Financial Reporting: Context, Framework, and Interpretation

VerifiedAdded on 2021/02/20

|16

|3622

|41

Report

AI Summary

This report provides a comprehensive overview of financial reporting, starting with its context and purpose, and then delving into the conceptual and regulatory frameworks that govern it. It explores the different types of stakeholders involved, detailing their interests and the benefits they derive from financial information. The report further examines how financial reports are utilized to meet company growth and objectives, including an analysis of financial statements. It also covers the presentation of financial statements, including profit and loss, changes in equity, and financial position, with examples. The report concludes with an interpretation of financial statements and a comparison of IAS and IFRS, highlighting the benefits of IFRS and the degree of compliance. The report is based on Price water coopers and the FTSE 100 company.

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

QUESTIONS...................................................................................................................................1

1. Context and purpose of financial reporting............................................................................1

2. Conceptual, regulatory framework and reliable financial information...................................2

3. Types of stakeholders and benefits from financial information..............................................3

4. Financial reports to meet companies growth and objectives..................................................4

5. Presentation of financial statements........................................................................................5

6. Interpretation of financial statements of a company which is listed in FTSE 100.................7

7. Comparison between IAS and IFRS.......................................................................................8

8. Benefits of IFRS......................................................................................................................8

9. Degree of compliance with IFRS............................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

INTRODUCTION ..........................................................................................................................1

QUESTIONS...................................................................................................................................1

1. Context and purpose of financial reporting............................................................................1

2. Conceptual, regulatory framework and reliable financial information...................................2

3. Types of stakeholders and benefits from financial information..............................................3

4. Financial reports to meet companies growth and objectives..................................................4

5. Presentation of financial statements........................................................................................5

6. Interpretation of financial statements of a company which is listed in FTSE 100.................7

7. Comparison between IAS and IFRS.......................................................................................8

8. Benefits of IFRS......................................................................................................................8

9. Degree of compliance with IFRS............................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial reporting, is defined as the wider process that includes the disclosure of useful

financial information through preparing and presenting financial statements to specific manager

and general public (Krishnan and Zhang, 2014). There are mainly two main purpose of financial

reporting, it helps accountant to engage in decision making mainly developing strategies to attain

company objective. Secondly, it gives crucial information related with financial status and

strength of firm to stakeholder that includes shareholder, investors, customer and regulator of

government. This report is based on Price water coopers have been selected which is one of the

large accountancy firm which is located in London UK.

In this report, context and purpose of financial reporting, interpretation of financial

statement of selected company from FTSE 100 is selected. Report also evaluate importance of

reporting standard and various theoretical model and concepts, it also evaluate international

differences in financial reporting.

QUESTIONS

1. Context and purpose of financial reporting.

The technique of demonstrating the firm's economic data in the manner of accounts is

known as financial reporting. The main goal of generating the financial statements would be to

remind interested parties regarding the current company's financial situation. As per the

International Accounting Standard Board (IASB), the primary goal of creating financial

statement is to generate valuable information that support to analyse the present financial

situation so that appropriate changes could be produced to enhance the business's position. It was

analysed that financial reporting comprises of a method that might help to track information

relevant to financing so impactful management or control of a an entity can be carried out

(Norwani, Zam and Chek, 2011). In addition, it is observed that International accounting

standard board mainly states that Price water coopers needs to prepare financial statement in

order to give stakeholders with the appropriate information directly relevant to company

resources. Different statement finally display genuine financial situation that can help to attract

new investments or expand current investors' value by shareholder.

Financial reporting is very essential to everyone involved in the activities and tasks of

business firm. There are number of objective of financial reporting that are discussed below:

1

Financial reporting, is defined as the wider process that includes the disclosure of useful

financial information through preparing and presenting financial statements to specific manager

and general public (Krishnan and Zhang, 2014). There are mainly two main purpose of financial

reporting, it helps accountant to engage in decision making mainly developing strategies to attain

company objective. Secondly, it gives crucial information related with financial status and

strength of firm to stakeholder that includes shareholder, investors, customer and regulator of

government. This report is based on Price water coopers have been selected which is one of the

large accountancy firm which is located in London UK.

In this report, context and purpose of financial reporting, interpretation of financial

statement of selected company from FTSE 100 is selected. Report also evaluate importance of

reporting standard and various theoretical model and concepts, it also evaluate international

differences in financial reporting.

QUESTIONS

1. Context and purpose of financial reporting.

The technique of demonstrating the firm's economic data in the manner of accounts is

known as financial reporting. The main goal of generating the financial statements would be to

remind interested parties regarding the current company's financial situation. As per the

International Accounting Standard Board (IASB), the primary goal of creating financial

statement is to generate valuable information that support to analyse the present financial

situation so that appropriate changes could be produced to enhance the business's position. It was

analysed that financial reporting comprises of a method that might help to track information

relevant to financing so impactful management or control of a an entity can be carried out

(Norwani, Zam and Chek, 2011). In addition, it is observed that International accounting

standard board mainly states that Price water coopers needs to prepare financial statement in

order to give stakeholders with the appropriate information directly relevant to company

resources. Different statement finally display genuine financial situation that can help to attract

new investments or expand current investors' value by shareholder.

Financial reporting is very essential to everyone involved in the activities and tasks of

business firm. There are number of objective of financial reporting that are discussed below:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It support in making essential decisions about future improvement and growth as it

consider a broad range of financial data related with company current and past business

transaction. Such as PWC takes the benefit of financial reports in order to make futuristic

determination.

In addition to it also helpful to provide data on net cash inflows and outflows over a

specific accounting year. The same as the respective company evaluate their liquidity

situation with the help of financial reports.

