Financial Accounting Report: Analysis of Persimmon PLC's Performance

VerifiedAdded on 2020/01/28

|13

|2476

|61

Report

AI Summary

This financial accounting report provides a detailed analysis of Persimmon PLC's financial performance. It begins with an introduction to financial accounting and its significance. The report then delves into ratio analysis, covering liquidity, solvency, efficiency, and profitability ratios for 2014 and 2015, offering interpretations and insights. A share price analysis of Persimmon over a 12-month period is presented, accompanied by interpretations of monthly trends. Furthermore, the report includes a trend analysis of the company's financial statements, focusing on the income statement and balance sheet. The conclusion summarizes the key findings and offers recommendations. Overall, the report assesses the company's financial health and performance.

Financial accounting report

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Table of Contents..................................................................................................................................2

Introduction..........................................................................................................................................3

Accounting ratios Analysis..............................................................................................................3

Share price analysis of Persimmon over the 12 months..................................................................5

Trend analysis of financial statements of Persimmon.....................................................................7

CONCLUSION ...................................................................................................................................9

REFERENCES...................................................................................................................................12

2

Table of Contents..................................................................................................................................2

Introduction..........................................................................................................................................3

Accounting ratios Analysis..............................................................................................................3

Share price analysis of Persimmon over the 12 months..................................................................5

Trend analysis of financial statements of Persimmon.....................................................................7

CONCLUSION ...................................................................................................................................9

REFERENCES...................................................................................................................................12

2

Illustration Index

Illustration 1: Ratio analysis.................................................................................................................5

Illustration 2: Share price analysis.......................................................................................................7

Illustration 3: Interactive chart of Persimmon......................................................................................8

Illustration 4: Income statement of Persimmon....................................................................................9

Illustration 5: Balance sheet of Permission PLC................................................................................11

3

Illustration 1: Ratio analysis.................................................................................................................5

Illustration 2: Share price analysis.......................................................................................................7

Illustration 3: Interactive chart of Persimmon......................................................................................8

Illustration 4: Income statement of Persimmon....................................................................................9

Illustration 5: Balance sheet of Permission PLC................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is recording of financial transactions by preparing financial statements

available for public to review the performance of the business which helps in taking decision to

invest in the company. Financial accounting is governed by the local and and international

accounting standards. Financial statements prepared under this head according to the Generally

Accepted accounting principles from beginning till its end. Persimmon company has been selected

for this project report and it is listed in London stock exchange. It is public limited company which

is a British housebuilding company located in York in England. It is a former constituent of the

FTSE 100 index in the London stock exchange market.

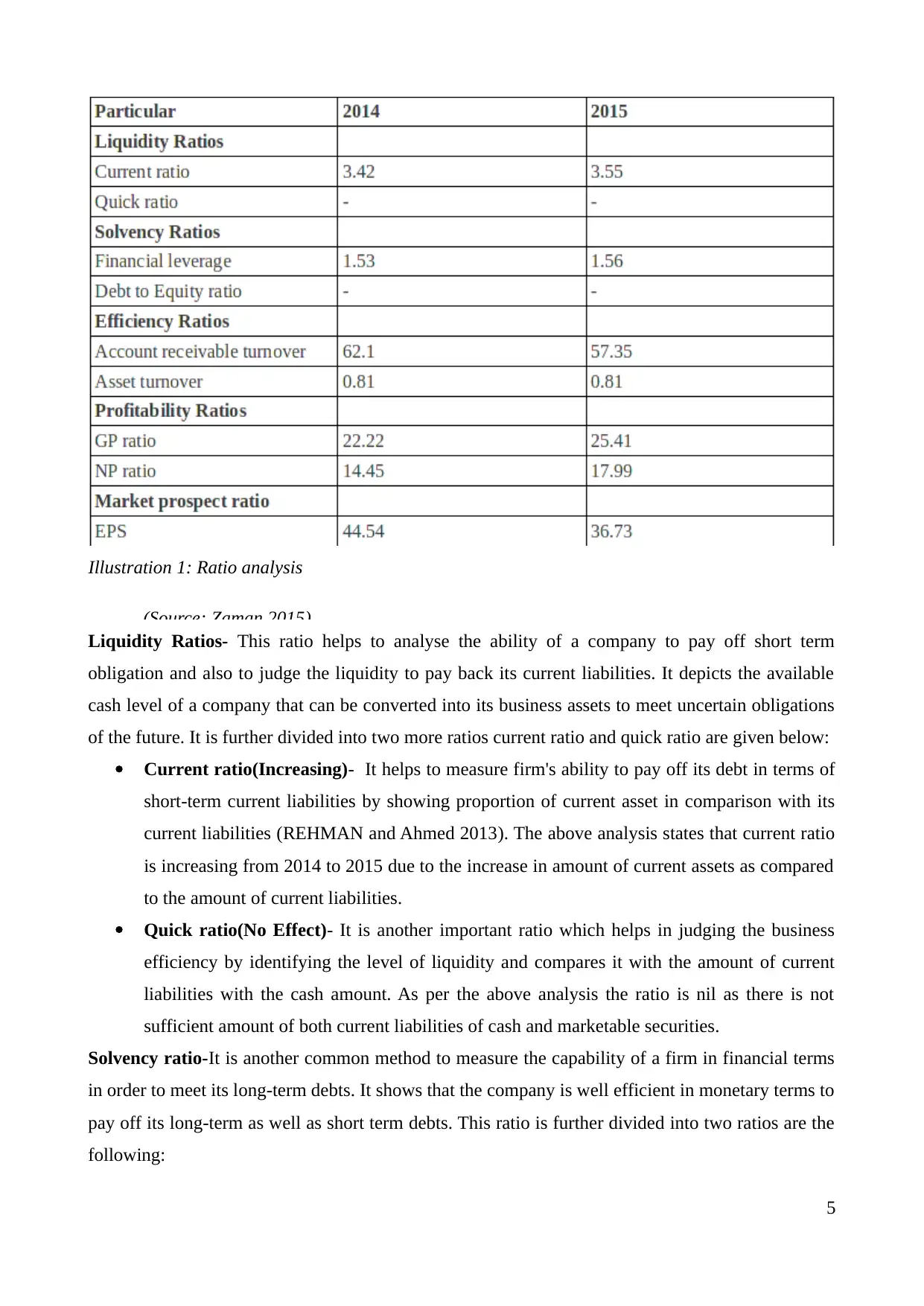

Accounting ratios Analysis

Ratio analysis is an quantitative analysis of financial information contained in the financial

