Financial Reporting Analysis: Evaluating ROB PLC Financials

VerifiedAdded on 2020/09/08

|11

|3263

|923

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, covering its purpose, regulatory frameworks, and conceptual underpinnings. It examines the benefits for key stakeholders such as investors, creditors, and management, while also exploring the value of financial reporting in meeting a firm's growth objectives. The report includes a detailed analysis of financial statements, ratio interpretations, and a comparison between IAS and IFRS. It also discusses the advantages of IFRS and the degree of its compliance by companies worldwide. The analysis is based on the financial data of ROB PLC, offering insights into the company's performance and financial position. The report emphasizes the importance of financial reporting in making informed decisions and achieving sustainable business success.

FINANCE REPORTING

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.....................................................................................................................................3

1. Outline Purpose of Financial Reporting...............................................................................................3

2. Examine regulatory and conceptual framework...................................................................................3

3. Identification of key stakeholders and their benefits............................................................................4

4. Value of financial reporting for meeting firm’s growth and objective.................................................5

5. Financial Analysis...............................................................................................................................5

6. Interpretation of Financial Statement and ratio....................................................................................7

7. Comparison between IAS and IFRS....................................................................................................9

8. Benefits of IFRS..................................................................................................................................9

9. Degree of IFRS Compliance by company all over the world.............................................................10

CONCLUSION........................................................................................................................................10

REFEENCES...........................................................................................................................................11

2

INTRODUCTION.....................................................................................................................................3

1. Outline Purpose of Financial Reporting...............................................................................................3

2. Examine regulatory and conceptual framework...................................................................................3

3. Identification of key stakeholders and their benefits............................................................................4

4. Value of financial reporting for meeting firm’s growth and objective.................................................5

5. Financial Analysis...............................................................................................................................5

6. Interpretation of Financial Statement and ratio....................................................................................7

7. Comparison between IAS and IFRS....................................................................................................9

8. Benefits of IFRS..................................................................................................................................9

9. Degree of IFRS Compliance by company all over the world.............................................................10

CONCLUSION........................................................................................................................................10

REFEENCES...........................................................................................................................................11

2

INTRODUCTION

Financial Reporting refers to the process of creating statements that reveals financial

status or position of business enterprise to investors, government, stakeholders and management.

These reports are mainly published by organization at the end of accounting or financial year

(Council, 2010). It generally disclose the financial position of a particular company for a

specified time period. It is essential for every enterprise and considered as a main part of

Corporate Governance. For listed companies, it mainly prepared on quarterly & annual basis. It

mainly consist of balance sheet, profit and loss, cash flow, company’s prospectus, management

analysis and discussion. It basically provides information related to company’s growth and

revenue as compared to its competitors. This report is based on ROB PLC. This report also

covers the purpose of financial statement, conceptual and regulatory framework, how

stakeholders get benefit from financial report, benefit of IFRS, analysis of financial performance

and degree of compliance in relation with IFRS.

1. Outline Purpose of Financial Reporting

Financial Reports mainly describes the financial position of the company in terms if

figures. It provides useful information to investors, stakeholders and management. This report

depicts whether the company has yield profit in a year or loss. It also valued their assets and

liabilities. At the end of every year, it is important for business concern to set off their accounts

and figures. They usually prepare profit and loss, cash flow and balance sheet statement. It is

mainly prepared when accounting or financial period or year ends. Following are the purpose of

Financial Reporting:

Providing necessary and useful information to stakeholders, investors and management of

business enterprise that further use is for planning, benchmarking, forecasting, analysis

and decision making.

Providing information to promoters, creditors and debt payer which assist them in

making prudent decision related to credit, investment etc.

Renders information to government bodies, public and shareholders at large that depicts

various aspect of organization in terms of its financial figures.

Provides information related to procurement and utilization of resources.

Delivers information to stakeholders in terms of financial performance of company and

its management as how ethically they are performing its responsibilities and duties.

Provides assistance to auditors by giving them information related to company’s financial

ratios, statement and accounts.

It also provides competitive advantage to company over their rivals in context of its

position in the market place.

Describes how company has arranged its funding for managing its day to day operations

and working capital (Beyer and Cohen and Walther, 2010).

2. Examine regulatory and conceptual framework

It is essential for ever business enterprise to follow and practice guidelines in order to

attain better results or outcome. Accounts manager of firm interpret their financials and numbers

3

Financial Reporting refers to the process of creating statements that reveals financial

status or position of business enterprise to investors, government, stakeholders and management.

These reports are mainly published by organization at the end of accounting or financial year

(Council, 2010). It generally disclose the financial position of a particular company for a

specified time period. It is essential for every enterprise and considered as a main part of

Corporate Governance. For listed companies, it mainly prepared on quarterly & annual basis. It

mainly consist of balance sheet, profit and loss, cash flow, company’s prospectus, management

analysis and discussion. It basically provides information related to company’s growth and

revenue as compared to its competitors. This report is based on ROB PLC. This report also

covers the purpose of financial statement, conceptual and regulatory framework, how

stakeholders get benefit from financial report, benefit of IFRS, analysis of financial performance

and degree of compliance in relation with IFRS.

1. Outline Purpose of Financial Reporting

Financial Reports mainly describes the financial position of the company in terms if

figures. It provides useful information to investors, stakeholders and management. This report

depicts whether the company has yield profit in a year or loss. It also valued their assets and

liabilities. At the end of every year, it is important for business concern to set off their accounts

and figures. They usually prepare profit and loss, cash flow and balance sheet statement. It is

mainly prepared when accounting or financial period or year ends. Following are the purpose of

Financial Reporting:

Providing necessary and useful information to stakeholders, investors and management of

business enterprise that further use is for planning, benchmarking, forecasting, analysis

and decision making.

Providing information to promoters, creditors and debt payer which assist them in

making prudent decision related to credit, investment etc.

Renders information to government bodies, public and shareholders at large that depicts

various aspect of organization in terms of its financial figures.

Provides information related to procurement and utilization of resources.