Financial reports assist to provide comprehensive information related with lenders,

debtors, actual investment, etc. Thus manager of PWC can monitor all economic data

with the assistance of financial reports (Perera and Chand, 2015).

2. Conceptual, regulatory framework and reliable financial information.

Conceptual and regulatory framework:

Conceptual and regulatory structure is a collection of strategies and procedures that

support the manager of company to address quantitative and subjective problems. Regulatory

frameworks are helpful for making predictions to improve the effectiveness and productivity of

financial reports and standards. In PWC all the frameworks are implemented while preparing

financial report that gives authentic information for entire year.

There are different types of significant principles of financial reporting that makes

information reliable. Some of these are discussed below:

Consistency: The financial reports must be produced year after year on an ongoing basis

according to this concept. Thus it is essential for preparing financial statements on

consistency principle that help to measure the performance of company by providing

information from past events. Full disclosure of information: According to this concept, most of the information in

the financial reports must be disclosed by company that remove chances of error (Powers,

Robinson and Stomberg, 2016). This is fundamentally essential to incorporate entire

financial business data so stakeholders can be acutely aware of present financial statues

of PWC.

Qualitative features of financial reporting: Some of the important qualitative features of

financial report are discussed below that makes information reliable for interested parties.

2

consider a broad range of financial data related with company current and past business

transaction. Such as PWC takes the benefit of financial reports in order to make futuristic

determination.

In addition to it also helpful to provide data on net cash inflows and outflows over a

specific accounting year. The same as the respective company evaluate their liquidity

situation with the help of financial reports.

Financial reports assist to provide comprehensive information related with lenders,

debtors, actual investment, etc. Thus manager of PWC can monitor all economic data

with the assistance of financial reports (Perera and Chand, 2015).

2. Conceptual, regulatory framework and reliable financial information.

Conceptual and regulatory framework:

Conceptual and regulatory structure is a collection of strategies and procedures that

support the manager of company to address quantitative and subjective problems. Regulatory

frameworks are helpful for making predictions to improve the effectiveness and productivity of

financial reports and standards. In PWC all the frameworks are implemented while preparing

financial report that gives authentic information for entire year.

There are different types of significant principles of financial reporting that makes

information reliable. Some of these are discussed below:

Consistency: The financial reports must be produced year after year on an ongoing basis

according to this concept. Thus it is essential for preparing financial statements on

consistency principle that help to measure the performance of company by providing

information from past events. Full disclosure of information: According to this concept, most of the information in

the financial reports must be disclosed by company that remove chances of error (Powers,

Robinson and Stomberg, 2016). This is fundamentally essential to incorporate entire

financial business data so stakeholders can be acutely aware of present financial statues

of PWC.

Qualitative features of financial reporting: Some of the important qualitative features of

financial report are discussed below that makes information reliable for interested parties.

2

Relevance: It is a type of financial reporting characteristic that specifies the significance

of financial reports to company operations.

Understandability: This qualitative features defines that financial reports must be

prepared in a manner that they are easy to understand by each and every stakeholder that

enables to make valuable decision (Rotimi, 2012).

3. Types of stakeholders and benefits from financial information.

As far as company is concerned, stakeholders can be government, consumers, distributors

or anyone else that gets impacted by organization's strategies. These stakeholders directly and

indirectly affected by alteration in policies of company and are considered as internal and

external stakeholders. In context of PWC there are number of stakeholder those are interested

with financial statements and other information. Some of these are discussed underneath:

Internal stakeholders: Interested parties that participate constantly within operations

and tasks of the company. In addition internal stakeholders, are affected or work according to the

plans and strategies of organizations. Some of these are listed below:

Employees: These stakeholders are engaged in fulfilling the work and operations. for

doing specific task employee are entitled to receive salaries, compensation packages and

other economic advantages (Schaltegger and Burritt, 2017). Employees take advantage of

financial reports by checking their monetary advantages, economic safety, etc.

Management: They are consider as company most significant internal stakeholders.

Thus, they are involved in phase of preparing strategic plans of company and thus

support in effectively managing valuable operations. Management receive appropriate

and necessary data for decision-making from financial reports to increase overall

performance of PWC.

External stakeholder: All those stakeholder those are not directly related with company

but have interest in the financial results and strength of company are consider as external

stakeholder. There are number of external stakeholder, some of these in context of PWC are

discussed below:

Creditors: These stakeholders gives the businesses with economic support and other

loan facilities. Creditors usually shows their interest to company financial reports and

take advantage related to evaluate the actual stability of respective firm in order to make

credit transaction.

3

of financial reports to company operations.

Understandability: This qualitative features defines that financial reports must be

prepared in a manner that they are easy to understand by each and every stakeholder that

enables to make valuable decision (Rotimi, 2012).

3. Types of stakeholders and benefits from financial information.

As far as company is concerned, stakeholders can be government, consumers, distributors

or anyone else that gets impacted by organization's strategies. These stakeholders directly and

indirectly affected by alteration in policies of company and are considered as internal and

external stakeholders. In context of PWC there are number of stakeholder those are interested

with financial statements and other information. Some of these are discussed underneath:

Internal stakeholders: Interested parties that participate constantly within operations

and tasks of the company. In addition internal stakeholders, are affected or work according to the

plans and strategies of organizations. Some of these are listed below:

Employees: These stakeholders are engaged in fulfilling the work and operations. for

doing specific task employee are entitled to receive salaries, compensation packages and

other economic advantages (Schaltegger and Burritt, 2017). Employees take advantage of

financial reports by checking their monetary advantages, economic safety, etc.

Management: They are consider as company most significant internal stakeholders.

