Kuafu Hotel Financial Analysis Report: Performance and Ratios

VerifiedAdded on 2023/04/22

|13

|2478

|59

Report

AI Summary

This report presents a comprehensive financial analysis of the Kuafu Hotel, a partnership venture, assessing its financial performance over a three-month period. The analysis includes a detailed examination of the income statement, focusing on sales, cost of sales, and various expenses, revealing negative EBITDA and net profit margins. Ratio analysis is conducted, comparing the hotel's performance against industry standards across profitability, financial stability, and asset utilization metrics. The report also undertakes a variance analysis to identify deviations from the budgeted financials and a CVP (Cost-Volume-Profit) analysis to determine the break-even point and assess the financial stability of the venture. The conclusion highlights the need for financial restructuring, including debt rationalization, increased sales, and cost minimization to ensure the hotel's long-term viability and sustainability, emphasizing the challenges of lower demand, high maintenance costs, and inadequate working capital.

Running Head: FINANCIAL ANALYSIS 0

KUAFU HOTEL

Financial Analysis

System04115

KUAFU HOTEL

Financial Analysis

System04115

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 1

Table of Contents

Introduction................................................................................................................................1

Importance of Financial Analysis..............................................................................................1

Financial Analysis..................................................................................................................1

Ratio Analysis............................................................................................................................3

Assessment of the ratios.........................................................................................................3

Profitability........................................................................................................................3

Financial Stability..............................................................................................................4

Asset utilisation..................................................................................................................4

Variance Analysis......................................................................................................................5

CVP analysis..............................................................................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................9

Table of Contents

Introduction................................................................................................................................1

Importance of Financial Analysis..............................................................................................1

Financial Analysis..................................................................................................................1

Ratio Analysis............................................................................................................................3

Assessment of the ratios.........................................................................................................3

Profitability........................................................................................................................3

Financial Stability..............................................................................................................4

Asset utilisation..................................................................................................................4

Variance Analysis......................................................................................................................5

CVP analysis..............................................................................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................9

FINANCIAL ANALYSIS 2

Introduction

Kuafu Hotel is a partnership venture. It is necessary to understand the reasonableness

of the revenue, cost assumptions and consequently the margins and sustainability check. The

relevant industry benchmarks are studied and applied using research and industry expertise.

This report projects the financial performance of the Company along with the Debt

sustainability Check. The financial analysis helps the members of the venture to take key

decisions and also understand the area that need working. The report discusses various aspect

of the financial such as ratios, the variance analysis and also the breakeven analysis

(Williams & Dobelman, 2017).

Importance of Financial Analysis

The primary reason for any business venture is to earn the profit, so we can find out

the financial position of business with the help of financial statements (Vogel, 2014). The

analysis of financial helps us to find the viability of the business and help the key decision

maker in making an important decision. (Corporate Finance Institute, 2019). The financial

analysis helps us to find that there is a proper allocation of resources. Different financial

analysis carries their own benefit and helps in determining something different such as

financial statement help un-understanding the financial position of the firm, break-even

analysis assists in determining the breakeven point for the firm (Titman et al., 2011).

Financial Analysis

The financial statements allow analysts to measure liquidity, profitability, company-

wide efficiency, and cash flow. There are three main types of financial statements: the

balance sheet, income statement and cash flow statement (Investopedia, 2019).

Introduction

Kuafu Hotel is a partnership venture. It is necessary to understand the reasonableness

of the revenue, cost assumptions and consequently the margins and sustainability check. The

relevant industry benchmarks are studied and applied using research and industry expertise.

This report projects the financial performance of the Company along with the Debt

sustainability Check. The financial analysis helps the members of the venture to take key

decisions and also understand the area that need working. The report discusses various aspect

of the financial such as ratios, the variance analysis and also the breakeven analysis

(Williams & Dobelman, 2017).

Importance of Financial Analysis

The primary reason for any business venture is to earn the profit, so we can find out

the financial position of business with the help of financial statements (Vogel, 2014). The

analysis of financial helps us to find the viability of the business and help the key decision

maker in making an important decision. (Corporate Finance Institute, 2019). The financial

analysis helps us to find that there is a proper allocation of resources. Different financial

analysis carries their own benefit and helps in determining something different such as

financial statement help un-understanding the financial position of the firm, break-even

analysis assists in determining the breakeven point for the firm (Titman et al., 2011).

Financial Analysis

The financial statements allow analysts to measure liquidity, profitability, company-

wide efficiency, and cash flow. There are three main types of financial statements: the

balance sheet, income statement and cash flow statement (Investopedia, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

