Financial Management in Organizations: A Comprehensive Analysis

VerifiedAdded on 2022/12/30

|11

|3790

|94

Report

AI Summary

This report delves into the intricacies of financial management within organizations, commencing with an examination of agency problems, particularly in the context of Morals PLC, and proposing solutions to mitigate potential conflicts of interest. The analysis extends to investment decisions, employing Net Present Value (NPV) and payback period calculations to evaluate the feasibility of a specific project, and comparing it with an alternative investment. Furthermore, the report addresses the financial challenges faced by Small and Medium Enterprises (SMEs) in securing medium to long-term finance, exploring the reasons behind these difficulties and the advantages and disadvantages of going public through an Initial Public Offering (IPO). The report also discusses the characteristics of an efficient market and the Alternative Investment Market (AIM) and various methods of flotation in the primary market.

Financial management in

organization

organization

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

SECTION A...............................................................................................................................3

Question 1..............................................................................................................................3

Question 2..............................................................................................................................4

Question 3..............................................................................................................................6

SECTION B...............................................................................................................................9

Question 4..............................................................................................................................9

REFERENCES.........................................................................................................................11

SECTION A...............................................................................................................................3

Question 1..............................................................................................................................3

Question 2..............................................................................................................................4

Question 3..............................................................................................................................6

SECTION B...............................................................................................................................9

Question 4..............................................................................................................................9

REFERENCES.........................................................................................................................11

SECTION A

Question 1

(a) The agency implies that the manager can maximize its own wealth instead of the

shareholders which is because of the difference in the objectives and the separation of

ownership and control. The first thing to note that the company has diversified its

various activities across a different range of various industrial sectors. This is

sometimes also justified by giving it a name of reducing the risk for the shareholders

but it is important to note that shareholders already have diversified their portfolios.

The company is trying its diversifying its business activities for its managerial

objectives, for instance, increasing the security of the directors through the way of

diversifying the unsystematic risk (Libson, 2018). Second is that the company is

maintaining its gearing ratio lower than that of the industry average. This is another

example of the agency problem where the shareholders prefer to have greater level of

debt due to the cost of debt to be cheaper and are also ready to accept the high risk

because they have already diversified their portfolio. The managers, nonetheless,

favour equity mode of finance because too high the financial risk which led to

compromising the job security. Directors are probably going to get self-satisfied with

agreements of such length. There is likewise an issue with the utilization and terms of

the share choices. With the historical growth rate in the share price of 6 %, the

organization's share value five years prior when the directors were given the offer

would have been roughly £2.24. At the offer cost to move above £3 in under five

years speaks to a very unchallenging objective.

(b) The company Morals plc needs to make amendment in its business structure a sit has

diversified its business in different segment in order to reduce the risk which is

creating complications. Along with this, the gearing ratio of the company is less than

the industrial ratio which means that Morals plc is making use of the equity finance

for raising its capital instead of debt finance with the objective of reducing the

financial burden but this will cause problem in respect to the ownership as issuing

more share will might reduce the specific percentage of ownership and will increase

the expectation of the equity holders for greater return. Therefore, Morals plc should

stop equity source of financing and look for debt instruments. For another issue, the

growth rate of the share price is placed at 6% which is unrealistic, thus, it should

make proper analysis and then put the growth rate.

Question 1

(a) The agency implies that the manager can maximize its own wealth instead of the

shareholders which is because of the difference in the objectives and the separation of

ownership and control. The first thing to note that the company has diversified its

various activities across a different range of various industrial sectors. This is

sometimes also justified by giving it a name of reducing the risk for the shareholders

but it is important to note that shareholders already have diversified their portfolios.

The company is trying its diversifying its business activities for its managerial

objectives, for instance, increasing the security of the directors through the way of

diversifying the unsystematic risk (Libson, 2018). Second is that the company is

maintaining its gearing ratio lower than that of the industry average. This is another

example of the agency problem where the shareholders prefer to have greater level of

debt due to the cost of debt to be cheaper and are also ready to accept the high risk

because they have already diversified their portfolio. The managers, nonetheless,

favour equity mode of finance because too high the financial risk which led to

compromising the job security. Directors are probably going to get self-satisfied with

agreements of such length. There is likewise an issue with the utilization and terms of

the share choices. With the historical growth rate in the share price of 6 %, the

organization's share value five years prior when the directors were given the offer

would have been roughly £2.24. At the offer cost to move above £3 in under five

years speaks to a very unchallenging objective.

(b) The company Morals plc needs to make amendment in its business structure a sit has

diversified its business in different segment in order to reduce the risk which is

creating complications. Along with this, the gearing ratio of the company is less than

the industrial ratio which means that Morals plc is making use of the equity finance

for raising its capital instead of debt finance with the objective of reducing the

financial burden but this will cause problem in respect to the ownership as issuing

more share will might reduce the specific percentage of ownership and will increase

the expectation of the equity holders for greater return. Therefore, Morals plc should

stop equity source of financing and look for debt instruments. For another issue, the

growth rate of the share price is placed at 6% which is unrealistic, thus, it should

make proper analysis and then put the growth rate.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(c) An efficient market can be characterized as a market where there are huge number of

discerning, benefit 'maximisers' effectively contending and competing, with each

other attempting to anticipate future market estimations of separate securities, and

where significant current data is easily accessible to all the members. In an efficient

market, rivalry among the numerous keen members prompts a circumstance where,

anytime, the real costs of individual security as of now mirror the impacts of data put

together both with respect to occasions that have just happened and on occasions

which, as of now, the market hopes to occur later on (Bird, Du and Willett, 2017). All

in all, in an efficient market anytime the actual cost of a security will be a decent

gauge of its intrinsic worth. Thus, the main characteristics of the efficient market is

the perfect, complete, costless and the instant transmission of the information. These

are the certain characteristics which are important for considering a market to be

efficient.

