HA2032 Corporate and Financial Accounting Report: Analysis and Review

VerifiedAdded on 2023/06/04

|16

|3253

|131

Report

AI Summary

This report analyzes corporate accounting practices, focusing on the regulatory framework and financial reporting standards in Australia. It examines the importance of corporate regulations, arguing for their necessity in ensuring accurate and comparable financial information, while also discussing the role of the Australian Accounting Standards Board (AASB) in global accounting standard setting. The report then delves into the analysis of owners' equity for four selected telecommunication companies listed on the Australian Securities Exchange (ASX): Queste Communication, TPG Telecom, Vodafone PLC, and Singtel Optus Limited. It provides a detailed breakdown of equity components, including issued capital, reserves, and retained earnings, and analyzes the changes in these components over a four-year period for each company. The analysis highlights key trends and provides insights into the financial performance and position of these companies.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Authors Note:

Corporate Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Executive summary:

Corporates in Australia are under obligation to issue periodic financial statements to the

stakeholders of the company. The financial reporting and accounting of entities in the country

should be in accordance with the Corporations Act, 2001. Section 1.5.10 of the act provides the

requirements for companies to comply with annual financial reporting and auditing requirements

for entities in Australia. Especially entities listed in Australian Securities Exchange (ASX) must

in addition to the requirements of Corporations Act, 2001 shall also abide by the corporate

regulations for financial reporting as recommended by Australian Securities and Investments

Commission. A detailed discussion on financial reporting and various elements of financial

reporting in the document shall be helpful to the readers of the document.

CORPORATE ACCOUNTING

Executive summary:

Corporates in Australia are under obligation to issue periodic financial statements to the

stakeholders of the company. The financial reporting and accounting of entities in the country

should be in accordance with the Corporations Act, 2001. Section 1.5.10 of the act provides the

requirements for companies to comply with annual financial reporting and auditing requirements

for entities in Australia. Especially entities listed in Australian Securities Exchange (ASX) must

in addition to the requirements of Corporations Act, 2001 shall also abide by the corporate

regulations for financial reporting as recommended by Australian Securities and Investments

Commission. A detailed discussion on financial reporting and various elements of financial

reporting in the document shall be helpful to the readers of the document.

2

CORPORATE ACCOUNTING

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Corporate regulations:.....................................................................................................................3

Australian Accounting Standards Board’s Role in global accounting standards setting process:. .5

Owners’ equity:...............................................................................................................................7

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

CORPORATE ACCOUNTING

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Corporate regulations:.....................................................................................................................3

Australian Accounting Standards Board’s Role in global accounting standards setting process:. .5

Owners’ equity:...............................................................................................................................7

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

Introduction:

Corporate regulations are formulated to ensure that accounting and financial reporting in the

country are properly governed. Only a suitable accounting and financial reporting environment

in a country will ensure that the corporates in the country are following proper guidelines and

regulations to ensure correct reporting of its financial results and position. Four entities from

Telecommunication industry in Australia have been selected to complete the exercise given in

this document, these entities are Vodafone PLC, Queste Communication, TPG Telecom and

Singtel Optus Limited. All these four entities are listed in ASX.

Corporate regulations:

(i) Corporate regulations:

Corporate regulations are combined rules and regulations that the premier legislation of a

country recommends the companies to follow compulsorily in reporting accounting and financial

matters. In Australia Corporations Act, 2001 and rules mentioned by Australian Securities and

Investments Commission (ASIC) must be followed strictly by entities listed in ASX for

accounting and financial reporting. The reason the premier corporate legislation and corporate

regulator make corporate regulations to govern the financial reporting and accounting should be

evaluated to understand the needs to have such regulations in place (Schaltegger and Burritt,

2017).

Managing the diverse accounting principles and policies:

Accounting provides number of alternative accounting principles and policies that can be used to

maintain accounts of an entity. It is due to the inherent limitations of the subject that it is not

possible to have a single set of principles and policies to maintain accounts of an entity.

CORPORATE ACCOUNTING

Introduction:

Corporate regulations are formulated to ensure that accounting and financial reporting in the

country are properly governed. Only a suitable accounting and financial reporting environment

in a country will ensure that the corporates in the country are following proper guidelines and

regulations to ensure correct reporting of its financial results and position. Four entities from

Telecommunication industry in Australia have been selected to complete the exercise given in

this document, these entities are Vodafone PLC, Queste Communication, TPG Telecom and

Singtel Optus Limited. All these four entities are listed in ASX.

Corporate regulations:

(i) Corporate regulations:

Corporate regulations are combined rules and regulations that the premier legislation of a

country recommends the companies to follow compulsorily in reporting accounting and financial

matters. In Australia Corporations Act, 2001 and rules mentioned by Australian Securities and

Investments Commission (ASIC) must be followed strictly by entities listed in ASX for

accounting and financial reporting. The reason the premier corporate legislation and corporate

regulator make corporate regulations to govern the financial reporting and accounting should be

evaluated to understand the needs to have such regulations in place (Schaltegger and Burritt,

2017).