Delivers information to stakeholders in terms of financial performance of company and

its management as how ethically they are performing its responsibilities and duties.

Provides assistance to auditors by giving them information related to company’s financial

ratios, statement and accounts.

It also provides competitive advantage to company over their rivals in context of its

position in the market place.

Describes how company has arranged its funding for managing its day to day operations

and working capital (Beyer and Cohen and Walther, 2010).

2. Examine regulatory and conceptual framework

It is essential for ever business enterprise to follow and practice guidelines in order to

attain better results or outcome. Accounts manager of firm interpret their financials and numbers

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and draw a conclusion that depicts its performance. Basically it provide presentation, disclosure

and measurement of financial statements in terms of material aspects. It is mainly classified into

two framework:

Conceptual Framework: This framework helps in preparing financial statement or report of the

company that depicts its performance throughout the year in order to accomplish its goals and

objectives (Deegan, 2013). Basically it deals with issues related to financial reporting in terms of

achieving goals, making financial information useful, components of financial statements etc.

Under this framework, information has been gathered for external users regarding the company’s

assets, liabilities, income, equity, expense etc. and the concept for recording it financial

statement.

Benefits

Useful for external users as it provides information related to company’s income,

expense, and profit for a particular accounting year.

Provides guidance and direction at the time of analyzing and reviewing financial

regulation and figures.

Implementing accounting standards at internal level of company.

Regulatory Framework: It deals with regulations and rules prepared by government bodies in

order to record various accounting & financial transaction. Every entry or transaction has been

recorded in its own way. There is defined pattern according to which transactions are being

recorded in the books of accounts. It also involves theories, concepts and principles according to

which entries have been recorded in books. It mainly includes going concern concept, matching

principle. Dual concept etc. Every organization is following this and they record their entries on

the basis of chronological order that includes journal, ledger, subsidiary books, profit and loss

and balance sheet. It eventually help the manager to take strategic decision related to company’s

growth and success.

Benefits

Assist in anticipating future needs related to fund.

Assist in making effective decision concerning firm’s profitability and performance in the

marketplace.

3. Identification of key stakeholders and their benefits

Stakeholder are generally parties, person, authorities and bodies that has specify interest

towards the organization. They are the one who directly or indirectly affects the firm’s

performance, objectives, goals and policies. Some one of the example of stakeholder are

government, investors, directors, suppliers, debtors, shareholders and creditors. They all

contributes in different manner towards accomplishing firm’s goals. Customers are also

considered as an important stakeholder but their contribution is limited to some extent.

Stakeholder basically determines the result or consequence of business decision (Li, 2010). They

can be employees, can be business partner or anyone who possess or holds stake in the company.

Following are the benefits of different stakeholders:

4

and measurement of financial statements in terms of material aspects. It is mainly classified into

two framework:

Conceptual Framework: This framework helps in preparing financial statement or report of the

company that depicts its performance throughout the year in order to accomplish its goals and

objectives (Deegan, 2013). Basically it deals with issues related to financial reporting in terms of

achieving goals, making financial information useful, components of financial statements etc.

Under this framework, information has been gathered for external users regarding the company’s

assets, liabilities, income, equity, expense etc. and the concept for recording it financial

statement.

Benefits

Useful for external users as it provides information related to company’s income,

expense, and profit for a particular accounting year.

Provides guidance and direction at the time of analyzing and reviewing financial

regulation and figures.

Implementing accounting standards at internal level of company.

Regulatory Framework: It deals with regulations and rules prepared by government bodies in

order to record various accounting & financial transaction. Every entry or transaction has been

recorded in its own way. There is defined pattern according to which transactions are being

recorded in the books of accounts. It also involves theories, concepts and principles according to

which entries have been recorded in books. It mainly includes going concern concept, matching

principle. Dual concept etc. Every organization is following this and they record their entries on

the basis of chronological order that includes journal, ledger, subsidiary books, profit and loss

and balance sheet. It eventually help the manager to take strategic decision related to company’s

growth and success.

Benefits

Assist in anticipating future needs related to fund.

Assist in making effective decision concerning firm’s profitability and performance in the

marketplace.

3. Identification of key stakeholders and their benefits

Stakeholder are generally parties, person, authorities and bodies that has specify interest

towards the organization. They are the one who directly or indirectly affects the firm’s

performance, objectives, goals and policies. Some one of the example of stakeholder are

government, investors, directors, suppliers, debtors, shareholders and creditors. They all

contributes in different manner towards accomplishing firm’s goals. Customers are also

considered as an important stakeholder but their contribution is limited to some extent.

Stakeholder basically determines the result or consequence of business decision (Li, 2010). They

can be employees, can be business partner or anyone who possess or holds stake in the company.

Following are the benefits of different stakeholders:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Long-Term Relationship: Stakeholders are essential for performance based and instrumental

reasons. When a company possess long term relationship with its various stakeholders, it

automatically operates more efficiently and holds better chance of generating more profits and

revenues. Long term relationship with stakeholder helps business concern to increase

productivity, creates loyal consumer base, High retention rate of employees and gain the

advantage of word of mouth advertising.

Feedback and Product Development: Stakeholders participate actively in the activities and

operation of company. By providing resources they ensures that they have control on business

operations and functions (Barth and Landsman, 2013). They act as per their wish and provide

effective and valuable feedback.

A sense of community: A sense of greater community and responsibility among various

stakeholders within an organization can positively increase its sales figures and provides shape to

its business development. It can generated via promotion, membership, loyalty program, virtual

services etc.

4. Value of financial reporting for meeting firm’s growth and objective.

The success and growth of every business enterprise whether small or large is depend

upon how well the company has perform in terms of earning profit and revenues during a

specified period of time say accounting or financial year. Thus, it become essential for every

single organization to records its transaction in a significant manner. Companies are required to

record every single transaction as per the given format. For instance, entry related to sales will

first record in journal, then in ledger, then in its subsidiary books and then finally in trading for

measuring or calculating gross profit. For instance, financial statement of referred firm describes

its performance, turnover, profits, and expenses for a particular year. It is advisable for every

firm to prepare this statements as they help in measuring the financial performance of company

over their rivals. Managers with the help of this report can take effective decision related to its

future growth or success (Altamuro and Beatty, 2015). It also enable the firm to identify the need

of funding in order to carry out day to day operation and manage sufficient and effective working

capital.

