Financial Reporting Assignment: Dynamics Co. Ltd Case Study Analysis

VerifiedAdded on 2021/04/19

|6

|956

|27

Report

AI Summary

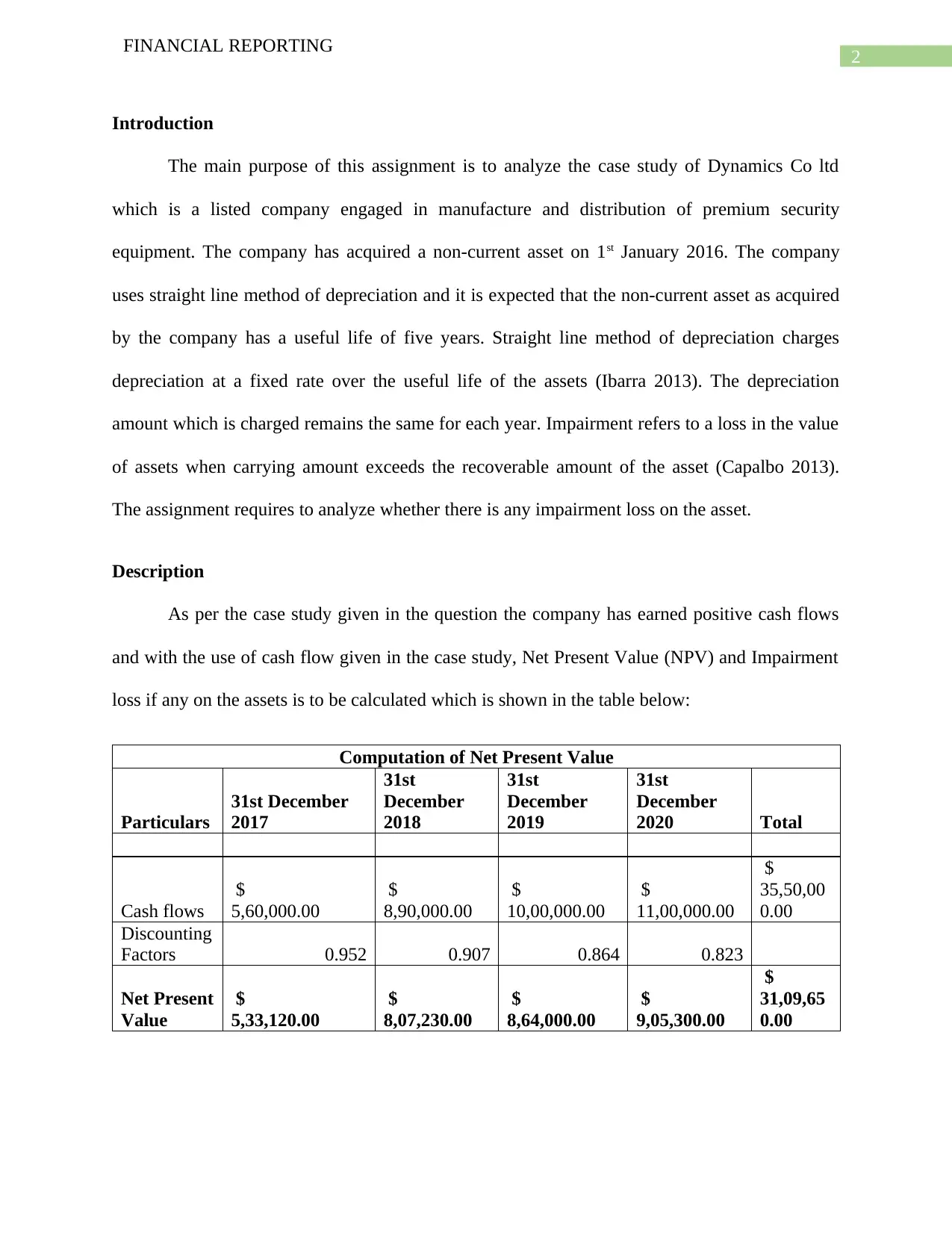

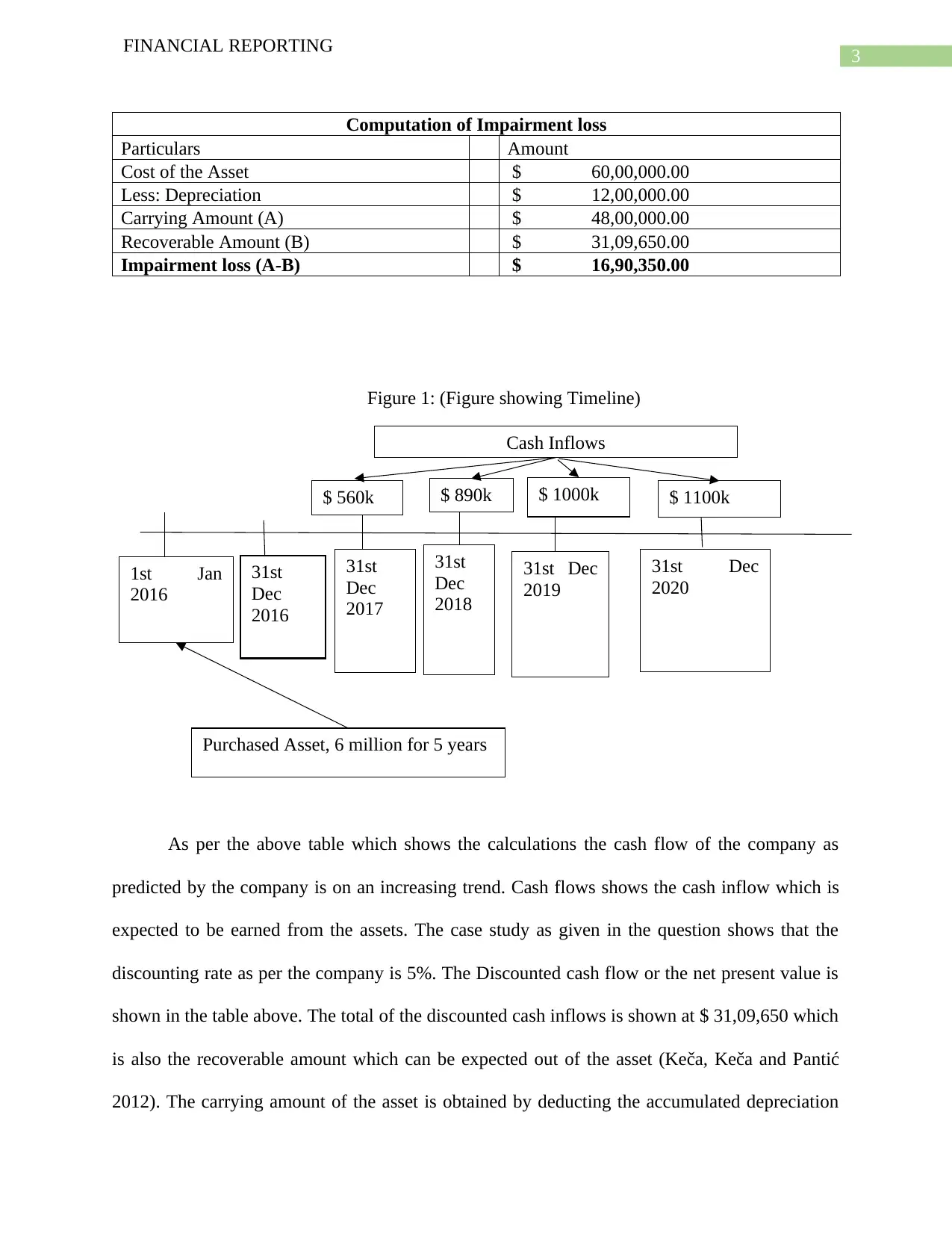

This report analyzes the financial reporting of Dynamics Co. Ltd, a company engaged in the manufacture and distribution of premium security equipment. The assignment focuses on a non-current asset acquired on January 1, 2016, with a five-year useful life, depreciated using the straight-line method. The analysis involves calculating the Net Present Value (NPV) of the asset's cash flows and determining any impairment loss. The report details the computation of NPV, which is used to determine the recoverable amount, and compares it with the carrying amount to identify an impairment loss of $16,90,350. The report also mentions that the government will compensate up to 20% of the impairment loss, reducing the overall impact. The conclusion emphasizes the need to recognize the impairment loss in the financial statements according to IFRS. The report highlights the importance of understanding impairment loss and the application of depreciation methods in financial reporting.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.