Financial Reporting: Glazers Chartered Accountants Financial Analysis

VerifiedAdded on 2021/02/21

|17

|4543

|98

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, focusing on the context, purpose, and key principles of financial reporting, including the conceptual and regulatory frameworks. It examines the main stakeholders of an organization and the benefits they derive from financial information, such as employees, managers, investors, and creditors. The report explores the value of financial reporting in meeting organizational objectives and fostering growth, detailing the preparation of main financial statements, including the profit and loss statement and the statement of changes in equity, based on provided information. It also covers the interpretation and communication of financial performance, including the differences between International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), and the advantages of the international financial reporting system. The report concludes by assessing the degree of compliance with international financial-reporting standards.

FINANCIAL-

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1.Context and purpose of financial reporting..............................................................................3

2. Conceptual, regulatory framework, key principle and qualitative characteristics..................4

3. Main stakeholders of an organisation and the benefit they get from financial information.. 5

4. Value of financial reporting for meeting organisational objectives and growth.....................6

5. Preparation of main financial statements on the basis of given information..........................7

6. Interpretation and communication of financial performance..................................................9

7. The difference between international Accounting Standards (IAS) and if international

Financial Reporting Standards (IFRS)......................................................................................14

8. Advantage of International financial reporting system.........................................................15

9. Degree of compliance with international financial-reporting standards...............................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1.Context and purpose of financial reporting..............................................................................3

2. Conceptual, regulatory framework, key principle and qualitative characteristics..................4

3. Main stakeholders of an organisation and the benefit they get from financial information.. 5

4. Value of financial reporting for meeting organisational objectives and growth.....................6

5. Preparation of main financial statements on the basis of given information..........................7

6. Interpretation and communication of financial performance..................................................9

7. The difference between international Accounting Standards (IAS) and if international

Financial Reporting Standards (IFRS)......................................................................................14

8. Advantage of International financial reporting system.........................................................15

9. Degree of compliance with international financial-reporting standards...............................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

The financial reporting may be defined as a method of analysing and spreading

information of financial position to external and internal stakeholders of companies (Chen,

Zhang and Zhou, 2018). This is necessary for companies to prepare financial reports at the end of

a particular financial year. It is so because by help of these reports, external stakeholders can

assess the information about financial condition and on the basis of it make investment. As well

as, the external stakeholders can also take many crucial decisions on the basis of information

provided under financial reports. For better understanding, a large accountancy firm is selected

that is Glazers Chartered Accountants. This company is located at London, UK and provides

financial services to a vital range of clients. Under the project, objective of financial reporting

and interpretation of these statements are done. In addition, evaluation of financial reporting

standards, models are detailed along with differences in international financial reporting. .

MAIN BODY

1.Context and purpose of financial reporting.

Financial reporting can be defined as preparation of reports on the basis of analysis of

financial statements in an effective manner. This is essential as with the assistance of this,

company’s manager can able to evaluate the actual position in context of finance so that as per

this, they can formulate effective decisions (Saccon and Dima, 2015). Moreover, financial

reports consist several statements like balance sheet, income statement and many others. In

addition to this, it is also related with the regulatory framework. Also, the respective reporting

includes accountabilities as well as duties of accountable individuals of organisation. Glazers

Chartered Accountants formulate this particular report for assessing their financial position and

also for analysing the field where improvement is required. The main purpose of financial

reporting is to aids firm to follow various types of regulations.

Financial reporting facilitates detailed data in context of firm's financial position.

This helps in assuring that companies are applying same regulations.

Also, financial reports are vital for enhancing the capital of the organisation. This is so

because by help of these reports companies can analyse need of future capital to

accomplish the operations and on the basis of it raise the capital.

The financial reporting may be defined as a method of analysing and spreading

information of financial position to external and internal stakeholders of companies (Chen,

Zhang and Zhou, 2018). This is necessary for companies to prepare financial reports at the end of

a particular financial year. It is so because by help of these reports, external stakeholders can

assess the information about financial condition and on the basis of it make investment. As well

as, the external stakeholders can also take many crucial decisions on the basis of information

provided under financial reports. For better understanding, a large accountancy firm is selected

that is Glazers Chartered Accountants. This company is located at London, UK and provides

financial services to a vital range of clients. Under the project, objective of financial reporting

and interpretation of these statements are done. In addition, evaluation of financial reporting

standards, models are detailed along with differences in international financial reporting. .

MAIN BODY

1.Context and purpose of financial reporting.

Financial reporting can be defined as preparation of reports on the basis of analysis of

financial statements in an effective manner. This is essential as with the assistance of this,

company’s manager can able to evaluate the actual position in context of finance so that as per

this, they can formulate effective decisions (Saccon and Dima, 2015). Moreover, financial

reports consist several statements like balance sheet, income statement and many others. In

addition to this, it is also related with the regulatory framework. Also, the respective reporting

includes accountabilities as well as duties of accountable individuals of organisation. Glazers

Chartered Accountants formulate this particular report for assessing their financial position and

also for analysing the field where improvement is required. The main purpose of financial

reporting is to aids firm to follow various types of regulations.

Financial reporting facilitates detailed data in context of firm's financial position.

This helps in assuring that companies are applying same regulations.

Also, financial reports are vital for enhancing the capital of the organisation. This is so

because by help of these reports companies can analyse need of future capital to

accomplish the operations and on the basis of it raise the capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Therefore, these are the essential financial reporting purpose. Thus, in Glazers Chartered

Accountants this particular reporting plays whole all give roles effectively and efficiently.

