Financial Decision Making Report: Analysis of Roast Ltd's Performance

VerifiedAdded on 2023/01/18

|17

|4314

|36

Report

AI Summary

This report offers a comprehensive analysis of financial decision-making at Roast Ltd, a UK coffee house chain. It begins with an industry review, examining key players and challenges within the coffee shop sector, including market trends and growth. The core of the report focuses on Roast Ltd's financial performance, utilizing ratio analysis to evaluate profitability, liquidity, and solvency based on financial statements from 2017 and 2018. It assesses the company's gross profit, net profit, current ratio, quick ratio, and debt-equity ratio, among others, providing interpretations of the trends. Furthermore, the report delves into the statement of cash flows, commenting on Roast Ltd's cash position and calculating its operating cash cycle. It also touches upon the company's dividend policy. The report also explores management forecasts and investment appraisal techniques that Roast Ltd could utilize. Finally, it examines potential sources of finance for the company, offering a holistic view of its financial strategies and challenges.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

Industry review...........................................................................................................................1

PART 2............................................................................................................................................3

2.1 Statement of profit & loss evaluation...................................................................................3

2.2 Analysing statement of financial position.............................................................................4

2.3 Statement of cash flows........................................................................................................8

Commenting on the cash position of Roast ltd...........................................................................8

Calculating operating cash cycle for Roast Ltd..........................................................................8

Critically evaluating company’s dividend policy.......................................................................9

PART 3..........................................................................................................................................10

3.1.a Management Forecast.......................................................................................................10

3.1.b Investment Appraisal techniques.....................................................................................10

3.2 Sources of Finance..............................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

Industry review...........................................................................................................................1

PART 2............................................................................................................................................3

2.1 Statement of profit & loss evaluation...................................................................................3

2.2 Analysing statement of financial position.............................................................................4

2.3 Statement of cash flows........................................................................................................8

Commenting on the cash position of Roast ltd...........................................................................8

Calculating operating cash cycle for Roast Ltd..........................................................................8

Critically evaluating company’s dividend policy.......................................................................9

PART 3..........................................................................................................................................10

3.1.a Management Forecast.......................................................................................................10

3.1.b Investment Appraisal techniques.....................................................................................10

3.2 Sources of Finance..............................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial decision making implies for the process that used for an effective decision

making with respect to the business cash management, liabilities and equities. In the context of

business organization, effectual financial decision making is significant which in turn facilitates

optimum utilization of financial resources (Chambers, Echenique and Saito, 2016). Hence, it is

the accountability of manager to take appropriate financial decisions by doing evaluation of

internal and external environmental aspects. The present study is based on different case

scenarios which will provide deeper insight about industry review and different key players that

operating in hospitality sector. Along with this, report will shed light on the financial

performance and position of Roast Ltd through the means of ratio analysis tool. It also presents

how investment appraisal tools can be used by the firm for assessing the viability of alternatives

available. Further, report also entails funding sources that can be undertaken by Roast ltd for

meeting monetary needs or requirements.

PART 1

Industry review

Roast Ltd., a UK coffee house chain, was established in the year 2008. Paola King is the

chairman of the company and considered to be a key player in taking various financial decision

associated with the company.

The UK coffee shop industry is growing at a higher pace where large number of coffee

companies are carrying out its operation in a systematic and efficient manner. By doing

assessment, it has identified that in UK total growth of UK branded coffee shop was 5.8%

significantly (Trends of the UK Coffee Shop Industry, 2019). Coffee is considered to be a global

commodity which in turn traded all across the world.

The retail sales of the coffee has increased to reach 69 million kg in the year 2019.

The total revenue generated by the coffee industry is £6 billion.

The estimated turnover which has been generated from the wholesale of the coffee is

£1499 million in the year 2017.

The estimated GVA contribution to UK GDP is approximately £3.7 billion in the year

2017.

1

Financial decision making implies for the process that used for an effective decision

making with respect to the business cash management, liabilities and equities. In the context of

business organization, effectual financial decision making is significant which in turn facilitates

optimum utilization of financial resources (Chambers, Echenique and Saito, 2016). Hence, it is

the accountability of manager to take appropriate financial decisions by doing evaluation of

internal and external environmental aspects. The present study is based on different case

scenarios which will provide deeper insight about industry review and different key players that

operating in hospitality sector. Along with this, report will shed light on the financial

performance and position of Roast Ltd through the means of ratio analysis tool. It also presents

how investment appraisal tools can be used by the firm for assessing the viability of alternatives

available. Further, report also entails funding sources that can be undertaken by Roast ltd for

meeting monetary needs or requirements.

PART 1

Industry review

Roast Ltd., a UK coffee house chain, was established in the year 2008. Paola King is the

chairman of the company and considered to be a key player in taking various financial decision

associated with the company.

The UK coffee shop industry is growing at a higher pace where large number of coffee

companies are carrying out its operation in a systematic and efficient manner. By doing

assessment, it has identified that in UK total growth of UK branded coffee shop was 5.8%

significantly (Trends of the UK Coffee Shop Industry, 2019). Coffee is considered to be a global

commodity which in turn traded all across the world.

The retail sales of the coffee has increased to reach 69 million kg in the year 2019.

The total revenue generated by the coffee industry is £6 billion.

The estimated turnover which has been generated from the wholesale of the coffee is

£1499 million in the year 2017.

The estimated GVA contribution to UK GDP is approximately £3.7 billion in the year

2017.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The annual growth of the Costa coffee from the year 2014 to 2019 is estimated to be

6.1%.

Key players in coffee industry

Costa Ltd: It is one of the well known coffee shop which was established in the year

1971 by Bruno Costa and Sergio Costa. Costa coffee is considered to be one of the leading

coffee chain in UK. Costa coffee has approximately 3882 stores in around 32 countries.

Starbucks: This is a coffee house chain which was founded in 1971 by Jerry Baldwin,

Zev Siegl and Gordon Bowker. This company operates its business in over 30000 locations

across the globe.

Pret a Manger: It is an international fast casual restaurant established in the year 1983

which was founded by Jeffery Hyman.

Cafe Nero group: This is a European coffee house which w as established in the year

1987 by Gerry Ford. This coffee house mainly deals in Espresso, Latte, Frappe, Tea and savoury

goods.

Key challenges faced

Maintaining the footfall of the customers is considered to be the major challenge because

of increase in competitors.

Rising property cost and rates and considered to be of the major challenge for the

business.

It is very difficult for any new company to establish business in a competitive market.

Change in the National minimum wage tends to largely influence the profit margins of

coffee industry.

With regard to UK coffee chain, Brexit will impose high risk in front of them. Moreover,

after brexit trade and consumer behaviour will be influenced adversely (UK coffee shop

sector achieves 20 years of sustained growth, 2019).

Key opportunities

2

6.1%.

Key players in coffee industry

Costa Ltd: It is one of the well known coffee shop which was established in the year

1971 by Bruno Costa and Sergio Costa. Costa coffee is considered to be one of the leading

coffee chain in UK. Costa coffee has approximately 3882 stores in around 32 countries.

Starbucks: This is a coffee house chain which was founded in 1971 by Jerry Baldwin,

Zev Siegl and Gordon Bowker. This company operates its business in over 30000 locations

across the globe.

Pret a Manger: It is an international fast casual restaurant established in the year 1983

which was founded by Jeffery Hyman.