Managing the diverse accounting principles and policies:

Accounting provides number of alternative accounting principles and policies that can be used to

maintain accounts of an entity. It is due to the inherent limitations of the subject that it is not

possible to have a single set of principles and policies to maintain accounts of an entity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

Corporate regulations reduce the diverse set of principles and policies to ensure that the

accounting principles and policies are within manageable limits (Ioannou and Serafeim, 2017).

Scope manipulation by the accountants and management is reduced:

It is not possible to completely take away the personal and professional inputs of accountants and

management in accounting but with corporate regulations at place it is very much possible to

reduce the scope of manipulation in accounts. Thus, regulations are important to ensure

corporate accounts are not manipulated (Nobes, 2014).

Ensure compliance with financial reporting requirements:

The corporate regulations ensure compliance with the financial reporting requirements.

Companies must follow these regulations in order to prepare accounts as per the relevant

accounting standards. Only by following the regulations an entity will be able to show the actual

financial performance and position in its financial reports (Tricker and Tricker, 2015).

Deregulation will lead to chaos:

Allowing managers to voluntarily disclose information as per their preference would end up

creating a chaos in financial reporting. The financial reports will not disclose the actual results of

an organization instead would be a tool in the hands of the management to portray a picture of

the organization as per their choice (Eccles and Serafeim, 2015).

Apart from that deregulation in financial reporting and accounting to allow managers choice to

disclose financial information of their choice would lead to degradation of quality of financial

reporting. The whole purpose of enabling users to provide useful information in financial reports

would be defeated if corporate regulations are withdrawn (Leuz and Wysocki, 2016). The

CORPORATE ACCOUNTING

Corporate regulations reduce the diverse set of principles and policies to ensure that the

accounting principles and policies are within manageable limits (Ioannou and Serafeim, 2017).

Scope manipulation by the accountants and management is reduced:

It is not possible to completely take away the personal and professional inputs of accountants and

management in accounting but with corporate regulations at place it is very much possible to

reduce the scope of manipulation in accounts. Thus, regulations are important to ensure

corporate accounts are not manipulated (Nobes, 2014).

Ensure compliance with financial reporting requirements:

The corporate regulations ensure compliance with the financial reporting requirements.

Companies must follow these regulations in order to prepare accounts as per the relevant

accounting standards. Only by following the regulations an entity will be able to show the actual

financial performance and position in its financial reports (Tricker and Tricker, 2015).

Deregulation will lead to chaos:

Allowing managers to voluntarily disclose information as per their preference would end up

creating a chaos in financial reporting. The financial reports will not disclose the actual results of

an organization instead would be a tool in the hands of the management to portray a picture of

the organization as per their choice (Eccles and Serafeim, 2015).

Apart from that deregulation in financial reporting and accounting to allow managers choice to

disclose financial information of their choice would lead to degradation of quality of financial

reporting. The whole purpose of enabling users to provide useful information in financial reports

would be defeated if corporate regulations are withdrawn (Leuz and Wysocki, 2016). The

5

CORPORATE ACCOUNTING

financial statements would then be prepared as per the managers’ wish and since managers are

different of different organizations hence, different information would be reported by different

entities. As a result financial statements will not be comparable anymore.

Observation:

Taking into consideration the discussion about the importance of corporate regulations and the

possible issues that would be created subsequent to the withdrawal of corporate regulations in

financial reporting, it is observed that allowing managers to disclose financial information

voluntarily would deteriorate accounting and financial reporting quality (Christensen et. al

2015).

Australian Accounting Standards Board’s Role in global accounting standards setting

process:

(ii) Role of Australian Accounting Standards Board in global accounting standard

setting process:

The International Accounting Standards Board (IASB) as its members have National accounting

standard boards of different countries including the Australian Accounting Standards Board

(AASB) (Bamber and McMeeking, 2016). The International Financial Reporting Standards are

issued by the IASB in consultation with its members after following the procedure provided

below:

Setting the agenda:

Firstly, the IASB sets the agenda for development of new standard in consultation with its

members. AASB plays an important role in setting the agenda for IASB by actively participating

in the process (Walton, 2016).

CORPORATE ACCOUNTING

financial statements would then be prepared as per the managers’ wish and since managers are

different of different organizations hence, different information would be reported by different

entities. As a result financial statements will not be comparable anymore.

Observation:

Taking into consideration the discussion about the importance of corporate regulations and the

possible issues that would be created subsequent to the withdrawal of corporate regulations in

financial reporting, it is observed that allowing managers to disclose financial information

voluntarily would deteriorate accounting and financial reporting quality (Christensen et. al

2015).

