Analysis of Tesco's Financial Information for Business Accounting

VerifiedAdded on 2021/04/21

|11

|3268

|56

Report

AI Summary

This report analyzes the financial information of Tesco Plc, a UK-based multinational retailer, focusing on how different non-management external users utilize financial statements to make informed decisions. The report examines key financial statements like the balance sheet, income statement, and cash flow statement, and how these are used by banks and financial institutions, creditors, tax authorities, customers, and investors. It highlights the qualitative characteristics of useful financial information, such as understanding, comparability, and verifiability, and discusses Tesco's adherence to International Financial Reporting Standards (IFRS). The report also provides an overview of Tesco's financial performance, including revenue and asset data, and emphasizes the importance of accurate and timely financial reporting for effective investment decisions. The accounting system adopted by Tesco provides all the useful information to a large set of stakeholders ranging from shareholders, creditors and all the persons who have the direct and indirect relation in the company.

RUNNING HEAD: Business Accounting 0

Name of the student

Topic- Business Accounting

University Name

Name of the student

Topic- Business Accounting

University Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Accounting 1

1 Introduction

This report is accompanied by the financial information of a company. It is evaluated that

there are several financial information which is used by the external users of the company to

make the investment decision such as balance sheet, profit and loss and shareholders information

statement. Non-management external users do not make Investment Company for its business

but they invest capital with a view to earning revenue on the same. In this report, Tesco

Company has been taken into consideration. It is the UK based listed company which is running

its business on a domestic and international basis. The non-management external users are

interested in evaluating the past performance of a company and invest on the basis of past and

existing financial performance. Therefore, they ideally use balance sheet, profit and loss and

shareholders information statement. It is evaluated that financial statements are the main key

source of information which is used by stakeholders to make effective investment decisions.

Description of the company

Tesco Plc, trading as Tesco, is a British multinational grocery and general merchandise

retailer company. The Headquarter of company is in Welwyn Garden city, United Kingdom. The

CEO of company is Dave Lewis who takes all the imperative decisions. The stock price of the

company is 202.00 GBX -6.60 (-3.16%) (Lakis and Masiulevičius, 2017).

Key information of Tesco

As Per the annual report of Tesco Company, the overall turnover of the company rose by

4.3% to £49.9 Billion. The operating profit of company is £5,750m which reflects the good

earning capacity of the organization.

The qualitative characteristics of useful financial information reflect the understanding,

comparability, verifiability and timeless which could improve the usefulness of information.

Non-management external users need to analyze whether the performance of a company is

effective or not. If they find that the financial performance of a company is not effective then it

may destruct the value of the investment (Lakis and Masiulevičius, 2017).

1 Introduction

This report is accompanied by the financial information of a company. It is evaluated that

there are several financial information which is used by the external users of the company to

make the investment decision such as balance sheet, profit and loss and shareholders information

statement. Non-management external users do not make Investment Company for its business

but they invest capital with a view to earning revenue on the same. In this report, Tesco

Company has been taken into consideration. It is the UK based listed company which is running

its business on a domestic and international basis. The non-management external users are

interested in evaluating the past performance of a company and invest on the basis of past and

existing financial performance. Therefore, they ideally use balance sheet, profit and loss and

shareholders information statement. It is evaluated that financial statements are the main key

source of information which is used by stakeholders to make effective investment decisions.

Description of the company

Tesco Plc, trading as Tesco, is a British multinational grocery and general merchandise

retailer company. The Headquarter of company is in Welwyn Garden city, United Kingdom. The

CEO of company is Dave Lewis who takes all the imperative decisions. The stock price of the

company is 202.00 GBX -6.60 (-3.16%) (Lakis and Masiulevičius, 2017).

Key information of Tesco

As Per the annual report of Tesco Company, the overall turnover of the company rose by

4.3% to £49.9 Billion. The operating profit of company is £5,750m which reflects the good

earning capacity of the organization.

The qualitative characteristics of useful financial information reflect the understanding,

comparability, verifiability and timeless which could improve the usefulness of information.

Non-management external users need to analyze whether the performance of a company is

effective or not. If they find that the financial performance of a company is not effective then it

may destruct the value of the investment (Lakis and Masiulevičius, 2017).

Business Accounting 2

The objective of financial statements is to provide the financial information such as a

performance of company, position and business sustainability of the company. It is considered

that if stakeholders use this information to either to invest in Tesco plc or to take their investment

decisions. There are several Non-management external users who evaluate financial information

named as balance sheet, profit and loss and shareholders information statement before investing

in Tesco Plc.