Cafe Nero group: This is a European coffee house which w as established in the year

1987 by Gerry Ford. This coffee house mainly deals in Espresso, Latte, Frappe, Tea and savoury

goods.

Key challenges faced

Maintaining the footfall of the customers is considered to be the major challenge because

of increase in competitors.

Rising property cost and rates and considered to be of the major challenge for the

business.

It is very difficult for any new company to establish business in a competitive market.

Change in the National minimum wage tends to largely influence the profit margins of

coffee industry.

With regard to UK coffee chain, Brexit will impose high risk in front of them. Moreover,

after brexit trade and consumer behaviour will be influenced adversely (UK coffee shop

sector achieves 20 years of sustained growth, 2019).

Key opportunities

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The key opportunity to the business is that coffee industry helps in strengthening the

economies of various coffee producing countries in Latin America and Africa.

The key opportunity to the business is that coffee industry leads to higher employment

level within the economy which leads to higher economic growth.

This is one of the most growing sector which aids to higher opportunity for the business

to carry out particular business operations.

The household spending on food and beverages is expected to rise in the year 2019-2020

which is considered to be one of the great opportunity to coffee industry.

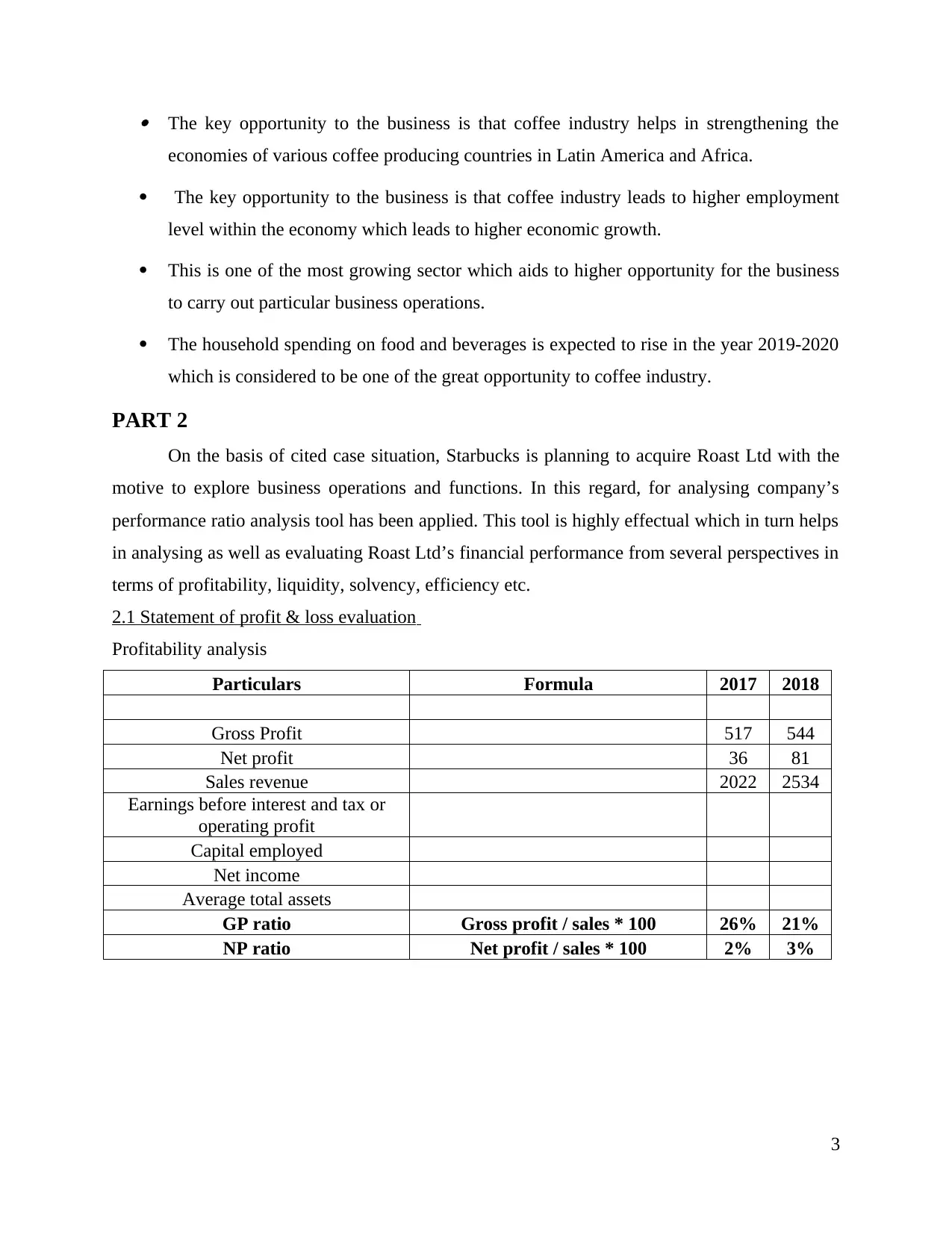

PART 2

On the basis of cited case situation, Starbucks is planning to acquire Roast Ltd with the

motive to explore business operations and functions. In this regard, for analysing company’s

performance ratio analysis tool has been applied. This tool is highly effectual which in turn helps

in analysing as well as evaluating Roast Ltd’s financial performance from several perspectives in

terms of profitability, liquidity, solvency, efficiency etc.

2.1 Statement of profit & loss evaluation

Profitability analysis

Particulars Formula 2017 2018

Gross Profit 517 544

Net profit 36 81

Sales revenue 2022 2534

Earnings before interest and tax or

operating profit

Capital employed

Net income

Average total assets

GP ratio Gross profit / sales * 100 26% 21%

NP ratio Net profit / sales * 100 2% 3%

3

economies of various coffee producing countries in Latin America and Africa.

The key opportunity to the business is that coffee industry leads to higher employment

level within the economy which leads to higher economic growth.

This is one of the most growing sector which aids to higher opportunity for the business

to carry out particular business operations.

The household spending on food and beverages is expected to rise in the year 2019-2020

which is considered to be one of the great opportunity to coffee industry.

PART 2

On the basis of cited case situation, Starbucks is planning to acquire Roast Ltd with the

motive to explore business operations and functions. In this regard, for analysing company’s

performance ratio analysis tool has been applied. This tool is highly effectual which in turn helps

in analysing as well as evaluating Roast Ltd’s financial performance from several perspectives in

terms of profitability, liquidity, solvency, efficiency etc.