2. Conceptual, regulatory framework, key principle and qualitative characteristics

Conceptual and Regulatory Framework- Financial reporting is defined as preparation

of different types of financial data for making better decision and plans to achieve goal and

objectives of organisation (Setia, Abhayawansa, Joshi and Huynh, 2015). The stakeholders such

as customers, suppliers, government, authorities always keep their eyes on respective

organisation financial performance in order to do investment accordingly.

The term conceptual is associated with process of preparation of various kind of financial

reports on particular time period. Eventually, ideal time to prepare and present financial reports

at end of financial year.

Regulatory Framework- This is defined as preparing financial report by using proper

accounting principles and standards which assist in getting consistency and accuracy for

financial statements. Glazers Chartered Accountant Company has to follow proper standards,

principles and rules of accounting according to international financial reporting.

Principals of financial reporting:

Materiality- According to this principle, only material and realistic information should

be included in financial statement. Glazers Charted Accountant Company has to include

such principle in their report for correct and accurate outcomes. It is usually implemented

in such situation where accounting effect is less than financial reports. As

Full Disclosure- According to this principle, it is essential to provide full and complete

information in financial statements. In case of any hidden or not disclosed information is

included in report then it leads problems in decision making. The respective organisation

has to included all relevant information while preparing financial statement to achieve

goal and objectives of business. The purpose of this is to include all kind of financial

information as well as transactions that occurs during a particular time period.

Qualitative Characteristics of Financial Reports

In order to prepare financial reports, there are some characteristics which has to be used

by respective organisation. They are described below:

Accountants this particular reporting plays whole all give roles effectively and efficiently.

2. Conceptual, regulatory framework, key principle and qualitative characteristics

Conceptual and Regulatory Framework- Financial reporting is defined as preparation

of different types of financial data for making better decision and plans to achieve goal and

objectives of organisation (Setia, Abhayawansa, Joshi and Huynh, 2015). The stakeholders such

as customers, suppliers, government, authorities always keep their eyes on respective

organisation financial performance in order to do investment accordingly.

The term conceptual is associated with process of preparation of various kind of financial

reports on particular time period. Eventually, ideal time to prepare and present financial reports

at end of financial year.

Regulatory Framework- This is defined as preparing financial report by using proper

accounting principles and standards which assist in getting consistency and accuracy for

financial statements. Glazers Chartered Accountant Company has to follow proper standards,

principles and rules of accounting according to international financial reporting.

Principals of financial reporting:

Materiality- According to this principle, only material and realistic information should

be included in financial statement. Glazers Charted Accountant Company has to include

such principle in their report for correct and accurate outcomes. It is usually implemented

in such situation where accounting effect is less than financial reports. As

Full Disclosure- According to this principle, it is essential to provide full and complete

information in financial statements. In case of any hidden or not disclosed information is

included in report then it leads problems in decision making. The respective organisation

has to included all relevant information while preparing financial statement to achieve

goal and objectives of business. The purpose of this is to include all kind of financial

information as well as transactions that occurs during a particular time period.

Qualitative Characteristics of Financial Reports

In order to prepare financial reports, there are some characteristics which has to be used

by respective organisation. They are described below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Comparability- This is a kind of characteristic of financial reports which defines that

financial reports can be compared with previous years reports. Here, there is comparison

of reports from one year to another. This is possible through using of common accounting

principle for whole financial years. It helps in providing more reliable information to

users.

Understandability- The financial report should contain information which should be

understandable by both internal and external stakeholders for knowing about financial

performance of organisation (Marshall, Schroeder and Yohn, 2018).

3. Main stakeholders of an organisation and the benefit they get from financial information.

Stakeholders are considered to be the person who reflects its interest within firm's

financial performance. So, it is essential to understand that stakeholders can be effected through

the modification into the company's policies as well as plans. Whole stakeholders of the firm are

not similar as all has several aim. For example: In Glazers, Chartered Accountants company has

generally two types of stakeholders such as external and internal. Both of them are discussed

below: Internal stakeholders: These stakeholders are the people or group who are involved

within the internal operations of organisation or who are directly impacted through

management decisions. Few internal stakeholders are staff, customers and others. All

these are important for the organisations as business activities and functions are

performed through them. Few kinds of Glazers Chartered Accountants internal

stakeholders are discussed below:

◦ Employees: These stakeholders are associated with accomplishing the activities of

firm where they perform (Velte and Stawinoga, 2017). Employees are considered as

essential for organisation as if staff does not work effectively then it can drive

towards ineffectiveness in performing task. The employees are benefited from

financial informations in order to take decision whether they should sustain in

company or not. This is so because if companies financial position is weak then

employees will not prefer to sustain due to risk of lower future growth. Therefore,

Glazers Chartered Accountants staff can check financial performance of several

activities to ascertain either they have to continue its work with respective company

or not.

financial reports can be compared with previous years reports. Here, there is comparison

of reports from one year to another. This is possible through using of common accounting

principle for whole financial years. It helps in providing more reliable information to

users.

Understandability- The financial report should contain information which should be

understandable by both internal and external stakeholders for knowing about financial

performance of organisation (Marshall, Schroeder and Yohn, 2018).

