Financial Principles and Techniques: Innovetec Ltd Case Study Report

VerifiedAdded on 2020/01/21

|24

|7571

|176

Report

AI Summary

This report examines the financial principles and techniques applied to Innovetec Ltd. It begins by analyzing the importance of costing in pricing strategies, designing a cost system, and exploring cost reduction ideas, including the potential use of activity-based costing. The report then delves into sources of finance, forecasting techniques for cost estimation, and budgeting processes, including variance analysis and budgetary monitoring. Investment appraisal techniques like payback period and net present value are calculated and recommendations are provided. Finally, the report includes a comparative analysis of financial statements from Tesco Plc and Sainsbury, offering recommendations and discussing the limitations of relying solely on financial information for decision-making. The report covers various aspects of financial management, providing a comprehensive overview of Innovetec Ltd's financial strategies and performance.

MANAGING FINANCIAL

PRINCIPLES AND

TECHNIQUES

PRINCIPLES AND

TECHNIQUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

ACTIVITY 1..............................................................................................................................1

1.1 Importance of costing in to pricing strategy of Innovetec ltd.....................................1

1.2 & 4.1 Designing a cost system for Innovetec ltd and cost reduction ideas regarding

same..................................................................................................................................3

4.2 Potential use of activity based costing for Innovetec ltd............................................4

2.2 Sources of finance for Innovetec................................................................................5

ACTIVITY 2..............................................................................................................................6

2.1 & 3.1 Forecasting technique to estimate cost and expected return and setting a

budgetary target for an organization.................................................................................6

3.2 Budgeted cash flow for first six months.....................................................................7

3.3 Reasons due to variance comes when budget is compared with actual results..........8

3.2 Budgetary monitoring process....................................................................................8

Tasks 5.1 Calculation of Pay-back period and net present value...................................10

AC 5.2 Recommendations..............................................................................................12

AC 5.3 Commercial factors relevant to the investment decisions..................................12

ACTIVITY 4............................................................................................................................13

Comparative analysis of the company's financial statements........................................18

Recommendations...........................................................................................................19

AC 6.3 Limitations of decisions that are based on financial information only..............20

CONCLUSION........................................................................................................................20

REFERENCES.........................................................................................................................22

INDEX OF TABLES

Table 1: Mater budget................................................................................................................6

Table 2: Calculation of profits and cash flows...........................................................................8

Table 3: Calculation of profits and cash flows...........................................................................9

Table 4: Calcualtion of NPV....................................................................................................10

Table 5: Ratio analysis of Sainsbury........................................................................................13

Table 6: Ratio analysis of Tesco Plc .......................................................................................14

INTRODUCTION......................................................................................................................1

ACTIVITY 1..............................................................................................................................1

1.1 Importance of costing in to pricing strategy of Innovetec ltd.....................................1

1.2 & 4.1 Designing a cost system for Innovetec ltd and cost reduction ideas regarding

same..................................................................................................................................3

4.2 Potential use of activity based costing for Innovetec ltd............................................4

2.2 Sources of finance for Innovetec................................................................................5

ACTIVITY 2..............................................................................................................................6

2.1 & 3.1 Forecasting technique to estimate cost and expected return and setting a

budgetary target for an organization.................................................................................6

3.2 Budgeted cash flow for first six months.....................................................................7

3.3 Reasons due to variance comes when budget is compared with actual results..........8

3.2 Budgetary monitoring process....................................................................................8

Tasks 5.1 Calculation of Pay-back period and net present value...................................10

AC 5.2 Recommendations..............................................................................................12

AC 5.3 Commercial factors relevant to the investment decisions..................................12

ACTIVITY 4............................................................................................................................13

Comparative analysis of the company's financial statements........................................18

Recommendations...........................................................................................................19

AC 6.3 Limitations of decisions that are based on financial information only..............20

CONCLUSION........................................................................................................................20

REFERENCES.........................................................................................................................22

INDEX OF TABLES

Table 1: Mater budget................................................................................................................6

Table 2: Calculation of profits and cash flows...........................................................................8

Table 3: Calculation of profits and cash flows...........................................................................9

Table 4: Calcualtion of NPV....................................................................................................10

Table 5: Ratio analysis of Sainsbury........................................................................................13

Table 6: Ratio analysis of Tesco Plc .......................................................................................14

INTRODUCTION

Finance plays a very important role in the organization success. Every organization is

required to have adequate availability of funds to run the business operations in a possible

manner. The present report will helps us in identifying the finance sources available to the

Innovetec Company. Further, cost and pricing decisions and its role in the business success

are also analysed in this report. Moreover, the budgeting process, preparation of budget and

variance analysis also has taken place. Variance is computed through identifying the

difference between actual and budgeted results. It helps to take effective business decisions.

In addition to it, different investment appraisal techniques such as payback period method

and net present value method also discuss in this report. At the end of the report financial

statements are analysed of two retail sector companies Tesco Plc and Sainsbury so as to take

decisions for making investment.