2.1 Statement of profit & loss evaluation

Profitability analysis

Particulars Formula 2017 2018

Gross Profit 517 544

Net profit 36 81

Sales revenue 2022 2534

Earnings before interest and tax or

operating profit

Capital employed

Net income

Average total assets

GP ratio Gross profit / sales * 100 26% 21%

NP ratio Net profit / sales * 100 2% 3%

3

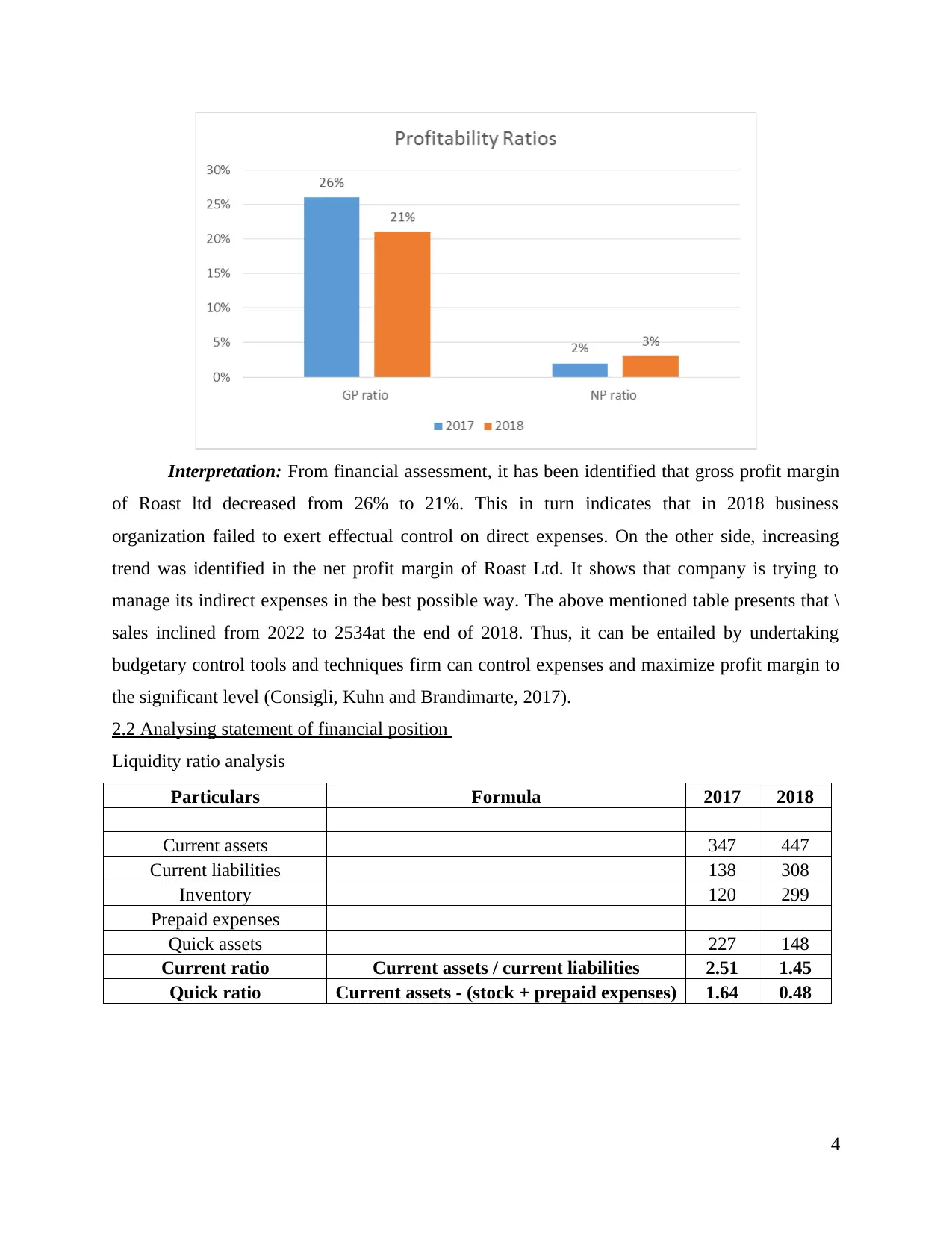

Interpretation: From financial assessment, it has been identified that gross profit margin

of Roast ltd decreased from 26% to 21%. This in turn indicates that in 2018 business

organization failed to exert effectual control on direct expenses. On the other side, increasing

trend was identified in the net profit margin of Roast Ltd. It shows that company is trying to

manage its indirect expenses in the best possible way. The above mentioned table presents that \

sales inclined from 2022 to 2534at the end of 2018. Thus, it can be entailed by undertaking

budgetary control tools and techniques firm can control expenses and maximize profit margin to

the significant level (Consigli, Kuhn and Brandimarte, 2017).

2.2 Analysing statement of financial position

Liquidity ratio analysis

Particulars Formula 2017 2018

Current assets 347 447

Current liabilities 138 308

Inventory 120 299

Prepaid expenses

Quick assets 227 148

Current ratio Current assets / current liabilities 2.51 1.45

Quick ratio Current assets - (stock + prepaid expenses) 1.64 0.48

4

of Roast ltd decreased from 26% to 21%. This in turn indicates that in 2018 business

organization failed to exert effectual control on direct expenses. On the other side, increasing

trend was identified in the net profit margin of Roast Ltd. It shows that company is trying to

manage its indirect expenses in the best possible way. The above mentioned table presents that \

sales inclined from 2022 to 2534at the end of 2018. Thus, it can be entailed by undertaking

budgetary control tools and techniques firm can control expenses and maximize profit margin to

the significant level (Consigli, Kuhn and Brandimarte, 2017).