statements of the company (Wessels 2012). It is based on line items in financial statements like the

balance sheet income statement and cash flow statements as these are the standard forms of the

financial statements. These are also known as mathematical comparisons of financial statements

accounts or categories. It defines the relationship between the financial statement accounts with

different stakeholders such as investors, creditors and internal management to understand the

business activities. It also denotes different areas in the company which requires improvements.

Following are the ratio analysis of Persimmon company of Two years 2014 and 2015 given below

are:

4

Financial accounting is recording of financial transactions by preparing financial statements

available for public to review the performance of the business which helps in taking decision to

invest in the company. Financial accounting is governed by the local and and international

accounting standards. Financial statements prepared under this head according to the Generally

Accepted accounting principles from beginning till its end. Persimmon company has been selected

for this project report and it is listed in London stock exchange. It is public limited company which

is a British housebuilding company located in York in England. It is a former constituent of the

FTSE 100 index in the London stock exchange market.

Accounting ratios Analysis

Ratio analysis is an quantitative analysis of financial information contained in the financial

statements of the company (Wessels 2012). It is based on line items in financial statements like the

balance sheet income statement and cash flow statements as these are the standard forms of the

financial statements. These are also known as mathematical comparisons of financial statements

accounts or categories. It defines the relationship between the financial statement accounts with

different stakeholders such as investors, creditors and internal management to understand the

business activities. It also denotes different areas in the company which requires improvements.

Following are the ratio analysis of Persimmon company of Two years 2014 and 2015 given below

are:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Illustration 1: Ratio analysis

(Source: Zaman 2015)

Liquidity Ratios- This ratio helps to analyse the ability of a company to pay off short term

obligation and also to judge the liquidity to pay back its current liabilities. It depicts the available

cash level of a company that can be converted into its business assets to meet uncertain obligations

of the future. It is further divided into two more ratios current ratio and quick ratio are given below:

Current ratio(Increasing)- It helps to measure firm's ability to pay off its debt in terms of

short-term current liabilities by showing proportion of current asset in comparison with its

current liabilities (REHMAN and Ahmed 2013). The above analysis states that current ratio

is increasing from 2014 to 2015 due to the increase in amount of current assets as compared

to the amount of current liabilities.

Quick ratio(No Effect)- It is another important ratio which helps in judging the business

efficiency by identifying the level of liquidity and compares it with the amount of current

liabilities with the cash amount. As per the above analysis the ratio is nil as there is not

sufficient amount of both current liabilities of cash and marketable securities.

Solvency ratio-It is another common method to measure the capability of a firm in financial terms

in order to meet its long-term debts. It shows that the company is well efficient in monetary terms to

pay off its long-term as well as short term debts. This ratio is further divided into two ratios are the

following:

5

(Source: Zaman 2015)

Liquidity Ratios- This ratio helps to analyse the ability of a company to pay off short term

obligation and also to judge the liquidity to pay back its current liabilities. It depicts the available

cash level of a company that can be converted into its business assets to meet uncertain obligations

of the future. It is further divided into two more ratios current ratio and quick ratio are given below:

Current ratio(Increasing)- It helps to measure firm's ability to pay off its debt in terms of

short-term current liabilities by showing proportion of current asset in comparison with its

current liabilities (REHMAN and Ahmed 2013). The above analysis states that current ratio

is increasing from 2014 to 2015 due to the increase in amount of current assets as compared

to the amount of current liabilities.

Quick ratio(No Effect)- It is another important ratio which helps in judging the business

efficiency by identifying the level of liquidity and compares it with the amount of current

liabilities with the cash amount. As per the above analysis the ratio is nil as there is not

sufficient amount of both current liabilities of cash and marketable securities.

Solvency ratio-It is another common method to measure the capability of a firm in financial terms

in order to meet its long-term debts. It shows that the company is well efficient in monetary terms to

pay off its long-term as well as short term debts. This ratio is further divided into two ratios are the

following:

5

Financial leverage(Increasing)- It is that ratio which defines that business require the need

of taking debt to acquire additional asset for the business such as equipment or machine. It

is also knowns as trading in equity in which business owner use its own money in the

business (Molnár 2015). The financial ratio is higher that means it increases the debt amount

which is not fruitful for company as it reduces the higher returns of the shareholders.

Debt to Equity ratio(NIL)- It is one of a kind of financial ratio indicating the relative

proportion of shareholders equity and debt used to finance its business projects. The debt

equity ratio proportion shows the overall balance among debt and equity in the business.

Efficiency Ratio- It used to analyse how well a company utilise their assets and liabilities internally

in order to reduces the impact of the external environment (Mathews and Lee 2016). This ratio is

explained further with the help of different ratios are:

Account receivable turnover(Positive)- It helps to calculate the total number of years

business can collect its average accounts receivable. The turnover of Persimmon company is

showing decrease in number of time period which is favourable condition for the company.

Asset turnover(Constant)- It helps to measure the efficiency of a business to use its assets

in generating sales revenue or sales income to the company. It shows the appropriate

proportion of assets in terms of its total sales turnover. From the above analysis it can be

said that the ratio remains the same from one period to the another period.

