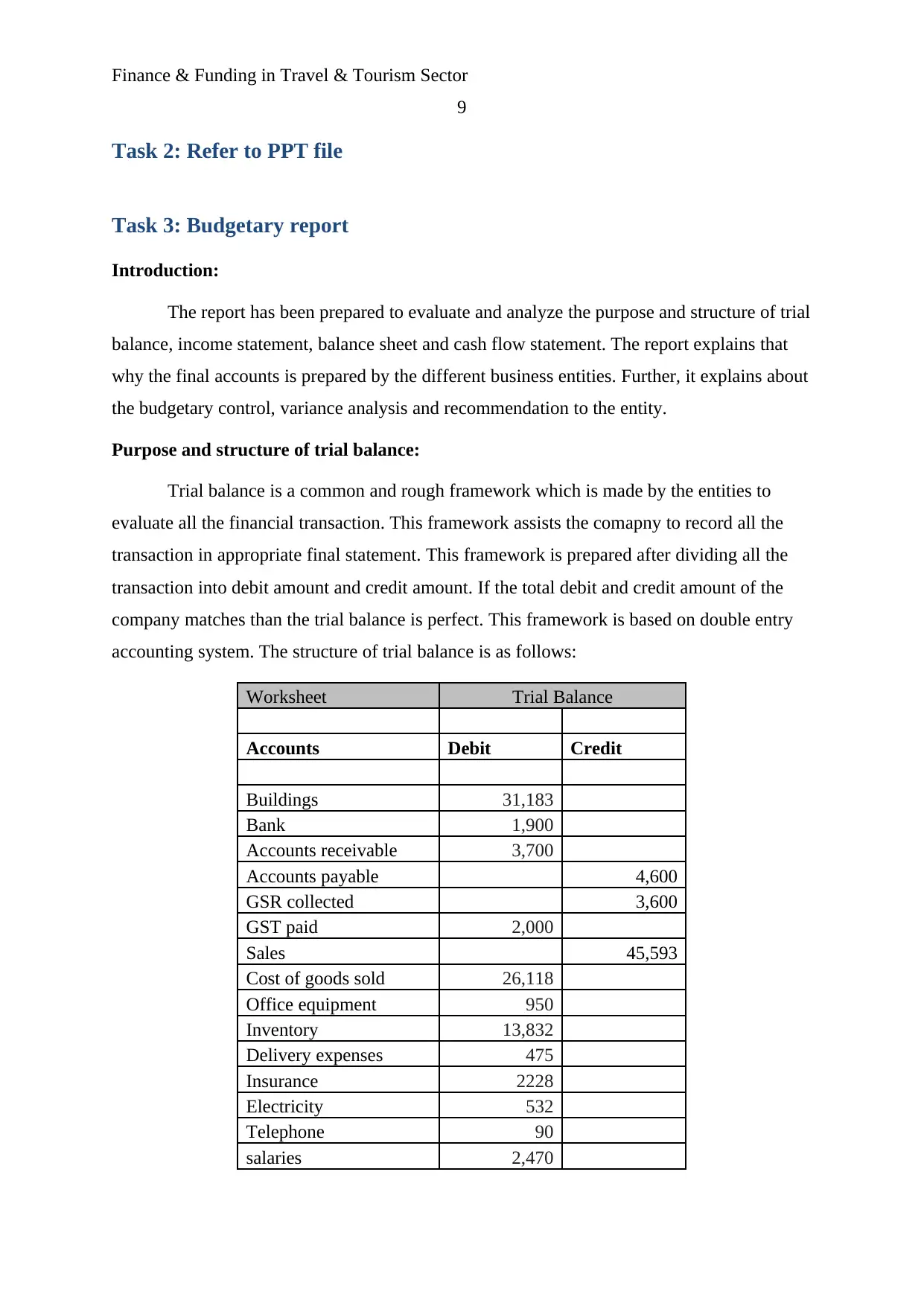

Purpose and structure of trial balance:

Trial balance is a common and rough framework which is made by the entities to

evaluate all the financial transaction. This framework assists the comapny to record all the

transaction in appropriate final statement. This framework is prepared after dividing all the

transaction into debit amount and credit amount. If the total debit and credit amount of the

company matches than the trial balance is perfect. This framework is based on double entry

accounting system. The structure of trial balance is as follows:

Worksheet Trial Balance

Accounts Debit Credit

Buildings 31,183

Bank 1,900

Accounts receivable 3,700

Accounts payable 4,600

GSR collected 3,600

GST paid 2,000

Sales 45,593

Cost of goods sold 26,118

Office equipment 950

Inventory 13,832

Delivery expenses 475

Insurance 2228

Electricity 532

Telephone 90

salaries 2,470

9

Task 2: Refer to PPT file

Task 3: Budgetary report

Introduction:

The report has been prepared to evaluate and analyze the purpose and structure of trial

balance, income statement, balance sheet and cash flow statement. The report explains that

why the final accounts is prepared by the different business entities. Further, it explains about

the budgetary control, variance analysis and recommendation to the entity.

