Financial Reporting: Preparation of Financial Statements and Analysis

VerifiedAdded on 2021/06/15

|11

|2123

|33

Homework Assignment

AI Summary

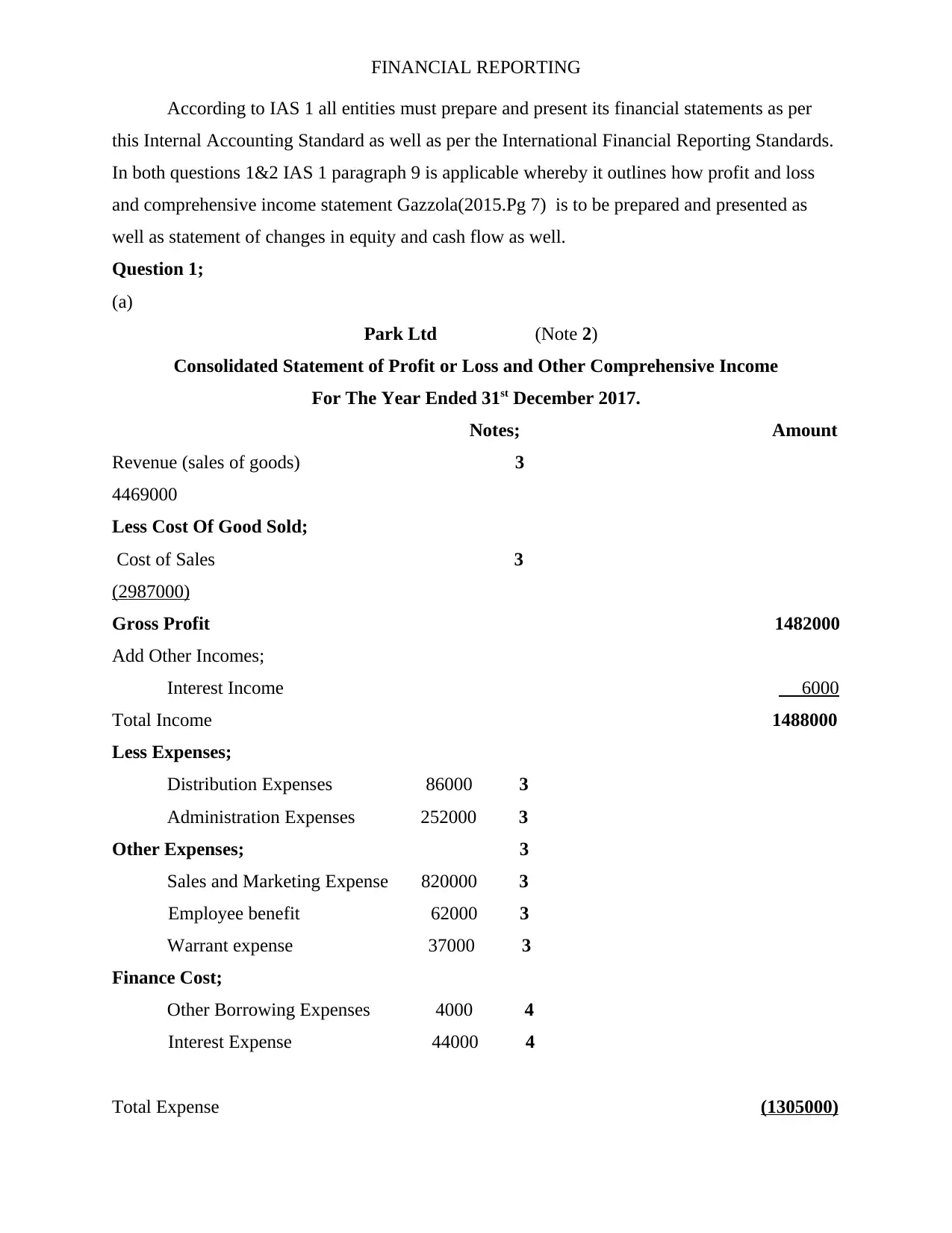

