Financial Reporting Analysis of Marks and Spencer Plc

VerifiedAdded on 2021/01/01

|14

|4020

|60

Report

AI Summary

This report delves into the intricacies of financial reporting, focusing on its purpose, regulatory frameworks, and stakeholder analysis, with Marks and Spencer (M&S) as a central case study. It explores the objectives of financial reporting, including its role in effective decision-making, ensuring accuracy, satisfying stakeholders, meeting legal requirements, and facilitating international trade. The report examines the regulatory framework, specifically the role of the IASB, and discusses the governance of financial reporting, highlighting qualitative characteristics like understandability and comparability. It identifies key stakeholders of M&S and their benefits from financial information, such as investors, suppliers, and governmental bodies. The report further analyzes financial statements, including a statement of profit and loss, changes in equity, and financial position, providing a comprehensive overview of M&S's financial performance. Additionally, it contrasts IAS and IFRS, discusses the benefits of IFRS, and explores the varying degrees of IFRS compliance across firms globally. The report concludes with a summary of the key findings and implications of financial reporting within the context of M&S's operations.

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1 Purpose of financial reporting..................................................................................................1

2. Regulatory frameworks of financial reporting........................................................................2

3. Stakeholder of Marks and Spencer plc and and its benefits from financial information........4

4. Financial reporting for meeting firm objectives......................................................................4

5. Financial statements................................................................................................................5

6. Financial statement of Marks and Spencer plc and interpretation of financial performance:.7

7. Difference between of IAS and IFRS.....................................................................................8

8. Benefits of IFRS......................................................................................................................8

9.Various degree of compliances with the IFRS by firms across the globe and components

affecting it...................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1 Purpose of financial reporting..................................................................................................1

2. Regulatory frameworks of financial reporting........................................................................2

3. Stakeholder of Marks and Spencer plc and and its benefits from financial information........4

4. Financial reporting for meeting firm objectives......................................................................4

5. Financial statements................................................................................................................5

6. Financial statement of Marks and Spencer plc and interpretation of financial performance:.7

7. Difference between of IAS and IFRS.....................................................................................8

8. Benefits of IFRS......................................................................................................................8

9.Various degree of compliances with the IFRS by firms across the globe and components

affecting it...................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial reporting is a process of developing and producing financial reports which

consists financial information for a business organisation. The main aim of this project report is

to build an understanding about the concept of financial reporting and its various aspects due to

which a company is selected named as “Marks and Spencer Financial services Plc”. It is a

financial services company which operates in retail banking in United Kingdom. In this project

report, framework and governance of financial reporting is mentioned along with its its

objectives. Financial statements of M&S bank is also analysed. Benefits of International

accounting standards are discussed with International financial reporting standards. Financial

reporting is a tool of ascertaining accurate performance of a company due to which difference in

the importance of financial reporting all various countries is analysed in this project report. As a

Junior Auditor of a large accounting firm, Financial ratios are calculated to determine

organisational performance and investment of M&S Bank.

MAIN BODY

1 Purpose of financial reporting

Financial reporting is a process of disclosing financial information of a company in

certain authorised formats. These formats in which financial data is disclosed are income

statement, balance sheet, cash flow and other accounts and statements. Main aim of this process

is to serve accurate and reliable information to stakeholders of a company such as shareholders,

suppliers, employees, governmental authorities and many more. Financial reporting are prepared

by accountants on quarter and annual basis (Nobes, 2014).

Purposes of financial reporting:

This reporting system has various purposes, the most important aim is to provide

financial information to management of an organisation so that they can plan their benchmarks

and conduct reliable decision making. Another main purpose of this system is to provide

information to all stakeholders so that they take profitable decisions such as investment

decisions. Financial reporting system serves various stakeholders to take effective decisions such

as credit decisions, investment decisions and taxation decisions. Purposes of financial reporting

for meeting organisational objectives, development and growth are mentioned below:

1

Financial reporting is a process of developing and producing financial reports which

consists financial information for a business organisation. The main aim of this project report is

to build an understanding about the concept of financial reporting and its various aspects due to

which a company is selected named as “Marks and Spencer Financial services Plc”. It is a

financial services company which operates in retail banking in United Kingdom. In this project

report, framework and governance of financial reporting is mentioned along with its its

objectives. Financial statements of M&S bank is also analysed. Benefits of International

accounting standards are discussed with International financial reporting standards. Financial

reporting is a tool of ascertaining accurate performance of a company due to which difference in

the importance of financial reporting all various countries is analysed in this project report. As a

Junior Auditor of a large accounting firm, Financial ratios are calculated to determine

organisational performance and investment of M&S Bank.

