Advanced Accounting Issues: Airline Lease Agreements of Australia

VerifiedAdded on 2023/01/23

|11

|2600

|65

Case Study

AI Summary

This case study delves into the intricacies of lease agreements within the Australian airline industry, specifically analyzing the financial reporting of Qantas Airlines Limited and Virgin Australia Holdings Limited. It explores the impact of lease arrangements, differentiating between operating and financial leases and their respective treatments in financial statements. The study examines the implications of proposed changes to accounting standards by the IASB, particularly the elimination of operating lease classification and its effect on debt-to-asset ratios and return on assets. It provides an overview of both airlines, their lease financing practices, and the impact of short-term and long-term leases. The analysis concludes with the significance of lease agreements in the financial performance of the companies and the broader implications for accounting policies, providing a comprehensive understanding of lease accounting within the airline industry.

Running head: ADVANCED ISSUE IN ACCOUNTING

Advanced issue in Accounting

Name of the Student

Name of the University

Author’s note

Advanced issue in Accounting

Name of the Student

Name of the University

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCED ISSUE IN ACCOUNTING

Executive summary:

This case study deals with the understanding of the lease agreement and the impact of

it in the current financial report of airlines industry. The study also deals with the detailed

demonstration of both operating and financial leases. Apart from this the reports are also

helpful in considering the lease valuation of the financial report which determines the current

performance of both the companies. Lastly the impact of the accounting rules for leases

which have a bug impact on the accounting impacts on Qantas Airlines Limited and Virgin

Australia Holdings Limited.

ADVANCED ISSUE IN ACCOUNTING

Executive summary:

This case study deals with the understanding of the lease agreement and the impact of

it in the current financial report of airlines industry. The study also deals with the detailed

demonstration of both operating and financial leases. Apart from this the reports are also

helpful in considering the lease valuation of the financial report which determines the current

performance of both the companies. Lastly the impact of the accounting rules for leases

which have a bug impact on the accounting impacts on Qantas Airlines Limited and Virgin

Australia Holdings Limited.

2

ADVANCED ISSUE IN ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................3

Impact of lease arrangement in the financial report:..............................................................3

Impact of the financial report:................................................................................................4

Operating versus financial lease:...........................................................................................5

Overview of Qantas Airways Limited:..................................................................................5

Overview of virgin Australia holdings limited:.....................................................................6

Impact of accounting rules for leases:....................................................................................6

Impact of the short and long term lease:....................................................................................7

Long term lease:.....................................................................................................................7

Short term leases:...................................................................................................................8

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

ADVANCED ISSUE IN ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................3

Impact of lease arrangement in the financial report:..............................................................3

Impact of the financial report:................................................................................................4

Operating versus financial lease:...........................................................................................5

Overview of Qantas Airways Limited:..................................................................................5

Overview of virgin Australia holdings limited:.....................................................................6

Impact of accounting rules for leases:....................................................................................6

Impact of the short and long term lease:....................................................................................7

Long term lease:.....................................................................................................................7

Short term leases:...................................................................................................................8

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCED ISSUE IN ACCOUNTING

Introduction:

The above case study deals with the understanding of the lease accounting policy and

procedures which have been implemented by two of the largest airlines company of Australia

namely Qantas Airlines Limited and Virgin Australia Holdings Limited. The study also deals

with the argument which the chairperson of IASB who have stated that the current accounting

and leasing policy does not match the economic standards and how the off balance sheet

lease liability is better than the debt valuation if the balance sheet followed by the annual

report of both the companies. The study is also supported with a suitable conclusion relating

to the report.

