Comprehensive Financial Analysis of SkyStudio: A Detailed Report

VerifiedAdded on 2023/04/22

|15

|2621

|312

Report

AI Summary

This report presents a financial analysis of SkyStudio, including ratio analysis, variance analysis, and cost-volume-profit (CVP) analysis. The ratio analysis assesses profitability, financial stability, and asset utilization, revealing areas where SkyStudio outperforms industry averages and areas needing improvement, such as return on equity and liquidity management. The variance analysis identifies significant differences between budgeted and actual figures, particularly in cost of sales and administrative expenses, warranting further investigation. The CVP analysis calculates the breakeven point and profitability at different sales levels. The report concludes with recommendations for enhancing financial performance and strategic decision-making. Desklib provides a platform for students to access similar solved assignments and study resources.

Running Head: FINANCIAL ANALYSIS OF SKYSTUDIO

0

FINANCIAL ANALYSIS OF SKYSTUDIO

0

FINANCIAL ANALYSIS OF SKYSTUDIO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS OF SKYSTUDIO 1

FINANCIAL ANALYSIS OF SKYSTUDIO 2

Table of Contents

Objective....................................................................................................................................3

Financial Analysis Purpose........................................................................................................3

Structure of the report................................................................................................................3

Ratio Analysis............................................................................................................................3

Assessment of the ratios.........................................................................................................3

Profitability.........................................................................................................................3

Financial Stability...............................................................................................................4

Asset utilisation...................................................................................................................5

Conclusion..................................................................................................................................5

Summary.................................................................................................................................5

Limitations of the financial analysis.......................................................................................5

Variance Analysis......................................................................................................................5

Part 1.......................................................................................................................................6

Part 2.......................................................................................................................................6

CVP analysis..............................................................................................................................7

A.............................................................................................................................................7

B.............................................................................................................................................8

C.............................................................................................................................................8

D.............................................................................................................................................9

Table of Contents

Objective....................................................................................................................................3

Financial Analysis Purpose........................................................................................................3

Structure of the report................................................................................................................3

Ratio Analysis............................................................................................................................3

Assessment of the ratios.........................................................................................................3

Profitability.........................................................................................................................3

Financial Stability...............................................................................................................4

Asset utilisation...................................................................................................................5

Conclusion..................................................................................................................................5

Summary.................................................................................................................................5

Limitations of the financial analysis.......................................................................................5

Variance Analysis......................................................................................................................5

Part 1.......................................................................................................................................6

Part 2.......................................................................................................................................6

CVP analysis..............................................................................................................................7

A.............................................................................................................................................7

B.............................................................................................................................................8

C.............................................................................................................................................8

D.............................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS OF SKYSTUDIO 3

Objective

The objective of this report is to determine the entire financial analysis including the

budgeted analysis of the company Sky Studio. The objective of carrying out the financial

analysis is to get a competitive advantage over the competitors and to be stable. With the

assistance of the analysis the company can found out whether the company is worthy for

investment from the point of view of investors. Further the financial analysis will also

determine how the company operates and what variances can be found out and must rectify

the same.

Financial Analysis Purpose

Financial analysis is the method used by the management of the company for the

purpose of evaluation of business and the projects, budgets and the entities which are dealing

in the financial means to determine their performance and long term sustainability. The four

pillars of the organization can be judged by the financial analysis, as to whether the company

is profitable, solvent, liquidity and the efficient or not to make an investment for. The

financial analysis is carried out with the help of the financial statements such as income

statement, balance sheet, and cash flow statement (Robinson Henry,Pirie & Broihahn, 2015).

Structure of the report

The structure of the report is bifurcated in so many parts and it moves basically with

the financial analysis is necessary from the point of view of not only management but also

from the perspective of the shareholders and the investors. They compare the data either with

the industry comparison or with the previous years. Moreover his report also talks about the

details of the purpose of the financial statements followed by the ratio analysis. The budgets

Objective

The objective of this report is to determine the entire financial analysis including the

budgeted analysis of the company Sky Studio. The objective of carrying out the financial

analysis is to get a competitive advantage over the competitors and to be stable. With the

assistance of the analysis the company can found out whether the company is worthy for

investment from the point of view of investors. Further the financial analysis will also

determine how the company operates and what variances can be found out and must rectify

the same.

Financial Analysis Purpose

Financial analysis is the method used by the management of the company for the

purpose of evaluation of business and the projects, budgets and the entities which are dealing

in the financial means to determine their performance and long term sustainability. The four

pillars of the organization can be judged by the financial analysis, as to whether the company

is profitable, solvent, liquidity and the efficient or not to make an investment for. The

financial analysis is carried out with the help of the financial statements such as income

statement, balance sheet, and cash flow statement (Robinson Henry,Pirie & Broihahn, 2015).