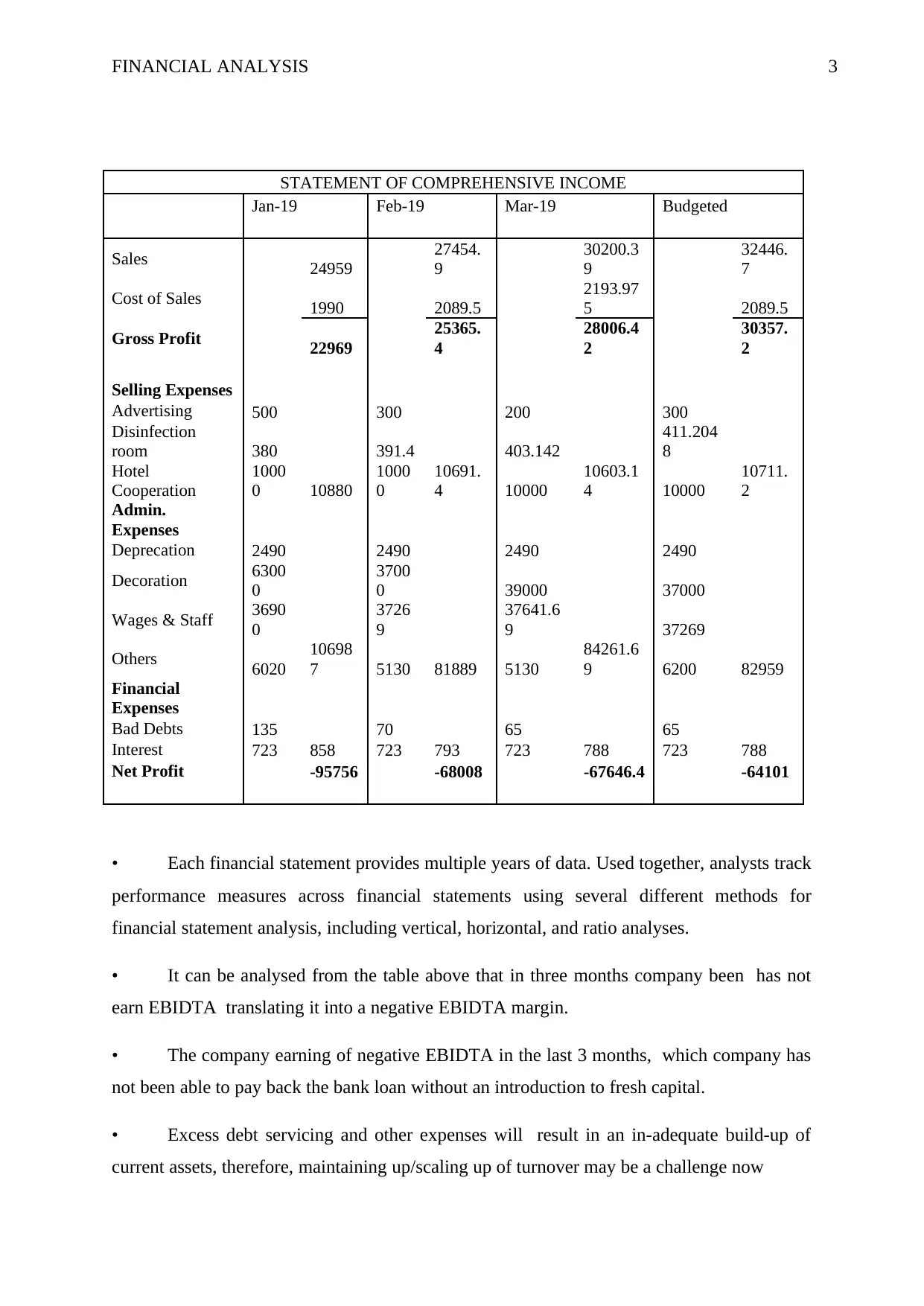

FINANCIAL ANALYSIS 3

STATEMENT OF COMPREHENSIVE INCOME

Jan-19 Feb-19 Mar-19 Budgeted

Sales 24959

27454.

9

30200.3

9

32446.

7

Cost of Sales 1990 2089.5

2193.97

5 2089.5

Gross Profit 22969

25365.

4

28006.4

2

30357.

2

Selling Expenses

Advertising 500 300 200 300

Disinfection

room 380 391.4 403.142

411.204

8

Hotel

Cooperation

1000

0 10880

1000

0

10691.

4 10000

10603.1

4 10000

10711.

2

Admin.

Expenses

Deprecation 2490 2490 2490 2490

Decoration 6300

0

3700

0 39000 37000

Wages & Staff 3690

0

3726

9

37641.6

9 37269

Others 6020

10698

7 5130 81889 5130

84261.6

9 6200 82959

Financial

Expenses

Bad Debts 135 70 65 65

Interest 723 858 723 793 723 788 723 788

Net Profit -95756 -68008 -67646.4 -64101

• Each financial statement provides multiple years of data. Used together, analysts track

performance measures across financial statements using several different methods for

financial statement analysis, including vertical, horizontal, and ratio analyses.

• It can be analysed from the table above that in three months company been has not

earn EBIDTA translating it into a negative EBIDTA margin.

• The company earning of negative EBIDTA in the last 3 months, which company has

not been able to pay back the bank loan without an introduction to fresh capital.

• Excess debt servicing and other expenses will result in an in-adequate build-up of

current assets, therefore, maintaining up/scaling up of turnover may be a challenge now

STATEMENT OF COMPREHENSIVE INCOME

Jan-19 Feb-19 Mar-19 Budgeted

Sales 24959

27454.

9

30200.3

9

32446.

7

Cost of Sales 1990 2089.5

2193.97

5 2089.5

Gross Profit 22969

25365.

4

28006.4

2

30357.

2

Selling Expenses

Advertising 500 300 200 300

Disinfection

room 380 391.4 403.142

411.204

8

Hotel

Cooperation

1000

0 10880

1000

0

10691.

4 10000

10603.1

4 10000

10711.

2

Admin.

Expenses

Deprecation 2490 2490 2490 2490

Decoration 6300

0

3700

0 39000 37000

Wages & Staff 3690

0

3726

9

37641.6

9 37269

Others 6020

10698

7 5130 81889 5130

84261.6

9 6200 82959

Financial

Expenses

Bad Debts 135 70 65 65

Interest 723 858 723 793 723 788 723 788

Net Profit -95756 -68008 -67646.4 -64101

• Each financial statement provides multiple years of data. Used together, analysts track

performance measures across financial statements using several different methods for

financial statement analysis, including vertical, horizontal, and ratio analyses.

• It can be analysed from the table above that in three months company been has not

earn EBIDTA translating it into a negative EBIDTA margin.

• The company earning of negative EBIDTA in the last 3 months, which company has

not been able to pay back the bank loan without an introduction to fresh capital.