Profitability Ratios- It checks the ability of a firm in generating higher amount of sales or revenue

as compared to expenses spend by the firm. This is further describing in another forms of this ratio

to judge the financial performance of Persimmon PLC by identifying its profitability are:

Gross profit ratio(Increasing)- It refers to a profitability ratio that shows the relationship

between gross profit and total net sales revenue (Edwards 2013). The ratio of the current

business is showing increasing trend from one period to another period.

Net profit ratio(Relatively increasing)- The net profit is that ratio of after tax profits to net

sales which reveals the remaining profit after considering all costs of

production,administration, and financing. It is showing increasing return of 5% from 2014 to

2015.

Market prospect ratio- These ratios are used to compare public companies share prices with other

financial measures to judge the efficiency of the earnings of the business. Investors used this ratio to

analyse future trends and help in figure out a stock's existing and future price.

EPS(Decreasing)- It is that ratio which helps to judge the efficiency of business in terms net

income per share against the total income available to shareholders to know the exact

amount.

6

of taking debt to acquire additional asset for the business such as equipment or machine. It

is also knowns as trading in equity in which business owner use its own money in the

business (Molnár 2015). The financial ratio is higher that means it increases the debt amount

which is not fruitful for company as it reduces the higher returns of the shareholders.

Debt to Equity ratio(NIL)- It is one of a kind of financial ratio indicating the relative

proportion of shareholders equity and debt used to finance its business projects. The debt

equity ratio proportion shows the overall balance among debt and equity in the business.

Efficiency Ratio- It used to analyse how well a company utilise their assets and liabilities internally

in order to reduces the impact of the external environment (Mathews and Lee 2016). This ratio is

explained further with the help of different ratios are:

Account receivable turnover(Positive)- It helps to calculate the total number of years

business can collect its average accounts receivable. The turnover of Persimmon company is

showing decrease in number of time period which is favourable condition for the company.

Asset turnover(Constant)- It helps to measure the efficiency of a business to use its assets

in generating sales revenue or sales income to the company. It shows the appropriate

proportion of assets in terms of its total sales turnover. From the above analysis it can be

said that the ratio remains the same from one period to the another period.

Profitability Ratios- It checks the ability of a firm in generating higher amount of sales or revenue

as compared to expenses spend by the firm. This is further describing in another forms of this ratio

to judge the financial performance of Persimmon PLC by identifying its profitability are:

Gross profit ratio(Increasing)- It refers to a profitability ratio that shows the relationship

between gross profit and total net sales revenue (Edwards 2013). The ratio of the current

business is showing increasing trend from one period to another period.

Net profit ratio(Relatively increasing)- The net profit is that ratio of after tax profits to net

sales which reveals the remaining profit after considering all costs of

production,administration, and financing. It is showing increasing return of 5% from 2014 to

2015.

Market prospect ratio- These ratios are used to compare public companies share prices with other

financial measures to judge the efficiency of the earnings of the business. Investors used this ratio to

analyse future trends and help in figure out a stock's existing and future price.

EPS(Decreasing)- It is that ratio which helps to judge the efficiency of business in terms net

income per share against the total income available to shareholders to know the exact