Structure of the report

The structure of the report is bifurcated in so many parts and it moves basically with

the financial analysis is necessary from the point of view of not only management but also

from the perspective of the shareholders and the investors. They compare the data either with

the industry comparison or with the previous years. Moreover his report also talks about the

details of the purpose of the financial statements followed by the ratio analysis. The budgets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS OF SKYSTUDIO 4

are prepared according to the assumptions and the requirements and the final CVP analysis is

also undertaken to get to know the movement of the costs.

Ratio Analysis

Ratio analysis is the technique which is used to determine the ability of the company

on several categories. A sound company is a combination of the efficiency, profitability,

solvency and the relevant market position and liquidity. The company is required to excel

these categories in order to satisfy the customers and the investors (Uechi Akutsu, Stanley,

Marcus & Kenett, 2015).

Assessment of the ratios

Profitability

The profitability ratios of the company are calculates to measure the financial

performance of the company in terms of the profitability over the period of years or in

comparison to the industry averages. Profit is the king of the organisation which keeps the

organisation stable and on-going and therefore the investors are also interested in calculating

the profitability ratio of the company (Williams & Dobelman, 2017).

The gross profit ratio determines the gross costs and the net profit ratio considers the

amount after the entire costs are being reduced from the earnings. The profitability ratio of

the Sky studio can be observed from the table. The gross profit being 98% and the net profit

being 63% showcases that the company is performing better than the industry averages.

However in terms of the return on equity the company is a bit behind. This may be due to the

management does not involve much in data driven decisions and this lacks the motive of the

shareholders to invest. This needs to be improved on emergency basis (Al-Jafari & Al

Samman, 2015).

Compan Industr

are prepared according to the assumptions and the requirements and the final CVP analysis is

also undertaken to get to know the movement of the costs.

Ratio Analysis

Ratio analysis is the technique which is used to determine the ability of the company

on several categories. A sound company is a combination of the efficiency, profitability,

solvency and the relevant market position and liquidity. The company is required to excel

these categories in order to satisfy the customers and the investors (Uechi Akutsu, Stanley,

Marcus & Kenett, 2015).

Assessment of the ratios

Profitability

The profitability ratios of the company are calculates to measure the financial

performance of the company in terms of the profitability over the period of years or in

comparison to the industry averages. Profit is the king of the organisation which keeps the

organisation stable and on-going and therefore the investors are also interested in calculating

the profitability ratio of the company (Williams & Dobelman, 2017).

The gross profit ratio determines the gross costs and the net profit ratio considers the

amount after the entire costs are being reduced from the earnings. The profitability ratio of

the Sky studio can be observed from the table. The gross profit being 98% and the net profit

being 63% showcases that the company is performing better than the industry averages.

However in terms of the return on equity the company is a bit behind. This may be due to the

management does not involve much in data driven decisions and this lacks the motive of the

shareholders to invest. This needs to be improved on emergency basis (Al-Jafari & Al

Samman, 2015).

Compan Industr

FINANCIAL ANALYSIS OF SKYSTUDIO 5

y y

Averag

e

Gross profit Ratio 2019

Gross profit 98% 64%

Net Sales

Net Profit ratio

Net Profit Ratio 63% 21.68%

Sales

Return on Equity ratio

Net income 22% 39.98%

Average Equity

Financial Stability

For any organization the financial stability is equally important and this can be judged

on the basis of the liquidity position of the company. Further the liquidity position of the

company is being determined by the current ratio and the quick ratio of the organization. The

current ratio of the Sky Studio is presented below in the table (Fuhrer, Müller & Steiner,

2017).

Current Ratio Compan

y

Industr

y

Averag

e

Current Assets 6.47 1.90:1

Current liabilities

Quick Ratio

Quick assets 6.29 1.15:1

Current Liabilities

The current ratio of the Sky Studio ids higher than the ideal ratio, yet on the other

hand the liabilities are quite increasing in nature, thus this suggests that though the company

is able to pay back the liabilities and have enough cash in hand yet it is a risky position. Too

much cash would reflect the negative aspect. To improve the company can expand its

y y

Averag

e

Gross profit Ratio 2019

Gross profit 98% 64%

Net Sales

Net Profit ratio

Net Profit Ratio 63% 21.68%

Sales

Return on Equity ratio

Net income 22% 39.98%

Average Equity

Financial Stability

For any organization the financial stability is equally important and this can be judged

on the basis of the liquidity position of the company. Further the liquidity position of the

company is being determined by the current ratio and the quick ratio of the organization. The

current ratio of the Sky Studio is presented below in the table (Fuhrer, Müller & Steiner,

2017).

Current Ratio Compan

y

Industr

y

Averag

e

Current Assets 6.47 1.90:1

Current liabilities

Quick Ratio

Quick assets 6.29 1.15:1

Current Liabilities

The current ratio of the Sky Studio ids higher than the ideal ratio, yet on the other

hand the liabilities are quite increasing in nature, thus this suggests that though the company

is able to pay back the liabilities and have enough cash in hand yet it is a risky position. Too

much cash would reflect the negative aspect. To improve the company can expand its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS OF SKYSTUDIO 6

business with the help of long term liabilities so that the sufficient cash will also stay with the

company. Similar is the case with the quick ratio as well (Saif-Alyousfi, Saha & Md-Rus,

2017).

