Financial Reporting: Framework, Statements, and Analysis Report

VerifiedAdded on 2020/06/03

|16

|4365

|119

Report

AI Summary

This report provides a comprehensive overview of financial reporting, covering key aspects such as the context and purpose of financial reporting, the conceptual and regulatory framework, and the major stakeholders of an organization. It delves into the importance of financial reporting for meeting organizational objectives and growth, exploring financial statements like the income statement, balance sheet, and cash flow statement, and their role in interpreting and communicating financial performance. The report also compares IAS and IFRS, evaluates the benefits of IFRS, and discusses the degree of IFRS compliance, including factors influencing compliance. Furthermore, it includes a ratio analysis of Tesco to reflect how financial results are reported in corporate sectors, aiding managers in making business decisions. The report emphasizes the significance of financial reporting for stakeholders such as managers, shareholders, creditors, government, and employees.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

INTRODUCTION.......................................................................................................................................3

(1)Context and purpose of financial reporting.........................................................................................3

(2) Conceptual and regulatory framework requirement, purpose and key principles...............................4

(3) Major stakeholder of organization and benefits they derive from financial information....................6

(4)Importance of financial reporting for meeting organization objectives and growth............................7

(5)Financial statements of companies and difference between cash flow statement, income statement

and balance sheet.....................................................................................................................................8

(6) Way in which financial statements are use to interpret and communicate financial performance....12

(7)Difference between IAS and IFRS....................................................................................................13

(8) Evaluate benefits of IFRS................................................................................................................13

(9) Degree to which organizations are complying with IFRS and factors in nation that may impact

compliance............................................................................................................................................13

CONCLUSION.........................................................................................................................................14

REFERENCES..........................................................................................................................................15

INTRODUCTION.......................................................................................................................................3

(1)Context and purpose of financial reporting.........................................................................................3

(2) Conceptual and regulatory framework requirement, purpose and key principles...............................4

(3) Major stakeholder of organization and benefits they derive from financial information....................6

(4)Importance of financial reporting for meeting organization objectives and growth............................7

(5)Financial statements of companies and difference between cash flow statement, income statement

and balance sheet.....................................................................................................................................8

(6) Way in which financial statements are use to interpret and communicate financial performance....12

(7)Difference between IAS and IFRS....................................................................................................13

(8) Evaluate benefits of IFRS................................................................................................................13

(9) Degree to which organizations are complying with IFRS and factors in nation that may impact

compliance............................................................................................................................................13

CONCLUSION.........................................................................................................................................14

REFERENCES..........................................................................................................................................15

INTRODUCTION

Financial reporting is the one of the major topic on which lots of discussions are carried

out on varied forums. In the present research study deep discussion is carried out on financial

reporting. Report is classified in to varied parts that cover topics and discussion related to

financial reporting, regulatory framework requirements and stakeholders. Apart from this, detail

discussion is carried out on financial statements of companies like income statement, balance

sheet and cash flow statement. In the report comparison is done between these financial

statements and difference between them is explained in detail. Ratio analysis of Tesco is done in

order to reflect way in which financial results are reported in corporate sectors in order to assist

mangers in making business decisions. Apart from financial reporting IFRS and IAS are also

considered one of the most important topics. Inn present research study IFRS and IAS are

compared with each other and benefits of IFRS are explained. Factors due to which IFRS does

not implement in nations in systematic manner is also discussed in detail at end of the report. It

can be said that vast amount of things are discussed in detail in present research study.

(1)Context and purpose of financial reporting

Financial reporting refers to the practice under which financial statements are produced in

order to disclose company financial performance. Preparation of income statement and balance

sheet are one of best examples of financial reporting. There are number of purpose of financial

reporting and maintaining a very close eye on business is one of them. Usually, business is

affected by number of factors like business environment and other factors. It is impossible for

managers to estimate likely impact that these factors have on business firm cash flows. Thus,

due to this reason financial reporting is necessary (Council, 2010). Under this varied techniques

are used like cash flow statement where cash flows are segregate in different categories like cash

flow from operations, financial and investment activities. Different statements that are prepared

under financial reporting and purpose behind their preparation is explained below. Income statement: It is one of the most important statements that is prepared by the

business firms. Reason for preparing income statement is to identify profit or loss that is

gained by the business firm. Other main purpose of financial reporting is to identify

trends that are going on in terms of making expenditure in the business. Income statement

Financial reporting is the one of the major topic on which lots of discussions are carried

out on varied forums. In the present research study deep discussion is carried out on financial

reporting. Report is classified in to varied parts that cover topics and discussion related to

financial reporting, regulatory framework requirements and stakeholders. Apart from this, detail

discussion is carried out on financial statements of companies like income statement, balance

sheet and cash flow statement. In the report comparison is done between these financial

statements and difference between them is explained in detail. Ratio analysis of Tesco is done in

order to reflect way in which financial results are reported in corporate sectors in order to assist

mangers in making business decisions. Apart from financial reporting IFRS and IAS are also

considered one of the most important topics. Inn present research study IFRS and IAS are

compared with each other and benefits of IFRS are explained. Factors due to which IFRS does

not implement in nations in systematic manner is also discussed in detail at end of the report. It

can be said that vast amount of things are discussed in detail in present research study.

