Financial Reporting ACC00145: Coles' Hedge Accounting Analysis Report

VerifiedAdded on 2022/11/15

|11

|2148

|208

Report

AI Summary

This report provides a comprehensive analysis of Coles' financial reporting practices, with a specific focus on hedge accounting. It begins by defining the concept of hedging and its importance in mitigating financial risks, then delves into the qualifying criteria for hedge accounting adopted by Coles, a subsidiary of Wesfarmers. The report examines the types of hedges employed by Coles, including foreign exchange contracts, interest rate swaps, and Brent oil contracts, in accordance with AASB standards. It further evaluates the advantages and disadvantages of Coles' hedge accounting strategies, considering both fair value and cash flow hedges. Finally, the report appraises the measurement of hedging instruments and hedged items, referencing relevant accounting standards and providing insights into how Coles manages its financial risk exposure. The report utilizes figures and tables to illustrate key concepts and data, providing a clear understanding of Coles' financial reporting approach.

Running head: FINANCIAL REPORTING

Financial Reporting

Name of the Student:

Name of the University:

Authors Note:

Financial Reporting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL REPORTING

1

Table of Contents

1. Amplifying the concept of hedge:..........................................................................................2

2. Amplifying the qualifying criteria of hedge accounting adopted by Coles:..........................3

3. Providing information about the advantage and disadvantage of hedge accounting used by

Coles:..........................................................................................................................................5

4. Appraising the measurement of hedging instrument and hedged items made by Coles:.......7

Reference and Bibliography:......................................................................................................9

1

Table of Contents

1. Amplifying the concept of hedge:..........................................................................................2

2. Amplifying the qualifying criteria of hedge accounting adopted by Coles:..........................3

3. Providing information about the advantage and disadvantage of hedge accounting used by

Coles:..........................................................................................................................................5

4. Appraising the measurement of hedging instrument and hedged items made by Coles:.......7

Reference and Bibliography:......................................................................................................9

FINANCIAL REPORTING

2

1. Amplifying the concept of hedge:

Hedge is a relevant term that indicates about the Measures that is taken by

organizations to mitigate the risk from operation. This considered an adequate investment

process that allows the organizations to secure their risky Assets and Investments, which can

negatively affect their capitals exposure and profitability. There are different types of hedging

instruments such as futures contract, option contract, and forward contract, which is used by

organizations to adequately minimize the exposure of external factors in their revenue

streams (Bessis 2015). The different contracts are relatively subjective to investment options

that are provided to the organization for adequately hedging their overall risk. The different

firms of contract such as future option and forward are directly utilized for effectively fixing

the current pricing conditions of the trade. This would eventually allow the organization to

minimize the level of risk exposure that might affect its profitability in future.

The companies to minimize their risk exposure in finance cost, while helps in

reducing the level of cash outflow and maximize the profit levels during the financial year.

Option contracts are considered to be the major hedging instruments that is used by

Organizations and other investors to mitigate the level of risk involved in their Investments

(Rampini, Sufi and Viswanathan 2014). Therefore, in accordance with the AASB 7 Financial

Instruments: Disclosures, relevant hedging measures that have been used by the organisation

needs to be mentioned in their financial report. The organization relatively uses the hedging

instruments to mitigate the risk from interest rates, foreign currency exchange, raw material

expenses and other cash flows during the financial year. Hedging instruments not only

conducted by organization but also, by investors for minimizing the level of risk involved in

their investments. Hedging instruments allow investors to mitigate the risk exposure and

effectively improve its profitability in the process.

2

1. Amplifying the concept of hedge:

Hedge is a relevant term that indicates about the Measures that is taken by

organizations to mitigate the risk from operation. This considered an adequate investment

process that allows the organizations to secure their risky Assets and Investments, which can

negatively affect their capitals exposure and profitability. There are different types of hedging

instruments such as futures contract, option contract, and forward contract, which is used by

organizations to adequately minimize the exposure of external factors in their revenue

streams (Bessis 2015). The different contracts are relatively subjective to investment options

that are provided to the organization for adequately hedging their overall risk. The different

firms of contract such as future option and forward are directly utilized for effectively fixing

the current pricing conditions of the trade. This would eventually allow the organization to

minimize the level of risk exposure that might affect its profitability in future.

The companies to minimize their risk exposure in finance cost, while helps in

reducing the level of cash outflow and maximize the profit levels during the financial year.

Option contracts are considered to be the major hedging instruments that is used by

Organizations and other investors to mitigate the level of risk involved in their Investments

(Rampini, Sufi and Viswanathan 2014). Therefore, in accordance with the AASB 7 Financial

Instruments: Disclosures, relevant hedging measures that have been used by the organisation

needs to be mentioned in their financial report. The organization relatively uses the hedging

instruments to mitigate the risk from interest rates, foreign currency exchange, raw material

expenses and other cash flows during the financial year. Hedging instruments not only

conducted by organization but also, by investors for minimizing the level of risk involved in

their investments. Hedging instruments allow investors to mitigate the risk exposure and

effectively improve its profitability in the process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL REPORTING