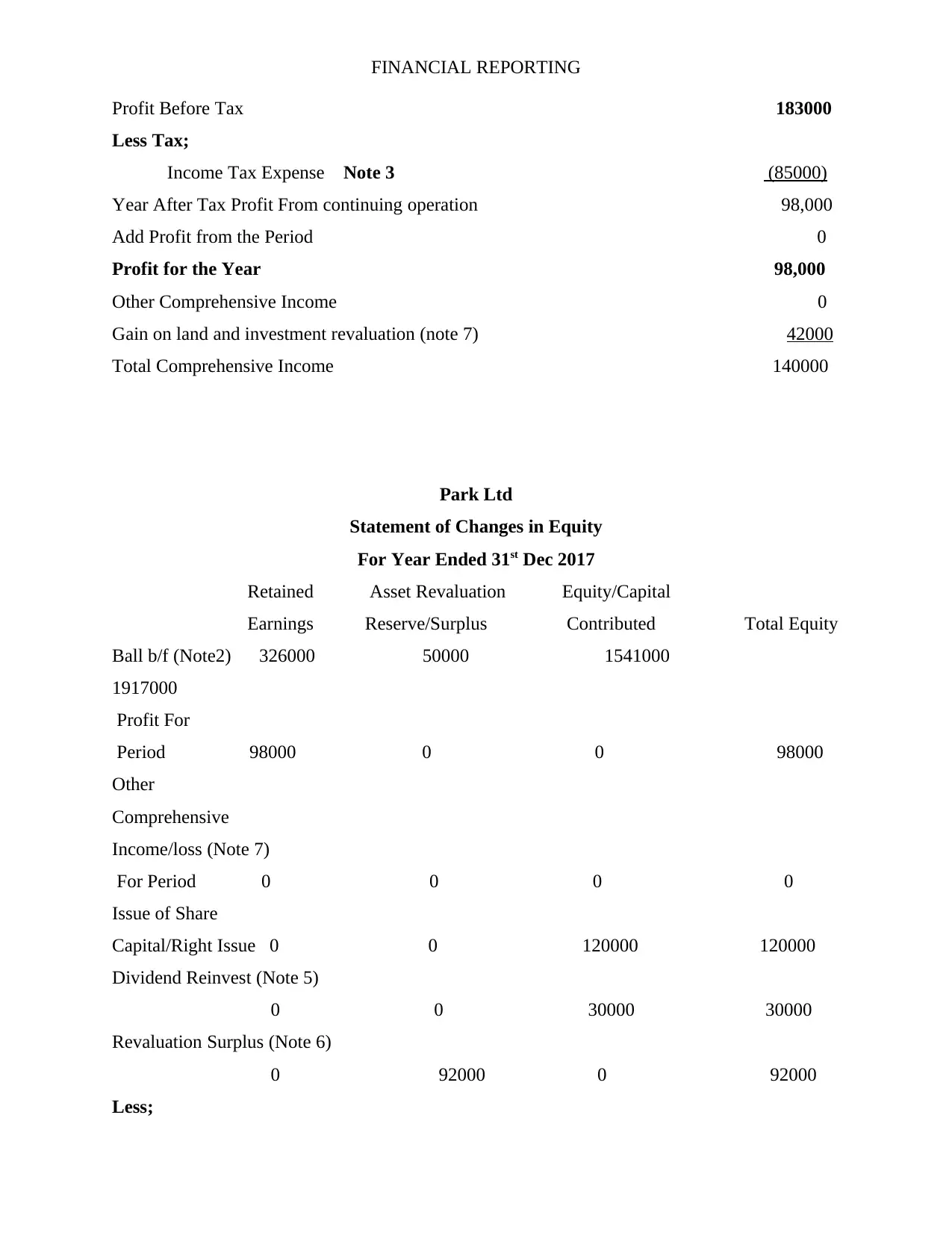

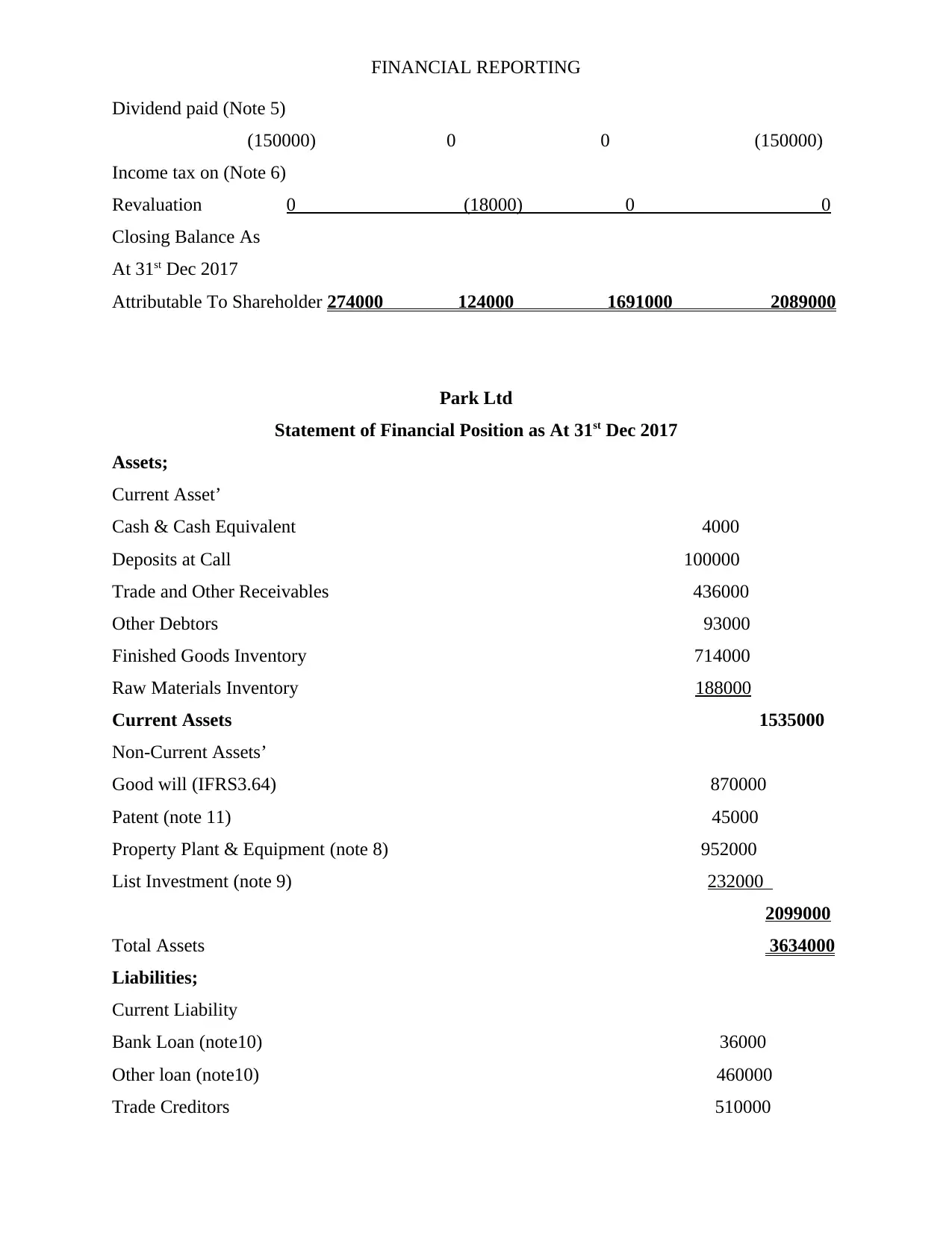

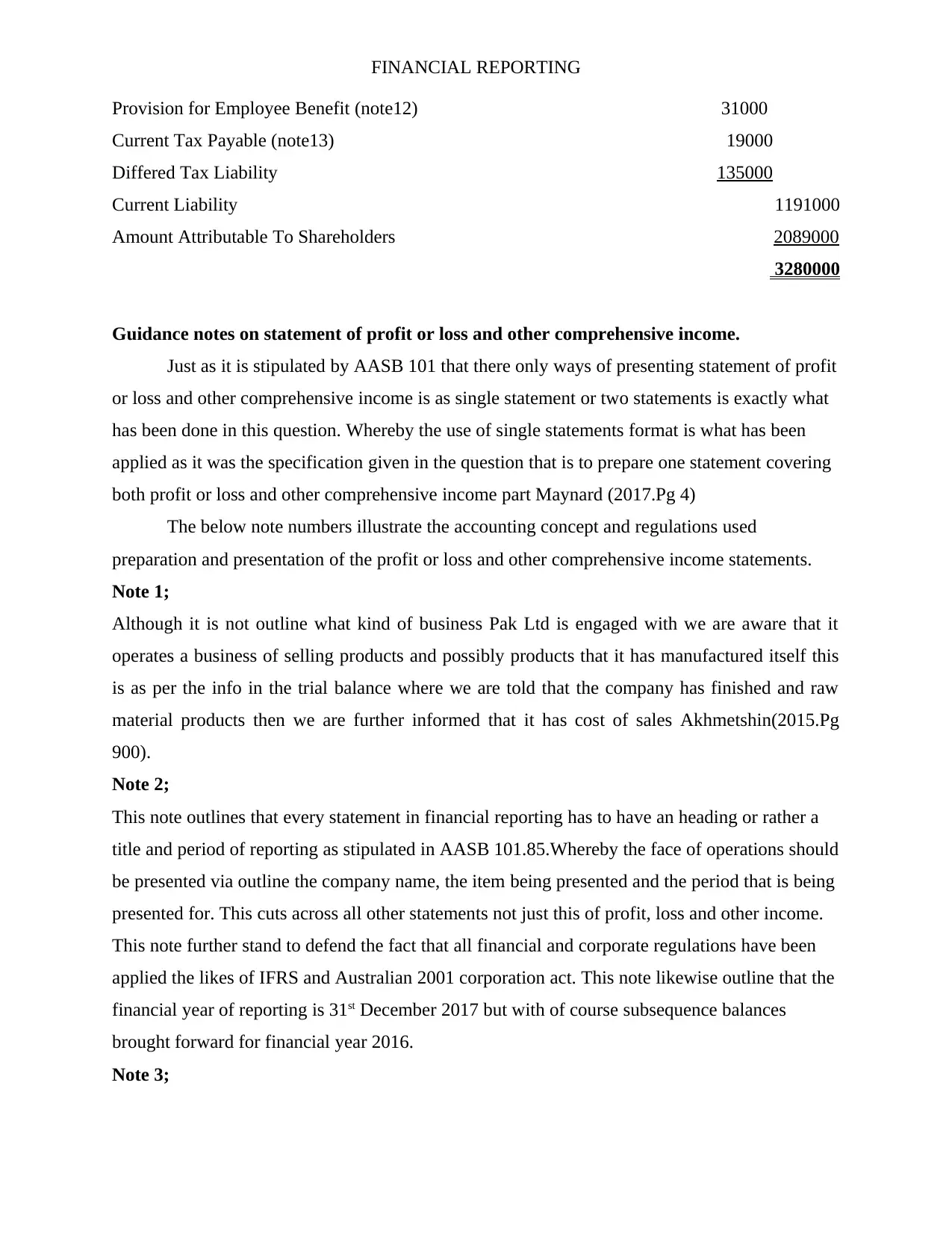

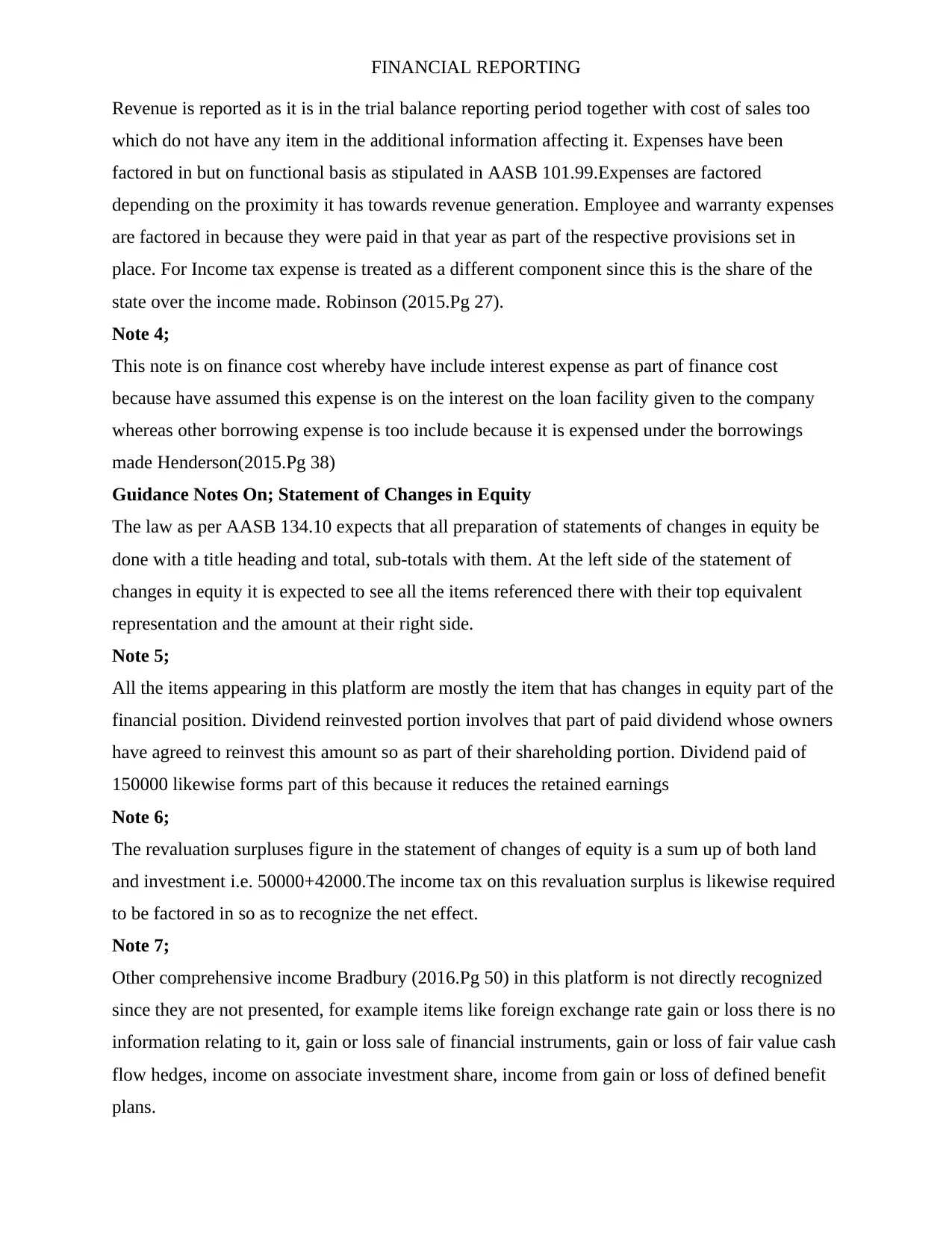

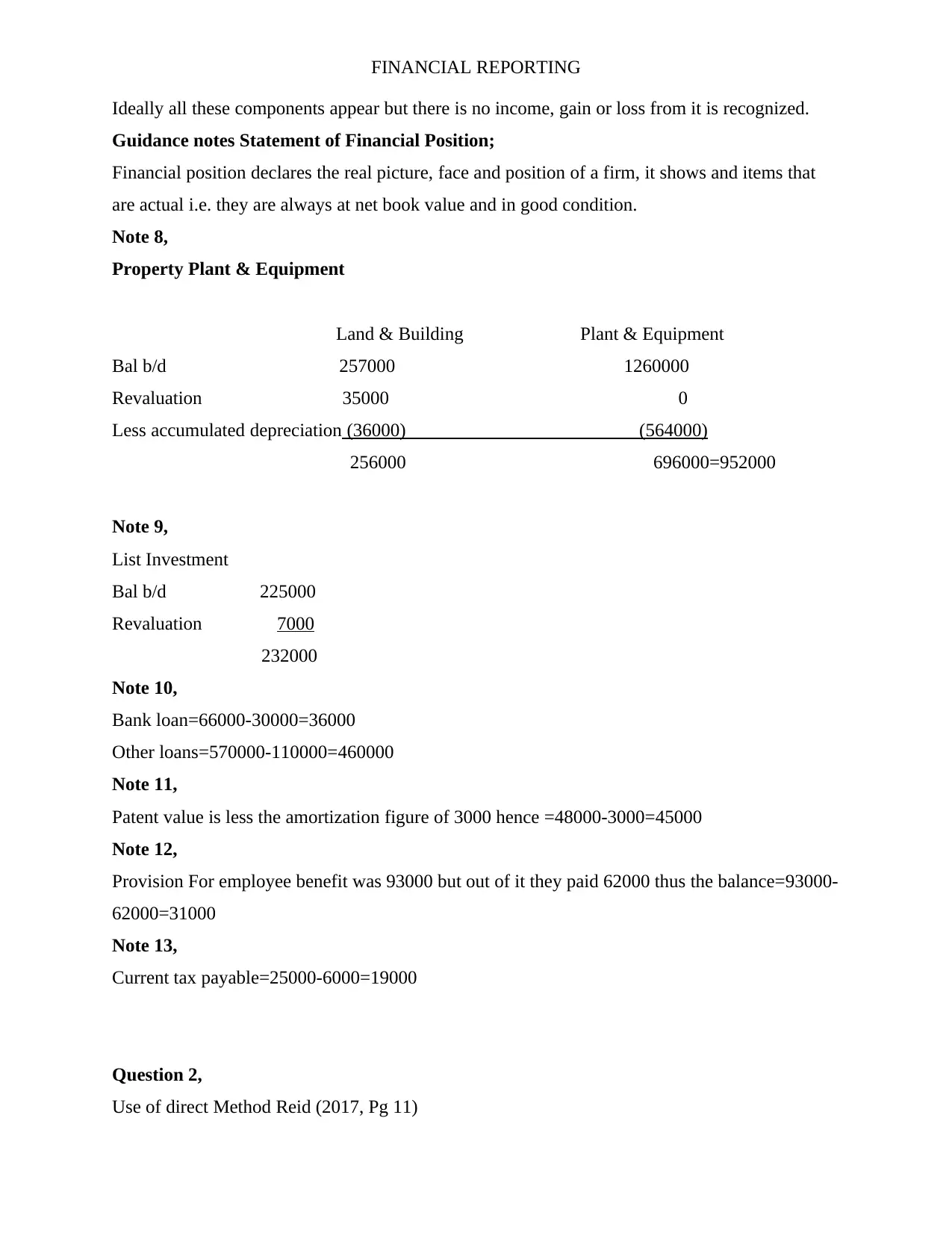