• Excess debt servicing and other expenses will result in an in-adequate build-up of

current assets, therefore, maintaining up/scaling up of turnover may be a challenge now

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 4

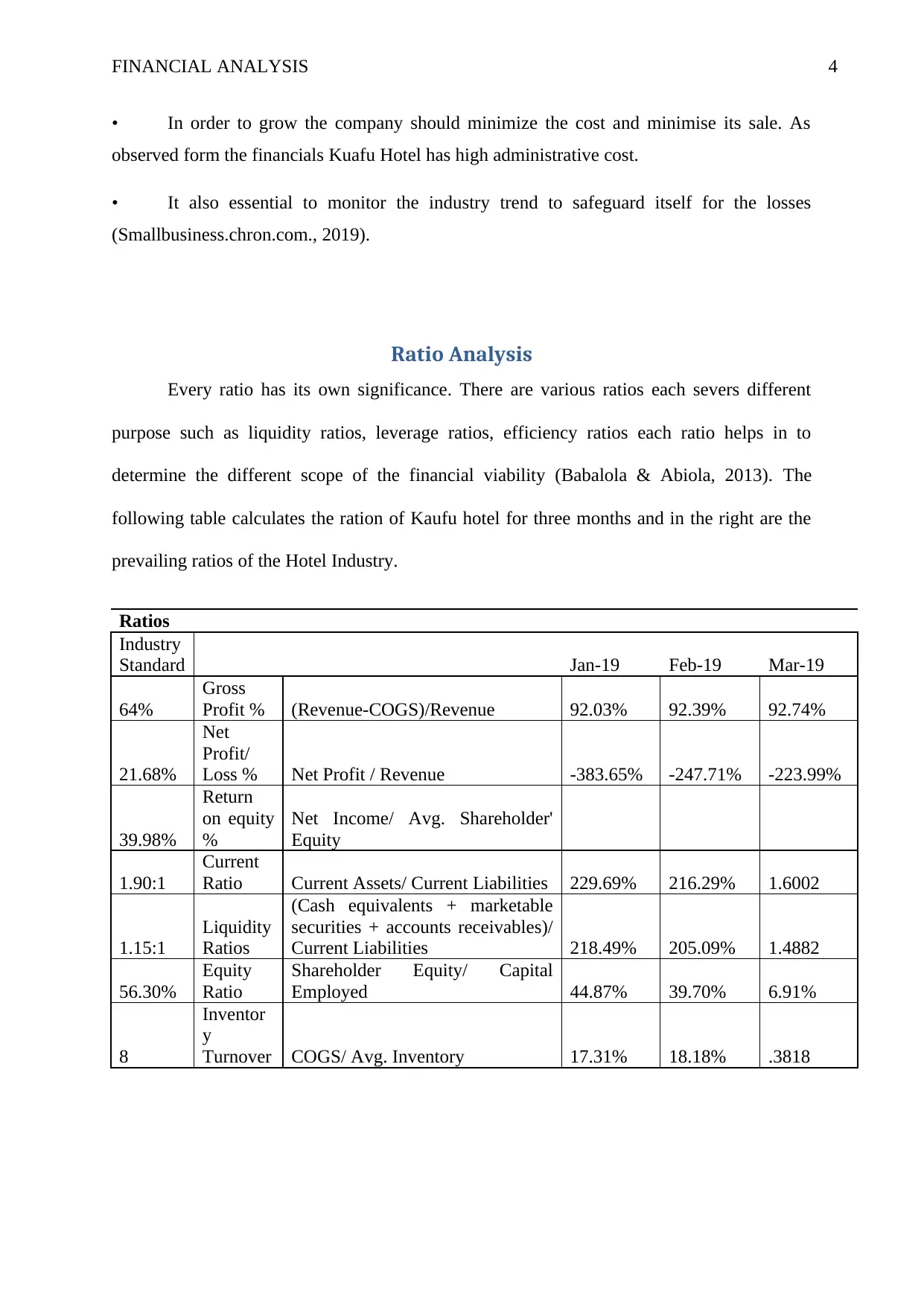

• In order to grow the company should minimize the cost and minimise its sale. As

observed form the financials Kuafu Hotel has high administrative cost.

• It also essential to monitor the industry trend to safeguard itself for the losses

(Smallbusiness.chron.com., 2019).

Ratio Analysis

Every ratio has its own significance. There are various ratios each severs different

purpose such as liquidity ratios, leverage ratios, efficiency ratios each ratio helps in to

determine the different scope of the financial viability (Babalola & Abiola, 2013). The

following table calculates the ration of Kaufu hotel for three months and in the right are the

prevailing ratios of the Hotel Industry.

Ratios

Industry

Standard Jan-19 Feb-19 Mar-19

64%

Gross

Profit % (Revenue-COGS)/Revenue 92.03% 92.39% 92.74%

21.68%

Net

Profit/

Loss % Net Profit / Revenue -383.65% -247.71% -223.99%

39.98%

Return

on equity

%

Net Income/ Avg. Shareholder'

Equity

1.90:1

Current

Ratio Current Assets/ Current Liabilities 229.69% 216.29% 1.6002

1.15:1

Liquidity

Ratios

(Cash equivalents + marketable

securities + accounts receivables)/

Current Liabilities 218.49% 205.09% 1.4882

56.30%

Equity

Ratio

Shareholder Equity/ Capital

Employed 44.87% 39.70% 6.91%

8

Inventor

y

Turnover COGS/ Avg. Inventory 17.31% 18.18% .3818

• In order to grow the company should minimize the cost and minimise its sale. As

observed form the financials Kuafu Hotel has high administrative cost.