(d) The Alternative investment Market is a sub market of the LSE which is mainly

designed for helping the small companies for gaining access to the raising capital

from the public market (Filip, Ghio and Paugam, 2020). This is considered to more

speculative because of relaxation in the regulations. It attracts the sophisticated and

the institutional investors who are having risk appetite along with the resources for

carrying out the due diligence. Yes, alternative investment market can also be

considered as an efficient market because it has the characteristics of an efficient

market.

Question 2

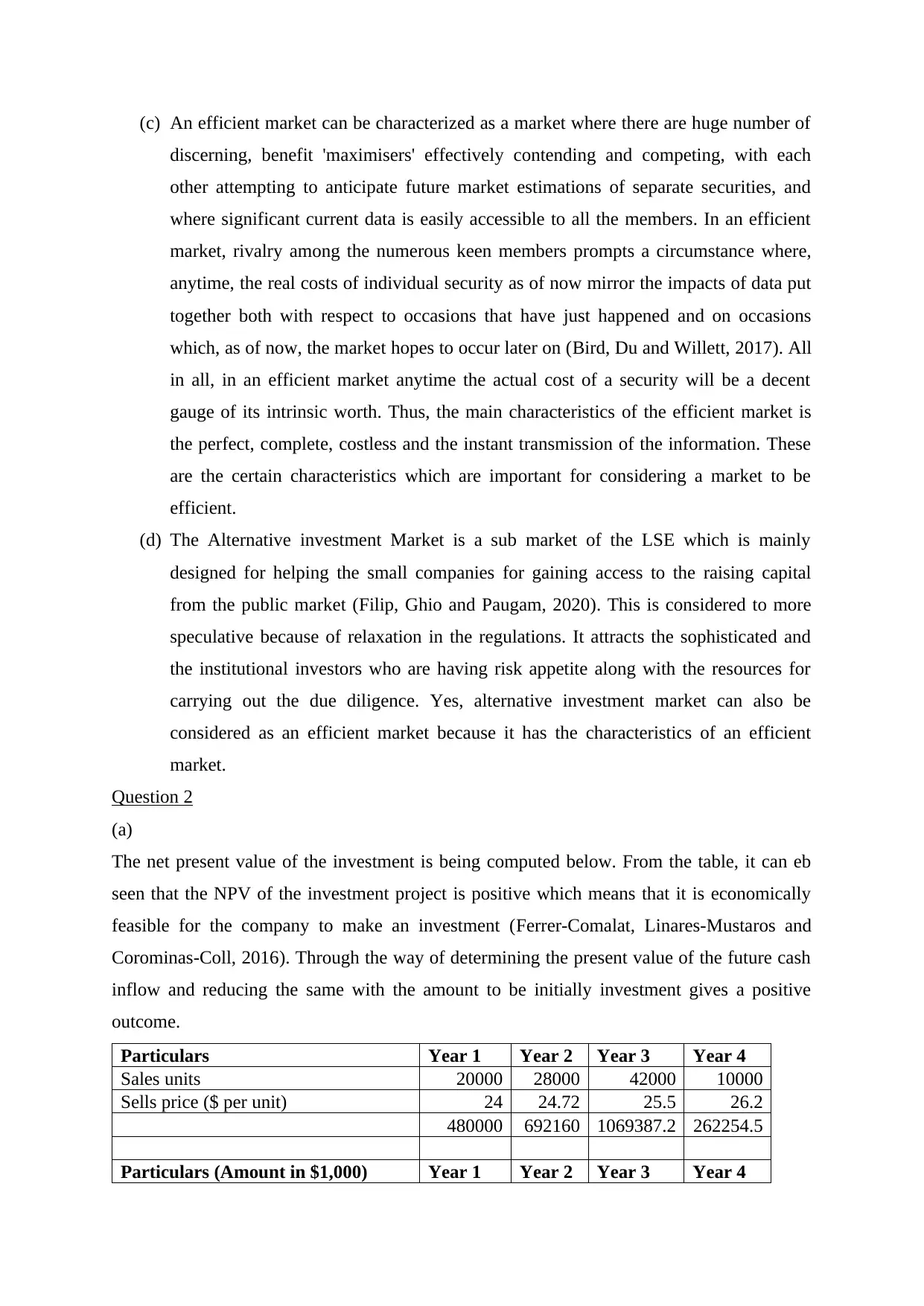

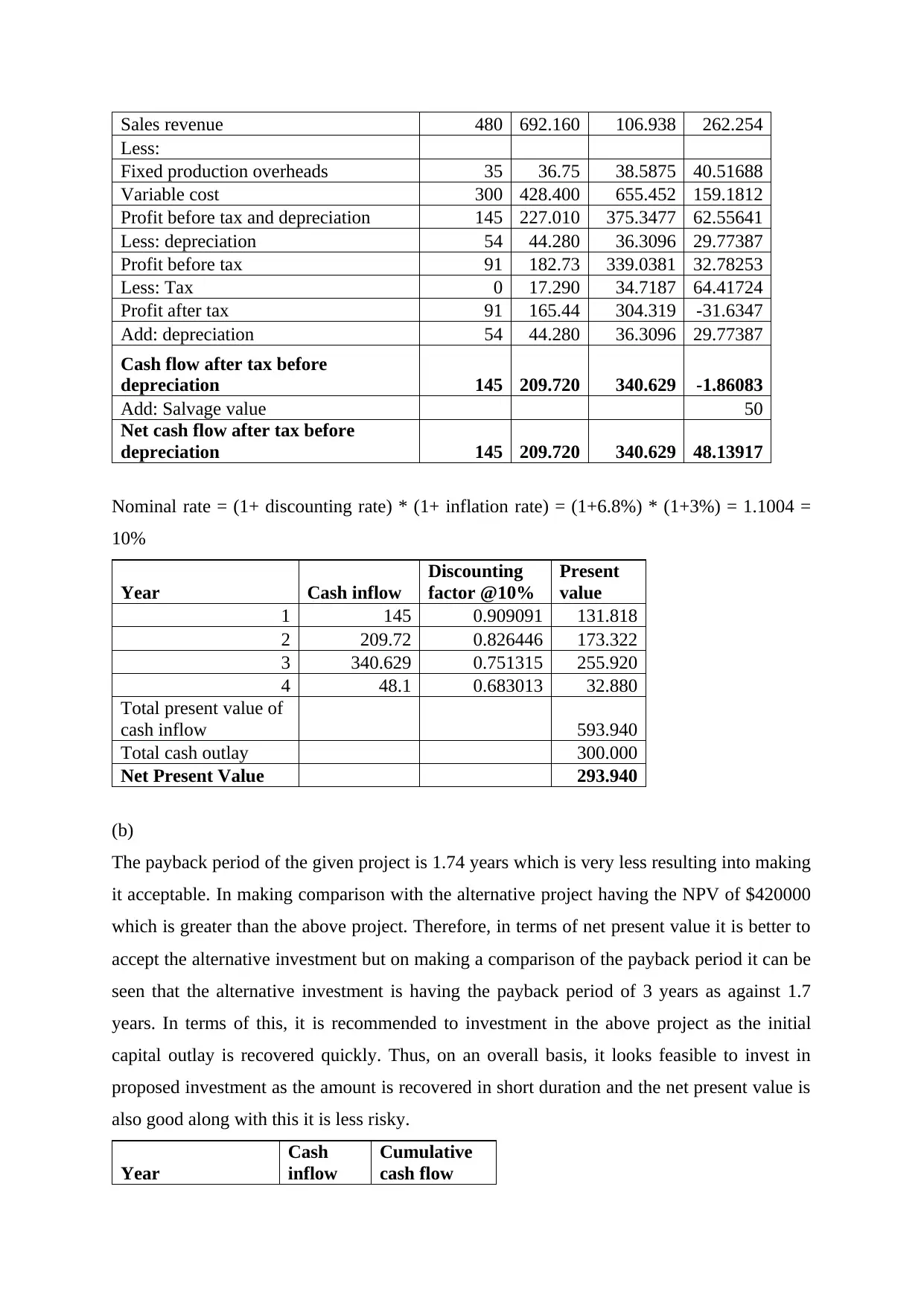

(a)

The net present value of the investment is being computed below. From the table, it can eb

seen that the NPV of the investment project is positive which means that it is economically

feasible for the company to make an investment (Ferrer-Comalat, Linares-Mustaros and

Corominas-Coll, 2016). Through the way of determining the present value of the future cash

inflow and reducing the same with the amount to be initially investment gives a positive

outcome.

Particulars Year 1 Year 2 Year 3 Year 4

Sales units 20000 28000 42000 10000

Sells price ($ per unit) 24 24.72 25.5 26.2

480000 692160 1069387.2 262254.5

Particulars (Amount in $1,000) Year 1 Year 2 Year 3 Year 4

discerning, benefit 'maximisers' effectively contending and competing, with each

other attempting to anticipate future market estimations of separate securities, and

where significant current data is easily accessible to all the members. In an efficient

market, rivalry among the numerous keen members prompts a circumstance where,

anytime, the real costs of individual security as of now mirror the impacts of data put

together both with respect to occasions that have just happened and on occasions

which, as of now, the market hopes to occur later on (Bird, Du and Willett, 2017). All

in all, in an efficient market anytime the actual cost of a security will be a decent

gauge of its intrinsic worth. Thus, the main characteristics of the efficient market is