3

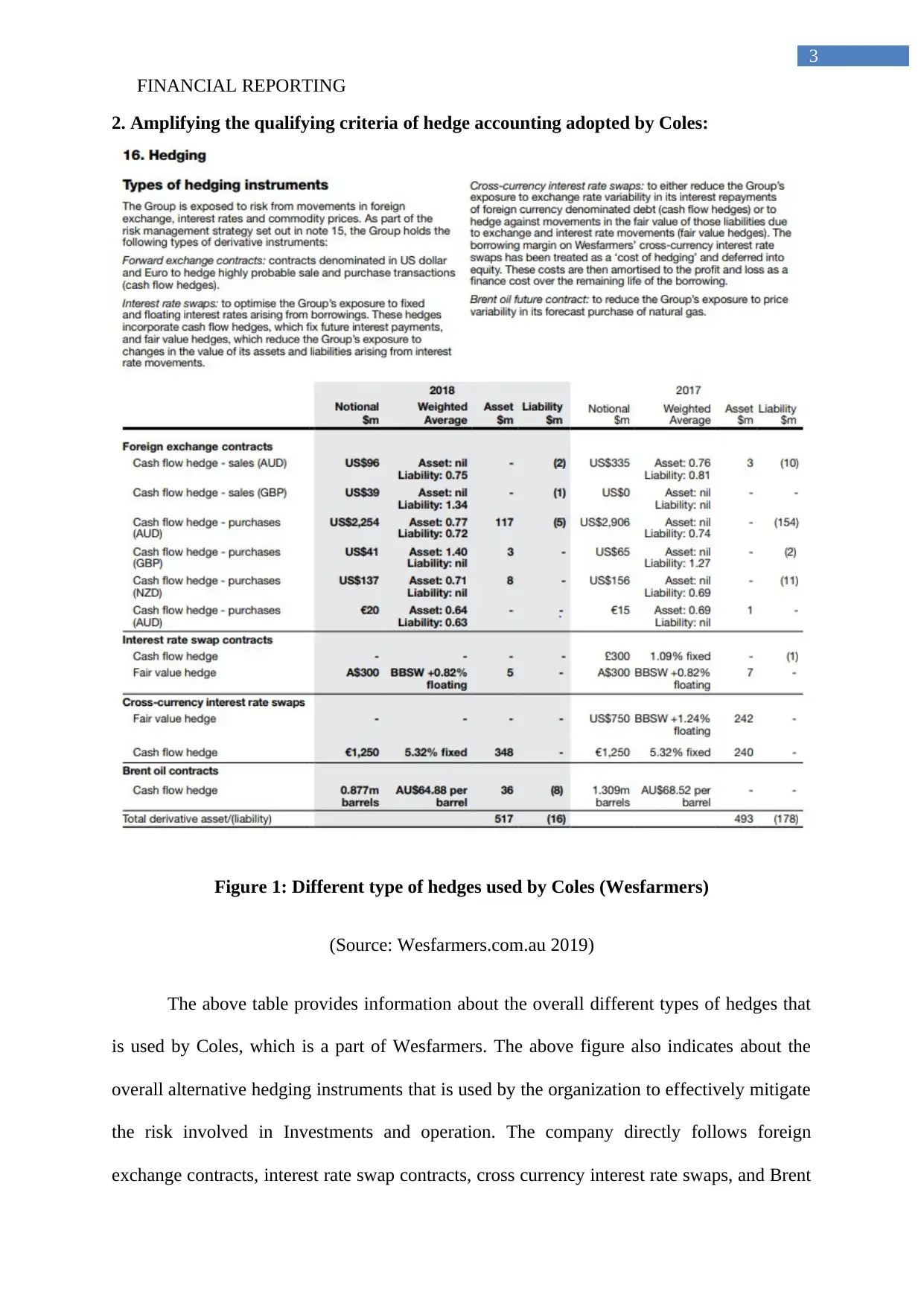

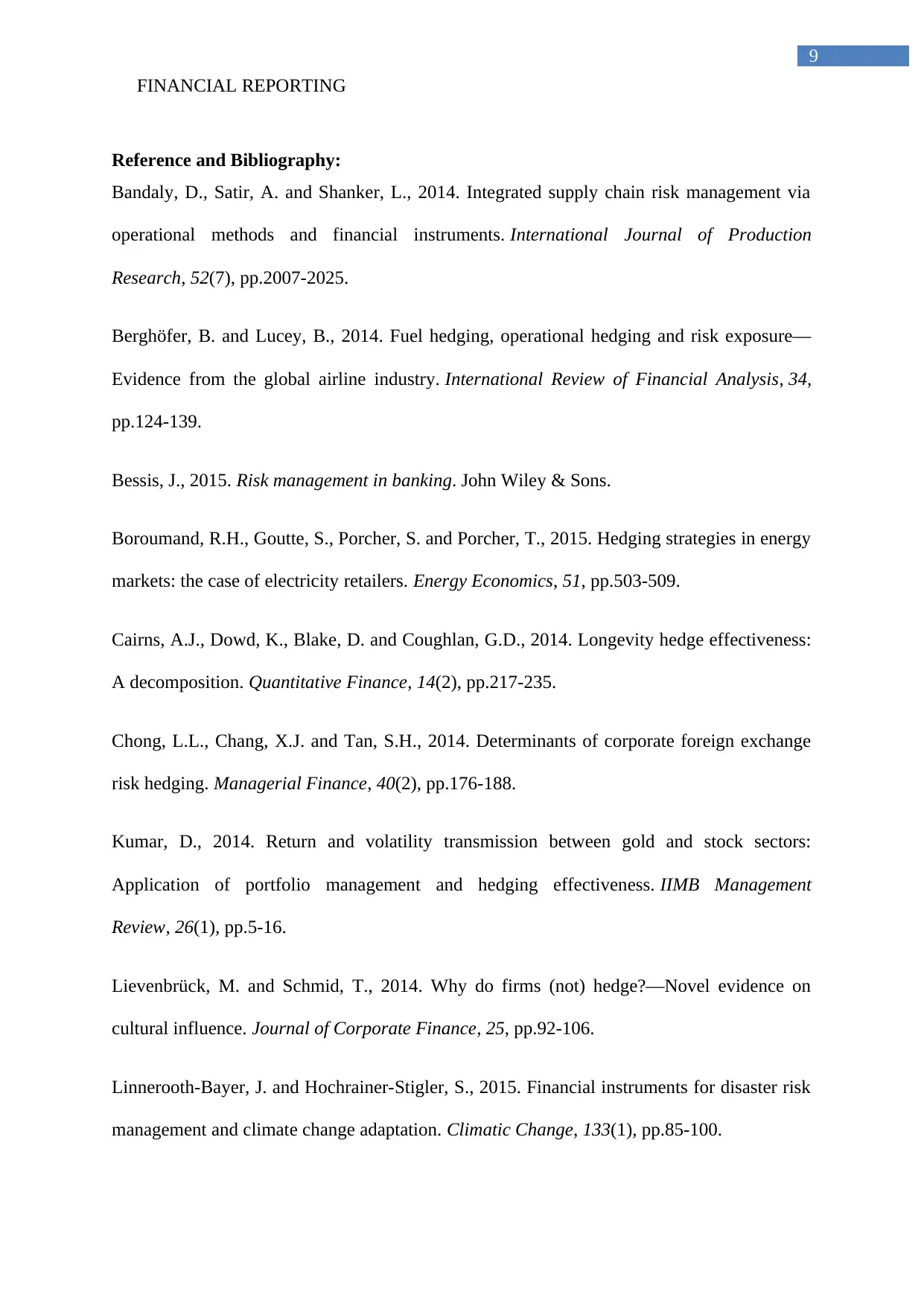

2. Amplifying the qualifying criteria of hedge accounting adopted by Coles:

Figure 1: Different type of hedges used by Coles (Wesfarmers)

(Source: Wesfarmers.com.au 2019)

The above table provides information about the overall different types of hedges that

is used by Coles, which is a part of Wesfarmers. The above figure also indicates about the

overall alternative hedging instruments that is used by the organization to effectively mitigate

the risk involved in Investments and operation. The company directly follows foreign

exchange contracts, interest rate swap contracts, cross currency interest rate swaps, and Brent

3

2. Amplifying the qualifying criteria of hedge accounting adopted by Coles:

Figure 1: Different type of hedges used by Coles (Wesfarmers)

(Source: Wesfarmers.com.au 2019)

The above table provides information about the overall different types of hedges that

is used by Coles, which is a part of Wesfarmers. The above figure also indicates about the

overall alternative hedging instruments that is used by the organization to effectively mitigate

the risk involved in Investments and operation. The company directly follows foreign

exchange contracts, interest rate swap contracts, cross currency interest rate swaps, and Brent

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL REPORTING

4

oil contacts (Bandaly, Satir and Shanker 2014). The above-mentioned contract selectively

conducted by the organization to minimize their risk that is affecting their operations in the

process. However, Coles being one of the major subsidiaries of Wesfarmers have adequately

increased their exposure in the above hedging instruments, which allow the management to

mitigate the risk in involved in investments. AASB 101 Presentation of Financial Statements,

indicate that all the relevant information about the hedging instruments need to be provided

by the company in their financial report.

Moreover, different types of cash flow ages and fair value has conducted by Coles in

the annual report, which is depicted in the above figure. There are relevant qualifying

criteria’s of hedge accounting that is adopted by the Coles, as it is required by the company to

support the relevant operations. Coles is a subsidiary of Wesfarmers who is responsible for

hedging foreign exchange contracts to minimize the risk involved in currency exchange. The

organization has mainly utilized the method for adequately improving the level of exposure

in their current financial conditions (Kumar 2014). The interest rates of contracts are

relatively used for hedging their overall finance cost, as it helps in minimizing the relevant

cash outflows and maximizing the overall income for the company. The cross currency

interest rate swaps are conducted for effective minimizing the negative impact of

international loan that is taken by the company support its operation. Lastly, the company has

adequately conducted contract for Brand oil, which is essential for reducing the risk level of

changes in oil prices as the company provides services for oil product. Changes in the value

of Brent oil directly have an impact on the current revenue generation capability of Coles

division (Lievenbrück and Schmid 2014).