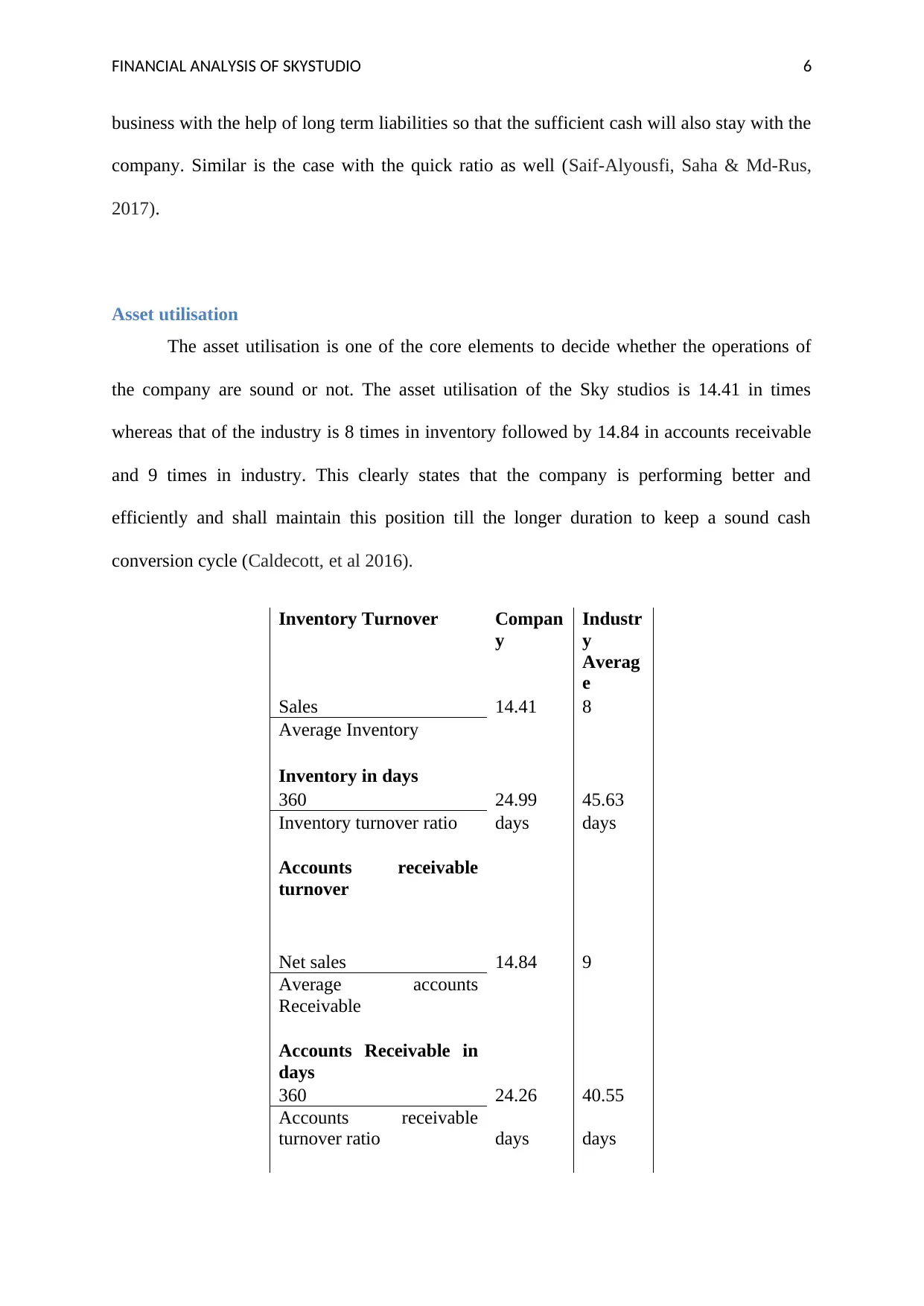

Asset utilisation

The asset utilisation is one of the core elements to decide whether the operations of

the company are sound or not. The asset utilisation of the Sky studios is 14.41 in times

whereas that of the industry is 8 times in inventory followed by 14.84 in accounts receivable

and 9 times in industry. This clearly states that the company is performing better and

efficiently and shall maintain this position till the longer duration to keep a sound cash

conversion cycle (Caldecott, et al 2016).

