West Ltd Financial Accounting Report: AASB Standards and Analysis

VerifiedAdded on 2021/02/21

|12

|3196

|27

Report

AI Summary

This report provides a detailed analysis of the financial accounting practices of West Ltd, focusing on the application of Australian Accounting Standards Board (AASB) standards. The report begins with an executive summary and an introduction to financial accounting, followed by an examination of the case study provided. The main body of the report delves into specific AASB standards, including AASB 136 (Impairment of Assets) and AASB 138 (Intangible Assets), and their relevance to West Ltd's operations. It analyzes the impact of potential asset impairments, particularly concerning the 'Steve Irwin' ship, and the treatment of goodwill and brand recognition. The report includes projected income statement and balance sheet data for 2018 and 2019, illustrating the financial effects of the proposed accounting treatments. Finally, the report offers recommendations based on the analysis and concludes with a summary of the key findings. The report aims to provide a clear understanding of financial accounting principles and their practical application in a business context.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Financial accounting is method of accounting system that follow the guideline of the

accounting standard which is provided by the AIAS. The study report is concise the main

framework of the accounting processes and accounting standard that is applicable on the given

case study. To better understand the concept of the financial accounting this report includes

virtual calculations and its recommendation in context to company West Ltd. Systematic

accounting treatment of the financial aspects also covered in this report.

Financial accounting is method of accounting system that follow the guideline of the

accounting standard which is provided by the AIAS. The study report is concise the main

framework of the accounting processes and accounting standard that is applicable on the given

case study. To better understand the concept of the financial accounting this report includes

virtual calculations and its recommendation in context to company West Ltd. Systematic

accounting treatment of the financial aspects also covered in this report.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................2

MAIN BODY ..................................................................................................................................2

TASK...............................................................................................................................................2

AASB 136: Impairment of Assets:.............................................................................................3

AASB 138 Intangible Assets:......................................................................................................4

Effect on income statement and balance sheet by this proposal to West Ltd: ............................5

RECOMMENDATION...................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

1

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................2

MAIN BODY ..................................................................................................................................2

TASK...............................................................................................................................................2

AASB 136: Impairment of Assets:.............................................................................................3

AASB 138 Intangible Assets:......................................................................................................4

Effect on income statement and balance sheet by this proposal to West Ltd: ............................5

RECOMMENDATION...................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is branch of accounting that keeps the record of the business

transaction by following the standard guideline of IAS. It is also defined as recording, analysing,

interpreting, reporting of the monetary transaction in order to prepare of the financial statement.

The business transaction are recorded in a summarizes form that provides the financial situation

of a company (Chen and et.al, 2016). It enables to ascertain the financial position of the company

in order to generating profit and loss from income statement and provides the data related to

financial situation from balance sheet. This report covers the case study of West Ltd and

provides recommendation to chairman of the West Ltd. In further to, it covers the certain

accounting standard and effect on the financial statement with this proposal.

MAIN BODY

TASK

As per the information in the case study, West Ltd is involved in selling the frozen and

canned fish products. The product are sold under different brand names. As those fishes caught

from southern Australian ocean are sold under the name of Artic fresh trade name. This brand

name is developed when the operation business started and still sold with the same name.

Another brand is 'tropical taste'. Those fishes caught from northern sea are sold with the brand

name of tropical taste. This brand is developed by the Fishy tales Ltd. West Ltd is acquire the

business of the fishy tales Ltd certain year prior. West Ltd is marketed its products in

environment friendly manner. And public recommended this company as dolphin friendly

company and marketing manager ascertained the efforts of ship, Steve Irwin, to potentially

prevent the whalers attempts in the southern-oceans and received the publicity (Al-Shaer, Salama

and Toms, 2017).

It is recommanded to the management body that West Ltd can enhance the

environmentally accountable image by assuring that if any hurt caused to Steve Irwin, It may

result as guaranty to repair the damages. As the management thinks this initiative can enhance

the public images of West Ltd and increase the goodwill too. He provides the guarantee that it

would not affect financial condition of West Ltd. He further discussed as if any damages to the

Steve Irwin fall out, West Ltd can capitalize the repair expenditure on carrying money of the

brands. All the expenses will be incurred by the company for marketing purpose. In this given

2

Financial accounting is branch of accounting that keeps the record of the business

transaction by following the standard guideline of IAS. It is also defined as recording, analysing,

interpreting, reporting of the monetary transaction in order to prepare of the financial statement.

The business transaction are recorded in a summarizes form that provides the financial situation

of a company (Chen and et.al, 2016). It enables to ascertain the financial position of the company

in order to generating profit and loss from income statement and provides the data related to

financial situation from balance sheet. This report covers the case study of West Ltd and

provides recommendation to chairman of the West Ltd. In further to, it covers the certain

accounting standard and effect on the financial statement with this proposal.