Australian Accounting Standards Board’s Role in global accounting standards setting

process:

(ii) Role of Australian Accounting Standards Board in global accounting standard

setting process:

The International Accounting Standards Board (IASB) as its members have National accounting

standard boards of different countries including the Australian Accounting Standards Board

(AASB) (Bamber and McMeeking, 2016). The International Financial Reporting Standards are

issued by the IASB in consultation with its members after following the procedure provided

below:

Setting the agenda:

Firstly, the IASB sets the agenda for development of new standard in consultation with its

members. AASB plays an important role in setting the agenda for IASB by actively participating

in the process (Walton, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

Planning the project:

After setting the agenda it is important to plan the project to complete the development of new

standard. In planning phase along with other members of IASB, AASB gives its important inputs

to ensure that a proper plan can be made to successfully plan the development of a standard

(Pacter, 2014).

Development and publication of discussion paper:

Development of discussion paper based on the contributions from member countries of IASB

shall be made. It is then published for the comment form different stakeholders. AASB being one

of the important constituents of IASB provides technical support to develop discussion paper

(Aronoff and Ward, 2016).

Development and publication of exposure draft:

Based on the technical evaluation from the technical experts of IASB and verifying the

comments from different stakeholders, exposure draft for the new standard is developed and

published to the member countries including AASB and all other stakeholders. AASB provides

its valuable comments and suggestions during the development phase of new standard (Veblen,

2017).

Development of final draft of the new standard:

Based on the comments and suggestions from member countries and others stakeholders of new

standard the IASB develops the final draft of the standard. Once the standard is developed it is

published after consulting with member countries of IASB.

CORPORATE ACCOUNTING

Planning the project:

After setting the agenda it is important to plan the project to complete the development of new

standard. In planning phase along with other members of IASB, AASB gives its important inputs

to ensure that a proper plan can be made to successfully plan the development of a standard

(Pacter, 2014).

Development and publication of discussion paper:

Development of discussion paper based on the contributions from member countries of IASB

shall be made. It is then published for the comment form different stakeholders. AASB being one

of the important constituents of IASB provides technical support to develop discussion paper

(Aronoff and Ward, 2016).

Development and publication of exposure draft:

Based on the technical evaluation from the technical experts of IASB and verifying the

comments from different stakeholders, exposure draft for the new standard is developed and

published to the member countries including AASB and all other stakeholders. AASB provides

its valuable comments and suggestions during the development phase of new standard (Veblen,

2017).

Development of final draft of the new standard:

Based on the comments and suggestions from member countries and others stakeholders of new

standard the IASB develops the final draft of the standard. Once the standard is developed it is

published after consulting with member countries of IASB.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

AASB is an integral member of IASB and participates from setting agenda for new standard to

the development and publication of final standard. Thus, in each step of setting the global

accounting standards, AASB plays important and crucial role to ensure that the final draft is

suitable for the purpose to which it is developed and will improve the quality of financial

reporting.

Owners’ equity:

As the document has mentioned to select 4 listed entities of ASX from same industry to complete

detailed evaluation of owners’ equity the following four companies have been selected from

telecommunications industry in the country.

Queste Communication Limited: It is currently the fastest growing telecommunication company

in Australia with annual growth of over 400%.

TPG Telecom Limited: A relatively established firm in telecommunication industry it is known

for its quality services at relatively low prices.

Vodafone PLC: A telecom giant in all across the globe, Vodafone has significant market share in

the telecommunication industry in Australia. The company operates as Vodafone Australia in the

country (Mietzner and Schweizer, 2014).

SingTel Optus Limited: Another ASX Company, SingTel Optus is known for its quality of

services in telecommunication industry.

(iii) Each of item of equity and changes in items of equity:

Queste:

In the Balance sheet of the company the following items have been reported as owners’ equity:

CORPORATE ACCOUNTING

AASB is an integral member of IASB and participates from setting agenda for new standard to

the development and publication of final standard. Thus, in each step of setting the global

accounting standards, AASB plays important and crucial role to ensure that the final draft is

suitable for the purpose to which it is developed and will improve the quality of financial

reporting.

Owners’ equity:

As the document has mentioned to select 4 listed entities of ASX from same industry to complete

detailed evaluation of owners’ equity the following four companies have been selected from

telecommunications industry in the country.

Queste Communication Limited: It is currently the fastest growing telecommunication company

in Australia with annual growth of over 400%.

TPG Telecom Limited: A relatively established firm in telecommunication industry it is known

for its quality services at relatively low prices.

Vodafone PLC: A telecom giant in all across the globe, Vodafone has significant market share in

the telecommunication industry in Australia. The company operates as Vodafone Australia in the

country (Mietzner and Schweizer, 2014).

SingTel Optus Limited: Another ASX Company, SingTel Optus is known for its quality of

services in telecommunication industry.