• It also essential to monitor the industry trend to safeguard itself for the losses

(Smallbusiness.chron.com., 2019).

Ratio Analysis

Every ratio has its own significance. There are various ratios each severs different

purpose such as liquidity ratios, leverage ratios, efficiency ratios each ratio helps in to

determine the different scope of the financial viability (Babalola & Abiola, 2013). The

following table calculates the ration of Kaufu hotel for three months and in the right are the

prevailing ratios of the Hotel Industry.

Ratios

Industry

Standard Jan-19 Feb-19 Mar-19

64%

Gross

Profit % (Revenue-COGS)/Revenue 92.03% 92.39% 92.74%

21.68%

Net

Profit/

Loss % Net Profit / Revenue -383.65% -247.71% -223.99%

39.98%

Return

on equity

%

Net Income/ Avg. Shareholder'

Equity

1.90:1

Current

Ratio Current Assets/ Current Liabilities 229.69% 216.29% 1.6002

1.15:1

Liquidity

Ratios

(Cash equivalents + marketable

securities + accounts receivables)/

Current Liabilities 218.49% 205.09% 1.4882

56.30%

Equity

Ratio

Shareholder Equity/ Capital

Employed 44.87% 39.70% 6.91%

8

Inventor

y

Turnover COGS/ Avg. Inventory 17.31% 18.18% .3818

FINANCIAL ANALYSIS 5

Assessment of the ratios

Profitability

The profitability analysis helps in accessing the cost and revenue of the firm which

determines whether or not the firm is profiting. The following table calculates the ration of

Kaufu hotel for three months and in the right are the prevailing ratios of the Hotel Industry.

Each ratio has its own significance. There are various ratios each severs different purpose

such as liquidity ratios, leverage ratios, efficiency ratios each ratio helps in to determine the

different scope of the financial viability (Babalola and Abiola, 2013).

If we compare the profitability ratio of Kuafu Hotels with the Industry standards we

will find even though the gross profit % of the industry is better than the industry standards

but the net profit % far below the industry standards. The net profit of the business is negative

for which we can assess that the indirect expense of the company are far more than the

industry standard.

Financial Stability

Business is an on-going process, at times it at highs whereas at other times it is at

lows. Business stability analysis of a business determines the ability of a venture to withstand

a temporary problem, such as a decrease in sales, lack of capital or loss of a key employee or

customer (Beaver, Correia, & McNichols, 2011).

It is necessary to access the financial viability of the company, to see the long term

stability of the venture. There are certain ratios that helps in finding the viability of the

business such as current ratio, liquidity ratio, equity ratio. We can discover form the analysis

that the Kaufu Hotel lacks the stability when compared to its peer industries. Therefore the

stability of the venture is questionable.

Assessment of the ratios

Profitability

The profitability analysis helps in accessing the cost and revenue of the firm which

determines whether or not the firm is profiting. The following table calculates the ration of

Kaufu hotel for three months and in the right are the prevailing ratios of the Hotel Industry.

Each ratio has its own significance. There are various ratios each severs different purpose

such as liquidity ratios, leverage ratios, efficiency ratios each ratio helps in to determine the

different scope of the financial viability (Babalola and Abiola, 2013).

If we compare the profitability ratio of Kuafu Hotels with the Industry standards we

will find even though the gross profit % of the industry is better than the industry standards

but the net profit % far below the industry standards. The net profit of the business is negative

for which we can assess that the indirect expense of the company are far more than the

industry standard.

Financial Stability

Business is an on-going process, at times it at highs whereas at other times it is at

lows. Business stability analysis of a business determines the ability of a venture to withstand

a temporary problem, such as a decrease in sales, lack of capital or loss of a key employee or

customer (Beaver, Correia, & McNichols, 2011).

It is necessary to access the financial viability of the company, to see the long term

stability of the venture. There are certain ratios that helps in finding the viability of the

business such as current ratio, liquidity ratio, equity ratio. We can discover form the analysis

that the Kaufu Hotel lacks the stability when compared to its peer industries. Therefore the

stability of the venture is questionable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS 6

Asset utilisation

It is an analysis tool that identifies whether a company is wasting its assets or putting

them to good use. Some asset-utilization ratios include total asset turnover ratios and fixed

asset turnover ratios (Synergetics, 2019). It is necessary for a venture to have proper

utilization of assets and to monitor that the assets serve the purpose for they were designed

for (Tanninen, 2010). Asset utilization remains a critical matter that determines the

performance of the company in long run. It involves various essential factors like

understanding the demand of the customers and planning the optimize utilization of the

resources. Enhanced asset utilization is often a natural outcome of improving the planning,

execution and measurement of an organization. Although the there should not be

overutilization of assets also as it result in reduced quality of products and services.

When compared to the industry standard, we can access that the Kaufu Hotel is far

behind the industry standards in the asset utilization. We can also access that the company

has large scope of increase to exploit the utilization of asset.

Variance Analysis

The budgeted financials are planned and prepared according the industry standards

together with the capability of the firm. The variance analysis is calculated to find the

variation between the achieved result of the firm and the planned behaviour in budgeting. The

deviation between the both is known as variance.

