Analysis of Reckitt Benckiser Group Financial Reporting 2018

VerifiedAdded on 2022/08/20

|9

|2695

|15

Report

AI Summary

This report provides a comprehensive analysis of Reckitt Benckiser Group plc's 2018 financial statements, focusing on key areas such as asset impairment, financial instruments, and defined benefit pension plans, in accordance with IFRS. The report examines the company's accounting policies and valuation methods for impairment, including the identification of cash-generating units (CGUs) and the assessment of recoverable amounts. It also delves into the treatment of financial instruments, including market risk, currency risk, and the application of IFRS 9, as well as the company's hedging strategies. Furthermore, the analysis covers the defined benefit pension plans, including the assumptions used to calculate obligations and the impact of these assumptions on the financial statements. The report concludes by highlighting the significance of these disclosures in providing stakeholders with a clear understanding of the accounting and valuation processes and their impact on the financial position of Reckitt Benckiser.

Running head: FINANCIAL REPORTING

FINANCIAL REPORTING

Name of the Student

Name of the University

Author Note

FINANCIAL REPORTING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL REPORTING

Executive Summary

The report focuses on discussion of impairment of assets, financial instruments, and

defiend benefit pension plan as per the accounting stndards and policies dopted by

Reckittt Benckiser for the year ended as on 2018. The report highlight the treatment and

method of valuation adopted by them, and how it affects the financial position of the

group.

FINANCIAL REPORTING

Executive Summary

The report focuses on discussion of impairment of assets, financial instruments, and

defiend benefit pension plan as per the accounting stndards and policies dopted by

Reckittt Benckiser for the year ended as on 2018. The report highlight the treatment and

method of valuation adopted by them, and how it affects the financial position of the

group.

2

FINANCIAL REPORTING

Table of Contents

Introduction:.......................................................................................................................3

Discussion:.........................................................................................................................3

a) Impairment as per IAS 36:..........................................................................................3

b) Financial instruments:.................................................................................................4

c) Defined Benefit Pension Plans:..................................................................................6

Conclusion.........................................................................................................................7

References.........................................................................................................................8

FINANCIAL REPORTING

Table of Contents

Introduction:.......................................................................................................................3

Discussion:.........................................................................................................................3

a) Impairment as per IAS 36:..........................................................................................3

b) Financial instruments:.................................................................................................4

c) Defined Benefit Pension Plans:..................................................................................6

Conclusion.........................................................................................................................7

References.........................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL REPORTING

Introduction:

The objective of this report is to conduct an analysis of the financial statements of

"Reckitt Benckiser." It is a “multinational company” which is engaged in the production

of consumer goods like home products related to hygiene and health. The organization

is listed on "London Stock Exchange" and also a component of the FTSE 100 Index.

The products range from disinfectant cleaners, automatic washing detergents, pest

control to acne treatment products. The company's segments are across various

regions, consisting of Europe, North America, including countries like Russia and other

segments, consists of North Africa, Middle EastAfrica, and South-east Asia. The brands

that the company has include Strepsils, Air Wick, Dettol, Harpic, Lysol, and Vanish. RB

Group Plc is holding 100% ordinary shares of RB Plc that are incorporated in England

and Wales. The financial statements are prepared in compliance with the EU endorsed

IFRS and interpretations issued by IFRIC. They have also followed the IFRS issued by

IASB. The report discusses the three items accounting treatment, accounting policies

used, and their impact on the financial statement.

Discussion:

The accounts are made under the historical cost method leaving few financial

assets and liabilities, which are accounted at “fair value through profit or loss” (Cristea

2017). The analysis is as follows:

a) Impairment as per IAS 36:

Based on cash flows generated by brand and other production assets and

depending on how management observes the business, the group CGUs

(GCGU) are identified for testing impairment. The company's goodwill and other

intangible assets that have indefinite lives are apportioned to either individual

CGU or to the group of CGUs. The assessment for allocation includes evaluation

of expected growth rates (short/long/medium - term) and calculation of discount

rates (pre-tax). The cash-generating units, as identified by RB Group Plc on the

basis of cash flow generation, are – Health, IFCN, Hygiene, and home. But from

now onwards, Home and Health will not be considered as distinct GCGU

(Rb.com 2020).

When the assets carrying value may not exceed its recoverable amount, then

these intangible assets will be tested for impairment. The recoverable amount is

higher of – (i) fair value (after deducting disposal costs), (ii) value in use. (Gros

and Koch 2018)

The cash flows for impairment purpose are determined on basis of followings:

The gross margin derived from past experience after adjusting for the

impact of estimated production cost.

Net revenue growth is established on anticipated sales quantity and

mix.

PV of cash flows are computed using the discount rate (Maisuradze

2019)

Marketing expenses and other expenditure

The management performed an impairment review for goodwill and other

indefinite-life intangible assets. After evaluating the management's analysis, the

FINANCIAL REPORTING

Introduction:

The objective of this report is to conduct an analysis of the financial statements of

"Reckitt Benckiser." It is a “multinational company” which is engaged in the production

of consumer goods like home products related to hygiene and health. The organization

is listed on "London Stock Exchange" and also a component of the FTSE 100 Index.