3. Main stakeholders of an organisation and the benefit they get from financial information.

Stakeholders are considered to be the person who reflects its interest within firm's

financial performance. So, it is essential to understand that stakeholders can be effected through

the modification into the company's policies as well as plans. Whole stakeholders of the firm are

not similar as all has several aim. For example: In Glazers, Chartered Accountants company has

generally two types of stakeholders such as external and internal. Both of them are discussed

below: Internal stakeholders: These stakeholders are the people or group who are involved

within the internal operations of organisation or who are directly impacted through

management decisions. Few internal stakeholders are staff, customers and others. All

these are important for the organisations as business activities and functions are

performed through them. Few kinds of Glazers Chartered Accountants internal

stakeholders are discussed below:

◦ Employees: These stakeholders are associated with accomplishing the activities of

firm where they perform (Velte and Stawinoga, 2017). Employees are considered as

essential for organisation as if staff does not work effectively then it can drive

towards ineffectiveness in performing task. The employees are benefited from

financial informations in order to take decision whether they should sustain in

company or not. This is so because if companies financial position is weak then

employees will not prefer to sustain due to risk of lower future growth. Therefore,

Glazers Chartered Accountants staff can check financial performance of several

activities to ascertain either they have to continue its work with respective company

or not.

◦ Manager: These types of internal stakeholders are very essential for organisation as

they are related with policies as well as plans formation for managing the resources

such as financial and human effectually and efficaciously. The success of the firm is

based upon the managers which shows that how they handle its subordinates. The

managers are get benefited from financial information because by help of utilisation

of proper financial informations they can make future plans and policies. As well as

can modify current years plans effectively. External stakeholders: These are the one who regularly analysis firm's financial

position for taking decision related to investment. These stakeholders do not get impacted

with the modification within the policies as well as plans of organisation as its objectives

is to accumulate data regarding financial performance as well as spends money

consequently. Few Glazers Chartered Accountants external stakeholders are discussed

below:

◦ Investors: This external stakeholder are the one who do investment within

organisation's projects as well as operations according to the financial situation

(Szabó and Sørensen, 2017). Its objectives is to obtain higher return on amount that is

invested by them. They obtain advantage from the firm's financial data to develop

decisions regarding investment as if they do not have any ideas about financial

position then this can be the risk for them. So, Glazers Chartered Accountants

investors analysis its financial condition as well as then do investment.

◦ Creditors: These stakeholders are associated with facilitating monetary help to firm

on credit. They take advantage from the financial data of organisation in respect of

deciding the financial status. Therefore, with the assistance of financial information

respective organisation can ascertain their credit score.

4. Value of financial reporting for meeting organisational objectives and growth

Financial reporting is considered as the essential aspects in order to attain the objectives

of the company and their development. It is so as with the assistance of financial reporting

evaluation firms can able to analysis the changes that are to be performed for attaining goals.

Financial reporting in order to meet objectives of firm: Financial reporting is related with

the organisational objectives as firm's manager can ascertain that what type of strategy is

required to be executed for achieving the goals (Pan and Patel, 2018). Glazers Chartered

they are related with policies as well as plans formation for managing the resources

such as financial and human effectually and efficaciously. The success of the firm is

based upon the managers which shows that how they handle its subordinates. The

managers are get benefited from financial information because by help of utilisation

of proper financial informations they can make future plans and policies. As well as

can modify current years plans effectively. External stakeholders: These are the one who regularly analysis firm's financial

position for taking decision related to investment. These stakeholders do not get impacted

with the modification within the policies as well as plans of organisation as its objectives

is to accumulate data regarding financial performance as well as spends money

consequently. Few Glazers Chartered Accountants external stakeholders are discussed

below:

◦ Investors: This external stakeholder are the one who do investment within

organisation's projects as well as operations according to the financial situation

(Szabó and Sørensen, 2017). Its objectives is to obtain higher return on amount that is

invested by them. They obtain advantage from the firm's financial data to develop

decisions regarding investment as if they do not have any ideas about financial

position then this can be the risk for them. So, Glazers Chartered Accountants

investors analysis its financial condition as well as then do investment.

◦ Creditors: These stakeholders are associated with facilitating monetary help to firm

on credit. They take advantage from the financial data of organisation in respect of

deciding the financial status. Therefore, with the assistance of financial information

respective organisation can ascertain their credit score.

4. Value of financial reporting for meeting organisational objectives and growth

Financial reporting is considered as the essential aspects in order to attain the objectives

of the company and their development. It is so as with the assistance of financial reporting

evaluation firms can able to analysis the changes that are to be performed for attaining goals.

Financial reporting in order to meet objectives of firm: Financial reporting is related with

the organisational objectives as firm's manager can ascertain that what type of strategy is

required to be executed for achieving the goals (Pan and Patel, 2018). Glazers Chartered

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accountants attain its objectives effectually through usages of financial reports. This becomes

possible as this particular reports show the actual results of several types of business practices

and according to this effective actions are taken through the manager of respective organisation.

Financial reporting for attaining growth: The another purpose of financial reporting is to

aids firm for future development as well as growth as this facilitates firm's present situation and

according to it they approximate the upcoming growth. For example: In this above, Glazers

Chartered Accountants company managers handle as well as sustain its growth with the

assistance of financial reporting. Thus, this can be considered that this particular report are

significant for the organisational growth.

Apart from it, there are some objectives of financial-reporting are mentioned in order to meet

objectives and attain growth :

Improved debt management- This is one of the important purpose of financial-reporting

which is linked with process of managing debts. It becomes possible because by help of

assessing information about taken short and long term loans, managers can aware that

which debts are needed to pay instantly. By this companies become able to attain growth.