the perfect, complete, costless and the instant transmission of the information. These

are the certain characteristics which are important for considering a market to be

efficient.

(d) The Alternative investment Market is a sub market of the LSE which is mainly

designed for helping the small companies for gaining access to the raising capital

from the public market (Filip, Ghio and Paugam, 2020). This is considered to more

speculative because of relaxation in the regulations. It attracts the sophisticated and

the institutional investors who are having risk appetite along with the resources for

carrying out the due diligence. Yes, alternative investment market can also be

considered as an efficient market because it has the characteristics of an efficient

market.

Question 2

(a)

The net present value of the investment is being computed below. From the table, it can eb

seen that the NPV of the investment project is positive which means that it is economically

feasible for the company to make an investment (Ferrer-Comalat, Linares-Mustaros and

Corominas-Coll, 2016). Through the way of determining the present value of the future cash

inflow and reducing the same with the amount to be initially investment gives a positive

outcome.

Particulars Year 1 Year 2 Year 3 Year 4

Sales units 20000 28000 42000 10000

Sells price ($ per unit) 24 24.72 25.5 26.2

480000 692160 1069387.2 262254.5

Particulars (Amount in $1,000) Year 1 Year 2 Year 3 Year 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales revenue 480 692.160 106.938 262.254

Less:

Fixed production overheads 35 36.75 38.5875 40.51688

Variable cost 300 428.400 655.452 159.1812

Profit before tax and depreciation 145 227.010 375.3477 62.55641

Less: depreciation 54 44.280 36.3096 29.77387

Profit before tax 91 182.73 339.0381 32.78253

Less: Tax 0 17.290 34.7187 64.41724

Profit after tax 91 165.44 304.319 -31.6347

Add: depreciation 54 44.280 36.3096 29.77387

Cash flow after tax before

depreciation 145 209.720 340.629 -1.86083

Add: Salvage value 50

Net cash flow after tax before

depreciation 145 209.720 340.629 48.13917

Nominal rate = (1+ discounting rate) * (1+ inflation rate) = (1+6.8%) * (1+3%) = 1.1004 =