Discussion:

Impact of lease arrangement in the financial report:

The international accounting standard board are preparing to make changes in the

accounting standards for financial statements of Qantas airlines limited and Virgin Australia

Holdings limited. Hence the proposed standard will eliminate the operating lease

classification and it will be required to pay highest amount of debt to asset ratio and return on

assets for many companies. Hence it is important that the users of the financial statements

understands the changes and effects they could implement. This study also estimates the

impact of changes in the company financial assets. However the current leasing standards and

issues can be classified under operating and financial lease. Under the operational lease, the

lease payment had been reported as the rental expense and no asset and liability has been

used in the financial statement. Hence the lesser of capital leasing transaction derecognizes

the leasing assets which represent both the leasing payments and expected residual value and

the revenue of income statement of both Qantas Airlines Limited and Virgin Australia

Holdings Limited. However a number of concerns have been raised about the leasing

ADVANCED ISSUE IN ACCOUNTING

Introduction:

The above case study deals with the understanding of the lease accounting policy and

procedures which have been implemented by two of the largest airlines company of Australia

namely Qantas Airlines Limited and Virgin Australia Holdings Limited. The study also deals

with the argument which the chairperson of IASB who have stated that the current accounting

and leasing policy does not match the economic standards and how the off balance sheet

lease liability is better than the debt valuation if the balance sheet followed by the annual

report of both the companies. The study is also supported with a suitable conclusion relating

to the report.

Discussion:

Impact of lease arrangement in the financial report:

The international accounting standard board are preparing to make changes in the

accounting standards for financial statements of Qantas airlines limited and Virgin Australia

Holdings limited. Hence the proposed standard will eliminate the operating lease

classification and it will be required to pay highest amount of debt to asset ratio and return on

assets for many companies. Hence it is important that the users of the financial statements

understands the changes and effects they could implement. This study also estimates the

impact of changes in the company financial assets. However the current leasing standards and

issues can be classified under operating and financial lease. Under the operational lease, the

lease payment had been reported as the rental expense and no asset and liability has been

used in the financial statement. Hence the lesser of capital leasing transaction derecognizes

the leasing assets which represent both the leasing payments and expected residual value and

the revenue of income statement of both Qantas Airlines Limited and Virgin Australia

Holdings Limited. However a number of concerns have been raised about the leasing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCED ISSUE IN ACCOUNTING

standards particularly by the operating lease. Hence the classifications are criticized on the

grounds of operating leases and all the rights and obligations related to the work.