MAIN BODY

1 Purpose of financial reporting

Financial reporting is a process of disclosing financial information of a company in

certain authorised formats. These formats in which financial data is disclosed are income

statement, balance sheet, cash flow and other accounts and statements. Main aim of this process

is to serve accurate and reliable information to stakeholders of a company such as shareholders,

suppliers, employees, governmental authorities and many more. Financial reporting are prepared

by accountants on quarter and annual basis (Nobes, 2014).

Purposes of financial reporting:

This reporting system has various purposes, the most important aim is to provide

financial information to management of an organisation so that they can plan their benchmarks

and conduct reliable decision making. Another main purpose of this system is to provide

information to all stakeholders so that they take profitable decisions such as investment

decisions. Financial reporting system serves various stakeholders to take effective decisions such

as credit decisions, investment decisions and taxation decisions. Purposes of financial reporting

for meeting organisational objectives, development and growth are mentioned below:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Effective decision making – Financial reporting is a process of producing financial

statements using accounting data. These statements can help in effective decision making to

various stakeholders. Investors are benefit from investor decisions, suppliers and creditors are

benefited with credit de scions etc. Financial reports also helps an organisation to take effective

taxation decisions.

Accuracy in financial statements – Financial reports are prepared using principles and

standards provided by international boards. Due to which information analysed in this report are

accurate and is based on arithmetical accuracy. This accuracy further assist an organisation in

performing various functions such as auditing.

Satisfaction of stakeholders – Main purpose of financial reporting is to serve reliable

information to stakeholders. By fulfilling this purpose an organisation can attain full satisfaction

of their stakeholders such as creditors, debtors, investors and many more.

Legal requirements – Another purpose of financial reporting is to ensure that all the

legal requirements of an organisation is fulfilled regarding financial information. For example:

International financial accounting standard says that all organisation are required to disclose all

the material information which helps in fulfil their legal requirement of disclosure and

materiality.

International trade – Another purpose of financial reporting is international trade. In

order to trade internationally, it is mandatory for all companies to serve their financial reports to

governmental authorities. For example: If a company like Marks and Spencer wishes to trade in

global market, they has to provide their financial statements such as cash flow, balance sheet and

income statements to governmental authorities.

The above mentioned purposes helps an organisation to achieve their organisational

objectives of profit maximisation and client satisfaction. By producing these information and

statements, an organisation can develop their business operations by expansion and grow overall

organisation (Laux, 2012).

2. Regulatory frameworks of financial reporting

Regulatory framework of financial reporting:

Regulatory framework are the regulatory authorities which are responsible for all affairs

of financial reporting. Regulatory framework can be different for every country, in the case of

United Kingdom IASB is the responsible authority. IASB or International Accounting standard

2

statements using accounting data. These statements can help in effective decision making to

various stakeholders. Investors are benefit from investor decisions, suppliers and creditors are

benefited with credit de scions etc. Financial reports also helps an organisation to take effective

taxation decisions.

Accuracy in financial statements – Financial reports are prepared using principles and

standards provided by international boards. Due to which information analysed in this report are

accurate and is based on arithmetical accuracy. This accuracy further assist an organisation in

performing various functions such as auditing.

Satisfaction of stakeholders – Main purpose of financial reporting is to serve reliable

information to stakeholders. By fulfilling this purpose an organisation can attain full satisfaction

of their stakeholders such as creditors, debtors, investors and many more.

Legal requirements – Another purpose of financial reporting is to ensure that all the

legal requirements of an organisation is fulfilled regarding financial information. For example:

International financial accounting standard says that all organisation are required to disclose all

the material information which helps in fulfil their legal requirement of disclosure and

materiality.

International trade – Another purpose of financial reporting is international trade. In

order to trade internationally, it is mandatory for all companies to serve their financial reports to

governmental authorities. For example: If a company like Marks and Spencer wishes to trade in

global market, they has to provide their financial statements such as cash flow, balance sheet and

income statements to governmental authorities.

The above mentioned purposes helps an organisation to achieve their organisational

objectives of profit maximisation and client satisfaction. By producing these information and

statements, an organisation can develop their business operations by expansion and grow overall

organisation (Laux, 2012).

2. Regulatory frameworks of financial reporting

Regulatory framework of financial reporting:

Regulatory framework are the regulatory authorities which are responsible for all affairs

of financial reporting. Regulatory framework can be different for every country, in the case of

United Kingdom IASB is the responsible authority. IASB or International Accounting standard

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Board is an independent private sector body which develops and approves International Financial

Reporting Standards. This board operates under IFRS foundation. Regulatory framework of

financial reporting addresses the fundamental financial reporting problems such as users of

financial statements, concepts and objectives (Kimand Zhang, 2014). The main aim behind

developing this regulatory is to ensure that all the methods and techniques of accountancy are

reliably followed by the organisation. According to this framework, it is mandatory to follow

structure of financial reports and statements in order to bring a similarity in the structure of

financial statements of all the companies across the world. IASB is the regulatory framework of

financial reporting system which does not only develops standards for accounting but also guides

other boards to prepare effective standards.