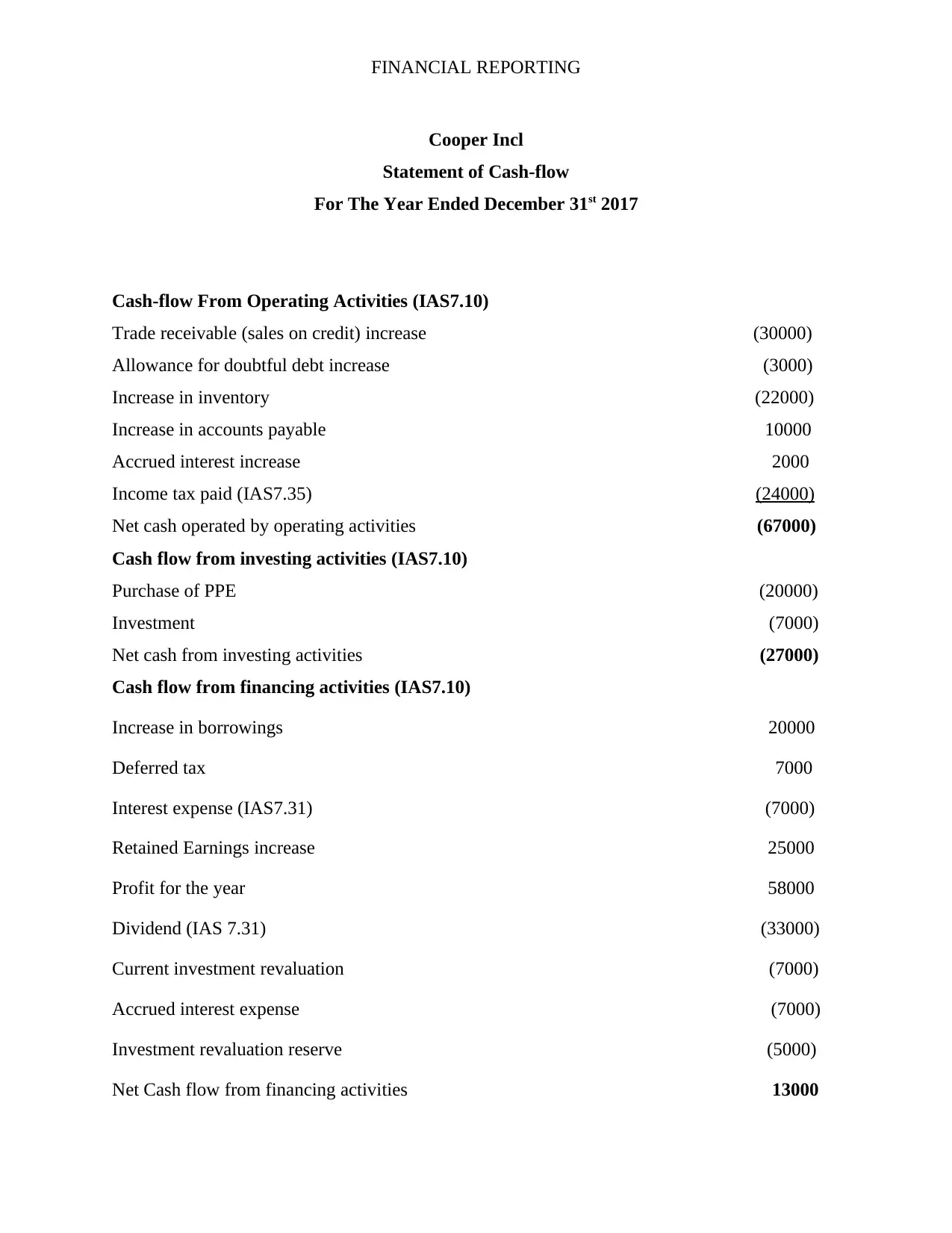

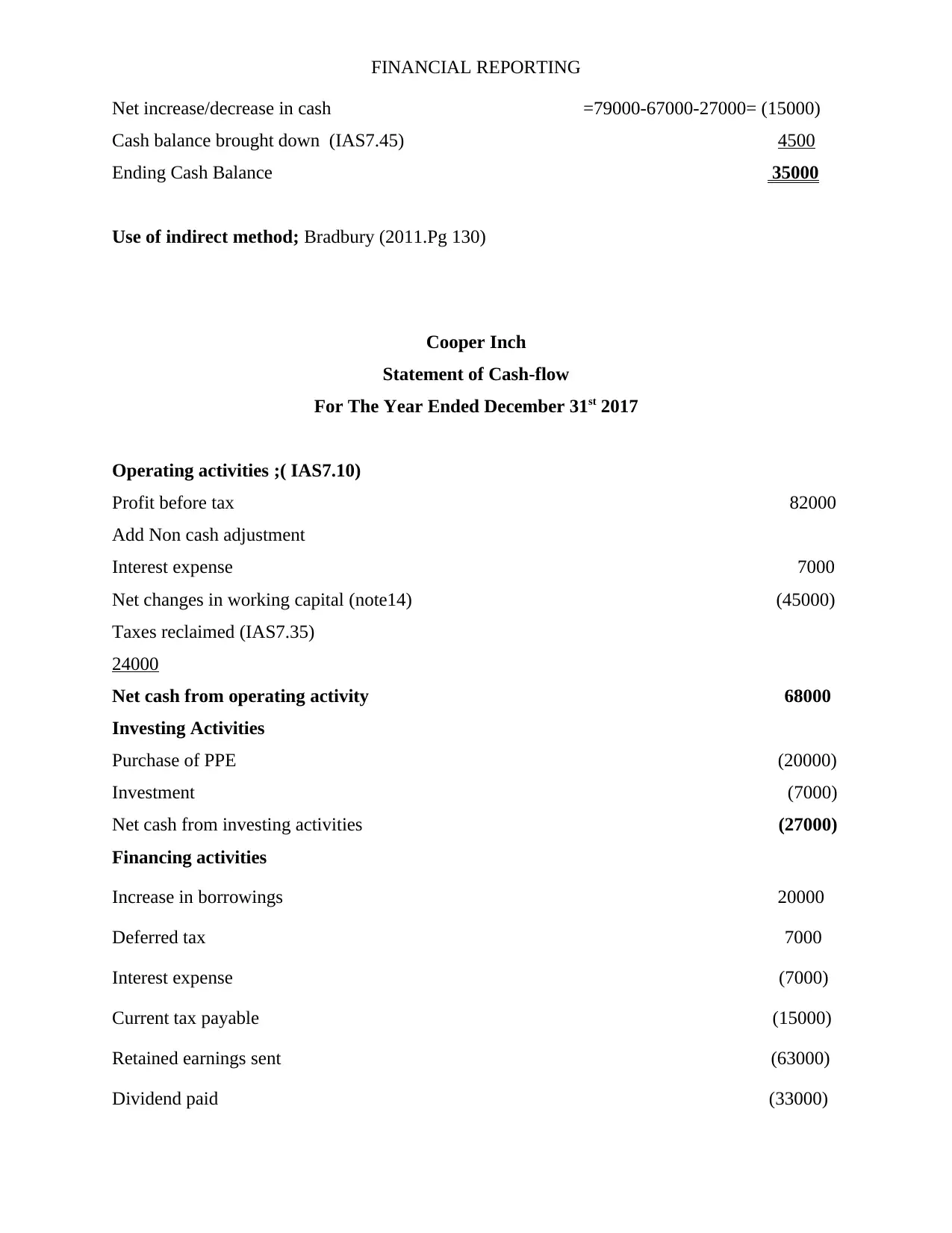

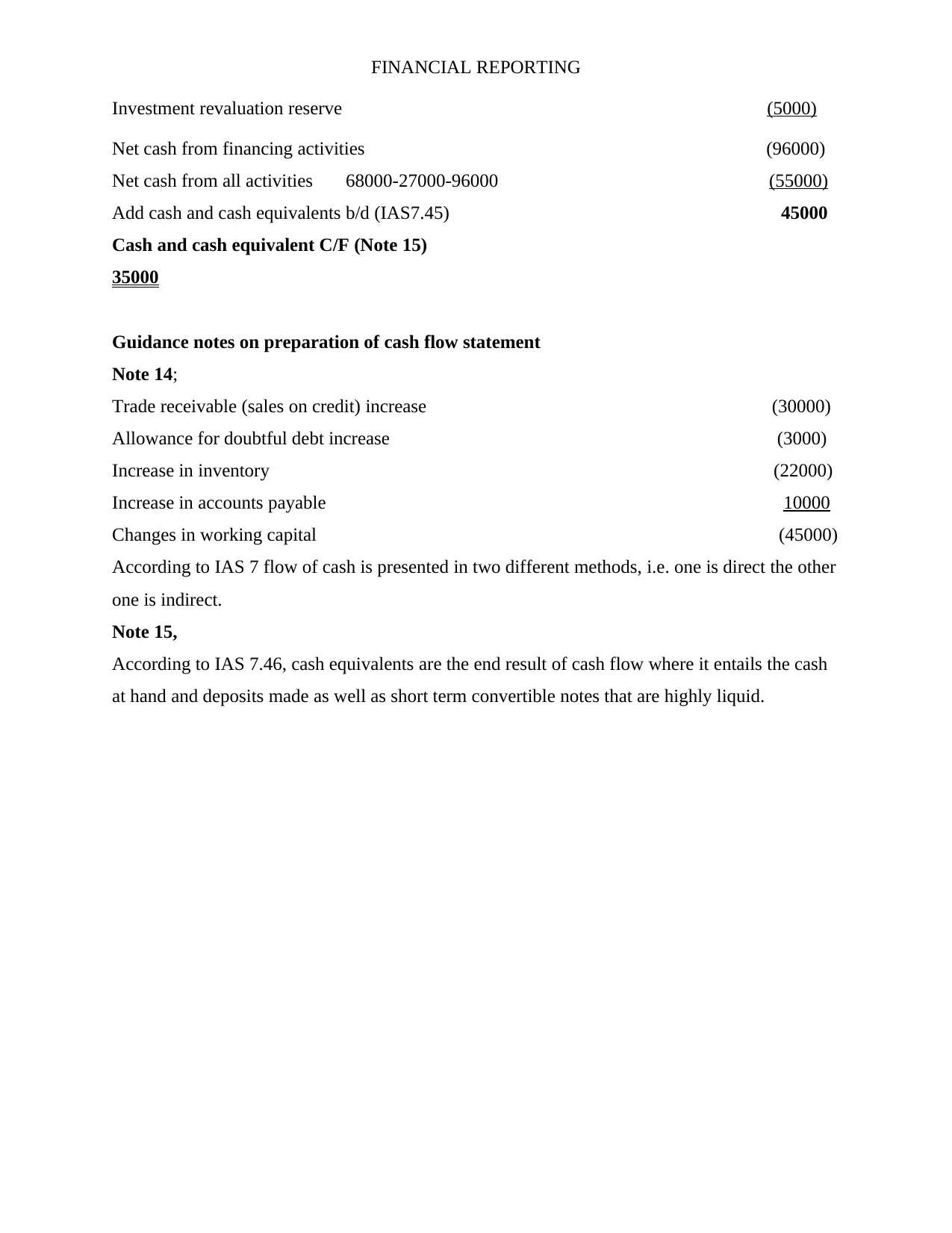

This assignment presents a comprehensive solution to a financial reporting problem, focusing on the preparation and analysis of financial statements. The solution adheres to International Financial Reporting Standards (IFRS) and Australian Accounting Standards (AASB). The first part of the assignment involves preparing a consolidated statement of profit or loss and other comprehensive income, a statement of changes in equity, and a statement of financial position for Park Ltd. Detailed notes are provided to explain the accounting concepts and regulations used in preparing these statements. The second part focuses on the preparation of a cash flow statement using both direct and indirect methods. The solution includes explanations and guidance notes for each statement, referencing relevant IAS and AASB standards. The assignment demonstrates the application of various accounting principles and the presentation of financial information in accordance with the required standards, offering a practical example for students studying financial reporting.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.