(1)Context and purpose of financial reporting

Financial reporting refers to the practice under which financial statements are produced in

order to disclose company financial performance. Preparation of income statement and balance

sheet are one of best examples of financial reporting. There are number of purpose of financial

reporting and maintaining a very close eye on business is one of them. Usually, business is

affected by number of factors like business environment and other factors. It is impossible for

managers to estimate likely impact that these factors have on business firm cash flows. Thus,

due to this reason financial reporting is necessary (Council, 2010). Under this varied techniques

are used like cash flow statement where cash flows are segregate in different categories like cash

flow from operations, financial and investment activities. Different statements that are prepared

under financial reporting and purpose behind their preparation is explained below. Income statement: It is one of the most important statements that is prepared by the

business firms. Reason for preparing income statement is to identify profit or loss that is

gained by the business firm. Other main purpose of financial reporting is to identify

trends that are going on in terms of making expenditure in the business. Income statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is the one of the important component of financial reporting method. In the annual report

different annexure are prepared and under this detail calculations are revealed that are

used to compute final values of variables that are in balance sheet (Beyer and et.al.,

2010). It can be said that income statement is the one of the most important statement that

is prepared by the business firms. Balance sheet: Balance sheet is the one of the important statement that is prepared by

every type of firm irrespective of their size whether it is small, medium or big in size.

Balance sheet reflects financial position of company and it is one of the most important

elements of financial reporting. Reporting and identification of financial health of firm is

the one of the main purpose behind preparing balance sheet. In corporate reporting

usually many ratios are computed by using information that is provided in the balance

sheet. On this basis financial condition of the firm is measured. Cash flow statement: Cash flow statement is usually prepared by large size business

firms in order to identify cash flow from operations, investing and financing activity. It is

very hard task to estimate likely cash flow that is happened from these different sorts of

activities. Main purpose of preparing cash flow statement in financial reporting is to

communicate managers net cash balance that remain after adjusting cash flows from

different sort of activities (Li, 2010). It can be said that cash flow statement is one of the

main statement that is integral part of financial reporting. It can be said that there are lots

of benefits of financial reporting for the business firms. It helps managers in making

prudent decisions for benefit of an organization.

(2) Conceptual and regulatory framework requirement, purpose and key principles

Conceptual framework refers to basic concepts that are used for preparation and

presentation of financial statements. In other words it can be said that under conceptual

framework there are some concepts that are strictly followed for preparing financial reports.

Main purpose behind preparing such kind of conceptual framework is to ensure that there are

certain concepts that will be followed by the business firms to report their results in systematic

manner. It can be said that this ensure that financials will be reported in best manner. There are

three principles of financial reporting and same are explained below.

different annexure are prepared and under this detail calculations are revealed that are

used to compute final values of variables that are in balance sheet (Beyer and et.al.,

2010). It can be said that income statement is the one of the most important statement that

is prepared by the business firms. Balance sheet: Balance sheet is the one of the important statement that is prepared by

every type of firm irrespective of their size whether it is small, medium or big in size.

Balance sheet reflects financial position of company and it is one of the most important

elements of financial reporting. Reporting and identification of financial health of firm is

the one of the main purpose behind preparing balance sheet. In corporate reporting

usually many ratios are computed by using information that is provided in the balance

sheet. On this basis financial condition of the firm is measured. Cash flow statement: Cash flow statement is usually prepared by large size business

firms in order to identify cash flow from operations, investing and financing activity. It is

very hard task to estimate likely cash flow that is happened from these different sorts of

activities. Main purpose of preparing cash flow statement in financial reporting is to

communicate managers net cash balance that remain after adjusting cash flows from

different sort of activities (Li, 2010). It can be said that cash flow statement is one of the

main statement that is integral part of financial reporting. It can be said that there are lots

of benefits of financial reporting for the business firms. It helps managers in making

prudent decisions for benefit of an organization.

(2) Conceptual and regulatory framework requirement, purpose and key principles

Conceptual framework refers to basic concepts that are used for preparation and

presentation of financial statements. In other words it can be said that under conceptual

framework there are some concepts that are strictly followed for preparing financial reports.

Main purpose behind preparing such kind of conceptual framework is to ensure that there are

certain concepts that will be followed by the business firms to report their results in systematic

manner. It can be said that this ensure that financials will be reported in best manner. There are

three principles of financial reporting and same are explained below.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Principle 1: First principle of financial reporting state that most relevant information

about elements of business must be reflected in the income statement, balance sheet and

cash flow statement. In financial reports it must also be reflected the way in which top

management of the business firm discharge its responsibilities in proper manner at

workplace. Principle 2: Relevance of any financial item depends on the extent to which it affects

financial statements like income statement, balance sheet and cash flow statement. Means

that for financial reporting purpose if anyone wants to include any item in the financial

statements then in that case it must ensure that proposed included item is relevant and

will affect financial statements in right manner. Principle 3: While including any item in income statement, balance sheet and cash flow

statement it must be identified whether it will be relevant for the potential investor’s

lender and shareholder etc (Armstrong, Guay and Weber, 2010). This is because main

purpose behind preparing these statements is to provide more and more information to

stakeholders and this problem can be solved only when all relevant information’s will be

available to them on single statement.

There are strong regulatory requirements of the business firms because it is important for them to

follow all relevant rules and regulations very tightly. It can be observed that with passage of time

many changes are made in regulations that are in respect to reporting of financial facts and

figures. Firms need to follow these regulations very tightly in order to ensure that they are

reporting results in best manner and according to requirements. Main purpose behind regulatory

framework is to ensure that no firm will be able mislead its stakeholders and true as well as full

amount of required information will be available to them. It can be said that there is huge

importance financial and regulatory framework for the business firms. Qualitative characteristics

make financial information more reliable. It must be noted that relevance and faithful

representation are the two most important qualitative characteristics that make financial

information more reliable. It is very important to ensure that in each and every element that is in

the financial statements there must be some qualitative characteristics. This is because if

information will be reliable then in that case financial statements that are prepared by the

business firm will be reliable (Barth and Landsman, 2010). Reliability of information can be

determine by ensuring that only relevant information is taken in to consideration for preparing

about elements of business must be reflected in the income statement, balance sheet and

cash flow statement. In financial reports it must also be reflected the way in which top

management of the business firm discharge its responsibilities in proper manner at

workplace. Principle 2: Relevance of any financial item depends on the extent to which it affects

financial statements like income statement, balance sheet and cash flow statement. Means

that for financial reporting purpose if anyone wants to include any item in the financial

statements then in that case it must ensure that proposed included item is relevant and

will affect financial statements in right manner. Principle 3: While including any item in income statement, balance sheet and cash flow

statement it must be identified whether it will be relevant for the potential investor’s

lender and shareholder etc (Armstrong, Guay and Weber, 2010). This is because main

purpose behind preparing these statements is to provide more and more information to

stakeholders and this problem can be solved only when all relevant information’s will be

available to them on single statement.