10%

Year Cash inflow

Discounting

factor @10%

Present

value

1 145 0.909091 131.818

2 209.72 0.826446 173.322

3 340.629 0.751315 255.920

4 48.1 0.683013 32.880

Total present value of

cash inflow 593.940

Total cash outlay 300.000

Net Present Value 293.940

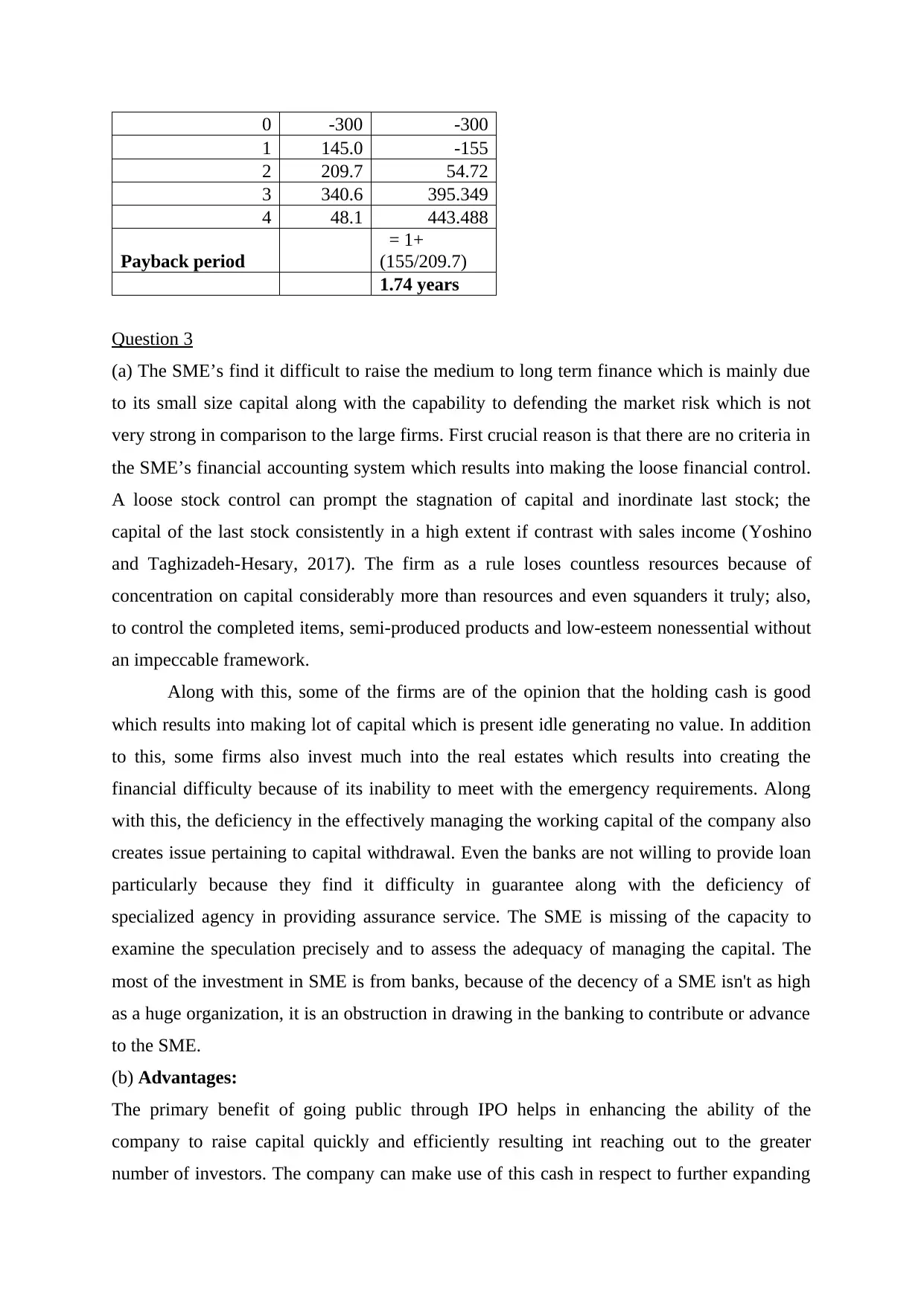

(b)

The payback period of the given project is 1.74 years which is very less resulting into making

it acceptable. In making comparison with the alternative project having the NPV of $420000

which is greater than the above project. Therefore, in terms of net present value it is better to

accept the alternative investment but on making a comparison of the payback period it can be

seen that the alternative investment is having the payback period of 3 years as against 1.7

years. In terms of this, it is recommended to investment in the above project as the initial

capital outlay is recovered quickly. Thus, on an overall basis, it looks feasible to invest in

proposed investment as the amount is recovered in short duration and the net present value is

also good along with this it is less risky.

Year

Cash

inflow

Cumulative

cash flow

Less:

Fixed production overheads 35 36.75 38.5875 40.51688

Variable cost 300 428.400 655.452 159.1812

Profit before tax and depreciation 145 227.010 375.3477 62.55641

Less: depreciation 54 44.280 36.3096 29.77387

Profit before tax 91 182.73 339.0381 32.78253

Less: Tax 0 17.290 34.7187 64.41724

Profit after tax 91 165.44 304.319 -31.6347

Add: depreciation 54 44.280 36.3096 29.77387

Cash flow after tax before

depreciation 145 209.720 340.629 -1.86083

Add: Salvage value 50

Net cash flow after tax before

depreciation 145 209.720 340.629 48.13917

Nominal rate = (1+ discounting rate) * (1+ inflation rate) = (1+6.8%) * (1+3%) = 1.1004 =

10%

Year Cash inflow

Discounting

factor @10%

Present

value

1 145 0.909091 131.818

2 209.72 0.826446 173.322

3 340.629 0.751315 255.920

4 48.1 0.683013 32.880

Total present value of

cash inflow 593.940

Total cash outlay 300.000

Net Present Value 293.940

(b)

The payback period of the given project is 1.74 years which is very less resulting into making

it acceptable. In making comparison with the alternative project having the NPV of $420000

which is greater than the above project. Therefore, in terms of net present value it is better to

accept the alternative investment but on making a comparison of the payback period it can be

seen that the alternative investment is having the payback period of 3 years as against 1.7

years. In terms of this, it is recommended to investment in the above project as the initial

capital outlay is recovered quickly. Thus, on an overall basis, it looks feasible to invest in

proposed investment as the amount is recovered in short duration and the net present value is

also good along with this it is less risky.