The products range from disinfectant cleaners, automatic washing detergents, pest

control to acne treatment products. The company's segments are across various

regions, consisting of Europe, North America, including countries like Russia and other

segments, consists of North Africa, Middle EastAfrica, and South-east Asia. The brands

that the company has include Strepsils, Air Wick, Dettol, Harpic, Lysol, and Vanish. RB

Group Plc is holding 100% ordinary shares of RB Plc that are incorporated in England

and Wales. The financial statements are prepared in compliance with the EU endorsed

IFRS and interpretations issued by IFRIC. They have also followed the IFRS issued by

IASB. The report discusses the three items accounting treatment, accounting policies

used, and their impact on the financial statement.

Discussion:

The accounts are made under the historical cost method leaving few financial

assets and liabilities, which are accounted at “fair value through profit or loss” (Cristea

2017). The analysis is as follows:

a) Impairment as per IAS 36:

Based on cash flows generated by brand and other production assets and

depending on how management observes the business, the group CGUs

(GCGU) are identified for testing impairment. The company's goodwill and other

intangible assets that have indefinite lives are apportioned to either individual

CGU or to the group of CGUs. The assessment for allocation includes evaluation

of expected growth rates (short/long/medium - term) and calculation of discount

rates (pre-tax). The cash-generating units, as identified by RB Group Plc on the

basis of cash flow generation, are – Health, IFCN, Hygiene, and home. But from

now onwards, Home and Health will not be considered as distinct GCGU

(Rb.com 2020).

When the assets carrying value may not exceed its recoverable amount, then

these intangible assets will be tested for impairment. The recoverable amount is

higher of – (i) fair value (after deducting disposal costs), (ii) value in use. (Gros

and Koch 2018)

The cash flows for impairment purpose are determined on basis of followings:

The gross margin derived from past experience after adjusting for the

impact of estimated production cost.

Net revenue growth is established on anticipated sales quantity and

mix.

PV of cash flows are computed using the discount rate (Maisuradze

2019)

Marketing expenses and other expenditure

The management performed an impairment review for goodwill and other

indefinite-life intangible assets. After evaluating the management's analysis, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL REPORTING

company established correctness of significant judgments, particular risk issues,

and sensitivities that are applied to separate CGU and GCGUS. The analysis

conducted by them showed that there was no impairment required on 31st

December 2018. For IFCN, recoverability of assets is evaluated by using

estimated financial information based on discounted cash flow model, which is

extremely sensitive to variations in assumptions. (Rb.com 2020).

There are deviations in those assumptions that will lead to recognition of

impairment. PPE is re-evaluated for impairment whenever carrying amount is not

appropriate, but on freehold land test for impairment is being conducted annually.

Recoverable amount is calculated for IFCN – by computing value in use taking

discount rate at 10% (pre-tax), and for Oriental Pharma, it is taken at 13%. The discount

rate is determined by management for each CGU and GCGU by performing a bottom-

up analysis of suitable WACC after combining with comparable companies' benchmark.

For health and hygiene home CGUs and also “Sexual Wellbeing” and “Brazilian Sexual

Wellbeing GCGUs”, any possible change, which results in rational and critical

assumptions for valuation, would not necessarily imply potential impairment. The

impairment loss is recognized in the income statement which is resulting from excess of

carrying value over its recoverable amount. The impairment loss results in lower profits

and also affects financial ratios. The assets WDV also reduces as it is deducted from

assets carrying value. The company has provided for impairment on PPE, goodwill, and

intangibles. Since they determine impairment based on historical operating results,

which is approved by the company's management, and it is either for a three or five year

period; hence they have historical impairment.

b) Financial instruments:

The company's financial instruments can be classified into the following category:

(i) Trade and Other receivables/payables

(ii) Equity Instruments

(iii) Derivative financial instruments

(iv) Cash and cash equivalents

(v) Borrowings/financial lease/term loans

(vi) Bonds

(vii) Senior notes

Due to the company's operations, it faces a lot of financial risks, including foreign

exchange risk, credit risk, liquidity, interest rates, and market price fluctuation. The main

financial risks can be classified as follows:

1) Market risk:

(a) Currency risk

(b) Price risk

(c) Interest rate risk

2) Credit risk

3) Liquidity risk

4) Capital Management

FINANCIAL REPORTING

company established correctness of significant judgments, particular risk issues,

and sensitivities that are applied to separate CGU and GCGUS. The analysis

conducted by them showed that there was no impairment required on 31st

December 2018. For IFCN, recoverability of assets is evaluated by using

estimated financial information based on discounted cash flow model, which is

extremely sensitive to variations in assumptions. (Rb.com 2020).