ACTIVITY 1

1.1 Importance of costing in to pricing strategy of Innovetec ltd.

Costing plays a very important role in the pricing strategy of the firm. This is because

it is the cost by using which any firm determines its own pricing strategy. With change in cost

firm pricing strategy also change. If any firm adopt a cost control measures then its cost of

production of reduced. Consequently it’s also change its pricing strategy. Thus, it can be said

that cost has a very high importance to the pricing strategy of the firm. In highly competitive

business environment it becomes necessary for the firms to give stiff competition to the

competitors. Innovetec is operating in market in which there are many competitors which are

offering innovative products at a low price in comparison to features (Abernethy, Lillis,

Brownell and Carter, 2001). Hence, Innovetec is going to launch a new mobile which is

totally different in features and it also needs to launch its product at low price in order to

make its product acceptable in the market. Hence, this target indicates that cost has a due

importance in the pricing strategy of Innovetec ltd pricing strategy. In order to reduce cost

firm needs to generate economies of scale. It can be generated by using supply chain

management techniques and cost concepts. Economies of scale refer to saving in cost that

comes in existence due to purchase of raw material in bulk or implementing any cost

reduction technique in an organization (Attwell and Laughlin, 2001). According to

economics as a discipline total cost is a combination of variable and fixed cost. Fixed cost

refers to the cost that does not get changed with change in production. On other hand,

variable cost is a cost that changes with change in a production. This means that if production

Finance plays a very important role in the organization success. Every organization is

required to have adequate availability of funds to run the business operations in a possible

manner. The present report will helps us in identifying the finance sources available to the

Innovetec Company. Further, cost and pricing decisions and its role in the business success

are also analysed in this report. Moreover, the budgeting process, preparation of budget and

variance analysis also has taken place. Variance is computed through identifying the

difference between actual and budgeted results. It helps to take effective business decisions.

In addition to it, different investment appraisal techniques such as payback period method

and net present value method also discuss in this report. At the end of the report financial

statements are analysed of two retail sector companies Tesco Plc and Sainsbury so as to take

decisions for making investment.

ACTIVITY 1

1.1 Importance of costing in to pricing strategy of Innovetec ltd.

Costing plays a very important role in the pricing strategy of the firm. This is because

it is the cost by using which any firm determines its own pricing strategy. With change in cost

firm pricing strategy also change. If any firm adopt a cost control measures then its cost of

production of reduced. Consequently it’s also change its pricing strategy. Thus, it can be said

that cost has a very high importance to the pricing strategy of the firm. In highly competitive

business environment it becomes necessary for the firms to give stiff competition to the

competitors. Innovetec is operating in market in which there are many competitors which are

offering innovative products at a low price in comparison to features (Abernethy, Lillis,

Brownell and Carter, 2001). Hence, Innovetec is going to launch a new mobile which is

totally different in features and it also needs to launch its product at low price in order to

make its product acceptable in the market. Hence, this target indicates that cost has a due

importance in the pricing strategy of Innovetec ltd pricing strategy. In order to reduce cost

firm needs to generate economies of scale. It can be generated by using supply chain

management techniques and cost concepts. Economies of scale refer to saving in cost that

comes in existence due to purchase of raw material in bulk or implementing any cost

reduction technique in an organization (Attwell and Laughlin, 2001). According to

economics as a discipline total cost is a combination of variable and fixed cost. Fixed cost

refers to the cost that does not get changed with change in production. On other hand,

variable cost is a cost that changes with change in a production. This means that if production

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

will increase then variable cost will also increase vice-verse. So, most of the firm increase

their production level up to certain limit in order to reduce variable cost to maximum level

(Definition of economies of scale. 2015). Hence, as production increase variable cost of the

firm decline but fixed cost remain same. Due to this reason cost of production also reduced.

Apart from this, firm can make change in its supply management strategies. This will help

firm in reducing its transportation or logistics cost (Blocher, Chen and Lin, 2008). Due to

adoption of these measures cost of production per unit will be reduced for then firm. Hence, it

can be said that Innovetec ltd can adopt these techniques in order to reduce its production

cost.

2 | P a g e

their production level up to certain limit in order to reduce variable cost to maximum level

(Definition of economies of scale. 2015). Hence, as production increase variable cost of the

firm decline but fixed cost remain same. Due to this reason cost of production also reduced.

Apart from this, firm can make change in its supply management strategies. This will help

firm in reducing its transportation or logistics cost (Blocher, Chen and Lin, 2008). Due to

adoption of these measures cost of production per unit will be reduced for then firm. Hence, it

can be said that Innovetec ltd can adopt these techniques in order to reduce its production

cost.

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2 & 4.1 Designing a cost system for Innovetec ltd and cost reduction ideas regarding same

Cost system refers to the process which a firm is using to compute cost of production

for its products. A costing system is mainly used by the management to monitor their cost of

production. It is also used to ensure that cost is incurred in line to the standards determined by

the management. In management accounting there are several costing systems and some of

them are as follows

1. Job order costing- This cost system is used when a firm is producing a multiple

products. In this costing system separate cost is prepared for each and every product

line. Firms mostly use this costing system when its multiple products produced are

different from each other on usage and features (Cagwin and Bouwman, 2002). This

costing system is also used when firm is receiving orders for production of goods. In

other words, it can be said that mentioned costing system is used by the firm when

they receive order for production of specific quantity of goods from various clients.

Due to this unique feature mentioned costing system is widely used by the business

firms.