Governance of financial reporting:

Financial reporting is a process of developing and serving financial statements of a

company to stakeholders. As this reporting system affects profitability of a company and

decisions of a stakeholder it is important to regulate and govern this system. Governance refers

to the authorisation of financial reporting. In the case of United Kingdom, governance of

financial reporting is done using financial standards. These standards are developed and guided

by International accounting standards board. For example: International financial reporting

standard 7 which is developed by IASB states that all financial statements must be disclosed to

stakeholders. This standard governs organisations to disclose all material financial information to

their stakeholders in order to protect their interest (Hope, Thomas and Vyas, 2013).

Qualitative characteristics:

Financial reporting enables an organisation to ascertain accurate and reliable financial

position. There are various qualitative characteristics which makes financial information more

reliable such as understandability, comparability, verifiability and timeliness. For example: The

characteristic of understandability helps to prepare financial statements in such a way that it can

be easily interpreted and evaluated. By the characteristic of comparability, financial statements

of two companies or of two years can be compared in order to identify variation so that reliable

decisions can be made. Principles of financial reporting such as economic entity assumption and

cost principle are developed in order to ensure that all financial standards are followed by

business organisations (Collins, Pasewark and Riley,2012).

3

Reporting Standards. This board operates under IFRS foundation. Regulatory framework of

financial reporting addresses the fundamental financial reporting problems such as users of

financial statements, concepts and objectives (Kimand Zhang, 2014). The main aim behind

developing this regulatory is to ensure that all the methods and techniques of accountancy are

reliably followed by the organisation. According to this framework, it is mandatory to follow

structure of financial reports and statements in order to bring a similarity in the structure of

financial statements of all the companies across the world. IASB is the regulatory framework of

financial reporting system which does not only develops standards for accounting but also guides

other boards to prepare effective standards.

Governance of financial reporting:

Financial reporting is a process of developing and serving financial statements of a

company to stakeholders. As this reporting system affects profitability of a company and

decisions of a stakeholder it is important to regulate and govern this system. Governance refers

to the authorisation of financial reporting. In the case of United Kingdom, governance of

financial reporting is done using financial standards. These standards are developed and guided

by International accounting standards board. For example: International financial reporting

standard 7 which is developed by IASB states that all financial statements must be disclosed to

stakeholders. This standard governs organisations to disclose all material financial information to

their stakeholders in order to protect their interest (Hope, Thomas and Vyas, 2013).

Qualitative characteristics:

Financial reporting enables an organisation to ascertain accurate and reliable financial

position. There are various qualitative characteristics which makes financial information more

reliable such as understandability, comparability, verifiability and timeliness. For example: The

characteristic of understandability helps to prepare financial statements in such a way that it can

be easily interpreted and evaluated. By the characteristic of comparability, financial statements

of two companies or of two years can be compared in order to identify variation so that reliable

decisions can be made. Principles of financial reporting such as economic entity assumption and

cost principle are developed in order to ensure that all financial standards are followed by

business organisations (Collins, Pasewark and Riley,2012).

3

3. Stakeholder of Marks and Spencer plc and and its benefits from financial information

Stakeholders are the related parties of an organisation which are benefited from the

financial information of Marks and Spencer. These stakeholders are customers, investors,

suppliers, government, creditors, debtors and many more. Some of these stakeholders are

analysed in order to identify benefits of these financial information.

Investors – These are the type of stakeholders which invest in company's equity in order

to earn profit from dividend and interest. Income statements helps investors to ascertain profit fro

the year so that they can take reliable investment decision about whether to invest in a company

or not. Information from which investors are benefited are income statements and changes in

equity. Marks and Spencer is a public limited bank in which various investors invest their

resources by analysing their financial performance mentioned in income statements.

Supplier – Suppliers are the stakeholders which supply their products and services to a

company. These stakeholders are benefited with the financial information such as cash flow

statements. As cash flow statements are the evidence of cash flows in an accounting year by

which suppliers can identify cash position of the company so that they can ascertain that whether

company is capable for clearing their debts or not (Cassell and et. al., 2013).

Government – This is the most important important stakeholder for the companies like

Marks and Spencer as they has to fulfil various types of requirements regarding their financial

information such as minimum liquidity ratio, maximum cash reserve ratio and many more.

Financial information which benefits governmental authorities is balance sheet of the

organisation and ratio analysis of the company. For example: Governmental authorities such as

taxation department has to review all their financial information in order to certain net taxable

income.

Shareholders – These type of stakeholder are the members of an organisation.