There are strong regulatory requirements of the business firms because it is important for them to

follow all relevant rules and regulations very tightly. It can be observed that with passage of time

many changes are made in regulations that are in respect to reporting of financial facts and

figures. Firms need to follow these regulations very tightly in order to ensure that they are

reporting results in best manner and according to requirements. Main purpose behind regulatory

framework is to ensure that no firm will be able mislead its stakeholders and true as well as full

amount of required information will be available to them. It can be said that there is huge

importance financial and regulatory framework for the business firms. Qualitative characteristics

make financial information more reliable. It must be noted that relevance and faithful

representation are the two most important qualitative characteristics that make financial

information more reliable. It is very important to ensure that in each and every element that is in

the financial statements there must be some qualitative characteristics. This is because if

information will be reliable then in that case financial statements that are prepared by the

business firm will be reliable (Barth and Landsman, 2010). Reliability of information can be

determine by ensuring that only relevant information is taken in to consideration for preparing

financial statements. Faithful information is another important qualitative characteristic that must

be followed while including any element or item in the income statement. This is because if

information will not be faithful then in that case it will be difficult to make financial statements

in proper manner. Thus, it can be said that these two qualitative characteristics have due

importance for the business firms and while including any element or factor in financial

statements it must be ensured that they are relevant and faithful in nature.

(3) Major stakeholder of organization and benefits they derive from financial information

Stakeholders are the entities that give boost to growth of any business firm. There are

number of stakeholders of business firm and it is very important to satisfy them by fulfilling their

interests. This is because they support an organization whenever they required. Thus, it is very

important to take care of stakeholders. Some of the stakeholders of the business firm are given

below. Manager: Managers are considered as one of the most important stakeholders of Tesco

then other stakeholders. This is because these are those who manage business at middle

level. Entire business operations remain in their hand and they play a very important role

in growth of an organization. Financial statements matter a lot for the managers because

on the basis of financial statements they come to know whether firm is performing well

or not. On the basis of information obtained mangers decide the direction in which they

need to work for benefit of an organization. Thus, it can be said that managers have a due

importance as stakeholder for the business firm. Shareholder: Shareholders are another important stakeholder of the business firm. These

are those entities that make investment in the firm and become its owners. Shareholders

have right to make decisions related to business and due to this reason financial

statements matter a lot for them. On the basis of condition reflected by financial

statements shareholders decide whether they must keep investment in the firm or pull

back investment amount (Chen and et.al., 2011). Thus, financial statement matter a lot for

shareholders. Apart from this, shareholders have right to participate in annual general

meeting of firm. In this meeting shareholders on the basis of obtained financial

information can give vote in support of business plan presented by CEO or can vote

be followed while including any element or item in the income statement. This is because if

information will not be faithful then in that case it will be difficult to make financial statements

in proper manner. Thus, it can be said that these two qualitative characteristics have due

importance for the business firms and while including any element or factor in financial

statements it must be ensured that they are relevant and faithful in nature.

(3) Major stakeholder of organization and benefits they derive from financial information

Stakeholders are the entities that give boost to growth of any business firm. There are

number of stakeholders of business firm and it is very important to satisfy them by fulfilling their

interests. This is because they support an organization whenever they required. Thus, it is very

important to take care of stakeholders. Some of the stakeholders of the business firm are given

below. Manager: Managers are considered as one of the most important stakeholders of Tesco

then other stakeholders. This is because these are those who manage business at middle

level. Entire business operations remain in their hand and they play a very important role

in growth of an organization. Financial statements matter a lot for the managers because

on the basis of financial statements they come to know whether firm is performing well

or not. On the basis of information obtained mangers decide the direction in which they

need to work for benefit of an organization. Thus, it can be said that managers have a due

importance as stakeholder for the business firm. Shareholder: Shareholders are another important stakeholder of the business firm. These

are those entities that make investment in the firm and become its owners. Shareholders

have right to make decisions related to business and due to this reason financial

statements matter a lot for them. On the basis of condition reflected by financial

statements shareholders decide whether they must keep investment in the firm or pull

back investment amount (Chen and et.al., 2011). Thus, financial statement matter a lot for

shareholders. Apart from this, shareholders have right to participate in annual general

meeting of firm. In this meeting shareholders on the basis of obtained financial

information can give vote in support of business plan presented by CEO or can vote

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

against it. Thus, shareholders need financial information to great extent to make

decisions. Creditors: Creditors are another important stakeholder of the business firm as these are

entities that give credit to the business firm. They needed income statement and balance

sheet because on that basis they identify firm financial condition and by computing ratios

identify whether firm will be able to pay debt amount of time. By accessing condition

they identify whether loan given by them to Tesco is secured and will be repaid on time.

Thus, it can be said that financial statements have due importance for creditors. Government: Government is another important stakeholder of the business firm because

it receive tax from the profit amount that is earned by the business firm from its

operations. Government needed income statement and balance sheet in order to determine

that right amount of tax is paid to it (Altamuro and Beatty, 2010). Thus, it also needed

financial statement of the business firm. Employees: Employees are also considered as stakeholder of business because they

operate day to day firm operations. On the basis of financial statements they identify firm

condition and in case of critical condition identify whether firm will be able to pay their

salary on time.