2. Process costing- This costing system is entirely different from batch costing because

in this mode of costing on process basis cost of production is determined. Means that

for producing a specific product many steps are performed (Dey, 2006). So in this

costing system cost of each and every step of production is considered for computing

final cost of production. In this costing system cost of production is determined in a

legitimate manner and due to this reason this method of costing is popular among

manufacturing firms.

3. Traditional costing system- This is old method of costing under which a rate is used

to determine cost of production. Means that different departments are involved in the

production process. So rate is determined for each of these departments and by suing

same cost of each department is determined by the cost manager. This feature is major

limitation of the costing system. With change in business environment cost of raw

material also changed (Drexler, Black and Sparks, 2013). These changes taken place

overnight. But overnight it is difficult to determine new rates of costing for each

department. Due to determination of wrong percentage wrong cost will be calculated

and due to this reason firm may face heavy loss in the business. Hence, due to this

limitation this technique is not used by the companies at the workplace.

3 | P a g e

Cost system refers to the process which a firm is using to compute cost of production

for its products. A costing system is mainly used by the management to monitor their cost of

production. It is also used to ensure that cost is incurred in line to the standards determined by

the management. In management accounting there are several costing systems and some of

them are as follows

1. Job order costing- This cost system is used when a firm is producing a multiple

products. In this costing system separate cost is prepared for each and every product

line. Firms mostly use this costing system when its multiple products produced are

different from each other on usage and features (Cagwin and Bouwman, 2002). This

costing system is also used when firm is receiving orders for production of goods. In

other words, it can be said that mentioned costing system is used by the firm when

they receive order for production of specific quantity of goods from various clients.

Due to this unique feature mentioned costing system is widely used by the business

firms.

2. Process costing- This costing system is entirely different from batch costing because

in this mode of costing on process basis cost of production is determined. Means that

for producing a specific product many steps are performed (Dey, 2006). So in this

costing system cost of each and every step of production is considered for computing

final cost of production. In this costing system cost of production is determined in a

legitimate manner and due to this reason this method of costing is popular among

manufacturing firms.

3. Traditional costing system- This is old method of costing under which a rate is used

to determine cost of production. Means that different departments are involved in the

production process. So rate is determined for each of these departments and by suing

same cost of each department is determined by the cost manager. This feature is major

limitation of the costing system. With change in business environment cost of raw

material also changed (Drexler, Black and Sparks, 2013). These changes taken place

overnight. But overnight it is difficult to determine new rates of costing for each

department. Due to determination of wrong percentage wrong cost will be calculated

and due to this reason firm may face heavy loss in the business. Hence, due to this

limitation this technique is not used by the companies at the workplace.

3 | P a g e

4. Activity based costing- This is unique costing system in which cost of each and every

activity performed for producing specific product is determined by the cost

accountant. After identification of activity cost for each and every activity that is

performed in production process is determined by the managers. Cost for these

activities is determined on the basis of use of resource done by these departments.

On the basis of evaluation of these costing system it can be said that activity based costing is

better for the firm (Garrison, Noreen and Brewer, 2003). This is because in mobile

manufacturing several tasks are performed in sequence. Hence, by determining cost of all

these activities cost of production can be determined. Hence, it can be said that this costing

system will be suitable for Innovetec ltd.

There are many ways that can be adopted in order to reduce cost. Some of them are as

follows.

Analysis of activities- In activity based costing several activities are performed. In

this method of cost reduction each and every activity will be analyzed. Main focus

will be on identifying sub unproductive task in each activity. Elimination of these

activities from production process will reduce both time and cost for the firm. In this

way cost of production will be reduced for the firm (Healy, 2002).

Management audit- It is a technique in which top managers analyse costs where firm

makes extravagance. After identification of such kind of costs managers identify the

reason due to which these over expenses co0mes in to existence. After identification

of reasons management identify the ways that can be adopted in order to prevent

repetition of such kind of mistakes (Horngren and et.al, 2002). Hence, this technique

is also very effective in cost control.

4.2 Potential use of activity based costing for Innovetec ltd

There are many uses of activity based costing and due to this reason this method is

widely used by the business firms. This technique compute cost of production in proper

manner in comparison to other costing techniques. This is because for producing goods

resources are required and these resources may be people working in an organization and

resources that are used for producing goods at the workplace (Huber, 2011). Basically

resources are used for producing goods and computation of their cost directly helps firms in

calculating cost of production. So, due to this reason this method of costing is assumed better

than other costing techniques. On other hand, by analyzing previous months activity based

4 | P a g e

activity performed for producing specific product is determined by the cost

accountant. After identification of activity cost for each and every activity that is

performed in production process is determined by the managers. Cost for these

activities is determined on the basis of use of resource done by these departments.

On the basis of evaluation of these costing system it can be said that activity based costing is

better for the firm (Garrison, Noreen and Brewer, 2003). This is because in mobile

manufacturing several tasks are performed in sequence. Hence, by determining cost of all

these activities cost of production can be determined. Hence, it can be said that this costing

system will be suitable for Innovetec ltd.

There are many ways that can be adopted in order to reduce cost. Some of them are as

follows.

Analysis of activities- In activity based costing several activities are performed. In

this method of cost reduction each and every activity will be analyzed. Main focus

will be on identifying sub unproductive task in each activity. Elimination of these

activities from production process will reduce both time and cost for the firm. In this

way cost of production will be reduced for the firm (Healy, 2002).

