Financial Reporting: Regression Analysis of Working Capital on ROA

VerifiedAdded on 2021/02/20

|20

|5138

|30

Report

AI Summary

This report delves into the application of financial econometrics, specifically focusing on the empirical relationship between Return on Assets (ROA) as the dependent variable and various working capital components, including accounts receivable, inventory, accounts payable, and the cash conversion cycle. It utilizes regression analysis to examine financial data from multiple companies, considering relevant assumptions and formulating hypotheses. The study reviews existing literature on working capital management and its impact on profitability, referencing studies that employ statistical techniques like correlation and regression to validate findings. The report specifies a regression model to assess the influence of independent variables such as accounts receivable, accounts payable, inventory, cash conversion cycle, and total assets on ROA. The hypotheses are formulated to test the significance of these variables' impact. The report also discusses the importance of managing working capital efficiently to enhance financial performance, emphasizing the need to reduce receivable and inventory days to increase profitability. The analysis considers the relationship between liquidity and profitability, with the cash conversion cycle being a key measure of liquidity. The ultimate goal is to provide insights into how effective working capital management can boost shareholder value.

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Assessment.......................................................................................................................................1

1. regression analysis .................................................................................................................1

2. Reviewing the relationship among the variables....................................................................2

(3) Specification of model and hypothesis..................................................................................6

(4) Data, variables and sources...................................................................................................7

(5) Documenting in standard format...........................................................................................8

(6) Analysis of results.................................................................................................................9

Conclusion and recommendation .............................................................................................11

CONCLUSION .............................................................................................................................12

REFERENCES .............................................................................................................................13

APPENDIX....................................................................................................................................14

INTRODUCTION...........................................................................................................................1

Assessment.......................................................................................................................................1

1. regression analysis .................................................................................................................1

2. Reviewing the relationship among the variables....................................................................2

(3) Specification of model and hypothesis..................................................................................6

(4) Data, variables and sources...................................................................................................7

(5) Documenting in standard format...........................................................................................8

(6) Analysis of results.................................................................................................................9

Conclusion and recommendation .............................................................................................11

CONCLUSION .............................................................................................................................12

REFERENCES .............................................................................................................................13

APPENDIX....................................................................................................................................14

INTRODUCTION

Financial econometrics refers to the application of the mathematical tools to the

economics for studying the problems, analysing the data, developing and testing the theories and

the models. It is counted as the fastest and wide branch of the economics presently in respect of

the industry as well as academia. With increasing sophistication of the financial models needs

equating sophisticated techniques for empirical execution. The present study focuses on the

empirical study regarding the relationship in between return on assets as the dependent variable

and working capital that includes accounts receivable, inventory, accounts payable, cash

conversion cycle. Furthermore, regression analysis is been made of different companies from

their financial data by applying the appropriate regression model. Moreover, it also includes

several assumptions that are been taken while conducting the study and facilitating adequate

recommendations with proper description of variables defined by making the relevant

hypotheses and inferring conclusions.

Assessment

1. regression analysis

1

Financial econometrics refers to the application of the mathematical tools to the

economics for studying the problems, analysing the data, developing and testing the theories and

the models. It is counted as the fastest and wide branch of the economics presently in respect of

the industry as well as academia. With increasing sophistication of the financial models needs

equating sophisticated techniques for empirical execution. The present study focuses on the

empirical study regarding the relationship in between return on assets as the dependent variable

and working capital that includes accounts receivable, inventory, accounts payable, cash

conversion cycle. Furthermore, regression analysis is been made of different companies from

their financial data by applying the appropriate regression model. Moreover, it also includes

several assumptions that are been taken while conducting the study and facilitating adequate

recommendations with proper description of variables defined by making the relevant

hypotheses and inferring conclusions.

Assessment

1. regression analysis

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Reviewing the relationship among the variables

As reviewed by the Afrifa and Tingbani, (2018), it has been analysed the study has

emphasized on the relationship in between the working capital of an enterprise with that of its

profitability that is been measured by evaluating the return on the total assets. For conducting the

study, correlation and regression analysis has been used as a statistical technique in order to

validate findings. The assessment has been made by taking the sample of the 20 firms for the

period of 10 years in order to make the study more useful.

Yenice, (2015) viewed the relation between the cash conversion cycle and profitability

or return on the assets of a corporate. From the study it has been considered that shorter the cycle

of the cash conversion, higher profitability is been gained by an entity. This has been revealed by

applying the chi-square test fro the hypotheses fro examining the financial data of 20 different

firms over the period of 10 years.

However, In accordance to Nobanee, (2017), different statistical tools could be used for

making the analysis more reliable such as correlation, multiple regression, non-parametric

process etc. These techniques helps in evaluating cross-sectional relation between the measures

of profitability and CCC. The resultant finding reflects that various along with their aggressive

procedures of liquidity management stated significant statistical inverse relationship between the

profitability and the CCC.

Jain, Bhargava and Bhargava, (2017), identified that by making use of the cash

conversion cycle variable as the comprehensive measure for managing working capital. As the

measure of the trade credit, inventory policies different variables are taken into account like

accounts receivable, payables and inventories as an independent variable. Regression analysis

with application of the model called fixed effect is been used for the purpose of capturing any

intercept of the companies that are found consistent over the time. The findings regarding the

accounts receivable variable reflected existence of the negative relationship. Increase in no. of

days trade receivables results to the decrease in the gross operating income. It has also been

determined that the gross profit of the firm increases with the firm size, fixed assets and the sales

growth. On the other hand, decrease in the gross profit is been observed with the growing

proportion of the financial debt.