(4)Importance of financial reporting for meeting organization objectives and growth

There is huge importance of financial reporting for the business firm because it help it in

achieving organization objectives and growth in business. This is because in financial report

different sort of statements like income statement, balance sheet and cash flow statement is

prepared. Managers analyze these statements deeply and identify firm financial condition. On the

basis of accessed condition direction in which work need to be done is identified and strategy is

formulated to achieve pre determined objectives. In case objective is achieved it pave a way of

growth for the business firm. Thus, it can be said that financial reporting have due importance for

meeting organization objectives and growth. In current time period most of business firms are

giving due emphasis on best use of results that are obtained from financial reporting. This is

because business conditions now become highly complex and due to this reason it is very

difficult task to pay attention on each and every weak point. Financial reporting ensured that only

relevant information and those need due attention of managers highlighted. Thus, clearly

managers get an input about direction in which they really need to work for benefit of an

decisions. Creditors: Creditors are another important stakeholder of the business firm as these are

entities that give credit to the business firm. They needed income statement and balance

sheet because on that basis they identify firm financial condition and by computing ratios

identify whether firm will be able to pay debt amount of time. By accessing condition

they identify whether loan given by them to Tesco is secured and will be repaid on time.

Thus, it can be said that financial statements have due importance for creditors. Government: Government is another important stakeholder of the business firm because

it receive tax from the profit amount that is earned by the business firm from its

operations. Government needed income statement and balance sheet in order to determine

that right amount of tax is paid to it (Altamuro and Beatty, 2010). Thus, it also needed

financial statement of the business firm. Employees: Employees are also considered as stakeholder of business because they

operate day to day firm operations. On the basis of financial statements they identify firm

condition and in case of critical condition identify whether firm will be able to pay their

salary on time.

(4)Importance of financial reporting for meeting organization objectives and growth

There is huge importance of financial reporting for the business firm because it help it in

achieving organization objectives and growth in business. This is because in financial report

different sort of statements like income statement, balance sheet and cash flow statement is

prepared. Managers analyze these statements deeply and identify firm financial condition. On the

basis of accessed condition direction in which work need to be done is identified and strategy is

formulated to achieve pre determined objectives. In case objective is achieved it pave a way of

growth for the business firm. Thus, it can be said that financial reporting have due importance for

meeting organization objectives and growth. In current time period most of business firms are

giving due emphasis on best use of results that are obtained from financial reporting. This is

because business conditions now become highly complex and due to this reason it is very

difficult task to pay attention on each and every weak point. Financial reporting ensured that only

relevant information and those need due attention of managers highlighted. Thus, clearly

managers get an input about direction in which they really need to work for benefit of an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organization and achievement of an objective. Usually, when financial statements are prepared

board meeting is organized and discussion is carried out on obtained results and weak areas of

business firm are identified and on that basis growth strategy is prepared by the managers. If

economic conditions of nation are not stable and firm is not earning good amount of return in its

business then retrenchment strategy is followed by the firm (Chen and et.al., 2010). Contrary to

this, both conditions are in support of business firm then growth strategy is prepared and

business operations are expanded at rapid rate.