In addition, the financial reporting is crucial for providing complete information about

external shareholders so that companies can make plans and policies to complete

objectives.

As well as the financial-reporting is beneficial for improving social welfare by

considering interest of employees. It overall leads to equal growth of employees and

organisation.

So these are the objectives of financial-reporting that are linked with achieving organisational

goals and objectives.

5. Preparation of main financial statements on the basis of given information.

A) Profit and Loss statement

31.12.18

(£'000)

Continuing operations

Particulars Amount

Revenue from Operations (A) 585100

possible as this particular reports show the actual results of several types of business practices

and according to this effective actions are taken through the manager of respective organisation.

Financial reporting for attaining growth: The another purpose of financial reporting is to

aids firm for future development as well as growth as this facilitates firm's present situation and

according to it they approximate the upcoming growth. For example: In this above, Glazers

Chartered Accountants company managers handle as well as sustain its growth with the

assistance of financial reporting. Thus, this can be considered that this particular report are

significant for the organisational growth.

Apart from it, there are some objectives of financial-reporting are mentioned in order to meet

objectives and attain growth :

Improved debt management- This is one of the important purpose of financial-reporting

which is linked with process of managing debts. It becomes possible because by help of

assessing information about taken short and long term loans, managers can aware that

which debts are needed to pay instantly. By this companies become able to attain growth.

In addition, the financial reporting is crucial for providing complete information about

external shareholders so that companies can make plans and policies to complete

objectives.

As well as the financial-reporting is beneficial for improving social welfare by

considering interest of employees. It overall leads to equal growth of employees and

organisation.

So these are the objectives of financial-reporting that are linked with achieving organisational

goals and objectives.

5. Preparation of main financial statements on the basis of given information.

A) Profit and Loss statement

31.12.18

(£'000)

Continuing operations

Particulars Amount

Revenue from Operations (A) 585100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

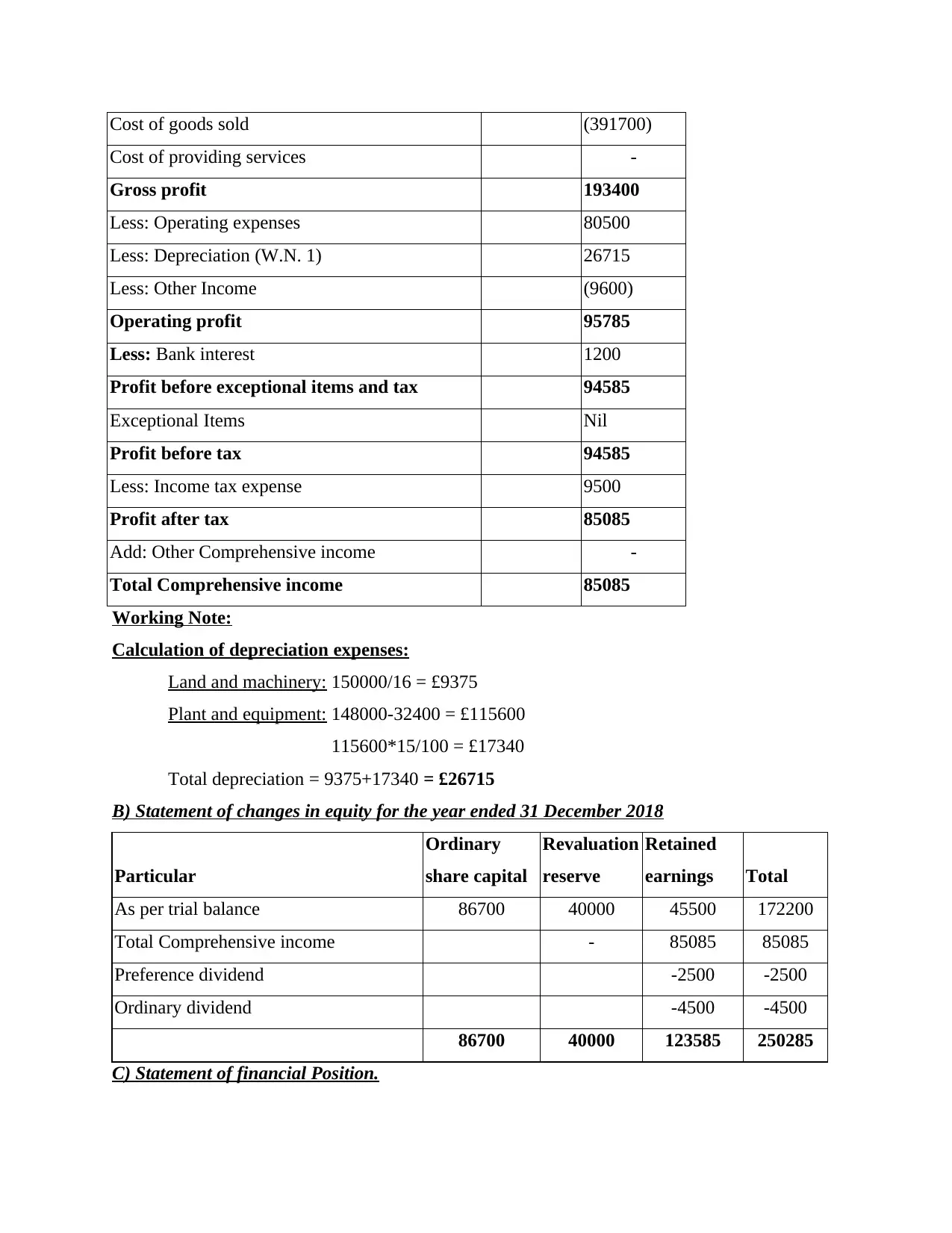

Cost of goods sold (391700)