Thus, they are involved in phase of preparing strategic plans of company and thus

support in effectively managing valuable operations. Management receive appropriate

and necessary data for decision-making from financial reports to increase overall

performance of PWC.

External stakeholder: All those stakeholder those are not directly related with company

but have interest in the financial results and strength of company are consider as external

stakeholder. There are number of external stakeholder, some of these in context of PWC are

discussed below:

Creditors: These stakeholders gives the businesses with economic support and other

loan facilities. Creditors usually shows their interest to company financial reports and

take advantage related to evaluate the actual stability of respective firm in order to make

credit transaction.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Governance: These type of external stakeholder usually collects taxes like goods tax,

service tax, taxes on salary, production etc. that contribute to nations' financial

development. They demonstrate their stake in financial statements of company to

estimate the actual quantity of tax payable which is being calculated on the basis of

revenue for that specific year (Siew, 2015).

4. Financial reports to meet companies growth and objectives.

In Business world, to meet various financial issues manager usually use financial

reporting methods that help to improve overall financial situation by concerning respective

framework that bring results in more efficient and effective way. These norms and elements that

help manager to communicate significant financial plans and techniques to meet companies

requirement. The financial reports are essential for achieving the development and goals of the

organization, thus they are prepared for some major reasons:

To meet Organisational growth: The annual reports are really essential to satisfy the

growth of the company because it enables in easy analyse of real financial situation that

provide assistance to make further financial choices related with improving performance

and reducing the reasons for any error in future. In PWC manager can take advantage by

developing financial reports, as they make decision to reduces the cost and other

miscellaneous expenses that reduces the profit for last year.

To meet organisational Objective: Financial reports perform a significant part in

achieving the goals of the organization because manager are able to create their plans and

strategies that benefits in attainment of goals depending upon the grounds of financial

reports. With the assistance of multiple kinds of financial statements and accounts, in the

corresponding business manager can create plans and policies that support in achieving

their objectives that is to expand business and provide more accounting services to large

number of clients at international level (Weygandt, Kimmel and Kieso, 2015).

Support in developing organisation: Besides these advantages financial reports is also

important in improving the goodwill of company by properly preparing every set of

financial statements and recoding each business transaction. If a business regularly

publishes the financial reports, it could be distributed across all shareholders, that can

result to increase the global image of company. Ultimately, financial reports are very

4

service tax, taxes on salary, production etc. that contribute to nations' financial

development. They demonstrate their stake in financial statements of company to

estimate the actual quantity of tax payable which is being calculated on the basis of

revenue for that specific year (Siew, 2015).

4. Financial reports to meet companies growth and objectives.

In Business world, to meet various financial issues manager usually use financial

reporting methods that help to improve overall financial situation by concerning respective

framework that bring results in more efficient and effective way. These norms and elements that

help manager to communicate significant financial plans and techniques to meet companies

requirement. The financial reports are essential for achieving the development and goals of the

organization, thus they are prepared for some major reasons:

To meet Organisational growth: The annual reports are really essential to satisfy the

growth of the company because it enables in easy analyse of real financial situation that

provide assistance to make further financial choices related with improving performance

and reducing the reasons for any error in future. In PWC manager can take advantage by

developing financial reports, as they make decision to reduces the cost and other

miscellaneous expenses that reduces the profit for last year.

To meet organisational Objective: Financial reports perform a significant part in

achieving the goals of the organization because manager are able to create their plans and

strategies that benefits in attainment of goals depending upon the grounds of financial

reports. With the assistance of multiple kinds of financial statements and accounts, in the

corresponding business manager can create plans and policies that support in achieving

their objectives that is to expand business and provide more accounting services to large

number of clients at international level (Weygandt, Kimmel and Kieso, 2015).

Support in developing organisation: Besides these advantages financial reports is also

important in improving the goodwill of company by properly preparing every set of

financial statements and recoding each business transaction. If a business regularly

publishes the financial reports, it could be distributed across all shareholders, that can

result to increase the global image of company. Ultimately, financial reports are very

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

essential in the context of PWC as it enables the growth of their business and making

available these report benefits to attract more number of investors.