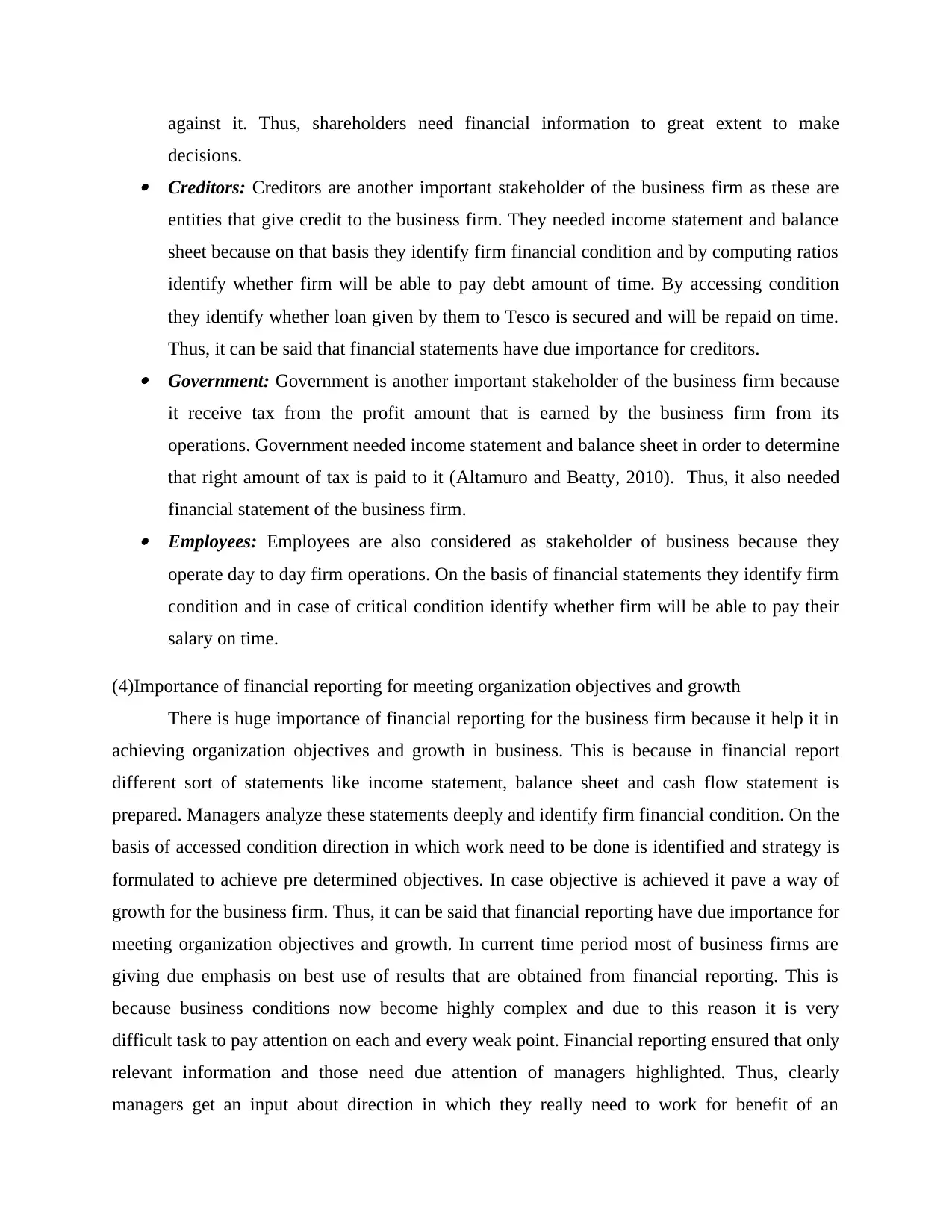

(5)Financial statements of companies and difference between cash flow statement, income

statement and balance sheet

Income statement

Figure 1Income statement of TESCO

(Source : TESCO, 2017)

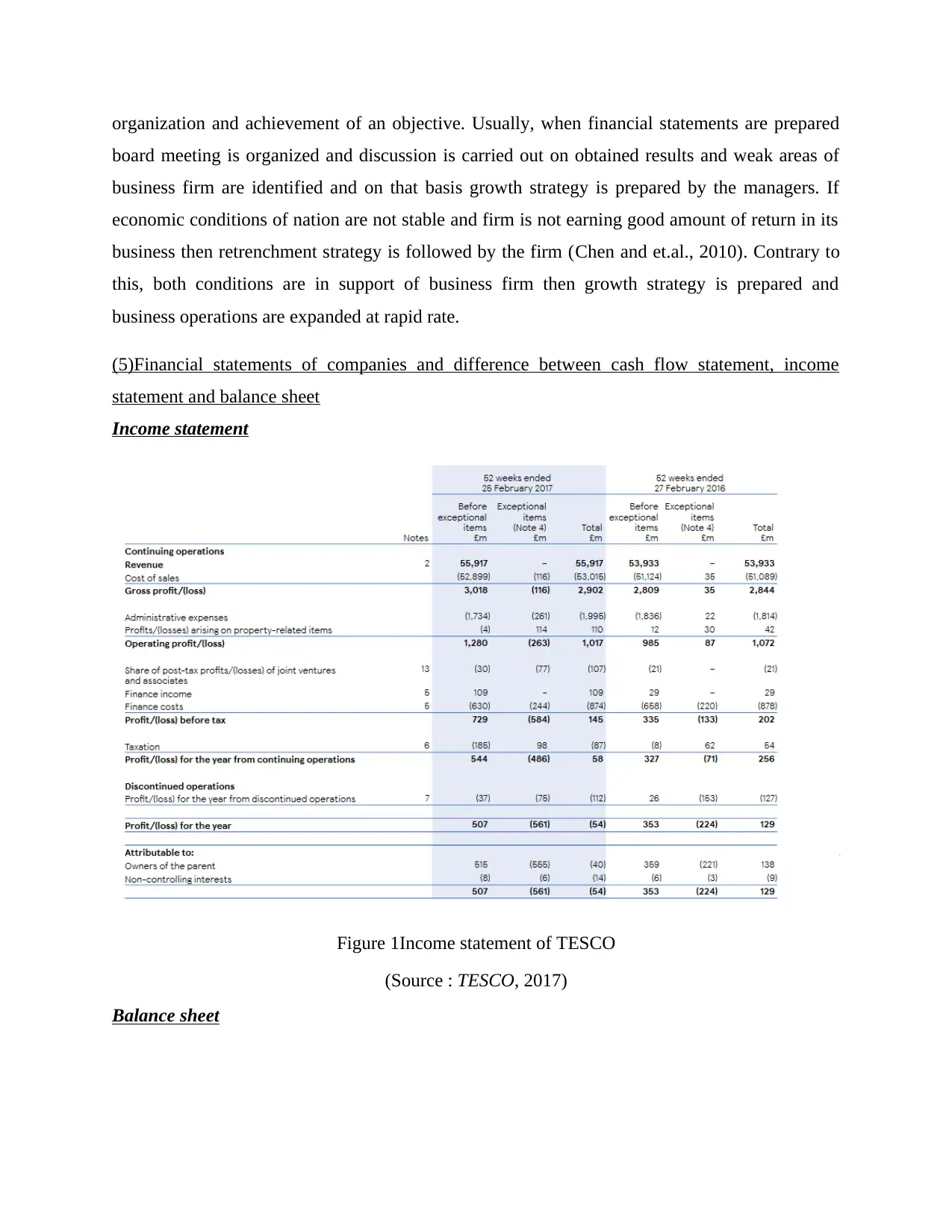

Balance sheet

board meeting is organized and discussion is carried out on obtained results and weak areas of

business firm are identified and on that basis growth strategy is prepared by the managers. If

economic conditions of nation are not stable and firm is not earning good amount of return in its

business then retrenchment strategy is followed by the firm (Chen and et.al., 2010). Contrary to

this, both conditions are in support of business firm then growth strategy is prepared and

business operations are expanded at rapid rate.