Cost of providing services -

Gross profit 193400

Less: Operating expenses 80500

Less: Depreciation (W.N. 1) 26715

Less: Other Income (9600)

Operating profit 95785

Less: Bank interest 1200

Profit before exceptional items and tax 94585

Exceptional Items Nil

Profit before tax 94585

Less: Income tax expense 9500

Profit after tax 85085

Add: Other Comprehensive income -

Total Comprehensive income 85085

Working Note:

Calculation of depreciation expenses:

Land and machinery: 150000/16 = £9375

Plant and equipment: 148000-32400 = £115600

115600*15/100 = £17340

Total depreciation = 9375+17340 = £26715

B) Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluation

reserve

Retained

earnings Total

As per trial balance 86700 40000 45500 172200

Total Comprehensive income - 85085 85085

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

C) Statement of financial Position.

Cost of providing services -

Gross profit 193400

Less: Operating expenses 80500

Less: Depreciation (W.N. 1) 26715

Less: Other Income (9600)

Operating profit 95785

Less: Bank interest 1200

Profit before exceptional items and tax 94585

Exceptional Items Nil

Profit before tax 94585

Less: Income tax expense 9500

Profit after tax 85085

Add: Other Comprehensive income -

Total Comprehensive income 85085

Working Note:

Calculation of depreciation expenses:

Land and machinery: 150000/16 = £9375

Plant and equipment: 148000-32400 = £115600

115600*15/100 = £17340

Total depreciation = 9375+17340 = £26715

B) Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluation

reserve

Retained

earnings Total

As per trial balance 86700 40000 45500 172200

Total Comprehensive income - 85085 85085

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

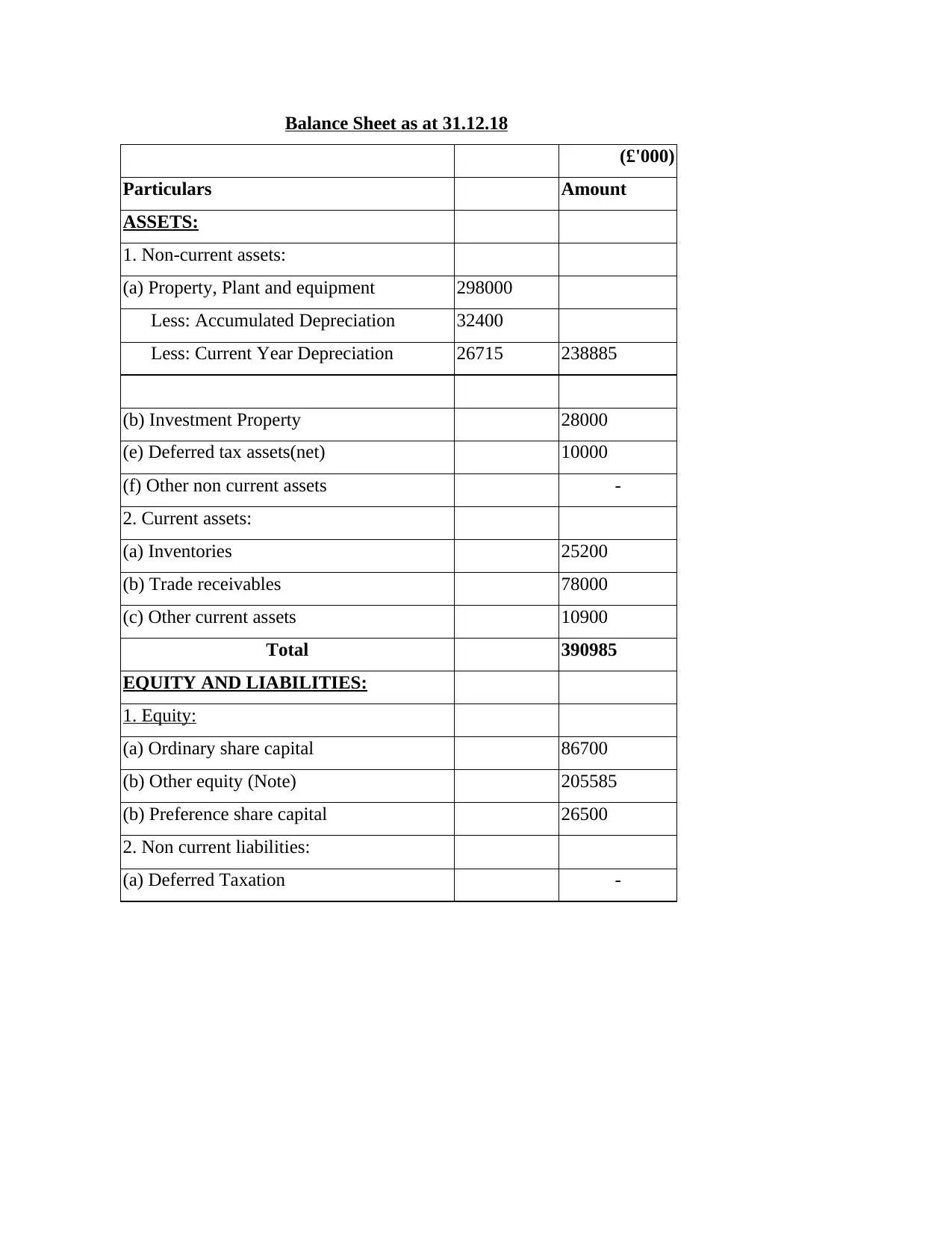

C) Statement of financial Position.