Management audit- It is a technique in which top managers analyse costs where firm

makes extravagance. After identification of such kind of costs managers identify the

reason due to which these over expenses co0mes in to existence. After identification

of reasons management identify the ways that can be adopted in order to prevent

repetition of such kind of mistakes (Horngren and et.al, 2002). Hence, this technique

is also very effective in cost control.

4.2 Potential use of activity based costing for Innovetec ltd

There are many uses of activity based costing and due to this reason this method is

widely used by the business firms. This technique compute cost of production in proper

manner in comparison to other costing techniques. This is because for producing goods

resources are required and these resources may be people working in an organization and

resources that are used for producing goods at the workplace (Huber, 2011). Basically

resources are used for producing goods and computation of their cost directly helps firms in

calculating cost of production. So, due to this reason this method of costing is assumed better

than other costing techniques. On other hand, by analyzing previous months activity based

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

costing data managers can identify resources whose consumption is increasing, decreasing or

remain stable in the production. Hence, on the basis of analysis of these trends managers gets

lots of information (Kaplan and Atkinson, 2015). They also get a direction on which they

need to work in order to control cost of production. So, it can be said that this costing

technique has a varied use for the business firms.

2.2 Sources of finance for Innovetec

There are many sources of finance and these sources may be divided in to two

categories one is internal and second is external sources of finance. These categories of

sources of finance are described below.

Internal sources of finance Retained earnings- It is a part of profit that remains after paying all expenses from

the revenue. There is cost of this source of finance and due to this reason this source

of finance is widely used by the firms. Sale of asset- Sale of asset is another common internal source of finance that is

widely used by the firms when an asset is not generating sufficient returns for the firm

or it remain idle for the firm for long time period (Kaplan and Schoar, 2005). There is

not cost of this source of finance which is major reason due to popularity as a source

of finance among large corporations.

External source of finance Equity- Under this source of finance firm raised a capital from the market by bringing

IPO or FPO. For doing this it needs to pass some criteria that are determined by the

recognized stock exchange. In this source of finance cost can be adjusted and due to

this reason this source of finance is widely used by the firms. Debentures – It is a written acknowledgment of debt taken by the firm from the

public. In return firm need to pay interest to the debenture holders. In this source of

finance, finance cost cannot be adjusted (Kennedy and Affleck-Graves, 2001). Due to

this reason equity is mainly prefer above debentures.

Hire purchase agreement- Under this agreement firm takes an asset on lease. It pay

lease amount on regular interval. If lease amount cumulatively become equivalent to

the price of the leased asset then it is amused to be purchased by the lessee (Koltai

and et.al, 2000). So, it can be said that in this source of finance by making payment in

instalments an asset can be purchased by the firm.

5 | P a g e

remain stable in the production. Hence, on the basis of analysis of these trends managers gets

lots of information (Kaplan and Atkinson, 2015). They also get a direction on which they

need to work in order to control cost of production. So, it can be said that this costing

technique has a varied use for the business firms.

2.2 Sources of finance for Innovetec

There are many sources of finance and these sources may be divided in to two

categories one is internal and second is external sources of finance. These categories of

sources of finance are described below.

Internal sources of finance Retained earnings- It is a part of profit that remains after paying all expenses from

the revenue. There is cost of this source of finance and due to this reason this source

of finance is widely used by the firms. Sale of asset- Sale of asset is another common internal source of finance that is

widely used by the firms when an asset is not generating sufficient returns for the firm

or it remain idle for the firm for long time period (Kaplan and Schoar, 2005). There is

not cost of this source of finance which is major reason due to popularity as a source

of finance among large corporations.

External source of finance Equity- Under this source of finance firm raised a capital from the market by bringing

IPO or FPO. For doing this it needs to pass some criteria that are determined by the

recognized stock exchange. In this source of finance cost can be adjusted and due to

this reason this source of finance is widely used by the firms. Debentures – It is a written acknowledgment of debt taken by the firm from the

public. In return firm need to pay interest to the debenture holders. In this source of

finance, finance cost cannot be adjusted (Kennedy and Affleck-Graves, 2001). Due to

this reason equity is mainly prefer above debentures.

Hire purchase agreement- Under this agreement firm takes an asset on lease. It pay

lease amount on regular interval. If lease amount cumulatively become equivalent to

the price of the leased asset then it is amused to be purchased by the lessee (Koltai

and et.al, 2000). So, it can be said that in this source of finance by making payment in

instalments an asset can be purchased by the firm.

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACTIVITY 2

2.1 & 3.1 Forecasting technique to estimate cost and expected return and setting a budgetary

target for an organization

Forecasting technique that Innovetec can use in the business is as follows. Cash flow forecast – In order to estimate cost and revenue for upcoming time period

technique of preparing a cash flow statement can be used by the Innovetec. Under this

technique a projection for cost and revenue is prepared. For this a technique of

financial modelling is used by the firm in which by using old data forecast for

upcoming month or year is prepared by the finance manager. In order to predict

output economic environment is analyzed by using economic data like GDP, IIP and

PMI. On the basis of output estimation revenue amount is envisaged by the firm (Lee,

Ellenbecker and Moure-Ersaso, 2004). After that first old data is taken and some

calculations regarding same is done. Cost covers a fixed percentage of sales. Even

sales increase or decrease this proportion remains same. Hence, in this technique

Innovetec will use revenue that it computes in early stage. After doing this it will use

cost percentage that was determined by doing calculation on old data to compute or

predict cost for upcoming time period. In this way cost and revenue will be

determined by the firm under this forecasting technique.