2.2 Analysing statement of financial position

Liquidity ratio analysis

Particulars Formula 2017 2018

Current assets 347 447

Current liabilities 138 308

Inventory 120 299

Prepaid expenses

Quick assets 227 148

Current ratio Current assets / current liabilities 2.51 1.45

Quick ratio Current assets - (stock + prepaid expenses) 1.64 0.48

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

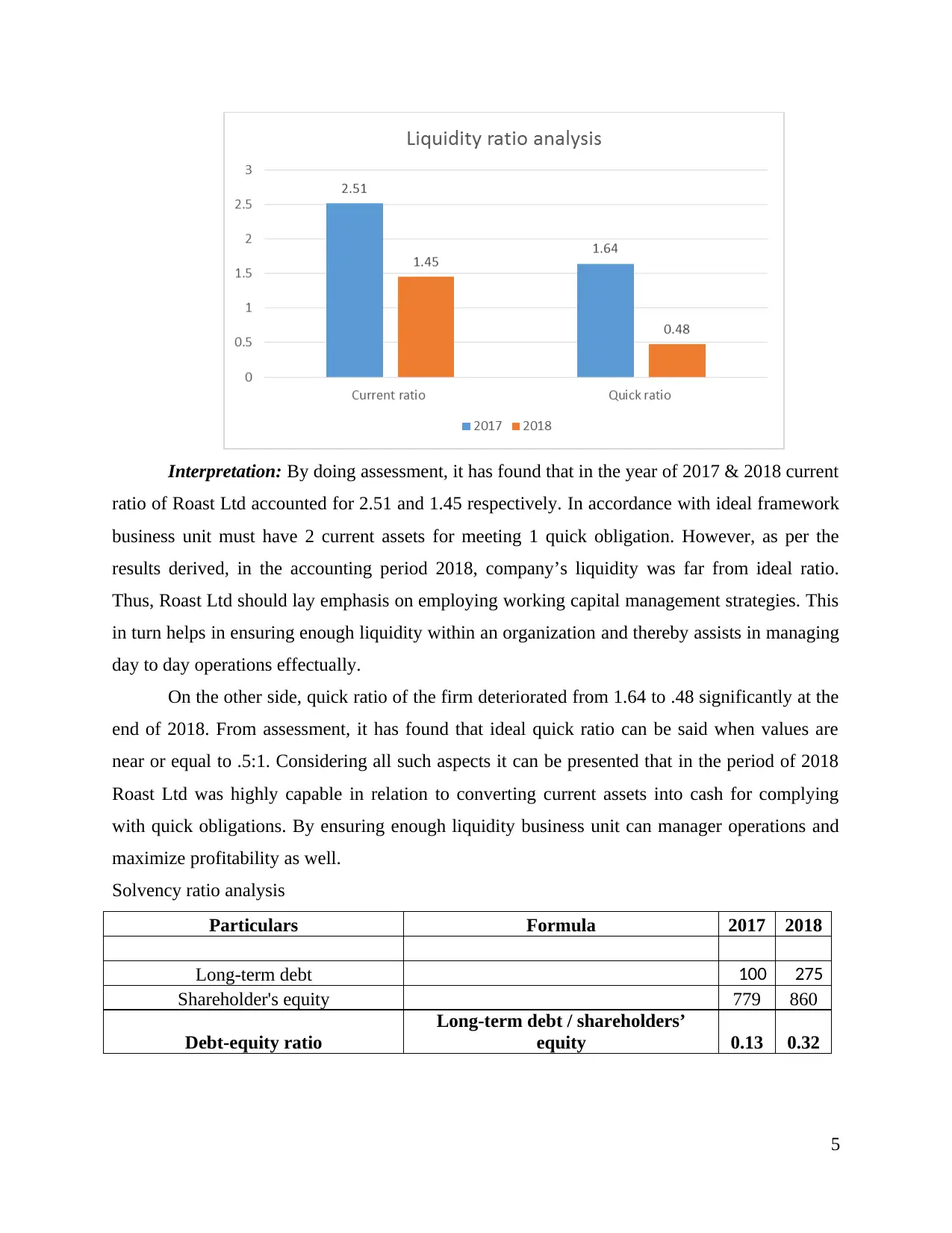

Interpretation: By doing assessment, it has found that in the year of 2017 & 2018 current

ratio of Roast Ltd accounted for 2.51 and 1.45 respectively. In accordance with ideal framework

business unit must have 2 current assets for meeting 1 quick obligation. However, as per the

results derived, in the accounting period 2018, company’s liquidity was far from ideal ratio.

Thus, Roast Ltd should lay emphasis on employing working capital management strategies. This

in turn helps in ensuring enough liquidity within an organization and thereby assists in managing

day to day operations effectually.

On the other side, quick ratio of the firm deteriorated from 1.64 to .48 significantly at the

end of 2018. From assessment, it has found that ideal quick ratio can be said when values are

near or equal to .5:1. Considering all such aspects it can be presented that in the period of 2018

Roast Ltd was highly capable in relation to converting current assets into cash for complying

with quick obligations. By ensuring enough liquidity business unit can manager operations and

maximize profitability as well.

Solvency ratio analysis

Particulars Formula 2017 2018

Long-term debt 100 275

Shareholder's equity 779 860

Debt-equity ratio

Long-term debt / shareholders’

equity 0.13 0.32

5

ratio of Roast Ltd accounted for 2.51 and 1.45 respectively. In accordance with ideal framework

business unit must have 2 current assets for meeting 1 quick obligation. However, as per the

results derived, in the accounting period 2018, company’s liquidity was far from ideal ratio.

Thus, Roast Ltd should lay emphasis on employing working capital management strategies. This

in turn helps in ensuring enough liquidity within an organization and thereby assists in managing

day to day operations effectually.

On the other side, quick ratio of the firm deteriorated from 1.64 to .48 significantly at the

end of 2018. From assessment, it has found that ideal quick ratio can be said when values are

near or equal to .5:1. Considering all such aspects it can be presented that in the period of 2018

Roast Ltd was highly capable in relation to converting current assets into cash for complying

with quick obligations. By ensuring enough liquidity business unit can manager operations and

maximize profitability as well.

Solvency ratio analysis

Particulars Formula 2017 2018

Long-term debt 100 275

Shareholder's equity 779 860

Debt-equity ratio

Long-term debt / shareholders’

equity 0.13 0.32

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

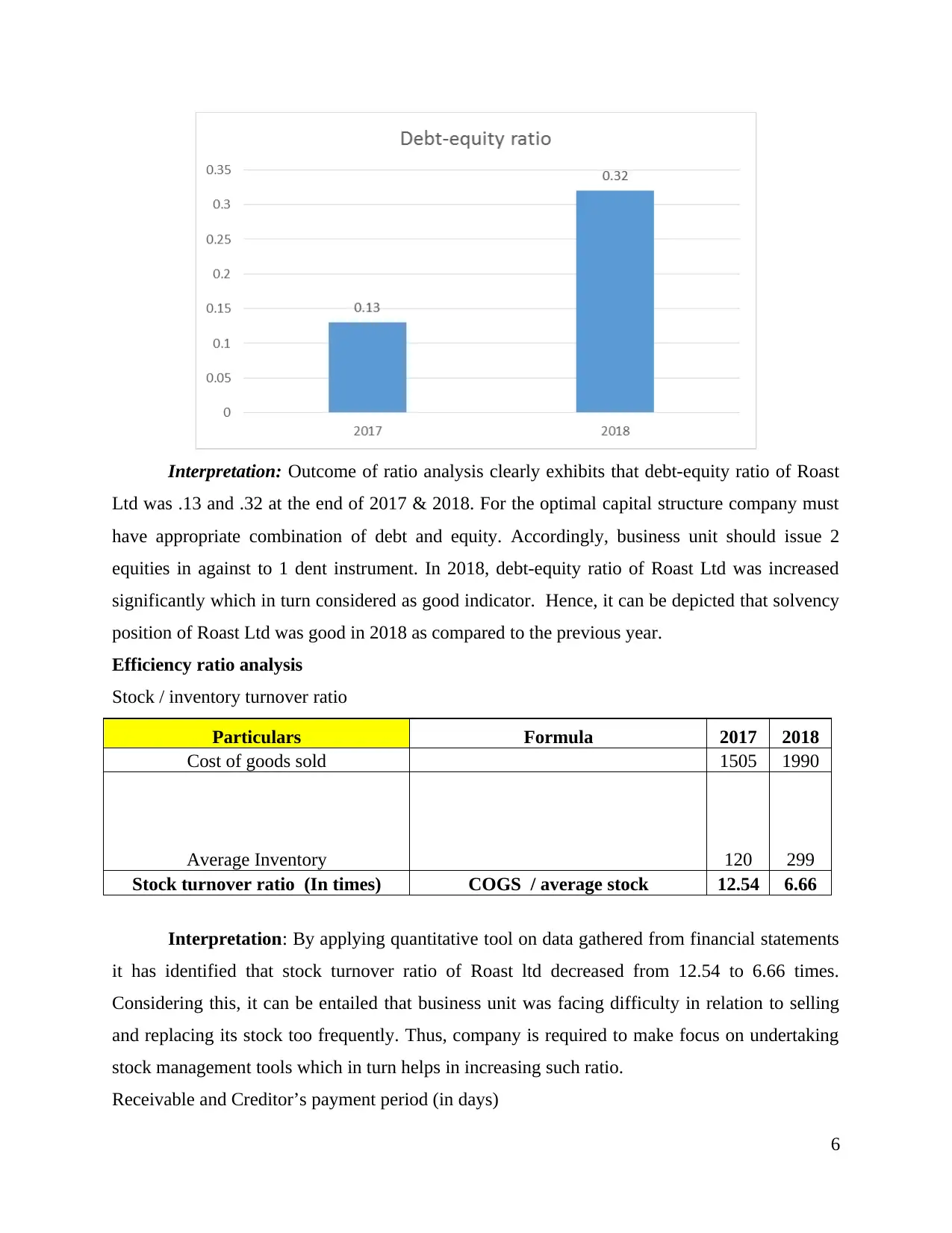

Interpretation: Outcome of ratio analysis clearly exhibits that debt-equity ratio of Roast

Ltd was .13 and .32 at the end of 2017 & 2018. For the optimal capital structure company must

have appropriate combination of debt and equity. Accordingly, business unit should issue 2

equities in against to 1 dent instrument. In 2018, debt-equity ratio of Roast Ltd was increased

significantly which in turn considered as good indicator. Hence, it can be depicted that solvency

position of Roast Ltd was good in 2018 as compared to the previous year.