Purpose and structure of trial balance:

Trial balance is a common and rough framework which is made by the entities to

evaluate all the financial transaction. This framework assists the comapny to record all the

transaction in appropriate final statement. This framework is prepared after dividing all the

transaction into debit amount and credit amount. If the total debit and credit amount of the

company matches than the trial balance is perfect. This framework is based on double entry

accounting system. The structure of trial balance is as follows:

Worksheet Trial Balance

Accounts Debit Credit

Buildings 31,183

Bank 1,900

Accounts receivable 3,700

Accounts payable 4,600

GSR collected 3,600

GST paid 2,000

Sales 45,593

Cost of goods sold 26,118

Office equipment 950

Inventory 13,832

Delivery expenses 475

Insurance 2228

Electricity 532

Telephone 90

salaries 2,470

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance & Funding in Travel & Tourism Sector

10

Rates 238

Discount allowed 1,007

Rent 484

Commission income 807

Capital (opening) 32,607

Net profit

Total 80607 80607

(Higgins, 2012)

The above table of trial balance briefs that the trial balance briefs about the entire

financial statement of the company in a particular time period.

Purpose of final accounts:

Final accounts are income statement, cash flow statement, changes in equity statement

and balance sheet. These accounts are prepared by the business entities after a particular

period of time. The main purpose of these final accounts is to identify the worth of the

company and the changes in the company in a particular time period. Income statement is

made by the companies to identify the turnover, operating profit, net profit etc of the

company. Balance sheet explains about the financial strength of the company and cash flow

statement evaluates about the total cash outflow and cash inflow of the company.

Purpose of final accounts for partnership, sole traders and limited company:

Final accounts are prepared by all the business entities to manage the performance of

the company. Some traders prepare the final statements to analyze all the transactions of the

company and the total profit of the firm. On the other hand, in partnership firm, final

statements are prepared by the firm to identify the total profit of the firm and the better

distribution of profit among the partners (Lord, 2012). In addition, the limited company is

required to make the final statements on the basis of company act. It assists the stakeholders

of the company to make a decision about the company. Though, there are various purposes

due to which the business entities prepare the final accounts.

Purpose and use of budgetary control:

Financial budget is vital for every company as it represents the future data of the

company. On the basis of budgets, future is predicted by the company. Financial budgets are

10

Rates 238

Discount allowed 1,007

Rent 484

Commission income 807

Capital (opening) 32,607

Net profit

Total 80607 80607

(Higgins, 2012)

The above table of trial balance briefs that the trial balance briefs about the entire

financial statement of the company in a particular time period.

Purpose of final accounts:

Final accounts are income statement, cash flow statement, changes in equity statement

and balance sheet. These accounts are prepared by the business entities after a particular

period of time. The main purpose of these final accounts is to identify the worth of the

company and the changes in the company in a particular time period. Income statement is

made by the companies to identify the turnover, operating profit, net profit etc of the

company. Balance sheet explains about the financial strength of the company and cash flow

statement evaluates about the total cash outflow and cash inflow of the company.

Purpose of final accounts for partnership, sole traders and limited company:

Final accounts are prepared by all the business entities to manage the performance of

the company. Some traders prepare the final statements to analyze all the transactions of the

company and the total profit of the firm. On the other hand, in partnership firm, final

statements are prepared by the firm to identify the total profit of the firm and the better

distribution of profit among the partners (Lord, 2012). In addition, the limited company is

required to make the final statements on the basis of company act. It assists the stakeholders

of the company to make a decision about the company. Though, there are various purposes

due to which the business entities prepare the final accounts.