4

oil contacts (Bandaly, Satir and Shanker 2014). The above-mentioned contract selectively

conducted by the organization to minimize their risk that is affecting their operations in the

process. However, Coles being one of the major subsidiaries of Wesfarmers have adequately

increased their exposure in the above hedging instruments, which allow the management to

mitigate the risk in involved in investments. AASB 101 Presentation of Financial Statements,

indicate that all the relevant information about the hedging instruments need to be provided

by the company in their financial report.

Moreover, different types of cash flow ages and fair value has conducted by Coles in

the annual report, which is depicted in the above figure. There are relevant qualifying

criteria’s of hedge accounting that is adopted by the Coles, as it is required by the company to

support the relevant operations. Coles is a subsidiary of Wesfarmers who is responsible for

hedging foreign exchange contracts to minimize the risk involved in currency exchange. The

organization has mainly utilized the method for adequately improving the level of exposure

in their current financial conditions (Kumar 2014). The interest rates of contracts are

relatively used for hedging their overall finance cost, as it helps in minimizing the relevant

cash outflows and maximizing the overall income for the company. The cross currency

interest rate swaps are conducted for effective minimizing the negative impact of

international loan that is taken by the company support its operation. Lastly, the company has

adequately conducted contract for Brand oil, which is essential for reducing the risk level of

changes in oil prices as the company provides services for oil product. Changes in the value

of Brent oil directly have an impact on the current revenue generation capability of Coles

division (Lievenbrück and Schmid 2014).

FINANCIAL REPORTING

5

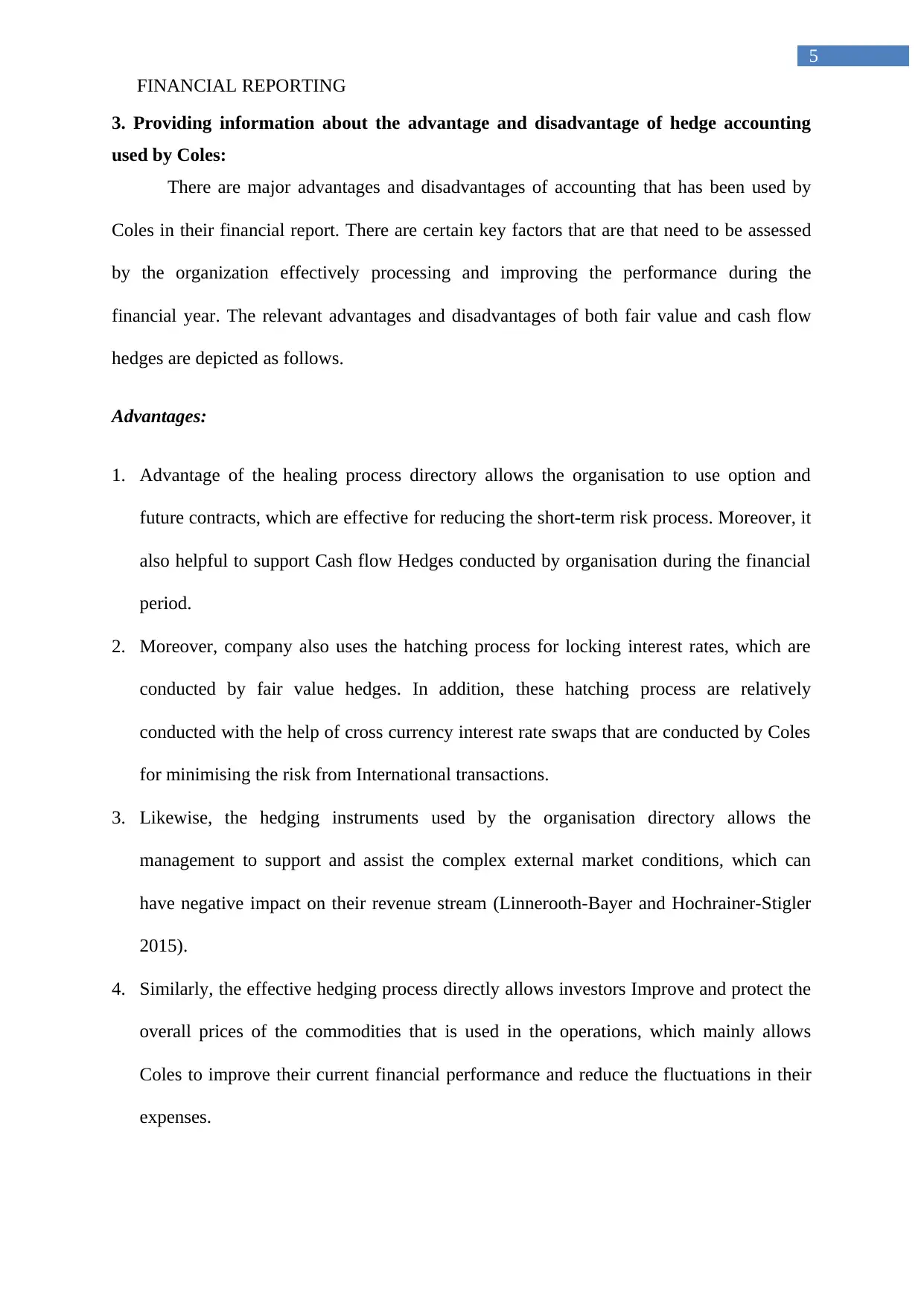

3. Providing information about the advantage and disadvantage of hedge accounting

used by Coles:

There are major advantages and disadvantages of accounting that has been used by

Coles in their financial report. There are certain key factors that are that need to be assessed

by the organization effectively processing and improving the performance during the

financial year. The relevant advantages and disadvantages of both fair value and cash flow

hedges are depicted as follows.