Shareholders are interested in balance sheet of an organisation in order to attain benefit of equity

dividend. For example: Shareholders of Marks and Spencer, review balance sheet in order to

ascertain possibility of their dividend (Botzem, 2012.).

4. Financial reporting for meeting firm objectives

Company have different departments in its organisation. All departments of company

provide its finance related information to the finance department. Finance departments of

company prepare the financial report. Financial report helps to analyse the financial position of

4

Stakeholders are the related parties of an organisation which are benefited from the

financial information of Marks and Spencer. These stakeholders are customers, investors,

suppliers, government, creditors, debtors and many more. Some of these stakeholders are

analysed in order to identify benefits of these financial information.

Investors – These are the type of stakeholders which invest in company's equity in order

to earn profit from dividend and interest. Income statements helps investors to ascertain profit fro

the year so that they can take reliable investment decision about whether to invest in a company

or not. Information from which investors are benefited are income statements and changes in

equity. Marks and Spencer is a public limited bank in which various investors invest their

resources by analysing their financial performance mentioned in income statements.

Supplier – Suppliers are the stakeholders which supply their products and services to a

company. These stakeholders are benefited with the financial information such as cash flow

statements. As cash flow statements are the evidence of cash flows in an accounting year by

which suppliers can identify cash position of the company so that they can ascertain that whether

company is capable for clearing their debts or not (Cassell and et. al., 2013).

Government – This is the most important important stakeholder for the companies like

Marks and Spencer as they has to fulfil various types of requirements regarding their financial

information such as minimum liquidity ratio, maximum cash reserve ratio and many more.

Financial information which benefits governmental authorities is balance sheet of the

organisation and ratio analysis of the company. For example: Governmental authorities such as

taxation department has to review all their financial information in order to certain net taxable

income.

Shareholders – These type of stakeholder are the members of an organisation.

Shareholders are interested in balance sheet of an organisation in order to attain benefit of equity

dividend. For example: Shareholders of Marks and Spencer, review balance sheet in order to

ascertain possibility of their dividend (Botzem, 2012.).

4. Financial reporting for meeting firm objectives

Company have different departments in its organisation. All departments of company

provide its finance related information to the finance department. Finance departments of

company prepare the financial report. Financial report helps to analyse the financial position of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the organisation. It is important to prepare because it provide information about financial

position, performance and changes in financial position of an organisation during a specific

period of time. It provide information to the management of an organisation and it is used for

planning and decision making for future. On the basis of it management can take decision for

future investment and strategy. It provide information about financial position of company to its

investors, shareholders, promoters, creditors etc. On the basis of this report shareholders and

investors will make investment in the organisation. It helps to increase the market value of its

share because people wants to invest in the company (Bevis, 2013). It will increase the market

value of the organisation. High market value help to increase the financial growth of the

organisation. So Financial reporting is important because it provide all financial information and

it can help in future planning, expansion and investment decision.