Purpose and use of budgetary control:

Financial budget is vital for every company as it represents the future data of the

company. On the basis of budgets, future is predicted by the company. Financial budgets are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance & Funding in Travel & Tourism Sector

11

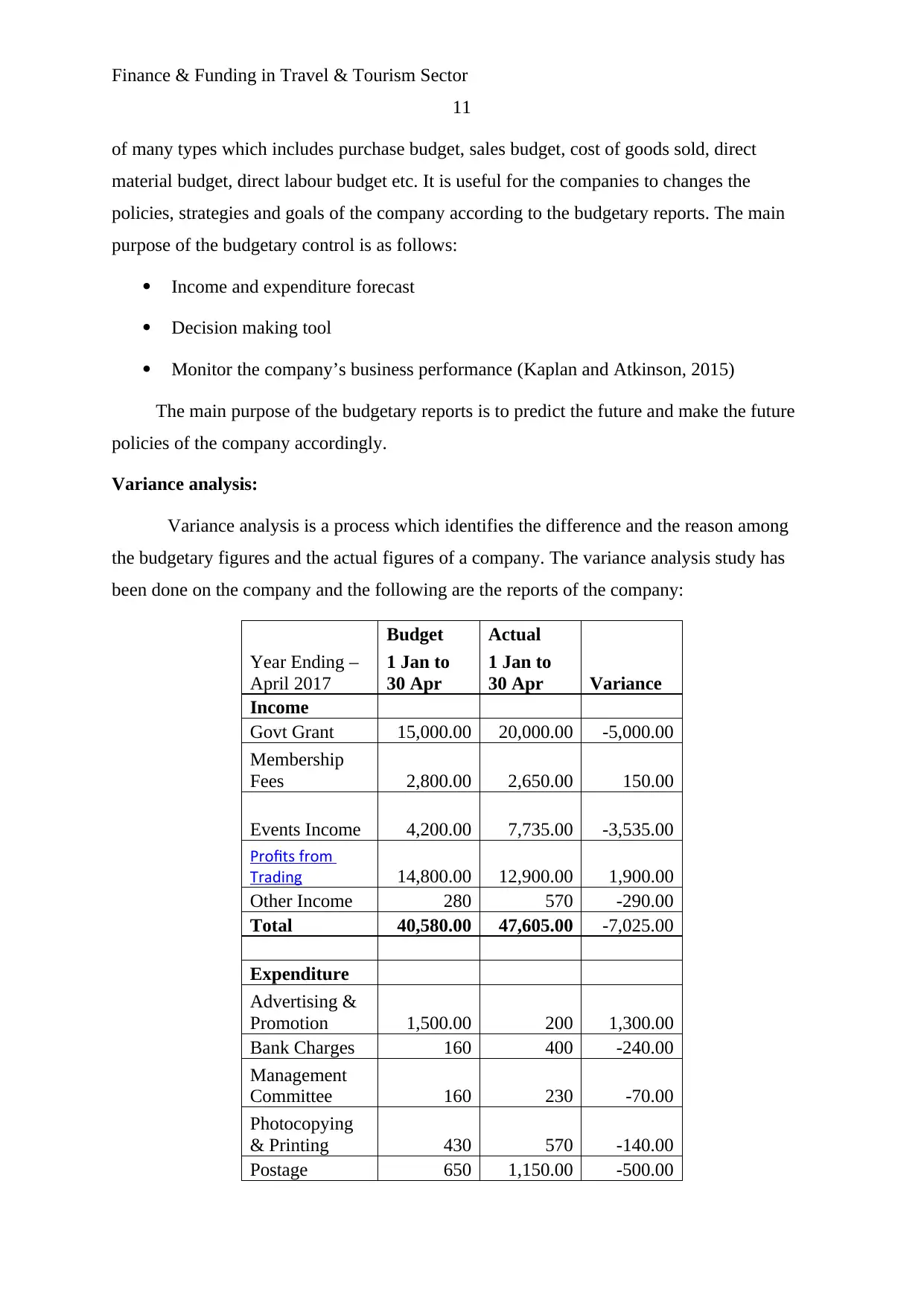

of many types which includes purchase budget, sales budget, cost of goods sold, direct

material budget, direct labour budget etc. It is useful for the companies to changes the

policies, strategies and goals of the company according to the budgetary reports. The main

purpose of the budgetary control is as follows:

Income and expenditure forecast

Decision making tool

Monitor the company’s business performance (Kaplan and Atkinson, 2015)

The main purpose of the budgetary reports is to predict the future and make the future

policies of the company accordingly.