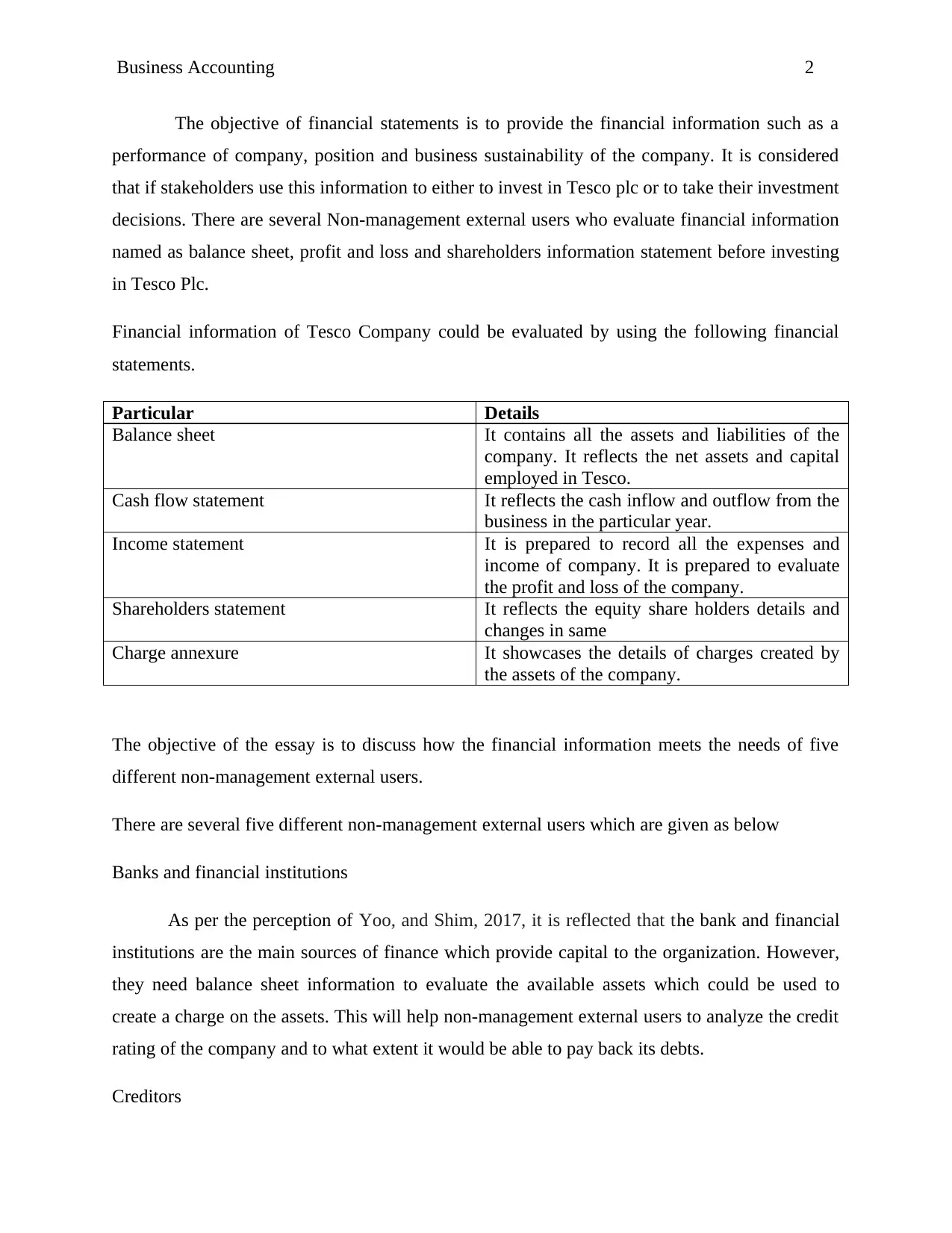

Financial information of Tesco Company could be evaluated by using the following financial

statements.

Particular Details

Balance sheet It contains all the assets and liabilities of the

company. It reflects the net assets and capital

employed in Tesco.

Cash flow statement It reflects the cash inflow and outflow from the

business in the particular year.

Income statement It is prepared to record all the expenses and

income of company. It is prepared to evaluate

the profit and loss of the company.

Shareholders statement It reflects the equity share holders details and

changes in same

Charge annexure It showcases the details of charges created by

the assets of the company.

The objective of the essay is to discuss how the financial information meets the needs of five

different non-management external users.

There are several five different non-management external users which are given as below

Banks and financial institutions

As per the perception of Yoo, and Shim, 2017, it is reflected that the bank and financial

institutions are the main sources of finance which provide capital to the organization. However,

they need balance sheet information to evaluate the available assets which could be used to

create a charge on the assets. This will help non-management external users to analyze the credit

rating of the company and to what extent it would be able to pay back its debts.