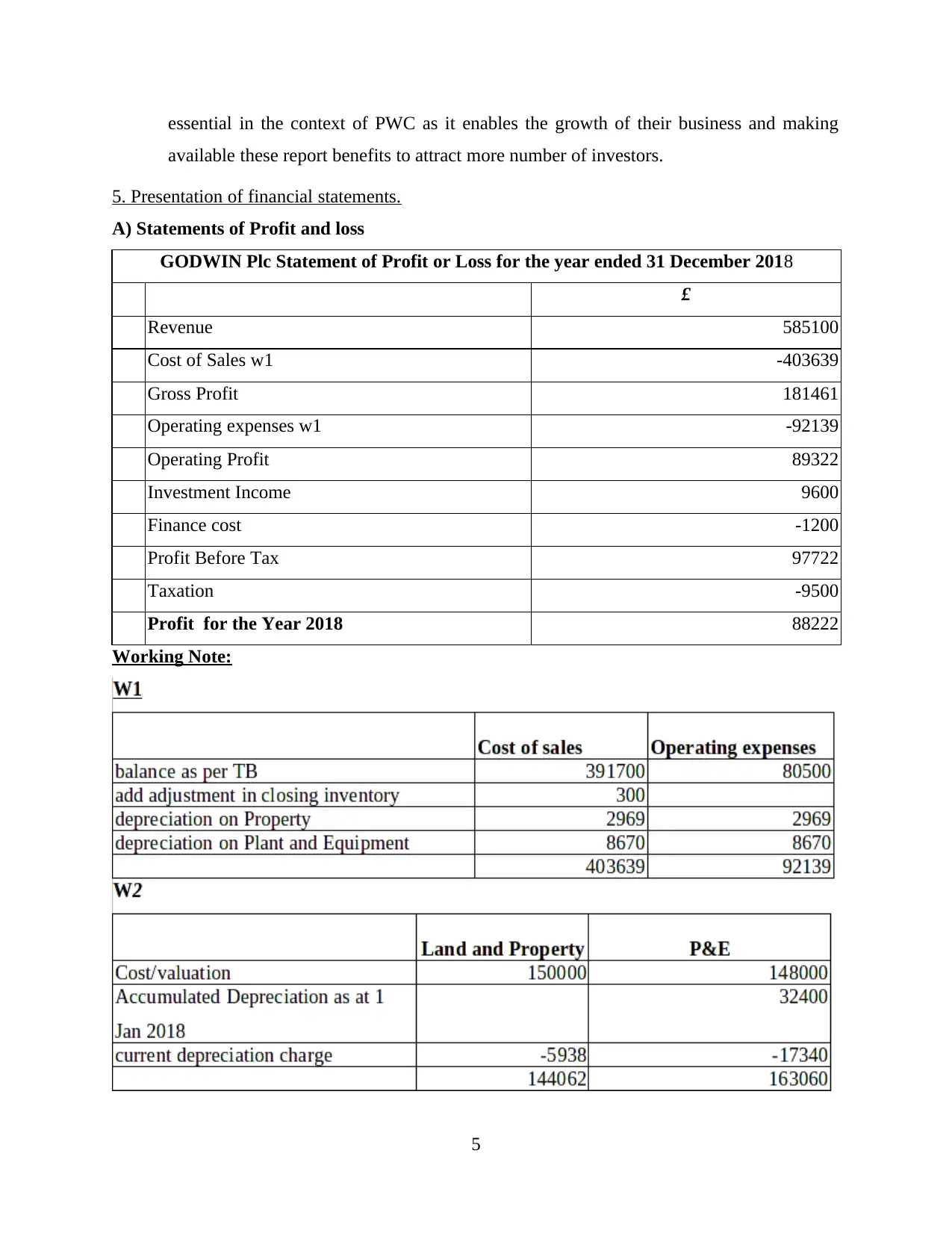

5. Presentation of financial statements.

A) Statements of Profit and loss

GODWIN Plc Statement of Profit or Loss for the year ended 31 December 2018

£

Revenue 585100

Cost of Sales w1 -403639

Gross Profit 181461

Operating expenses w1 -92139

Operating Profit 89322

Investment Income 9600

Finance cost -1200

Profit Before Tax 97722

Taxation -9500

Profit for the Year 2018 88222

Working Note:

5

available these report benefits to attract more number of investors.

5. Presentation of financial statements.

A) Statements of Profit and loss

GODWIN Plc Statement of Profit or Loss for the year ended 31 December 2018

£

Revenue 585100

Cost of Sales w1 -403639

Gross Profit 181461

Operating expenses w1 -92139

Operating Profit 89322

Investment Income 9600

Finance cost -1200

Profit Before Tax 97722

Taxation -9500

Profit for the Year 2018 88222

Working Note:

5

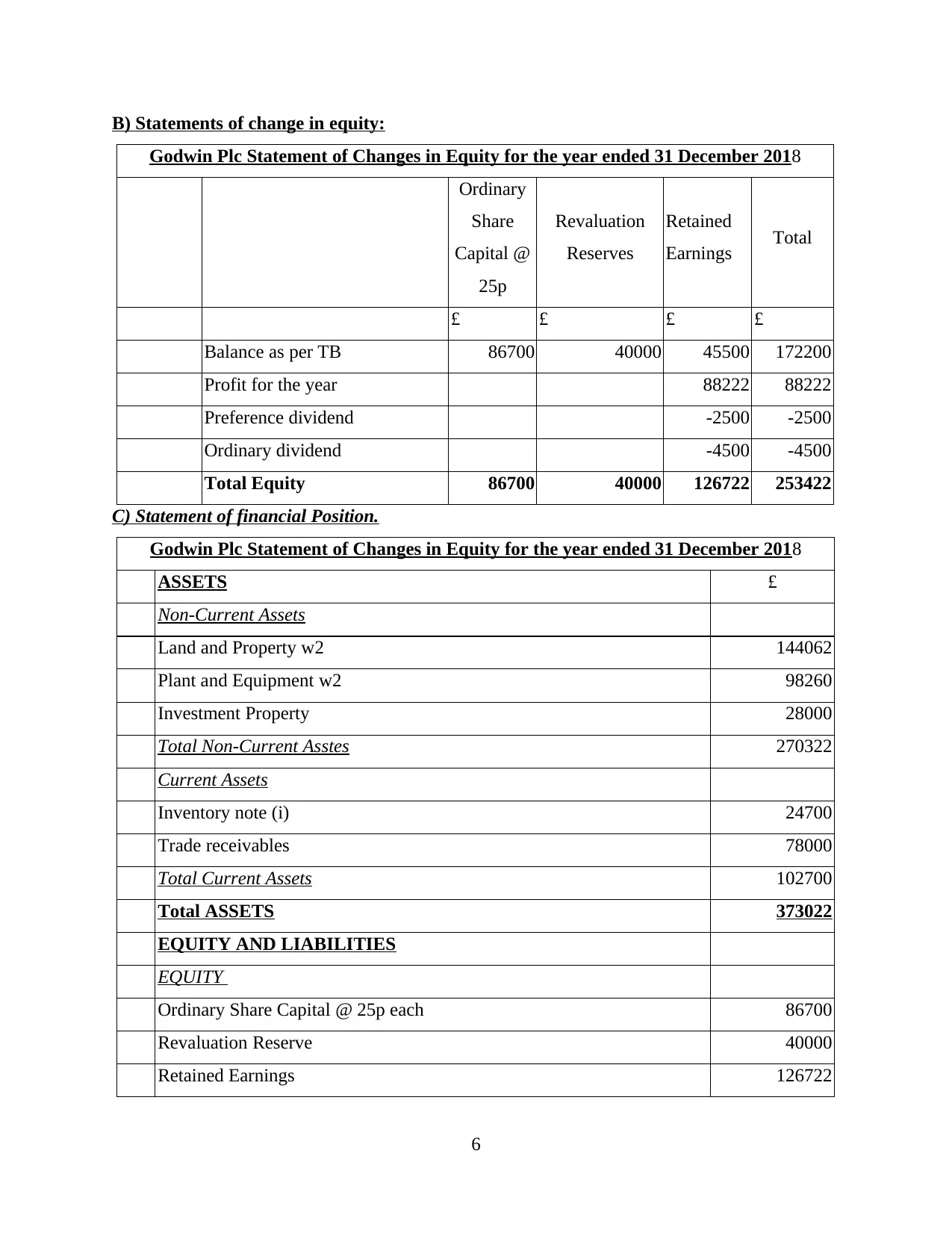

B) Statements of change in equity:

Godwin Plc Statement of Changes in Equity for the year ended 31 December 2018

Ordinary

Share

Capital @

25p

Revaluation

Reserves

Retained

Earnings Total

£ £ £ £

Balance as per TB 86700 40000 45500 172200

Profit for the year 88222 88222

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

Total Equity 86700 40000 126722 253422

C) Statement of financial Position.

Godwin Plc Statement of Changes in Equity for the year ended 31 December 2018

ASSETS £

Non-Current Assets

Land and Property w2 144062

Plant and Equipment w2 98260

Investment Property 28000

Total Non-Current Asstes 270322

Current Assets

Inventory note (i) 24700

Trade receivables 78000

Total Current Assets 102700

Total ASSETS 373022

EQUITY AND LIABILITIES

EQUITY

Ordinary Share Capital @ 25p each 86700

Revaluation Reserve 40000

Retained Earnings 126722

6

Godwin Plc Statement of Changes in Equity for the year ended 31 December 2018

Ordinary

Share

Capital @

25p

Revaluation

Reserves

Retained

Earnings Total

£ £ £ £

Balance as per TB 86700 40000 45500 172200

Profit for the year 88222 88222

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

Total Equity 86700 40000 126722 253422

C) Statement of financial Position.