Efficiency ratio analysis

Stock / inventory turnover ratio

Particulars Formula 2017 2018

Cost of goods sold 1505 1990

Average Inventory 120 299

Stock turnover ratio (In times) COGS / average stock 12.54 6.66

Interpretation: By applying quantitative tool on data gathered from financial statements

it has identified that stock turnover ratio of Roast ltd decreased from 12.54 to 6.66 times.

Considering this, it can be entailed that business unit was facing difficulty in relation to selling

and replacing its stock too frequently. Thus, company is required to make focus on undertaking

stock management tools which in turn helps in increasing such ratio.

Receivable and Creditor’s payment period (in days)

6

Ltd was .13 and .32 at the end of 2017 & 2018. For the optimal capital structure company must

have appropriate combination of debt and equity. Accordingly, business unit should issue 2

equities in against to 1 dent instrument. In 2018, debt-equity ratio of Roast Ltd was increased

significantly which in turn considered as good indicator. Hence, it can be depicted that solvency

position of Roast Ltd was good in 2018 as compared to the previous year.

Efficiency ratio analysis

Stock / inventory turnover ratio

Particulars Formula 2017 2018

Cost of goods sold 1505 1990

Average Inventory 120 299

Stock turnover ratio (In times) COGS / average stock 12.54 6.66

Interpretation: By applying quantitative tool on data gathered from financial statements

it has identified that stock turnover ratio of Roast ltd decreased from 12.54 to 6.66 times.

Considering this, it can be entailed that business unit was facing difficulty in relation to selling

and replacing its stock too frequently. Thus, company is required to make focus on undertaking

stock management tools which in turn helps in increasing such ratio.

Receivable and Creditor’s payment period (in days)

6

Particulars Formula 2017 2018

Cost of goods sold 1505 1990

Turnover or sales revenue 2022 2534

Receivables or debtors 93 148

Creditors or payables 138 235

Receivables or debtors turnover

ratio (in days) (Debtors * 365) / Credit sales 17 21

Creditors turnover ratio (in days) (Creditors * 365) / COGS 33 43

Interpretation: Results of ratio analysis presents that receivable ratio or period of Roast

ltd increased from 17 to 21 days. Accordingly, credit period given by Roast Ltd to its debtors

increased by 4 days in the financial year 2018 which in turn not goo. Moreover, in the case of

high receivable period, working capital of the firm affected negatively. However, on the other

side, creditor’s period also increased from 33 to 43 days. It is good for firm when suppliers grant

credit for longer duration. Moreover, it offers opportunity to the firm in relation to investing

funds in other operations for improving profitability aspects.

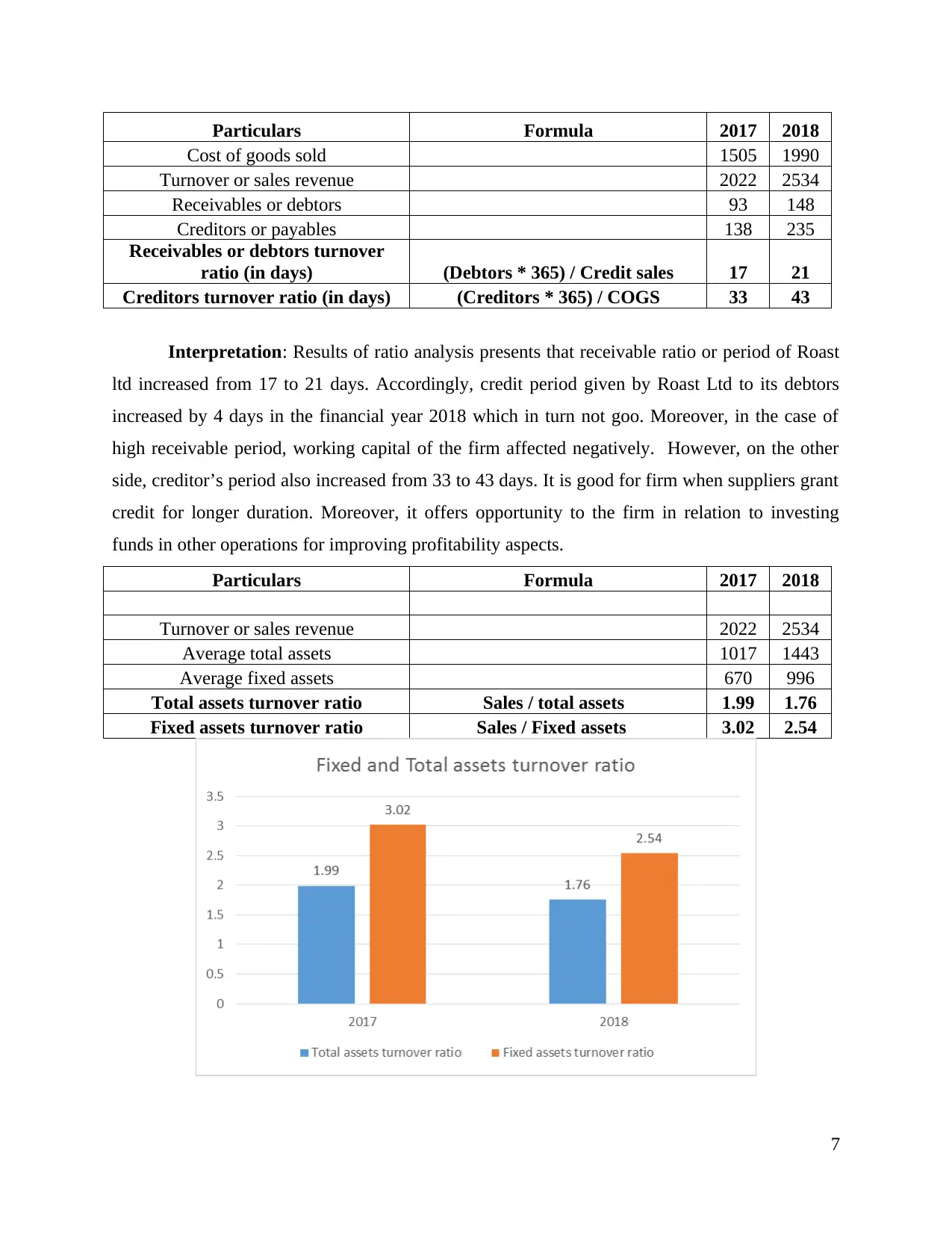

Particulars Formula 2017 2018

Turnover or sales revenue 2022 2534

Average total assets 1017 1443

Average fixed assets 670 996

Total assets turnover ratio Sales / total assets 1.99 1.76

Fixed assets turnover ratio Sales / Fixed assets 3.02 2.54

7

Cost of goods sold 1505 1990

Turnover or sales revenue 2022 2534

Receivables or debtors 93 148

Creditors or payables 138 235

Receivables or debtors turnover

ratio (in days) (Debtors * 365) / Credit sales 17 21

Creditors turnover ratio (in days) (Creditors * 365) / COGS 33 43

Interpretation: Results of ratio analysis presents that receivable ratio or period of Roast

ltd increased from 17 to 21 days. Accordingly, credit period given by Roast Ltd to its debtors

increased by 4 days in the financial year 2018 which in turn not goo. Moreover, in the case of

high receivable period, working capital of the firm affected negatively. However, on the other

side, creditor’s period also increased from 33 to 43 days. It is good for firm when suppliers grant

credit for longer duration. Moreover, it offers opportunity to the firm in relation to investing

funds in other operations for improving profitability aspects.