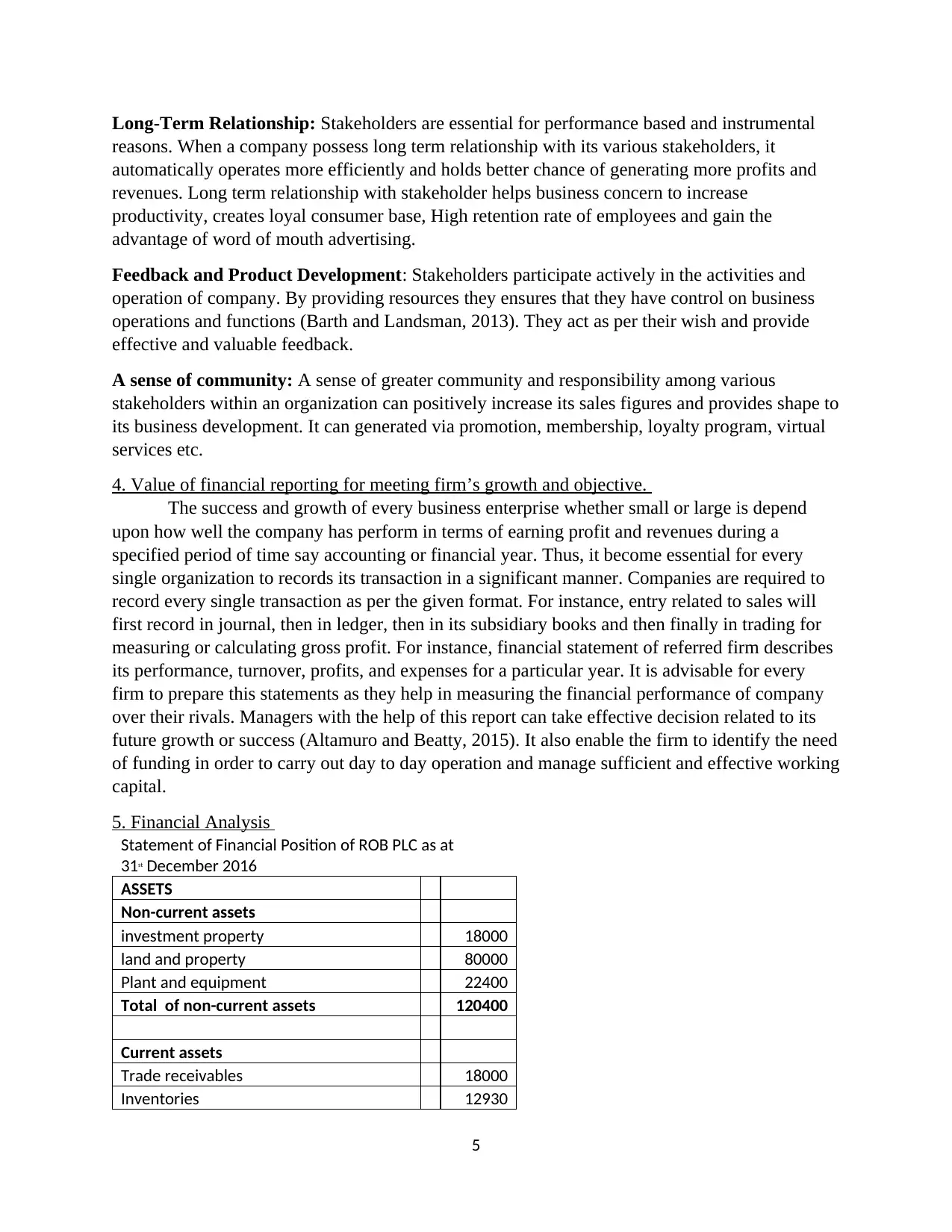

5. Financial Analysis

Statement of Financial Position of ROB PLC as at

31st December 2016

ASSETS

Non-current assets

investment property 18000

land and property 80000

Plant and equipment 22400

Total of non-current assets 120400

Current assets

Trade receivables 18000

Inventories 12930

5

reasons. When a company possess long term relationship with its various stakeholders, it

automatically operates more efficiently and holds better chance of generating more profits and

revenues. Long term relationship with stakeholder helps business concern to increase

productivity, creates loyal consumer base, High retention rate of employees and gain the

advantage of word of mouth advertising.

Feedback and Product Development: Stakeholders participate actively in the activities and

operation of company. By providing resources they ensures that they have control on business

operations and functions (Barth and Landsman, 2013). They act as per their wish and provide

effective and valuable feedback.

A sense of community: A sense of greater community and responsibility among various

stakeholders within an organization can positively increase its sales figures and provides shape to

its business development. It can generated via promotion, membership, loyalty program, virtual

services etc.

4. Value of financial reporting for meeting firm’s growth and objective.

The success and growth of every business enterprise whether small or large is depend

upon how well the company has perform in terms of earning profit and revenues during a

specified period of time say accounting or financial year. Thus, it become essential for every

single organization to records its transaction in a significant manner. Companies are required to

record every single transaction as per the given format. For instance, entry related to sales will

first record in journal, then in ledger, then in its subsidiary books and then finally in trading for

measuring or calculating gross profit. For instance, financial statement of referred firm describes

its performance, turnover, profits, and expenses for a particular year. It is advisable for every

firm to prepare this statements as they help in measuring the financial performance of company

over their rivals. Managers with the help of this report can take effective decision related to its

future growth or success (Altamuro and Beatty, 2015). It also enable the firm to identify the need

of funding in order to carry out day to day operation and manage sufficient and effective working

capital.