amount.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

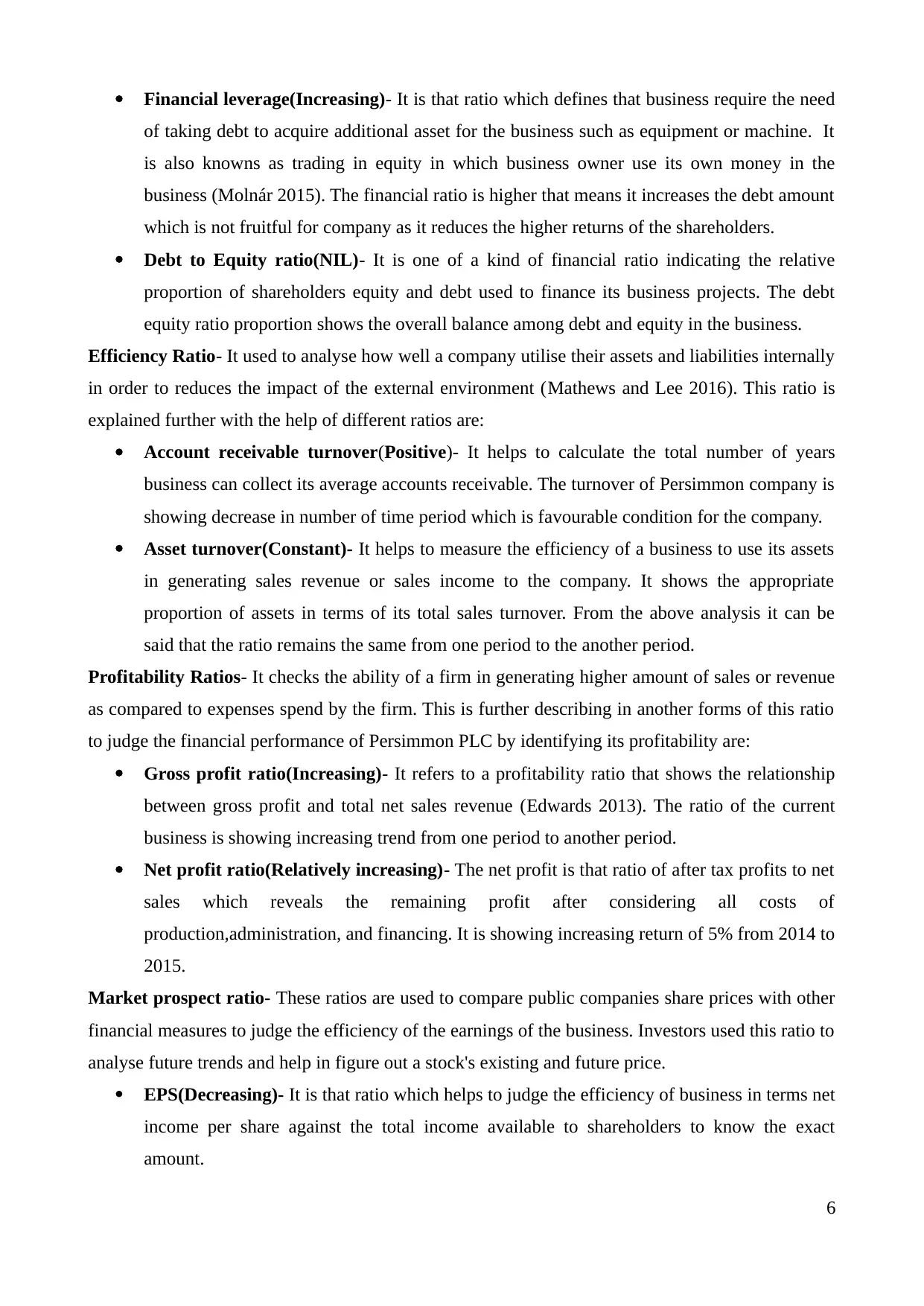

Share price analysis of Persimmon over the 12 months

Persimmon is one of the leading UK house builders company serving local markets with 28

offices and branches across the country. The share price of the company is 1695.00p

Illustration 2: Share price analysis

(Source: Edwards 2013 )

Interpretations

As per the above analysis of share price of the company its shows monthly division of share

prices. It starts from may with open price of 1957 and closes with the same amount which shows

that there will be no purchasing or selling of share prices during the day at the end. But the higher

and lower trend shows that the purchasing and selling exists but it will not create higher impact to

induce the level of share prices. The next opening amount in next month is higher than the previous

month that is 2094 and ends up with 2038 which is even adverse condition from the previous

situations (Dickinson and Sommers 2012). It is a conditions of loss for the company. Next month

opens up with 1441 and ending with 1540 which is good amount but decreasing in amount from the

previous month. Another month starts with share price of 1715 and closes with 1640 which shows

the inability of an enterprise to meet their debt6 obligations and suffered loss in the capital market.

From the above analysis it can be stated that the monthly trend of the share prices shows adverse

effect on the financial performance of the business and unable to attract more shareholders and

business clients to invest in the company. The investors will not invest in that company which is

loosing their market share and goes in to the debt trap.

7

Persimmon is one of the leading UK house builders company serving local markets with 28

offices and branches across the country. The share price of the company is 1695.00p

Illustration 2: Share price analysis

(Source: Edwards 2013 )

Interpretations

As per the above analysis of share price of the company its shows monthly division of share

prices. It starts from may with open price of 1957 and closes with the same amount which shows

that there will be no purchasing or selling of share prices during the day at the end. But the higher

and lower trend shows that the purchasing and selling exists but it will not create higher impact to

induce the level of share prices. The next opening amount in next month is higher than the previous

month that is 2094 and ends up with 2038 which is even adverse condition from the previous

situations (Dickinson and Sommers 2012). It is a conditions of loss for the company. Next month

opens up with 1441 and ending with 1540 which is good amount but decreasing in amount from the

previous month. Another month starts with share price of 1715 and closes with 1640 which shows

the inability of an enterprise to meet their debt6 obligations and suffered loss in the capital market.

From the above analysis it can be stated that the monthly trend of the share prices shows adverse

effect on the financial performance of the business and unable to attract more shareholders and

business clients to invest in the company. The investors will not invest in that company which is

loosing their market share and goes in to the debt trap.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