There are deviations in those assumptions that will lead to recognition of

impairment. PPE is re-evaluated for impairment whenever carrying amount is not

appropriate, but on freehold land test for impairment is being conducted annually.

Recoverable amount is calculated for IFCN – by computing value in use taking

discount rate at 10% (pre-tax), and for Oriental Pharma, it is taken at 13%. The discount

rate is determined by management for each CGU and GCGU by performing a bottom-

up analysis of suitable WACC after combining with comparable companies' benchmark.

For health and hygiene home CGUs and also “Sexual Wellbeing” and “Brazilian Sexual

Wellbeing GCGUs”, any possible change, which results in rational and critical

assumptions for valuation, would not necessarily imply potential impairment. The

impairment loss is recognized in the income statement which is resulting from excess of

carrying value over its recoverable amount. The impairment loss results in lower profits

and also affects financial ratios. The assets WDV also reduces as it is deducted from

assets carrying value. The company has provided for impairment on PPE, goodwill, and

intangibles. Since they determine impairment based on historical operating results,

which is approved by the company's management, and it is either for a three or five year

period; hence they have historical impairment.

b) Financial instruments:

The company's financial instruments can be classified into the following category:

(i) Trade and Other receivables/payables

(ii) Equity Instruments

(iii) Derivative financial instruments

(iv) Cash and cash equivalents

(v) Borrowings/financial lease/term loans

(vi) Bonds

(vii) Senior notes

Due to the company's operations, it faces a lot of financial risks, including foreign

exchange risk, credit risk, liquidity, interest rates, and market price fluctuation. The main

financial risks can be classified as follows:

1) Market risk:

(a) Currency risk

(b) Price risk

(c) Interest rate risk

2) Credit risk

3) Liquidity risk

4) Capital Management

5

FINANCIAL REPORTING

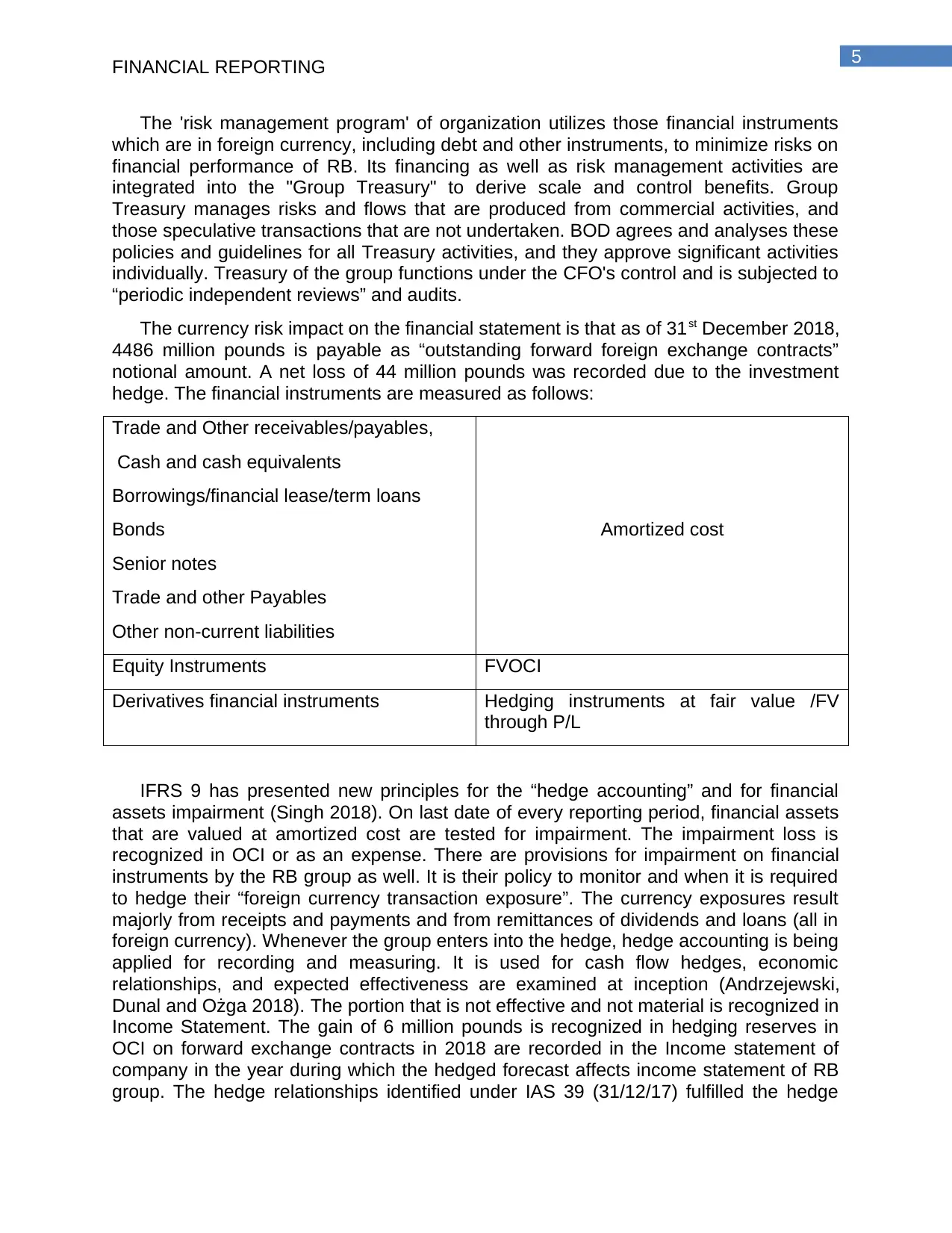

The 'risk management program' of organization utilizes those financial instruments