Year

Cash

inflow

Cumulative

cash flow

0 -300 -300

1 145.0 -155

2 209.7 54.72

3 340.6 395.349

4 48.1 443.488

Payback period

= 1+

(155/209.7)

1.74 years

Question 3

(a) The SME’s find it difficult to raise the medium to long term finance which is mainly due

to its small size capital along with the capability to defending the market risk which is not

very strong in comparison to the large firms. First crucial reason is that there are no criteria in

the SME’s financial accounting system which results into making the loose financial control.

A loose stock control can prompt the stagnation of capital and inordinate last stock; the

capital of the last stock consistently in a high extent if contrast with sales income (Yoshino

and Taghizadeh-Hesary, 2017). The firm as a rule loses countless resources because of

concentration on capital considerably more than resources and even squanders it truly; also,

to control the completed items, semi-produced products and low-esteem nonessential without

an impeccable framework.

Along with this, some of the firms are of the opinion that the holding cash is good

which results into making lot of capital which is present idle generating no value. In addition

to this, some firms also invest much into the real estates which results into creating the

financial difficulty because of its inability to meet with the emergency requirements. Along

with this, the deficiency in the effectively managing the working capital of the company also

creates issue pertaining to capital withdrawal. Even the banks are not willing to provide loan

particularly because they find it difficulty in guarantee along with the deficiency of

specialized agency in providing assurance service. The SME is missing of the capacity to

examine the speculation precisely and to assess the adequacy of managing the capital. The

most of the investment in SME is from banks, because of the decency of a SME isn't as high

as a huge organization, it is an obstruction in drawing in the banking to contribute or advance

to the SME.

(b) Advantages:

The primary benefit of going public through IPO helps in enhancing the ability of the

company to raise capital quickly and efficiently resulting int reaching out to the greater

number of investors. The company can make use of this cash in respect to further expanding

1 145.0 -155

2 209.7 54.72

3 340.6 395.349

4 48.1 443.488

Payback period

= 1+

(155/209.7)

1.74 years

Question 3

(a) The SME’s find it difficult to raise the medium to long term finance which is mainly due

to its small size capital along with the capability to defending the market risk which is not

very strong in comparison to the large firms. First crucial reason is that there are no criteria in

the SME’s financial accounting system which results into making the loose financial control.

A loose stock control can prompt the stagnation of capital and inordinate last stock; the

capital of the last stock consistently in a high extent if contrast with sales income (Yoshino

and Taghizadeh-Hesary, 2017). The firm as a rule loses countless resources because of

concentration on capital considerably more than resources and even squanders it truly; also,

to control the completed items, semi-produced products and low-esteem nonessential without

an impeccable framework.

Along with this, some of the firms are of the opinion that the holding cash is good

which results into making lot of capital which is present idle generating no value. In addition

to this, some firms also invest much into the real estates which results into creating the

financial difficulty because of its inability to meet with the emergency requirements. Along

with this, the deficiency in the effectively managing the working capital of the company also

creates issue pertaining to capital withdrawal. Even the banks are not willing to provide loan

particularly because they find it difficulty in guarantee along with the deficiency of

specialized agency in providing assurance service. The SME is missing of the capacity to

examine the speculation precisely and to assess the adequacy of managing the capital. The

most of the investment in SME is from banks, because of the decency of a SME isn't as high

as a huge organization, it is an obstruction in drawing in the banking to contribute or advance

to the SME.

(b) Advantages:

The primary benefit of going public through IPO helps in enhancing the ability of the

company to raise capital quickly and efficiently resulting int reaching out to the greater

number of investors. The company can make use of this cash in respect to further expanding

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the business which can be in the form of research, infrastructure development and so forth

(Ghonyan, 2017). Along with this, through the way of issuing shares the newer and the less

known corporates can create publicity which results into creating the new business

opportunities. Apart from this, there are other benefits of being listed on a stock exchange

like increase in the motivation level of the employees. Another crucial advantage is that it

creates awareness about the company’s products and services to the potential customer group.

Along these lines, this may prompt an expansion in market share for the organization. An

IPO additionally might be utilized by establishing people as an exit strategy or procedure.

Many investors have utilized IPOs to take advantage of fruitful organizations that they helped

starting up.

Disadvantages:

One significant downside of listing on stock exchange by utilizing an IPO is the time and cost

of experiencing the cycle. It's basic for an IPO to take somewhere in the range of six to nine

months or more (Matuszyk and Rymkiewicz, 2018). During this time, the organization's

supervisory group is probably going to be centred around that IPO, which could make other

areas of the business suffer. Additionally, it costs money to proceed with an IPO, from

monetary assistance and underwriting expenses to documenting charges. What's more, when

an organization opens up to the public, it gets subject to a large group of extra detailing and

revelation necessities, all of which likewise cost huge money.

(c) The methods of flotation in the primary market along with advantages and disadvantages

are stated below.

Offer through prospectus: It refers to inviting subscription for the shares through the way of

issue of prospectus. The advantage of this to create trust among the subscriber but on the

other side, it is a complex process and requires compliance with the various regulations.