Creditors

The objective of financial statements is to provide the financial information such as a

performance of company, position and business sustainability of the company. It is considered

that if stakeholders use this information to either to invest in Tesco plc or to take their investment

decisions. There are several Non-management external users who evaluate financial information

named as balance sheet, profit and loss and shareholders information statement before investing

in Tesco Plc.

Financial information of Tesco Company could be evaluated by using the following financial

statements.

Particular Details

Balance sheet It contains all the assets and liabilities of the

company. It reflects the net assets and capital

employed in Tesco.

Cash flow statement It reflects the cash inflow and outflow from the

business in the particular year.

Income statement It is prepared to record all the expenses and

income of company. It is prepared to evaluate

the profit and loss of the company.

Shareholders statement It reflects the equity share holders details and

changes in same

Charge annexure It showcases the details of charges created by

the assets of the company.

The objective of the essay is to discuss how the financial information meets the needs of five

different non-management external users.

There are several five different non-management external users which are given as below

Banks and financial institutions

As per the perception of Yoo, and Shim, 2017, it is reflected that the bank and financial

institutions are the main sources of finance which provide capital to the organization. However,

they need balance sheet information to evaluate the available assets which could be used to

create a charge on the assets. This will help non-management external users to analyze the credit

rating of the company and to what extent it would be able to pay back its debts.

Creditors

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Accounting 3

These are the persons who provide stocks and other material to the organization on credit

basis. They need the income statement and last past years financial books to determine whether

they should give stocks and other material on credit basis or not.

Tax authorities and regulatory agencies

These tax authorities and regulatory agencies are the main bodies that implement tax

regulatory requirements and impose tax amount. It is evaluated that Tesco needs to submit SEC

regulatory compliance report with the tax authorities to showcase how much tax company has

been paying to the government.

Customers

These are the key stakeholders in the company. They evaluate the quality check list and

other trademarks detail of company to determine whether the company is providing the good

quality of products in the market (Jhanji, Facebook Inc, 2017).

Investors

It is evaluated that investors are the persons who invest in the capital. They need to analyze

the balance sheet, profit and loss and shareholders information statement before investing capital

in the business. In addition to this, the company needs to summarize the historical information on

performance, financial position, and business activities to make an investment decision in the

company (Cañibano, 2017).

As per the perception of Henderson, et al. 2015 it is reflected that the qualitative intents of useful

financial information reflect the understanding, comparability, verifiability and timeless of the

company by using the financial information of the Tesco. It is analyzed that company needs to

provide all the imperative information to its stakeholders so that they could make their financial

investment decisions. However, Tesco Plc has been following international financial reporting

standards in its financial reporting framework (Henderson, et al. 2015). It not only helps in

complying with the reporting requirements but also establishes harmonization in the domestic

and international reporting rules and regulations (Collier, 2015).

These are the persons who provide stocks and other material to the organization on credit

basis. They need the income statement and last past years financial books to determine whether

they should give stocks and other material on credit basis or not.

Tax authorities and regulatory agencies

These tax authorities and regulatory agencies are the main bodies that implement tax

regulatory requirements and impose tax amount. It is evaluated that Tesco needs to submit SEC

regulatory compliance report with the tax authorities to showcase how much tax company has

been paying to the government.

Customers

These are the key stakeholders in the company. They evaluate the quality check list and

other trademarks detail of company to determine whether the company is providing the good

quality of products in the market (Jhanji, Facebook Inc, 2017).

Investors

It is evaluated that investors are the persons who invest in the capital. They need to analyze

the balance sheet, profit and loss and shareholders information statement before investing capital

in the business. In addition to this, the company needs to summarize the historical information on

performance, financial position, and business activities to make an investment decision in the

company (Cañibano, 2017).

As per the perception of Henderson, et al. 2015 it is reflected that the qualitative intents of useful

financial information reflect the understanding, comparability, verifiability and timeless of the

company by using the financial information of the Tesco. It is analyzed that company needs to

provide all the imperative information to its stakeholders so that they could make their financial

investment decisions. However, Tesco Plc has been following international financial reporting

standards in its financial reporting framework (Henderson, et al. 2015). It not only helps in

complying with the reporting requirements but also establishes harmonization in the domestic

and international reporting rules and regulations (Collier, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Accounting 4

It is analyzed that if company shares all the possible information with the stakeholders then it

will increase the overall efficiency of their investment decisions. Accounting system adopted by

the Tesco is designed to provide all the useful information to a large set of stakeholders ranging

from shareholders, creditors and all the persons who have the direct and indirect relation in the

company.

