Financial Reporting Analysis and Evaluation: A Comprehensive Overview

VerifiedAdded on 2020/07/22

|14

|4002

|87

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, encompassing the interpretation of profit and loss statements, cash flow statements, and balance sheets. It delves into the calculation and presentation of financial ratios to assess industrial performance and investment potential. The report also explores the benefits of International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), evaluating various financial reporting and auditing models. Furthermore, it critically examines financial reporting practices across different countries and analyzes factors that influence reporting. The analysis includes a discussion on the regulatory framework, governance of financial reporting, and the objectives of financial reporting for industrial targets, growth, and development. The report also critiques the regulatory framework and governance, offering suggestions for organizations to solve financial problems based on theories and models. Finally, it offers a critical evaluation of IFRS and its application in various countries.

FINANCIAL REPORT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P 1 Analysing the financial reporting, regulatory framework as well as governance of them.1

P 2 Analysing objectives of financial reporting for Industrial targets, growth and development

................................................................................................................................................2

M1 Analysing the efficiency of financial reporting in context with requirements of

stakeholders............................................................................................................................3

D1 Regulatory framework and governance of financial reporting to stakeholders will be

criticised.................................................................................................................................3

TASK 2............................................................................................................................................3

P 3 Interpretation of profit and loss, cash flow and balance sheets........................................3

P4 Calculation and presentation of financial ratios for industrial performance and investment 6

M 2 Interpretation of Financial ratios and statements in context with better decision making7

D 2 Suggesting organisations as per theories and models in context with solving the financial

problem...................................................................................................................................7

TASK 3............................................................................................................................................7

P 5 Explaining benefits of IAS and IFRS...............................................................................7

P 6 Evaluating models of financial reporting and auditing....................................................8

M 3 Critically evaluating Financial reporting with Judgements and Conclusion..................9

D 3 Criticised evaluation of IFRS and its application in various countries...........................9

TASK 4............................................................................................................................................9

P 7 Evaluating the financial reporting across different countries...........................................9

M 4 Analysing the factors which influence reporting..........................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P 1 Analysing the financial reporting, regulatory framework as well as governance of them.1

P 2 Analysing objectives of financial reporting for Industrial targets, growth and development

................................................................................................................................................2

M1 Analysing the efficiency of financial reporting in context with requirements of

stakeholders............................................................................................................................3

D1 Regulatory framework and governance of financial reporting to stakeholders will be

criticised.................................................................................................................................3

TASK 2............................................................................................................................................3

P 3 Interpretation of profit and loss, cash flow and balance sheets........................................3

P4 Calculation and presentation of financial ratios for industrial performance and investment 6

M 2 Interpretation of Financial ratios and statements in context with better decision making7

D 2 Suggesting organisations as per theories and models in context with solving the financial

problem...................................................................................................................................7

TASK 3............................................................................................................................................7

P 5 Explaining benefits of IAS and IFRS...............................................................................7

P 6 Evaluating models of financial reporting and auditing....................................................8

M 3 Critically evaluating Financial reporting with Judgements and Conclusion..................9

D 3 Criticised evaluation of IFRS and its application in various countries...........................9

TASK 4............................................................................................................................................9

P 7 Evaluating the financial reporting across different countries...........................................9

M 4 Analysing the factors which influence reporting..........................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

In the present report, there will be discussion based on the various terms of financial

reporting which an organisation can use to gather profitable investments. However, there will be

use of various statements such cash flow, profit and loss as well as balance sheet which in turn

helps stakeholders to know the actual financial position of such industry. Thus, such reporting

will help business professionals in making the favourable decisions as well as gathering funds

from investments through investors. In the present era, there will be analysis based on regulatory

framework of financial reporting, IAS and IFRSA which in context with making the fruitful

governance of such reporting used by various industries.

TASK 1

P 1 Analysing the financial reporting, regulatory framework as well as governance of them.

Financial reporting consists with making the statements of an organisation which

contains all the profit and losses, purchase and sale, revenue generation as well as financial

position of an entity. This information is later provided to various stakeholders such as investors,

consumers, organisational heads as to make investment decisions. However, such reporting

regulates better corporate decisions (Leuz and Wysocki, 2016). It brings transparency in such

reporting techniques which will help organisation in generating favourable numbers of

stakeholders or investors. Thus, with the help of such reporting techniques there will be better

governance in industry as the managers or the operating professional will plan new policies and

procedure to lower down costs or expenses. Hence, for better decision making and the

governance in the organisational environment, professionals will make the comparison on the

basis of various operations held in previous years as well as the performance of business during

such years.