(5)Financial statements of companies and difference between cash flow statement, income

statement and balance sheet

Income statement

Figure 1Income statement of TESCO

(Source : TESCO, 2017)

Balance sheet

Figure 2Balance sheet

(Source: TESCO, 2017)

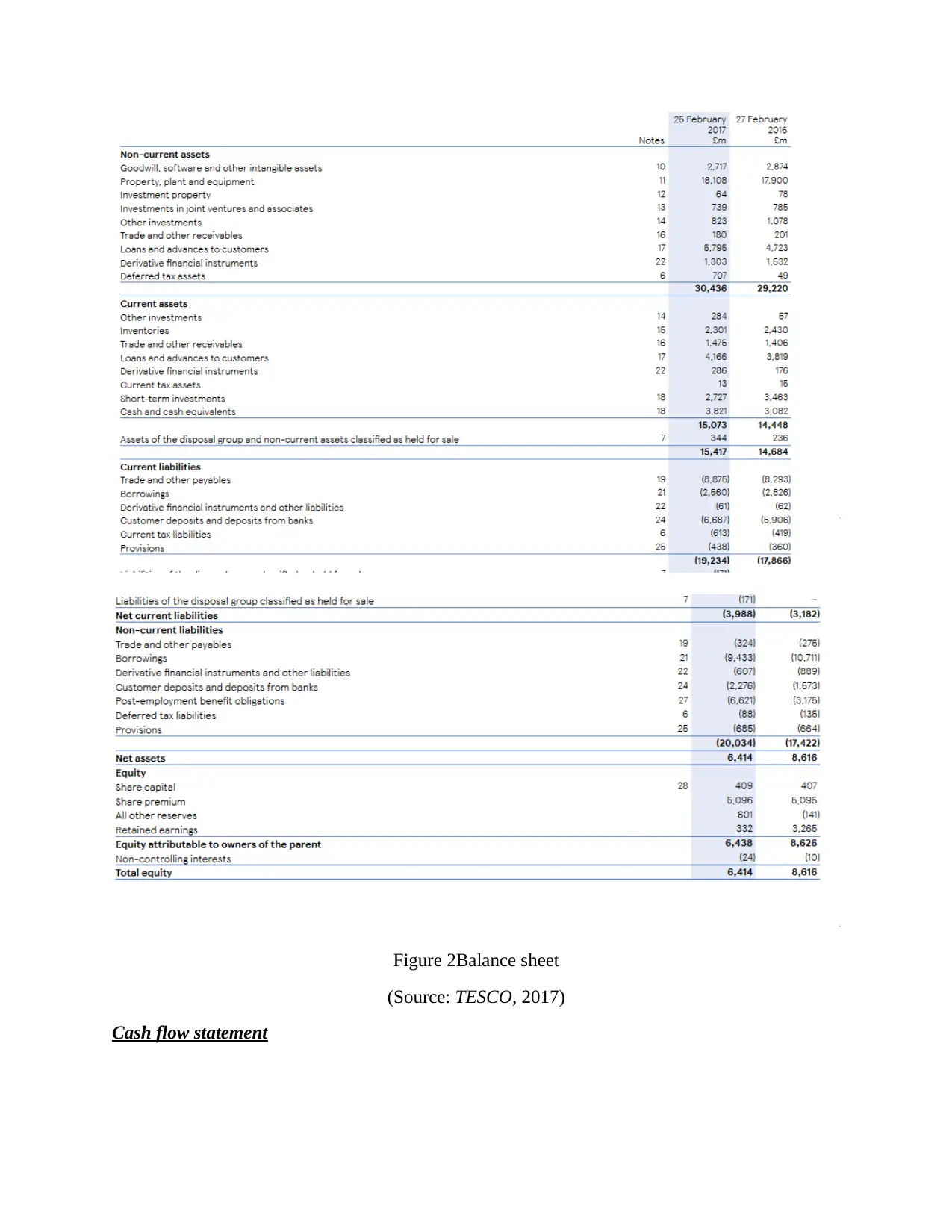

Cash flow statement

(Source: TESCO, 2017)

Cash flow statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 3Cash flow statement of TESCO

(Source: TESCO, 2017)