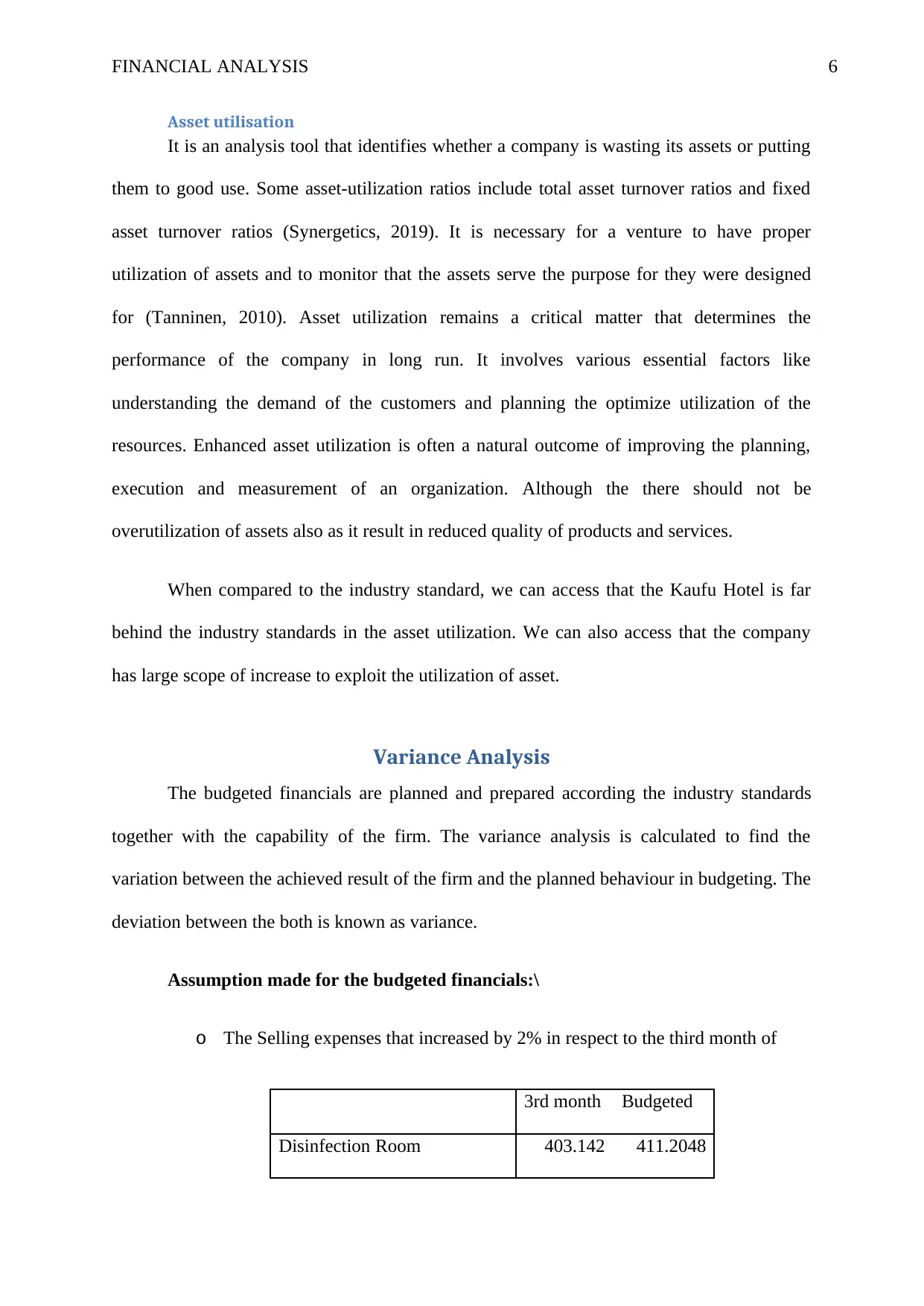

Assumption made for the budgeted financials:\

o The Selling expenses that increased by 2% in respect to the third month of

3rd month Budgeted

Disinfection Room 403.142 411.2048

Asset utilisation

It is an analysis tool that identifies whether a company is wasting its assets or putting

them to good use. Some asset-utilization ratios include total asset turnover ratios and fixed

asset turnover ratios (Synergetics, 2019). It is necessary for a venture to have proper

utilization of assets and to monitor that the assets serve the purpose for they were designed

for (Tanninen, 2010). Asset utilization remains a critical matter that determines the

performance of the company in long run. It involves various essential factors like

understanding the demand of the customers and planning the optimize utilization of the

resources. Enhanced asset utilization is often a natural outcome of improving the planning,

execution and measurement of an organization. Although the there should not be

overutilization of assets also as it result in reduced quality of products and services.

When compared to the industry standard, we can access that the Kaufu Hotel is far

behind the industry standards in the asset utilization. We can also access that the company

has large scope of increase to exploit the utilization of asset.

Variance Analysis

The budgeted financials are planned and prepared according the industry standards

together with the capability of the firm. The variance analysis is calculated to find the

variation between the achieved result of the firm and the planned behaviour in budgeting. The

deviation between the both is known as variance.