Offer for sale: In this method, securities are not issued directly to the public but are provided

for sale by the intermediaries such as the issuing houses or brokers (Kocoń, 2017). The

benefits for using this method is saving the underwriting expenses along with getting

expertise of the issuing house. In contrast to it, this method limits the bidding window and

limited reservation for the retail investors.

Private Placement: Under this approach, the allotment of the securities is being done to the

institutional investors and other selected individuals. The advantage of this is that company

can select to whom shares to be offered and it requires less investment of time and money.

The disadvantage is that it limits the number of investors and reduced market having long

term effect.

(Ghonyan, 2017). Along with this, through the way of issuing shares the newer and the less

known corporates can create publicity which results into creating the new business

opportunities. Apart from this, there are other benefits of being listed on a stock exchange

like increase in the motivation level of the employees. Another crucial advantage is that it

creates awareness about the company’s products and services to the potential customer group.

Along these lines, this may prompt an expansion in market share for the organization. An

IPO additionally might be utilized by establishing people as an exit strategy or procedure.

Many investors have utilized IPOs to take advantage of fruitful organizations that they helped

starting up.

Disadvantages:

One significant downside of listing on stock exchange by utilizing an IPO is the time and cost

of experiencing the cycle. It's basic for an IPO to take somewhere in the range of six to nine

months or more (Matuszyk and Rymkiewicz, 2018). During this time, the organization's

supervisory group is probably going to be centred around that IPO, which could make other

areas of the business suffer. Additionally, it costs money to proceed with an IPO, from

monetary assistance and underwriting expenses to documenting charges. What's more, when

an organization opens up to the public, it gets subject to a large group of extra detailing and

revelation necessities, all of which likewise cost huge money.

(c) The methods of flotation in the primary market along with advantages and disadvantages

are stated below.

Offer through prospectus: It refers to inviting subscription for the shares through the way of

issue of prospectus. The advantage of this to create trust among the subscriber but on the

other side, it is a complex process and requires compliance with the various regulations.

Offer for sale: In this method, securities are not issued directly to the public but are provided

for sale by the intermediaries such as the issuing houses or brokers (Kocoń, 2017). The

benefits for using this method is saving the underwriting expenses along with getting

expertise of the issuing house. In contrast to it, this method limits the bidding window and

limited reservation for the retail investors.

Private Placement: Under this approach, the allotment of the securities is being done to the

institutional investors and other selected individuals. The advantage of this is that company

can select to whom shares to be offered and it requires less investment of time and money.

The disadvantage is that it limits the number of investors and reduced market having long

term effect.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Right issue: This is the privilege being offered to the existing shareholders for subscribing

the new shares as per the terms of the issue. The main benefit is that it is cheaper than public

issue but it also puts limitation on the amount that can be raised.

E – IPO: Under this, the company proposing the issue of shares to the general public goes

through the way of online system of the exchange by the way of entering into an agreement

with the stock exchange. Advantage is it compliance with all the guidelines as per exchange

but the company needs to appoint registrar for having electronic connectivity with the

exchange.

(d) Number of shares already issued by the company = 28 million

Current share price = 300p

Amount raised through right issue = (28 million *4/7) * 240p = 16 million * 240p =

3840p million

Theoretical Ex-rights Price = (New Shares × Issue Price + Old Shares × Market Price)/

(New Shares + Old Shares)

= (16 * 240 + 28 * 300) / (16+28) = 278p

Therefore, the shares are likely to be traded at 278p after the new issue of shares.

(e) Understanding the impact of right issue on the wealth of the investor having 35,000 shares

of Dare plc.

If she takes up her rights: Under this, situation, the shares held is 35,000 and the

value of current holding will be 10,500,000p (35,000*300p). the number of shares being

available through the right issue is = 35,000 * 4/7 = 20,000 shares. The cost to be incurred for

participating in the right issue = 20,000 * 240p = 4,800,000p. Therefore, the total number of

holdings after the right issue will be 35,000 + 20,000 = 55,000. Also, the value of portfolio

including investment from rights will be 15,300,000p (10,500,000p + 4,800,000p). Along

with this, the ex-right price post right issue will be = 15,300,000 / 55,000 = 278p.

It can eb interpreted from the above that it will be beneficial for the investor as even

though the investor has paid 240p for each share, but it will be theoretically be anticipated to

be worth at 278p post the issue.

If she sells on her rights: There are times when the shareholder decides to take no

action but the preferential rights being given here are come with the risk of dilution. In the

given case, the shareholder would be left with only 35,000 shares post the issue. For example,

if the price remains same with ex right price, this will mean that the ex-right shares which

were earlier valued at 10,500,000p would be valued at 13,230,000p after the issue. This is the

starting of the effects as the shares will be further impacted in the future also. For instance,

the new shares as per the terms of the issue. The main benefit is that it is cheaper than public

issue but it also puts limitation on the amount that can be raised.

E – IPO: Under this, the company proposing the issue of shares to the general public goes

through the way of online system of the exchange by the way of entering into an agreement

with the stock exchange. Advantage is it compliance with all the guidelines as per exchange

but the company needs to appoint registrar for having electronic connectivity with the

exchange.

(d) Number of shares already issued by the company = 28 million

Current share price = 300p

Amount raised through right issue = (28 million *4/7) * 240p = 16 million * 240p =

3840p million

Theoretical Ex-rights Price = (New Shares × Issue Price + Old Shares × Market Price)/

(New Shares + Old Shares)

= (16 * 240 + 28 * 300) / (16+28) = 278p

Therefore, the shares are likely to be traded at 278p after the new issue of shares.

(e) Understanding the impact of right issue on the wealth of the investor having 35,000 shares

of Dare plc.