5. Financial Analysis

Statement of Financial Position of ROB PLC as at

31st December 2016

ASSETS

Non-current assets

investment property 18000

land and property 80000

Plant and equipment 22400

Total of non-current assets 120400

Current assets

Trade receivables 18000

Inventories 12930

5

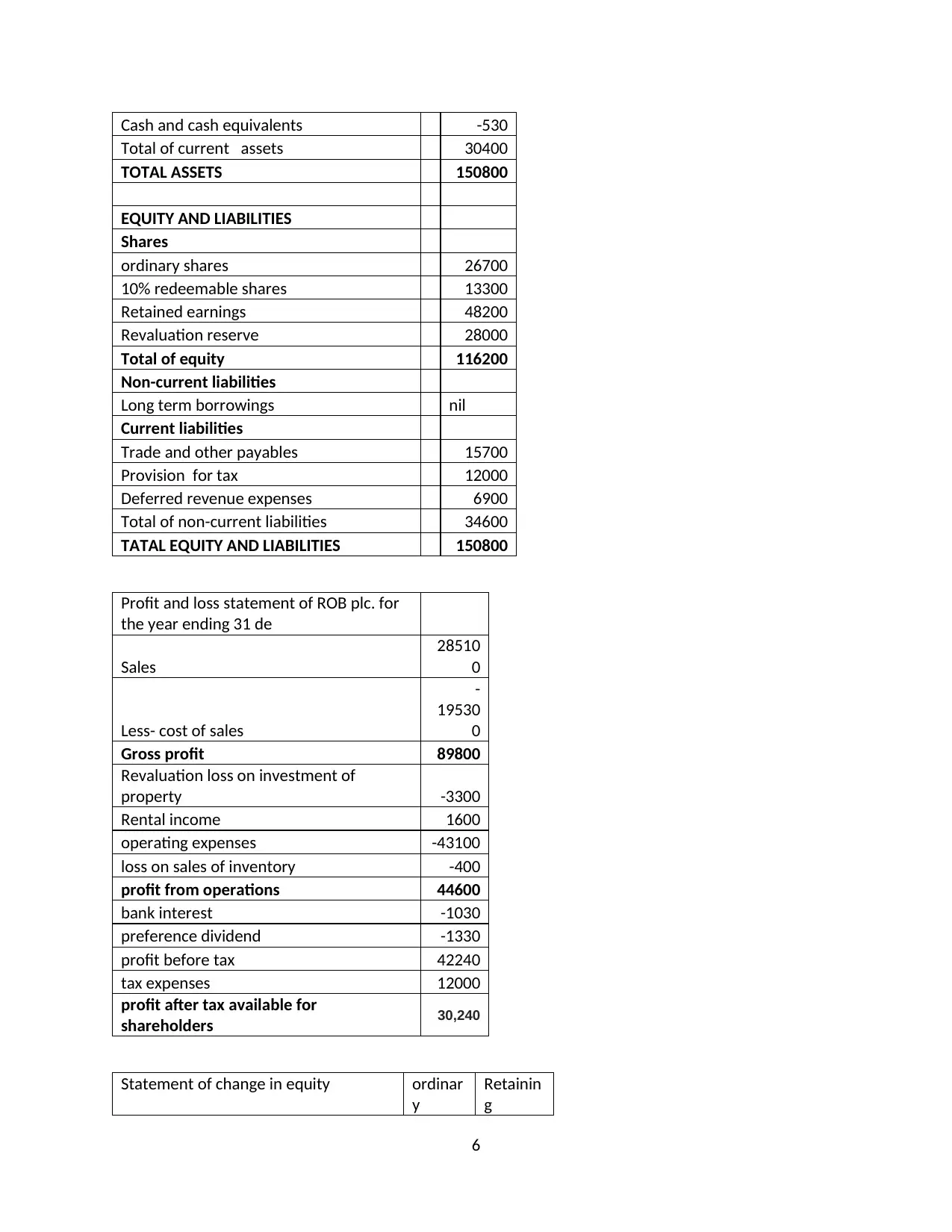

Cash and cash equivalents -530

Total of current assets 30400

TOTAL ASSETS 150800

EQUITY AND LIABILITIES

Shares

ordinary shares 26700

10% redeemable shares 13300

Retained earnings 48200

Revaluation reserve 28000

Total of equity 116200

Non-current liabilities

Long term borrowings nil

Current liabilities

Trade and other payables 15700

Provision for tax 12000

Deferred revenue expenses 6900

Total of non-current liabilities 34600

TATAL EQUITY AND LIABILITIES 150800

Profit and loss statement of ROB plc. for

the year ending 31 de

Sales

28510

0

Less- cost of sales

-

19530

0

Gross profit 89800

Revaluation loss on investment of

property -3300

Rental income 1600

operating expenses -43100

loss on sales of inventory -400

profit from operations 44600

bank interest -1030

preference dividend -1330

profit before tax 42240

tax expenses 12000

profit after tax available for

shareholders 30,240

Statement of change in equity ordinar

y

Retainin

g

6

Total of current assets 30400

TOTAL ASSETS 150800

EQUITY AND LIABILITIES

Shares

ordinary shares 26700

10% redeemable shares 13300

Retained earnings 48200

Revaluation reserve 28000

Total of equity 116200

Non-current liabilities

Long term borrowings nil

Current liabilities

Trade and other payables 15700

Provision for tax 12000

Deferred revenue expenses 6900

Total of non-current liabilities 34600

TATAL EQUITY AND LIABILITIES 150800

Profit and loss statement of ROB plc. for

the year ending 31 de

Sales

28510

0

Less- cost of sales

-

19530

0

Gross profit 89800

Revaluation loss on investment of

property -3300

Rental income 1600

operating expenses -43100

loss on sales of inventory -400

profit from operations 44600

bank interest -1030

preference dividend -1330

profit before tax 42240

tax expenses 12000

profit after tax available for

shareholders 30,240

Statement of change in equity ordinar

y

Retainin

g

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

capital earnings

opening balance 26700 23300

Dividend Paid -5340

Profit for current year 30240

closing balance 26700 48200

6. Interpretation of Financial Statement and ratio

With the help of Ratio Analysis, organization can develop effective strategy that leads to

attain their objective in a structured way. Financial reports assist the manager towards depicting

the future performance of company anticipating their needs. Though this process is little complex

and time consuming but it describes accurate information related to company’s growth,

profitability, liquidity, expenses, debts, income etc. It can better interpret when we compare it

with their last year annual report or last year performance report (Chen, Tang and Lin, 2016).