2

As reviewed by the Afrifa and Tingbani, (2018), it has been analysed the study has

emphasized on the relationship in between the working capital of an enterprise with that of its

profitability that is been measured by evaluating the return on the total assets. For conducting the

study, correlation and regression analysis has been used as a statistical technique in order to

validate findings. The assessment has been made by taking the sample of the 20 firms for the

period of 10 years in order to make the study more useful.

Yenice, (2015) viewed the relation between the cash conversion cycle and profitability

or return on the assets of a corporate. From the study it has been considered that shorter the cycle

of the cash conversion, higher profitability is been gained by an entity. This has been revealed by

applying the chi-square test fro the hypotheses fro examining the financial data of 20 different

firms over the period of 10 years.

However, In accordance to Nobanee, (2017), different statistical tools could be used for

making the analysis more reliable such as correlation, multiple regression, non-parametric

process etc. These techniques helps in evaluating cross-sectional relation between the measures

of profitability and CCC. The resultant finding reflects that various along with their aggressive

procedures of liquidity management stated significant statistical inverse relationship between the

profitability and the CCC.

Jain, Bhargava and Bhargava, (2017), identified that by making use of the cash

conversion cycle variable as the comprehensive measure for managing working capital. As the

measure of the trade credit, inventory policies different variables are taken into account like

accounts receivable, payables and inventories as an independent variable. Regression analysis

with application of the model called fixed effect is been used for the purpose of capturing any

intercept of the companies that are found consistent over the time. The findings regarding the

accounts receivable variable reflected existence of the negative relationship. Increase in no. of

days trade receivables results to the decrease in the gross operating income. It has also been

determined that the gross profit of the firm increases with the firm size, fixed assets and the sales

growth. On the other hand, decrease in the gross profit is been observed with the growing

proportion of the financial debt.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the viewpoint of Rahaman, Rabbi and Alam, (2018), it has been highlighted that

inventory days significantly having a negative relationship with that of the operating income.

This means that the managers must reduce receivable days along with its inventories for

increasing the corporate profitability. However, on the other side, enterprise with less amount of

profits accounted as it has waiting for the payment of the bill for the long time. The study states

that the regression model reflects a higher proportion of the changes in the amount of

profitability among the firms. It has been suggested that for creating the shareholders value,

managers of an enterprise must reduce receivable days and the inventory days to lower level.

As per the Aktas, Croci and Petmezas, (2015), researcher could make use of the current

ratio, cash gap for empirically examining relationship in between the profitability and the

liquidity. In this report, cash gap is been computed by subtracting accounts payable days from

inventory and receivable days. With respect of the statistical tools, correlation tool has used for

determining association between the profitability and the liquidity indicators in consideration

with the other appropriate related variables. It has also been found that there is a positive and the

significant association present in between measures of the size and the profits. Highly positive

and the strong relation exist between the total assets and sales which is been marked for

becoming substitute of the measure size. The study also examined the relation in between level

of liquidity, cash gap and the profitability existed as the efficiency function in managing the cash

cycle. Thus, the report draws conclusions as that the cash gap or the CCC represented as the

essential measure of the liquidity in comparison to the impact of the current ratio on the

profitability. However, with more and more segment of labour intensive such as cash gap seeks

to lose importance as the liquidity measure.

Naeem, Awais and Shahzadi, (2017), also reviewed that key elements of the working

capital management in the study are been examined in respect of the selected firms for

generating an insights towards their financial performance. The major dimensions that are been

reflected in the hypothesis is to determine significant differences among the industries in respect

to measures of efficiency in working capital and application of ANOVA in finding out the

suitable results. The other hypotheses is been developed for assessing that whether the measures

of working capital for an enterprise within the industry had changed over the time. It has also

been mentioned that the evaluation had been made for a shorter period of time within an

improving market which may suffer survivorship bias.

3

inventory days significantly having a negative relationship with that of the operating income.

This means that the managers must reduce receivable days along with its inventories for

increasing the corporate profitability. However, on the other side, enterprise with less amount of

profits accounted as it has waiting for the payment of the bill for the long time. The study states

that the regression model reflects a higher proportion of the changes in the amount of

profitability among the firms. It has been suggested that for creating the shareholders value,

managers of an enterprise must reduce receivable days and the inventory days to lower level.

As per the Aktas, Croci and Petmezas, (2015), researcher could make use of the current

ratio, cash gap for empirically examining relationship in between the profitability and the

liquidity. In this report, cash gap is been computed by subtracting accounts payable days from

inventory and receivable days. With respect of the statistical tools, correlation tool has used for

determining association between the profitability and the liquidity indicators in consideration

with the other appropriate related variables. It has also been found that there is a positive and the

significant association present in between measures of the size and the profits. Highly positive

and the strong relation exist between the total assets and sales which is been marked for

becoming substitute of the measure size. The study also examined the relation in between level

of liquidity, cash gap and the profitability existed as the efficiency function in managing the cash

cycle. Thus, the report draws conclusions as that the cash gap or the CCC represented as the

essential measure of the liquidity in comparison to the impact of the current ratio on the

profitability. However, with more and more segment of labour intensive such as cash gap seeks

to lose importance as the liquidity measure.