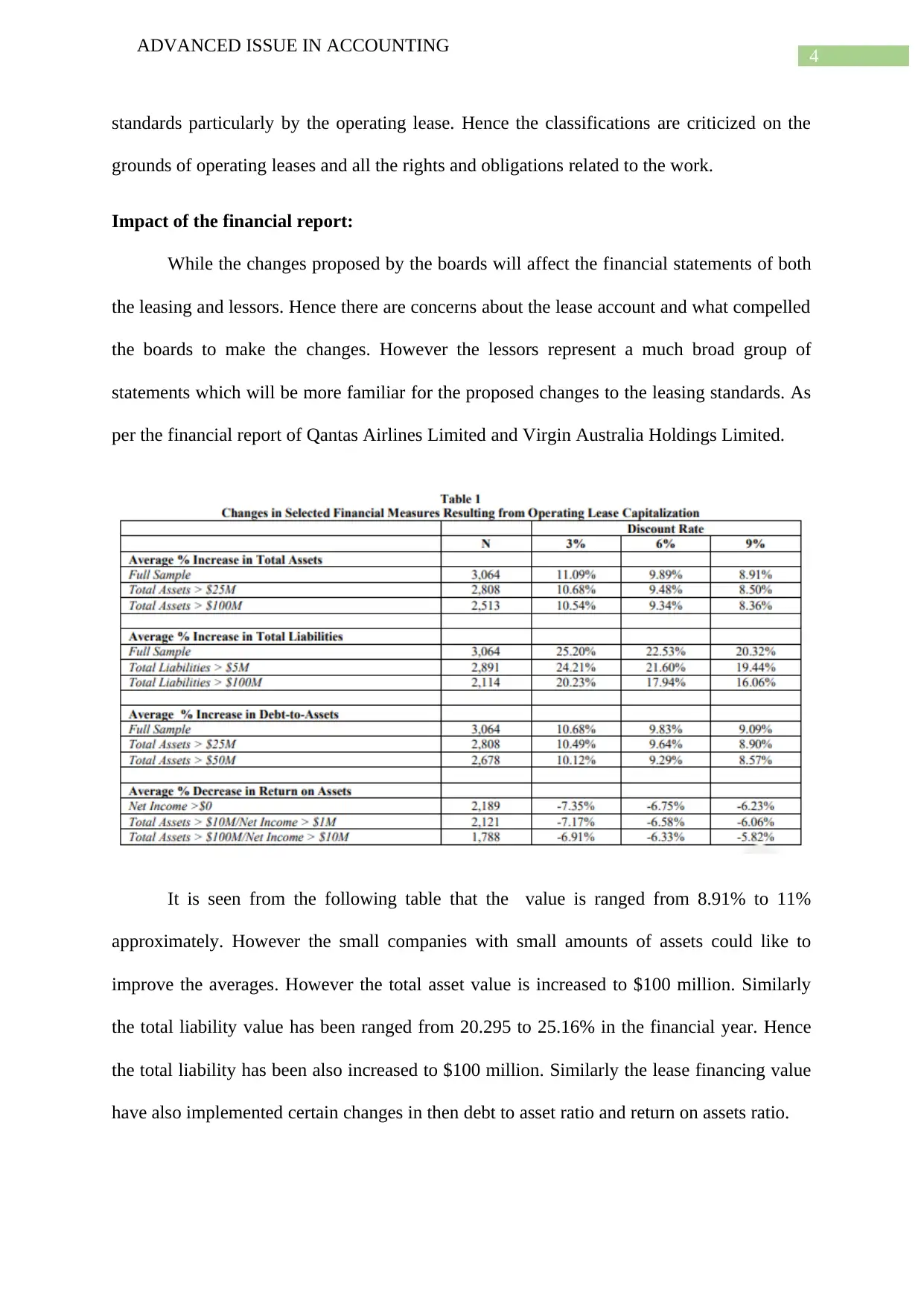

Impact of the financial report:

While the changes proposed by the boards will affect the financial statements of both

the leasing and lessors. Hence there are concerns about the lease account and what compelled

the boards to make the changes. However the lessors represent a much broad group of

statements which will be more familiar for the proposed changes to the leasing standards. As

per the financial report of Qantas Airlines Limited and Virgin Australia Holdings Limited.

It is seen from the following table that the value is ranged from 8.91% to 11%

approximately. However the small companies with small amounts of assets could like to

improve the averages. However the total asset value is increased to $100 million. Similarly

the total liability value has been ranged from 20.295 to 25.16% in the financial year. Hence

the total liability has been also increased to $100 million. Similarly the lease financing value

have also implemented certain changes in then debt to asset ratio and return on assets ratio.

ADVANCED ISSUE IN ACCOUNTING

standards particularly by the operating lease. Hence the classifications are criticized on the

grounds of operating leases and all the rights and obligations related to the work.

Impact of the financial report:

While the changes proposed by the boards will affect the financial statements of both

the leasing and lessors. Hence there are concerns about the lease account and what compelled

the boards to make the changes. However the lessors represent a much broad group of

statements which will be more familiar for the proposed changes to the leasing standards. As

per the financial report of Qantas Airlines Limited and Virgin Australia Holdings Limited.

It is seen from the following table that the value is ranged from 8.91% to 11%

approximately. However the small companies with small amounts of assets could like to

improve the averages. However the total asset value is increased to $100 million. Similarly

the total liability value has been ranged from 20.295 to 25.16% in the financial year. Hence

the total liability has been also increased to $100 million. Similarly the lease financing value

have also implemented certain changes in then debt to asset ratio and return on assets ratio.