(iii) Each of item of equity and changes in items of equity:

Queste:

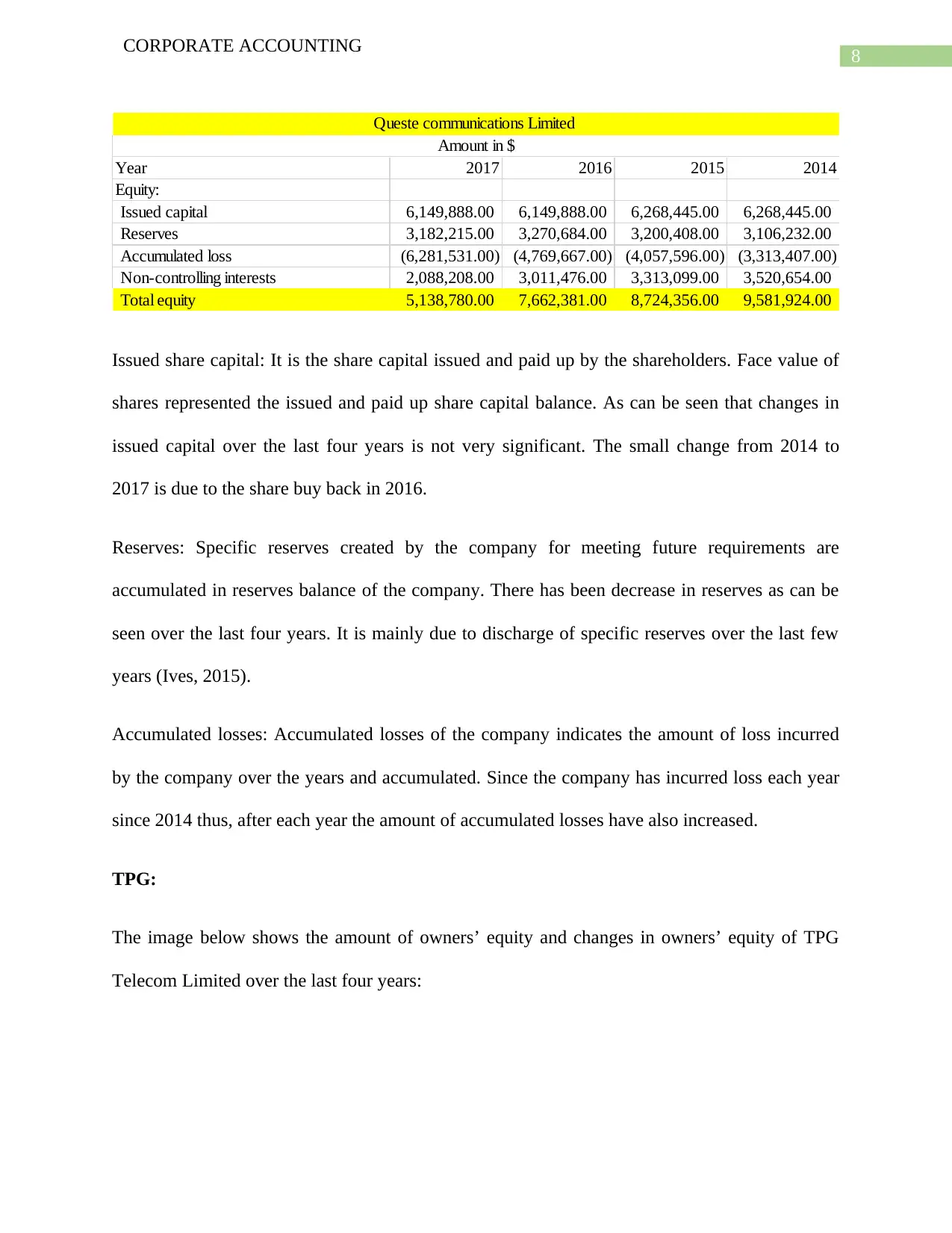

In the Balance sheet of the company the following items have been reported as owners’ equity:

8

CORPORATE ACCOUNTING

Year 2017 2016 2015 2014

Equity:

Issued capital 6,149,888.00 6,149,888.00 6,268,445.00 6,268,445.00

Reserves 3,182,215.00 3,270,684.00 3,200,408.00 3,106,232.00

Accumulated loss (6,281,531.00) (4,769,667.00) (4,057,596.00) (3,313,407.00)

Non-controlling interests 2,088,208.00 3,011,476.00 3,313,099.00 3,520,654.00

Total equity 5,138,780.00 7,662,381.00 8,724,356.00 9,581,924.00

Queste communications Limited

Amount in $

Issued share capital: It is the share capital issued and paid up by the shareholders. Face value of

shares represented the issued and paid up share capital balance. As can be seen that changes in

issued capital over the last four years is not very significant. The small change from 2014 to

2017 is due to the share buy back in 2016.

Reserves: Specific reserves created by the company for meeting future requirements are

accumulated in reserves balance of the company. There has been decrease in reserves as can be

seen over the last four years. It is mainly due to discharge of specific reserves over the last few

years (Ives, 2015).

Accumulated losses: Accumulated losses of the company indicates the amount of loss incurred

by the company over the years and accumulated. Since the company has incurred loss each year

since 2014 thus, after each year the amount of accumulated losses have also increased.