Manager of referred firm is also doing the same. By comparing, it will help them to determine

the current position of the company in terms of earning profit or income. It also depicts whether

firm has incurred any loss for a particular year or not.

2016 2017

Fiscal Year Ends 28/02/2017 27/02/2016

Turnover 56,004.38 53,933.00

Expenses 61,661.39 52,861.00

EBITDA 2,114.68 2,617.00

EBIT 589.75 1,386.00

Operating Profit

(reported)

-5,657.01 1,072.00

Operating Profit

(adjusted)

604.07 1,417.00

Investment

Income

-38.37 329

Exceptional

Items

-6,261.08 -345

Net Interest -536.19 -830

Pre-tax Profit -6,231.56 202

Tax -659.16 -54

Net Profit -5,572.40 256

Minority

Interests

-24.6 -9

Profit For

Financial Year

-5,648.15 138

Ordinary

Dividends

899.22 0

Non Equity 0 0

7

opening balance 26700 23300

Dividend Paid -5340

Profit for current year 30240

closing balance 26700 48200

6. Interpretation of Financial Statement and ratio

With the help of Ratio Analysis, organization can develop effective strategy that leads to

attain their objective in a structured way. Financial reports assist the manager towards depicting

the future performance of company anticipating their needs. Though this process is little complex

and time consuming but it describes accurate information related to company’s growth,

profitability, liquidity, expenses, debts, income etc. It can better interpret when we compare it

with their last year annual report or last year performance report (Chen, Tang and Lin, 2016).

Manager of referred firm is also doing the same. By comparing, it will help them to determine

the current position of the company in terms of earning profit or income. It also depicts whether

firm has incurred any loss for a particular year or not.

2016 2017

Fiscal Year Ends 28/02/2017 27/02/2016

Turnover 56,004.38 53,933.00

Expenses 61,661.39 52,861.00

EBITDA 2,114.68 2,617.00

EBIT 589.75 1,386.00

Operating Profit

(reported)

-5,657.01 1,072.00

Operating Profit

(adjusted)