As per the views of Scott, 2015 it is reflected that the non-management external users are

the key investors who invest their capital, and time in the business with a view to creating value

on their capital. However, it could be inferred that lenders like banks and financial institutions

could invest capital in Tesco after evaluating the financial performance of the company. The

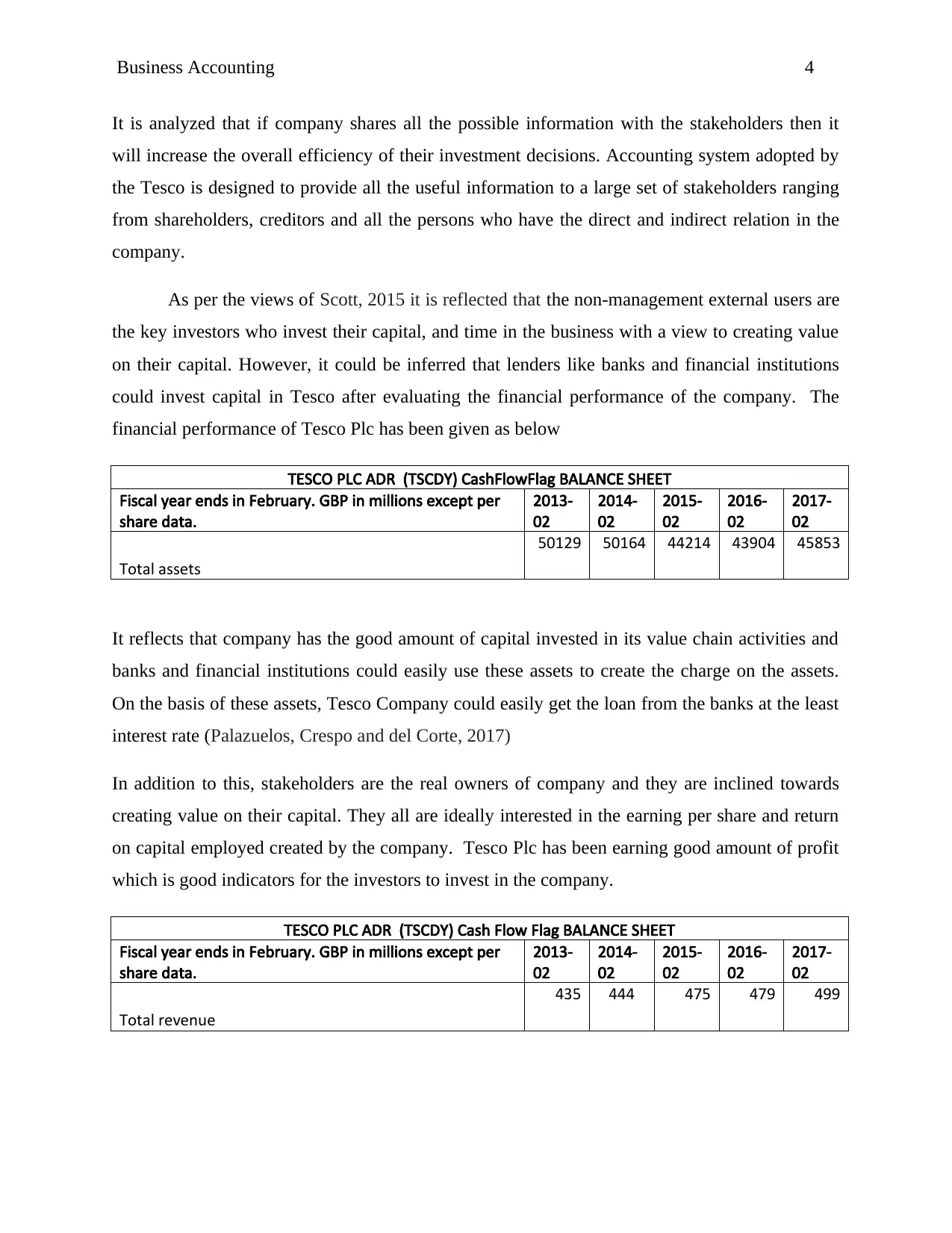

financial performance of Tesco Plc has been given as below

TESCO PLC ADR (TSCDY) CashFlowFlag BALANCE SHEET

Fiscal year ends in February. GBP in millions except per

share data.

2013-

02

2014-

02

2015-

02

2016-

02

2017-

02

Total assets

50129 50164 44214 43904 45853

It reflects that company has the good amount of capital invested in its value chain activities and

banks and financial institutions could easily use these assets to create the charge on the assets.