5

ADVANCED ISSUE IN ACCOUNTING

Operating versus financial lease:

1. Operating lease is relates to the assets ownership with the lessor for the leased assets.

It is returned by the lessee after using it for lease from agreed upon. Whereas in the

financial lease the risk and reward related to the assets and leased which are

transferred to the lessee (xu et al., 2017).

2. The ownership of the asset remains with the lessor for the entire lease period whereas

in case of financial lease the lease period is there with the lessee. Hence the title might

or might not be transferred eventually.

Overview of Qantas Airways Limited:

This company had been founded in the year 1920 and happens to be one of the largest

airlines services provides of Australia. Registered as the Queensland and Northern Areal

Service (QANTAS). They are widely regarded as the world’s leading long distance airline

and of the big brands of Australia. They have also built up a reputation for excellence in

safety, operational reliability, engineering and many customer services. However the main

business of this group has been laid behind the transportation of the customers by using of

two brands namely Qantas and Jet star. Apart from the company also provide the service like

Q catering. Else the company also operate the regional, domestic and international services to

the customers. However the group’s broad subsidiary business ranges from Qantas freight

enterprises to the Qantas frequent flyer. The company had also employed over 30000 people

worldwide and 93% of the service has been based within Australia. However the company

management have also stated the current lease financing policy which includes the lease of

the airport, lease of the flights and the other expenses (Sieverding, 2018). Hence from the

company annual report for the year 2018 it is seen that out of various expenses the company

have also included the lease financing value in the net cash flow. Hence it is seen the net cash

flow after excluding the aircraft operation from the lease financing has been increased to

ADVANCED ISSUE IN ACCOUNTING

Operating versus financial lease:

1. Operating lease is relates to the assets ownership with the lessor for the leased assets.

It is returned by the lessee after using it for lease from agreed upon. Whereas in the

financial lease the risk and reward related to the assets and leased which are

transferred to the lessee (xu et al., 2017).

2. The ownership of the asset remains with the lessor for the entire lease period whereas

in case of financial lease the lease period is there with the lessee. Hence the title might

or might not be transferred eventually.

Overview of Qantas Airways Limited:

This company had been founded in the year 1920 and happens to be one of the largest

airlines services provides of Australia. Registered as the Queensland and Northern Areal

Service (QANTAS). They are widely regarded as the world’s leading long distance airline

and of the big brands of Australia. They have also built up a reputation for excellence in

safety, operational reliability, engineering and many customer services. However the main

business of this group has been laid behind the transportation of the customers by using of

two brands namely Qantas and Jet star. Apart from the company also provide the service like

Q catering. Else the company also operate the regional, domestic and international services to

the customers. However the group’s broad subsidiary business ranges from Qantas freight

enterprises to the Qantas frequent flyer. The company had also employed over 30000 people

worldwide and 93% of the service has been based within Australia. However the company

management have also stated the current lease financing policy which includes the lease of

the airport, lease of the flights and the other expenses (Sieverding, 2018). Hence from the

company annual report for the year 2018 it is seen that out of various expenses the company

have also included the lease financing value in the net cash flow. Hence it is seen the net cash

flow after excluding the aircraft operation from the lease financing has been increased to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ADVANCED ISSUE IN ACCOUNTING

$1442million dollar which is the most than rest of the other cases. However the lease value

had been increased due to the increase in number of domestic and international flights.

However the net debt have also been decreased during the financial year 2018 to 4903

million (Jung et al.,2018).

Overview of virgin Australia holdings limited:

Virgin Australia holdings limited is an organization which engages in the operation of

domestic and international airlines business in Australia. However the company operates

through the virgin Australia domestic, virgin Australia international, velocity and Tigerair

Australia segments. Hence its aircraft files to the domestic destinations including the regional

network charter and cargo services. However the company operates in the fleet primarily

includes the Boeing B737 and B777. This company is considered as the second largest

airlines service provider after Qantas. This company had also gained much in the year 2018

in lease financing of the aircraft which is valued at $563 million and it had surely increased

than that of 2017. Hence the business of the company had also increased in the financial year.