Variance analysis:

Variance analysis is a process which identifies the difference and the reason among

the budgetary figures and the actual figures of a company. The variance analysis study has

been done on the company and the following are the reports of the company:

Year Ending –

April 2017

Budget Actual

Variance

1 Jan to

30 Apr

1 Jan to

30 Apr

Income

Govt Grant 15,000.00 20,000.00 -5,000.00

Membership

Fees 2,800.00 2,650.00 150.00

Events Income 4,200.00 7,735.00 -3,535.00

Profits from

Trading 14,800.00 12,900.00 1,900.00

Other Income 280 570 -290.00

Total 40,580.00 47,605.00 -7,025.00

Expenditure

Advertising &

Promotion 1,500.00 200 1,300.00

Bank Charges 160 400 -240.00

Management

Committee 160 230 -70.00

Photocopying

& Printing 430 570 -140.00

Postage 650 1,150.00 -500.00

11

of many types which includes purchase budget, sales budget, cost of goods sold, direct

material budget, direct labour budget etc. It is useful for the companies to changes the

policies, strategies and goals of the company according to the budgetary reports. The main

purpose of the budgetary control is as follows:

Income and expenditure forecast

Decision making tool

Monitor the company’s business performance (Kaplan and Atkinson, 2015)

The main purpose of the budgetary reports is to predict the future and make the future

policies of the company accordingly.

Variance analysis:

Variance analysis is a process which identifies the difference and the reason among

the budgetary figures and the actual figures of a company. The variance analysis study has

been done on the company and the following are the reports of the company:

Year Ending –

April 2017

Budget Actual

Variance

1 Jan to

30 Apr

1 Jan to

30 Apr

Income

Govt Grant 15,000.00 20,000.00 -5,000.00

Membership

Fees 2,800.00 2,650.00 150.00

Events Income 4,200.00 7,735.00 -3,535.00

Profits from

Trading 14,800.00 12,900.00 1,900.00

Other Income 280 570 -290.00

Total 40,580.00 47,605.00 -7,025.00

Expenditure

Advertising &

Promotion 1,500.00 200 1,300.00

Bank Charges 160 400 -240.00

Management

Committee 160 230 -70.00

Photocopying

& Printing 430 570 -140.00

Postage 650 1,150.00 -500.00

Finance & Funding in Travel & Tourism Sector

12

Rent 1,300.00 1,000.00 300.00

Repairs &

Renewals 300 225 75.00

Salaries 18,300.00 18,300.00 0.00

Stationery &

Computer 500 630 -130.00

Telephone 1,000.00 1,665.00 -665.00

Total 24,300.00 24,370.00 -70.00

Surplus/Deficit 16,280.00 23,235.00 -6,955.00

(Glajnaric, 2016)

The variance analysis expresses about huge changes which has taken place into the

company in a particular period of time.

Recommendation and conclusion:

The variance analysis study explains that the budgetary reports of the company are

not much effective. It is recommended to the company to follow more effective budgetary

techniques and predict the future on the basis of historical data as well as the current trend.

To conclude, final statement and budgetary reports both are quite crucial for an organization

to maintain and manage the performance of the company.

Task 4: Ratio analysis:

Introduction:

The report has been prepared to evaluate the financial performance of the company. It

evaluates the final statement of the company and evaluates the final statement on the basis of

ratio analysis. It explains about the performance of the company and makes a

recommendation about the management of the company to make better strategies.

Ratio analysis:

Ratio analysis is a process of financial statement analysis which evaluates the final

statement of the company on various bases such as liquidity, profitability, efficiency and

financial performance of the company. Following is the study and the analysis of the ratio

analysis of the company:

12

Rent 1,300.00 1,000.00 300.00

Repairs &

Renewals 300 225 75.00

Salaries 18,300.00 18,300.00 0.00

Stationery &

Computer 500 630 -130.00

Telephone 1,000.00 1,665.00 -665.00

Total 24,300.00 24,370.00 -70.00

Surplus/Deficit 16,280.00 23,235.00 -6,955.00

(Glajnaric, 2016)

The variance analysis expresses about huge changes which has taken place into the

company in a particular period of time.

Recommendation and conclusion:

The variance analysis study explains that the budgetary reports of the company are

not much effective. It is recommended to the company to follow more effective budgetary

techniques and predict the future on the basis of historical data as well as the current trend.

To conclude, final statement and budgetary reports both are quite crucial for an organization

to maintain and manage the performance of the company.

Task 4: Ratio analysis:

Introduction:

The report has been prepared to evaluate the financial performance of the company. It

evaluates the final statement of the company and evaluates the final statement on the basis of

ratio analysis. It explains about the performance of the company and makes a

recommendation about the management of the company to make better strategies.

Ratio analysis:

Ratio analysis is a process of financial statement analysis which evaluates the final

statement of the company on various bases such as liquidity, profitability, efficiency and

financial performance of the company. Following is the study and the analysis of the ratio

analysis of the company:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.