Inventory Turnover Compan

y

Industr

y

Averag

e

Sales 14.41 8

Average Inventory

Inventory in days

360 24.99 45.63

Inventory turnover ratio days days

Accounts receivable

turnover

Net sales 14.84 9

Average accounts

Receivable

Accounts Receivable in

days

360 24.26 40.55

Accounts receivable

turnover ratio days days

business with the help of long term liabilities so that the sufficient cash will also stay with the

company. Similar is the case with the quick ratio as well (Saif-Alyousfi, Saha & Md-Rus,

2017).

Asset utilisation

The asset utilisation is one of the core elements to decide whether the operations of

the company are sound or not. The asset utilisation of the Sky studios is 14.41 in times

whereas that of the industry is 8 times in inventory followed by 14.84 in accounts receivable

and 9 times in industry. This clearly states that the company is performing better and

efficiently and shall maintain this position till the longer duration to keep a sound cash

conversion cycle (Caldecott, et al 2016).

Inventory Turnover Compan

y

Industr

y

Averag

e

Sales 14.41 8

Average Inventory

Inventory in days

360 24.99 45.63

Inventory turnover ratio days days

Accounts receivable

turnover

Net sales 14.84 9

Average accounts

Receivable

Accounts Receivable in

days

360 24.26 40.55

Accounts receivable

turnover ratio days days

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS OF SKYSTUDIO 7

Conclusion

From the above analysis it can be concluded that the Sky Studio is performing better

than the industry averages and the few areas where the company lacks shall be rectified

immediately. This will not only help the company in growing with the greater market share

but the company will also be able to provide the futuristic returns to its shareholders as well

as then investors.

Summary

The summary suggests that the Sky Studio clearly needs to improve the return on

equity and the liquidity positions (Easton & Sommers, 2018).

Limitations of the financial analysis

Though the financial statement analysis is healthy yet it is prone to have certain

limitations which start with that there is no sound judgement that can be made just on the

basis of the financial statements. The data is also prepared on the basis of the past and at

times there is a problem in comparability when two different organisations are using different

mechanisms to value inventory and such as FIFO or LIFO. Hence at times the data is not

reliable (Mei, Fei, Zhilong & Jinghua, 2018).

Variance Analysis

The variance analysis is the key concept in the process of the budgeting. The

budgeting ensures the gap between the actual and the budgeted figures. The key functions of

the managers of the company are to perform the budgeted analysis to find out any variances if

possible and rectifying those variances by taking the possible measures (Chiu, et al 2018).

Part 1

Particulars Actual Budgete

d

Variance variance

%

$ $

Sales (all on credit) 2,53,27 3,29,2 -75,981 -23%

Conclusion

From the above analysis it can be concluded that the Sky Studio is performing better

than the industry averages and the few areas where the company lacks shall be rectified

immediately. This will not only help the company in growing with the greater market share

but the company will also be able to provide the futuristic returns to its shareholders as well

as then investors.

Summary

The summary suggests that the Sky Studio clearly needs to improve the return on

equity and the liquidity positions (Easton & Sommers, 2018).

Limitations of the financial analysis

Though the financial statement analysis is healthy yet it is prone to have certain

limitations which start with that there is no sound judgement that can be made just on the

basis of the financial statements. The data is also prepared on the basis of the past and at

times there is a problem in comparability when two different organisations are using different

mechanisms to value inventory and such as FIFO or LIFO. Hence at times the data is not

reliable (Mei, Fei, Zhilong & Jinghua, 2018).

Variance Analysis

The variance analysis is the key concept in the process of the budgeting. The

budgeting ensures the gap between the actual and the budgeted figures. The key functions of

the managers of the company are to perform the budgeted analysis to find out any variances if

possible and rectifying those variances by taking the possible measures (Chiu, et al 2018).

Part 1

Particulars Actual Budgete

d

Variance variance

%

$ $

Sales (all on credit) 2,53,27 3,29,2 -75,981 -23%

FINANCIAL ANALYSIS OF SKYSTUDIO 8

0 51

Cost of Sales 5,360

6,9

68 -1,608 -23%

Gross Profit

2,47,91

0 3,22,283 -74,373 -23%

Selling Expenses

Selling Expenses 5,000

5,0

00 0 -38%

Depreciation 2,342

2,3

89 -47 -2%

Admin and General

Expenses 14180

16,7

32 -2,552 -15%

Total expenses 21,522 24,121 -2,599 -11%

EBIT

2,26,38

8 2,98,162 -71,774 -24%

Interest 5,512 5,512 0 0%

EBT

2,20,87

6 2,92,650 -71,774 -25%

Tax 61845 81942 -20,097 -25%

Other income 275 300

profit after tax

1,59,03

1 2,10,708 -51,677 -25%

The following is the budget report which determines the assumptions taken on the

basis of the case option one. Under this report it can be observed that the figures are taken

form the income statement prepared which can be found in the appendix. Further the variance

is calculated by applying the formula of actual less budgeted. These variances are than

converted into the percentage format. There are several variances which are unfavourable for

the company and require immediate action from the company side (Webb, 2016).