604.07 1,417.00

Investment

Income

-38.37 329

Exceptional

Items

-6,261.08 -345

Net Interest -536.19 -830

Pre-tax Profit -6,231.56 202

Tax -659.16 -54

Net Profit -5,572.40 256

Minority

Interests

-24.6 -9

Profit For

Financial Year

-5,648.15 138

Ordinary

Dividends

899.22 0

Non Equity 0 0

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Dividends

Retained Profit -6,547.37 138

Per Share Data

DPS p 11.11 0

Normalized

EPS p

9.21 7.1

Reported EPS p -68.44 3.25

Norm

Discontinued

EPS p

2.32 0.35

Investment Ratios

Operating

Margin

0.84 1.25

DPS Growth % -24.75 -

Dividend Cover

x

0.83 0

Norm EPS

Growth %

-68.89 -22.86

Reported EPS

Growth %

- -

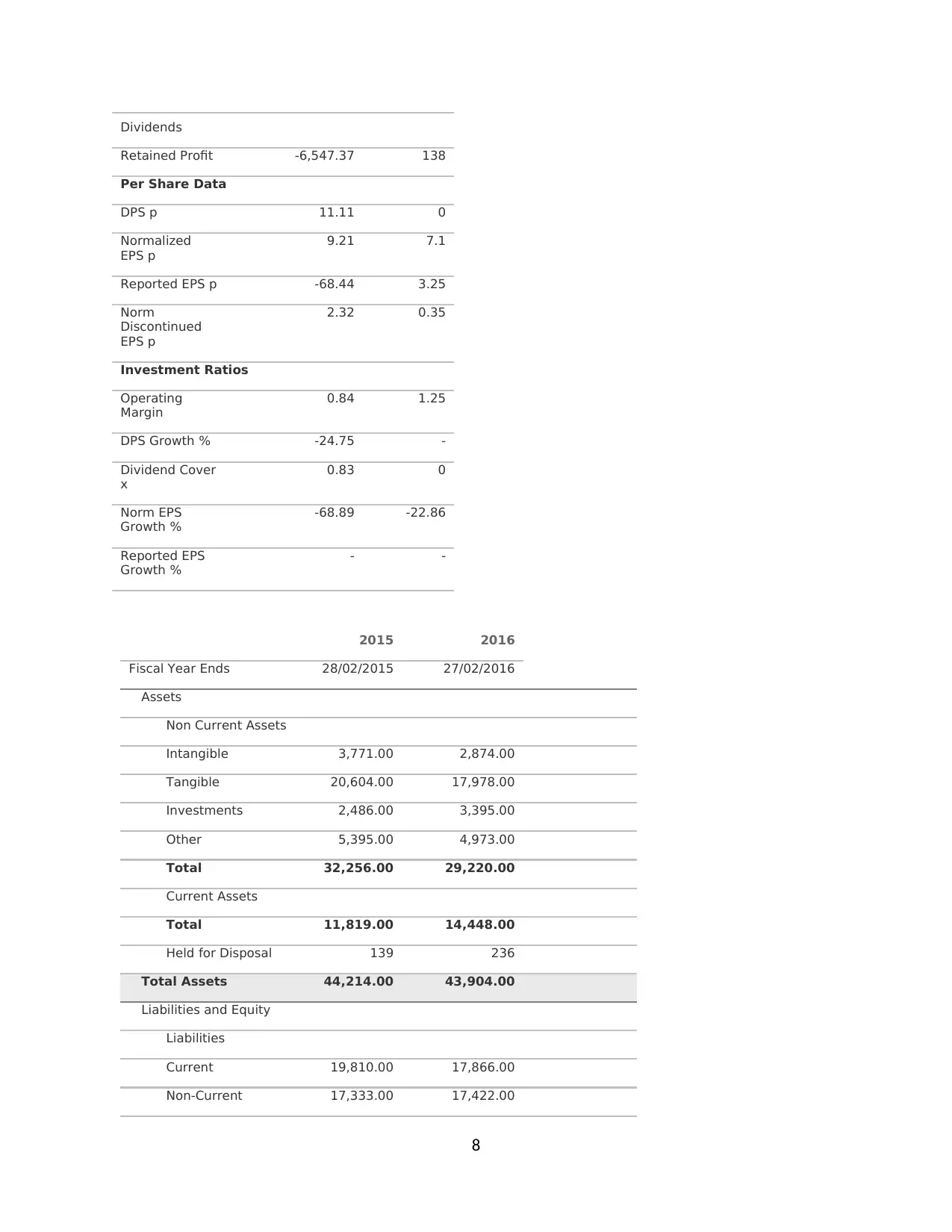

2015 2016

Fiscal Year Ends 28/02/2015 27/02/2016

Assets

Non Current Assets

Intangible 3,771.00 2,874.00

Tangible 20,604.00 17,978.00

Investments 2,486.00 3,395.00

Other 5,395.00 4,973.00

Total 32,256.00 29,220.00

Current Assets

Total 11,819.00 14,448.00

Held for Disposal 139 236

Total Assets 44,214.00 43,904.00

Liabilities and Equity

Liabilities

Current 19,810.00 17,866.00

Non-Current 17,333.00 17,422.00

8

Retained Profit -6,547.37 138

Per Share Data

DPS p 11.11 0

Normalized

EPS p

9.21 7.1

Reported EPS p -68.44 3.25

Norm

Discontinued

EPS p

2.32 0.35

Investment Ratios

Operating

Margin

0.84 1.25

DPS Growth % -24.75 -

Dividend Cover

x

0.83 0

Norm EPS

Growth %

-68.89 -22.86

Reported EPS

Growth %

- -

2015 2016

Fiscal Year Ends 28/02/2015 27/02/2016

Assets

Non Current Assets

Intangible 3,771.00 2,874.00

Tangible 20,604.00 17,978.00

Investments 2,486.00 3,395.00

Other 5,395.00 4,973.00

Total 32,256.00 29,220.00

Current Assets

Total 11,819.00 14,448.00

Held for Disposal 139 236

Total Assets 44,214.00 43,904.00

Liabilities and Equity

Liabilities

Current 19,810.00 17,866.00

Non-Current 17,333.00 17,422.00

8

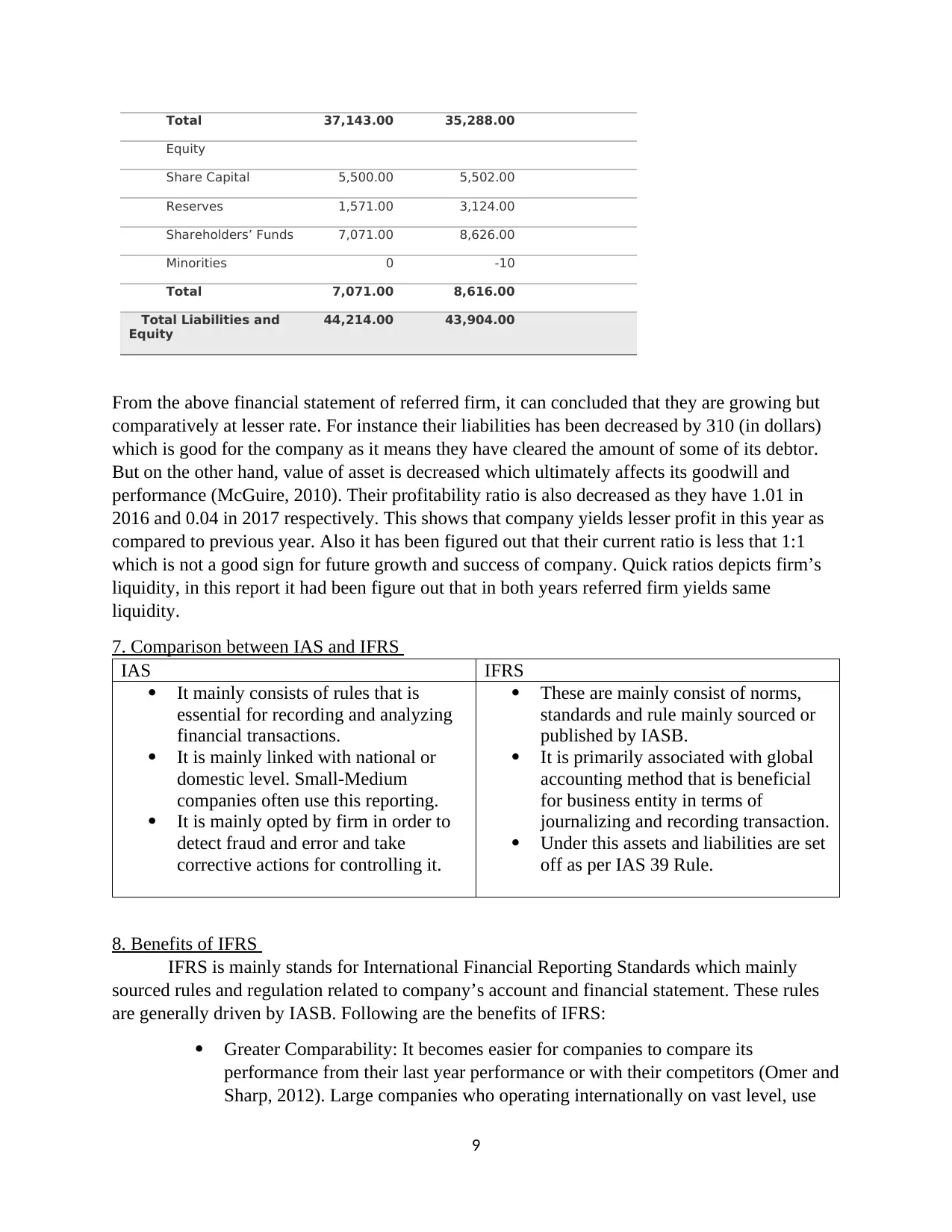

Total 37,143.00 35,288.00

Equity

Share Capital 5,500.00 5,502.00

Reserves 1,571.00 3,124.00

Shareholders’ Funds 7,071.00 8,626.00

Minorities 0 -10

Total 7,071.00 8,616.00

Total Liabilities and

Equity

44,214.00 43,904.00

From the above financial statement of referred firm, it can concluded that they are growing but

comparatively at lesser rate. For instance their liabilities has been decreased by 310 (in dollars)

which is good for the company as it means they have cleared the amount of some of its debtor.

But on the other hand, value of asset is decreased which ultimately affects its goodwill and

performance (McGuire, 2010). Their profitability ratio is also decreased as they have 1.01 in

2016 and 0.04 in 2017 respectively. This shows that company yields lesser profit in this year as

compared to previous year. Also it has been figured out that their current ratio is less that 1:1

which is not a good sign for future growth and success of company. Quick ratios depicts firm’s

liquidity, in this report it had been figure out that in both years referred firm yields same

liquidity.

7. Comparison between IAS and IFRS

IAS IFRS

It mainly consists of rules that is

essential for recording and analyzing

financial transactions.

It is mainly linked with national or

domestic level. Small-Medium

companies often use this reporting.

It is mainly opted by firm in order to

detect fraud and error and take

corrective actions for controlling it.

These are mainly consist of norms,

standards and rule mainly sourced or

published by IASB.

It is primarily associated with global

accounting method that is beneficial

for business entity in terms of

journalizing and recording transaction.

Under this assets and liabilities are set

off as per IAS 39 Rule.

8. Benefits of IFRS

IFRS is mainly stands for International Financial Reporting Standards which mainly

sourced rules and regulation related to company’s account and financial statement. These rules

are generally driven by IASB. Following are the benefits of IFRS:

Greater Comparability: It becomes easier for companies to compare its

performance from their last year performance or with their competitors (Omer and

Sharp, 2012). Large companies who operating internationally on vast level, use

9

Equity

Share Capital 5,500.00 5,502.00

Reserves 1,571.00 3,124.00