If she takes up her rights: Under this, situation, the shares held is 35,000 and the

value of current holding will be 10,500,000p (35,000*300p). the number of shares being

available through the right issue is = 35,000 * 4/7 = 20,000 shares. The cost to be incurred for

participating in the right issue = 20,000 * 240p = 4,800,000p. Therefore, the total number of

holdings after the right issue will be 35,000 + 20,000 = 55,000. Also, the value of portfolio

including investment from rights will be 15,300,000p (10,500,000p + 4,800,000p). Along

with this, the ex-right price post right issue will be = 15,300,000 / 55,000 = 278p.

It can eb interpreted from the above that it will be beneficial for the investor as even

though the investor has paid 240p for each share, but it will be theoretically be anticipated to

be worth at 278p post the issue.

If she sells on her rights: There are times when the shareholder decides to take no

action but the preferential rights being given here are come with the risk of dilution. In the

given case, the shareholder would be left with only 35,000 shares post the issue. For example,

if the price remains same with ex right price, this will mean that the ex-right shares which

were earlier valued at 10,500,000p would be valued at 13,230,000p after the issue. This is the

starting of the effects as the shares will be further impacted in the future also. For instance,

the income of the company which is being distributed in the form of dividends will now be

distributed among 44 million shares rather than 28 million.

SECTION B

Question 4

(a) Contrast the Interest Rate Parity Theorem and Purchasing Power Parity Theorem

The theory of the purchasing power parity (PPP) states that the FOREX rate should be

determined by the relative prices in respect to the similar basket of the goods among the two

countries. The possible variation in the inflation rate of a particular country requires to be

balanced by the opposite variation of the nation’s exchange rate. Therefore, if the price of the

nation is surging due to the reason of inflation then the nation’s exchange rate should also fall

in order to return back to the parity (Papadamou and Theodosiou, 2019). In contrast to it, if

the two currencies are having a different interest rates then this will be accounted as the

discount or the premium in respect to the exchange rate with the purpose to avoid the

arbitrage chances. The interest rate parity works by connecting the interest, spot exchange

and the forex rates which plays an important role in the foreign exchange market. This theory

puts stress on the fact that the size of the premium or the discount on the foreign currency is

equivalent to the variation among the spot and forward interest rates of the countries in

comparison.

(b) Identifying the best foreign exchange hedge for Teller to undertake

Forward market hedge

Sell CAD$425,000, 6 months forward to produce a receipt of:

CAD$425,000 * 1.6765 = £712512.5 is the amount receivable in 6 months’ time.

Money market hedge

Now 6 months

Borrow CAD$412621

(425000/1.03)

Canadian borrowing rate

1.03

Receive CAD$425,000 and

settle the liability

Convert at spot 1.646

Deposit amount £679174

(412621*1.646)

Pound deposit rate 1.015 Final income £689361.61

(679174*1.015)

As this is smaller amount than received from the forward market hedge, therefore, it can be

stated that the forward market support gives the better result.

(c) No, it is not recommended to Teller to offer its Canadian customers a discount of 1.5% on

the invoice in exchange for leading the payment instead of entering into the hedge. The

distributed among 44 million shares rather than 28 million.

SECTION B

Question 4

(a) Contrast the Interest Rate Parity Theorem and Purchasing Power Parity Theorem

The theory of the purchasing power parity (PPP) states that the FOREX rate should be

determined by the relative prices in respect to the similar basket of the goods among the two

countries. The possible variation in the inflation rate of a particular country requires to be

balanced by the opposite variation of the nation’s exchange rate. Therefore, if the price of the

nation is surging due to the reason of inflation then the nation’s exchange rate should also fall

in order to return back to the parity (Papadamou and Theodosiou, 2019). In contrast to it, if

the two currencies are having a different interest rates then this will be accounted as the

discount or the premium in respect to the exchange rate with the purpose to avoid the

arbitrage chances. The interest rate parity works by connecting the interest, spot exchange

and the forex rates which plays an important role in the foreign exchange market. This theory

puts stress on the fact that the size of the premium or the discount on the foreign currency is

equivalent to the variation among the spot and forward interest rates of the countries in

comparison.

(b) Identifying the best foreign exchange hedge for Teller to undertake

Forward market hedge

Sell CAD$425,000, 6 months forward to produce a receipt of:

CAD$425,000 * 1.6765 = £712512.5 is the amount receivable in 6 months’ time.

Money market hedge

Now 6 months

Borrow CAD$412621

(425000/1.03)

Canadian borrowing rate

1.03

Receive CAD$425,000 and

settle the liability

Convert at spot 1.646

Deposit amount £679174

(412621*1.646)

Pound deposit rate 1.015 Final income £689361.61

(679174*1.015)

As this is smaller amount than received from the forward market hedge, therefore, it can be

stated that the forward market support gives the better result.

(c) No, it is not recommended to Teller to offer its Canadian customers a discount of 1.5% on

the invoice in exchange for leading the payment instead of entering into the hedge. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reason behind is that if the Teller Ltd, does not enter into hedge then there might be chances

of getting into a huge risk. In case the currency appreciates in the future then the seller will be

receiving the less amount or pound against the CAD $. The exporter or the Teller Ltd can

offset the CAD$ and pounds futures at the present value and then sell them after 6 months.

By doing this, the exporter can protect itself from the fall in the profits which will help in

compensating the loss which was incurred on the export transaction. Therefore, through the

way of hedging Teller can eliminate the loss incurred in the foreign exchange and the protect

the expected profits.

(d) The other internal hedging techniques that can be used by Teller Ltd are stated below.

Exposure netting: This technique involves creating exposure in the daily business

that offsets the current exposure. This process of making adjustment in the foreign currency

being receivable and payable at a specific time is known as the netting. The exposure created

can be in the same currency or in the other currency (Denga and Jain, 2017). But it is

important to note that the effect should be such that, that any movement in the exchange rate

which might result into loss over the original exposure should also result into gain in respect

to the new exposure. The main objective behind this technique is to offset the likeliness of the

loss in one exposure with the expected gain in the other.