Particulars Formula 2017 2018

Turnover or sales revenue 2022 2534

Average total assets 1017 1443

Average fixed assets 670 996

Total assets turnover ratio Sales / total assets 1.99 1.76

Fixed assets turnover ratio Sales / Fixed assets 3.02 2.54

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

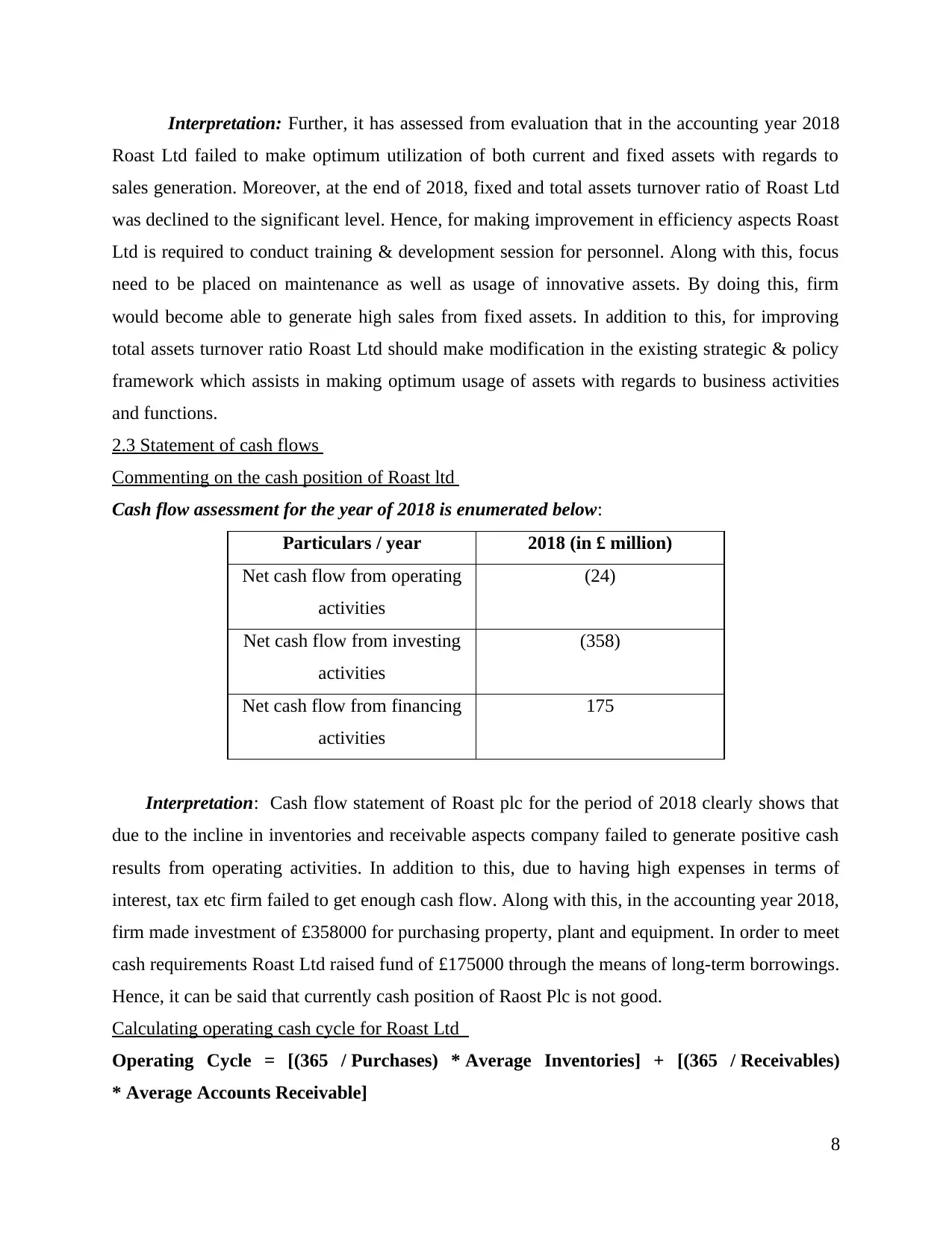

Interpretation: Further, it has assessed from evaluation that in the accounting year 2018

Roast Ltd failed to make optimum utilization of both current and fixed assets with regards to

sales generation. Moreover, at the end of 2018, fixed and total assets turnover ratio of Roast Ltd

was declined to the significant level. Hence, for making improvement in efficiency aspects Roast

Ltd is required to conduct training & development session for personnel. Along with this, focus

need to be placed on maintenance as well as usage of innovative assets. By doing this, firm

would become able to generate high sales from fixed assets. In addition to this, for improving

total assets turnover ratio Roast Ltd should make modification in the existing strategic & policy

framework which assists in making optimum usage of assets with regards to business activities

and functions.

2.3 Statement of cash flows

Commenting on the cash position of Roast ltd

Cash flow assessment for the year of 2018 is enumerated below:

Particulars / year 2018 (in £ million)

Net cash flow from operating

activities

(24)

Net cash flow from investing

activities

(358)

Net cash flow from financing

activities

175

Interpretation: Cash flow statement of Roast plc for the period of 2018 clearly shows that

due to the incline in inventories and receivable aspects company failed to generate positive cash

results from operating activities. In addition to this, due to having high expenses in terms of

interest, tax etc firm failed to get enough cash flow. Along with this, in the accounting year 2018,

firm made investment of £358000 for purchasing property, plant and equipment. In order to meet

cash requirements Roast Ltd raised fund of £175000 through the means of long-term borrowings.

Hence, it can be said that currently cash position of Raost Plc is not good.

Calculating operating cash cycle for Roast Ltd

Operating Cycle = [(365 / Purchases) * Average Inventories] + [(365 / Receivables)

* Average Accounts Receivable]

8

Roast Ltd failed to make optimum utilization of both current and fixed assets with regards to

sales generation. Moreover, at the end of 2018, fixed and total assets turnover ratio of Roast Ltd

was declined to the significant level. Hence, for making improvement in efficiency aspects Roast

Ltd is required to conduct training & development session for personnel. Along with this, focus

need to be placed on maintenance as well as usage of innovative assets. By doing this, firm

would become able to generate high sales from fixed assets. In addition to this, for improving

total assets turnover ratio Roast Ltd should make modification in the existing strategic & policy

framework which assists in making optimum usage of assets with regards to business activities

and functions.