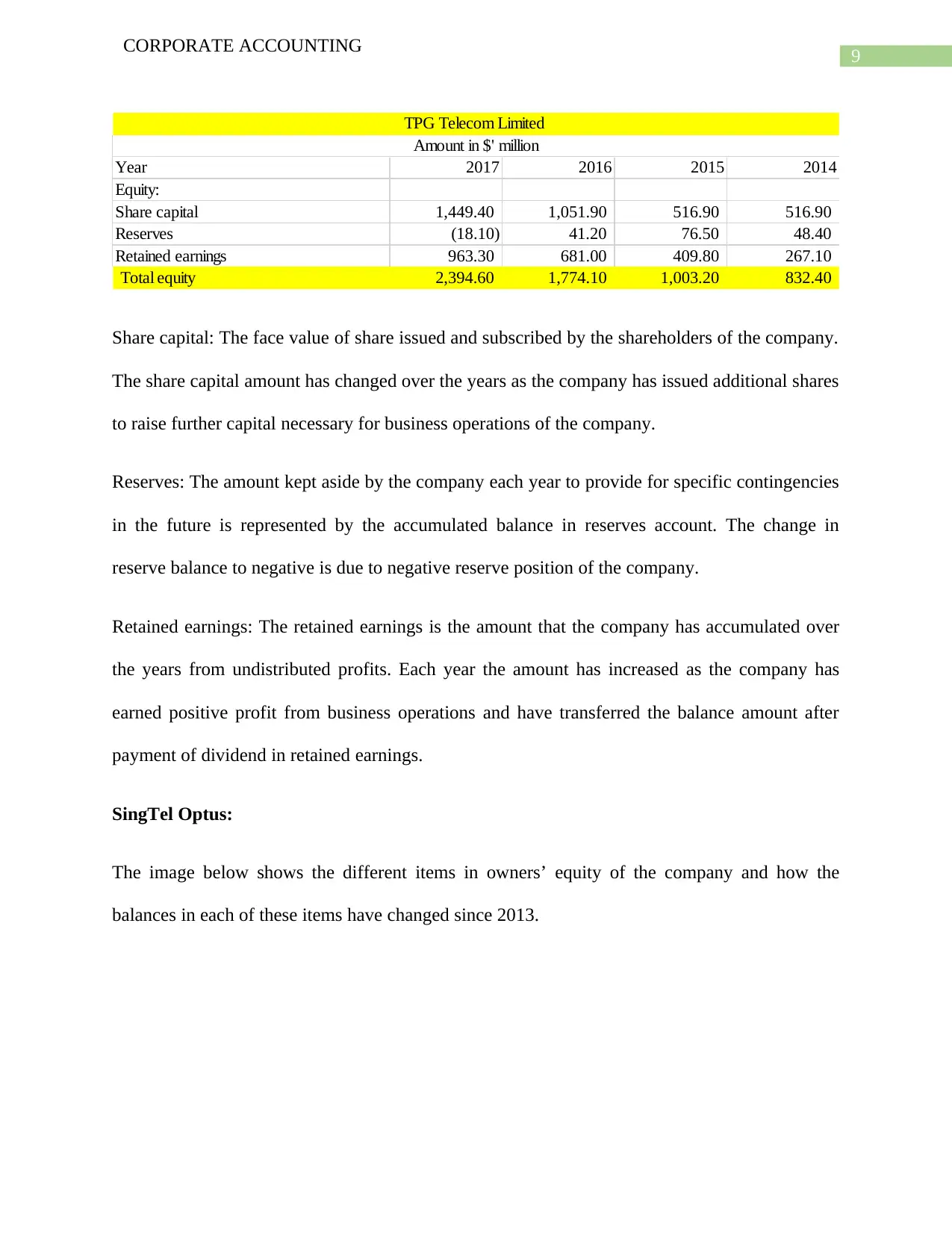

TPG:

The image below shows the amount of owners’ equity and changes in owners’ equity of TPG

Telecom Limited over the last four years:

CORPORATE ACCOUNTING

Year 2017 2016 2015 2014

Equity:

Issued capital 6,149,888.00 6,149,888.00 6,268,445.00 6,268,445.00

Reserves 3,182,215.00 3,270,684.00 3,200,408.00 3,106,232.00

Accumulated loss (6,281,531.00) (4,769,667.00) (4,057,596.00) (3,313,407.00)

Non-controlling interests 2,088,208.00 3,011,476.00 3,313,099.00 3,520,654.00

Total equity 5,138,780.00 7,662,381.00 8,724,356.00 9,581,924.00

Queste communications Limited

Amount in $

Issued share capital: It is the share capital issued and paid up by the shareholders. Face value of

shares represented the issued and paid up share capital balance. As can be seen that changes in

issued capital over the last four years is not very significant. The small change from 2014 to

2017 is due to the share buy back in 2016.

Reserves: Specific reserves created by the company for meeting future requirements are

accumulated in reserves balance of the company. There has been decrease in reserves as can be

seen over the last four years. It is mainly due to discharge of specific reserves over the last few

years (Ives, 2015).

Accumulated losses: Accumulated losses of the company indicates the amount of loss incurred

by the company over the years and accumulated. Since the company has incurred loss each year

since 2014 thus, after each year the amount of accumulated losses have also increased.