Forecasting prices movement of metals using indices- Innovetec is using metals for

producing mobiles. Thus, change in price of these metals brings changes in the cost of

production of the firm. Due to this reason it becomes necessary for the firm to predict

price changes because it directly affects firm cost and revenue. In order to forecast

changes in price of base metals managers can review change in LME indices of base

metals (Marginson and Ogden, 2005). Changes in the price of these indices will

indicate the direction in which price of these metal may go. In order to confirm this

trend manager can use concept of open interest. It is a terminology that is used in

commodity market. This terminology indicates the number of fresh contracts that are

newly opened in the market. Increase in open interest indicates that fresh money is

introduced in the market. Similarly, decrease in open interest indicates that fresh

money is coming in market at slow pace. Means that in upcoming months price may

fall or grow at a slow rate (Maskell and et.al, 2007). By using such kind of data cost

of raw material can be estimated and by using this cost of raw material will be

determined. On other hand, increase in cost cannot be passed to consumers. Hence,

6 | P a g e

2.1 & 3.1 Forecasting technique to estimate cost and expected return and setting a budgetary

target for an organization

Forecasting technique that Innovetec can use in the business is as follows. Cash flow forecast – In order to estimate cost and revenue for upcoming time period

technique of preparing a cash flow statement can be used by the Innovetec. Under this

technique a projection for cost and revenue is prepared. For this a technique of

financial modelling is used by the firm in which by using old data forecast for

upcoming month or year is prepared by the finance manager. In order to predict

output economic environment is analyzed by using economic data like GDP, IIP and

PMI. On the basis of output estimation revenue amount is envisaged by the firm (Lee,

Ellenbecker and Moure-Ersaso, 2004). After that first old data is taken and some

calculations regarding same is done. Cost covers a fixed percentage of sales. Even

sales increase or decrease this proportion remains same. Hence, in this technique

Innovetec will use revenue that it computes in early stage. After doing this it will use

cost percentage that was determined by doing calculation on old data to compute or

predict cost for upcoming time period. In this way cost and revenue will be

determined by the firm under this forecasting technique.

Forecasting prices movement of metals using indices- Innovetec is using metals for

producing mobiles. Thus, change in price of these metals brings changes in the cost of

production of the firm. Due to this reason it becomes necessary for the firm to predict

price changes because it directly affects firm cost and revenue. In order to forecast

changes in price of base metals managers can review change in LME indices of base

metals (Marginson and Ogden, 2005). Changes in the price of these indices will

indicate the direction in which price of these metal may go. In order to confirm this

trend manager can use concept of open interest. It is a terminology that is used in

commodity market. This terminology indicates the number of fresh contracts that are

newly opened in the market. Increase in open interest indicates that fresh money is

introduced in the market. Similarly, decrease in open interest indicates that fresh

money is coming in market at slow pace. Means that in upcoming months price may

fall or grow at a slow rate (Maskell and et.al, 2007). By using such kind of data cost

of raw material can be estimated and by using this cost of raw material will be

determined. On other hand, increase in cost cannot be passed to consumers. Hence,

6 | P a g e

trends in price change can be used to predict firm revenue. In this way, index helps

firm in determining cost and profit of then firm.

Setting a budgetary target requires determination of cost and revenue of the firm.

Revenue of the firm is directly affected by the economic environment. Hence, change in

economic environment affects revenue of the firm. Due to this reason before preparing a

budget economic environment must be analyzed. On the basis of analysis revenue amount

must be determined in the budget (Mayer, Schoors and Yafeh, 2005). Firm must consider old

budget performance and economic data of GDP, PMI and IIP for estimating accurate amount

of revenue for the budget. By using economic data and previous month cost sheet firm can

estimate cost for the budget. Hence, in this way budgetary target can be set for an

organization.