MAIN BODY

TASK

As per the information in the case study, West Ltd is involved in selling the frozen and

canned fish products. The product are sold under different brand names. As those fishes caught

from southern Australian ocean are sold under the name of Artic fresh trade name. This brand

name is developed when the operation business started and still sold with the same name.

Another brand is 'tropical taste'. Those fishes caught from northern sea are sold with the brand

name of tropical taste. This brand is developed by the Fishy tales Ltd. West Ltd is acquire the

business of the fishy tales Ltd certain year prior. West Ltd is marketed its products in

environment friendly manner. And public recommended this company as dolphin friendly

company and marketing manager ascertained the efforts of ship, Steve Irwin, to potentially

prevent the whalers attempts in the southern-oceans and received the publicity (Al-Shaer, Salama

and Toms, 2017).

It is recommanded to the management body that West Ltd can enhance the

environmentally accountable image by assuring that if any hurt caused to Steve Irwin, It may

result as guaranty to repair the damages. As the management thinks this initiative can enhance

the public images of West Ltd and increase the goodwill too. He provides the guarantee that it

would not affect financial condition of West Ltd. He further discussed as if any damages to the

Steve Irwin fall out, West Ltd can capitalize the repair expenditure on carrying money of the

brands. All the expenses will be incurred by the company for marketing purpose. In this given

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

situation the net assets position of the company may be increased but there is no effect on the

income statement of the company. This is the good situation for company to grow in the future.

So as per content conferred by managers of the West's Ltd. here is a further discussion on

importance, relevance of accounting standards as well as specific treatment of accounting

standards in presented case scenario (Brusca and Martínez, 2016).

Accounting standard are the common set of principles, regulation, rules and standard

that defined the fundamental business practice and policies of financial accounting. Accounting

standards improves the quality of the financial statements and enrich the transparency of

financial reporting. Financial statements are presented by the management of a firm by following

certain rule and processor and the accounting standard guide the whole financial report in such as

systematic and well defined manner. These are the fundamental rule that needs to be adopted by

the business organisation to present a better understanding through the financial system. As the

business situated in the Australia so in the financial statement of the West Ltd are prepared by

considering the rules and regulation of the Australia accounting standards. AAS are developed

by the Australian accounting standards boards. The main purpose of the AAS is to elevate the

structure of the financial accounting. The financial reports are being prepared by the West Ltd in

accordance with the norms of the AAS. If they fails to adopt the financial regulation provided by

boards, it needs to be pay for it (Gimbar, Hansen and Ozlanski, 2016). Accounting measure

enable managers to provide data in a significant way so it can be easily processed and interpreted

by internal as well as external stakeholder of the firm through annual reports of the business. The

business data and information needs to be provided in a systematic manner and accurate to the

internal management of the company so they can easily make the decision regards in future. Well

designed data and followed by the accounting standards surge the trust of the external user of the

business. The company needs to appoint a accountant in the firm to records and check the

operational activities of the firm. An accountant's obligation is to provide accurate, positive,

appropriate and systematic data to the management. Financial reports that are prepared with

compliance of the accounting standards inflate investor belief. Here is described some key

relevant accounting standard that applicable on case study of West Ltd-

AASB 136: Impairment of Assets:

This is the accounting standard related to financial structure of a firm that provides a

framework to the business model in order to ensure the non financial assets are not carried the

3

income statement of the company. This is the good situation for company to grow in the future.

So as per content conferred by managers of the West's Ltd. here is a further discussion on

importance, relevance of accounting standards as well as specific treatment of accounting

standards in presented case scenario (Brusca and Martínez, 2016).

Accounting standard are the common set of principles, regulation, rules and standard

that defined the fundamental business practice and policies of financial accounting. Accounting

standards improves the quality of the financial statements and enrich the transparency of

financial reporting. Financial statements are presented by the management of a firm by following

certain rule and processor and the accounting standard guide the whole financial report in such as

systematic and well defined manner. These are the fundamental rule that needs to be adopted by

the business organisation to present a better understanding through the financial system. As the

business situated in the Australia so in the financial statement of the West Ltd are prepared by

considering the rules and regulation of the Australia accounting standards. AAS are developed

by the Australian accounting standards boards. The main purpose of the AAS is to elevate the

structure of the financial accounting. The financial reports are being prepared by the West Ltd in

accordance with the norms of the AAS. If they fails to adopt the financial regulation provided by

boards, it needs to be pay for it (Gimbar, Hansen and Ozlanski, 2016). Accounting measure

enable managers to provide data in a significant way so it can be easily processed and interpreted

by internal as well as external stakeholder of the firm through annual reports of the business. The

business data and information needs to be provided in a systematic manner and accurate to the

internal management of the company so they can easily make the decision regards in future. Well

designed data and followed by the accounting standards surge the trust of the external user of the

business. The company needs to appoint a accountant in the firm to records and check the

operational activities of the firm. An accountant's obligation is to provide accurate, positive,

appropriate and systematic data to the management. Financial reports that are prepared with

compliance of the accounting standards inflate investor belief. Here is described some key

relevant accounting standard that applicable on case study of West Ltd-

AASB 136: Impairment of Assets:

This is the accounting standard related to financial structure of a firm that provides a

framework to the business model in order to ensure the non financial assets are not carried the

3

amount from its recoverable amount. This is basically defines the class of assets and net

recoverable value from it. AASB asses the value of the assets that is not to be over from its

recoverable amount or fair value of the assets. In case, a assets can be diminished in the present

scenario is needs to be ascertain the current value of the assets. This accounting standard applies

on the intangible assets such as goodwill, copyrights, patent and other that can not be amortise or

not physically present in the business. The main concept of this AS is to a assets value and cost

should not be overvalued in the financial statement that shows the fair value or most recoverable

amount in the books of accounts. If the assets is damages than its carries the recoverable amount

that's the only purpose behind this AASB 136. A business should diminished the value of assets

to it recoverable amount to proper representation of the financial statement (Hoitash and Hoitash,

2017).

Recoverable amount is assessed for those assets class which are related with amount

generating business unit in the organisation. The cash creating business unit is lowest cash

inflow generating unit that is dependent on the other class or group of assets. These business unit

can not be better than institution's operating section. So in the case amount can be analysed in

respect with individual asset class.

Impairment loss is acknowledged as profit or loss as such asset is shown at revalued price

according to the provisions of accounting Standard which is settled in AASB 116. Revaluation of

the assets class may occur the impairment loss that is basically treated in the decrement of the

value of assets as per accounting standard (Weygandt, Kimmel and Kieso, 2018).

In this case study of West Ltd, after the acquisition of the Fishy tales Ltd all the financial

value like assets and liabilities of the business also taken into account by West Ltd so the ship

named Steve Irwin added to impairment of assets in the business. By utilisation of the Steve

Irwin in business, it increase the operational function as well as goodwill of the organisation.

According to this AASB 138 on above case scenario there will be no impairment loss in

goodwill of firm. In addition to, Steve Irwin is asset of West Ltd and the expenses of it can

capitalise as repair costs to the carrying sum of money of goodwill. An impairment loss is

recognized as profit or loss of the firm (Sunder, 2016).

AASB 138 Intangible Assets:

This is accounting standard that issued by the international accounting standard board. It

is all about the recognition an intangible assets,measurement and requirement for disclosing of

4

recoverable value from it. AASB asses the value of the assets that is not to be over from its

recoverable amount or fair value of the assets. In case, a assets can be diminished in the present

scenario is needs to be ascertain the current value of the assets. This accounting standard applies

on the intangible assets such as goodwill, copyrights, patent and other that can not be amortise or

not physically present in the business. The main concept of this AS is to a assets value and cost

should not be overvalued in the financial statement that shows the fair value or most recoverable

amount in the books of accounts. If the assets is damages than its carries the recoverable amount

that's the only purpose behind this AASB 136. A business should diminished the value of assets

to it recoverable amount to proper representation of the financial statement (Hoitash and Hoitash,

2017).

Recoverable amount is assessed for those assets class which are related with amount

generating business unit in the organisation. The cash creating business unit is lowest cash

inflow generating unit that is dependent on the other class or group of assets. These business unit

can not be better than institution's operating section. So in the case amount can be analysed in

respect with individual asset class.

Impairment loss is acknowledged as profit or loss as such asset is shown at revalued price

according to the provisions of accounting Standard which is settled in AASB 116. Revaluation of

the assets class may occur the impairment loss that is basically treated in the decrement of the

value of assets as per accounting standard (Weygandt, Kimmel and Kieso, 2018).

In this case study of West Ltd, after the acquisition of the Fishy tales Ltd all the financial

value like assets and liabilities of the business also taken into account by West Ltd so the ship

named Steve Irwin added to impairment of assets in the business. By utilisation of the Steve

Irwin in business, it increase the operational function as well as goodwill of the organisation.

According to this AASB 138 on above case scenario there will be no impairment loss in

goodwill of firm. In addition to, Steve Irwin is asset of West Ltd and the expenses of it can

capitalise as repair costs to the carrying sum of money of goodwill. An impairment loss is

recognized as profit or loss of the firm (Sunder, 2016).