Part 2

The variances are determined as the favourable and unfavourable in the following manner.

Variance report

Particulars Actual Budgete

d

Varian

ce

varian

ce %

favourable/

Unfavourable

$ $

0 51

Cost of Sales 5,360

6,9

68 -1,608 -23%

Gross Profit

2,47,91

0 3,22,283 -74,373 -23%

Selling Expenses

Selling Expenses 5,000

5,0

00 0 -38%

Depreciation 2,342

2,3

89 -47 -2%

Admin and General

Expenses 14180

16,7

32 -2,552 -15%

Total expenses 21,522 24,121 -2,599 -11%

EBIT

2,26,38

8 2,98,162 -71,774 -24%

Interest 5,512 5,512 0 0%

EBT

2,20,87

6 2,92,650 -71,774 -25%

Tax 61845 81942 -20,097 -25%

Other income 275 300

profit after tax

1,59,03

1 2,10,708 -51,677 -25%

The following is the budget report which determines the assumptions taken on the

basis of the case option one. Under this report it can be observed that the figures are taken

form the income statement prepared which can be found in the appendix. Further the variance

is calculated by applying the formula of actual less budgeted. These variances are than

converted into the percentage format. There are several variances which are unfavourable for

the company and require immediate action from the company side (Webb, 2016).

Part 2

The variances are determined as the favourable and unfavourable in the following manner.

Variance report

Particulars Actual Budgete

d

Varian

ce

varian

ce %

favourable/

Unfavourable

$ $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

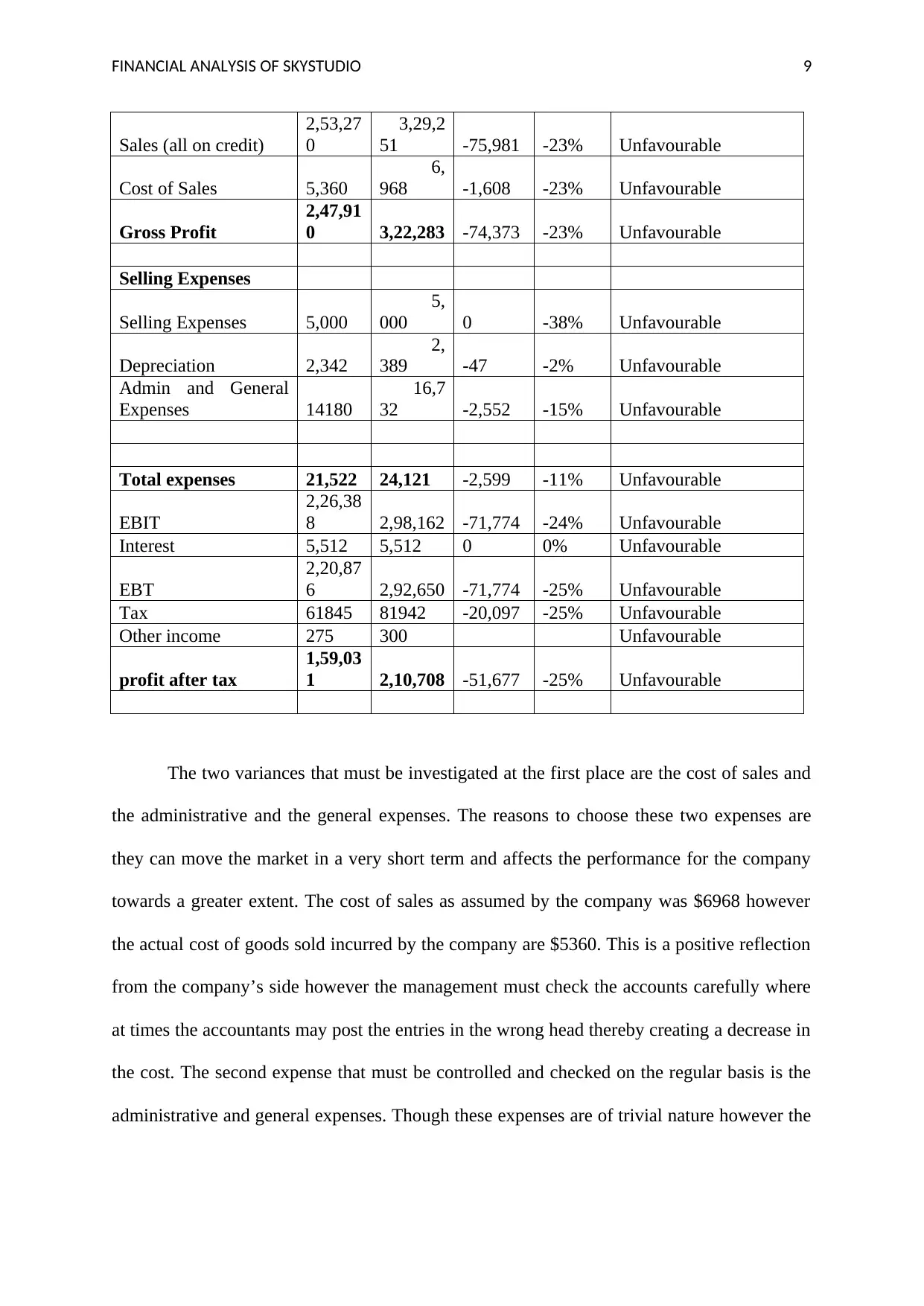

FINANCIAL ANALYSIS OF SKYSTUDIO 9

Sales (all on credit)