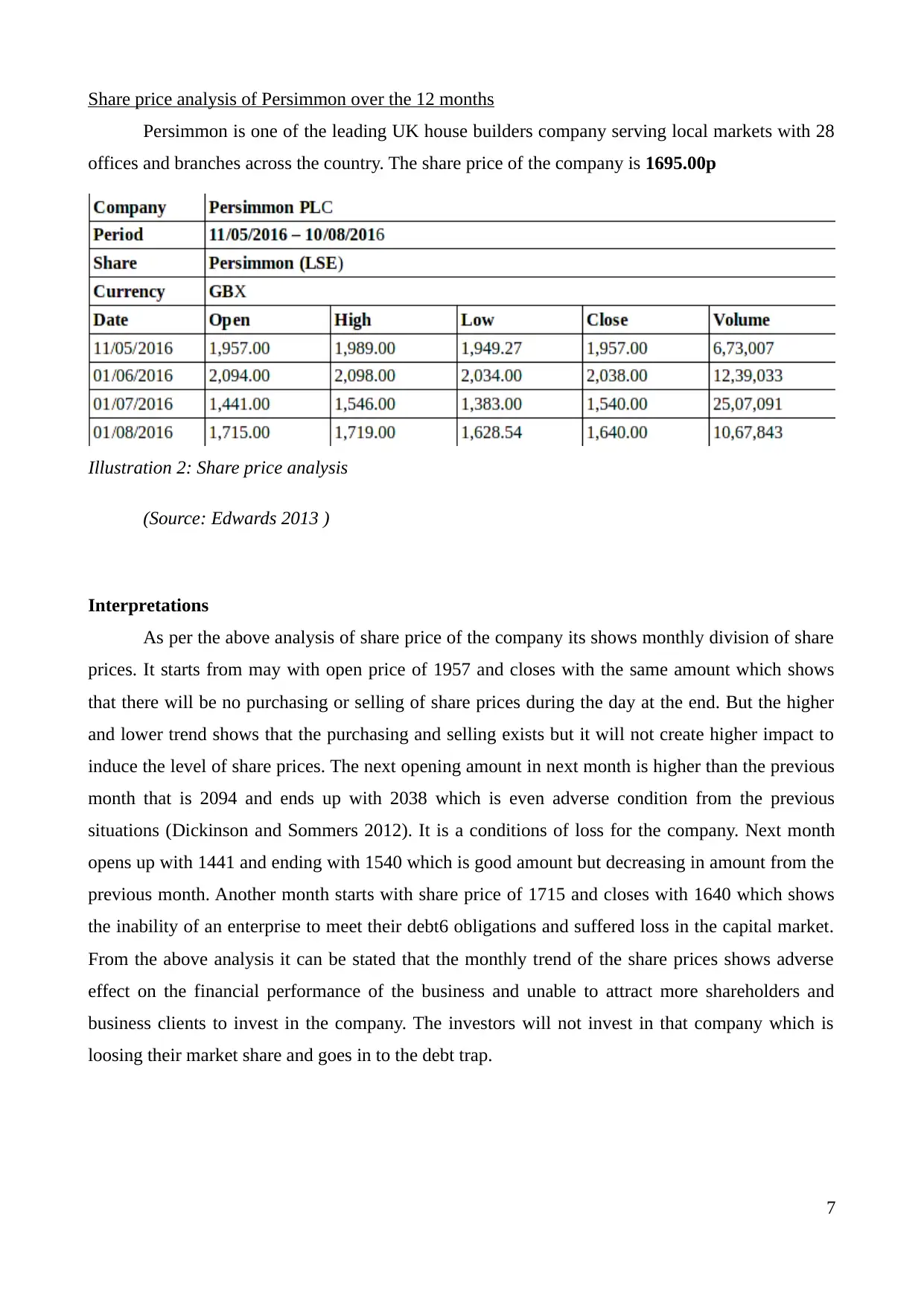

Interpretations

From the above interactive chart of Persimmon which is a public limited company describes

the different trends of the share prices of the company. It depicts that in 2015 the share price is

higher and slowly slanting to towards downward slope. The share price is slightly decreasing in the

moth of august in the year 2016. It shows many differentiation in the overall trends due to

fluctuations in the amount of share prices due to the future uncertainties.

Trend analysis of financial statements of Persimmon

8

Illustration 3: Interactive chart of Persimmon

(Source:Cordis 2014 )

From the above interactive chart of Persimmon which is a public limited company describes

the different trends of the share prices of the company. It depicts that in 2015 the share price is

higher and slowly slanting to towards downward slope. The share price is slightly decreasing in the

moth of august in the year 2016. It shows many differentiation in the overall trends due to

fluctuations in the amount of share prices due to the future uncertainties.

Trend analysis of financial statements of Persimmon

8

Illustration 3: Interactive chart of Persimmon

(Source:Cordis 2014 )

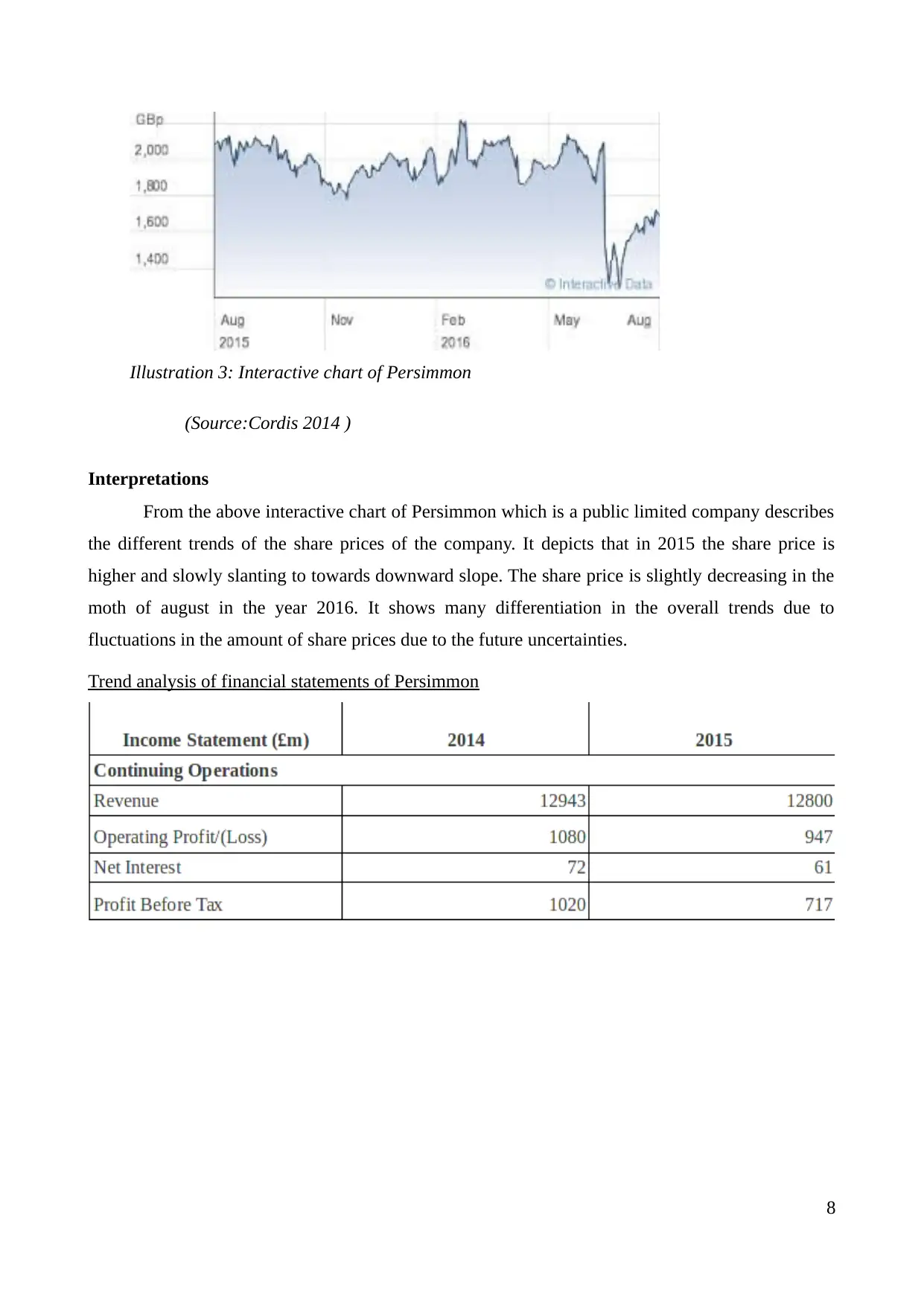

Illustration 4: Income statement of Persimmon

(Source: Wessels 2012)