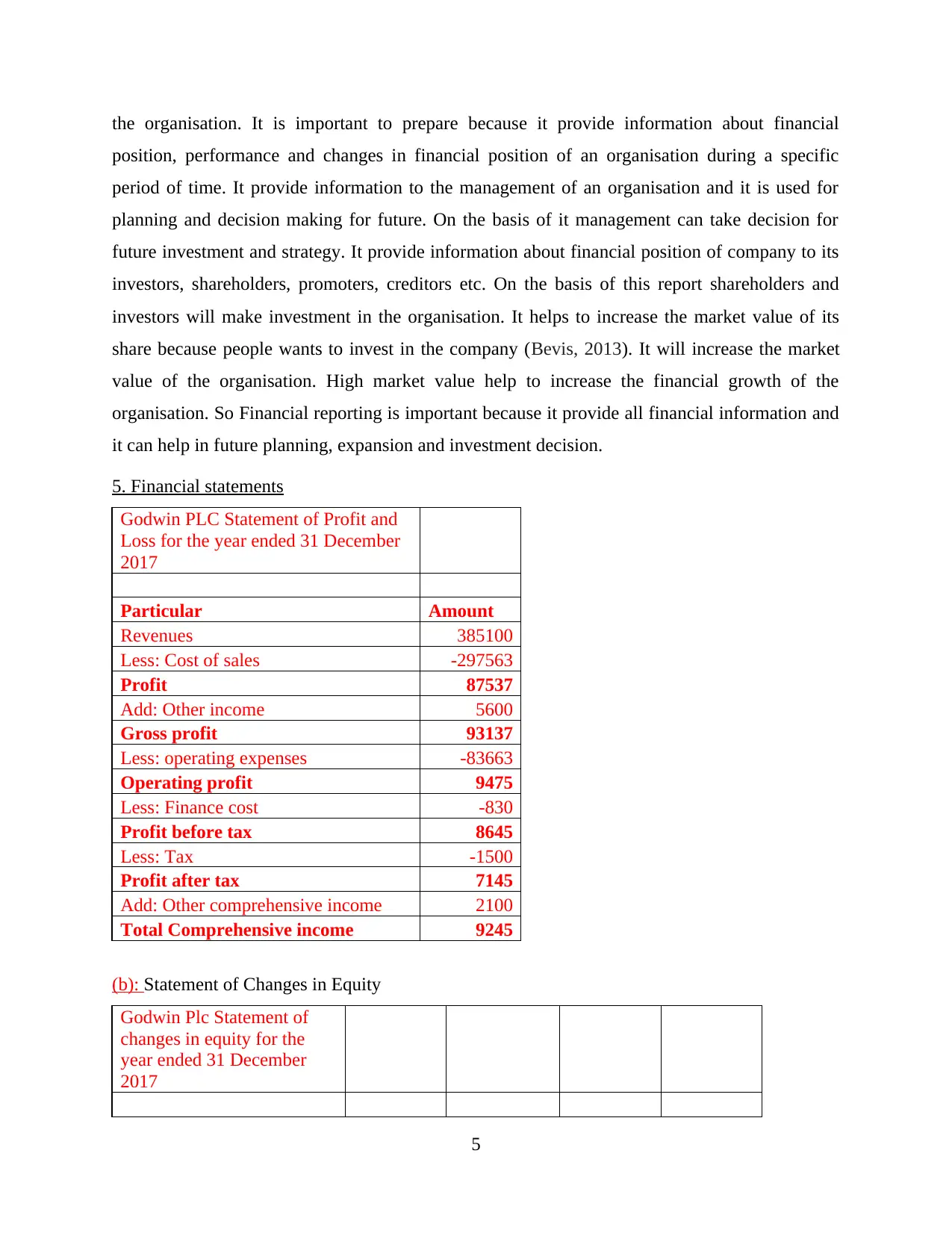

5. Financial statements

Godwin PLC Statement of Profit and

Loss for the year ended 31 December

2017

Particular Amount

Revenues 385100

Less: Cost of sales -297563

Profit 87537

Add: Other income 5600

Gross profit 93137

Less: operating expenses -83663

Operating profit 9475

Less: Finance cost -830

Profit before tax 8645

Less: Tax -1500

Profit after tax 7145

Add: Other comprehensive income 2100

Total Comprehensive income 9245

(b): Statement of Changes in Equity

Godwin Plc Statement of

changes in equity for the

year ended 31 December

2017

5

position, performance and changes in financial position of an organisation during a specific

period of time. It provide information to the management of an organisation and it is used for

planning and decision making for future. On the basis of it management can take decision for

future investment and strategy. It provide information about financial position of company to its

investors, shareholders, promoters, creditors etc. On the basis of this report shareholders and

investors will make investment in the organisation. It helps to increase the market value of its

share because people wants to invest in the company (Bevis, 2013). It will increase the market

value of the organisation. High market value help to increase the financial growth of the

organisation. So Financial reporting is important because it provide all financial information and

it can help in future planning, expansion and investment decision.