TPG:

The image below shows the amount of owners’ equity and changes in owners’ equity of TPG

Telecom Limited over the last four years:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

Year 2017 2016 2015 2014

Equity:

Share capital 1,449.40 1,051.90 516.90 516.90

Reserves (18.10) 41.20 76.50 48.40

Retained earnings 963.30 681.00 409.80 267.10

Total equity 2,394.60 1,774.10 1,003.20 832.40

TPG Telecom Limited

Amount in $' million

Share capital: The face value of share issued and subscribed by the shareholders of the company.

The share capital amount has changed over the years as the company has issued additional shares

to raise further capital necessary for business operations of the company.

Reserves: The amount kept aside by the company each year to provide for specific contingencies

in the future is represented by the accumulated balance in reserves account. The change in

reserve balance to negative is due to negative reserve position of the company.

Retained earnings: The retained earnings is the amount that the company has accumulated over

the years from undistributed profits. Each year the amount has increased as the company has

earned positive profit from business operations and have transferred the balance amount after

payment of dividend in retained earnings.

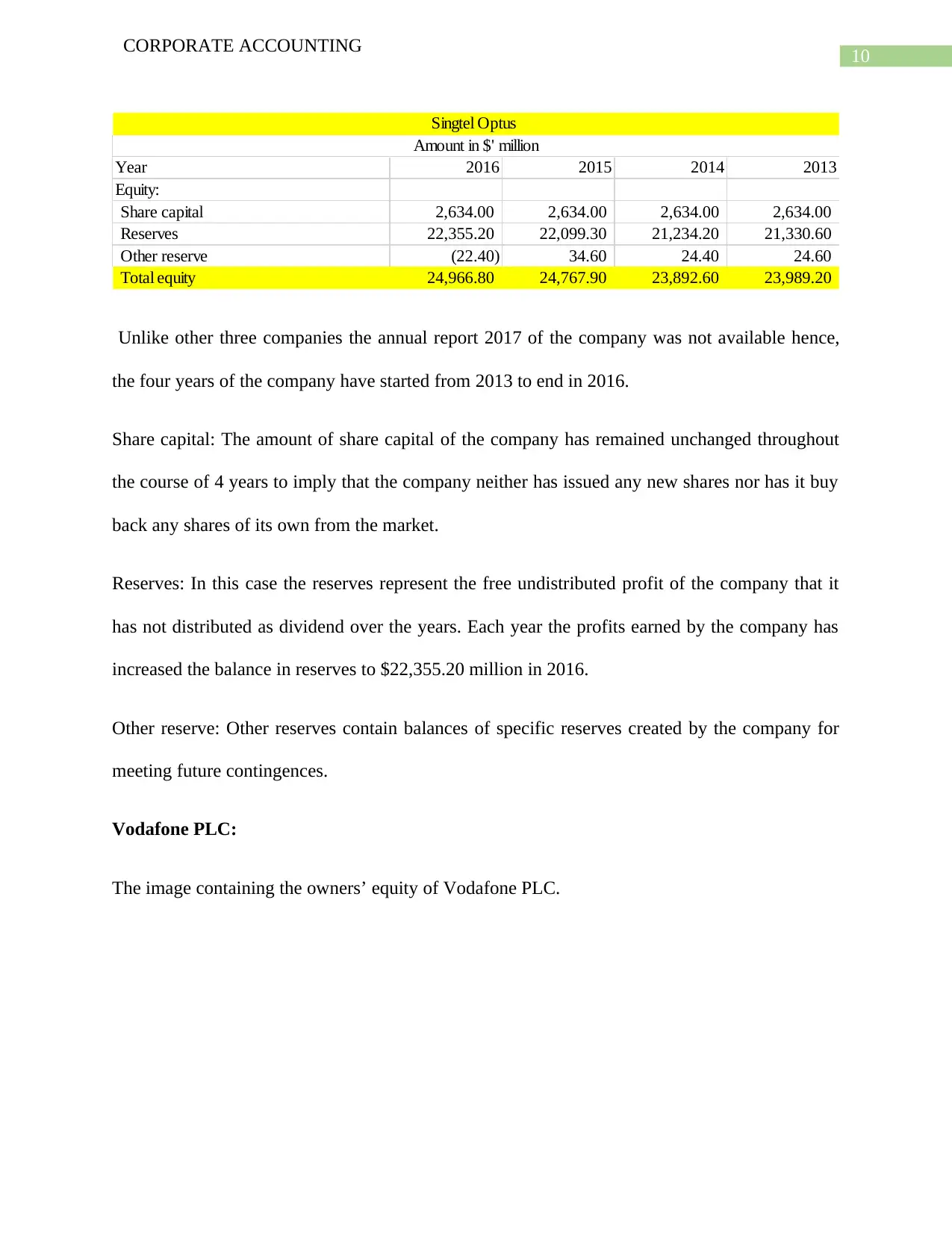

SingTel Optus:

The image below shows the different items in owners’ equity of the company and how the

balances in each of these items have changed since 2013.