Advantages:

1. Advantage of the healing process directory allows the organisation to use option and

future contracts, which are effective for reducing the short-term risk process. Moreover, it

also helpful to support Cash flow Hedges conducted by organisation during the financial

period.

2. Moreover, company also uses the hatching process for locking interest rates, which are

conducted by fair value hedges. In addition, these hatching process are relatively

conducted with the help of cross currency interest rate swaps that are conducted by Coles

for minimising the risk from International transactions.

3. Likewise, the hedging instruments used by the organisation directory allows the

management to support and assist the complex external market conditions, which can

have negative impact on their revenue stream (Linnerooth-Bayer and Hochrainer-Stigler

2015).

4. Similarly, the effective hedging process directly allows investors Improve and protect the

overall prices of the commodities that is used in the operations, which mainly allows

Coles to improve their current financial performance and reduce the fluctuations in their

expenses.

5

3. Providing information about the advantage and disadvantage of hedge accounting

used by Coles:

There are major advantages and disadvantages of accounting that has been used by

Coles in their financial report. There are certain key factors that are that need to be assessed

by the organization effectively processing and improving the performance during the

financial year. The relevant advantages and disadvantages of both fair value and cash flow

hedges are depicted as follows.

Advantages:

1. Advantage of the healing process directory allows the organisation to use option and

future contracts, which are effective for reducing the short-term risk process. Moreover, it

also helpful to support Cash flow Hedges conducted by organisation during the financial

period.

2. Moreover, company also uses the hatching process for locking interest rates, which are

conducted by fair value hedges. In addition, these hatching process are relatively

conducted with the help of cross currency interest rate swaps that are conducted by Coles

for minimising the risk from International transactions.

3. Likewise, the hedging instruments used by the organisation directory allows the

management to support and assist the complex external market conditions, which can

have negative impact on their revenue stream (Linnerooth-Bayer and Hochrainer-Stigler

2015).

4. Similarly, the effective hedging process directly allows investors Improve and protect the

overall prices of the commodities that is used in the operations, which mainly allows

Coles to improve their current financial performance and reduce the fluctuations in their

expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL REPORTING

6

5. Furthermore, hedging provide adequate exposure to the organisation with low monitoring

process, as it can allow the management to effectively reduce the volatility in the daily

market prices and smoothly conduct operations without increasing the relevant risk.

6. Hedging process allows the organisations are able to secure their risk from Complex

plans, which can have negative impact on the future growth of the organisation.

Disadvantages:

1. The major disadvantages that can be presented from hedging are the relevant losses that

might occur due to the lack of adequate research conducted by companies.

2. Risk and reward conditions in the hatching process are relatively similar where wrong

assumptions would directly lead to higher losses and increased risk from the operation of

the organization (Berghofer and Lucey 2014).

3. Moreover, hedging process is relatively conducted for short duration, as it helps in

minimizing the risk involved in investment and does not accommodate long-term

transactions.

4. Moreover, the hedging process loses friction when the overall market is performing

sidewise, as the actual benefits that would be generated from the process is mitigated.

However, in this scenario company has to incur losses from premiums, which can have

negative impact on their cash flow conditions.

5. Furthermore, the use of hedging contract such as futures and options directly require

adequate balances and capital for effectively securing risk involved in investment. This

increases the restrictions on the cash that can be used by the company due to the presence

of hedging contracts.

6

5. Furthermore, hedging provide adequate exposure to the organisation with low monitoring

process, as it can allow the management to effectively reduce the volatility in the daily

market prices and smoothly conduct operations without increasing the relevant risk.

6. Hedging process allows the organisations are able to secure their risk from Complex

plans, which can have negative impact on the future growth of the organisation.

Disadvantages:

1. The major disadvantages that can be presented from hedging are the relevant losses that

might occur due to the lack of adequate research conducted by companies.

2. Risk and reward conditions in the hatching process are relatively similar where wrong

assumptions would directly lead to higher losses and increased risk from the operation of

the organization (Berghofer and Lucey 2014).

3. Moreover, hedging process is relatively conducted for short duration, as it helps in

minimizing the risk involved in investment and does not accommodate long-term

transactions.

4. Moreover, the hedging process loses friction when the overall market is performing

sidewise, as the actual benefits that would be generated from the process is mitigated.

However, in this scenario company has to incur losses from premiums, which can have

negative impact on their cash flow conditions.