5. Financial statements

Godwin PLC Statement of Profit and

Loss for the year ended 31 December

2017

Particular Amount

Revenues 385100

Less: Cost of sales -297563

Profit 87537

Add: Other income 5600

Gross profit 93137

Less: operating expenses -83663

Operating profit 9475

Less: Finance cost -830

Profit before tax 8645

Less: Tax -1500

Profit after tax 7145

Add: Other comprehensive income 2100

Total Comprehensive income 9245

(b): Statement of Changes in Equity

Godwin Plc Statement of

changes in equity for the

year ended 31 December

2017

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

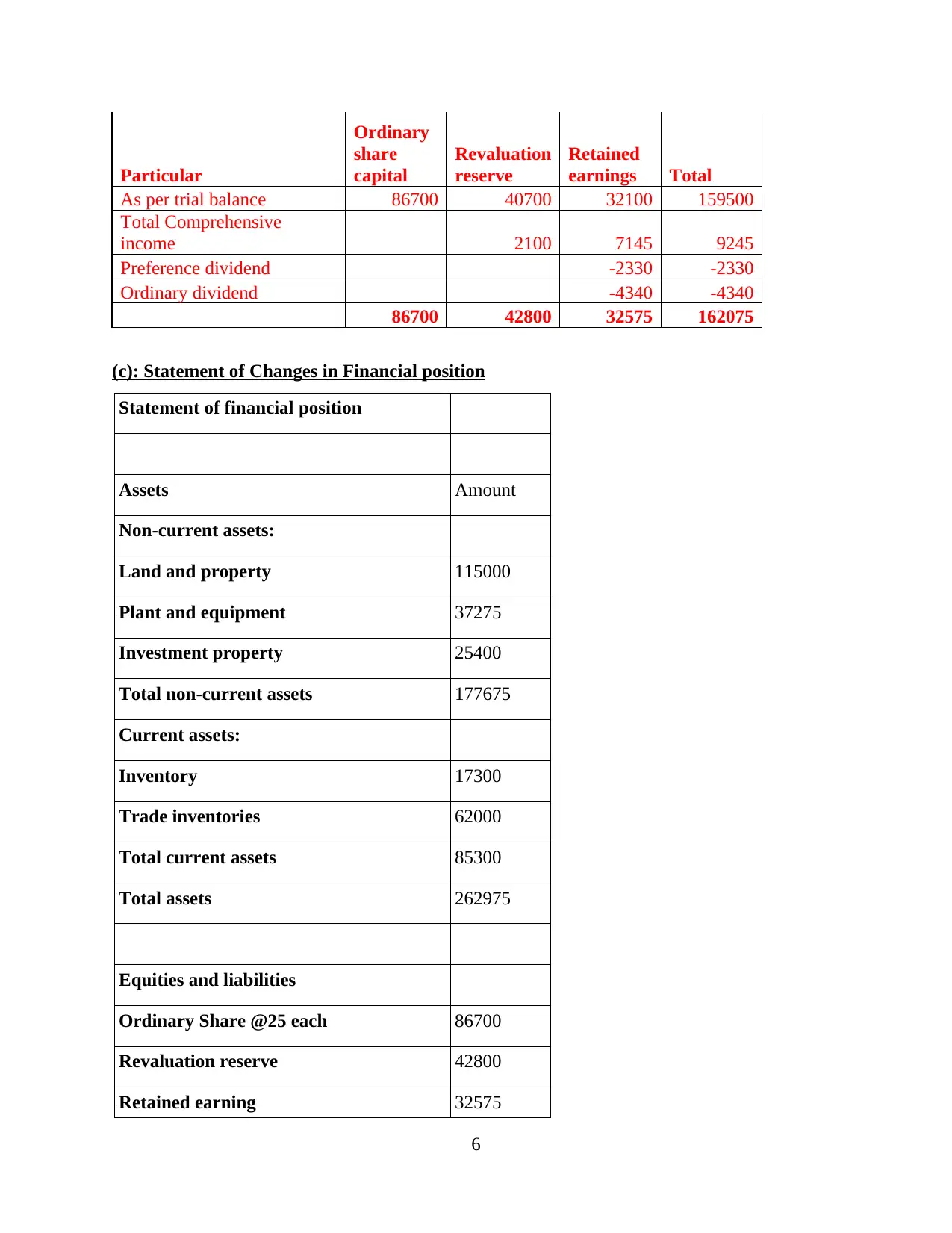

Particular

Ordinary

share

capital

Revaluation

reserve

Retained

earnings Total

As per trial balance 86700 40700 32100 159500

Total Comprehensive

income 2100 7145 9245

Preference dividend -2330 -2330

Ordinary dividend -4340 -4340

86700 42800 32575 162075

(c): Statement of Changes in Financial position

Statement of financial position

Assets Amount

Non-current assets:

Land and property 115000

Plant and equipment 37275

Investment property 25400

Total non-current assets 177675

Current assets:

Inventory 17300

Trade inventories 62000

Total current assets 85300

Total assets 262975

Equities and liabilities

Ordinary Share @25 each 86700

Revaluation reserve 42800

Retained earning 32575

6

Ordinary

share

capital

Revaluation

reserve

Retained

earnings Total

As per trial balance 86700 40700 32100 159500

Total Comprehensive

income 2100 7145 9245

Preference dividend -2330 -2330

Ordinary dividend -4340 -4340

86700 42800 32575 162075

(c): Statement of Changes in Financial position

Statement of financial position

Assets Amount

Non-current assets:

Land and property 115000

Plant and equipment 37275

Investment property 25400

Total non-current assets 177675

Current assets:

Inventory 17300

Trade inventories 62000

Total current assets 85300

Total assets 262975

Equities and liabilities

Ordinary Share @25 each 86700

Revaluation reserve 42800

Retained earning 32575

6

Total equities 162075

Noncurrent liabilities:

10% redeemable preference share 23300

Deferred taxation 8900

Total noncurrent liabilities 32200

Trade payables 65700

Bank overdraft 1500

Tax payables 1500

Total current liabilities 68700

Total equities and liabilities 262975

Calculation of Depreciation:

On Land and property:

Property 4000

Plant and equipment 3200

Total 7200

Charged to cost of sales 3600

Charged to operating expenses 3600

6. Financial statement of Marks and Spencer plc and interpretation of financial

performance:

Financial ratios of Mark and Spencer

Particular ratios Formula 2017 2018

Liquidity ratios:

Current ratio: Current asset/ current liabilities

0.721741511

5

0.7277449

324

7

Noncurrent liabilities:

10% redeemable preference share 23300

Deferred taxation 8900

Total noncurrent liabilities 32200

Trade payables 65700

Bank overdraft 1500

Tax payables 1500

Total current liabilities 68700

Total equities and liabilities 262975

Calculation of Depreciation:

On Land and property:

Property 4000

Plant and equipment 3200

Total 7200

Charged to cost of sales 3600

Charged to operating expenses 3600

6. Financial statement of Marks and Spencer plc and interpretation of financial

performance:

Financial ratios of Mark and Spencer

Particular ratios Formula 2017 2018

Liquidity ratios:

Current ratio: Current asset/ current liabilities

0.721741511

5

0.7277449

324

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Liquid ratio: Current asset- inventory+ prepaid

expenses/ Current liabilities

0.294030668

1

0.4073057

432

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.089248729

1 0.272008

Gross profit ratios Gross profit/ Sales *100

2.383731877

2

1.4628629

115

ROE Total income/ shareholder equity

0.022431327

8

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.098344370

9

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets

1.616939657

8

1.7165412

448

From the financial statements of two years of Marks and Spencer it has ascertained that

this company classifies their information in various categories. This company prepares financial

information by consolidates income of their organisation and of their subsidiary organisations.

Income statement and comprehensive income statement are separately prepared in order to

ascertain their realisable value. Along with balance and cash flow statement, this company also

prepares their changes in equity.

From the ascertained ratios, it has been analysed that company is having high liquidity in

the year of 2017. But on the other hand, in 2016 company was having high profitability which

shows that in 2017 company utilises all their resources in operational activities. By ascertaining

efficiency ratios, it has analysed that company was more efficient in 2017.

7. Difference between of IAS and IFRS

IAS: These are the older accounting standards that are currently replaced by IFRS. IAS

was the first set of accounting standards that are introduced by international accounting standards

committee in year 1973. It helps to enhance transparency, accountability, accuracy and

8

expenses/ Current liabilities

0.294030668

1

0.4073057

432

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.089248729

1 0.272008

Gross profit ratios Gross profit/ Sales *100

2.383731877

2

1.4628629

115

ROE Total income/ shareholder equity

0.022431327

8

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.098344370

9

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets

1.616939657

8

1.7165412

448

From the financial statements of two years of Marks and Spencer it has ascertained that

this company classifies their information in various categories. This company prepares financial

information by consolidates income of their organisation and of their subsidiary organisations.

Income statement and comprehensive income statement are separately prepared in order to

ascertain their realisable value. Along with balance and cash flow statement, this company also

prepares their changes in equity.

From the ascertained ratios, it has been analysed that company is having high liquidity in

the year of 2017. But on the other hand, in 2016 company was having high profitability which

shows that in 2017 company utilises all their resources in operational activities. By ascertaining

efficiency ratios, it has analysed that company was more efficient in 2017.

7. Difference between of IAS and IFRS

IAS: These are the older accounting standards that are currently replaced by IFRS. IAS

was the first set of accounting standards that are introduced by international accounting standards

committee in year 1973. It helps to enhance transparency, accountability, accuracy and

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

effectiveness in the financial statements. It facilitates investors to make investment decision and

to figure out its risk and profits.

IFRS: It was introduced by IFRS foundation and international accounting standards

board in year 2001 to resolve contradictions in IAS. It provides a common worldwide language

to different business that are running globally to analyse accounts of the company. It has

replaced a few standards of international accounting standards (IFRS, 2018).

Difference between IAS and IFRS:

IAS IFRS

It stands for international accounting standards. It stands for international financial reporting

standards.

It was introduced by international accounting

standards committee.

It was launched by international accounting

standard board in year 2001.

IAS was launched to reduce accounting errors in

international financial reporting.

IFRS was introduced when there are various

contradictions in IAS and it helped to reduce

those contradictions.

It has become popular in year 1973. It was introduced in year 2001.

8. Benefits of IFRS

Benefits of IFRS: Following are the benefits of IFRS:

It has helped to build ethical relation all around the world as it considers input from

professionals and legal authorities around the world.

It has enhanced the quality of financial reports because it leaves little room for

countermining the aims of set standards.

It has facilitated the international investors to make strategic decision because now they

can compare financial statements of companies and analyse that companies are following

international accounting standards and other guidelines.

It facilitates the investors while analysing convergence and transparency of accounting

practices (Beatty, Liao and Yu, 2013).

International trade has been enhanced with the help of IFRS as it guides organisations to

find strategic partners and customers from different regions.

9

to figure out its risk and profits.