Naeem, Awais and Shahzadi, (2017), also reviewed that key elements of the working

capital management in the study are been examined in respect of the selected firms for

generating an insights towards their financial performance. The major dimensions that are been

reflected in the hypothesis is to determine significant differences among the industries in respect

to measures of efficiency in working capital and application of ANOVA in finding out the

suitable results. The other hypotheses is been developed for assessing that whether the measures

of working capital for an enterprise within the industry had changed over the time. It has also

been mentioned that the evaluation had been made for a shorter period of time within an

improving market which may suffer survivorship bias.

3

In view of Singh, Kumar and Colombage, (2017), it has been represented that four

major regression equations are used in the study for estimating relationship between both

dependent and the independent variable where the dependent variable is Return on assets and

the independent variable is stated as AR, AP, INV and CCC. Control variables are also used that

involves total assets, sales growth, GDP and debt in regression equations for generating the

results. The most crucial observation on the credit policy was that the performance of an

enterprise get improve when credit policy becomes more and more restrictive with very less

given to the customers for making the payments. On contrary to it, it is been observed that profits

could be increased with respect to the payment facility which is customer oriented and induces

the sales growth. It has also been found that reduction in the inventory days improves the

profitability and increase in account payable days reduces profitability. Gao and Wang, (2017),

highlighted that profitability of the companies improves with the shorter CCC which is been

measured as the combined influence of the accounts receivable days, payable days and inventory

days.

It has been suggested by the Hailu and Venkateswarlu, (2016) that use of the aggressive

investment policy resulted a minimum investment level in the current assets in comparison to the

investment in the fixed assets. Similarly, conservative investment policy leads to large capital in

the liquid assets and results in opportunity cost regarding the less profitability. In the report,

scholar measured degree net profit with respect to total assets. This ratio indicates the return

generated by the firms from total assets and is stated as that lower ratio means that the policy is

relatively aggressive. In respect of profitability measure, return on asset is computed by dividing

the net earnings with the book value of the total assets. The finding generated showed that firms

which had adopted the aggressive approach for managing the current liabilities are been

perceived as most valuable by the investors. In case if the working capital policy is aggressive

then it does not result in generating larger profits.

Kasozi, (2017) states that profitability and the firm's value were been used as a biggest

measure of the firm's performance. As the indicator of the profitability, gross operating profit has

been used that is measured by dividing the cost of sales with that of the difference in between the

financial and total assets. The outcome from the assessment reflects a shortening of receivable

days and the CCC had resulted a positive influence on the profitability.

4

major regression equations are used in the study for estimating relationship between both

dependent and the independent variable where the dependent variable is Return on assets and

the independent variable is stated as AR, AP, INV and CCC. Control variables are also used that

involves total assets, sales growth, GDP and debt in regression equations for generating the

results. The most crucial observation on the credit policy was that the performance of an

enterprise get improve when credit policy becomes more and more restrictive with very less

given to the customers for making the payments. On contrary to it, it is been observed that profits

could be increased with respect to the payment facility which is customer oriented and induces

the sales growth. It has also been found that reduction in the inventory days improves the

profitability and increase in account payable days reduces profitability. Gao and Wang, (2017),

highlighted that profitability of the companies improves with the shorter CCC which is been

measured as the combined influence of the accounts receivable days, payable days and inventory

days.

It has been suggested by the Hailu and Venkateswarlu, (2016) that use of the aggressive

investment policy resulted a minimum investment level in the current assets in comparison to the

investment in the fixed assets. Similarly, conservative investment policy leads to large capital in

the liquid assets and results in opportunity cost regarding the less profitability. In the report,

scholar measured degree net profit with respect to total assets. This ratio indicates the return

generated by the firms from total assets and is stated as that lower ratio means that the policy is

relatively aggressive. In respect of profitability measure, return on asset is computed by dividing

the net earnings with the book value of the total assets. The finding generated showed that firms

which had adopted the aggressive approach for managing the current liabilities are been

perceived as most valuable by the investors. In case if the working capital policy is aggressive

then it does not result in generating larger profits.

Kasozi, (2017) states that profitability and the firm's value were been used as a biggest

measure of the firm's performance. As the indicator of the profitability, gross operating profit has

been used that is measured by dividing the cost of sales with that of the difference in between the

financial and total assets. The outcome from the assessment reflects a shortening of receivable

days and the CCC had resulted a positive influence on the profitability.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Sharaf and Haddad, (2015) find out that the relations between the management of

working capital and the profitability of the firm. From this it has been carried out that

management of the working capital leads to improved performance and increased profitability.

Under this, an investigator examines CCC as well as the net trade cycle. Financial data of

different companies is gathered from the year 2009 to 2018 that for the period of 10 years.

Regression equations are been used for testing the relationship between the WCM and the

profitability. The findings shows that the CCC and the size of the firm positively relates to its

profitability. It has also been found that larger firm with the greater level of the inventory and the

better terms of credit for the clients leads to higher profitability and also the value of an

enterprise increases. There exist an inverse relation in between the risk profile of the firm and the

profitability.