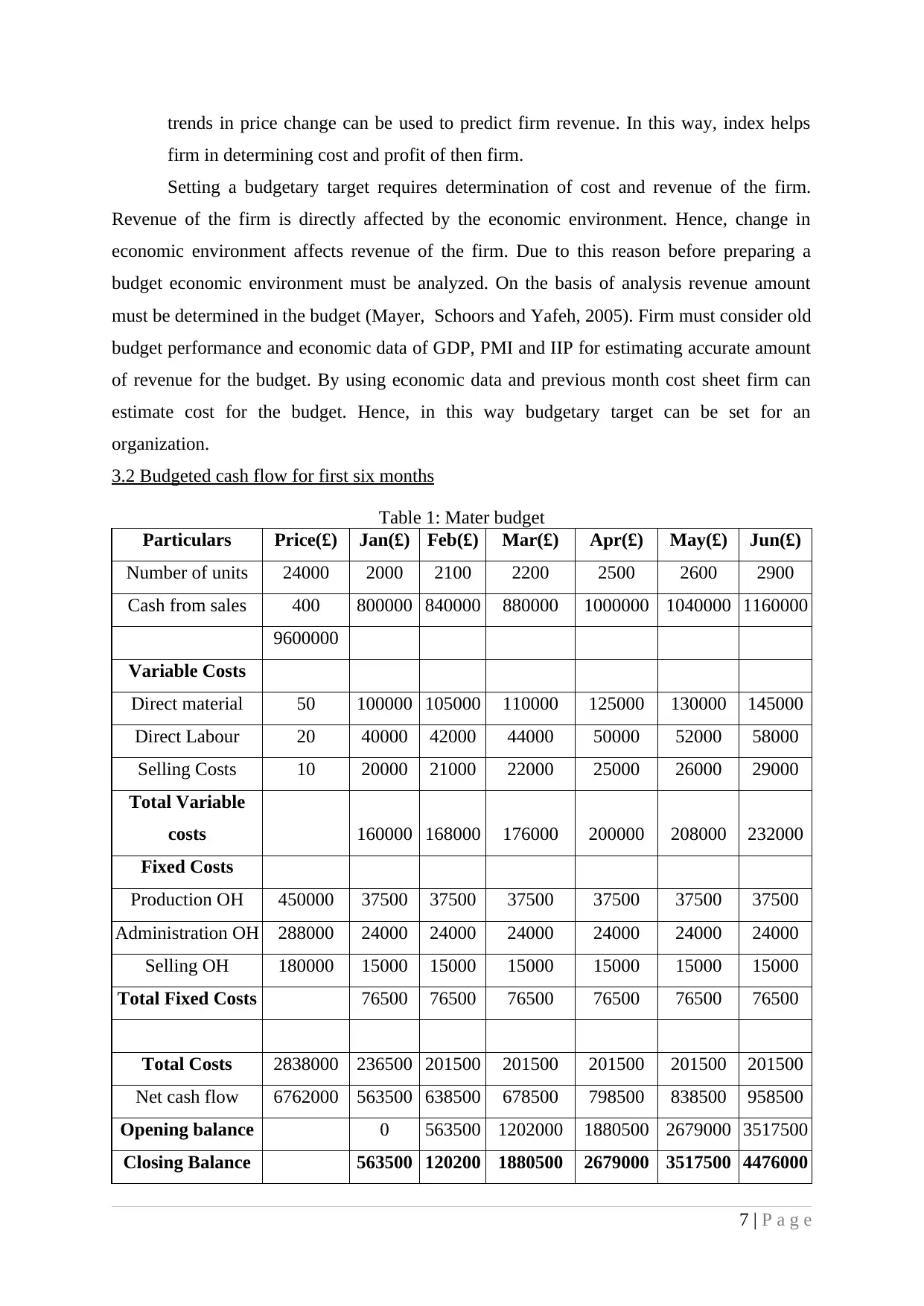

3.2 Budgeted cash flow for first six months

Table 1: Mater budget

Particulars Price(£) Jan(£) Feb(£) Mar(£) Apr(£) May(£) Jun(£)

Number of units 24000 2000 2100 2200 2500 2600 2900

Cash from sales 400 800000 840000 880000 1000000 1040000 1160000

9600000

Variable Costs

Direct material 50 100000 105000 110000 125000 130000 145000

Direct Labour 20 40000 42000 44000 50000 52000 58000

Selling Costs 10 20000 21000 22000 25000 26000 29000

Total Variable

costs 160000 168000 176000 200000 208000 232000

Fixed Costs

Production OH 450000 37500 37500 37500 37500 37500 37500

Administration OH 288000 24000 24000 24000 24000 24000 24000

Selling OH 180000 15000 15000 15000 15000 15000 15000

Total Fixed Costs 76500 76500 76500 76500 76500 76500

Total Costs 2838000 236500 201500 201500 201500 201500 201500

Net cash flow 6762000 563500 638500 678500 798500 838500 958500

Opening balance 0 563500 1202000 1880500 2679000 3517500

Closing Balance 563500 120200 1880500 2679000 3517500 4476000

7 | P a g e

firm in determining cost and profit of then firm.

Setting a budgetary target requires determination of cost and revenue of the firm.

Revenue of the firm is directly affected by the economic environment. Hence, change in

economic environment affects revenue of the firm. Due to this reason before preparing a

budget economic environment must be analyzed. On the basis of analysis revenue amount

must be determined in the budget (Mayer, Schoors and Yafeh, 2005). Firm must consider old

budget performance and economic data of GDP, PMI and IIP for estimating accurate amount

of revenue for the budget. By using economic data and previous month cost sheet firm can

estimate cost for the budget. Hence, in this way budgetary target can be set for an

organization.

3.2 Budgeted cash flow for first six months

Table 1: Mater budget

Particulars Price(£) Jan(£) Feb(£) Mar(£) Apr(£) May(£) Jun(£)

Number of units 24000 2000 2100 2200 2500 2600 2900

Cash from sales 400 800000 840000 880000 1000000 1040000 1160000

9600000

Variable Costs

Direct material 50 100000 105000 110000 125000 130000 145000

Direct Labour 20 40000 42000 44000 50000 52000 58000

Selling Costs 10 20000 21000 22000 25000 26000 29000

Total Variable

costs 160000 168000 176000 200000 208000 232000

Fixed Costs

Production OH 450000 37500 37500 37500 37500 37500 37500

Administration OH 288000 24000 24000 24000 24000 24000 24000

Selling OH 180000 15000 15000 15000 15000 15000 15000

Total Fixed Costs 76500 76500 76500 76500 76500 76500

Total Costs 2838000 236500 201500 201500 201500 201500 201500

Net cash flow 6762000 563500 638500 678500 798500 838500 958500

Opening balance 0 563500 1202000 1880500 2679000 3517500

Closing Balance 563500 120200 1880500 2679000 3517500 4476000

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0

Interpretation

On analysis of budget it can be seen that management think that with passage of time

sales of the firm will increase. Due to this reason it increases its production of goods. With

increase in production cost keeps on changing which is variable in nature. But fixed cost is

same with change in level of output. Due to continue increase in sale and stability in growth

rate of cost of the firm closing balance is increasing. Hence, it can be said that firm is

performing well.