On the basis of these assets, Tesco Company could easily get the loan from the banks at the least

interest rate (Palazuelos, Crespo and del Corte, 2017)

In addition to this, stakeholders are the real owners of company and they are inclined towards

creating value on their capital. They all are ideally interested in the earning per share and return

on capital employed created by the company. Tesco Plc has been earning good amount of profit

which is good indicators for the investors to invest in the company.

TESCO PLC ADR (TSCDY) Cash Flow Flag BALANCE SHEET

Fiscal year ends in February. GBP in millions except per

share data.

2013-

02

2014-

02

2015-

02

2016-

02

2017-

02

Total revenue

435 444 475 479 499

It is analyzed that if company shares all the possible information with the stakeholders then it

will increase the overall efficiency of their investment decisions. Accounting system adopted by

the Tesco is designed to provide all the useful information to a large set of stakeholders ranging

from shareholders, creditors and all the persons who have the direct and indirect relation in the

company.

As per the views of Scott, 2015 it is reflected that the non-management external users are

the key investors who invest their capital, and time in the business with a view to creating value

on their capital. However, it could be inferred that lenders like banks and financial institutions

could invest capital in Tesco after evaluating the financial performance of the company. The

financial performance of Tesco Plc has been given as below

TESCO PLC ADR (TSCDY) CashFlowFlag BALANCE SHEET

Fiscal year ends in February. GBP in millions except per

share data.

2013-

02

2014-

02

2015-

02

2016-

02

2017-

02

Total assets

50129 50164 44214 43904 45853

It reflects that company has the good amount of capital invested in its value chain activities and

banks and financial institutions could easily use these assets to create the charge on the assets.

On the basis of these assets, Tesco Company could easily get the loan from the banks at the least

interest rate (Palazuelos, Crespo and del Corte, 2017)

In addition to this, stakeholders are the real owners of company and they are inclined towards

creating value on their capital. They all are ideally interested in the earning per share and return

on capital employed created by the company. Tesco Plc has been earning good amount of profit

which is good indicators for the investors to invest in the company.

TESCO PLC ADR (TSCDY) Cash Flow Flag BALANCE SHEET

Fiscal year ends in February. GBP in millions except per

share data.

2013-

02

2014-

02

2015-

02

2016-

02

2017-

02

Total revenue

435 444 475 479 499

Business Accounting 5

After evaluating the annual report of Tesco, it is evaluated that the total revenue of company has

increased by 15% since last five years. It is good indictors for the shareholders to invest money

in the business of Tesco. In addition to this, the consistent returns to investors will also assist in

creating the value of the investment in determined approach. It is evaluated that shareholders

find this information from the income statement of the company and analysis the same for their

investment decision (Lanen, 2016).

On the contrary to that, investors such as angle investors, venture capitalist and other investors

asses all the past and present financial data of company before investing their capital. After

evaluating their all the financial records and performance of the company, if they find that

company has good potential to earn return in future then they could easily invest in Tesco (Khairi

and Baridwan, 2015).

It requires the company to implement consistent impairment test to determine whether the assets

shown in the books of accounts are booked at their original value. It helps in eliminating the

assets books cost and reflects the true and fair view of assets in the best possible manner

(Palazuelos, Crespo and del Corte, 2017).

As stated by Bach and Hang, 2016 it is revealed that financial information presented in the

financial statements need to have some quality intents which make this information useful for the

users. It is evaluated that generally accepted accounting principles and IFRS rules and standards

helps an organization to include all these characterized and enhancing qualitative intents. It

includes following factors which are given as below.

Relevancy- The Tesco Company has made all of its financial information relevant to its

stakeholders. All the financial information has been formulated in the particular statement as per

its relevancy. For instance, all the capital expenses have been shown on the balance sheet and on

the contrary to that, revenue expenses have been included in the profit and loss account. This

relevancy is designed on the basis of materiality concept. It increases the overall interpretability

of the financial data (Super and Shil, 2017).

Faithfull representation- The financial statement of Tesco has been formulated on the basis of

accounting standards and accounting rules. For instance, Tesco implements proper impairment

test on its assets whenever it requires reflecting the true and fair view of its assets.

After evaluating the annual report of Tesco, it is evaluated that the total revenue of company has

increased by 15% since last five years. It is good indictors for the shareholders to invest money

in the business of Tesco. In addition to this, the consistent returns to investors will also assist in

creating the value of the investment in determined approach. It is evaluated that shareholders

find this information from the income statement of the company and analysis the same for their

investment decision (Lanen, 2016).