AASB 138 Intangible Assets:

This is accounting standard that issued by the international accounting standard board. It

is all about the recognition an intangible assets,measurement and requirement for disclosing of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

these assets class. As per this standard, the proper accounting treatment of the intangible assets

in the financial statement of an company. The accounting standard specks about the carrying

amount that needs to be disclosed in the financial accounting. In this standard the discloser

amount of R&D expenditure, start up, advertisement expenses, training and induction

programme and other capital expenses included (Kanagaretnam, Zhang and Zhang, 2016) .

Intangible assets are those which is lack of physical presence in nature and some of the

example are goodwill, brand recognition, patents. Value of Goodwill shown in balance sheet is

goodwill amount that consider the value from business merger, acquisition for which a particular

cost has been made by receiving company in prospect of future benefits.

In the context to this company, brand goodwill has increased at the time of the formal

acquiring of the business. In the assets class, condition that caused the impairment loss are

favourably settled. At the time of occurrence of acquisition, asset’s carrying amount will

increase, but not as extra value that it would have been adjust with prior impairment loss.

Depreciation on Steve Irwin repair cost can be tuned in future time period (Duff, 2016).

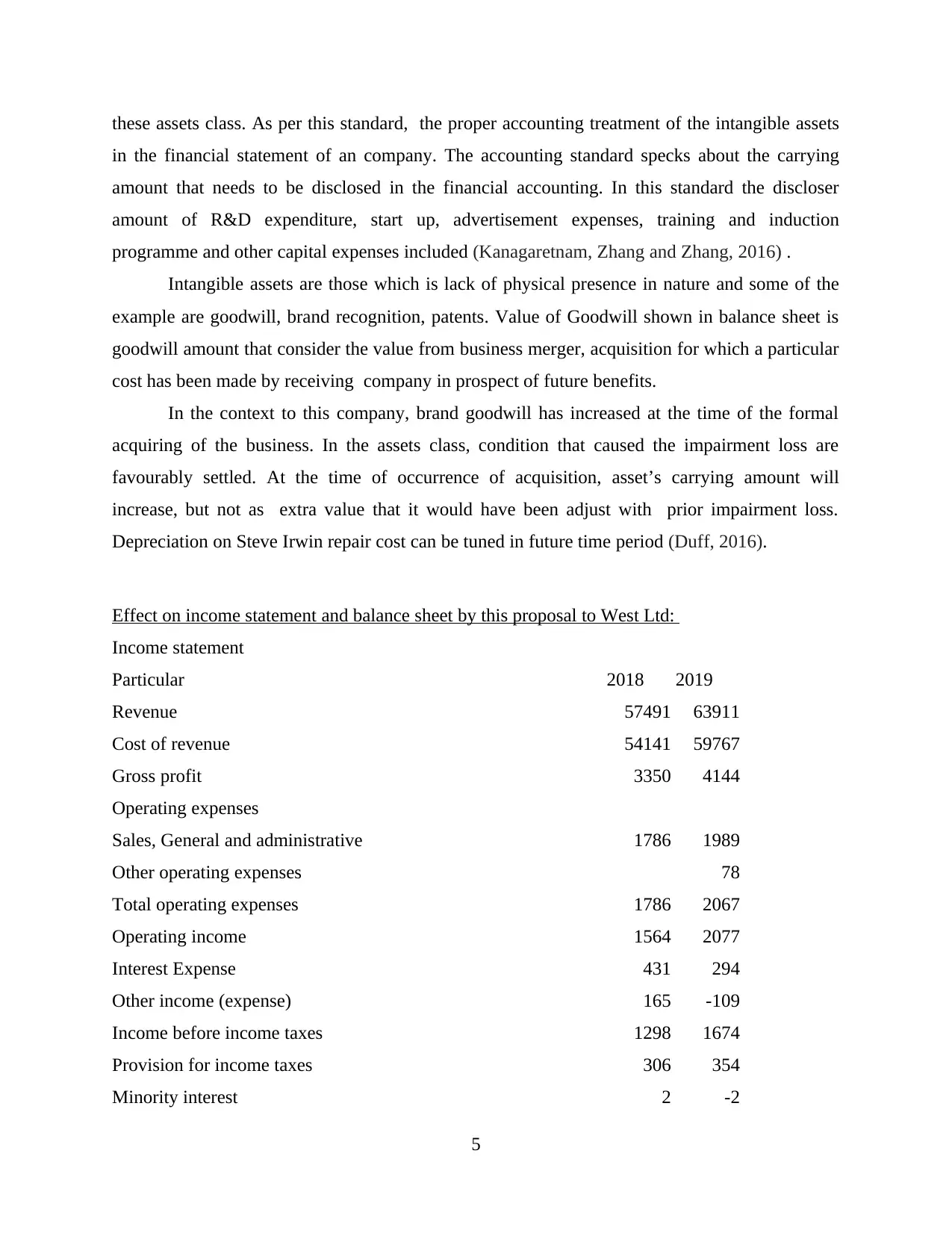

Effect on income statement and balance sheet by this proposal to West Ltd:

Income statement

Particular 2018 2019

Revenue 57491 63911

Cost of revenue 54141 59767

Gross profit 3350 4144

Operating expenses

Sales, General and administrative 1786 1989

Other operating expenses 78

Total operating expenses 1786 2067

Operating income 1564 2077

Interest Expense 431 294

Other income (expense) 165 -109

Income before income taxes 1298 1674

Provision for income taxes 306 354

Minority interest 2 -2

5

in the financial statement of an company. The accounting standard specks about the carrying

amount that needs to be disclosed in the financial accounting. In this standard the discloser

amount of R&D expenditure, start up, advertisement expenses, training and induction

programme and other capital expenses included (Kanagaretnam, Zhang and Zhang, 2016) .

Intangible assets are those which is lack of physical presence in nature and some of the

example are goodwill, brand recognition, patents. Value of Goodwill shown in balance sheet is

goodwill amount that consider the value from business merger, acquisition for which a particular

cost has been made by receiving company in prospect of future benefits.

In the context to this company, brand goodwill has increased at the time of the formal

acquiring of the business. In the assets class, condition that caused the impairment loss are

favourably settled. At the time of occurrence of acquisition, asset’s carrying amount will

increase, but not as extra value that it would have been adjust with prior impairment loss.

Depreciation on Steve Irwin repair cost can be tuned in future time period (Duff, 2016).

Effect on income statement and balance sheet by this proposal to West Ltd:

Income statement

Particular 2018 2019

Revenue 57491 63911

Cost of revenue 54141 59767

Gross profit 3350 4144

Operating expenses

Sales, General and administrative 1786 1989

Other operating expenses 78

Total operating expenses 1786 2067

Operating income 1564 2077

Interest Expense 431 294

Other income (expense) 165 -109

Income before income taxes 1298 1674

Provision for income taxes 306 354

Minority interest 2 -2

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Other income 2 -2

Net income from continuing operations 992 1320

Net income from discontinuing ops 216

Other -2 2

Net income 1206 1322

Balance sheet:

Particular 2018 2019

Assets

Current assets

Cash

Cash and cash equivalents 3282 2916

Short-term investments 1097 457

Total cash 4379 3373

Inventories 2263 2617

Prepaid expenses

Other current assets 7084 6678

Total current assets 13726 12668

Non-current assets

Property, plant and equipment

Fixtures and equipment 10909 7063

Other properties 23453 24949

Property and equipment, at cost 34362 32012

Accumulated Depreciation -15841 -12989

Property, plant and equipment, net 18521 19023

Goodwill 1796 4909

Intangible assets 865 1355

Deferred income taxes 117 132

Other long-term assets 9837 10960

6

Net income from continuing operations 992 1320

Net income from discontinuing ops 216

Other -2 2

Net income 1206 1322

Balance sheet:

Particular 2018 2019

Assets

Current assets

Cash

Cash and cash equivalents 3282 2916

Short-term investments 1097 457

Total cash 4379 3373

Inventories 2263 2617

Prepaid expenses

Other current assets 7084 6678

Total current assets 13726 12668

Non-current assets

Property, plant and equipment

Fixtures and equipment 10909 7063

Other properties 23453 24949

Property and equipment, at cost 34362 32012

Accumulated Depreciation -15841 -12989

Property, plant and equipment, net 18521 19023

Goodwill 1796 4909

Intangible assets 865 1355

Deferred income taxes 117 132

Other long-term assets 9837 10960

6

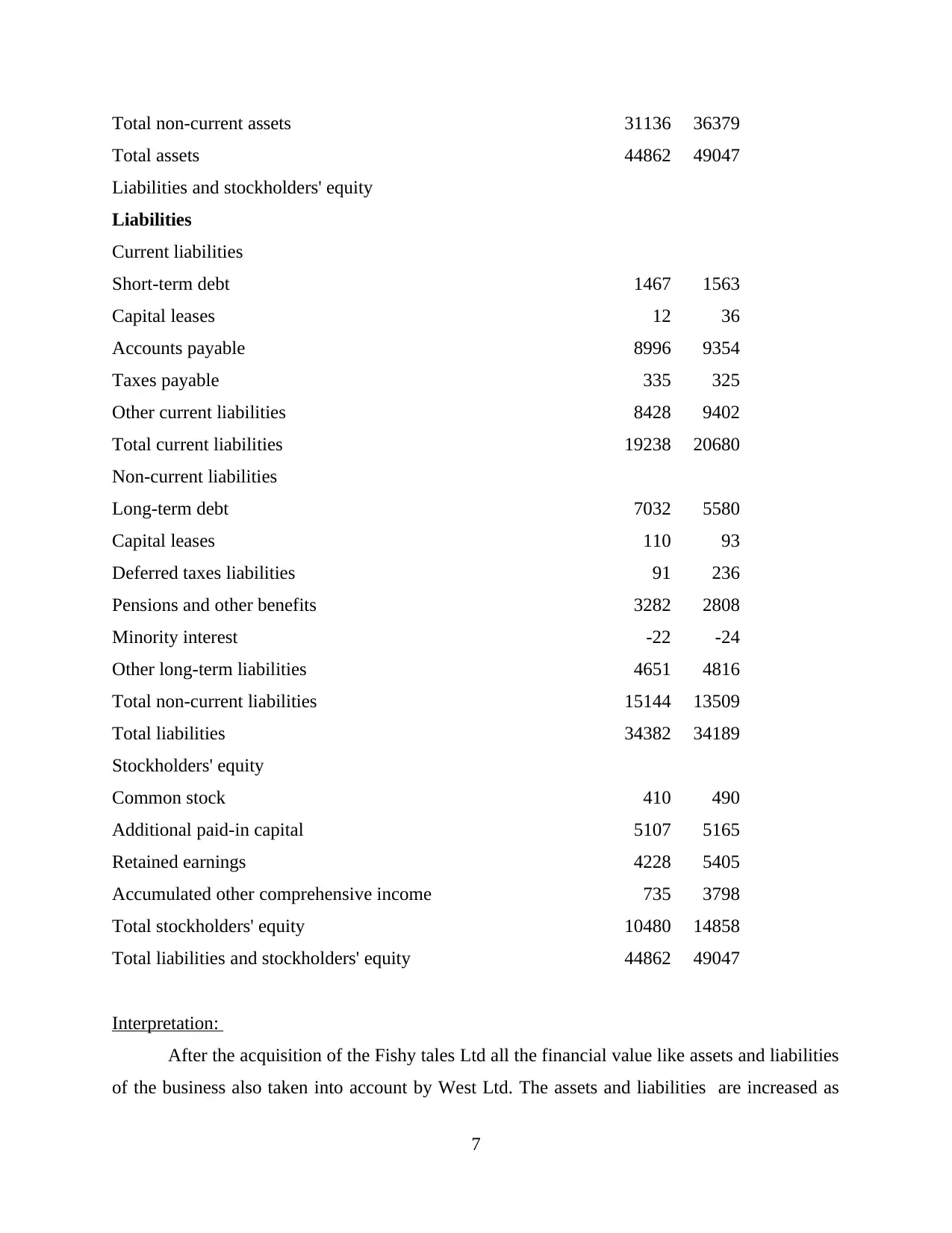

Total non-current assets 31136 36379

Total assets 44862 49047

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 1467 1563

Capital leases 12 36

Accounts payable 8996 9354

Taxes payable 335 325

Other current liabilities 8428 9402

Total current liabilities 19238 20680

Non-current liabilities

Long-term debt 7032 5580

Capital leases 110 93

Deferred taxes liabilities 91 236

Pensions and other benefits 3282 2808

Minority interest -22 -24

Other long-term liabilities 4651 4816

Total non-current liabilities 15144 13509

Total liabilities 34382 34189

Stockholders' equity

Common stock 410 490

Additional paid-in capital 5107 5165

Retained earnings 4228 5405

Accumulated other comprehensive income 735 3798

Total stockholders' equity 10480 14858

Total liabilities and stockholders' equity 44862 49047

Interpretation:

After the acquisition of the Fishy tales Ltd all the financial value like assets and liabilities

of the business also taken into account by West Ltd. The assets and liabilities are increased as

7

Total assets 44862 49047

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 1467 1563

Capital leases 12 36

Accounts payable 8996 9354

Taxes payable 335 325

Other current liabilities 8428 9402

Total current liabilities 19238 20680

Non-current liabilities

Long-term debt 7032 5580

Capital leases 110 93

Deferred taxes liabilities 91 236

Pensions and other benefits 3282 2808

Minority interest -22 -24

Other long-term liabilities 4651 4816

Total non-current liabilities 15144 13509

Total liabilities 34382 34189

Stockholders' equity

Common stock 410 490

Additional paid-in capital 5107 5165

Retained earnings 4228 5405

Accumulated other comprehensive income 735 3798

Total stockholders' equity 10480 14858

Total liabilities and stockholders' equity 44862 49047

Interpretation:

After the acquisition of the Fishy tales Ltd all the financial value like assets and liabilities

of the business also taken into account by West Ltd. The assets and liabilities are increased as

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

compare to last year. And operating cost also increased in the income statement. In balance sheet

the amount of the goodwill is increased to 4909.