2,53,27

0

3,29,2

51 -75,981 -23% Unfavourable

Cost of Sales 5,360

6,

968 -1,608 -23% Unfavourable

Gross Profit

2,47,91

0 3,22,283 -74,373 -23% Unfavourable

Selling Expenses

Selling Expenses 5,000

5,

000 0 -38% Unfavourable

Depreciation 2,342

2,

389 -47 -2% Unfavourable

Admin and General

Expenses 14180

16,7

32 -2,552 -15% Unfavourable

Total expenses 21,522 24,121 -2,599 -11% Unfavourable

EBIT

2,26,38

8 2,98,162 -71,774 -24% Unfavourable

Interest 5,512 5,512 0 0% Unfavourable

EBT

2,20,87

6 2,92,650 -71,774 -25% Unfavourable

Tax 61845 81942 -20,097 -25% Unfavourable

Other income 275 300 Unfavourable

profit after tax

1,59,03

1 2,10,708 -51,677 -25% Unfavourable

The two variances that must be investigated at the first place are the cost of sales and

the administrative and the general expenses. The reasons to choose these two expenses are

they can move the market in a very short term and affects the performance for the company

towards a greater extent. The cost of sales as assumed by the company was $6968 however

the actual cost of goods sold incurred by the company are $5360. This is a positive reflection

from the company’s side however the management must check the accounts carefully where

at times the accountants may post the entries in the wrong head thereby creating a decrease in

the cost. The second expense that must be controlled and checked on the regular basis is the

administrative and general expenses. Though these expenses are of trivial nature however the

Sales (all on credit)

2,53,27

0

3,29,2

51 -75,981 -23% Unfavourable

Cost of Sales 5,360

6,

968 -1,608 -23% Unfavourable

Gross Profit

2,47,91

0 3,22,283 -74,373 -23% Unfavourable

Selling Expenses

Selling Expenses 5,000

5,

000 0 -38% Unfavourable

Depreciation 2,342

2,

389 -47 -2% Unfavourable

Admin and General

Expenses 14180

16,7

32 -2,552 -15% Unfavourable

Total expenses 21,522 24,121 -2,599 -11% Unfavourable

EBIT

2,26,38

8 2,98,162 -71,774 -24% Unfavourable

Interest 5,512 5,512 0 0% Unfavourable

EBT

2,20,87

6 2,92,650 -71,774 -25% Unfavourable

Tax 61845 81942 -20,097 -25% Unfavourable

Other income 275 300 Unfavourable

profit after tax

1,59,03

1 2,10,708 -51,677 -25% Unfavourable

The two variances that must be investigated at the first place are the cost of sales and

the administrative and the general expenses. The reasons to choose these two expenses are

they can move the market in a very short term and affects the performance for the company

towards a greater extent. The cost of sales as assumed by the company was $6968 however

the actual cost of goods sold incurred by the company are $5360. This is a positive reflection

from the company’s side however the management must check the accounts carefully where

at times the accountants may post the entries in the wrong head thereby creating a decrease in

the cost. The second expense that must be controlled and checked on the regular basis is the

administrative and general expenses. Though these expenses are of trivial nature however the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS OF SKYSTUDIO 10

company must carefully assess the reasons of the increase and shall immediately take the

steps to curb it (Balaev, 2017).