Godwin Plc Statement of Changes in Equity for the year ended 31 December 2018

ASSETS £

Non-Current Assets

Land and Property w2 144062

Plant and Equipment w2 98260

Investment Property 28000

Total Non-Current Asstes 270322

Current Assets

Inventory note (i) 24700

Trade receivables 78000

Total Current Assets 102700

Total ASSETS 373022

EQUITY AND LIABILITIES

EQUITY

Ordinary Share Capital @ 25p each 86700

Revaluation Reserve 40000

Retained Earnings 126722

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

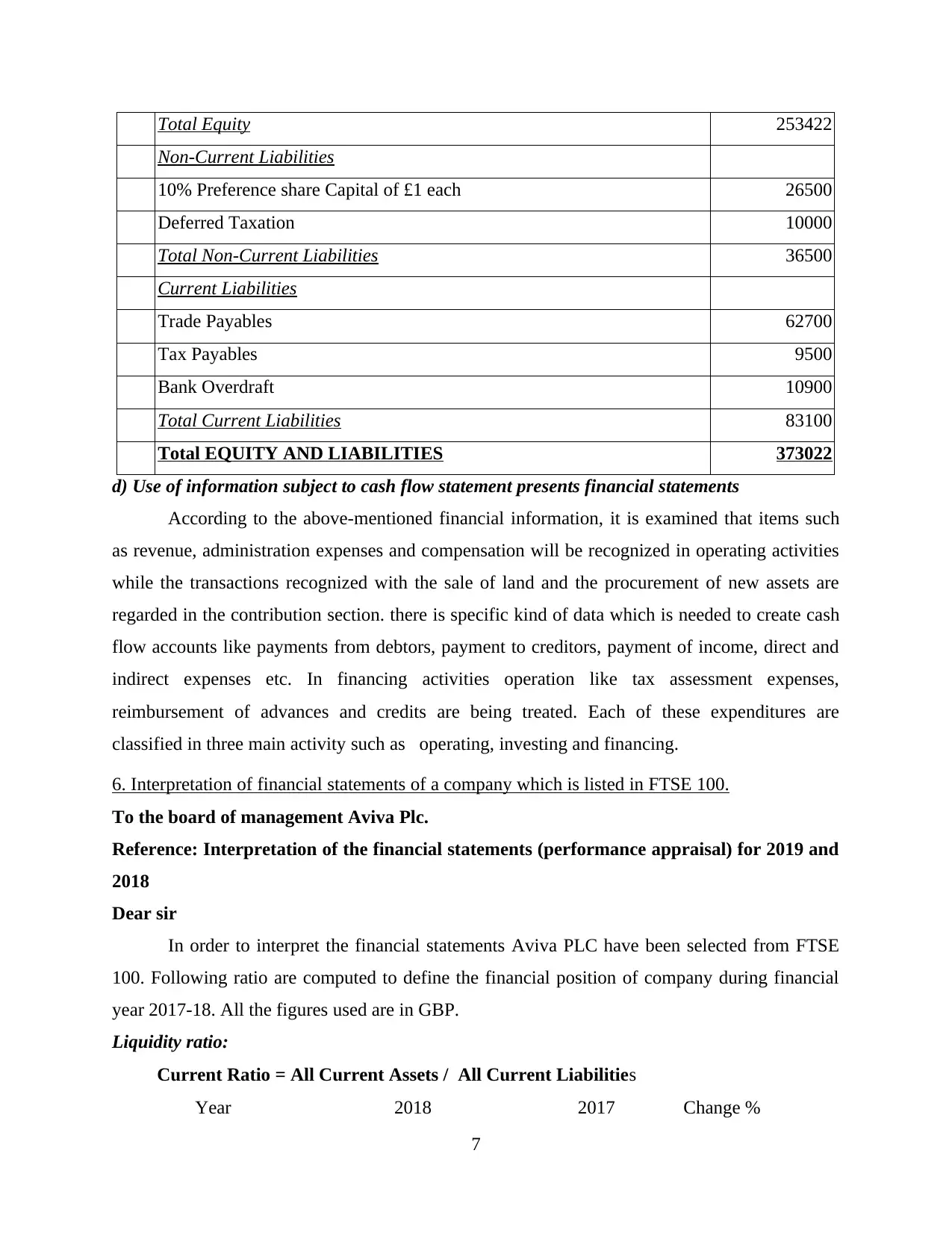

Total Equity 253422

Non-Current Liabilities

10% Preference share Capital of £1 each 26500

Deferred Taxation 10000

Total Non-Current Liabilities 36500

Current Liabilities

Trade Payables 62700

Tax Payables 9500

Bank Overdraft 10900

Total Current Liabilities 83100

Total EQUITY AND LIABILITIES 373022

d) Use of information subject to cash flow statement presents financial statements

According to the above-mentioned financial information, it is examined that items such

as revenue, administration expenses and compensation will be recognized in operating activities

while the transactions recognized with the sale of land and the procurement of new assets are

regarded in the contribution section. there is specific kind of data which is needed to create cash

flow accounts like payments from debtors, payment to creditors, payment of income, direct and

indirect expenses etc. In financing activities operation like tax assessment expenses,

reimbursement of advances and credits are being treated. Each of these expenditures are

classified in three main activity such as operating, investing and financing.

6. Interpretation of financial statements of a company which is listed in FTSE 100.

To the board of management Aviva Plc.

Reference: Interpretation of the financial statements (performance appraisal) for 2019 and

2018

Dear sir

In order to interpret the financial statements Aviva PLC have been selected from FTSE

100. Following ratio are computed to define the financial position of company during financial

year 2017-18. All the figures used are in GBP.

Liquidity ratio:

Current Ratio = All Current Assets / All Current Liabilities

Year 2018 2017 Change %

7

Non-Current Liabilities

10% Preference share Capital of £1 each 26500

Deferred Taxation 10000

Total Non-Current Liabilities 36500

Current Liabilities

Trade Payables 62700

Tax Payables 9500

Bank Overdraft 10900

Total Current Liabilities 83100

Total EQUITY AND LIABILITIES 373022

d) Use of information subject to cash flow statement presents financial statements

According to the above-mentioned financial information, it is examined that items such

as revenue, administration expenses and compensation will be recognized in operating activities

while the transactions recognized with the sale of land and the procurement of new assets are

regarded in the contribution section. there is specific kind of data which is needed to create cash

flow accounts like payments from debtors, payment to creditors, payment of income, direct and

indirect expenses etc. In financing activities operation like tax assessment expenses,

reimbursement of advances and credits are being treated. Each of these expenditures are

classified in three main activity such as operating, investing and financing.

6. Interpretation of financial statements of a company which is listed in FTSE 100.

To the board of management Aviva Plc.

Reference: Interpretation of the financial statements (performance appraisal) for 2019 and

2018

Dear sir

In order to interpret the financial statements Aviva PLC have been selected from FTSE

100. Following ratio are computed to define the financial position of company during financial

year 2017-18. All the figures used are in GBP.

Liquidity ratio:

Current Ratio = All Current Assets / All Current Liabilities

Year 2018 2017 Change %

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

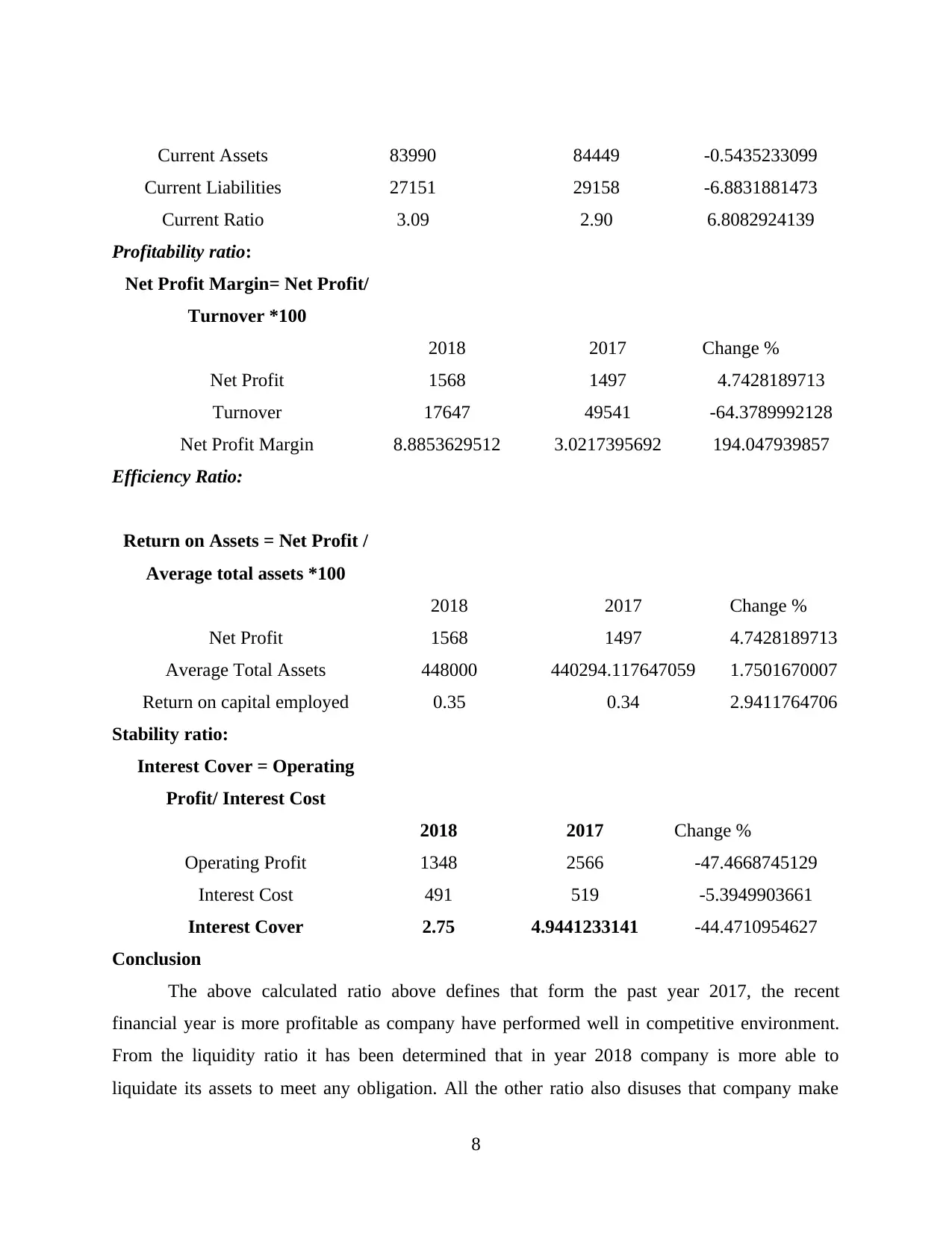

Current Assets 83990 84449 -0.5435233099

Current Liabilities 27151 29158 -6.8831881473

Current Ratio 3.09 2.90 6.8082924139

Profitability ratio:

Net Profit Margin= Net Profit/

Turnover *100

2018 2017 Change %

Net Profit 1568 1497 4.7428189713

Turnover 17647 49541 -64.3789992128

Net Profit Margin 8.8853629512 3.0217395692 194.047939857

Efficiency Ratio:

Return on Assets = Net Profit /

Average total assets *100

2018 2017 Change %

Net Profit 1568 1497 4.7428189713

Average Total Assets 448000 440294.117647059 1.7501670007

Return on capital employed 0.35 0.34 2.9411764706

Stability ratio:

Interest Cover = Operating

Profit/ Interest Cost

2018 2017 Change %

Operating Profit 1348 2566 -47.4668745129

Interest Cost 491 519 -5.3949903661

Interest Cover 2.75 4.9441233141 -44.4710954627

Conclusion

The above calculated ratio above defines that form the past year 2017, the recent

financial year is more profitable as company have performed well in competitive environment.

From the liquidity ratio it has been determined that in year 2018 company is more able to

liquidate its assets to meet any obligation. All the other ratio also disuses that company make

8

Current Liabilities 27151 29158 -6.8831881473

Current Ratio 3.09 2.90 6.8082924139

Profitability ratio:

Net Profit Margin= Net Profit/

Turnover *100

2018 2017 Change %

Net Profit 1568 1497 4.7428189713

Turnover 17647 49541 -64.3789992128

Net Profit Margin 8.8853629512 3.0217395692 194.047939857

Efficiency Ratio:

Return on Assets = Net Profit /

Average total assets *100

2018 2017 Change %

Net Profit 1568 1497 4.7428189713

Average Total Assets 448000 440294.117647059 1.7501670007

Return on capital employed 0.35 0.34 2.9411764706

Stability ratio:

Interest Cover = Operating

Profit/ Interest Cost

2018 2017 Change %

Operating Profit 1348 2566 -47.4668745129

Interest Cost 491 519 -5.3949903661

Interest Cover 2.75 4.9441233141 -44.4710954627

Conclusion

The above calculated ratio above defines that form the past year 2017, the recent

financial year is more profitable as company have performed well in competitive environment.

From the liquidity ratio it has been determined that in year 2018 company is more able to

liquidate its assets to meet any obligation. All the other ratio also disuses that company make

8

effective policies that enables to reach the desired targets and increase the profitability in future

year.