Regulatory framework: Financial reporting is based on EU framework which contains

Banking regulations under CRR and CRD which in turn helps professionals to follow the

templates issued by IFRS. Hence, the motive of such regulations' is to make a fixed standard of

financial accounting which in respect with gathering better information as well as recording the

authenticated data (Financial Reporting and Governance, 2017). However, with the help of IAS,

organisations or individual were guided to follow standardise method of preparing such reports

which is universally imposed by this group. Thus, such reporting techniques will help the

1

In the present report, there will be discussion based on the various terms of financial

reporting which an organisation can use to gather profitable investments. However, there will be

use of various statements such cash flow, profit and loss as well as balance sheet which in turn

helps stakeholders to know the actual financial position of such industry. Thus, such reporting

will help business professionals in making the favourable decisions as well as gathering funds

from investments through investors. In the present era, there will be analysis based on regulatory

framework of financial reporting, IAS and IFRSA which in context with making the fruitful

governance of such reporting used by various industries.

TASK 1

P 1 Analysing the financial reporting, regulatory framework as well as governance of them.

Financial reporting consists with making the statements of an organisation which

contains all the profit and losses, purchase and sale, revenue generation as well as financial

position of an entity. This information is later provided to various stakeholders such as investors,

consumers, organisational heads as to make investment decisions. However, such reporting

regulates better corporate decisions (Leuz and Wysocki, 2016). It brings transparency in such

reporting techniques which will help organisation in generating favourable numbers of

stakeholders or investors. Thus, with the help of such reporting techniques there will be better

governance in industry as the managers or the operating professional will plan new policies and

procedure to lower down costs or expenses. Hence, for better decision making and the

governance in the organisational environment, professionals will make the comparison on the

basis of various operations held in previous years as well as the performance of business during

such years.

Regulatory framework: Financial reporting is based on EU framework which contains

Banking regulations under CRR and CRD which in turn helps professionals to follow the

templates issued by IFRS. Hence, the motive of such regulations' is to make a fixed standard of

financial accounting which in respect with gathering better information as well as recording the

authenticated data (Financial Reporting and Governance, 2017). However, with the help of IAS,

organisations or individual were guided to follow standardise method of preparing such reports

which is universally imposed by this group. Thus, such reporting techniques will help the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organisation to have the better supervision over preparation of such financial statements as well

as better liquidity and capital structure which will fruitful in risk controlling as well as

favourable earning. Hence, there will be difference in financial reporting as well as regulatory

framework. Thus, such reporting technique mainly focuses over gathering the number of

investors or paying the creditors. On the other side, regulatory targets the bank supervisors which

in turn help the organisation for having the better interest over r loan, interest rates and the

creditability.

Governance: Financial reporting indicates better corporate governance which in turn

helps organisation in resolving industrial conflicts as well as increasing efficiency of firm

(CORPORATE GOVERNANCE ROLE IN FINANCIAL REPORTING, 2017). However, such

reporting facilitate transparency in statements as well as present such information among

organisational professionals such as Capital providers, managerial directors and supervisors in

firm. Hence, such governance of financial reporting consists with various frameworks such as

financial reporting environment, statement presentation, reporting actual performance, Assets

and liabilities of organisation and the conceptual framework. These are universal standards

which are fixed for financial statements. However, in context with analysing such statements

there need to get the financial ratio analysis and group account transactions which in turn

beneficial for industry to analyse the ability of firm in meeting debts.

P 2 Analysing objectives of financial reporting for Industrial targets, growth and development

With the help of various techniques, regulatory and governance related with developing

the financial reports, will be beneficial for the organisations in having profitable growth of

industry. Hence, Business will be benefited with having conceptual framework which are based

on various logical methods of doing such work (Bishop, DeZoort and Hermanson, 2016). There

can be influence of various external parties such as investors of consumers which in turn make

the profitable judgements for organisation. Thus, such framework considered equity capital

markets for making better financing in the organisation which is influenced by government rules

and regulations, bankruptcy, court decisions, income tax as well as legislations. There will be

several objectives of financial reporting such as:

2

as better liquidity and capital structure which will fruitful in risk controlling as well as

favourable earning. Hence, there will be difference in financial reporting as well as regulatory

framework. Thus, such reporting technique mainly focuses over gathering the number of

investors or paying the creditors. On the other side, regulatory targets the bank supervisors which

in turn help the organisation for having the better interest over r loan, interest rates and the

creditability.