Thus, it has been concluded by the Mun and Jang, (2015) that WCM is considered as an

essential component for the firm in developing its overall strategy fro boosting the value of their

shareholders. From the study, it has been interpreted that negative relationship is present in

between measure of cycle and the debt, however, positive relationship is been found in between

ROA and the size, sales growth and GDP rate of the working capital. Bulin, Basit and Hamza,

(2016), suggested that managers could maximize wealth and improves profitability by dropping

the receivable days, payable days, inventory days and in making substantial efforts for

maintaining optimal level of CCC. WCM has a direct impact on the risk and the profitability

measure of a corporate. It is been counted as the routine management function of an entity. The

main components of working capital are current assets that includes cash, accounts receivable

and the short term liabilities that involves accounts payables, short term loans etc.

WCM is counted as the most important module of the finance and is having an

undeviating effect on profitability and liquidity of the company. Both these factors act as crucial

module of the finance and has undeviating influence on profitability and liquidity of an

enterprise. It has been also been reflected that there is a significant negative relation in between

CCC and profitability while the companies that are having the shorter CCC states the

insignificant negative relation with the profitability. Significant positive relation is been found

between firm size that are having longer and the shorter CCC.

5

working capital and the profitability of the firm. From this it has been carried out that

management of the working capital leads to improved performance and increased profitability.

Under this, an investigator examines CCC as well as the net trade cycle. Financial data of

different companies is gathered from the year 2009 to 2018 that for the period of 10 years.

Regression equations are been used for testing the relationship between the WCM and the

profitability. The findings shows that the CCC and the size of the firm positively relates to its

profitability. It has also been found that larger firm with the greater level of the inventory and the

better terms of credit for the clients leads to higher profitability and also the value of an

enterprise increases. There exist an inverse relation in between the risk profile of the firm and the

profitability.

Thus, it has been concluded by the Mun and Jang, (2015) that WCM is considered as an

essential component for the firm in developing its overall strategy fro boosting the value of their

shareholders. From the study, it has been interpreted that negative relationship is present in

between measure of cycle and the debt, however, positive relationship is been found in between

ROA and the size, sales growth and GDP rate of the working capital. Bulin, Basit and Hamza,

(2016), suggested that managers could maximize wealth and improves profitability by dropping

the receivable days, payable days, inventory days and in making substantial efforts for

maintaining optimal level of CCC. WCM has a direct impact on the risk and the profitability

measure of a corporate. It is been counted as the routine management function of an entity. The

main components of working capital are current assets that includes cash, accounts receivable

and the short term liabilities that involves accounts payables, short term loans etc.

WCM is counted as the most important module of the finance and is having an

undeviating effect on profitability and liquidity of the company. Both these factors act as crucial

module of the finance and has undeviating influence on profitability and liquidity of an

enterprise. It has been also been reflected that there is a significant negative relation in between

CCC and profitability while the companies that are having the shorter CCC states the

insignificant negative relation with the profitability. Significant positive relation is been found

between firm size that are having longer and the shorter CCC.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(3) Specification of model and hypothesis

Regression is the one of the model that is used to investigate relationship between dependent

variable and independent variable. In the current research ROA or return on asset is the

dependent variable and its relationship to independent variable account receivable, account

payable, inventory, cash conversion cycle, total asset is used. Regression model is given below.

ROA = Account receivableX1+Account payableX2+InventoryX3+Cash conversion

cycleX4+Total assetsX5

H0: There is not significant impact of account receivable, account payable, inventory, cash

conversion cycle and total assets on ROA.

H1: There is significant impact of account receivable, account payable, inventory, cash

conversion cycle and total assets on ROA.

In the current model receivable is taken in to account as if receivable amount is high

across years then it means that cash amount is blocked in account receivable which means that

less cash is available for making investment in business. Ultimately profit get declined and lead

to low ROA. Such kind of relationship is taken in to account and because of this account

receivable is considered as independent variable.

Apart from account receivable, payable is also taken in account. In case across years

account payable is high then it means that less amount of cash is available to make investment in

business. As discussed above less profit will be earned in the business which ultimately lead to

low ROA.

Inventory is another area which heavily affect profitability. If there is higher amount of

inventory in business then it means that large amount of cash is blocked in unsold or unused

inventory. Again, less cash available for making investment in business which lead to low ROA.

In case of CCC also same thing applied if it takes lot of time to convert anything in to

cash profit will be significantly get affected. More total assets increase profit in business is

assumed to increase which lead to higher ROA.

Thus, these are specific reasons because of which account receivable, payable, inventory,

total assets and cash conversion cycle are considered as independent variable to explain

performance of return on assets.

6

Regression is the one of the model that is used to investigate relationship between dependent

variable and independent variable. In the current research ROA or return on asset is the

dependent variable and its relationship to independent variable account receivable, account

payable, inventory, cash conversion cycle, total asset is used. Regression model is given below.

ROA = Account receivableX1+Account payableX2+InventoryX3+Cash conversion

cycleX4+Total assetsX5

H0: There is not significant impact of account receivable, account payable, inventory, cash

conversion cycle and total assets on ROA.