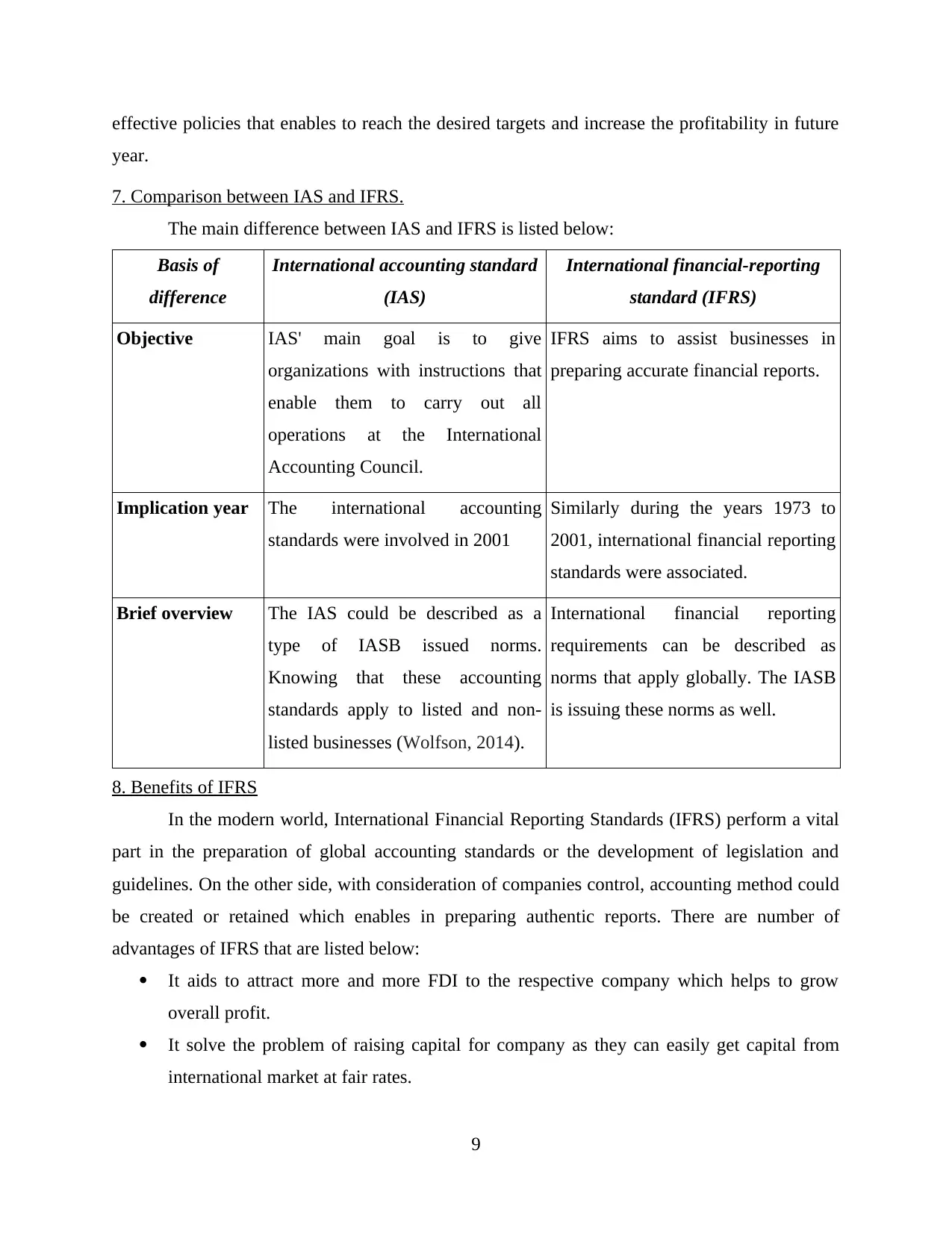

7. Comparison between IAS and IFRS.

The main difference between IAS and IFRS is listed below:

Basis of

difference

International accounting standard

(IAS)

International financial-reporting

standard (IFRS)

Objective IAS' main goal is to give

organizations with instructions that

enable them to carry out all

operations at the International

Accounting Council.

IFRS aims to assist businesses in

preparing accurate financial reports.

Implication year The international accounting

standards were involved in 2001

Similarly during the years 1973 to

2001, international financial reporting

standards were associated.

Brief overview The IAS could be described as a

type of IASB issued norms.

Knowing that these accounting

standards apply to listed and non-

listed businesses (Wolfson, 2014).

International financial reporting

requirements can be described as

norms that apply globally. The IASB

is issuing these norms as well.

8. Benefits of IFRS

In the modern world, International Financial Reporting Standards (IFRS) perform a vital

part in the preparation of global accounting standards or the development of legislation and

guidelines. On the other side, with consideration of companies control, accounting method could

be created or retained which enables in preparing authentic reports. There are number of

advantages of IFRS that are listed below:

It aids to attract more and more FDI to the respective company which helps to grow

overall profit.

It solve the problem of raising capital for company as they can easily get capital from

international market at fair rates.

9

year.

7. Comparison between IAS and IFRS.

The main difference between IAS and IFRS is listed below:

Basis of

difference

International accounting standard

(IAS)

International financial-reporting

standard (IFRS)

Objective IAS' main goal is to give

organizations with instructions that

enable them to carry out all

operations at the International

Accounting Council.

IFRS aims to assist businesses in

preparing accurate financial reports.

Implication year The international accounting

standards were involved in 2001

Similarly during the years 1973 to

2001, international financial reporting

standards were associated.

Brief overview The IAS could be described as a

type of IASB issued norms.

Knowing that these accounting

standards apply to listed and non-

listed businesses (Wolfson, 2014).

International financial reporting

requirements can be described as

norms that apply globally. The IASB

is issuing these norms as well.

8. Benefits of IFRS

In the modern world, International Financial Reporting Standards (IFRS) perform a vital

part in the preparation of global accounting standards or the development of legislation and

guidelines. On the other side, with consideration of companies control, accounting method could

be created or retained which enables in preparing authentic reports. There are number of

advantages of IFRS that are listed below:

It aids to attract more and more FDI to the respective company which helps to grow

overall profit.

It solve the problem of raising capital for company as they can easily get capital from

international market at fair rates.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.