Balance Sheet as at 31.12.18

(£'000)

Particulars Amount

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

1. Equity:

(a) Ordinary share capital 86700

(b) Other equity (Note) 205585

(b) Preference share capital 26500

2. Non current liabilities:

(a) Deferred Taxation -

(£'000)

Particulars Amount

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

1. Equity:

(a) Ordinary share capital 86700

(b) Other equity (Note) 205585

(b) Preference share capital 26500

2. Non current liabilities:

(a) Deferred Taxation -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

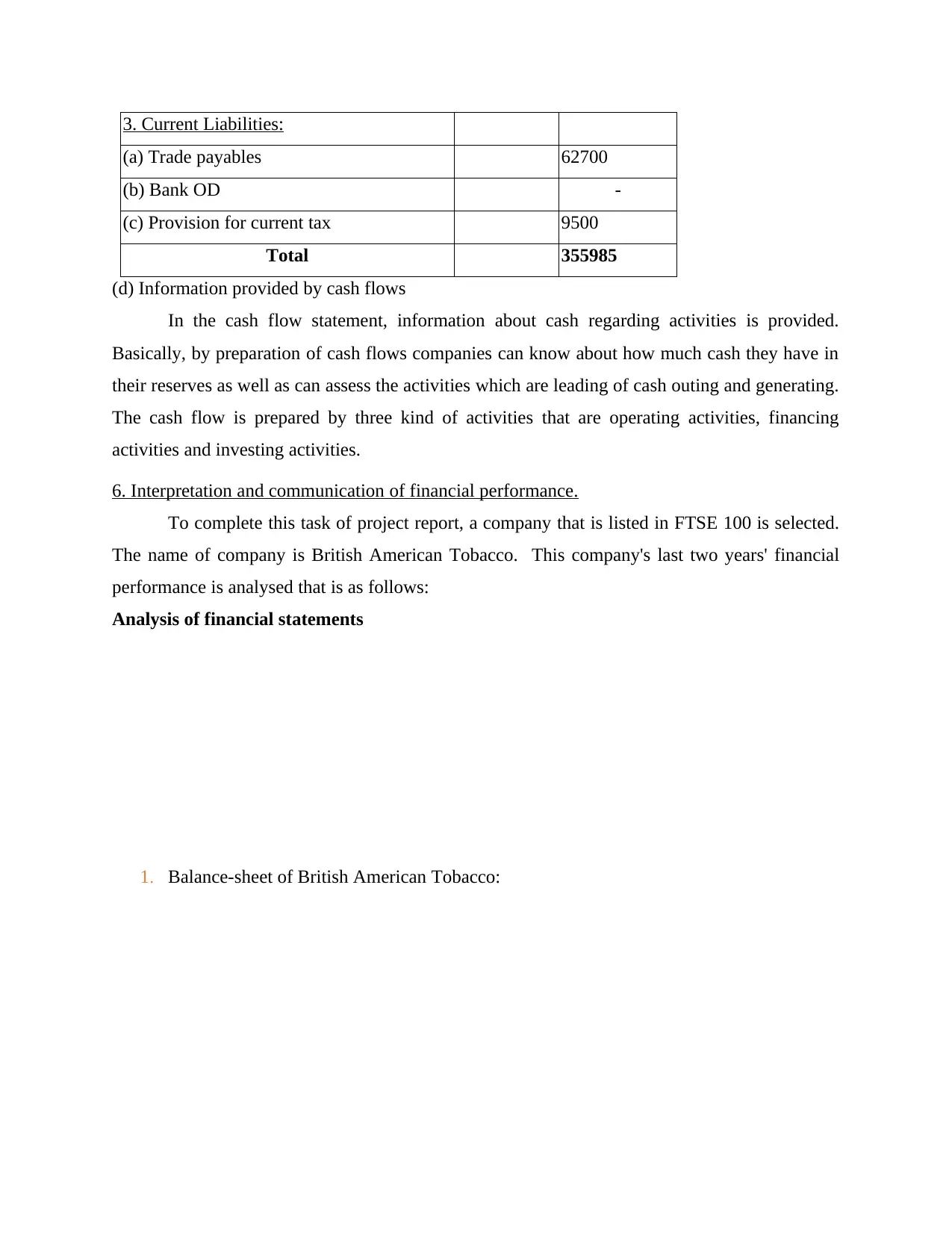

3. Current Liabilities:

(a) Trade payables 62700

(b) Bank OD -

(c) Provision for current tax 9500

Total 355985

(d) Information provided by cash flows

In the cash flow statement, information about cash regarding activities is provided.

Basically, by preparation of cash flows companies can know about how much cash they have in

their reserves as well as can assess the activities which are leading of cash outing and generating.

The cash flow is prepared by three kind of activities that are operating activities, financing

activities and investing activities.

6. Interpretation and communication of financial performance.

To complete this task of project report, a company that is listed in FTSE 100 is selected.

The name of company is British American Tobacco. This company's last two years' financial

performance is analysed that is as follows:

Analysis of financial statements

1. Balance-sheet of British American Tobacco:

(a) Trade payables 62700

(b) Bank OD -

(c) Provision for current tax 9500

Total 355985

(d) Information provided by cash flows

In the cash flow statement, information about cash regarding activities is provided.