Income statements- It is that statement which helps in measuring the profitability of the company

by calculating profit of the year in order to attract an individual towards the business. The investors

and shareholders get impressed by the profitability of the business and attract them to invest in the

company. From the above analysis it has been observed that the amount of profit is higher as

compared to 2015. It shows relevant areas of the improvements in the existing business process to

amend them according to the various needs of the external and dynamic environment which is

constantly changing (Weil and Schipper 2013). Tax is that component which have strong impact on

the profitability of the business in terms of reducing the amount of profit. The profitability can be

positive or negative is totally depends on the capability of the business to react in the dangerous

situations positively or negatively. A statement showing all the income and expenditure of the

company. It shows the business better way of increasing their performance over a certain time

period. It shows the profitability of the company such as gross profit and gross loss. It also includes

the amount of revenue, sales and cost of goods sold.

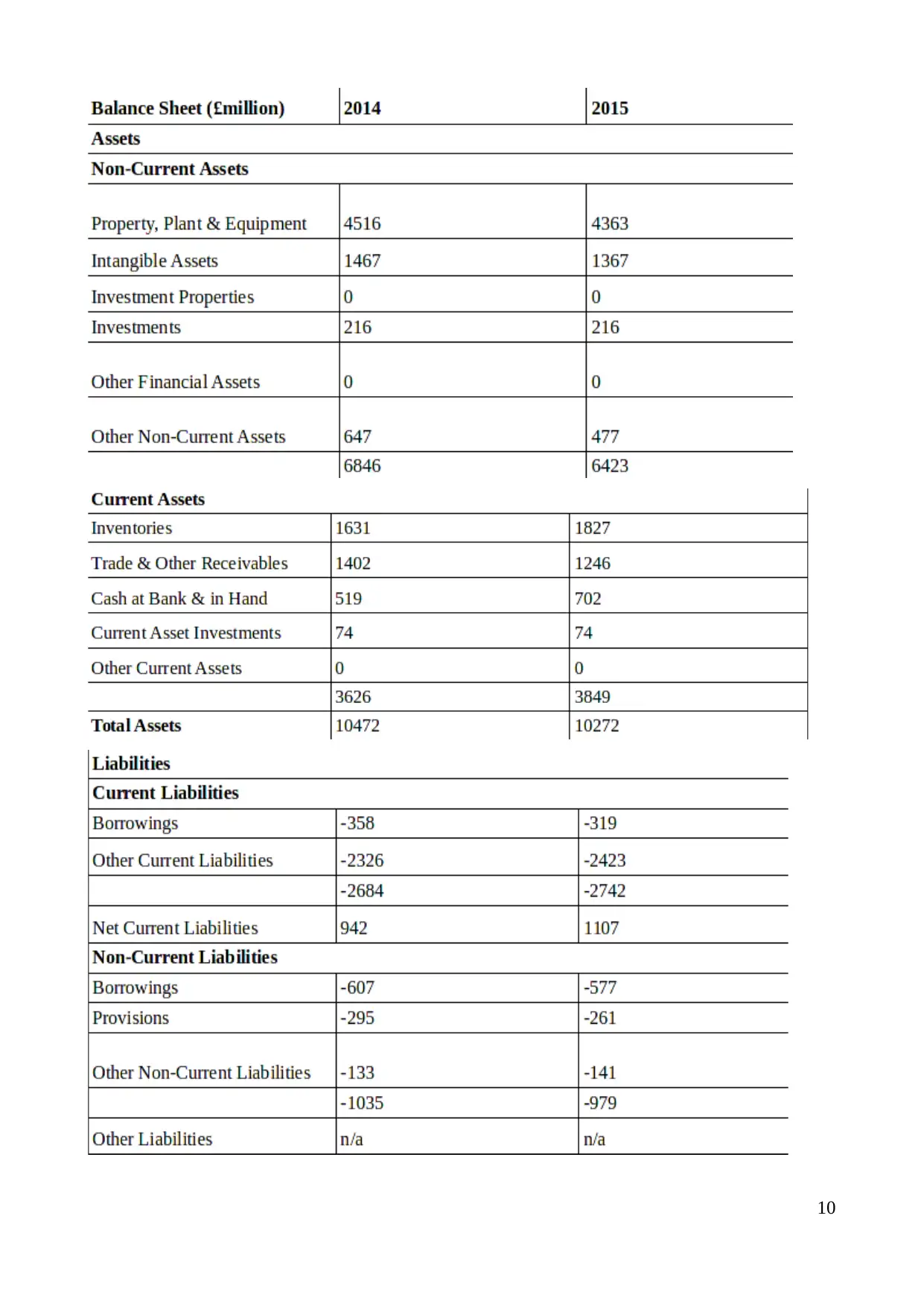

Balance sheet- It is most common form of the financial statements which helps to identify the exact

position of the company in the current business scenario. It is also known as position statements

which describes the position of the business among different competitors and other external

members. It determines the financial position of the company for a particular time period. It has two

dimensions asset and the liabilities. It includes accounting equation (Assets= Liabilities+ Owner's

equity). The company prepare accounts as per international accounting standard provision so as to

know their financial position (Choi 2015). It includes heads such as fixed asset, current asset,

current liabilities, non current liabilities as well as shareholder's equity. It has been observed that the

company is showing higher balance in 2014 than 2015.