5. Furthermore, the use of hedging contract such as futures and options directly require

adequate balances and capital for effectively securing risk involved in investment. This

increases the restrictions on the cash that can be used by the company due to the presence

of hedging contracts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL REPORTING

7

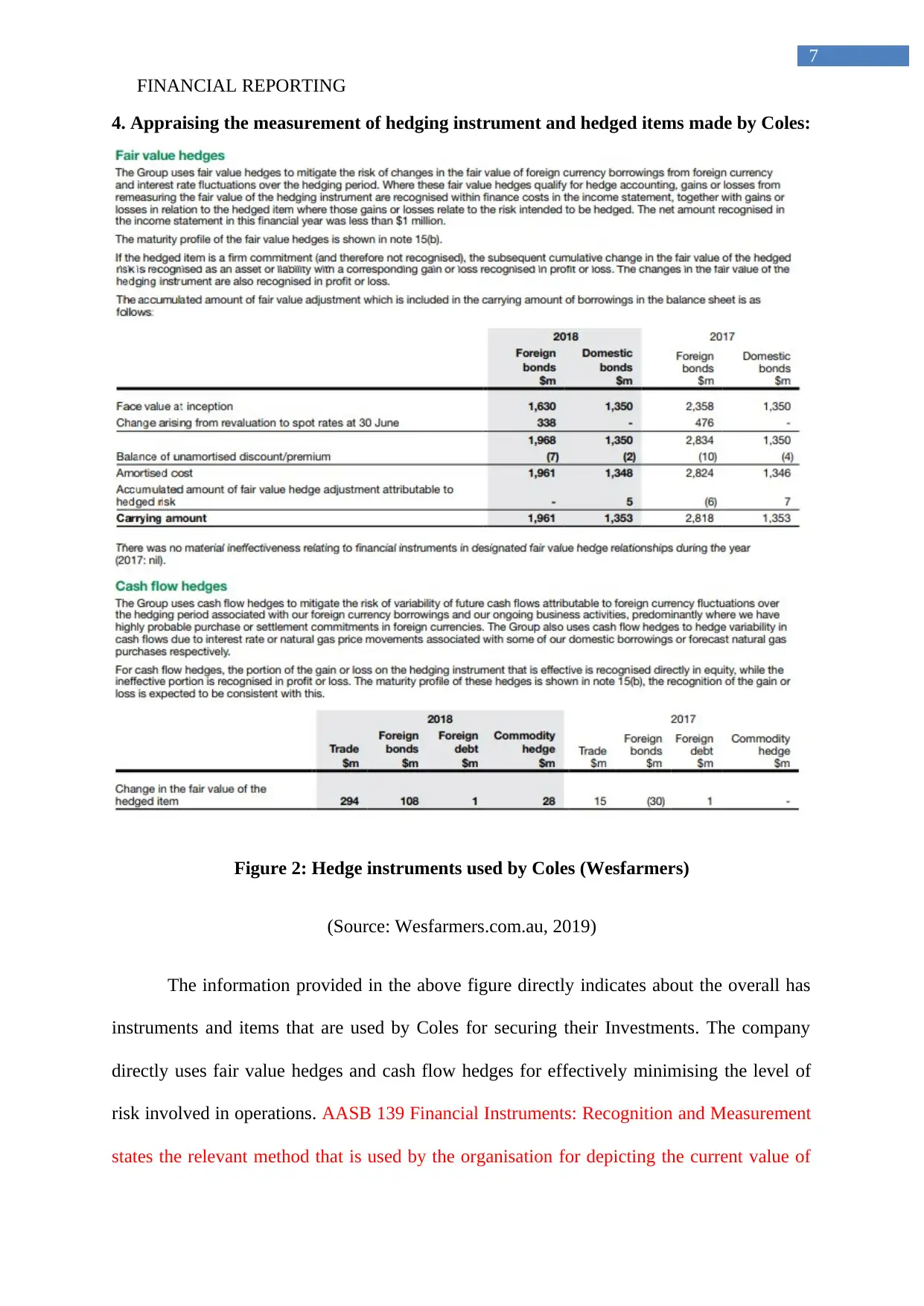

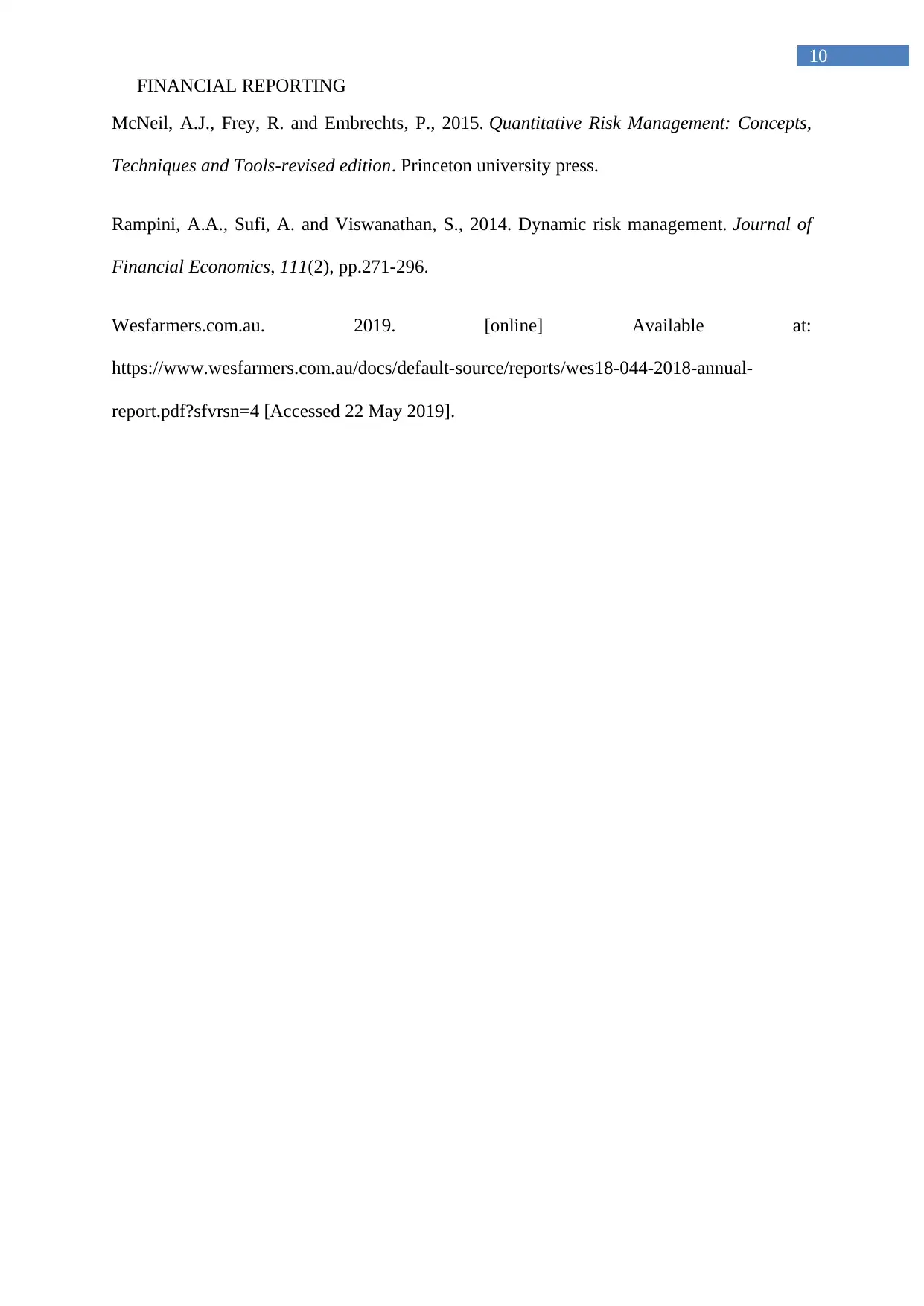

4. Appraising the measurement of hedging instrument and hedged items made by Coles:

Figure 2: Hedge instruments used by Coles (Wesfarmers)

(Source: Wesfarmers.com.au, 2019)

The information provided in the above figure directly indicates about the overall has

instruments and items that are used by Coles for securing their Investments. The company

directly uses fair value hedges and cash flow hedges for effectively minimising the level of

risk involved in operations. AASB 139 Financial Instruments: Recognition and Measurement

states the relevant method that is used by the organisation for depicting the current value of

7

4. Appraising the measurement of hedging instrument and hedged items made by Coles:

Figure 2: Hedge instruments used by Coles (Wesfarmers)

(Source: Wesfarmers.com.au, 2019)

The information provided in the above figure directly indicates about the overall has

instruments and items that are used by Coles for securing their Investments. The company

directly uses fair value hedges and cash flow hedges for effectively minimising the level of

risk involved in operations. AASB 139 Financial Instruments: Recognition and Measurement

states the relevant method that is used by the organisation for depicting the current value of

FINANCIAL REPORTING

8

the financial instruments. Moreover, from the relevant figure it could be identified that fair

value hedge us relatively segregated into different sections such as foreign bonds and

domestic bonds. Both the sections directly provide adequate agent measure that is used by the