which are in foreign currency, including debt and other instruments, to minimize risks on

financial performance of RB. Its financing as well as risk management activities are

integrated into the "Group Treasury" to derive scale and control benefits. Group

Treasury manages risks and flows that are produced from commercial activities, and

those speculative transactions that are not undertaken. BOD agrees and analyses these

policies and guidelines for all Treasury activities, and they approve significant activities

individually. Treasury of the group functions under the CFO's control and is subjected to

“periodic independent reviews” and audits.

The currency risk impact on the financial statement is that as of 31st December 2018,

4486 million pounds is payable as “outstanding forward foreign exchange contracts”

notional amount. A net loss of 44 million pounds was recorded due to the investment

hedge. The financial instruments are measured as follows:

Trade and Other receivables/payables,

Cash and cash equivalents

Borrowings/financial lease/term loans

Bonds

Senior notes

Trade and other Payables

Other non-current liabilities

Amortized cost

Equity Instruments FVOCI

Derivatives financial instruments Hedging instruments at fair value /FV

through P/L

IFRS 9 has presented new principles for the “hedge accounting” and for financial

assets impairment (Singh 2018). On last date of every reporting period, financial assets

that are valued at amortized cost are tested for impairment. The impairment loss is

recognized in OCI or as an expense. There are provisions for impairment on financial

instruments by the RB group as well. It is their policy to monitor and when it is required

to hedge their “foreign currency transaction exposure”. The currency exposures result

majorly from receipts and payments and from remittances of dividends and loans (all in

foreign currency). Whenever the group enters into the hedge, hedge accounting is being

applied for recording and measuring. It is used for cash flow hedges, economic

relationships, and expected effectiveness are examined at inception (Andrzejewski,

Dunal and Ożga 2018). The portion that is not effective and not material is recognized in

Income Statement. The gain of 6 million pounds is recognized in hedging reserves in

OCI on forward exchange contracts in 2018 are recorded in the Income statement of

company in the year during which the hedged forecast affects income statement of RB

group. The hedge relationships identified under IAS 39 (31/12/17) fulfilled the hedge

FINANCIAL REPORTING

The 'risk management program' of organization utilizes those financial instruments

which are in foreign currency, including debt and other instruments, to minimize risks on

financial performance of RB. Its financing as well as risk management activities are

integrated into the "Group Treasury" to derive scale and control benefits. Group

Treasury manages risks and flows that are produced from commercial activities, and

those speculative transactions that are not undertaken. BOD agrees and analyses these

policies and guidelines for all Treasury activities, and they approve significant activities

individually. Treasury of the group functions under the CFO's control and is subjected to

“periodic independent reviews” and audits.

The currency risk impact on the financial statement is that as of 31st December 2018,

4486 million pounds is payable as “outstanding forward foreign exchange contracts”

notional amount. A net loss of 44 million pounds was recorded due to the investment

hedge. The financial instruments are measured as follows:

Trade and Other receivables/payables,

Cash and cash equivalents

Borrowings/financial lease/term loans

Bonds

Senior notes

Trade and other Payables

Other non-current liabilities

Amortized cost

Equity Instruments FVOCI

Derivatives financial instruments Hedging instruments at fair value /FV

through P/L

IFRS 9 has presented new principles for the “hedge accounting” and for financial

assets impairment (Singh 2018). On last date of every reporting period, financial assets

that are valued at amortized cost are tested for impairment. The impairment loss is

recognized in OCI or as an expense. There are provisions for impairment on financial

instruments by the RB group as well. It is their policy to monitor and when it is required

to hedge their “foreign currency transaction exposure”. The currency exposures result

majorly from receipts and payments and from remittances of dividends and loans (all in

foreign currency). Whenever the group enters into the hedge, hedge accounting is being

applied for recording and measuring. It is used for cash flow hedges, economic

relationships, and expected effectiveness are examined at inception (Andrzejewski,

Dunal and Ożga 2018). The portion that is not effective and not material is recognized in

Income Statement. The gain of 6 million pounds is recognized in hedging reserves in

OCI on forward exchange contracts in 2018 are recorded in the Income statement of

company in the year during which the hedged forecast affects income statement of RB

group. The hedge relationships identified under IAS 39 (31/12/17) fulfilled the hedge

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL REPORTING

accounting criteria under IFRS 9 (1/01/18) and were hence considered as hedging

transactions (Gornjak 2017).