On the contrary to that, investors such as angle investors, venture capitalist and other investors

asses all the past and present financial data of company before investing their capital. After

evaluating their all the financial records and performance of the company, if they find that

company has good potential to earn return in future then they could easily invest in Tesco (Khairi

and Baridwan, 2015).

It requires the company to implement consistent impairment test to determine whether the assets

shown in the books of accounts are booked at their original value. It helps in eliminating the

assets books cost and reflects the true and fair view of assets in the best possible manner

(Palazuelos, Crespo and del Corte, 2017).

As stated by Bach and Hang, 2016 it is revealed that financial information presented in the

financial statements need to have some quality intents which make this information useful for the

users. It is evaluated that generally accepted accounting principles and IFRS rules and standards

helps an organization to include all these characterized and enhancing qualitative intents. It

includes following factors which are given as below.

Relevancy- The Tesco Company has made all of its financial information relevant to its

stakeholders. All the financial information has been formulated in the particular statement as per

its relevancy. For instance, all the capital expenses have been shown on the balance sheet and on

the contrary to that, revenue expenses have been included in the profit and loss account. This

relevancy is designed on the basis of materiality concept. It increases the overall interpretability

of the financial data (Super and Shil, 2017).

Faithfull representation- The financial statement of Tesco has been formulated on the basis of

accounting standards and accounting rules. For instance, Tesco implements proper impairment

test on its assets whenever it requires reflecting the true and fair view of its assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Accounting 6

Comparability- It requires the financial information of company comparable to other financial

data of company. The financial data of Tesco Company has been recorded on the basis of listing

rules and regulations. Therefore, it could be compared only with the listed companies in the UK

(Dechow and Skinner, 2010).

Verifiability- It requires communication of the all the financial information of Tesco with the

people or stakeholders. Management verifies all the financial records of the company by using

the invoices and financial books of company.

Timeliness- It is evaluated that all the financial information and records of the company should

be periodically disclosed by following the proper reporting rules and regulations. In addition to

this, timelessness also put emphasis upon providing all the financial information to the users in

time so that they could make their investment decisions on the basis of available financial data.

Understand ability- It is analyzed that all the financial information and financial records should

be easy to understand. Tesco Company has followed international financial reporting standards

to eliminate the recording and reporting issues in the financial records. All the information in the

annual report of a company has been presented clearly and concisely. Nonetheless, in order to

mitigate the complex issue data, notes to financial information have also been added for the

better understanding of data.

They use this information to make effective business and implement proper business functioning.

On the other hand, employees are interested in using the books and raw data to evaluate whether

they are performing in right way or not. In context with the banks and financial institutions, they

check the financial performance such as total revenue, total assets, charged created assets and

other information. It helps them to determine whether the company is eligible to take the loan

from them or not (Chaney, Faccio and Parsley, 2011).

Government entities need financial information such as balance sheet, income statements to

determine the accuracy of the taxes payable by company and other duties. It helps them to assess

whether Tesco Company is providing proper amount of tax or not.

It is evaluated that the share market is highly based on the financial data shared by

company in its annual report. It is analyzed that Tesco Company has the strong financial position

Comparability- It requires the financial information of company comparable to other financial

data of company. The financial data of Tesco Company has been recorded on the basis of listing

rules and regulations. Therefore, it could be compared only with the listed companies in the UK

(Dechow and Skinner, 2010).

Verifiability- It requires communication of the all the financial information of Tesco with the

people or stakeholders. Management verifies all the financial records of the company by using

the invoices and financial books of company.

Timeliness- It is evaluated that all the financial information and records of the company should

be periodically disclosed by following the proper reporting rules and regulations. In addition to

this, timelessness also put emphasis upon providing all the financial information to the users in

time so that they could make their investment decisions on the basis of available financial data.

Understand ability- It is analyzed that all the financial information and financial records should

be easy to understand. Tesco Company has followed international financial reporting standards

to eliminate the recording and reporting issues in the financial records. All the information in the

annual report of a company has been presented clearly and concisely. Nonetheless, in order to

mitigate the complex issue data, notes to financial information have also been added for the

better understanding of data.

They use this information to make effective business and implement proper business functioning.

On the other hand, employees are interested in using the books and raw data to evaluate whether

they are performing in right way or not. In context with the banks and financial institutions, they

check the financial performance such as total revenue, total assets, charged created assets and

other information. It helps them to determine whether the company is eligible to take the loan

from them or not (Chaney, Faccio and Parsley, 2011).

Government entities need financial information such as balance sheet, income statements to

determine the accuracy of the taxes payable by company and other duties. It helps them to assess

whether Tesco Company is providing proper amount of tax or not.