H1: There is significant impact of account receivable, account payable, inventory, cash

conversion cycle and total assets on ROA.

In the current model receivable is taken in to account as if receivable amount is high

across years then it means that cash amount is blocked in account receivable which means that

less cash is available for making investment in business. Ultimately profit get declined and lead

to low ROA. Such kind of relationship is taken in to account and because of this account

receivable is considered as independent variable.

Apart from account receivable, payable is also taken in account. In case across years

account payable is high then it means that less amount of cash is available to make investment in

business. As discussed above less profit will be earned in the business which ultimately lead to

low ROA.

Inventory is another area which heavily affect profitability. If there is higher amount of

inventory in business then it means that large amount of cash is blocked in unsold or unused

inventory. Again, less cash available for making investment in business which lead to low ROA.

In case of CCC also same thing applied if it takes lot of time to convert anything in to

cash profit will be significantly get affected. More total assets increase profit in business is

assumed to increase which lead to higher ROA.

Thus, these are specific reasons because of which account receivable, payable, inventory,

total assets and cash conversion cycle are considered as independent variable to explain

performance of return on assets.

6

(4) Data, variables and sources

In the raw data set multiple variables data is available namely ROA, Account receivable,

Account payable, total inventories, cash conversion cycle and total assets. In order to prepare

final data 20 FTSE firms financials are taken in to account for 10 years. Thereafter, some

functions like TRANSFORM and SUMIF are used in Excel to obtain final data set which is used

to obtain regression results. 30 years financials for all 20 companies was obtained from website

gurufocus. com. In the regression model ROA is taken as dependent variable and account

receivable, payable, inventory, cash conversion cycle and total assets are considered as

independent variable. Brief explanation on variables is given below. ROA: ROA is not constant and is changing at rapid across years. Interesting fact is that

particular trend remains in existence for three years. In chart attached in appendix it can

be observed that if ROA start decline it reduce consistently for three years. Similarly, if

ROA start increase it almost increase three years. Account receivable: With passage of year account receivable decline consistently which

reflect that firm with change in year successfully reduce cash blockage in receivables. Account payable: Interesting fact is that account payable of firms increase year over year

which means that corporate focus on retaining more and more cash on side of payable.

This reflect that there is already scarcity of cash in business. Payable not paid in current

year carry forward in next year which further mount pressure on the business firm. Inventory: Inventory increase consistently which means that less inventory convert into

cash and more cash is blocked in unsold or unused inventory. Total assets: Total assets increased consistently in the business which is good for the

business firm.

Cash conversion cycle: Cash conversion cycle value decline consistently which good for

the firms. Higher cash conversion cycle reflect situation where firm is taking long time to

convert produced units and inventory in to sales and less time to pay payables. On other

hand, less cash conversion cycle refers to the situation where days of produced units and

inventory conversion in to sales reduced which is good for the firm. In current scenario

cash conversion cycle reduced to great extent which reflect that quickly inventory and

7

In the raw data set multiple variables data is available namely ROA, Account receivable,

Account payable, total inventories, cash conversion cycle and total assets. In order to prepare

final data 20 FTSE firms financials are taken in to account for 10 years. Thereafter, some

functions like TRANSFORM and SUMIF are used in Excel to obtain final data set which is used

to obtain regression results. 30 years financials for all 20 companies was obtained from website

gurufocus. com. In the regression model ROA is taken as dependent variable and account

receivable, payable, inventory, cash conversion cycle and total assets are considered as

independent variable. Brief explanation on variables is given below. ROA: ROA is not constant and is changing at rapid across years. Interesting fact is that

particular trend remains in existence for three years. In chart attached in appendix it can

be observed that if ROA start decline it reduce consistently for three years. Similarly, if

ROA start increase it almost increase three years. Account receivable: With passage of year account receivable decline consistently which

reflect that firm with change in year successfully reduce cash blockage in receivables. Account payable: Interesting fact is that account payable of firms increase year over year

which means that corporate focus on retaining more and more cash on side of payable.

This reflect that there is already scarcity of cash in business. Payable not paid in current

year carry forward in next year which further mount pressure on the business firm. Inventory: Inventory increase consistently which means that less inventory convert into

cash and more cash is blocked in unsold or unused inventory. Total assets: Total assets increased consistently in the business which is good for the

business firm.

Cash conversion cycle: Cash conversion cycle value decline consistently which good for

the firms. Higher cash conversion cycle reflect situation where firm is taking long time to

convert produced units and inventory in to sales and less time to pay payables. On other

hand, less cash conversion cycle refers to the situation where days of produced units and

inventory conversion in to sales reduced which is good for the firm. In current scenario

cash conversion cycle reduced to great extent which reflect that quickly inventory and

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sales on credit convert in to cash. Thus, on this front excellent performance is observed

because substantial decline in cash conversion cycle is observed from FY 2009 to 2018.