Basically, by preparation of cash flows companies can know about how much cash they have in

their reserves as well as can assess the activities which are leading of cash outing and generating.

The cash flow is prepared by three kind of activities that are operating activities, financing

activities and investing activities.

6. Interpretation and communication of financial performance.

To complete this task of project report, a company that is listed in FTSE 100 is selected.

The name of company is British American Tobacco. This company's last two years' financial

performance is analysed that is as follows:

Analysis of financial statements

1. Balance-sheet of British American Tobacco:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BRITISH AMERICAN TOBACCO PLC (BATS) BALANCE SHEET

Fiscal year ends in December. GBP in millions except per share data. 2017-12 2018-12

Assets

Current assets

Cash

Cash and cash equivalents 3131 2432

Short-term investments 65 178

Total cash 3196 2610

Receivables 4053 3588

Inventories 5864 6029

Other current assets 853 428

Total current assets 13966 12655

Non-current assets

Property, plant and equipment

Gross property, plant and equipment 8191 8654

Accumulated Depreciation -3309 -3488

Net property, plant and equipment 4882 5166

Goodwill 44147 46163

Intangible assets 73638 77850

Deferred income taxes 317 344

Prepaid pension benefit 1123 1147

Other long-term assets 2965 3017

Total non-current assets 127072 133687

Total assets 141038 146342

Liabilities and stockholders' equity

Liabilities

Current liabilities

Capital leases 5423 4225

Accounts payable 8847 10631

Taxes payable 720 853

Other current liabilities 554 620

Total current liabilities 15544 16329

Non-current liabilities

Deferred taxes liabilities 17129 17776

Pensions and other benefits 1821 1665

Minority interest 222 244

Other long-term liabilities 45518 44884

Total non-current liabilities 64690 64569

Total liabilities 80234 80898

Stockholders' equity

Common stock 614 614

Additional paid-in capital 26602 192

Retained earnings 36983 38557

Accumulated other comprehensive income -3395 26081

Total stockholders' equity 60804 65444

Total liabilities and stockholders' equity 141038 146342

Interpretation- On the basis of above balance-sheet, this can be find out that company's total

assets are increasing in current year 2018 as compare to previous year 2017. Such as in year

2017, the amount of total assets was of £ 141038 GBP million that increased and became of £

Fiscal year ends in December. GBP in millions except per share data. 2017-12 2018-12

Assets

Current assets

Cash

Cash and cash equivalents 3131 2432

Short-term investments 65 178

Total cash 3196 2610

Receivables 4053 3588

Inventories 5864 6029

Other current assets 853 428

Total current assets 13966 12655

Non-current assets

Property, plant and equipment

Gross property, plant and equipment 8191 8654

Accumulated Depreciation -3309 -3488

Net property, plant and equipment 4882 5166

Goodwill 44147 46163

Intangible assets 73638 77850

Deferred income taxes 317 344

Prepaid pension benefit 1123 1147

Other long-term assets 2965 3017

Total non-current assets 127072 133687

Total assets 141038 146342

Liabilities and stockholders' equity

Liabilities

Current liabilities

Capital leases 5423 4225

Accounts payable 8847 10631

Taxes payable 720 853

Other current liabilities 554 620

Total current liabilities 15544 16329

Non-current liabilities

Deferred taxes liabilities 17129 17776

Pensions and other benefits 1821 1665

Minority interest 222 244

Other long-term liabilities 45518 44884

Total non-current liabilities 64690 64569

Total liabilities 80234 80898

Stockholders' equity

Common stock 614 614

Additional paid-in capital 26602 192

Retained earnings 36983 38557

Accumulated other comprehensive income -3395 26081

Total stockholders' equity 60804 65444

Total liabilities and stockholders' equity 141038 146342

Interpretation- On the basis of above balance-sheet, this can be find out that company's total

assets are increasing in current year 2018 as compare to previous year 2017. Such as in year

2017, the amount of total assets was of £ 141038 GBP million that increased and became of £

146342 GBP million in year 2019. While the total liabilities were of £ 80234 GBP million that

raised and became of £ 80898 GBP million in year 2018. It is showing that company has enough

number of assets to make payment of their liabilities.