2.3 Statement of cash flows

Commenting on the cash position of Roast ltd

Cash flow assessment for the year of 2018 is enumerated below:

Particulars / year 2018 (in £ million)

Net cash flow from operating

activities

(24)

Net cash flow from investing

activities

(358)

Net cash flow from financing

activities

175

Interpretation: Cash flow statement of Roast plc for the period of 2018 clearly shows that

due to the incline in inventories and receivable aspects company failed to generate positive cash

results from operating activities. In addition to this, due to having high expenses in terms of

interest, tax etc firm failed to get enough cash flow. Along with this, in the accounting year 2018,

firm made investment of £358000 for purchasing property, plant and equipment. In order to meet

cash requirements Roast Ltd raised fund of £175000 through the means of long-term borrowings.

Hence, it can be said that currently cash position of Raost Plc is not good.

Calculating operating cash cycle for Roast Ltd

Operating Cycle = [(365 / Purchases) * Average Inventories] + [(365 / Receivables)

* Average Accounts Receivable]

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

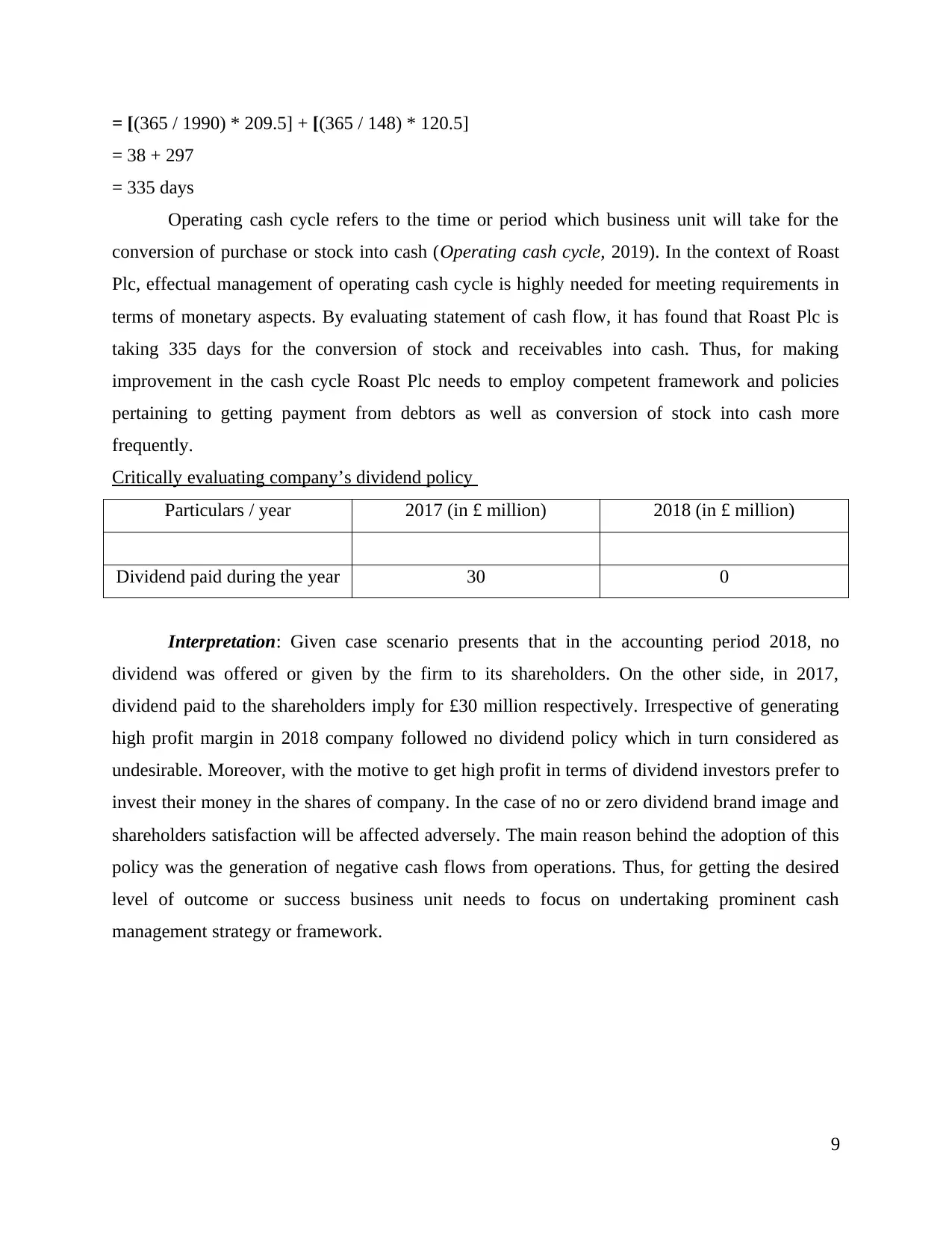

= [(365 / 1990) * 209.5] + [(365 / 148) * 120.5]

= 38 + 297

= 335 days

Operating cash cycle refers to the time or period which business unit will take for the

conversion of purchase or stock into cash (Operating cash cycle, 2019). In the context of Roast

Plc, effectual management of operating cash cycle is highly needed for meeting requirements in

terms of monetary aspects. By evaluating statement of cash flow, it has found that Roast Plc is

taking 335 days for the conversion of stock and receivables into cash. Thus, for making

improvement in the cash cycle Roast Plc needs to employ competent framework and policies

pertaining to getting payment from debtors as well as conversion of stock into cash more

frequently.

Critically evaluating company’s dividend policy

Particulars / year 2017 (in £ million) 2018 (in £ million)

Dividend paid during the year 30 0

Interpretation: Given case scenario presents that in the accounting period 2018, no

dividend was offered or given by the firm to its shareholders. On the other side, in 2017,

dividend paid to the shareholders imply for £30 million respectively. Irrespective of generating

high profit margin in 2018 company followed no dividend policy which in turn considered as

undesirable. Moreover, with the motive to get high profit in terms of dividend investors prefer to

invest their money in the shares of company. In the case of no or zero dividend brand image and

shareholders satisfaction will be affected adversely. The main reason behind the adoption of this

policy was the generation of negative cash flows from operations. Thus, for getting the desired

level of outcome or success business unit needs to focus on undertaking prominent cash

management strategy or framework.

9

= 38 + 297

= 335 days

Operating cash cycle refers to the time or period which business unit will take for the

conversion of purchase or stock into cash (Operating cash cycle, 2019). In the context of Roast

Plc, effectual management of operating cash cycle is highly needed for meeting requirements in

terms of monetary aspects. By evaluating statement of cash flow, it has found that Roast Plc is

taking 335 days for the conversion of stock and receivables into cash. Thus, for making

improvement in the cash cycle Roast Plc needs to employ competent framework and policies

pertaining to getting payment from debtors as well as conversion of stock into cash more

frequently.