RECOMMENDATION

As per the above discussed case study of west Ltd, it is suggested to the company to

adopt the process estimation of the impairment cost by considering the accounting standard. The

process is talks about the capital expenditure and goodwill of firm that may be increased the

value of organisation. So the assertion of the marketing manager is little bit wrong. As by using

the services of acquisition company its brands value increased and there are certain increment in

the profit and financial condition also. And company’s net position will increase which is

asserted by the marketing manager. There are effect on the statement of profit or loss which goes

wrong as comprehensive profit also increased. To avoid complexness in accounting activity it is

informed West Ltd to properly adjust the benefit of impairment of Steve Irwin by considering

Accounting Standard 136 and AAS 138. so this proposal should be accounted as it affect the

income statement and balance sheet of the West Ltd.

CONCLUSION

As per the above study report, it is concluded that marketing manager should be consider

the compliance of accounting process to avoid any complexness in financial accounting. Before

making the financial decision in the business he needs to be address the financial changes in

income statement and balance sheet such as profit and goodwill to better the decision making

process. Financial transparency can be established in the statement and report by following the

guidelines of the accounting standards that may help in the make the trust in financial structure

of the company by external user.

8

the amount of the goodwill is increased to 4909.

RECOMMENDATION

As per the above discussed case study of west Ltd, it is suggested to the company to

adopt the process estimation of the impairment cost by considering the accounting standard. The

process is talks about the capital expenditure and goodwill of firm that may be increased the

value of organisation. So the assertion of the marketing manager is little bit wrong. As by using

the services of acquisition company its brands value increased and there are certain increment in

the profit and financial condition also. And company’s net position will increase which is

asserted by the marketing manager. There are effect on the statement of profit or loss which goes

wrong as comprehensive profit also increased. To avoid complexness in accounting activity it is

informed West Ltd to properly adjust the benefit of impairment of Steve Irwin by considering

Accounting Standard 136 and AAS 138. so this proposal should be accounted as it affect the

income statement and balance sheet of the West Ltd.

CONCLUSION

As per the above study report, it is concluded that marketing manager should be consider

the compliance of accounting process to avoid any complexness in financial accounting. Before

making the financial decision in the business he needs to be address the financial changes in

income statement and balance sheet such as profit and goodwill to better the decision making

process. Financial transparency can be established in the statement and report by following the

guidelines of the accounting standards that may help in the make the trust in financial structure

of the company by external user.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journal:

Chen, L. and et.al, 2016. Audited financial reporting and voluntary disclosure of corporate social

responsibility (CSR) reports. Journal of Management Accounting Research. 28(2).

pp.53-76.

Al-Shaer, H., Salama, A. and Toms, S., 2017. Audit committees and financial reporting quality:

Evidence from UK environmental accounting disclosures. Journal of Applied

Accounting Research. 18(1). pp.2-21.

Brusca, I. and Martínez, J. C., 2016. Adopting International Public Sector Accounting Standards:

a challenge for modernizing and harmonizing public sector accounting. International

Review of Administrative Sciences. 82(4). pp.724-744.

Gimbar, C., Hansen, B. and Ozlanski, M. E., 2016. The effects of critical audit matter paragraphs

and accounting standard precision on auditor liability. The Accounting Review. 91(6).

pp.1629-1646.

Hoitash, R. and Hoitash, U., 2017. Measuring accounting reporting complexity with XBRL. The

Accounting Review. 93(1). pp.259-287.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E., 2018. Financial and Managerial Accounting,

Loose-leaf Print Companion. John Wiley & Sons.

Kanagaretnam, K., Zhang, G. and Zhang, S. B., 2016. CDS pricing and accounting disclosures:

Evidence from US bank holding corporations around the recent financial crisis. Journal

of Financial Stability. 22. pp.33-44.

Duff, A., 2016. Corporate social responsibility reporting in professional accounting firms. The

British Accounting Review. 48(1). pp.74-86.

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Brown, J., Dillard, J., Hopper, T., Atkins, J., Atkins, B.C., Thomson, I. and Maroun, W., 2015.

