University Financial Accounting Report: JB HI-FI PPE Analysis 2017

VerifiedAdded on 2021/06/14

|8

|906

|25

Report

AI Summary

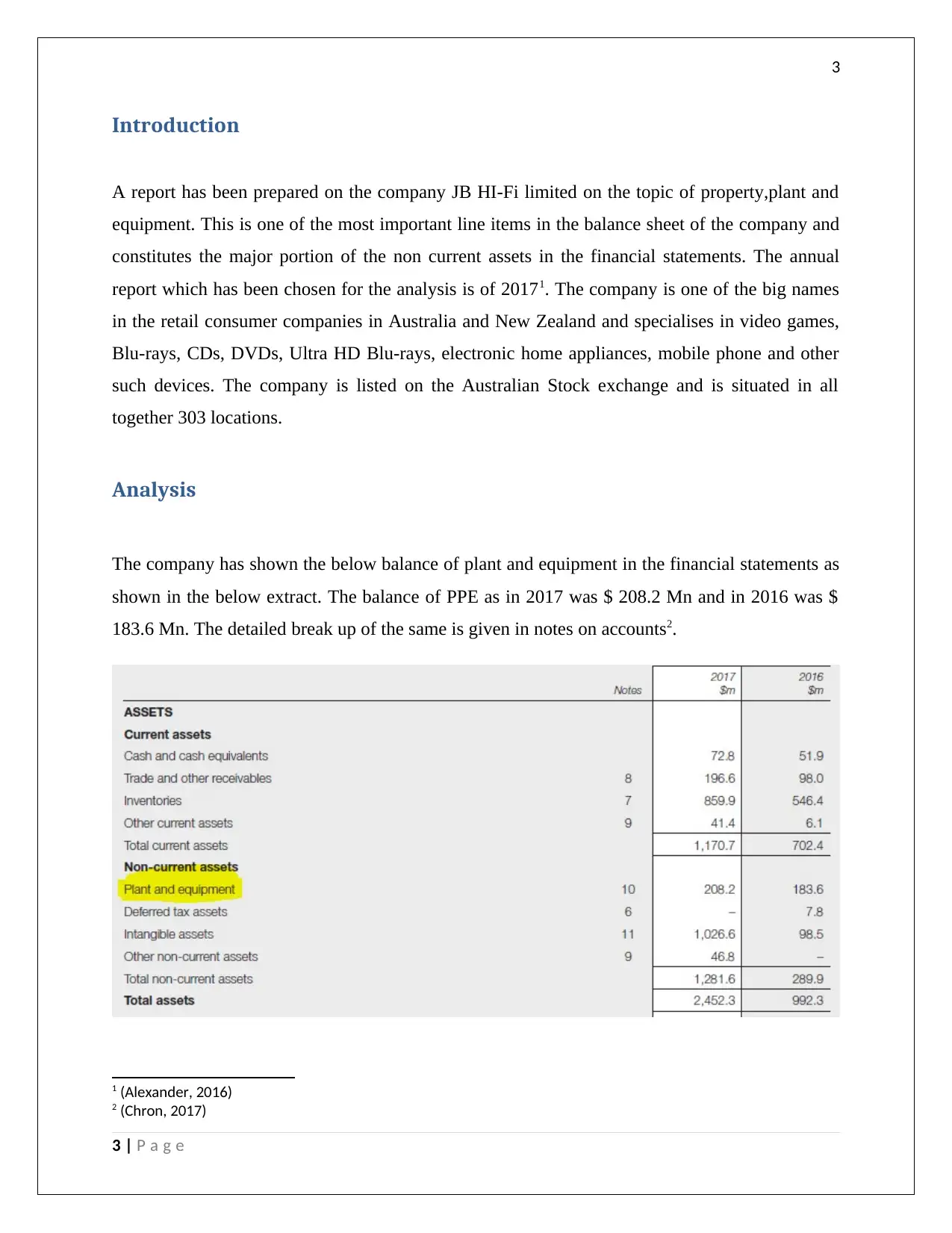

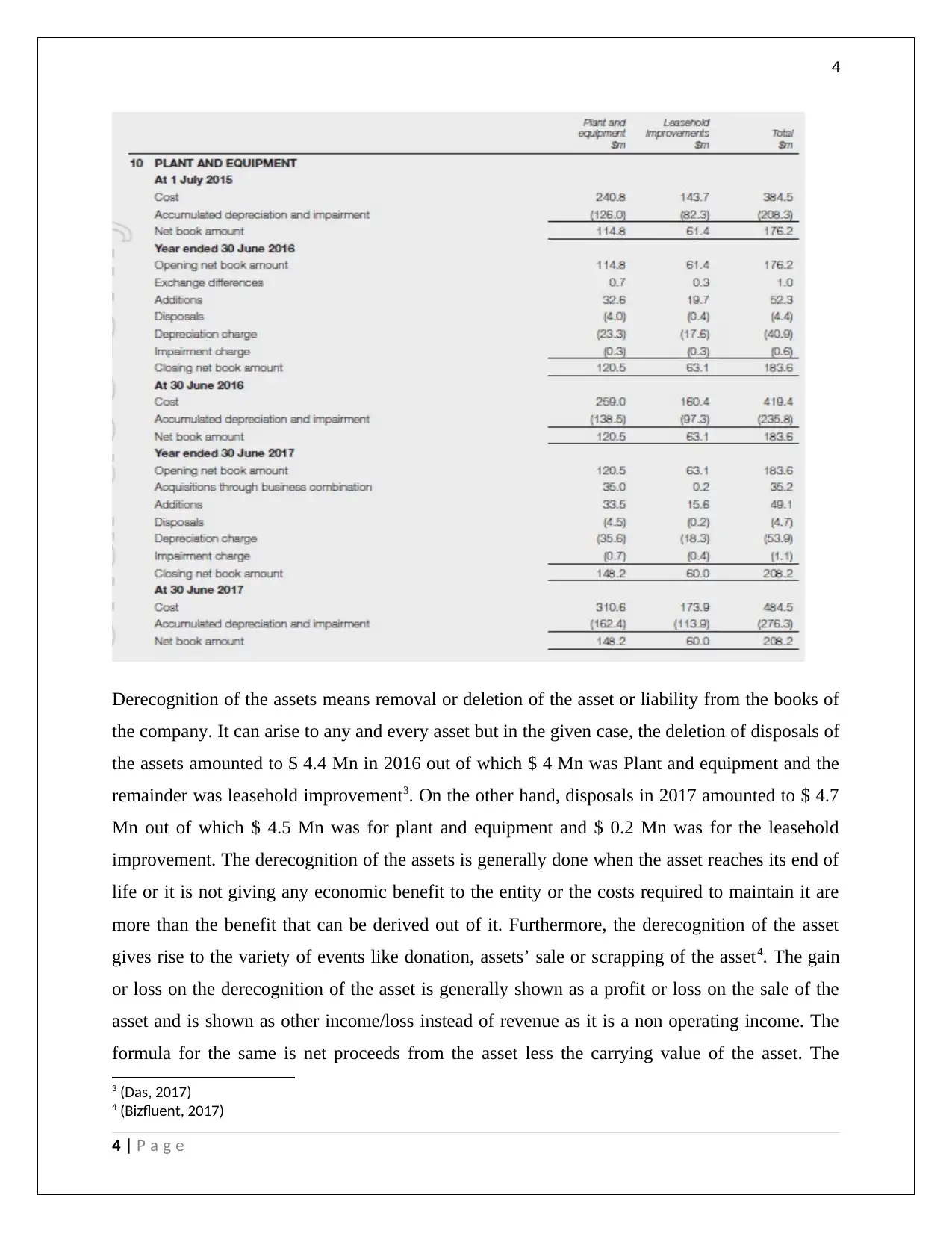

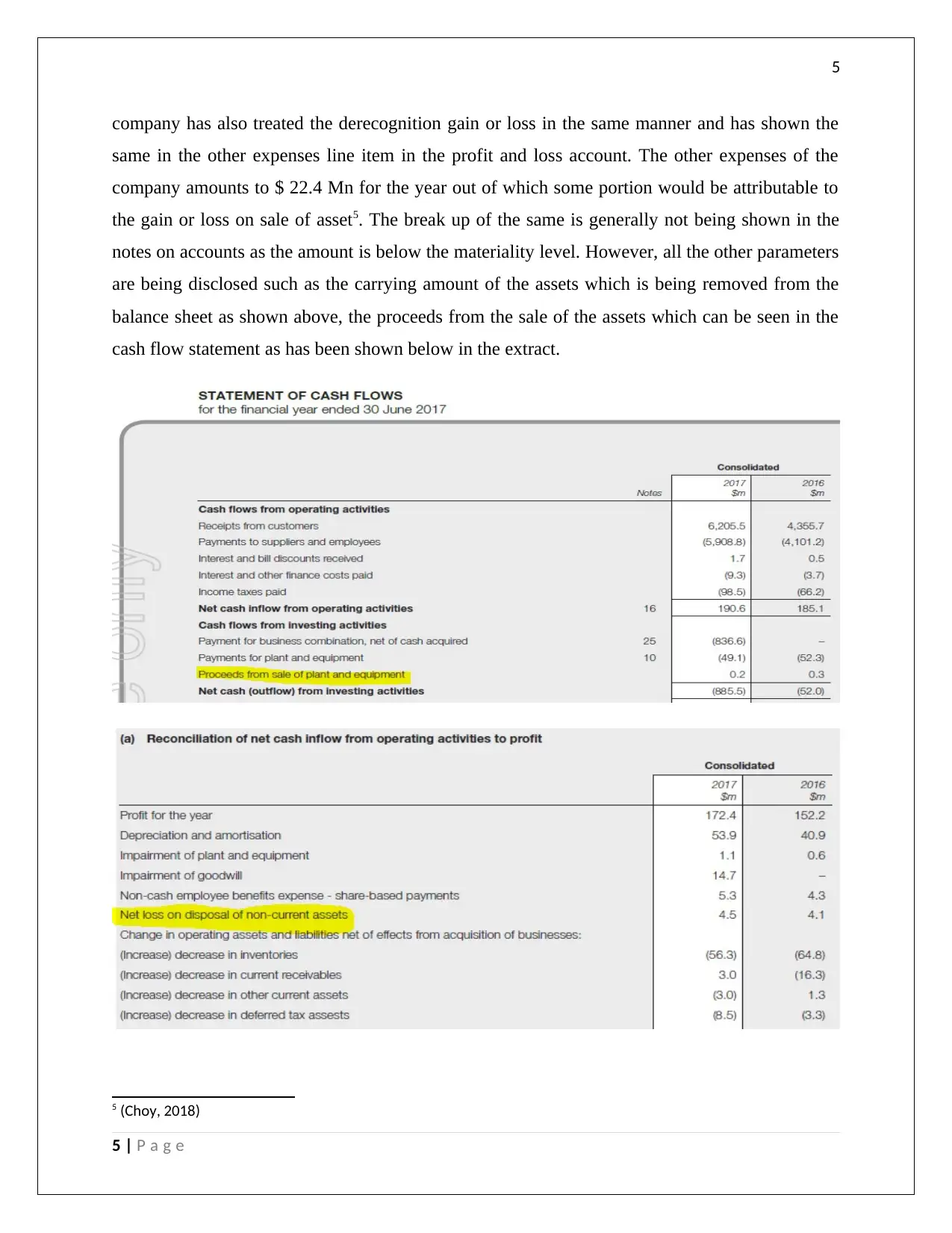

This report provides an analysis of JB HI-FI Limited's financial statements, specifically focusing on property, plant, and equipment (PPE). The report examines the balance of PPE, asset derecognition, and its impact on the financial statements, including the balance sheet, income statement, and cash flow statement. It delves into the company's accounting practices related to the disposal of assets, the recognition of gains and losses, and compliance with GAAP and AASB standards. The analysis includes a breakdown of the financial data from 2016 and 2017, offering insights into the company's financial performance and adherence to accounting principles. The report concludes that JB HI-FI has followed all the rules and guidelines for disclosure of the derecognition gain and loss as per the GAAP and AASB standards, with proper disclosures and workings given in the notes to accounts, the profit and loss statements, the cash flow statement and the balance sheet of the company. The bibliography includes sources used in the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.