It is evaluated that the share market is highly based on the financial data shared by

company in its annual report. It is analyzed that Tesco Company has the strong financial position

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Accounting 7

and consistently increasing its overall profit. It is determined that investors are vigilant about the

market risk and make their investment decisions on the basis of all the financial documents of the

company. They analyze the growth and efficiency and past financial performance of company

before investing the capital. On the basis of last five years data of Tesco, it is analyzed that Tesco

has increased its overall profit and turnover. It has increased the return on capital employed

available to shareholders (Barth, Landsman and Lang, 2008).

Weakness of the provision of financial information

It is evaluated that when a company does not have adequate control in the recording and

reporting framework of financial information then it may destruct the true and fair view of assets

of company. The main weakness of the financial statement of the company is given below

Dependence of historical costs- All the transactions in the books of accounts of Tesco are

recorded at their cost. It may distract the true and fair view of the assets as compared to their

market value.

Inflationary Effects- If the inflation rate is relatively high, the amounts associated with the assets

and liabilities shown in the balance sheet would appear very low. This may also distract the true

value of assets.

No recording of intangible assets- It is easy to understand that Brand value cannot be quantified

by the company so it is not recorded in the books of account. Nonetheless, any expenses made on

the intangible assets are charged as revenue expenses. It may also deviate the profit and loss of

the company.

No future results- All the data shown in the financial statements either reflects the historical data

or present year data which may not be the good use for the investors who are unable to

implement proper trend analysis (Lobo. and Zhou, 2011).

2 Conclusion

These financial statements could be described as records of financial and non-financial

information. Financial statements are used by investors to make important financial decisions.

Owners and management of company require financial information to make effective business

and consistently increasing its overall profit. It is determined that investors are vigilant about the

market risk and make their investment decisions on the basis of all the financial documents of the

company. They analyze the growth and efficiency and past financial performance of company

before investing the capital. On the basis of last five years data of Tesco, it is analyzed that Tesco

has increased its overall profit and turnover. It has increased the return on capital employed

available to shareholders (Barth, Landsman and Lang, 2008).

Weakness of the provision of financial information

It is evaluated that when a company does not have adequate control in the recording and

reporting framework of financial information then it may destruct the true and fair view of assets

of company. The main weakness of the financial statement of the company is given below

Dependence of historical costs- All the transactions in the books of accounts of Tesco are

recorded at their cost. It may distract the true and fair view of the assets as compared to their

market value.

Inflationary Effects- If the inflation rate is relatively high, the amounts associated with the assets

and liabilities shown in the balance sheet would appear very low. This may also distract the true

value of assets.

No recording of intangible assets- It is easy to understand that Brand value cannot be quantified

by the company so it is not recorded in the books of account. Nonetheless, any expenses made on

the intangible assets are charged as revenue expenses. It may also deviate the profit and loss of

the company.

No future results- All the data shown in the financial statements either reflects the historical data

or present year data which may not be the good use for the investors who are unable to

implement proper trend analysis (Lobo. and Zhou, 2011).

2 Conclusion

These financial statements could be described as records of financial and non-financial

information. Financial statements are used by investors to make important financial decisions.

Owners and management of company require financial information to make effective business

Business Accounting 8

decisions. It assists stakeholders to make effective investment decisions. After evaluating all the

financial information and its uses for the non-management external users, it could be inferred

that they need to first analysis this information in their hand before taking any investment

decisions. The Tesco Company has been performing good amount of return from its business.

However, the financial statement and other documents of company have been reported on the

basis of proper IFRS rules and accounting standards. IAS-136 rules and regulation have been

followed by Tesco Company to reflect the true and fair value of its assets to its stakeholder.

However, Tesco Company is reflecting the strong financial position but non – management

external users could also use financial analysis tools such as ratio analysis, capital budgeting

technique and cost-benefit analysis to make effective investment decisions.

decisions. It assists stakeholders to make effective investment decisions. After evaluating all the

financial information and its uses for the non-management external users, it could be inferred

that they need to first analysis this information in their hand before taking any investment

decisions. The Tesco Company has been performing good amount of return from its business.

However, the financial statement and other documents of company have been reported on the

basis of proper IFRS rules and accounting standards. IAS-136 rules and regulation have been

followed by Tesco Company to reflect the true and fair value of its assets to its stakeholder.

However, Tesco Company is reflecting the strong financial position but non – management

external users could also use financial analysis tools such as ratio analysis, capital budgeting

technique and cost-benefit analysis to make effective investment decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Accounting 9

3 References

Bach, L.T., and Hang, N.T., 2016. Accounting information quality in emerging markets:

Conservatism in financial reporting of Vietnamese firms in the context of international economic

integration. International Journal of Economics and Financial Issues, 6(6S).