(Source: TESCO, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

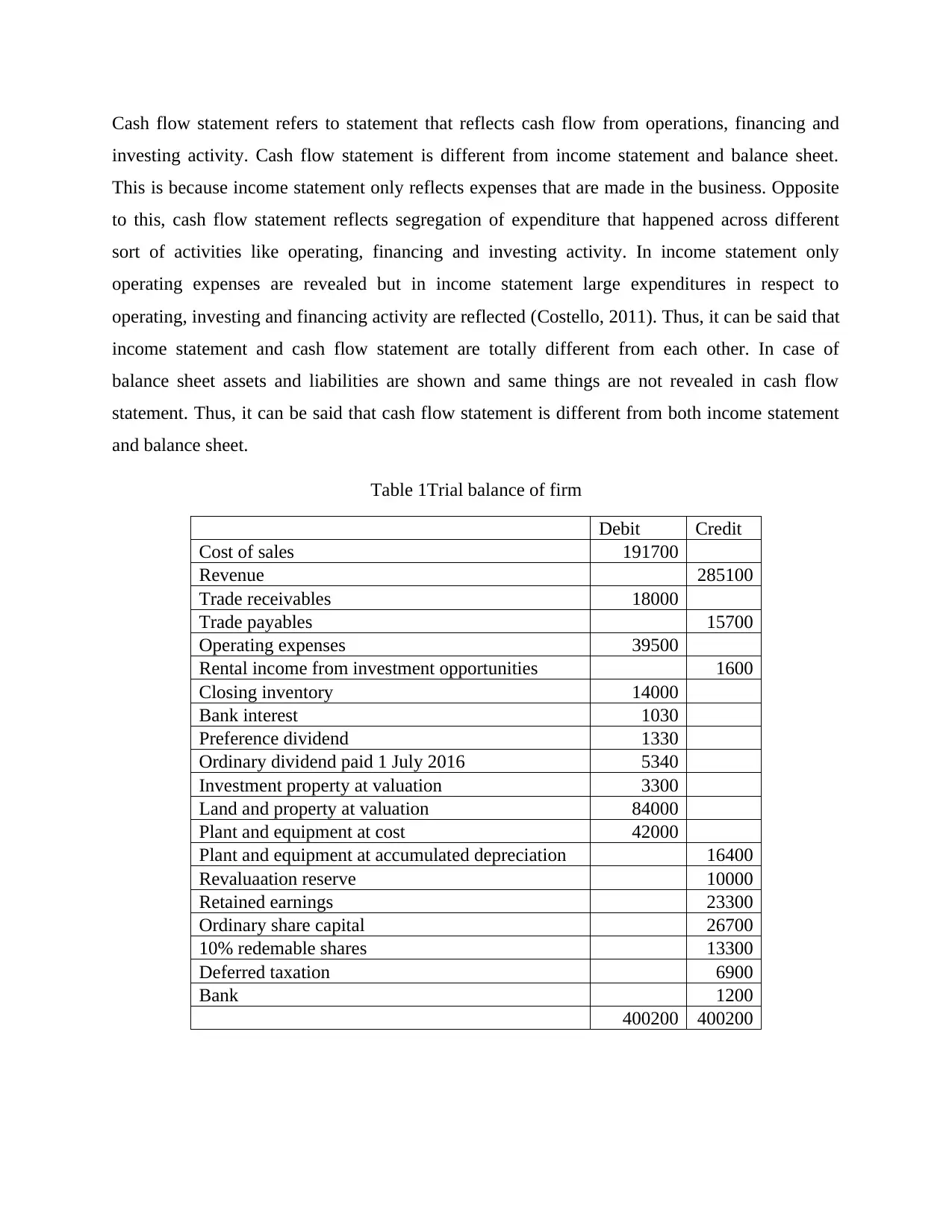

Cash flow statement refers to statement that reflects cash flow from operations, financing and

investing activity. Cash flow statement is different from income statement and balance sheet.

This is because income statement only reflects expenses that are made in the business. Opposite

to this, cash flow statement reflects segregation of expenditure that happened across different

sort of activities like operating, financing and investing activity. In income statement only

operating expenses are revealed but in income statement large expenditures in respect to

operating, investing and financing activity are reflected (Costello, 2011). Thus, it can be said that

income statement and cash flow statement are totally different from each other. In case of

balance sheet assets and liabilities are shown and same things are not revealed in cash flow

statement. Thus, it can be said that cash flow statement is different from both income statement

and balance sheet.

Table 1Trial balance of firm

Debit Credit

Cost of sales 191700

Revenue 285100

Trade receivables 18000

Trade payables 15700

Operating expenses 39500

Rental income from investment opportunities 1600

Closing inventory 14000

Bank interest 1030

Preference dividend 1330

Ordinary dividend paid 1 July 2016 5340

Investment property at valuation 3300

Land and property at valuation 84000

Plant and equipment at cost 42000

Plant and equipment at accumulated depreciation 16400

Revaluaation reserve 10000

Retained earnings 23300

Ordinary share capital 26700

10% redemable shares 13300

Deferred taxation 6900

Bank 1200

400200 400200

investing activity. Cash flow statement is different from income statement and balance sheet.

This is because income statement only reflects expenses that are made in the business. Opposite

to this, cash flow statement reflects segregation of expenditure that happened across different

sort of activities like operating, financing and investing activity. In income statement only

operating expenses are revealed but in income statement large expenditures in respect to

operating, investing and financing activity are reflected (Costello, 2011). Thus, it can be said that

income statement and cash flow statement are totally different from each other. In case of

balance sheet assets and liabilities are shown and same things are not revealed in cash flow

statement. Thus, it can be said that cash flow statement is different from both income statement

and balance sheet.