CORPORATE ACCOUNTING

Year 2017 2016 2015 2014

Equity:

Share capital 1,449.40 1,051.90 516.90 516.90

Reserves (18.10) 41.20 76.50 48.40

Retained earnings 963.30 681.00 409.80 267.10

Total equity 2,394.60 1,774.10 1,003.20 832.40

TPG Telecom Limited

Amount in $' million

Share capital: The face value of share issued and subscribed by the shareholders of the company.

The share capital amount has changed over the years as the company has issued additional shares

to raise further capital necessary for business operations of the company.

Reserves: The amount kept aside by the company each year to provide for specific contingencies

in the future is represented by the accumulated balance in reserves account. The change in

reserve balance to negative is due to negative reserve position of the company.

Retained earnings: The retained earnings is the amount that the company has accumulated over

the years from undistributed profits. Each year the amount has increased as the company has

earned positive profit from business operations and have transferred the balance amount after

payment of dividend in retained earnings.

SingTel Optus:

The image below shows the different items in owners’ equity of the company and how the

balances in each of these items have changed since 2013.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

Year 2016 2015 2014 2013

Equity:

Share capital 2,634.00 2,634.00 2,634.00 2,634.00

Reserves 22,355.20 22,099.30 21,234.20 21,330.60

Other reserve (22.40) 34.60 24.40 24.60

Total equity 24,966.80 24,767.90 23,892.60 23,989.20

Singtel Optus

Amount in $' million

Unlike other three companies the annual report 2017 of the company was not available hence,

the four years of the company have started from 2013 to end in 2016.

Share capital: The amount of share capital of the company has remained unchanged throughout

the course of 4 years to imply that the company neither has issued any new shares nor has it buy

back any shares of its own from the market.

Reserves: In this case the reserves represent the free undistributed profit of the company that it

has not distributed as dividend over the years. Each year the profits earned by the company has

increased the balance in reserves to $22,355.20 million in 2016.

Other reserve: Other reserves contain balances of specific reserves created by the company for

meeting future contingences.

