Detailed Analysis of Financial Reporting for Decision Making

VerifiedAdded on 2023/04/11

|11

|774

|201

Report

AI Summary

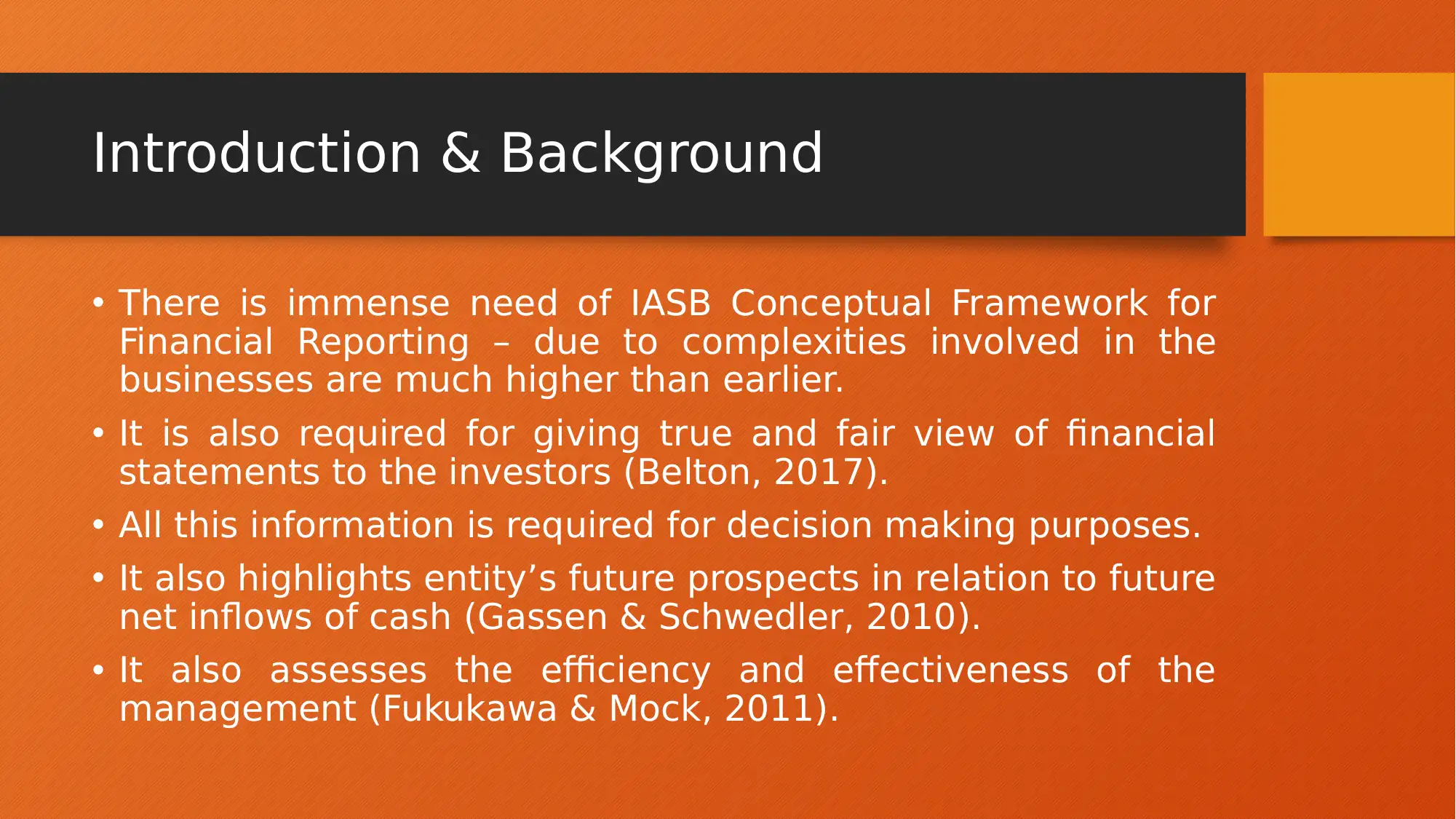

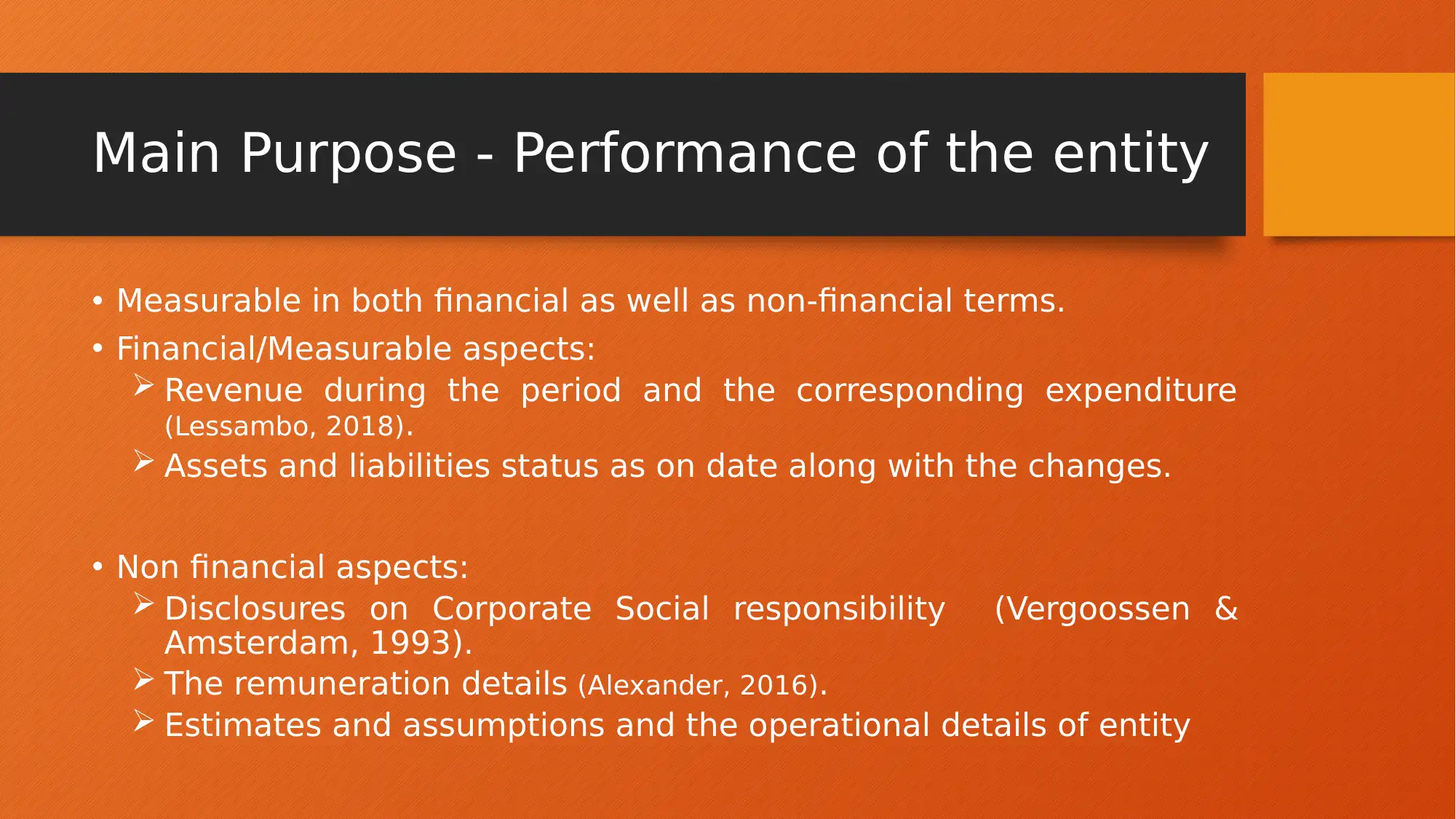

This report provides an overview of financial reporting, emphasizing its importance in today's complex business environment. It outlines the key purposes of financial reporting, including assessing an entity's performance in both financial and non-financial terms, such as revenue, expenditure, and corporate social responsibility. The report also details the significance of financial position disclosures, covering control over financial structure, resource details, and liquidity aspects. Furthermore, it examines the role of financial reporting in financing and investing activities, highlighting how stakeholders can understand fund procurement and investment strategies. Finally, the report addresses the compliance activities, ensuring that the entity adheres to all rules and regulations, as per the NZ Conceptual framework, thereby providing a comprehensive understanding of financial reporting's role in decision-making and stakeholder communication.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.