The company conducts sensitivity analysis for each assumption to evaluate the

changes in those assumptions in comparison with previous estimates and then identify

the most sensitive assumption. The principles of IFRS 9 were adopted by RB Group,

and there were no material changes in the classification of income and expenses to the

P/L as well as all liabilities and organization’s assets in the Balance Sheet including

measurement for the same. The classes of financial assets and liabilities have a similar

carrying value under IFRS 9 as it was under IAS 39. There is no material impact of the

changes, and there is complete disclosure.

c) Defined Benefit Pension Plans:

The members of defined contribution plans are the employees of the organization

and these are provided with pension, and that pension is being charged to Profit /Loss

Statement (Glaum, Keller and Street 2018). It is recorded as contributions that are

made to such members. RB group has no other payment liability once this contribution

has been paid. For the defined pension plan, any gain or loss is the Present value less

fair value of plan assets as on the last date of accounting year. Present value is

computed by discounting the probable and prospect cash-flows at the yield on similar

“corporate bonds” that are denominated in the currency in which the pension benefits

are rewarded to the employees.

Yes, obligations for the “defined benefit pension plans” are based on assumptions

regarding the upcoming mortality experience, which are set as per the published

statistics and overall experience. And for their UK plan, assumptions are based on the

standard 'SAPS mortality table.' The assumption (UK) includes a 5.4% increase in rate

for pensionable salaries, a discount rate of 2.7%, 3% increase in pension payments

(Rb.com 2020). The assumptions are realistic as they are based on the overall practice

and experience considering every region. The impact of such assumptions on the

financial statement is such that gains are occurring from deviation in demographic

assumptions and surplus from such deviations in all the assumptions.

For defined plan discount rate is used to compute the liabilities, and the rate is

determined according to the yield on corporate bonds. When plan assets’ performance

falls below this bonds’ yield, it will lead to a deficit. There is a sensitivity analysis for