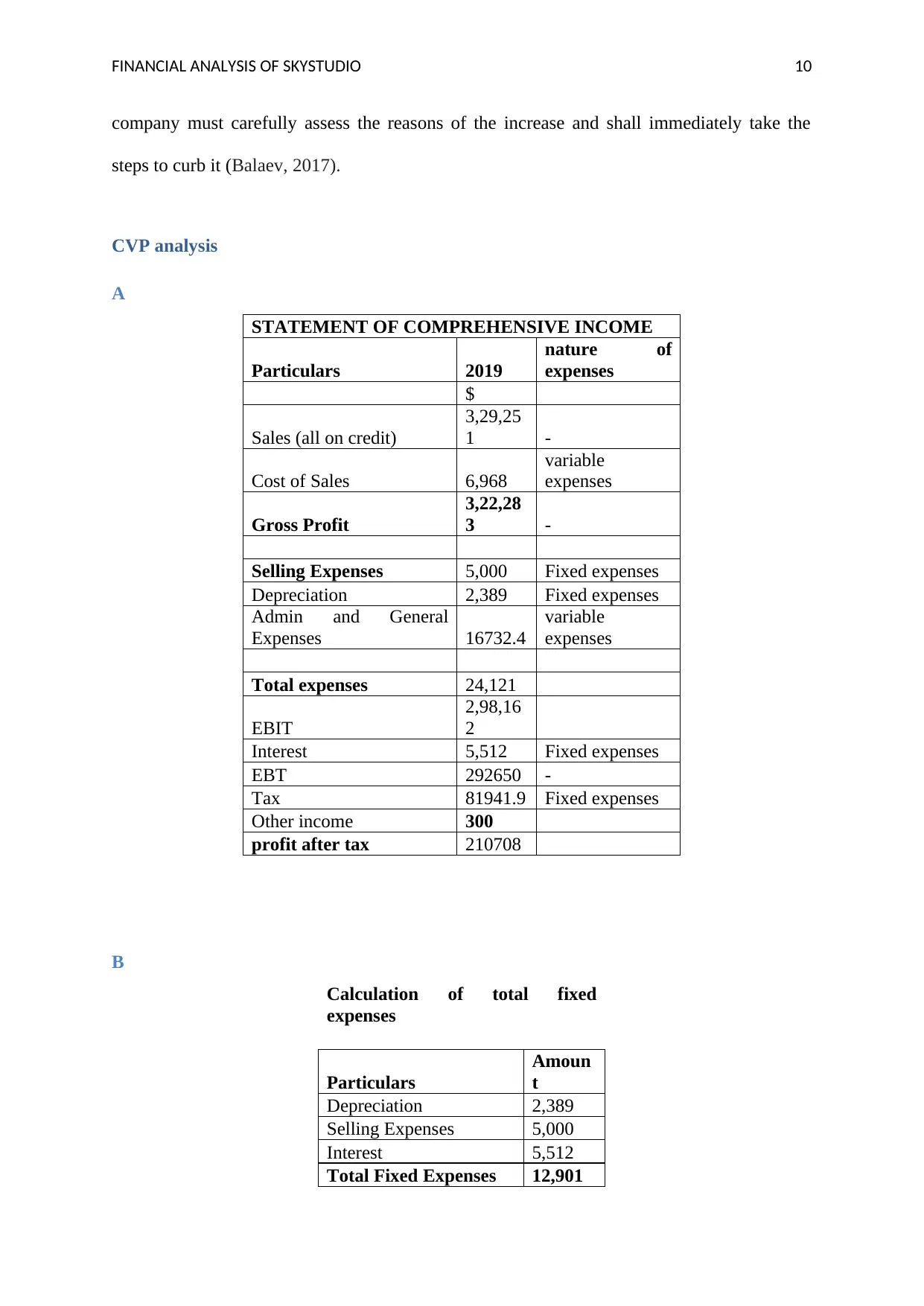

CVP analysis

A

STATEMENT OF COMPREHENSIVE INCOME

Particulars 2019

nature of

expenses

$

Sales (all on credit)

3,29,25

1 -

Cost of Sales 6,968

variable

expenses

Gross Profit

3,22,28

3 -

Selling Expenses 5,000 Fixed expenses

Depreciation 2,389 Fixed expenses

Admin and General

Expenses 16732.4

variable

expenses

Total expenses 24,121

EBIT

2,98,16

2

Interest 5,512 Fixed expenses

EBT 292650 -

Tax 81941.9 Fixed expenses

Other income 300

profit after tax 210708

B

Calculation of total fixed

expenses

Particulars

Amoun

t

Depreciation 2,389

Selling Expenses 5,000

Interest 5,512

Total Fixed Expenses 12,901

company must carefully assess the reasons of the increase and shall immediately take the

steps to curb it (Balaev, 2017).

CVP analysis

A

STATEMENT OF COMPREHENSIVE INCOME

Particulars 2019

nature of

expenses

$

Sales (all on credit)