(5) Documenting in standard format

Y= α+β*X1+ β*X2+ β*X3+ β*X4++ β*X5

Where

Y= Dependent variable

X= Independent variable

In present case equation is

ROA = Account receivableX1+Account payableX2+InventoryX3+Cash conversion

cycleX4+Total assetsX5

Where

Y= ROA

X1 = Account receivable

X2= Account payable

X3= Inventory

X4= Cash conversion cycle

X5 = Total assets

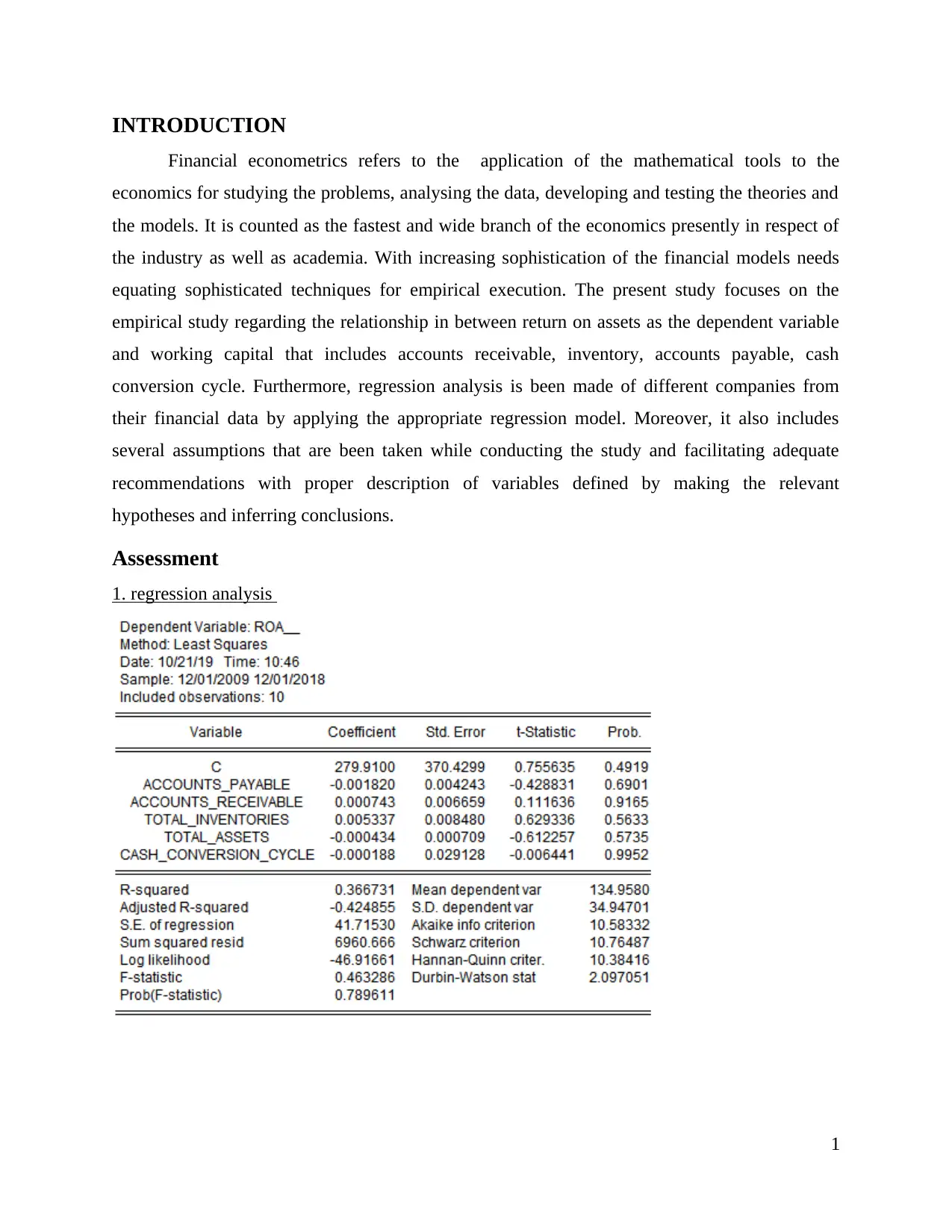

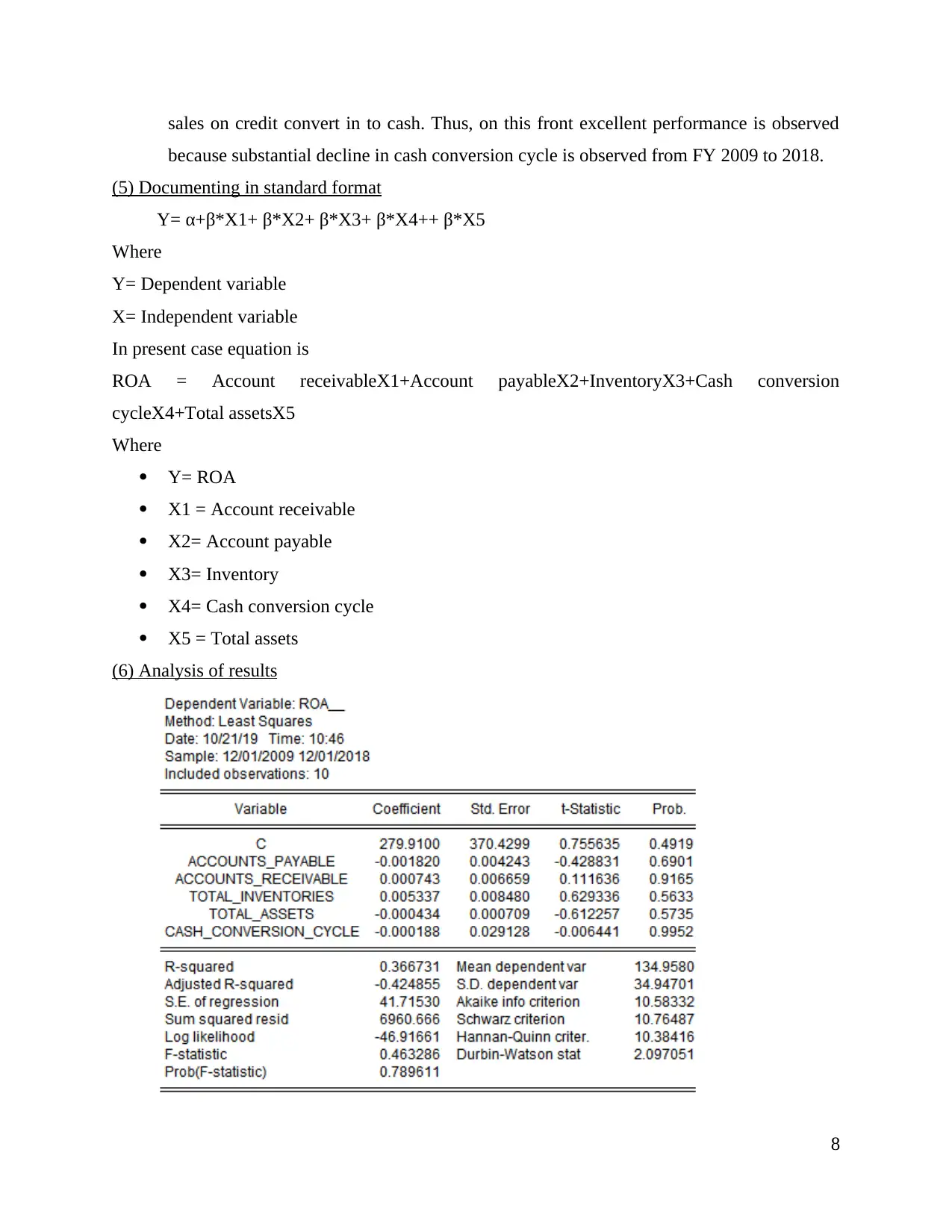

(6) Analysis of results

8

because substantial decline in cash conversion cycle is observed from FY 2009 to 2018.

(5) Documenting in standard format

Y= α+β*X1+ β*X2+ β*X3+ β*X4++ β*X5

Where

Y= Dependent variable

X= Independent variable

In present case equation is

ROA = Account receivableX1+Account payableX2+InventoryX3+Cash conversion

cycleX4+Total assetsX5

Where

Y= ROA

X1 = Account receivable

X2= Account payable

X3= Inventory

X4= Cash conversion cycle

X5 = Total assets

(6) Analysis of results

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation

In the image given above dependent variable is ROA (Return on assets) and independent

variable is account receivable, payable, inventory, total assets and cash conversion cycle. Value

of level of significance is 0.78>0.05 which reflect that because of change in independent variable

any significant change is not observed in dependent variable. Means that if variables payable,

receivable, inventory, assets and cash conversion cycle get changed any big change will not be

observed in dependent variable. R square value is 0.36 which means that independent variable is

explaining 36% variation of dependent variable. Means that there may be any other variable that

is impacting dependent variable and not included in the model. Coefficient values are quite low

in case of payable, receivable, inventory and asset. In case of payable it can be observed that

value of coefficient is only -0.0 which reflect that payable have no impact on return on assets. On

other hand, in case of receivable also same trends are observed and no impact of receivable

observed on return on assets. Inventory, total assets and conversion cycle also indicate same

thing which means that with change in these variables any change does not come in ROA. If we

connect R square values and coefficient values together then in that case it can be observed that

there is relationship between independent variables and dependent variable but same is weak as

only one fourth of variation in dependent variable is explained by independent variable.

Probability value for account receivable is 0.91>0.05 which means that coefficient value in terms

of standard deviation is not far away from zero value. Probability value for account payable is

0.69>0.05 which means that coefficient value in terms of standard deviation is not far away from

zero value. Probability value for inventory is 0.56>0.05 which means that coefficient value in

terms of standard deviation is not far away from zero value. Probability value for total assets is

0.57>0.05 which means that coefficient value in terms of standard deviation is not far away from

zero value. Probability value for cash conversion cycle is 0.99>0.05 which means that coefficient

value in terms of standard deviation is not far away from zero value. Thus, overall it is concluded

that independent variables are not bringing any big change in dependent variable.