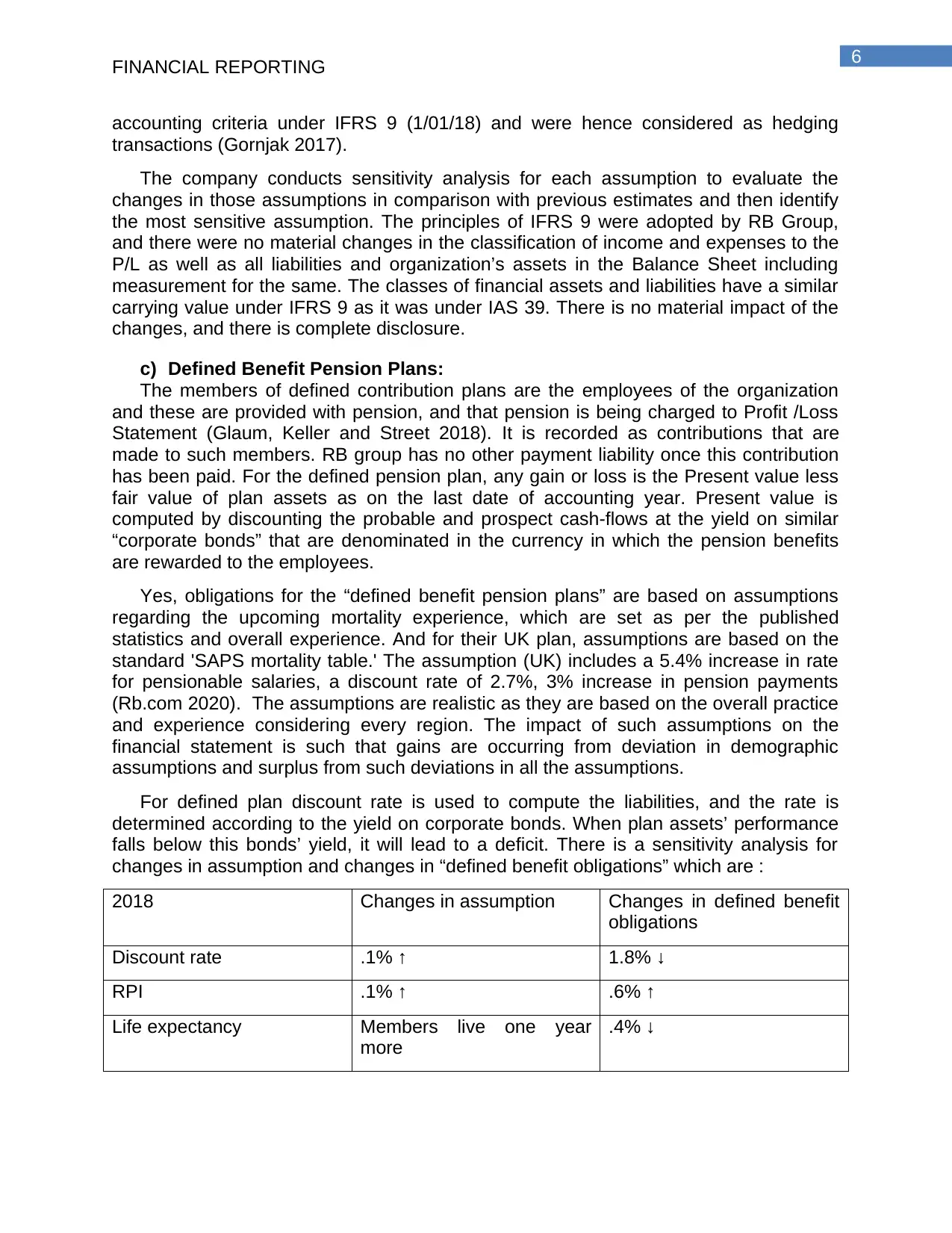

changes in assumption and changes in “defined benefit obligations” which are :

2018 Changes in assumption Changes in defined benefit

obligations

Discount rate .1% ↑ 1.8% ↓

RPI .1% ↑ .6% ↑

Life expectancy Members live one year

more

.4% ↓

FINANCIAL REPORTING

accounting criteria under IFRS 9 (1/01/18) and were hence considered as hedging

transactions (Gornjak 2017).

The company conducts sensitivity analysis for each assumption to evaluate the

changes in those assumptions in comparison with previous estimates and then identify

the most sensitive assumption. The principles of IFRS 9 were adopted by RB Group,

and there were no material changes in the classification of income and expenses to the

P/L as well as all liabilities and organization’s assets in the Balance Sheet including

measurement for the same. The classes of financial assets and liabilities have a similar

carrying value under IFRS 9 as it was under IAS 39. There is no material impact of the

changes, and there is complete disclosure.

c) Defined Benefit Pension Plans:

The members of defined contribution plans are the employees of the organization

and these are provided with pension, and that pension is being charged to Profit /Loss

Statement (Glaum, Keller and Street 2018). It is recorded as contributions that are

made to such members. RB group has no other payment liability once this contribution

has been paid. For the defined pension plan, any gain or loss is the Present value less

fair value of plan assets as on the last date of accounting year. Present value is

computed by discounting the probable and prospect cash-flows at the yield on similar

“corporate bonds” that are denominated in the currency in which the pension benefits

are rewarded to the employees.

Yes, obligations for the “defined benefit pension plans” are based on assumptions

regarding the upcoming mortality experience, which are set as per the published

statistics and overall experience. And for their UK plan, assumptions are based on the

standard 'SAPS mortality table.' The assumption (UK) includes a 5.4% increase in rate

for pensionable salaries, a discount rate of 2.7%, 3% increase in pension payments

(Rb.com 2020). The assumptions are realistic as they are based on the overall practice

and experience considering every region. The impact of such assumptions on the

financial statement is such that gains are occurring from deviation in demographic

assumptions and surplus from such deviations in all the assumptions.

For defined plan discount rate is used to compute the liabilities, and the rate is

determined according to the yield on corporate bonds. When plan assets’ performance

falls below this bonds’ yield, it will lead to a deficit. There is a sensitivity analysis for

changes in assumption and changes in “defined benefit obligations” which are :

2018 Changes in assumption Changes in defined benefit

obligations

Discount rate .1% ↑ 1.8% ↓

RPI .1% ↑ .6% ↑

Life expectancy Members live one year

more

.4% ↓

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL REPORTING

This analysis is conducted on the basis of change in the assumption while

keeping various other assumptions at constant, which is not realistic and not likely to

occur. Few assumptions are made on the basis of historical events and experiences.