IFRS: It was introduced by IFRS foundation and international accounting standards

board in year 2001 to resolve contradictions in IAS. It provides a common worldwide language

to different business that are running globally to analyse accounts of the company. It has

replaced a few standards of international accounting standards (IFRS, 2018).

Difference between IAS and IFRS:

IAS IFRS

It stands for international accounting standards. It stands for international financial reporting

standards.

It was introduced by international accounting

standards committee.

It was launched by international accounting

standard board in year 2001.

IAS was launched to reduce accounting errors in

international financial reporting.

IFRS was introduced when there are various

contradictions in IAS and it helped to reduce

those contradictions.

It has become popular in year 1973. It was introduced in year 2001.

8. Benefits of IFRS

Benefits of IFRS: Following are the benefits of IFRS:

It has helped to build ethical relation all around the world as it considers input from

professionals and legal authorities around the world.

It has enhanced the quality of financial reports because it leaves little room for

countermining the aims of set standards.

It has facilitated the international investors to make strategic decision because now they

can compare financial statements of companies and analyse that companies are following

international accounting standards and other guidelines.

It facilitates the investors while analysing convergence and transparency of accounting

practices (Beatty, Liao and Yu, 2013).

International trade has been enhanced with the help of IFRS as it guides organisations to

find strategic partners and customers from different regions.

9

It is flexible to both expected or unexpected changes in worldwide business environment

as it is mainly based on broad principles. It provides liberty to the organisations of

choosing the format for presentation which suits to its users and stakeholders.

It has simplified the accounting procedure for multinational companies who are operating

their businesses in different countries.

It helps to reduce business costs to the organisations of preparing financial statements

oriented for international customers.

It assists those organisations who are willing to deal in foreign trade and are trying to

expand their business globally.

IFRS is mainly introduced by IASB to direct companies while they are generating their

financial statements in order to analyse actual position of company. It has succeeded in

this task as companies are now able to acquire more and more profits.

All the above mentioned advantages are related to the IFRS it, helps organisation to

formulated their financial statements accurately. The business entities who are adopting these

standards can attain various benefits with the help of IFRS as it guides to record appropriate

information to the final accounts.

9.Various degree of compliances with the IFRS by firms across the globe and components

affecting it

IFRS is a standard which is used by most of the company while generating their financial

statements (Ball, Jayaraman and Shivakumar, 2012.). This a type of standards which is used by

almost each and every country across the world in order to maintain transparency in their final

accounts. It also guides to run all the operational activities effectively and smoothly. With the

help of this standards companies can ignore contingencies and enhance their performance. Under

this, various standards are set out by IASB in order to provide ease in the process of financial

reporting. The firms who are applying these can get advantages such as reduced frauds and risks.

All the nations in the world are having their own accounting standards that are followed

by them while formulating statements like income statement, balance sheet, statement for

comprehensive income and cash flow statement. This is possible that these standards are having

issues so IFRS can help to resolve all the issues. Such type of problems can affect investors

decisions as it can result in decreased profits. In United Kingdom, accounting standard boards

issues standards for the process of formulation of financial reports that are applicable for every

10

as it is mainly based on broad principles. It provides liberty to the organisations of

choosing the format for presentation which suits to its users and stakeholders.

It has simplified the accounting procedure for multinational companies who are operating

their businesses in different countries.

It helps to reduce business costs to the organisations of preparing financial statements

oriented for international customers.

It assists those organisations who are willing to deal in foreign trade and are trying to

expand their business globally.

IFRS is mainly introduced by IASB to direct companies while they are generating their

financial statements in order to analyse actual position of company. It has succeeded in

this task as companies are now able to acquire more and more profits.

All the above mentioned advantages are related to the IFRS it, helps organisation to

formulated their financial statements accurately. The business entities who are adopting these

standards can attain various benefits with the help of IFRS as it guides to record appropriate

information to the final accounts.

9.Various degree of compliances with the IFRS by firms across the globe and components

affecting it

IFRS is a standard which is used by most of the company while generating their financial

statements (Ball, Jayaraman and Shivakumar, 2012.). This a type of standards which is used by

almost each and every country across the world in order to maintain transparency in their final

accounts. It also guides to run all the operational activities effectively and smoothly. With the

help of this standards companies can ignore contingencies and enhance their performance. Under

this, various standards are set out by IASB in order to provide ease in the process of financial

reporting. The firms who are applying these can get advantages such as reduced frauds and risks.

All the nations in the world are having their own accounting standards that are followed

by them while formulating statements like income statement, balance sheet, statement for

comprehensive income and cash flow statement. This is possible that these standards are having

issues so IFRS can help to resolve all the issues. Such type of problems can affect investors

decisions as it can result in decreased profits. In United Kingdom, accounting standard boards

issues standards for the process of formulation of financial reports that are applicable for every

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.