Critically evaluating company’s dividend policy

Particulars / year 2017 (in £ million) 2018 (in £ million)

Dividend paid during the year 30 0

Interpretation: Given case scenario presents that in the accounting period 2018, no

dividend was offered or given by the firm to its shareholders. On the other side, in 2017,

dividend paid to the shareholders imply for £30 million respectively. Irrespective of generating

high profit margin in 2018 company followed no dividend policy which in turn considered as

undesirable. Moreover, with the motive to get high profit in terms of dividend investors prefer to

invest their money in the shares of company. In the case of no or zero dividend brand image and

shareholders satisfaction will be affected adversely. The main reason behind the adoption of this

policy was the generation of negative cash flows from operations. Thus, for getting the desired

level of outcome or success business unit needs to focus on undertaking prominent cash

management strategy or framework.

9

PART 3

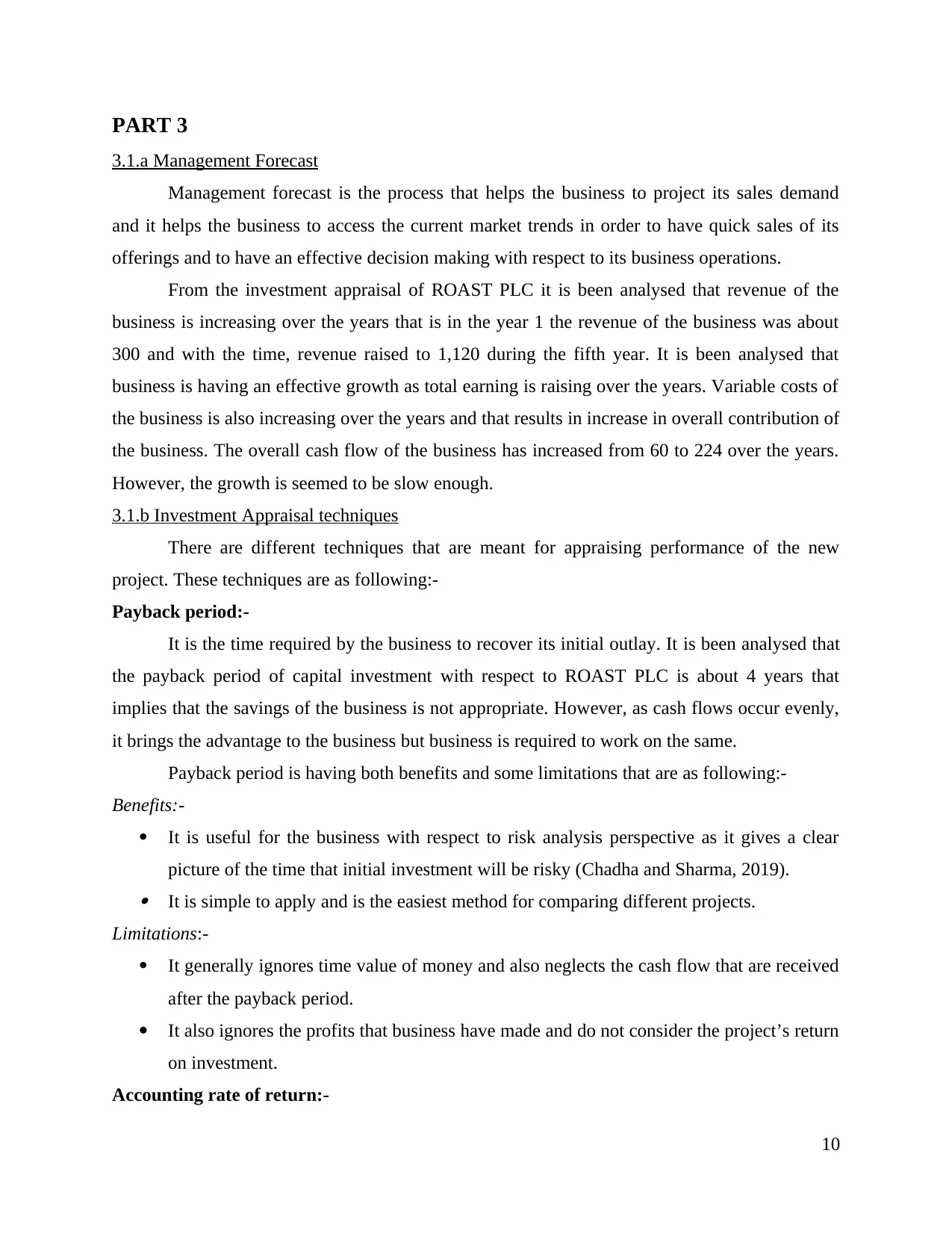

3.1.a Management Forecast

Management forecast is the process that helps the business to project its sales demand

and it helps the business to access the current market trends in order to have quick sales of its

offerings and to have an effective decision making with respect to its business operations.

From the investment appraisal of ROAST PLC it is been analysed that revenue of the

business is increasing over the years that is in the year 1 the revenue of the business was about

300 and with the time, revenue raised to 1,120 during the fifth year. It is been analysed that

business is having an effective growth as total earning is raising over the years. Variable costs of

the business is also increasing over the years and that results in increase in overall contribution of

the business. The overall cash flow of the business has increased from 60 to 224 over the years.

However, the growth is seemed to be slow enough.

3.1.b Investment Appraisal techniques

There are different techniques that are meant for appraising performance of the new

project. These techniques are as following:-

Payback period:-

It is the time required by the business to recover its initial outlay. It is been analysed that

the payback period of capital investment with respect to ROAST PLC is about 4 years that

implies that the savings of the business is not appropriate. However, as cash flows occur evenly,

it brings the advantage to the business but business is required to work on the same.

Payback period is having both benefits and some limitations that are as following:-

Benefits:-

It is useful for the business with respect to risk analysis perspective as it gives a clear

picture of the time that initial investment will be risky (Chadha and Sharma, 2019). It is simple to apply and is the easiest method for comparing different projects.

Limitations:-

It generally ignores time value of money and also neglects the cash flow that are received

after the payback period.

It also ignores the profits that business have made and do not consider the project’s return

on investment.

Accounting rate of return:-

10

3.1.a Management Forecast

Management forecast is the process that helps the business to project its sales demand

and it helps the business to access the current market trends in order to have quick sales of its

offerings and to have an effective decision making with respect to its business operations.

From the investment appraisal of ROAST PLC it is been analysed that revenue of the

business is increasing over the years that is in the year 1 the revenue of the business was about

300 and with the time, revenue raised to 1,120 during the fifth year. It is been analysed that

business is having an effective growth as total earning is raising over the years. Variable costs of

the business is also increasing over the years and that results in increase in overall contribution of

the business. The overall cash flow of the business has increased from 60 to 224 over the years.

However, the growth is seemed to be slow enough.

3.1.b Investment Appraisal techniques

There are different techniques that are meant for appraising performance of the new

project. These techniques are as following:-

Payback period:-

It is the time required by the business to recover its initial outlay. It is been analysed that

the payback period of capital investment with respect to ROAST PLC is about 4 years that

implies that the savings of the business is not appropriate. However, as cash flows occur evenly,

it brings the advantage to the business but business is required to work on the same.

Payback period is having both benefits and some limitations that are as following:-

Benefits:-

It is useful for the business with respect to risk analysis perspective as it gives a clear

picture of the time that initial investment will be risky (Chadha and Sharma, 2019). It is simple to apply and is the easiest method for comparing different projects.

Limitations:-

It generally ignores time value of money and also neglects the cash flow that are received

after the payback period.

It also ignores the profits that business have made and do not consider the project’s return

on investment.

Accounting rate of return:-

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.