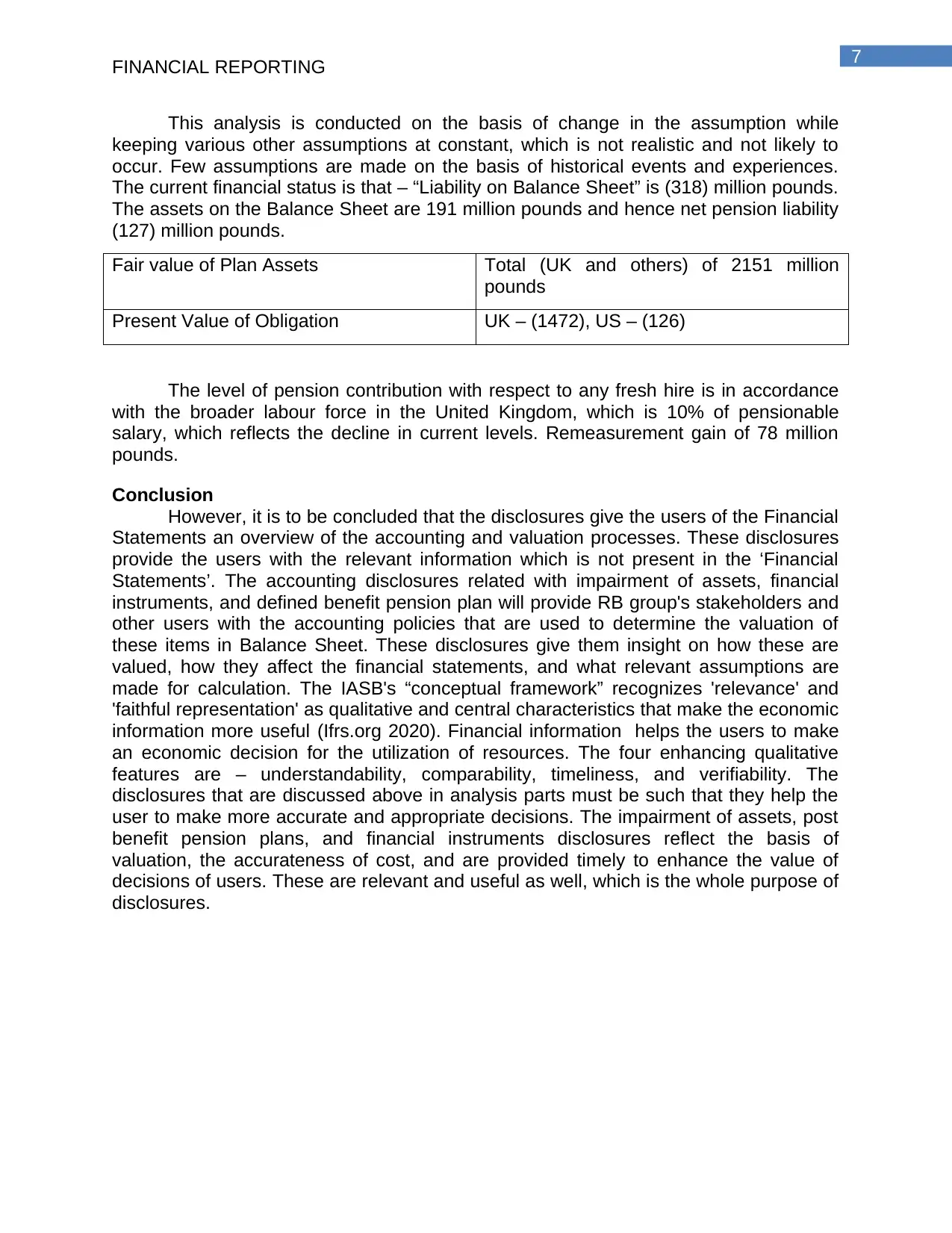

The current financial status is that – “Liability on Balance Sheet” is (318) million pounds.

The assets on the Balance Sheet are 191 million pounds and hence net pension liability

(127) million pounds.

Fair value of Plan Assets Total (UK and others) of 2151 million

pounds

Present Value of Obligation UK – (1472), US – (126)

The level of pension contribution with respect to any fresh hire is in accordance

with the broader labour force in the United Kingdom, which is 10% of pensionable

salary, which reflects the decline in current levels. Remeasurement gain of 78 million

pounds.

Conclusion

However, it is to be concluded that the disclosures give the users of the Financial

Statements an overview of the accounting and valuation processes. These disclosures

provide the users with the relevant information which is not present in the ‘Financial

Statements’. The accounting disclosures related with impairment of assets, financial

instruments, and defined benefit pension plan will provide RB group's stakeholders and

other users with the accounting policies that are used to determine the valuation of

these items in Balance Sheet. These disclosures give them insight on how these are

valued, how they affect the financial statements, and what relevant assumptions are

made for calculation. The IASB's “conceptual framework” recognizes 'relevance' and

'faithful representation' as qualitative and central characteristics that make the economic

information more useful (Ifrs.org 2020). Financial information helps the users to make

an economic decision for the utilization of resources. The four enhancing qualitative

features are – understandability, comparability, timeliness, and verifiability. The

disclosures that are discussed above in analysis parts must be such that they help the

user to make more accurate and appropriate decisions. The impairment of assets, post

benefit pension plans, and financial instruments disclosures reflect the basis of

valuation, the accurateness of cost, and are provided timely to enhance the value of

decisions of users. These are relevant and useful as well, which is the whole purpose of

disclosures.

FINANCIAL REPORTING

This analysis is conducted on the basis of change in the assumption while

keeping various other assumptions at constant, which is not realistic and not likely to

occur. Few assumptions are made on the basis of historical events and experiences.

The current financial status is that – “Liability on Balance Sheet” is (318) million pounds.

The assets on the Balance Sheet are 191 million pounds and hence net pension liability

(127) million pounds.

Fair value of Plan Assets Total (UK and others) of 2151 million

pounds

Present Value of Obligation UK – (1472), US – (126)

The level of pension contribution with respect to any fresh hire is in accordance

with the broader labour force in the United Kingdom, which is 10% of pensionable

salary, which reflects the decline in current levels. Remeasurement gain of 78 million

pounds.