This is the reason that both the companies had been able to improve lease financing.

Impact of accounting rules for leases:

The lease accounting standard will dramatically change the financial reporting of

nearly all business including the Qantas Airlines Limited and Virgin Australia Holdings

Limited. Hence the impact will be on the significant for private equity firms which utilize the

financial statements metrics to evaluate the portfolio of the company investments. Hence the

key performance ratio such as the such as the return on capital and leverage ratios will change

the company valuations of Qantas and Virgin in addition to the assets and liabilities value of

the company balance sheet. Hence the changes could also trigger debt- covenant valuation

which leads the creditors to recheck the investments more closely. However the biggest

changes will be on how the leases are recognized on the company balance sheet. Hence it is

ADVANCED ISSUE IN ACCOUNTING

$1442million dollar which is the most than rest of the other cases. However the lease value

had been increased due to the increase in number of domestic and international flights.

However the net debt have also been decreased during the financial year 2018 to 4903

million (Jung et al.,2018).

Overview of virgin Australia holdings limited:

Virgin Australia holdings limited is an organization which engages in the operation of

domestic and international airlines business in Australia. However the company operates

through the virgin Australia domestic, virgin Australia international, velocity and Tigerair

Australia segments. Hence its aircraft files to the domestic destinations including the regional

network charter and cargo services. However the company operates in the fleet primarily

includes the Boeing B737 and B777. This company is considered as the second largest

airlines service provider after Qantas. This company had also gained much in the year 2018

in lease financing of the aircraft which is valued at $563 million and it had surely increased

than that of 2017. Hence the business of the company had also increased in the financial year.

This is the reason that both the companies had been able to improve lease financing.

Impact of accounting rules for leases:

The lease accounting standard will dramatically change the financial reporting of

nearly all business including the Qantas Airlines Limited and Virgin Australia Holdings

Limited. Hence the impact will be on the significant for private equity firms which utilize the

financial statements metrics to evaluate the portfolio of the company investments. Hence the

key performance ratio such as the such as the return on capital and leverage ratios will change

the company valuations of Qantas and Virgin in addition to the assets and liabilities value of

the company balance sheet. Hence the changes could also trigger debt- covenant valuation

which leads the creditors to recheck the investments more closely. However the biggest

changes will be on how the leases are recognized on the company balance sheet. Hence it is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCED ISSUE IN ACCOUNTING

important for the lese and the lessor to clarify the lease on the onset as either an operating and

financial lease which vary slightly. However substantially the long term operating leases

could have a right to use assets and a lease liability on the balance sheet of the airlines

company and record a straight line expense on the income statements of the company

(Joubert et al.,2017). Hence the financial leases will also recognize a right of use assets and a

lease liability which will recognize the amortization of the assets and liability interest

(Hughes and Hoy 2013).

1. The airlines could get the clarity on the current systems and resources to establish a

team and guide the transition.

2. They could use some additional resources as a team and collect valid information out

of it (Giner et al.,2018).

3. After the implementation has started and the compliance gap is filled the financial

instruments to be understood and new procedures are to be started.

Impact of the short and long term lease:

As per the report it is seen that the industrial and commercial listed in the airlines

industry were selected to examine the impact of the lease capitalization on the company

financial statements. Hence the study adopted the lease capitalization and suggested an

increase in the lease assets and lease liabilities of approximately 6% and 395 respectively.

Therefore the study also decrease in the mean of economy which replicated the study of

financial statements of the airlines company (Dakis,2016). Hence the short and long term

impact of the lease financing are as follows-

Long term lease:

1. Stability: long term lease provide the income sustainability and ongoing guaranteed

tenann (Berk et al.,2013).

ADVANCED ISSUE IN ACCOUNTING

important for the lese and the lessor to clarify the lease on the onset as either an operating and

financial lease which vary slightly. However substantially the long term operating leases

could have a right to use assets and a lease liability on the balance sheet of the airlines

company and record a straight line expense on the income statements of the company

(Joubert et al.,2017). Hence the financial leases will also recognize a right of use assets and a

lease liability which will recognize the amortization of the assets and liability interest

(Hughes and Hoy 2013).