Sourcing: This is a more specific exposure netting in which the company buys the

raw material under the same currency in which the company sells its products. This results

into netting of the transaction in some extent. This is because, when receivables are sold

lower price is received and when payables are bought company pays high. So, it makes sense

to settle the receivables and payables in part or whole.

of getting into a huge risk. In case the currency appreciates in the future then the seller will be

receiving the less amount or pound against the CAD $. The exporter or the Teller Ltd can

offset the CAD$ and pounds futures at the present value and then sell them after 6 months.

By doing this, the exporter can protect itself from the fall in the profits which will help in

compensating the loss which was incurred on the export transaction. Therefore, through the

way of hedging Teller can eliminate the loss incurred in the foreign exchange and the protect

the expected profits.

(d) The other internal hedging techniques that can be used by Teller Ltd are stated below.

Exposure netting: This technique involves creating exposure in the daily business

that offsets the current exposure. This process of making adjustment in the foreign currency

being receivable and payable at a specific time is known as the netting. The exposure created

can be in the same currency or in the other currency (Denga and Jain, 2017). But it is

important to note that the effect should be such that, that any movement in the exchange rate

which might result into loss over the original exposure should also result into gain in respect

to the new exposure. The main objective behind this technique is to offset the likeliness of the

loss in one exposure with the expected gain in the other.

Sourcing: This is a more specific exposure netting in which the company buys the

raw material under the same currency in which the company sells its products. This results

into netting of the transaction in some extent. This is because, when receivables are sold

lower price is received and when payables are bought company pays high. So, it makes sense

to settle the receivables and payables in part or whole.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Bird, G., Du, W. and Willett, T., 2017. Behavioral finance and efficient markets: What does

the euro crisis tell us?. Open Economies Review. 28(2). pp.273-295.

Denga, S. and Jain, A., 2017. Forex risk management for multinationals: internal and external

hedging techniques. In София (Vol. 280, pp. 51-61).

Ferrer-Comalat, J. C., Linares-Mustaros, S. and Corominas-Coll, D., 2016. A MODEL FOR

OPTIMAL INVESTMENT PROJECT CHOICE USING FUZZY

PROBABILITY. Economic Computation & Economic Cybernetics Studies &

Research. 50(4).

Filip, A., Ghio, A. and Paugam, L., 2020. Accounting information in innovative small cap

firms: evidence from London’s alternative investment market. Accounting and

Business Research. pp.1-36.

Ghonyan, L., 2017. Advantages and Disadvantages of Going Public and Becoming a Listed

Company. Available at SSRN 2995271.

Kocoń, K., 2017. The Management of Flotation in Corporative Debenture

Expense. Przedsiębiorstwo we współczesnej gospodarce–teoria i praktyka. 22(3).

pp.231-248.

Libson, A., 2018. Taking Shareholders' Social Preferences Seriously: Confronting a New

Agency Problem. UC Irvine L. Rev.. 9. p.699.

Matuszyk, I. and Rymkiewicz, B., 2018. Integrated Reporting as a Tool for Communicating

with Stakeholders–Advantages and Disadvantages. In E3S Web of Conferences (Vol.

35, p. 06004). EDP Sciences.

Papadamou, S. and Theodosiou, E., 2019. An empirical investigation of covered interest rate

parity: the case of the GBP/USD and SEK/USD exchange rates. International

Journal of Financial Engineering and Risk Management. 3(2). pp.114-129.

Yoshino, N. and Taghizadeh-Hesary, F., 2017. Solutions for small and medium-sized

entreprises' difficulties in accessing finance: Asian experiences (No. 768). ADBI

Working Paper.

Books and Journals

Bird, G., Du, W. and Willett, T., 2017. Behavioral finance and efficient markets: What does

the euro crisis tell us?. Open Economies Review. 28(2). pp.273-295.

Denga, S. and Jain, A., 2017. Forex risk management for multinationals: internal and external

hedging techniques. In София (Vol. 280, pp. 51-61).

Ferrer-Comalat, J. C., Linares-Mustaros, S. and Corominas-Coll, D., 2016. A MODEL FOR

OPTIMAL INVESTMENT PROJECT CHOICE USING FUZZY

PROBABILITY. Economic Computation & Economic Cybernetics Studies &

Research. 50(4).

Filip, A., Ghio, A. and Paugam, L., 2020. Accounting information in innovative small cap

firms: evidence from London’s alternative investment market. Accounting and

Business Research. pp.1-36.

Ghonyan, L., 2017. Advantages and Disadvantages of Going Public and Becoming a Listed

Company. Available at SSRN 2995271.

Kocoń, K., 2017. The Management of Flotation in Corporative Debenture

Expense. Przedsiębiorstwo we współczesnej gospodarce–teoria i praktyka. 22(3).

pp.231-248.

Libson, A., 2018. Taking Shareholders' Social Preferences Seriously: Confronting a New

Agency Problem. UC Irvine L. Rev.. 9. p.699.

Matuszyk, I. and Rymkiewicz, B., 2018. Integrated Reporting as a Tool for Communicating

with Stakeholders–Advantages and Disadvantages. In E3S Web of Conferences (Vol.

35, p. 06004). EDP Sciences.

Papadamou, S. and Theodosiou, E., 2019. An empirical investigation of covered interest rate

parity: the case of the GBP/USD and SEK/USD exchange rates. International

Journal of Financial Engineering and Risk Management. 3(2). pp.114-129.

Yoshino, N. and Taghizadeh-Hesary, F., 2017. Solutions for small and medium-sized

entreprises' difficulties in accessing finance: Asian experiences (No. 768). ADBI

Working Paper.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.