Some of the common assumptions of simple linear regression model is given below. Linear relationship: This assumption state that there must be linear relationship between

dependent and independent variable. Means that direction of change must be in specific

pattern for both (Chatterjee and Hadi, 2015). In case movement of both variables

happened not in respect to each other then in that case it become very hard for linear

9

In the image given above dependent variable is ROA (Return on assets) and independent

variable is account receivable, payable, inventory, total assets and cash conversion cycle. Value

of level of significance is 0.78>0.05 which reflect that because of change in independent variable

any significant change is not observed in dependent variable. Means that if variables payable,

receivable, inventory, assets and cash conversion cycle get changed any big change will not be

observed in dependent variable. R square value is 0.36 which means that independent variable is

explaining 36% variation of dependent variable. Means that there may be any other variable that

is impacting dependent variable and not included in the model. Coefficient values are quite low

in case of payable, receivable, inventory and asset. In case of payable it can be observed that

value of coefficient is only -0.0 which reflect that payable have no impact on return on assets. On

other hand, in case of receivable also same trends are observed and no impact of receivable

observed on return on assets. Inventory, total assets and conversion cycle also indicate same

thing which means that with change in these variables any change does not come in ROA. If we

connect R square values and coefficient values together then in that case it can be observed that

there is relationship between independent variables and dependent variable but same is weak as

only one fourth of variation in dependent variable is explained by independent variable.

Probability value for account receivable is 0.91>0.05 which means that coefficient value in terms

of standard deviation is not far away from zero value. Probability value for account payable is

0.69>0.05 which means that coefficient value in terms of standard deviation is not far away from

zero value. Probability value for inventory is 0.56>0.05 which means that coefficient value in

terms of standard deviation is not far away from zero value. Probability value for total assets is

0.57>0.05 which means that coefficient value in terms of standard deviation is not far away from

zero value. Probability value for cash conversion cycle is 0.99>0.05 which means that coefficient

value in terms of standard deviation is not far away from zero value. Thus, overall it is concluded

that independent variables are not bringing any big change in dependent variable.

Some of the common assumptions of simple linear regression model is given below. Linear relationship: This assumption state that there must be linear relationship between

dependent and independent variable. Means that direction of change must be in specific

pattern for both (Chatterjee and Hadi, 2015). In case movement of both variables

happened not in respect to each other then in that case it become very hard for linear

9

regression algorithm to investigate relationship between variables. Thus, it is the one of

the major limitation of linear model that it can measure relationship between two

variables only when there is linear relationship between both variables. Multivariate normality: In linear regression it is assumed that data taken in to account

must be normally distributed. In case data is not normally distributed regression failed to

generate better results. Data scientist usually if data is not normally distributed use non-

parametric test to investigate relationship between variables. Many times, in dataset

outliers are present. Outliers refers to the extreme points in the data set. These outliers

need to be removed in order to obtain modified data that can be used to obtain accurate

results. No multicollinearity: It is one of the main issue associated with linear regression mode.

It refers to the situation where multiple independent variable have strong correlation with

each other (Schroeder, Sjoquist and Stephan, 2016). If such correlation is high then in

that case model cannot generate results. Thus, multicellularity problem is big in

regression model. In order to deal with problem of multi collinearity many experts make

use of log approach and by doing so many times problem of multicollinearity is

controlled.

Homoscedasticity: It is another most important assumption of linear regression approach.

In this assumption it is assumed that predicted values and observed values must be same

or there must not be much difference between them. In other words, it can be said that

there must be almost equal difference between predicted and actual values across all data

points. There is direction connection between R square and homoscedasticity. If there

will be homotheticity R square value will be high (Levine and et.al., 2017). Usually,

Homoscedasticity is not observed when there is any other independent variable

responsible for variation in dependent variable and not included in the regression model.

In such kind of situation R square value always remain low and it is assumed that model

is not best fit. Thus, it is assumption in the linear regression model that error must have

homoscedasticity so that it can be ensured that change in dependent variable is exactly

explained by independent variable.

In present case in regression model homoscedasticity assumption is violated. It is observed

that there is huge variation in residual value that is computed by subtracting predicted value

10

the major limitation of linear model that it can measure relationship between two

variables only when there is linear relationship between both variables. Multivariate normality: In linear regression it is assumed that data taken in to account

must be normally distributed. In case data is not normally distributed regression failed to

generate better results. Data scientist usually if data is not normally distributed use non-

parametric test to investigate relationship between variables. Many times, in dataset

outliers are present. Outliers refers to the extreme points in the data set. These outliers

need to be removed in order to obtain modified data that can be used to obtain accurate

results. No multicollinearity: It is one of the main issue associated with linear regression mode.

It refers to the situation where multiple independent variable have strong correlation with

each other (Schroeder, Sjoquist and Stephan, 2016). If such correlation is high then in

that case model cannot generate results. Thus, multicellularity problem is big in

regression model. In order to deal with problem of multi collinearity many experts make

use of log approach and by doing so many times problem of multicollinearity is

controlled.

Homoscedasticity: It is another most important assumption of linear regression approach.

In this assumption it is assumed that predicted values and observed values must be same

or there must not be much difference between them. In other words, it can be said that

there must be almost equal difference between predicted and actual values across all data

points. There is direction connection between R square and homoscedasticity. If there

will be homotheticity R square value will be high (Levine and et.al., 2017). Usually,

Homoscedasticity is not observed when there is any other independent variable

responsible for variation in dependent variable and not included in the regression model.

In such kind of situation R square value always remain low and it is assumed that model

is not best fit. Thus, it is assumption in the linear regression model that error must have

homoscedasticity so that it can be ensured that change in dependent variable is exactly

explained by independent variable.

In present case in regression model homoscedasticity assumption is violated. It is observed

that there is huge variation in residual value that is computed by subtracting predicted value

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.