1. The airlines could get the clarity on the current systems and resources to establish a

team and guide the transition.

2. They could use some additional resources as a team and collect valid information out

of it (Giner et al.,2018).

3. After the implementation has started and the compliance gap is filled the financial

instruments to be understood and new procedures are to be started.

Impact of the short and long term lease:

As per the report it is seen that the industrial and commercial listed in the airlines

industry were selected to examine the impact of the lease capitalization on the company

financial statements. Hence the study adopted the lease capitalization and suggested an

increase in the lease assets and lease liabilities of approximately 6% and 395 respectively.

Therefore the study also decrease in the mean of economy which replicated the study of

financial statements of the airlines company (Dakis,2016). Hence the short and long term

impact of the lease financing are as follows-

Long term lease:

1. Stability: long term lease provide the income sustainability and ongoing guaranteed

tenann (Berk et al.,2013).

8

ADVANCED ISSUE IN ACCOUNTING

Certainty: A long term lease allows the owner to calculate the return on investment lease

period which allows the long run commercial properties are valued and sold based on the

return in investment. Hence in case if the airlines industry if the supply is outstrips the

demand, then the premises will remain vacant(Ali et al.,2013).

Short term leases:

Flexibility: These kind of leasing are very much flexible for tenant selection. If the property

is in a high demand and the demand is more than supply then the lease value is increased.

However if the market performs well then there is an opportunity to increase the rent and as

well as the subsequent lease (Aruppala, 2013).

Conclusion:

Hence it can be concluded from the above study is that the lease agreement has been

considered as an important factor for both Qantas airways limited and Virgin Australia

Holdings Limited. Hence this company have done a good amount of business in the financial

year 2018. However the lease agreement has fulfilled all the requirements in the company

and they have made well amount of business altogether. However the short and long term

lease policy has also made a good amount of business in the financial year. Thus all these

policies had a good amount of impact on the company accounting policy which was stated by

the chairperson of the IASB in his report determining the impact of lease policy.

ADVANCED ISSUE IN ACCOUNTING

Certainty: A long term lease allows the owner to calculate the return on investment lease

period which allows the long run commercial properties are valued and sold based on the

return in investment. Hence in case if the airlines industry if the supply is outstrips the

demand, then the premises will remain vacant(Ali et al.,2013).

Short term leases:

Flexibility: These kind of leasing are very much flexible for tenant selection. If the property

is in a high demand and the demand is more than supply then the lease value is increased.

However if the market performs well then there is an opportunity to increase the rent and as

well as the subsequent lease (Aruppala, 2013).

Conclusion:

Hence it can be concluded from the above study is that the lease agreement has been

considered as an important factor for both Qantas airways limited and Virgin Australia

Holdings Limited. Hence this company have done a good amount of business in the financial

year 2018. However the lease agreement has fulfilled all the requirements in the company

and they have made well amount of business altogether. However the short and long term

lease policy has also made a good amount of business in the financial year. Thus all these

policies had a good amount of impact on the company accounting policy which was stated by

the chairperson of the IASB in his report determining the impact of lease policy.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ADVANCED ISSUE IN ACCOUNTING

References:

Ali, P., McRae, C. H., Ramsay, I., & Saw, T. (2013).

Aruppala, D. (2013). Lease Accounting Disclosure Practice of Non Bank Financial

Institutions (NBFIs) in Sri Lanka: A Lessor’s Perspective.

Australian Business Law Review, 41(5), 240-269.

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V., & Finch, N. (2013). Fundamentals

of corporate finance. Pearson Higher Education AU.

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V., & Finch, N. (2013). Fundamentals

of corporate finance. Pearson Higher Education AU.