organisation to effectively reduce interest rate risk for Coles. Therefore, with adequate

measuring instruments the company is able to minimise the level of risk involved in foreign

bonds and domestic bonds, as it allows them to mitigate the risk by utilising cross currency

interest rate swaps (Chong, Chang and Tan 2014).

The second hedging instruments that are used by the organization are cash flow

hedges, which relatively minimize the risk from trade, foreign bonds, foreign debt, and

commodity hedge. This relevantly measures the cash flow hedge, which directly helps in

minimizing the level of risk involved in operations and maximizes the profit levels in the

long run. The effective hedging process used by the organization has minimized the level of

risk involved in cash flow hedges and maximizes the overall profit that could be generated

from trade (McNeil, Frey and Embrechts 2015). The trade hedge directly helps in minimizing

the risk involved from International transactions, which is conducted by the company for

securing the risk in their operations. Thus, Coles have maintained adequate hedging process

for securing their operations and minimizing the level of risk involved in operations.

Therefore, with the help of AASB 7, 9, 101, 132 and 139 the organization is able to project

the correct value and presentation of the financial instruments in their annual report.

8

the financial instruments. Moreover, from the relevant figure it could be identified that fair

value hedge us relatively segregated into different sections such as foreign bonds and

domestic bonds. Both the sections directly provide adequate agent measure that is used by the

organisation to effectively reduce interest rate risk for Coles. Therefore, with adequate

measuring instruments the company is able to minimise the level of risk involved in foreign

bonds and domestic bonds, as it allows them to mitigate the risk by utilising cross currency

interest rate swaps (Chong, Chang and Tan 2014).