Shareholders’ Funds 7,071.00 8,626.00

Minorities 0 -10

Total 7,071.00 8,616.00

Total Liabilities and

Equity

44,214.00 43,904.00

From the above financial statement of referred firm, it can concluded that they are growing but

comparatively at lesser rate. For instance their liabilities has been decreased by 310 (in dollars)

which is good for the company as it means they have cleared the amount of some of its debtor.

But on the other hand, value of asset is decreased which ultimately affects its goodwill and

performance (McGuire, 2010). Their profitability ratio is also decreased as they have 1.01 in

2016 and 0.04 in 2017 respectively. This shows that company yields lesser profit in this year as

compared to previous year. Also it has been figured out that their current ratio is less that 1:1

which is not a good sign for future growth and success of company. Quick ratios depicts firm’s

liquidity, in this report it had been figure out that in both years referred firm yields same

liquidity.

7. Comparison between IAS and IFRS

IAS IFRS

It mainly consists of rules that is

essential for recording and analyzing

financial transactions.

It is mainly linked with national or

domestic level. Small-Medium

companies often use this reporting.

It is mainly opted by firm in order to

detect fraud and error and take

corrective actions for controlling it.

These are mainly consist of norms,

standards and rule mainly sourced or

published by IASB.

It is primarily associated with global

accounting method that is beneficial

for business entity in terms of

journalizing and recording transaction.

Under this assets and liabilities are set

off as per IAS 39 Rule.

8. Benefits of IFRS

IFRS is mainly stands for International Financial Reporting Standards which mainly

sourced rules and regulation related to company’s account and financial statement. These rules

are generally driven by IASB. Following are the benefits of IFRS:

Greater Comparability: It becomes easier for companies to compare its

performance from their last year performance or with their competitors (Omer and

Sharp, 2012). Large companies who operating internationally on vast level, use

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this as they compare between their branches. It enables to notify themselves

regarding the financial position of both branches. With this they can easily

compare its profits, loss, revenues or incomes.

Flexibility: Simple approachability makes regulation and rules easier and flexible.

They follow on the footprints of principle based accounting rather than rule based.

Principle based means recording the amount of asset and liabilities at its revalued

rate. IFRS measure the value of asset and liabilities after deducting depreciation

from it. Thus it is required to record each and every transaction in proper format

and up-to their time period (Nobes, 2014).

Manipulation: This is considered as main Function of IFRS. Organizations are

required to set their own rules and regulation according to which they will record

accounting transaction. There should clear picture of all guidelines related to that.

It helps in determining actual profits and income figure of the firm which enables

them to take the advantage of higher competitiveness level over its rivals or

competitors.

9. Degree of IFRS Compliance by company all over the world.

Compliance means control of standards and rules for better management and operation. IFRS

considered as the set of principles that manages financial statement and accounts in a structured

and thorough manner. Different factors are there that affects the performance and profitability of

business enterprise. Various tools, predetermined standards, prescribing habits are the key

elements that affect the structure and compliance of annual or financial and reporting. Economic

and Demographic are two factors that adversely controls the profitability of company. Liquidity,

market risk, coverage ratio are some factors that falls under this and which directly or indirectly

impacts the overall functioning and management of business concern. Export policies, Interest

Rates, inflation rate, purchasing power, foreign exchange rate are some economic factors also

influence the profitability of company (Epstein and Jermakowicz, 2010).