3.3 Reasons due to variance comes when budget is compared with actual results

Mostly it has been seen that when budget is compared with actual results variance

comes in existence. This variance may be positive or negative in nature. It is very difficult to

predict change in economic environment in accurate manner. With change in economic

environment cost of raw material and sales of the firm also get changed. Hence, actual results

do not come in line to budget prepared (Mestry and Naidoo, 2009). If variance is positive

then there is no problem but if variance is negative then management needs to take action

immediately in order to ensure that mistakes will not committed again which was responsible

for variance in the budget.

3.2 Budgetary monitoring process

Following is a process that is followed for monitoring a budget. Determination of standard- In this stage a standard is prepared for the budget. These

standards are determined by the managers by considering various economic data and

company past performance in several business situations (Olawale, Olumuyiwa and

George, 2010). These are use by the firm in later stage in order to identify company

performance. Measurement of performance- After a specific time period performance of the

company is identified on the basis of values or unit. This period may be three months

or a year. Comparison with standard- In this stage actual figures that were identified in earlier

stage is compared with budgeted figures in order to identify that company perform

better or worse.

Taking corrective action- In this stage if variance is negative then corrective actions

are taken in order to make sure that mistakes committed in this stage will not be

committed again in future (Panayotidis, Montesanto. and Orfanidis, 2004).

8 | P a g e

Interpretation

On analysis of budget it can be seen that management think that with passage of time

sales of the firm will increase. Due to this reason it increases its production of goods. With

increase in production cost keeps on changing which is variable in nature. But fixed cost is

same with change in level of output. Due to continue increase in sale and stability in growth

rate of cost of the firm closing balance is increasing. Hence, it can be said that firm is

performing well.

3.3 Reasons due to variance comes when budget is compared with actual results

Mostly it has been seen that when budget is compared with actual results variance

comes in existence. This variance may be positive or negative in nature. It is very difficult to

predict change in economic environment in accurate manner. With change in economic

environment cost of raw material and sales of the firm also get changed. Hence, actual results

do not come in line to budget prepared (Mestry and Naidoo, 2009). If variance is positive

then there is no problem but if variance is negative then management needs to take action

immediately in order to ensure that mistakes will not committed again which was responsible

for variance in the budget.

3.2 Budgetary monitoring process

Following is a process that is followed for monitoring a budget. Determination of standard- In this stage a standard is prepared for the budget. These

standards are determined by the managers by considering various economic data and

company past performance in several business situations (Olawale, Olumuyiwa and

George, 2010). These are use by the firm in later stage in order to identify company

performance. Measurement of performance- After a specific time period performance of the

company is identified on the basis of values or unit. This period may be three months

or a year. Comparison with standard- In this stage actual figures that were identified in earlier

stage is compared with budgeted figures in order to identify that company perform

better or worse.

Taking corrective action- In this stage if variance is negative then corrective actions

are taken in order to make sure that mistakes committed in this stage will not be

committed again in future (Panayotidis, Montesanto. and Orfanidis, 2004).