9

(Source: Wessels 2012)

Income statements- It is that statement which helps in measuring the profitability of the company

by calculating profit of the year in order to attract an individual towards the business. The investors

and shareholders get impressed by the profitability of the business and attract them to invest in the

company. From the above analysis it has been observed that the amount of profit is higher as

compared to 2015. It shows relevant areas of the improvements in the existing business process to

amend them according to the various needs of the external and dynamic environment which is

constantly changing (Weil and Schipper 2013). Tax is that component which have strong impact on

the profitability of the business in terms of reducing the amount of profit. The profitability can be

positive or negative is totally depends on the capability of the business to react in the dangerous

situations positively or negatively. A statement showing all the income and expenditure of the

company. It shows the business better way of increasing their performance over a certain time

period. It shows the profitability of the company such as gross profit and gross loss. It also includes

the amount of revenue, sales and cost of goods sold.

Balance sheet- It is most common form of the financial statements which helps to identify the exact

position of the company in the current business scenario. It is also known as position statements

which describes the position of the business among different competitors and other external

members. It determines the financial position of the company for a particular time period. It has two

dimensions asset and the liabilities. It includes accounting equation (Assets= Liabilities+ Owner's

equity). The company prepare accounts as per international accounting standard provision so as to

know their financial position (Choi 2015). It includes heads such as fixed asset, current asset,

current liabilities, non current liabilities as well as shareholder's equity. It has been observed that the

company is showing higher balance in 2014 than 2015.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

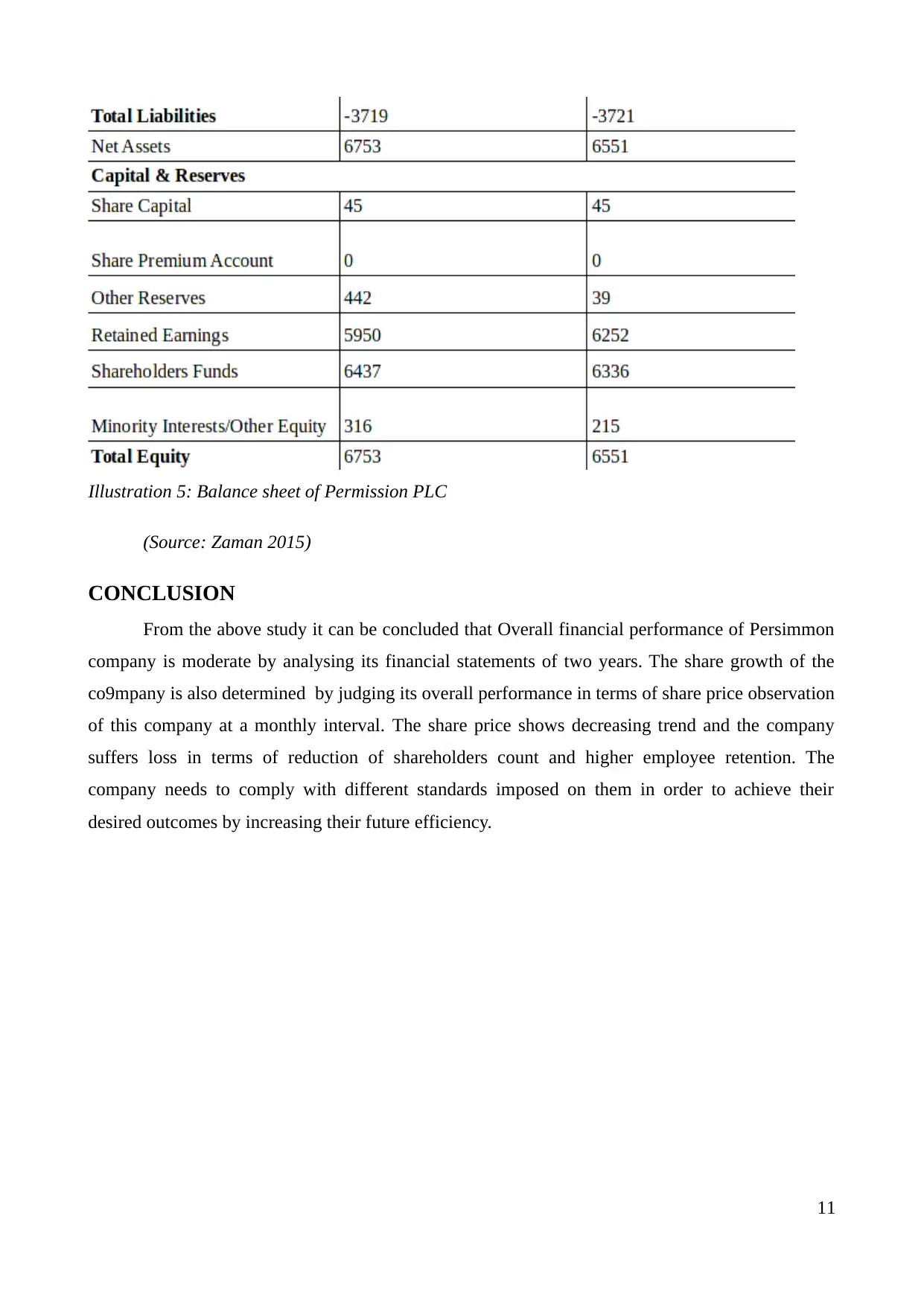

Illustration 5: Balance sheet of Permission PLC

(Source: Zaman 2015)

CONCLUSION

From the above study it can be concluded that Overall financial performance of Persimmon

company is moderate by analysing its financial statements of two years. The share growth of the

co9mpany is also determined by judging its overall performance in terms of share price observation

of this company at a monthly interval. The share price shows decreasing trend and the company

suffers loss in terms of reduction of shareholders count and higher employee retention. The

company needs to comply with different standards imposed on them in order to achieve their

desired outcomes by increasing their future efficiency.