Conclusion

However, it is to be concluded that the disclosures give the users of the Financial

Statements an overview of the accounting and valuation processes. These disclosures

provide the users with the relevant information which is not present in the ‘Financial

Statements’. The accounting disclosures related with impairment of assets, financial

instruments, and defined benefit pension plan will provide RB group's stakeholders and

other users with the accounting policies that are used to determine the valuation of

these items in Balance Sheet. These disclosures give them insight on how these are

valued, how they affect the financial statements, and what relevant assumptions are

made for calculation. The IASB's “conceptual framework” recognizes 'relevance' and

'faithful representation' as qualitative and central characteristics that make the economic

information more useful (Ifrs.org 2020). Financial information helps the users to make

an economic decision for the utilization of resources. The four enhancing qualitative

features are – understandability, comparability, timeliness, and verifiability. The

disclosures that are discussed above in analysis parts must be such that they help the

user to make more accurate and appropriate decisions. The impairment of assets, post

benefit pension plans, and financial instruments disclosures reflect the basis of

valuation, the accurateness of cost, and are provided timely to enhance the value of

decisions of users. These are relevant and useful as well, which is the whole purpose of

disclosures.

8

FINANCIAL REPORTING

References

Andrzejewski, M., Dunal, P. and Ożga, P., 2018. True and Fair View of Derivative

Instruments in Hedge Accounting Model under IFRS 9. Folia Oeconomic, 6(339),

pp.185-201.

Cristea, VG, 2017. ACCOUNTING HARMONIZATION AND HISTORICAL COST

ACCOUNTING. Challenges of the Knowledge Society, pp.697-700.

Glaum, M., Keller, T. and Street, D.L., 2018. Discretionary accounting choices: The

case of IAS 19 pension accounting. Accounting and Business Research, 48(2), pp.139-

170.

Gornjak, M., 2017. Comparison of IAS 39 and IFRS 9: The Analysis of

Replacement. International Journal of Management, Knowledge and Learning, (1),

pp.115-130.

Gros, M. and Koch, S., 2018. Goodwill Impairment Test Disclosures under IAS 36:

Compliance and Disclosure Quality, Disclosure Determinants, and the Role of

Enforcement. Corporate Ownership & Control, 16, pp.145-167.

Ifrs.org, 2020. IFRS. [online] Ifrs.org. Available at:

<https://www.ifrs.org/groups/international-accounting-standards-board/> [Accessed 17

March 2020].

Maisuradze, M., 2019. BASIC ASPECTS OF MEASUREMENT OF IMPAIRMENT OF

LONG-TERM ASSETS OF AN ENTITY. Ecoforum Journal, 8(3).

Rb.com, 2020. RB | Annual Report 2018 | Investors. [online] Rb.com. Available at:

<https://www.rb.com/investors/annual-report-2018/> [Accessed 17 March 2020].

Singh, J.P., 2018. On hedge effectiveness assessment under IFRS 9. Audit

Financiar, 16(149), pp.157-170.

FINANCIAL REPORTING

References

Andrzejewski, M., Dunal, P. and Ożga, P., 2018. True and Fair View of Derivative

Instruments in Hedge Accounting Model under IFRS 9. Folia Oeconomic, 6(339),

pp.185-201.

Cristea, VG, 2017. ACCOUNTING HARMONIZATION AND HISTORICAL COST

ACCOUNTING. Challenges of the Knowledge Society, pp.697-700.

Glaum, M., Keller, T. and Street, D.L., 2018. Discretionary accounting choices: The

case of IAS 19 pension accounting. Accounting and Business Research, 48(2), pp.139-

170.

Gornjak, M., 2017. Comparison of IAS 39 and IFRS 9: The Analysis of

Replacement. International Journal of Management, Knowledge and Learning, (1),

pp.115-130.

Gros, M. and Koch, S., 2018. Goodwill Impairment Test Disclosures under IAS 36:

Compliance and Disclosure Quality, Disclosure Determinants, and the Role of

Enforcement. Corporate Ownership & Control, 16, pp.145-167.

Ifrs.org, 2020. IFRS. [online] Ifrs.org. Available at:

<https://www.ifrs.org/groups/international-accounting-standards-board/> [Accessed 17

March 2020].

Maisuradze, M., 2019. BASIC ASPECTS OF MEASUREMENT OF IMPAIRMENT OF

LONG-TERM ASSETS OF AN ENTITY. Ecoforum Journal, 8(3).

Rb.com, 2020. RB | Annual Report 2018 | Investors. [online] Rb.com. Available at:

<https://www.rb.com/investors/annual-report-2018/> [Accessed 17 March 2020].

Singh, J.P., 2018. On hedge effectiveness assessment under IFRS 9. Audit

Financiar, 16(149), pp.157-170.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.