3,29,25

1 -

Cost of Sales 6,968

variable

expenses

Gross Profit

3,22,28

3 -

Selling Expenses 5,000 Fixed expenses

Depreciation 2,389 Fixed expenses

Admin and General

Expenses 16732.4

variable

expenses

Total expenses 24,121

EBIT

2,98,16

2

Interest 5,512 Fixed expenses

EBT 292650 -

Tax 81941.9 Fixed expenses

Other income 300

profit after tax 210708

B

Calculation of total fixed

expenses

Particulars

Amoun

t

Depreciation 2,389

Selling Expenses 5,000

Interest 5,512

Total Fixed Expenses 12,901

FINANCIAL ANALYSIS OF SKYSTUDIO 11

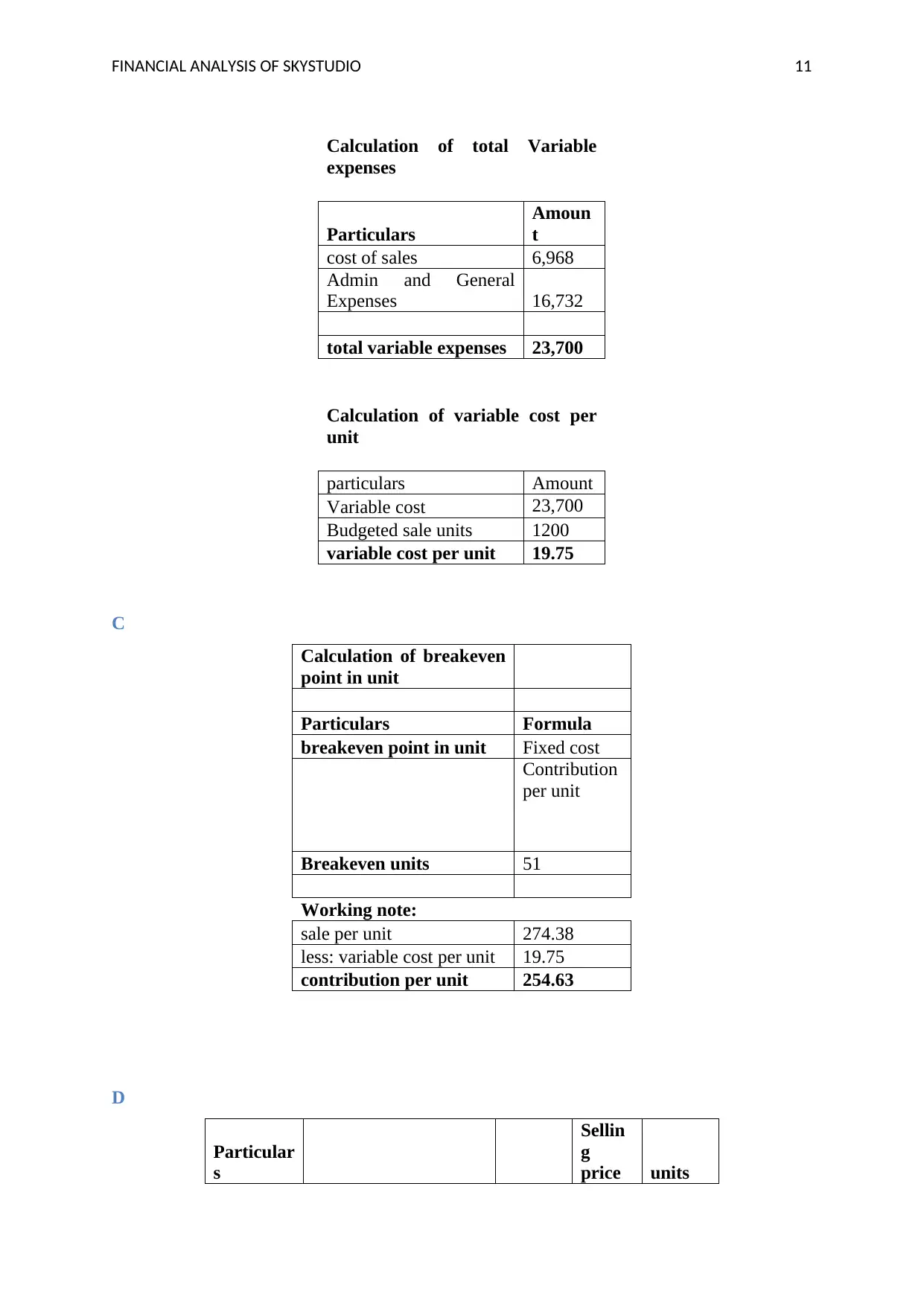

Calculation of total Variable

expenses

Particulars

Amoun

t

cost of sales 6,968

Admin and General

Expenses 16,732

total variable expenses 23,700

Calculation of variable cost per

unit

particulars Amount

Variable cost 23,700

Budgeted sale units 1200

variable cost per unit 19.75

C

Calculation of breakeven

point in unit

Particulars Formula

breakeven point in unit Fixed cost

Contribution

per unit

Breakeven units 51

Working note:

sale per unit 274.38

less: variable cost per unit 19.75

contribution per unit 254.63

D

Particular

s

Sellin

g

price units

Calculation of total Variable

expenses

Particulars

Amoun

t

cost of sales 6,968

Admin and General

Expenses 16,732

total variable expenses 23,700

Calculation of variable cost per

unit

particulars Amount

Variable cost 23,700

Budgeted sale units 1200

variable cost per unit 19.75

C

Calculation of breakeven

point in unit

Particulars Formula

breakeven point in unit Fixed cost

Contribution

per unit

Breakeven units 51

Working note:

sale per unit 274.38

less: variable cost per unit 19.75

contribution per unit 254.63

D

Particular

s

Sellin

g

price units

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.