“Good” news from nowhere: imagining utopian sustainable accounting. Accounting,

Auditing & Accountability Journal.

Edwards, J. R. ed., 2014. Twentieth Century Accounting Thinkers (RLE Accounting). Routledge.

Gabrusewicz, T., 2013. Sustainability accounting–definition and trends. Prace Naukowe

Uniwersytetu Ekonomicznego we Wrocławiu, (302), pp.37-46.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control

research. Journal of Management Control. 24(3). pp.223-240.

Jackson, M. and Cossitt, B., 2015. Is intelligent online tutoring software useful in refreshing

financial accounting knowledge?. In Advances in Accounting Education: Teaching and

Curriculum Innovations (pp. 1-19). Emerald Group Publishing Limited.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Maheshwari, S.N., Maheshwari, S.K. and Maheshwari, S.K., 2013. Financial Accounting, 6e.

Vikas Publishing House.

McEnroe, J. E. and Sullivan, M., 2013. An examination of the perceptions of auditors and chief

financial officers regarding principles versus rules based accounting

standards. Research in Accounting Regulation. 25(2). pp.196-207.

Sunder, S., 2016. Better financial reporting: Meanings and means. Journal of Accounting and

Public Policy. 35(3). pp.211-223.

9

Books and Journal:

Chen, L. and et.al, 2016. Audited financial reporting and voluntary disclosure of corporate social

responsibility (CSR) reports. Journal of Management Accounting Research. 28(2).

pp.53-76.

Al-Shaer, H., Salama, A. and Toms, S., 2017. Audit committees and financial reporting quality:

Evidence from UK environmental accounting disclosures. Journal of Applied

Accounting Research. 18(1). pp.2-21.

Brusca, I. and Martínez, J. C., 2016. Adopting International Public Sector Accounting Standards:

a challenge for modernizing and harmonizing public sector accounting. International

Review of Administrative Sciences. 82(4). pp.724-744.

Gimbar, C., Hansen, B. and Ozlanski, M. E., 2016. The effects of critical audit matter paragraphs

and accounting standard precision on auditor liability. The Accounting Review. 91(6).

pp.1629-1646.

Hoitash, R. and Hoitash, U., 2017. Measuring accounting reporting complexity with XBRL. The

Accounting Review. 93(1). pp.259-287.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E., 2018. Financial and Managerial Accounting,

Loose-leaf Print Companion. John Wiley & Sons.

Kanagaretnam, K., Zhang, G. and Zhang, S. B., 2016. CDS pricing and accounting disclosures:

Evidence from US bank holding corporations around the recent financial crisis. Journal

of Financial Stability. 22. pp.33-44.

Duff, A., 2016. Corporate social responsibility reporting in professional accounting firms. The

British Accounting Review. 48(1). pp.74-86.

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Brown, J., Dillard, J., Hopper, T., Atkins, J., Atkins, B.C., Thomson, I. and Maroun, W., 2015.

“Good” news from nowhere: imagining utopian sustainable accounting. Accounting,

Auditing & Accountability Journal.

Edwards, J. R. ed., 2014. Twentieth Century Accounting Thinkers (RLE Accounting). Routledge.

Gabrusewicz, T., 2013. Sustainability accounting–definition and trends. Prace Naukowe

Uniwersytetu Ekonomicznego we Wrocławiu, (302), pp.37-46.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control

research. Journal of Management Control. 24(3). pp.223-240.

Jackson, M. and Cossitt, B., 2015. Is intelligent online tutoring software useful in refreshing

financial accounting knowledge?. In Advances in Accounting Education: Teaching and

Curriculum Innovations (pp. 1-19). Emerald Group Publishing Limited.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Maheshwari, S.N., Maheshwari, S.K. and Maheshwari, S.K., 2013. Financial Accounting, 6e.

Vikas Publishing House.

McEnroe, J. E. and Sullivan, M., 2013. An examination of the perceptions of auditors and chief

financial officers regarding principles versus rules based accounting

standards. Research in Accounting Regulation. 25(2). pp.196-207.

Sunder, S., 2016. Better financial reporting: Meanings and means. Journal of Accounting and

Public Policy. 35(3). pp.211-223.

9

Trotman, K. and Carson, E., 2018. Financial accounting: an integrated approach. Cengage AU.

Zied, B. and Mohamed, T., 2013. The impact of the characteristics of the board of directors on

the financial performance of Tunisian companies. International Journal of Managerial

and Financial Accounting. 5(2). pp.178-201.

10

Zied, B. and Mohamed, T., 2013. The impact of the characteristics of the board of directors on

the financial performance of Tunisian companies. International Journal of Managerial

and Financial Accounting. 5(2). pp.178-201.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.