Table 1Trial balance of firm

Debit Credit

Cost of sales 191700

Revenue 285100

Trade receivables 18000

Trade payables 15700

Operating expenses 39500

Rental income from investment opportunities 1600

Closing inventory 14000

Bank interest 1030

Preference dividend 1330

Ordinary dividend paid 1 July 2016 5340

Investment property at valuation 3300

Land and property at valuation 84000

Plant and equipment at cost 42000

Plant and equipment at accumulated depreciation 16400

Revaluaation reserve 10000

Retained earnings 23300

Ordinary share capital 26700

10% redemable shares 13300

Deferred taxation 6900

Bank 1200

400200 400200

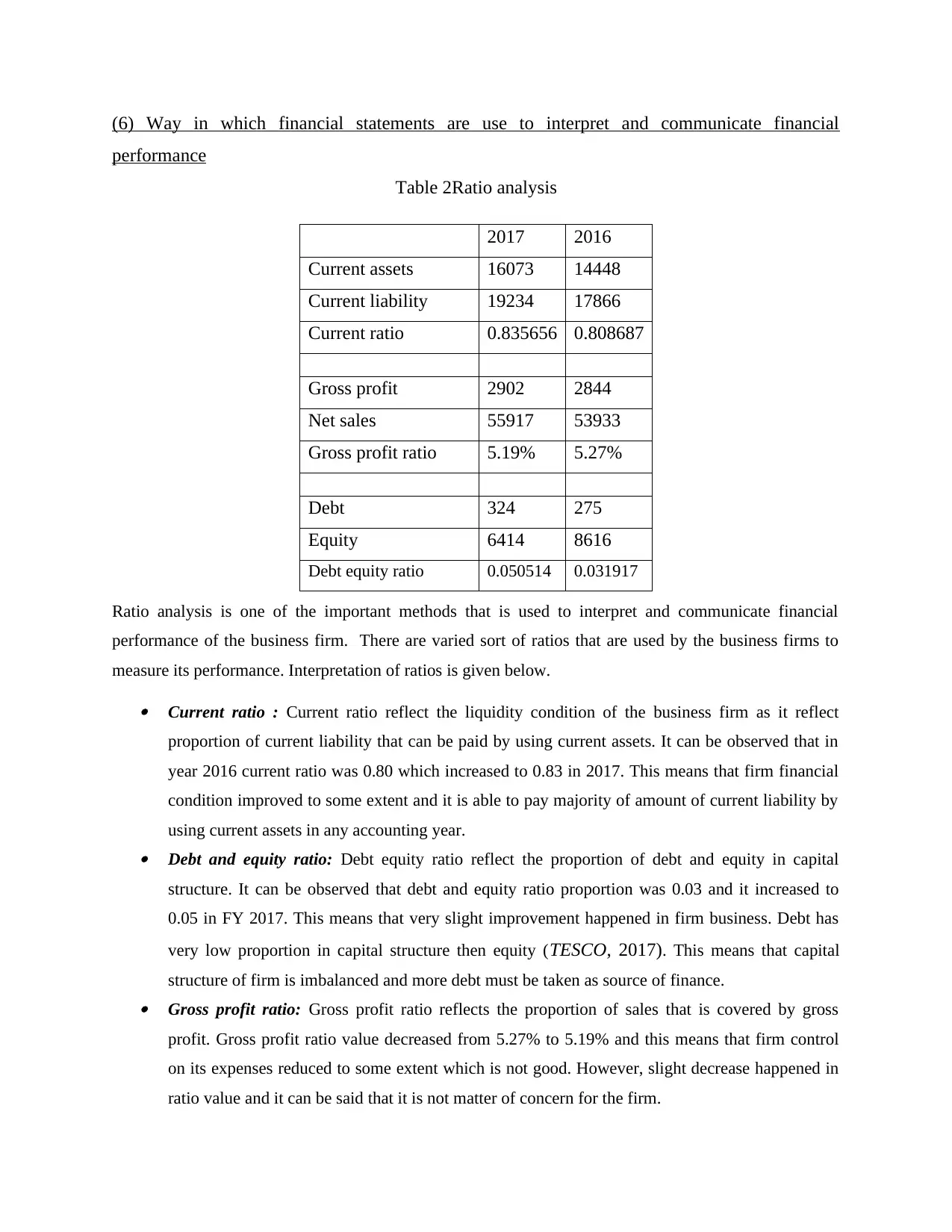

(6) Way in which financial statements are use to interpret and communicate financial

performance

Table 2Ratio analysis

Ratio analysis is one of the important methods that is used to interpret and communicate financial

performance of the business firm. There are varied sort of ratios that are used by the business firms to

measure its performance. Interpretation of ratios is given below. Current ratio : Current ratio reflect the liquidity condition of the business firm as it reflect

proportion of current liability that can be paid by using current assets. It can be observed that in

year 2016 current ratio was 0.80 which increased to 0.83 in 2017. This means that firm financial

condition improved to some extent and it is able to pay majority of amount of current liability by

using current assets in any accounting year. Debt and equity ratio: Debt equity ratio reflect the proportion of debt and equity in capital

structure. It can be observed that debt and equity ratio proportion was 0.03 and it increased to

0.05 in FY 2017. This means that very slight improvement happened in firm business. Debt has

very low proportion in capital structure then equity (TESCO, 2017). This means that capital

structure of firm is imbalanced and more debt must be taken as source of finance. Gross profit ratio: Gross profit ratio reflects the proportion of sales that is covered by gross

profit. Gross profit ratio value decreased from 5.27% to 5.19% and this means that firm control

on its expenses reduced to some extent which is not good. However, slight decrease happened in

ratio value and it can be said that it is not matter of concern for the firm.

2017 2016

Current assets 16073 14448

Current liability 19234 17866

Current ratio 0.835656 0.808687

Gross profit 2902 2844

Net sales 55917 53933

Gross profit ratio 5.19% 5.27%

Debt 324 275

Equity 6414 8616

Debt equity ratio 0.050514 0.031917

performance

Table 2Ratio analysis

Ratio analysis is one of the important methods that is used to interpret and communicate financial

performance of the business firm. There are varied sort of ratios that are used by the business firms to

measure its performance. Interpretation of ratios is given below. Current ratio : Current ratio reflect the liquidity condition of the business firm as it reflect

proportion of current liability that can be paid by using current assets. It can be observed that in

year 2016 current ratio was 0.80 which increased to 0.83 in 2017. This means that firm financial

condition improved to some extent and it is able to pay majority of amount of current liability by

using current assets in any accounting year. Debt and equity ratio: Debt equity ratio reflect the proportion of debt and equity in capital

structure. It can be observed that debt and equity ratio proportion was 0.03 and it increased to

0.05 in FY 2017. This means that very slight improvement happened in firm business. Debt has

very low proportion in capital structure then equity (TESCO, 2017). This means that capital

structure of firm is imbalanced and more debt must be taken as source of finance. Gross profit ratio: Gross profit ratio reflects the proportion of sales that is covered by gross

profit. Gross profit ratio value decreased from 5.27% to 5.19% and this means that firm control

on its expenses reduced to some extent which is not good. However, slight decrease happened in

ratio value and it can be said that it is not matter of concern for the firm.

2017 2016

Current assets 16073 14448

Current liability 19234 17866

Current ratio 0.835656 0.808687

Gross profit 2902 2844

Net sales 55917 53933

Gross profit ratio 5.19% 5.27%

Debt 324 275

Equity 6414 8616

Debt equity ratio 0.050514 0.031917

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.