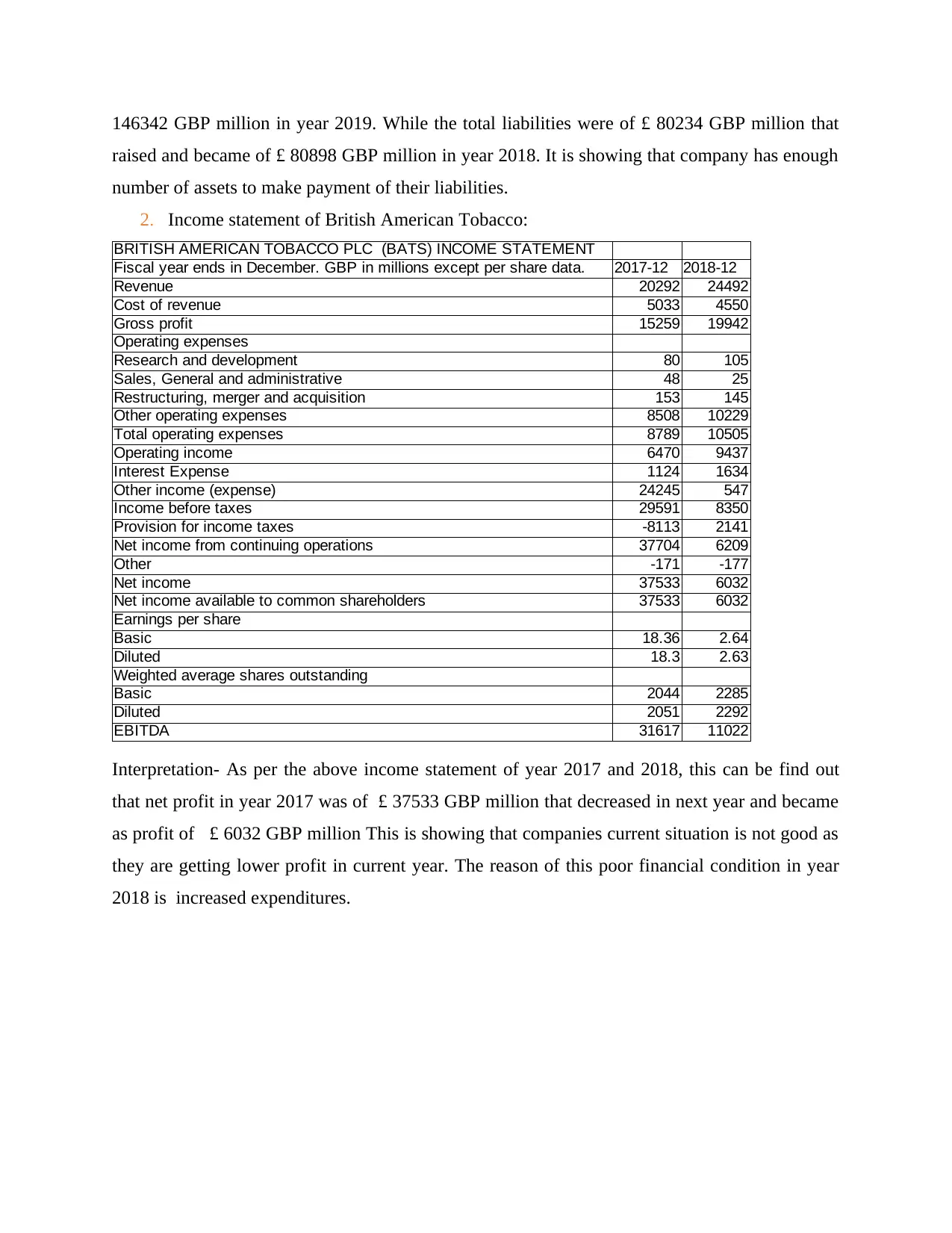

2. Income statement of British American Tobacco:

BRITISH AMERICAN TOBACCO PLC (BATS) INCOME STATEMENT

Fiscal year ends in December. GBP in millions except per share data. 2017-12 2018-12

Revenue 20292 24492

Cost of revenue 5033 4550

Gross profit 15259 19942

Operating expenses

Research and development 80 105

Sales, General and administrative 48 25

Restructuring, merger and acquisition 153 145

Other operating expenses 8508 10229

Total operating expenses 8789 10505

Operating income 6470 9437

Interest Expense 1124 1634

Other income (expense) 24245 547

Income before taxes 29591 8350

Provision for income taxes -8113 2141

Net income from continuing operations 37704 6209

Other -171 -177

Net income 37533 6032

Net income available to common shareholders 37533 6032

Earnings per share

Basic 18.36 2.64

Diluted 18.3 2.63

Weighted average shares outstanding

Basic 2044 2285

Diluted 2051 2292

EBITDA 31617 11022

Interpretation- As per the above income statement of year 2017 and 2018, this can be find out

that net profit in year 2017 was of £ 37533 GBP million that decreased in next year and became

as profit of £ 6032 GBP million This is showing that companies current situation is not good as

they are getting lower profit in current year. The reason of this poor financial condition in year

2018 is increased expenditures.

raised and became of £ 80898 GBP million in year 2018. It is showing that company has enough

number of assets to make payment of their liabilities.

2. Income statement of British American Tobacco:

BRITISH AMERICAN TOBACCO PLC (BATS) INCOME STATEMENT

Fiscal year ends in December. GBP in millions except per share data. 2017-12 2018-12

Revenue 20292 24492

Cost of revenue 5033 4550

Gross profit 15259 19942

Operating expenses

Research and development 80 105

Sales, General and administrative 48 25

Restructuring, merger and acquisition 153 145

Other operating expenses 8508 10229

Total operating expenses 8789 10505

Operating income 6470 9437

Interest Expense 1124 1634

Other income (expense) 24245 547

Income before taxes 29591 8350

Provision for income taxes -8113 2141

Net income from continuing operations 37704 6209

Other -171 -177

Net income 37533 6032

Net income available to common shareholders 37533 6032

Earnings per share

Basic 18.36 2.64

Diluted 18.3 2.63

Weighted average shares outstanding

Basic 2044 2285

Diluted 2051 2292

EBITDA 31617 11022

Interpretation- As per the above income statement of year 2017 and 2018, this can be find out

that net profit in year 2017 was of £ 37533 GBP million that decreased in next year and became

as profit of £ 6032 GBP million This is showing that companies current situation is not good as

they are getting lower profit in current year. The reason of this poor financial condition in year

2018 is increased expenditures.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.