Assumption made for the budgeted financials:\

o The Selling expenses that increased by 2% in respect to the third month of

3rd month Budgeted

Disinfection Room 403.142 411.2048

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 7

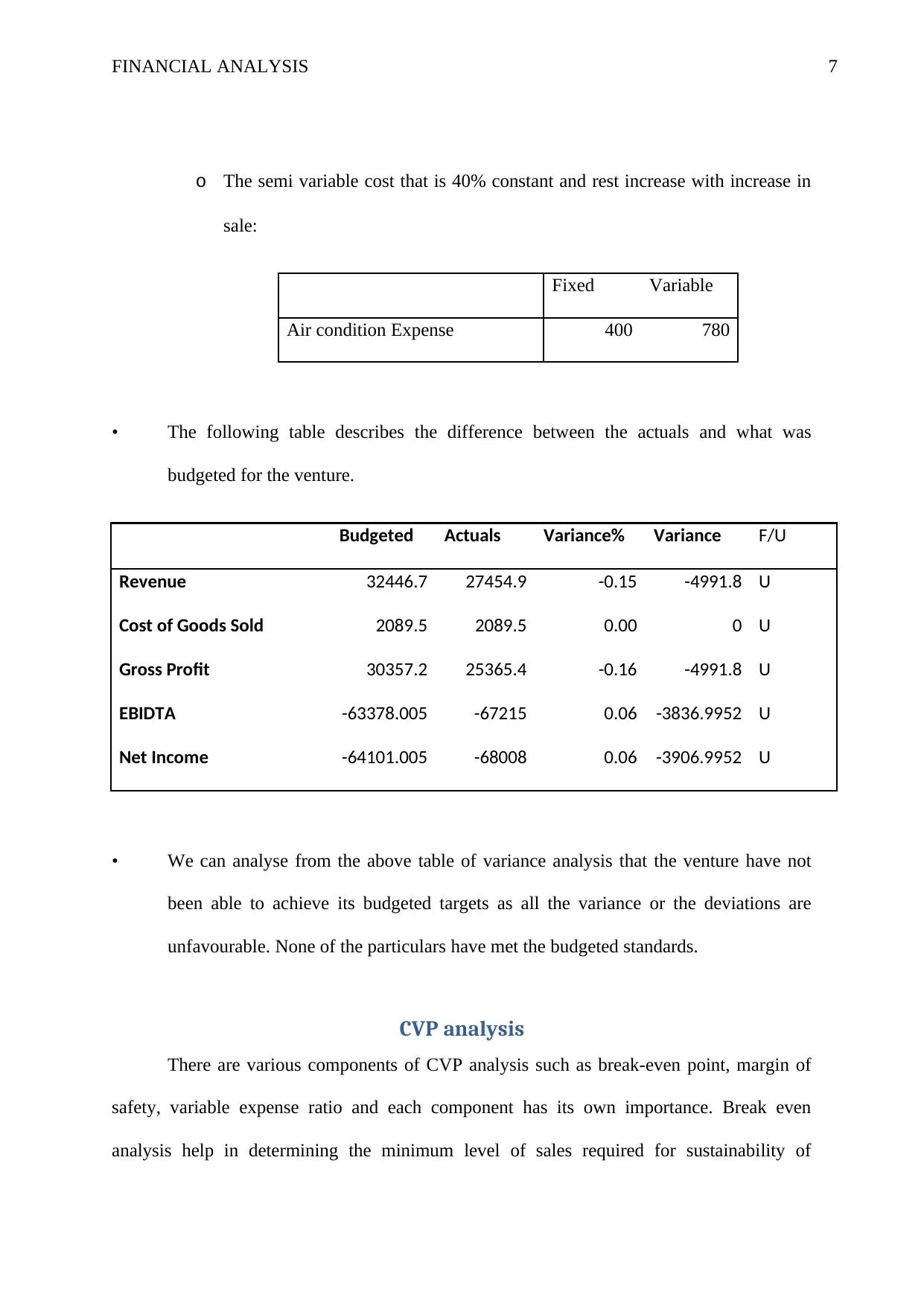

o The semi variable cost that is 40% constant and rest increase with increase in

sale:

Fixed Variable

Air condition Expense 400 780

• The following table describes the difference between the actuals and what was

budgeted for the venture.

Budgeted Actuals Variance% Variance F/U

Revenue 32446.7 27454.9 -0.15 -4991.8 U

Cost of Goods Sold 2089.5 2089.5 0.00 0 U

Gross Profit 30357.2 25365.4 -0.16 -4991.8 U

EBIDTA -63378.005 -67215 0.06 -3836.9952 U

Net Income -64101.005 -68008 0.06 -3906.9952 U

• We can analyse from the above table of variance analysis that the venture have not

been able to achieve its budgeted targets as all the variance or the deviations are

unfavourable. None of the particulars have met the budgeted standards.

CVP analysis

There are various components of CVP analysis such as break-even point, margin of

safety, variable expense ratio and each component has its own importance. Break even

analysis help in determining the minimum level of sales required for sustainability of

o The semi variable cost that is 40% constant and rest increase with increase in

sale:

Fixed Variable

Air condition Expense 400 780

• The following table describes the difference between the actuals and what was

budgeted for the venture.

Budgeted Actuals Variance% Variance F/U

Revenue 32446.7 27454.9 -0.15 -4991.8 U

Cost of Goods Sold 2089.5 2089.5 0.00 0 U

Gross Profit 30357.2 25365.4 -0.16 -4991.8 U

EBIDTA -63378.005 -67215 0.06 -3836.9952 U

Net Income -64101.005 -68008 0.06 -3906.9952 U

• We can analyse from the above table of variance analysis that the venture have not

been able to achieve its budgeted targets as all the variance or the deviations are

unfavourable. None of the particulars have met the budgeted standards.

CVP analysis

There are various components of CVP analysis such as break-even point, margin of

safety, variable expense ratio and each component has its own importance. Break even

analysis help in determining the minimum level of sales required for sustainability of