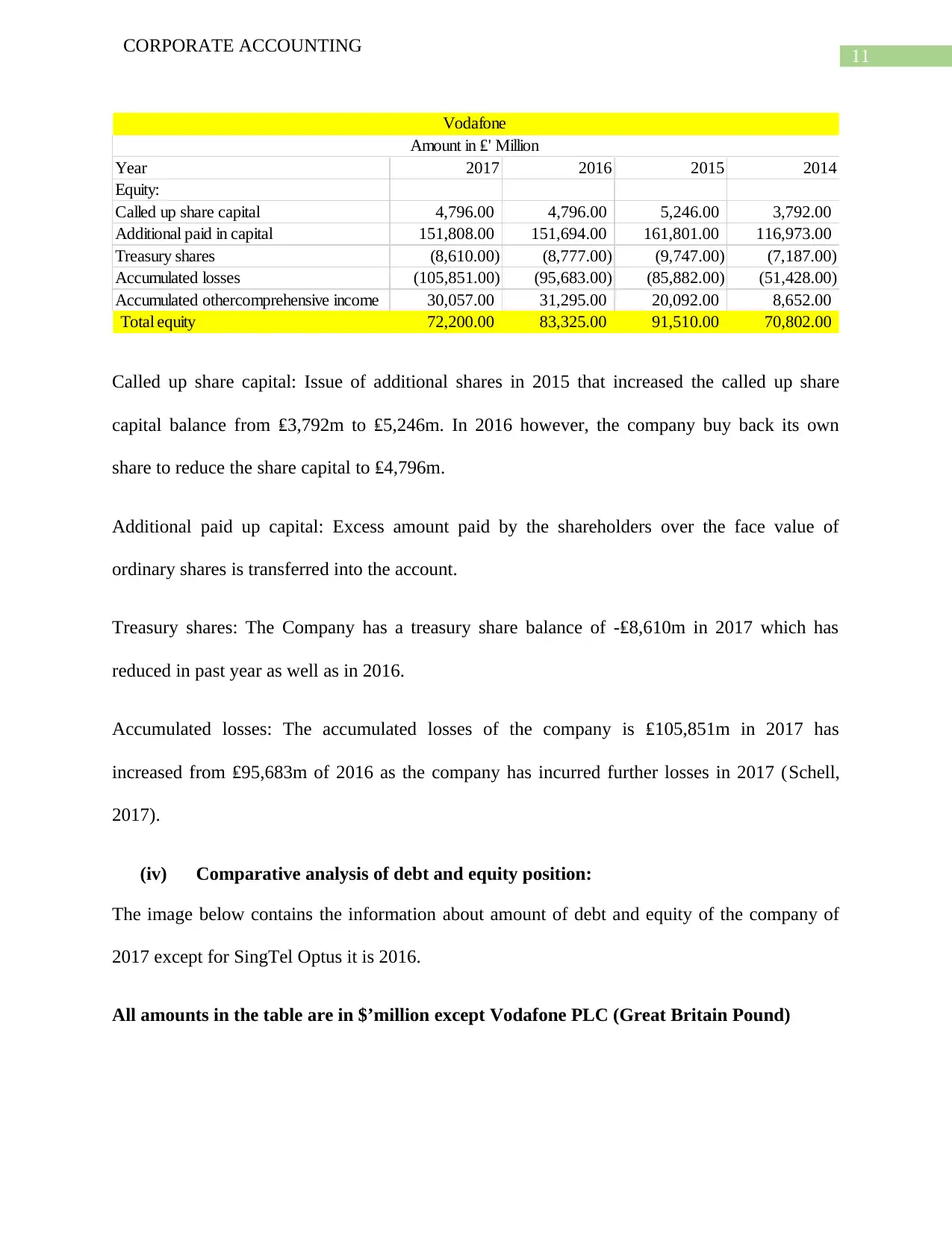

Vodafone PLC:

The image containing the owners’ equity of Vodafone PLC.

CORPORATE ACCOUNTING

Year 2016 2015 2014 2013

Equity:

Share capital 2,634.00 2,634.00 2,634.00 2,634.00

Reserves 22,355.20 22,099.30 21,234.20 21,330.60

Other reserve (22.40) 34.60 24.40 24.60

Total equity 24,966.80 24,767.90 23,892.60 23,989.20

Singtel Optus

Amount in $' million

Unlike other three companies the annual report 2017 of the company was not available hence,

the four years of the company have started from 2013 to end in 2016.

Share capital: The amount of share capital of the company has remained unchanged throughout

the course of 4 years to imply that the company neither has issued any new shares nor has it buy

back any shares of its own from the market.

Reserves: In this case the reserves represent the free undistributed profit of the company that it

has not distributed as dividend over the years. Each year the profits earned by the company has

increased the balance in reserves to $22,355.20 million in 2016.

Other reserve: Other reserves contain balances of specific reserves created by the company for

meeting future contingences.

Vodafone PLC:

The image containing the owners’ equity of Vodafone PLC.

11

CORPORATE ACCOUNTING

Year 2017 2016 2015 2014

Equity:

Called up share capital 4,796.00 4,796.00 5,246.00 3,792.00

Additional paid in capital 151,808.00 151,694.00 161,801.00 116,973.00

Treasury shares (8,610.00) (8,777.00) (9,747.00) (7,187.00)

Accumulated losses (105,851.00) (95,683.00) (85,882.00) (51,428.00)

Accumulated othercomprehensive income 30,057.00 31,295.00 20,092.00 8,652.00

Total equity 72,200.00 83,325.00 91,510.00 70,802.00

Vodafone

Amount in ₤' Million

Called up share capital: Issue of additional shares in 2015 that increased the called up share

capital balance from ₤3,792m to ₤5,246m. In 2016 however, the company buy back its own

share to reduce the share capital to ₤4,796m.

Additional paid up capital: Excess amount paid by the shareholders over the face value of

ordinary shares is transferred into the account.

Treasury shares: The Company has a treasury share balance of -₤8,610m in 2017 which has

reduced in past year as well as in 2016.

Accumulated losses: The accumulated losses of the company is ₤105,851m in 2017 has

increased from ₤95,683m of 2016 as the company has incurred further losses in 2017 (Schell,

2017).

(iv) Comparative analysis of debt and equity position:

The image below contains the information about amount of debt and equity of the company of

2017 except for SingTel Optus it is 2016.

All amounts in the table are in $’million except Vodafone PLC (Great Britain Pound)

CORPORATE ACCOUNTING

Year 2017 2016 2015 2014

Equity:

Called up share capital 4,796.00 4,796.00 5,246.00 3,792.00

Additional paid in capital 151,808.00 151,694.00 161,801.00 116,973.00

Treasury shares (8,610.00) (8,777.00) (9,747.00) (7,187.00)

Accumulated losses (105,851.00) (95,683.00) (85,882.00) (51,428.00)

Accumulated othercomprehensive income 30,057.00 31,295.00 20,092.00 8,652.00

Total equity 72,200.00 83,325.00 91,510.00 70,802.00

Vodafone

Amount in ₤' Million

Called up share capital: Issue of additional shares in 2015 that increased the called up share

capital balance from ₤3,792m to ₤5,246m. In 2016 however, the company buy back its own

share to reduce the share capital to ₤4,796m.

Additional paid up capital: Excess amount paid by the shareholders over the face value of

ordinary shares is transferred into the account.

Treasury shares: The Company has a treasury share balance of -₤8,610m in 2017 which has

reduced in past year as well as in 2016.

Accumulated losses: The accumulated losses of the company is ₤105,851m in 2017 has

increased from ₤95,683m of 2016 as the company has incurred further losses in 2017 (Schell,

2017).

(iv) Comparative analysis of debt and equity position:

The image below contains the information about amount of debt and equity of the company of

2017 except for SingTel Optus it is 2016.

All amounts in the table are in $’million except Vodafone PLC (Great Britain Pound)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.