University Finance Assignment: Financial Reporting and AASB 116

VerifiedAdded on 2020/04/07

|10

|2051

|53

Report

AI Summary

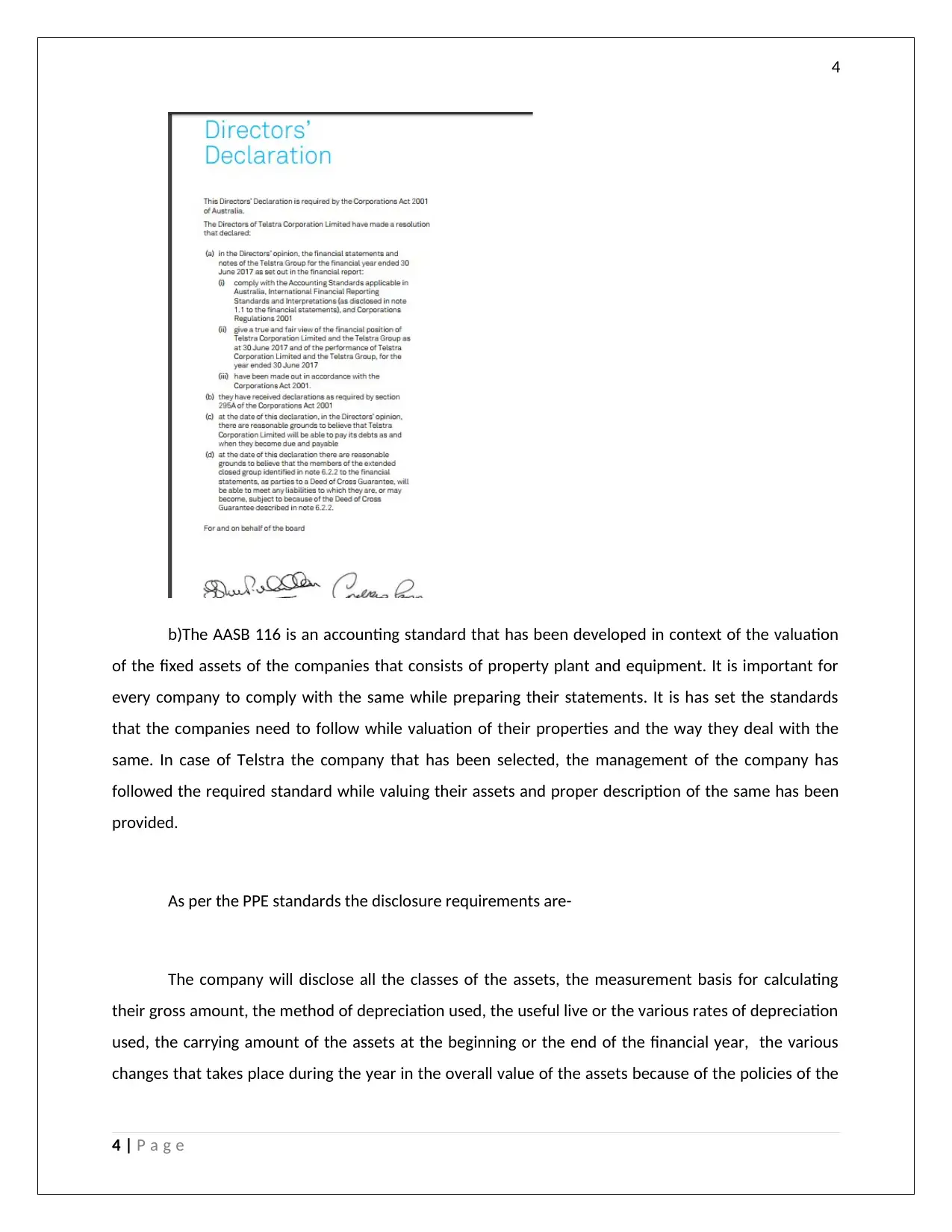

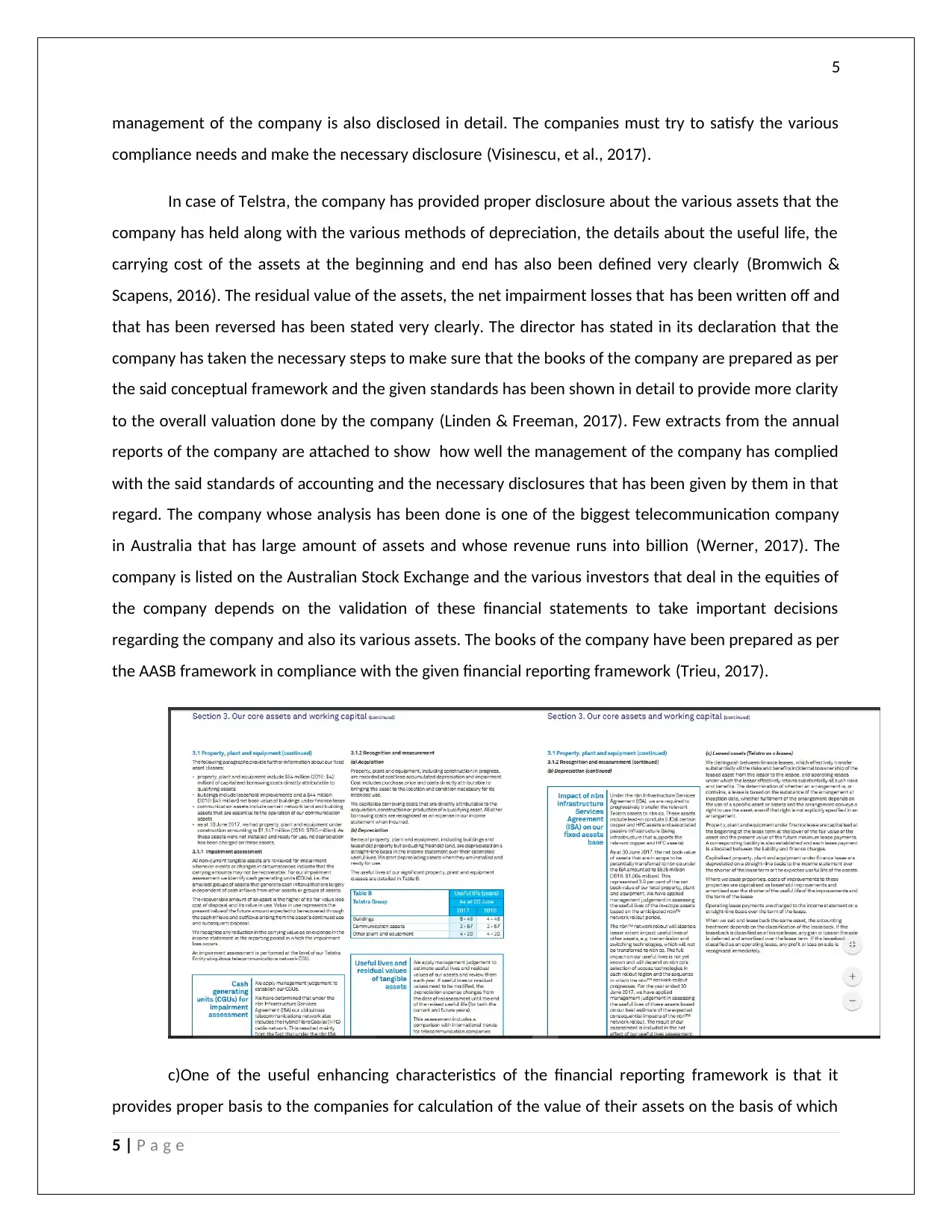

This report provides an executive summary and detailed analysis of financial reporting standards, focusing on the conceptual framework and AASB 116. It explores the objectives of the general-purpose framework and its implications, particularly in relation to property, plant, and equipment valuation. The report examines how companies prepare and present financial statements, emphasizing the importance of adhering to accounting standards and ensuring the needs of end-users are met. It includes a case study using Telstra to illustrate the application of AASB 116, including disclosure requirements and the impact on financial reporting. The report also discusses the enhancing qualitative characteristics of the financial reporting framework and concludes with the importance of transparency and accuracy in financial statements. It suggests areas for improvement in the framework, such as simplifying application and enhancing user feedback.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.