FINANCIAL ANALYSIS 8

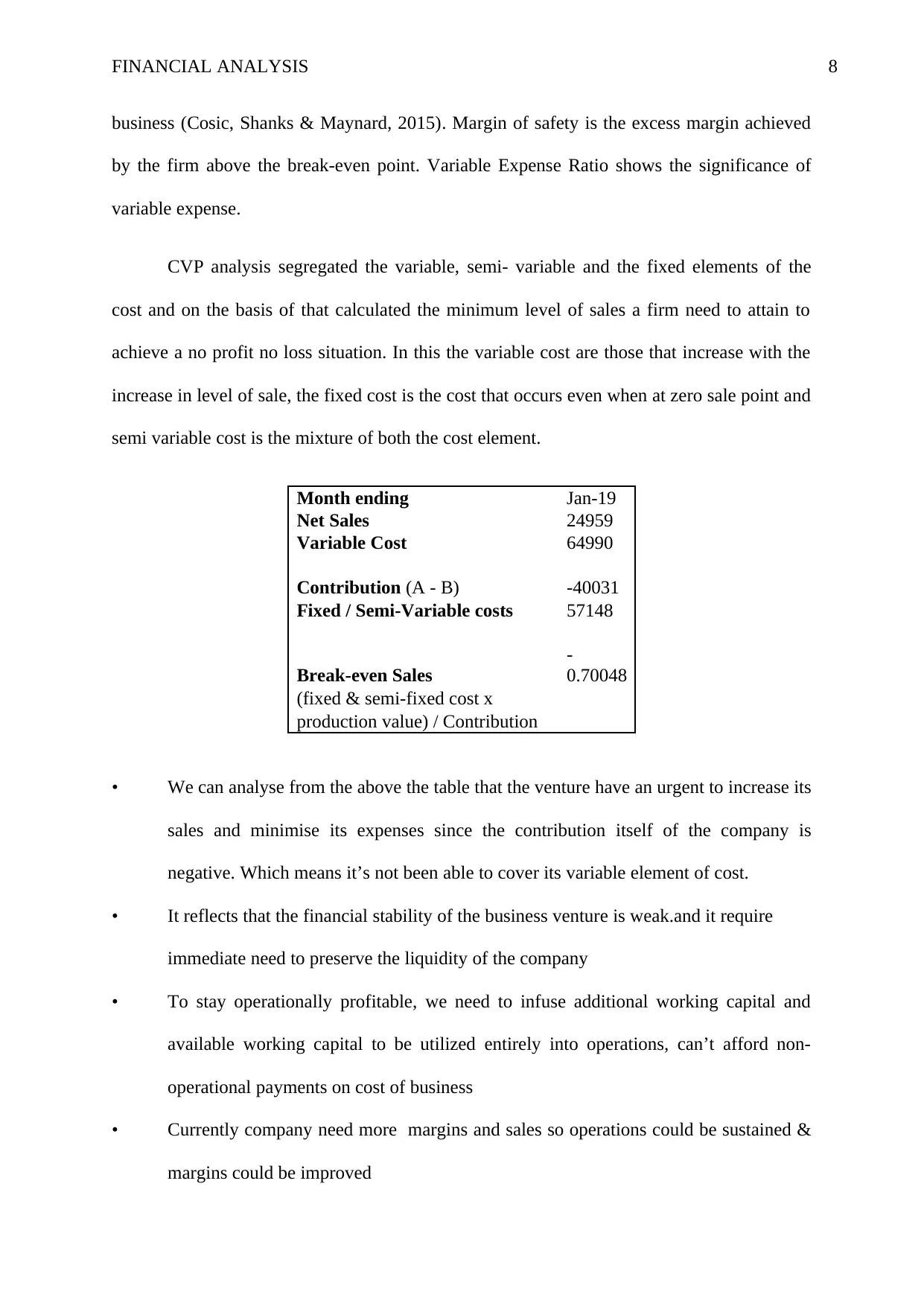

business (Cosic, Shanks & Maynard, 2015). Margin of safety is the excess margin achieved

by the firm above the break-even point. Variable Expense Ratio shows the significance of

variable expense.

CVP analysis segregated the variable, semi- variable and the fixed elements of the

cost and on the basis of that calculated the minimum level of sales a firm need to attain to

achieve a no profit no loss situation. In this the variable cost are those that increase with the

increase in level of sale, the fixed cost is the cost that occurs even when at zero sale point and

semi variable cost is the mixture of both the cost element.

Month ending Jan-19

Net Sales 24959

Variable Cost 64990

Contribution (A - B) -40031

Fixed / Semi-Variable costs 57148

Break-even Sales

-

0.70048

(fixed & semi-fixed cost x

production value) / Contribution

• We can analyse from the above the table that the venture have an urgent to increase its

sales and minimise its expenses since the contribution itself of the company is

negative. Which means it’s not been able to cover its variable element of cost.

• It reflects that the financial stability of the business venture is weak.and it require

immediate need to preserve the liquidity of the company

• To stay operationally profitable, we need to infuse additional working capital and

available working capital to be utilized entirely into operations, can’t afford non-

operational payments on cost of business

• Currently company need more margins and sales so operations could be sustained &

margins could be improved

business (Cosic, Shanks & Maynard, 2015). Margin of safety is the excess margin achieved

by the firm above the break-even point. Variable Expense Ratio shows the significance of

variable expense.

CVP analysis segregated the variable, semi- variable and the fixed elements of the

cost and on the basis of that calculated the minimum level of sales a firm need to attain to

achieve a no profit no loss situation. In this the variable cost are those that increase with the

increase in level of sale, the fixed cost is the cost that occurs even when at zero sale point and

semi variable cost is the mixture of both the cost element.

Month ending Jan-19

Net Sales 24959

Variable Cost 64990

Contribution (A - B) -40031

Fixed / Semi-Variable costs 57148

Break-even Sales

-

0.70048

(fixed & semi-fixed cost x

production value) / Contribution

• We can analyse from the above the table that the venture have an urgent to increase its

sales and minimise its expenses since the contribution itself of the company is

negative. Which means it’s not been able to cover its variable element of cost.

• It reflects that the financial stability of the business venture is weak.and it require

immediate need to preserve the liquidity of the company

• To stay operationally profitable, we need to infuse additional working capital and

available working capital to be utilized entirely into operations, can’t afford non-

operational payments on cost of business

• Currently company need more margins and sales so operations could be sustained &

margins could be improved

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 10

Conclusion

It can be concludes the current liability position of the company and found that

prevailing level of liability if not settled is unviable. Company with given setup, cannot

sustain the liability hence if liability is not rationalised than same would result in closure of

the factory and huge unemployment. Thus, rationalisation of the bank liabilities on the

company is critical for its sustainability.