Dakis, G. S. (2016). Upcoming changes to contributions and leasing standards. Governance

Directions, 68(2), 99.

Giner, B., Merello, P., & Pardo, F. (2018). Assessing the impact of operating lease

capitalization with dynamic Monte Carlo simulation. Journal of Business Research.

Hughes, M., & Hoy, S. (2013). Two Steps Backward and One Step Forward: The IASB's

Response to Off-Balance Sheet Financing Through Investments in Other Entities.

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. The

Journal of New Business Ideas & Trends, 15(2), 1-11.

Jung, J., Herbohn, K., & Clarkson, P. (2018). Carbon risk, carbon risk awareness and the cost

of debt financing. Journal of Business Ethics, 150(4), 1151-1171.

ADVANCED ISSUE IN ACCOUNTING

References:

Ali, P., McRae, C. H., Ramsay, I., & Saw, T. (2013).

Aruppala, D. (2013). Lease Accounting Disclosure Practice of Non Bank Financial

Institutions (NBFIs) in Sri Lanka: A Lessor’s Perspective.

Australian Business Law Review, 41(5), 240-269.

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V., & Finch, N. (2013). Fundamentals

of corporate finance. Pearson Higher Education AU.

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V., & Finch, N. (2013). Fundamentals

of corporate finance. Pearson Higher Education AU.

Dakis, G. S. (2016). Upcoming changes to contributions and leasing standards. Governance

Directions, 68(2), 99.

Giner, B., Merello, P., & Pardo, F. (2018). Assessing the impact of operating lease

capitalization with dynamic Monte Carlo simulation. Journal of Business Research.

Hughes, M., & Hoy, S. (2013). Two Steps Backward and One Step Forward: The IASB's

Response to Off-Balance Sheet Financing Through Investments in Other Entities.

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. The

Journal of New Business Ideas & Trends, 15(2), 1-11.

Jung, J., Herbohn, K., & Clarkson, P. (2018). Carbon risk, carbon risk awareness and the cost

of debt financing. Journal of Business Ethics, 150(4), 1151-1171.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCED ISSUE IN ACCOUNTING

Matos, N. B., & Niyama, J. K. (2018). IFRS 16-Leases: desafios, perspectivas e implicações

à luz da essência sobre a forma. Revista de Educação e Pesquisa em Contabilidade

(REPeC), 12(3).

Sieverding, A. (2018). A critical analysis of the accounting for sale and lease back

transactions under the new IFRS 16(Doctoral dissertation).

Wong, J., Wong, N., & Jeter, D. C. (2016). The economics of accounting for property

leases. Accounting Horizons, 30(2), 239-254.

Wong, K., & Joshi, M. (2015). The impact of lease capitalisation on financial statements and

key ratios: Evidence from Australia. Australasian Accounting, Business and Finance

Journal, 9(3), 27-44.

Xu, W., Davidson, R. A., & Cheong, C. S. (2017). Converting financial statements: operating

to capitalised leases. Pacific accounting review, 29(1), 34-54.

ADVANCED ISSUE IN ACCOUNTING

Matos, N. B., & Niyama, J. K. (2018). IFRS 16-Leases: desafios, perspectivas e implicações

à luz da essência sobre a forma. Revista de Educação e Pesquisa em Contabilidade

(REPeC), 12(3).

Sieverding, A. (2018). A critical analysis of the accounting for sale and lease back

transactions under the new IFRS 16(Doctoral dissertation).

Wong, J., Wong, N., & Jeter, D. C. (2016). The economics of accounting for property

leases. Accounting Horizons, 30(2), 239-254.

Wong, K., & Joshi, M. (2015). The impact of lease capitalisation on financial statements and

key ratios: Evidence from Australia. Australasian Accounting, Business and Finance

Journal, 9(3), 27-44.

Xu, W., Davidson, R. A., & Cheong, C. S. (2017). Converting financial statements: operating

to capitalised leases. Pacific accounting review, 29(1), 34-54.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.