The second hedging instruments that are used by the organization are cash flow

hedges, which relatively minimize the risk from trade, foreign bonds, foreign debt, and

commodity hedge. This relevantly measures the cash flow hedge, which directly helps in

minimizing the level of risk involved in operations and maximizes the profit levels in the

long run. The effective hedging process used by the organization has minimized the level of

risk involved in cash flow hedges and maximizes the overall profit that could be generated

from trade (McNeil, Frey and Embrechts 2015). The trade hedge directly helps in minimizing

the risk involved from International transactions, which is conducted by the company for

securing the risk in their operations. Thus, Coles have maintained adequate hedging process

for securing their operations and minimizing the level of risk involved in operations.

Therefore, with the help of AASB 7, 9, 101, 132 and 139 the organization is able to project

the correct value and presentation of the financial instruments in their annual report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL REPORTING

9

Reference and Bibliography:

Bandaly, D., Satir, A. and Shanker, L., 2014. Integrated supply chain risk management via

operational methods and financial instruments. International Journal of Production

Research, 52(7), pp.2007-2025.

Berghöfer, B. and Lucey, B., 2014. Fuel hedging, operational hedging and risk exposure—

Evidence from the global airline industry. International Review of Financial Analysis, 34,

pp.124-139.

Bessis, J., 2015. Risk management in banking. John Wiley & Sons.

Boroumand, R.H., Goutte, S., Porcher, S. and Porcher, T., 2015. Hedging strategies in energy

markets: the case of electricity retailers. Energy Economics, 51, pp.503-509.

Cairns, A.J., Dowd, K., Blake, D. and Coughlan, G.D., 2014. Longevity hedge effectiveness:

A decomposition. Quantitative Finance, 14(2), pp.217-235.

Chong, L.L., Chang, X.J. and Tan, S.H., 2014. Determinants of corporate foreign exchange

risk hedging. Managerial Finance, 40(2), pp.176-188.

Kumar, D., 2014. Return and volatility transmission between gold and stock sectors:

Application of portfolio management and hedging effectiveness. IIMB Management

Review, 26(1), pp.5-16.

Lievenbrück, M. and Schmid, T., 2014. Why do firms (not) hedge?—Novel evidence on

cultural influence. Journal of Corporate Finance, 25, pp.92-106.

Linnerooth-Bayer, J. and Hochrainer-Stigler, S., 2015. Financial instruments for disaster risk

management and climate change adaptation. Climatic Change, 133(1), pp.85-100.

9

Reference and Bibliography:

Bandaly, D., Satir, A. and Shanker, L., 2014. Integrated supply chain risk management via

operational methods and financial instruments. International Journal of Production

Research, 52(7), pp.2007-2025.

Berghöfer, B. and Lucey, B., 2014. Fuel hedging, operational hedging and risk exposure—

Evidence from the global airline industry. International Review of Financial Analysis, 34,

pp.124-139.

Bessis, J., 2015. Risk management in banking. John Wiley & Sons.

Boroumand, R.H., Goutte, S., Porcher, S. and Porcher, T., 2015. Hedging strategies in energy

markets: the case of electricity retailers. Energy Economics, 51, pp.503-509.

Cairns, A.J., Dowd, K., Blake, D. and Coughlan, G.D., 2014. Longevity hedge effectiveness:

A decomposition. Quantitative Finance, 14(2), pp.217-235.

Chong, L.L., Chang, X.J. and Tan, S.H., 2014. Determinants of corporate foreign exchange

risk hedging. Managerial Finance, 40(2), pp.176-188.

Kumar, D., 2014. Return and volatility transmission between gold and stock sectors:

Application of portfolio management and hedging effectiveness. IIMB Management

Review, 26(1), pp.5-16.

Lievenbrück, M. and Schmid, T., 2014. Why do firms (not) hedge?—Novel evidence on

cultural influence. Journal of Corporate Finance, 25, pp.92-106.

Linnerooth-Bayer, J. and Hochrainer-Stigler, S., 2015. Financial instruments for disaster risk

management and climate change adaptation. Climatic Change, 133(1), pp.85-100.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL REPORTING

10

McNeil, A.J., Frey, R. and Embrechts, P., 2015. Quantitative Risk Management: Concepts,

Techniques and Tools-revised edition. Princeton university press.

Rampini, A.A., Sufi, A. and Viswanathan, S., 2014. Dynamic risk management. Journal of

Financial Economics, 111(2), pp.271-296.

Wesfarmers.com.au. 2019. [online] Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/wes18-044-2018-annual-

report.pdf?sfvrsn=4 [Accessed 22 May 2019].

10

McNeil, A.J., Frey, R. and Embrechts, P., 2015. Quantitative Risk Management: Concepts,

Techniques and Tools-revised edition. Princeton university press.

Rampini, A.A., Sufi, A. and Viswanathan, S., 2014. Dynamic risk management. Journal of

Financial Economics, 111(2), pp.271-296.

Wesfarmers.com.au. 2019. [online] Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/wes18-044-2018-annual-

report.pdf?sfvrsn=4 [Accessed 22 May 2019].

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.