Governance: Financial reporting indicates better corporate governance which in turn

helps organisation in resolving industrial conflicts as well as increasing efficiency of firm

(CORPORATE GOVERNANCE ROLE IN FINANCIAL REPORTING, 2017). However, such

reporting facilitate transparency in statements as well as present such information among

organisational professionals such as Capital providers, managerial directors and supervisors in

firm. Hence, such governance of financial reporting consists with various frameworks such as

financial reporting environment, statement presentation, reporting actual performance, Assets

and liabilities of organisation and the conceptual framework. These are universal standards

which are fixed for financial statements. However, in context with analysing such statements

there need to get the financial ratio analysis and group account transactions which in turn

beneficial for industry to analyse the ability of firm in meeting debts.

P 2 Analysing objectives of financial reporting for Industrial targets, growth and development

With the help of various techniques, regulatory and governance related with developing

the financial reports, will be beneficial for the organisations in having profitable growth of

industry. Hence, Business will be benefited with having conceptual framework which are based

on various logical methods of doing such work (Bishop, DeZoort and Hermanson, 2016). There

can be influence of various external parties such as investors of consumers which in turn make

the profitable judgements for organisation. Thus, such framework considered equity capital

markets for making better financing in the organisation which is influenced by government rules

and regulations, bankruptcy, court decisions, income tax as well as legislations. There will be

several objectives of financial reporting such as:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Presenting disclosure of such financial statements among managerial heads of the

organisation in context with having better planning, judgements as well as fruitful

decision making.

Disclosing such information in external environment as to have proper capital gathering,

investment as well as financial support.

To lower down the cost, liability as well as claims over owner's equity for specific period.

Improving social responsibilities in context with benefiting employees, governments as

well as trade union with favourable allowances.

Facilitate industry in context with reducing cost of work so that professionals with use

funds for expanding the organisational operations.

M1 Analysing the efficiency of financial reporting in context with requirements of stakeholders

Financial reporting will be beneficial for organization in the context with providing fruitful

information to various stakeholders. Thus, it will be beneficial in catching their interest in

making favourable investments decision. Statement contains all the necessary details which are

related to liquidity ratio, annual turnover as well as overall performance of the management. The

owner or board of directors in an entity must implement the use of financial reporting which in

turn helps them in analysing business performance in previous years to be compared with the

current state (Abbott and et.al., 2016). Hence, shareholders will be benefited with their

consideration in the organisation as to earn the sufficient amount of dividend as per shares they

have purchased.

D1 Regulatory framework and governance of financial reporting to stakeholders will be

criticised.

Financial reporting or corporate reporting were developed under the consideration of

company law which in turn helps in governing financial requirements in organisation

(Flower, 2016). Hence, in the current era, it can be seen that use of such statements depends

over attracting investors in having better capital strength.

3

organisation in context with having better planning, judgements as well as fruitful

decision making.

Disclosing such information in external environment as to have proper capital gathering,

investment as well as financial support.

To lower down the cost, liability as well as claims over owner's equity for specific period.

Improving social responsibilities in context with benefiting employees, governments as

well as trade union with favourable allowances.

Facilitate industry in context with reducing cost of work so that professionals with use

funds for expanding the organisational operations.

M1 Analysing the efficiency of financial reporting in context with requirements of stakeholders

Financial reporting will be beneficial for organization in the context with providing fruitful

information to various stakeholders. Thus, it will be beneficial in catching their interest in

making favourable investments decision. Statement contains all the necessary details which are

related to liquidity ratio, annual turnover as well as overall performance of the management. The

owner or board of directors in an entity must implement the use of financial reporting which in

turn helps them in analysing business performance in previous years to be compared with the

current state (Abbott and et.al., 2016). Hence, shareholders will be benefited with their

consideration in the organisation as to earn the sufficient amount of dividend as per shares they

have purchased.

D1 Regulatory framework and governance of financial reporting to stakeholders will be

criticised.

Financial reporting or corporate reporting were developed under the consideration of

company law which in turn helps in governing financial requirements in organisation

(Flower, 2016). Hence, in the current era, it can be seen that use of such statements depends

over attracting investors in having better capital strength.