Barth, M.E., Landsman, W.R. and Lang, M.H., 2008. International accounting standards and

accounting quality. Journal of accounting research, 46(3), pp.467-498.

Cañibano, L., 2017. Accounting and intangibles.

Chaney, P.K., Faccio, M. and Parsley, D., 2011. The quality of accounting information in

politically connected firms. Journal of Accounting and Economics, 51(1-2), pp.58-76.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Dechow, P.M. and Skinner, D.J., 2010. Earnings management: Reconciling the views of

accounting academics, practitioners, and regulators. Accounting Horizons, 14(2), pp.235-250.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Jhanji, N., Facebook Inc, 2017. Communicating information describing the activity of computer

system users among computer system users. U.S. Patent 9,584,460.

Khairi, M.S., and Baridwan, Z., 2015. An empirical study on organizational acceptance

accounting information systems in Sharia banking. The International Journal of Accounting and

Business Society, 23(1), pp.97-122.

Lakis, V. and Masiulevičius, A., 2017. ACCEPTABLE AUDIT MATERIALITY FOR USERS

OF FINANCIAL STATEMENTS. Journal of Management, 2(31).

Lanen, W., 2016. Fundamentals of cost accounting. McGraw-Hill Higher Education.

3 References

Bach, L.T., and Hang, N.T., 2016. Accounting information quality in emerging markets:

Conservatism in financial reporting of Vietnamese firms in the context of international economic

integration. International Journal of Economics and Financial Issues, 6(6S).

Barth, M.E., Landsman, W.R. and Lang, M.H., 2008. International accounting standards and

accounting quality. Journal of accounting research, 46(3), pp.467-498.

Cañibano, L., 2017. Accounting and intangibles.

Chaney, P.K., Faccio, M. and Parsley, D., 2011. The quality of accounting information in

politically connected firms. Journal of Accounting and Economics, 51(1-2), pp.58-76.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Dechow, P.M. and Skinner, D.J., 2010. Earnings management: Reconciling the views of

accounting academics, practitioners, and regulators. Accounting Horizons, 14(2), pp.235-250.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Jhanji, N., Facebook Inc, 2017. Communicating information describing the activity of computer

system users among computer system users. U.S. Patent 9,584,460.

Khairi, M.S., and Baridwan, Z., 2015. An empirical study on organizational acceptance

accounting information systems in Sharia banking. The International Journal of Accounting and

Business Society, 23(1), pp.97-122.

Lakis, V. and Masiulevičius, A., 2017. ACCEPTABLE AUDIT MATERIALITY FOR USERS

OF FINANCIAL STATEMENTS. Journal of Management, 2(31).

Lanen, W., 2016. Fundamentals of cost accounting. McGraw-Hill Higher Education.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Accounting 10

Lobo, G.J., and Zhou, J., 2011. Disclosure quality and earnings management. Asia-Pacific

Journal of Accounting & Economics, 8(1), pp.1-20.

Palazuelos, E., Crespo, Á.H. and del Corte, J.M., 2017. Accounting information quality and trust

as determinants of credit granting to SMEs: the role of external audit. Small Business Economics,

pp.1-17.

Palazuelos, E., Crespo, Á.H. and del Corte, J.M., 2017. Accounting information quality and trust

as determinants of credit granting to SMEs: the role of external audit. Small Business Economics,

pp.1-17.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Super, S.O. and Shil, N.C., 2017. Determinants of Quality Accounting Information

Disclosure. Journal of Accounting and Finance in Emerging Economies, 3(1), pp.79-86.

Yoo, J.S. and Shim, T., 2017. The Effect of Financial Statement Presentation on Behavior of

Professional and Nonprofessional Information Users.

Lobo, G.J., and Zhou, J., 2011. Disclosure quality and earnings management. Asia-Pacific

Journal of Accounting & Economics, 8(1), pp.1-20.

Palazuelos, E., Crespo, Á.H. and del Corte, J.M., 2017. Accounting information quality and trust

as determinants of credit granting to SMEs: the role of external audit. Small Business Economics,

pp.1-17.

Palazuelos, E., Crespo, Á.H. and del Corte, J.M., 2017. Accounting information quality and trust

as determinants of credit granting to SMEs: the role of external audit. Small Business Economics,

pp.1-17.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Super, S.O. and Shil, N.C., 2017. Determinants of Quality Accounting Information

Disclosure. Journal of Accounting and Finance in Emerging Economies, 3(1), pp.79-86.

Yoo, J.S. and Shim, T., 2017. The Effect of Financial Statement Presentation on Behavior of

Professional and Nonprofessional Information Users.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.