CONCLUSION

As per the above report it can be concluded that in order to figure out the growth of a

company, it is essential to assess its financial statements as it describes company’s position in

terms of its profits, revenues, growth, debt, liquidity, asset, liabilities etc. All these information

proves to be beneficial and useful for various stakeholders that contributes effectively towards

making strategic decision related to firm’s growth. Financial Report usually made at the end of

year which gives company plenty of time to maintain and record its data on timely basis. IFRS

and IASB has its own regulation and guidelines that company follows and they record the

transaction in that manner.

10

regarding the financial position of both branches. With this they can easily

compare its profits, loss, revenues or incomes.

Flexibility: Simple approachability makes regulation and rules easier and flexible.

They follow on the footprints of principle based accounting rather than rule based.

Principle based means recording the amount of asset and liabilities at its revalued

rate. IFRS measure the value of asset and liabilities after deducting depreciation

from it. Thus it is required to record each and every transaction in proper format

and up-to their time period (Nobes, 2014).

Manipulation: This is considered as main Function of IFRS. Organizations are

required to set their own rules and regulation according to which they will record

accounting transaction. There should clear picture of all guidelines related to that.

It helps in determining actual profits and income figure of the firm which enables

them to take the advantage of higher competitiveness level over its rivals or

competitors.

9. Degree of IFRS Compliance by company all over the world.

Compliance means control of standards and rules for better management and operation. IFRS

considered as the set of principles that manages financial statement and accounts in a structured

and thorough manner. Different factors are there that affects the performance and profitability of

business enterprise. Various tools, predetermined standards, prescribing habits are the key

elements that affect the structure and compliance of annual or financial and reporting. Economic

and Demographic are two factors that adversely controls the profitability of company. Liquidity,

market risk, coverage ratio are some factors that falls under this and which directly or indirectly

impacts the overall functioning and management of business concern. Export policies, Interest

Rates, inflation rate, purchasing power, foreign exchange rate are some economic factors also

influence the profitability of company (Epstein and Jermakowicz, 2010).

CONCLUSION

As per the above report it can be concluded that in order to figure out the growth of a

company, it is essential to assess its financial statements as it describes company’s position in

terms of its profits, revenues, growth, debt, liquidity, asset, liabilities etc. All these information

proves to be beneficial and useful for various stakeholders that contributes effectively towards

making strategic decision related to firm’s growth. Financial Report usually made at the end of

year which gives company plenty of time to maintain and record its data on timely basis. IFRS

and IASB has its own regulation and guidelines that company follows and they record the

transaction in that manner.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFEENCES

Books and Journal

Council, F.R., 2010. The UK corporate governance code. London: Financial Reporting Council.

Beyer, A., Cohen, D.A., and Walther, B.R., 2010. The financial reporting environment: Review of the

recent literature. Journal of accounting and economics. 50(2). pp.296-343.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Li, S., 2010. Does mandatory adoption of International Financial Reporting Standards in the European

Union reduce the cost of equity capital?. The accounting review. 85(2). pp.607-636.

Barth, M.E. and Landsman, W.R., 2010. How did financial reporting contribute to the financial

crisis?. European accounting review.19(3). pp.399-423.

Altamuro, J. and Beatty, A., 2010. How does internal control regulation affect financial reporting?. Journal

of accounting and Economics. 49(1). pp.58-74.

Chen, H., Tang, Q., and Lin, Z., 2010. The role of international financial reporting standards in accounting

quality: Evidence from the European Union. Journal of International Financial Management &

Accounting. 21(3). pp.220-278.

McGuire, S.T., Omer, T.C. and Sharp, N.Y., 2011. The impact of religion on financial reporting

irregularities. The Accounting Review. 87(2). pp.645-673.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Epstein, B.J. and Jermakowicz, E.K., 2010. WILEY Interpretation and Application of International

Financial Reporting Standards 2010. John Wiley & Sons.

Ball, R., Jayaraman, S. and Shivakumar, L., 2012. Audited financial reporting and voluntary disclosure as

complements: A test of the confirmation hypothesis. Journal of Accounting and Economics. 53(1). pp.136-

166.

Iatridis, G., 2010. International Financial Reporting Standards and the quality of financial statement

information. International review of financial analysis. 19(3). pp.193-204.

11

Books and Journal

Council, F.R., 2010. The UK corporate governance code. London: Financial Reporting Council.

Beyer, A., Cohen, D.A., and Walther, B.R., 2010. The financial reporting environment: Review of the

recent literature. Journal of accounting and economics. 50(2). pp.296-343.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Li, S., 2010. Does mandatory adoption of International Financial Reporting Standards in the European

Union reduce the cost of equity capital?. The accounting review. 85(2). pp.607-636.

Barth, M.E. and Landsman, W.R., 2010. How did financial reporting contribute to the financial

crisis?. European accounting review.19(3). pp.399-423.

Altamuro, J. and Beatty, A., 2010. How does internal control regulation affect financial reporting?. Journal

of accounting and Economics. 49(1). pp.58-74.

Chen, H., Tang, Q., and Lin, Z., 2010. The role of international financial reporting standards in accounting

quality: Evidence from the European Union. Journal of International Financial Management &

Accounting. 21(3). pp.220-278.

McGuire, S.T., Omer, T.C. and Sharp, N.Y., 2011. The impact of religion on financial reporting

irregularities. The Accounting Review. 87(2). pp.645-673.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Epstein, B.J. and Jermakowicz, E.K., 2010. WILEY Interpretation and Application of International

Financial Reporting Standards 2010. John Wiley & Sons.

Ball, R., Jayaraman, S. and Shivakumar, L., 2012. Audited financial reporting and voluntary disclosure as

complements: A test of the confirmation hypothesis. Journal of Accounting and Economics. 53(1). pp.136-

166.

Iatridis, G., 2010. International Financial Reporting Standards and the quality of financial statement

information. International review of financial analysis. 19(3). pp.193-204.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.