11

(Source: Zaman 2015)

CONCLUSION

From the above study it can be concluded that Overall financial performance of Persimmon

company is moderate by analysing its financial statements of two years. The share growth of the

co9mpany is also determined by judging its overall performance in terms of share price observation

of this company at a monthly interval. The share price shows decreasing trend and the company

suffers loss in terms of reduction of shareholders count and higher employee retention. The

company needs to comply with different standards imposed on them in order to achieve their

desired outcomes by increasing their future efficiency.

11

REFERENCES

Books and Journals

Choi, Y. J. and et.al., 2015. Trend Analysis of 1-Day Probable Maximum Precipitation.Journal of

Korean Society of Hazard Mitigation.15(1). pp.369-375.

Cordis, A. S., 2014. Accounting Ratios and the Cross‐section of Expected Stock Returns.Journal of

Business Finance & Accounting.41(9-10). pp.1157-1192.

Dickinson, V. and Sommers, G. A., 2012. Which competitive efforts lead to future abnormal

economic rents? Using accounting ratios to assess competitive advantage.Journal of Business

Finance & Accounting. 39(3‐4). pp.360-398.

Edwards, J. R., 2013.A History of Financial Accounting (RLE Accounting)(Vol. 29). Routledge.

Gatua, F. K., 2013.Analysis of share price determinants at Nairobi Securities Exchange(Doctoral

dissertation, School of Business, University of Nairobi).

Mao, A. and Iravani, M. R., 2014. A trend-oriented power system security analysis method based on

load profile.IEEE Transactions on Power Systems. 29(3). pp.1279-1286.

Mathews, B., Lee 2016. Impact of a new mandatory reporting law on reporting and identification of

child sexual abuse: a seven year time trend analysis.Child abuse & neglect. 56. pp.62-79.

Molnár, S. and et.al., 2015. Forecasting share price movements using news sentiment analysis in a

multinational environment.HUNGARIAN AGRICULTURAL ENGINEERIN. (28). pp.53-55.

REHMAN, A. U., Ahmed 2013. Analyzing the Accounting Ratios of Islamic and Conventional

Banks through Linear and Non-linear Classification Techniques: The Case of

Pakistan.European Academic Research.1(8). pp.2232-2254.

Weil, R. L., Schipper 2013.Financial accounting: an introduction to concepts, methods and uses.

Cengage Learning.

Wessels, K. J. 2012. Limits to detectability of land degradation by trend analysis of vegetation index

data.Remote sensing of Environment. 125. pp.10-22.

Zaman, S., 2015, May. Can accounting ratios differentiate between Islamic banks and conventional

banks? A Study on the Dhaka Stock Exchange Listed Private Commercial Banks of

Bangladesh. In INTERNATIONAL INTERDISCIPLINARY BUSINESS-ECONOMICS

ADVANCEMENT CONFERENCE(p. 143).

Online

Financial accounting tools, 2016 Available

through:<http://www.accountingtools.com/financial-accounting-

basics>[Accessed on 11th August 2016].

12

Books and Journals

Choi, Y. J. and et.al., 2015. Trend Analysis of 1-Day Probable Maximum Precipitation.Journal of

Korean Society of Hazard Mitigation.15(1). pp.369-375.

Cordis, A. S., 2014. Accounting Ratios and the Cross‐section of Expected Stock Returns.Journal of

Business Finance & Accounting.41(9-10). pp.1157-1192.

Dickinson, V. and Sommers, G. A., 2012. Which competitive efforts lead to future abnormal

economic rents? Using accounting ratios to assess competitive advantage.Journal of Business

Finance & Accounting. 39(3‐4). pp.360-398.

Edwards, J. R., 2013.A History of Financial Accounting (RLE Accounting)(Vol. 29). Routledge.

Gatua, F. K., 2013.Analysis of share price determinants at Nairobi Securities Exchange(Doctoral

dissertation, School of Business, University of Nairobi).

Mao, A. and Iravani, M. R., 2014. A trend-oriented power system security analysis method based on

load profile.IEEE Transactions on Power Systems. 29(3). pp.1279-1286.

Mathews, B., Lee 2016. Impact of a new mandatory reporting law on reporting and identification of

child sexual abuse: a seven year time trend analysis.Child abuse & neglect. 56. pp.62-79.

Molnár, S. and et.al., 2015. Forecasting share price movements using news sentiment analysis in a

multinational environment.HUNGARIAN AGRICULTURAL ENGINEERIN. (28). pp.53-55.

REHMAN, A. U., Ahmed 2013. Analyzing the Accounting Ratios of Islamic and Conventional

Banks through Linear and Non-linear Classification Techniques: The Case of

Pakistan.European Academic Research.1(8). pp.2232-2254.

Weil, R. L., Schipper 2013.Financial accounting: an introduction to concepts, methods and uses.

Cengage Learning.

Wessels, K. J. 2012. Limits to detectability of land degradation by trend analysis of vegetation index

data.Remote sensing of Environment. 125. pp.10-22.

Zaman, S., 2015, May. Can accounting ratios differentiate between Islamic banks and conventional

banks? A Study on the Dhaka Stock Exchange Listed Private Commercial Banks of

Bangladesh. In INTERNATIONAL INTERDISCIPLINARY BUSINESS-ECONOMICS

ADVANCEMENT CONFERENCE(p. 143).

Online

Financial accounting tools, 2016 Available

through:<http://www.accountingtools.com/financial-accounting-

basics>[Accessed on 11th August 2016].

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.