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

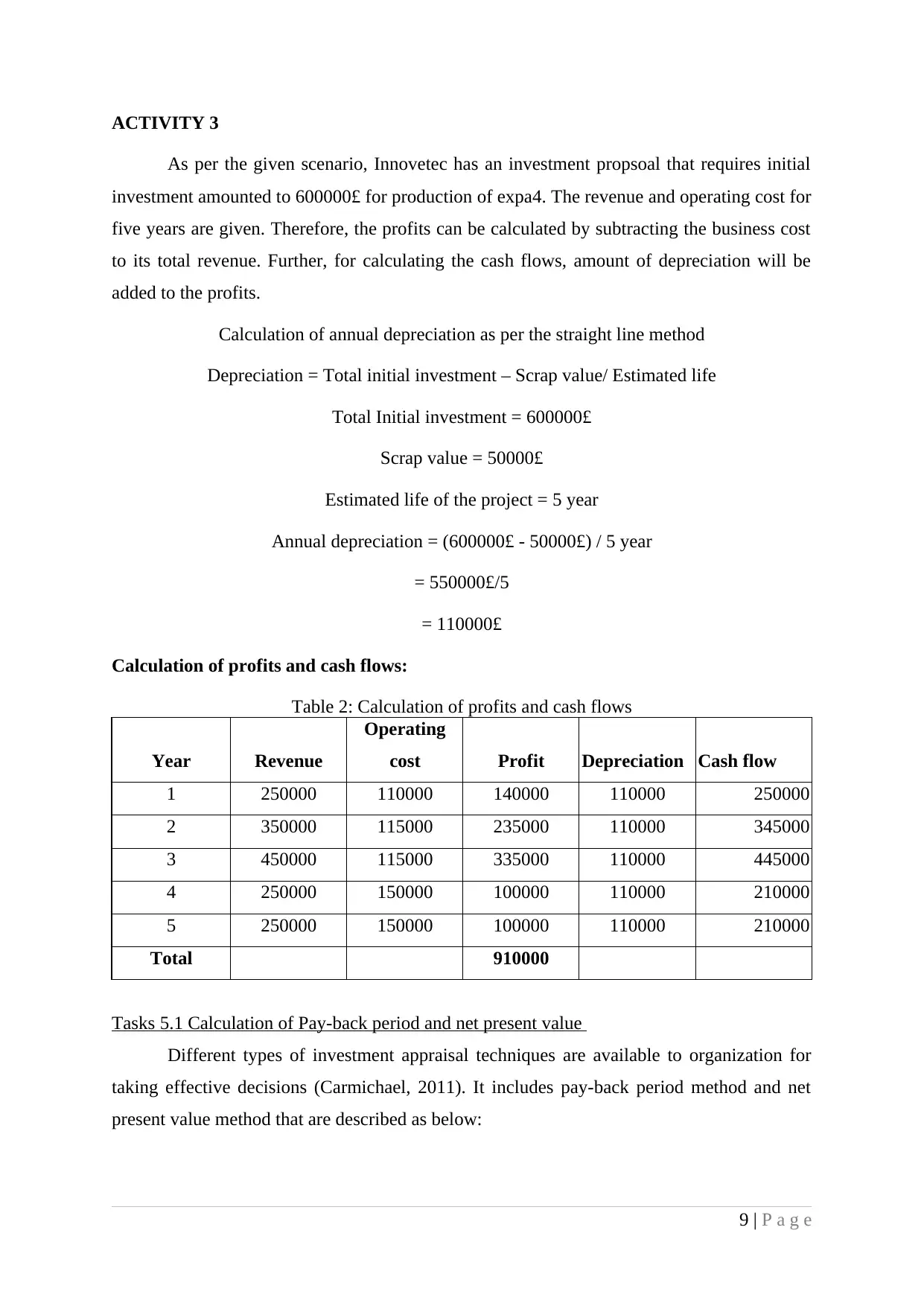

ACTIVITY 3

As per the given scenario, Innovetec has an investment propsoal that requires initial

investment amounted to 600000£ for production of expa4. The revenue and operating cost for

five years are given. Therefore, the profits can be calculated by subtracting the business cost

to its total revenue. Further, for calculating the cash flows, amount of depreciation will be

added to the profits.

Calculation of annual depreciation as per the straight line method

Depreciation = Total initial investment – Scrap value/ Estimated life

Total Initial investment = 600000£

Scrap value = 50000£

Estimated life of the project = 5 year

Annual depreciation = (600000£ - 50000£) / 5 year

= 550000£/5

= 110000£

Calculation of profits and cash flows:

Table 2: Calculation of profits and cash flows

Year Revenue

Operating

cost Profit Depreciation Cash flow

1 250000 110000 140000 110000 250000

2 350000 115000 235000 110000 345000

3 450000 115000 335000 110000 445000

4 250000 150000 100000 110000 210000

5 250000 150000 100000 110000 210000

Total 910000

Tasks 5.1 Calculation of Pay-back period and net present value

Different types of investment appraisal techniques are available to organization for

taking effective decisions (Carmichael, 2011). It includes pay-back period method and net

present value method that are described as below:

9 | P a g e

As per the given scenario, Innovetec has an investment propsoal that requires initial

investment amounted to 600000£ for production of expa4. The revenue and operating cost for

five years are given. Therefore, the profits can be calculated by subtracting the business cost

to its total revenue. Further, for calculating the cash flows, amount of depreciation will be

added to the profits.

Calculation of annual depreciation as per the straight line method

Depreciation = Total initial investment – Scrap value/ Estimated life

Total Initial investment = 600000£

Scrap value = 50000£

Estimated life of the project = 5 year

Annual depreciation = (600000£ - 50000£) / 5 year

= 550000£/5

= 110000£

Calculation of profits and cash flows:

Table 2: Calculation of profits and cash flows

Year Revenue

Operating

cost Profit Depreciation Cash flow

1 250000 110000 140000 110000 250000

2 350000 115000 235000 110000 345000

3 450000 115000 335000 110000 445000

4 250000 150000 100000 110000 210000

5 250000 150000 100000 110000 210000

Total 910000

Tasks 5.1 Calculation of Pay-back period and net present value

Different types of investment appraisal techniques are available to organization for

taking effective decisions (Carmichael, 2011). It includes pay-back period method and net

present value method that are described as below:

9 | P a g e

Pay-back period = It is the time period that the project will take to get an initial investment

of 600000£. Lower the pay-back period of investment, to a high extent, the proposal will be

good for company (Irani, 2010). The pay-back period for the given scenario is calculated here

as under:

Table 3: Calculation of profits and cash flows

10 | P a g e

of 600000£. Lower the pay-back period of investment, to a high extent, the proposal will be

good for company (Irani, 2010). The pay-back period for the given scenario is calculated here

as under:

Table 3: Calculation of profits and cash flows

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.