Accounting Systems and Processes: Financial Reporting and Analysis

VerifiedAdded on 2020/04/07

|29

|1869

|36

Homework Assignment

AI Summary

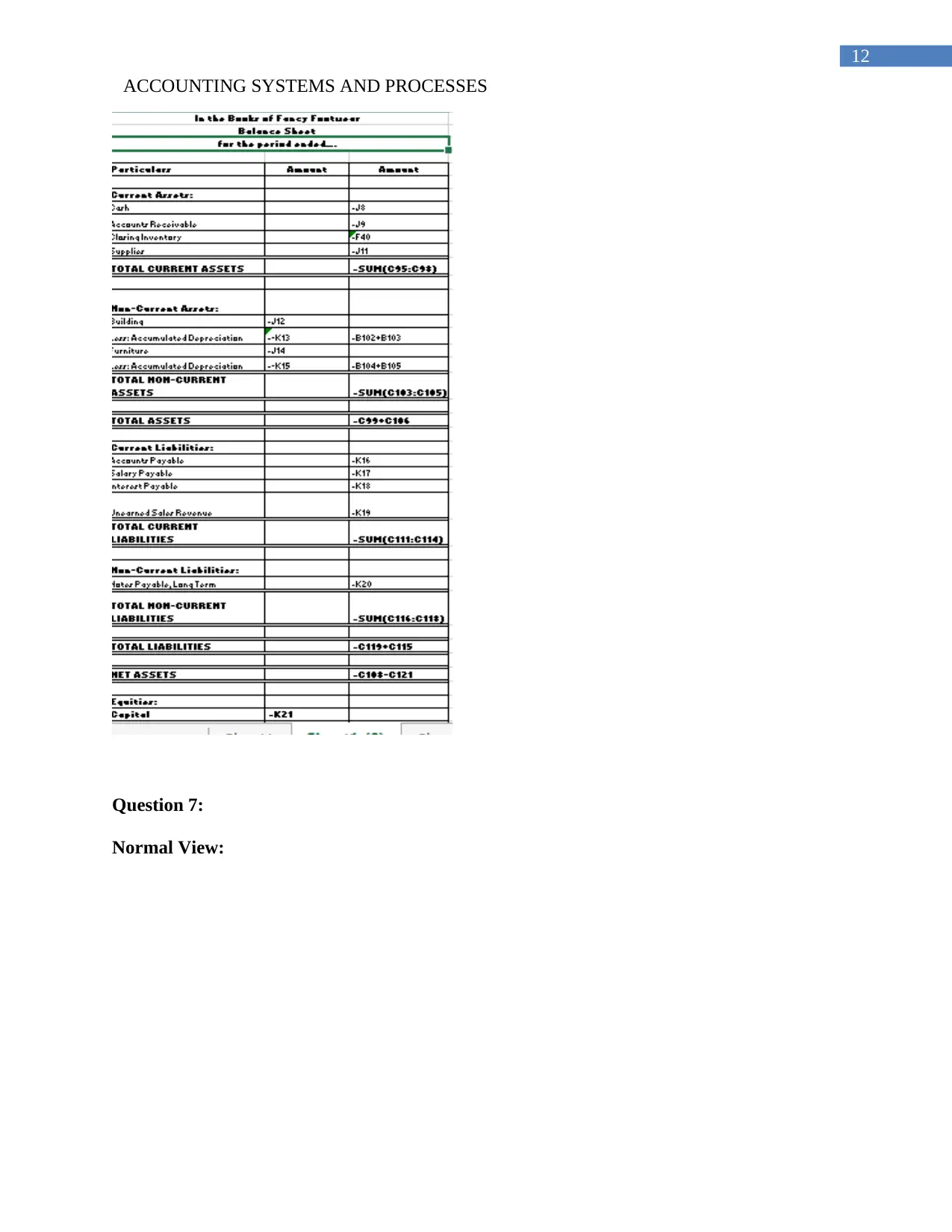

This assignment focuses on accounting systems and processes, covering various aspects of financial reporting and analysis. It includes detailed answers to questions on topics such as cell referencing in Excel, displaying negative numbers, separating data entry and report areas, utilizing IF functions, and understanding periodic inventory systems. The assignment also explores bad debt estimation methods, the role of accounts receivable in evaluating financial position, and provides an analysis of Wesfarmers' financial statements, including its statement of comprehensive income, dividends, earnings per share, return on equity, and risk mitigation strategies. Additionally, it includes calculations of working capital ratios and provides a recommendation for investment based on the analysis. The document also references several accounting research papers.

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.