The report studies that is very complex, requires extra resources both in terms of time

& money and necessitates the infusion of additional working capital to maintain the

compliances. Some of the critical issues that afloat are lower demand, high maintenance cost,

in-adequate working capital is likely to remain a challenge in next 2 years.

In our assessment is that post settling the dues with banks, repayment of private

investor’s money, increasing the sale and minimizing the cost would be the priority which

would take minimum 1-2 years else unit would need to be closed. The report discusses

various aspect of the financial such as ratios, the variance analysis and also the breakeven

analysis. It also helps in accessing the financial performance of the Company along with the

Debt sustainability Check.

Conclusion

It can be concludes the current liability position of the company and found that

prevailing level of liability if not settled is unviable. Company with given setup, cannot

sustain the liability hence if liability is not rationalised than same would result in closure of

the factory and huge unemployment. Thus, rationalisation of the bank liabilities on the

company is critical for its sustainability.

The report studies that is very complex, requires extra resources both in terms of time

& money and necessitates the infusion of additional working capital to maintain the

compliances. Some of the critical issues that afloat are lower demand, high maintenance cost,

in-adequate working capital is likely to remain a challenge in next 2 years.

In our assessment is that post settling the dues with banks, repayment of private

investor’s money, increasing the sale and minimizing the cost would be the priority which

would take minimum 1-2 years else unit would need to be closed. The report discusses

various aspect of the financial such as ratios, the variance analysis and also the breakeven

analysis. It also helps in accessing the financial performance of the Company along with the

Debt sustainability Check.

FINANCIAL ANALYSIS 11

References

Babalola, Y. A., & Abiola, F. R. (2013). Financial ratio analysis of firms: A tool for decision

making. International journal of management sciences, 1(4), 132-137.

Beaver, W. H., Correia, M., & McNichols, M. F. (2011). Financial statement analysis and the

prediction of financial distress. Foundations and Trends® in Accounting, 5(2), 99-

173.

Cliffsnotes. (2019). Cost-Volume-Profit Analysis. Cliffsnotes.com. Retrieved from

https://www.cliffsnotes.com/study-guides/accounting/accounting-principles-ii/cost-

volume-profit-relationships/cost-volume-profit-analysis

Corporate Finance Institute. (2019). Analysis of Financial Statements - Free Financial

Analysis Guide. Corporate Finance Institute. Retrieved from

https://corporatefinanceinstitute.com/resources/knowledge/finance/analysis-of-

financial-statements/

Cosic, R., Shanks, G., & Maynard, S. B. (2015). A business analytics capability framework.

Australasian Journal of Information Systems, 19.

Investopedia. (2019). Financial Analysis. Investopedia. Retrieved from

https://www.investopedia.com/terms/f/financial-analysis.asp .

Smallbusiness.chron.com.. (2019). How to Determine the Financial Stability of a Small

Business. Smallbusiness.chron.com. Retrieved from

https://smallbusiness.chron.com/determine-financial-stability-small-business-

58597.html

Synergetics. (2019). Asset Utilization. Synergeticsww.com. Retrieved from

http://www.synergeticsww.com/problems-we-solve/return-on-assets/asset-utilization/

Tanninen, K., Puumalainen, K., & Sandström, J. (2010). The power of TQM: analysis of its

effects on profitability, productivity and customer satisfaction. Total Quality

Management, 21(2), 171-184.

Titman, S., Keown, A. J., Martin, J. D., & Martin, T. (2011). Financial management:

Principles and applications (Vol. 11). Boston: Prentice Hall.

References

Babalola, Y. A., & Abiola, F. R. (2013). Financial ratio analysis of firms: A tool for decision

making. International journal of management sciences, 1(4), 132-137.

Beaver, W. H., Correia, M., & McNichols, M. F. (2011). Financial statement analysis and the

prediction of financial distress. Foundations and Trends® in Accounting, 5(2), 99-

173.

Cliffsnotes. (2019). Cost-Volume-Profit Analysis. Cliffsnotes.com. Retrieved from

https://www.cliffsnotes.com/study-guides/accounting/accounting-principles-ii/cost-

volume-profit-relationships/cost-volume-profit-analysis

Corporate Finance Institute. (2019). Analysis of Financial Statements - Free Financial

Analysis Guide. Corporate Finance Institute. Retrieved from

https://corporatefinanceinstitute.com/resources/knowledge/finance/analysis-of-

financial-statements/

Cosic, R., Shanks, G., & Maynard, S. B. (2015). A business analytics capability framework.

Australasian Journal of Information Systems, 19.

Investopedia. (2019). Financial Analysis. Investopedia. Retrieved from

https://www.investopedia.com/terms/f/financial-analysis.asp .

Smallbusiness.chron.com.. (2019). How to Determine the Financial Stability of a Small

Business. Smallbusiness.chron.com. Retrieved from

https://smallbusiness.chron.com/determine-financial-stability-small-business-

58597.html

Synergetics. (2019). Asset Utilization. Synergeticsww.com. Retrieved from

http://www.synergeticsww.com/problems-we-solve/return-on-assets/asset-utilization/

Tanninen, K., Puumalainen, K., & Sandström, J. (2010). The power of TQM: analysis of its

effects on profitability, productivity and customer satisfaction. Total Quality

Management, 21(2), 171-184.

Titman, S., Keown, A. J., Martin, J. D., & Martin, T. (2011). Financial management:

Principles and applications (Vol. 11). Boston: Prentice Hall.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.