3

TASK 2

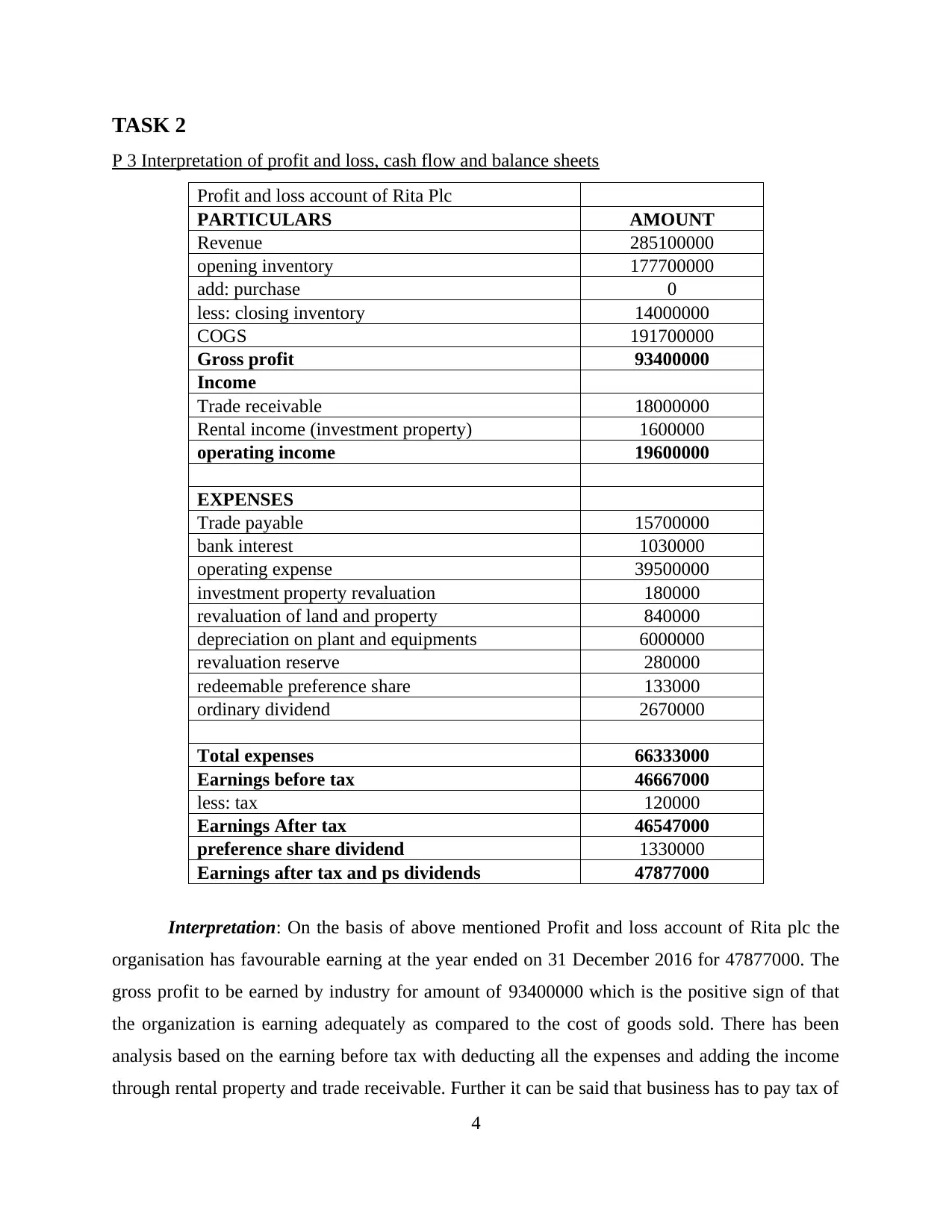

P 3 Interpretation of profit and loss, cash flow and balance sheets

Profit and loss account of Rita Plc

PARTICULARS AMOUNT

Revenue 285100000

opening inventory 177700000

add: purchase 0

less: closing inventory 14000000

COGS 191700000

Gross profit 93400000

Income

Trade receivable 18000000

Rental income (investment property) 1600000

operating income 19600000

EXPENSES

Trade payable 15700000

bank interest 1030000

operating expense 39500000

investment property revaluation 180000

revaluation of land and property 840000

depreciation on plant and equipments 6000000

revaluation reserve 280000

redeemable preference share 133000

ordinary dividend 2670000

Total expenses 66333000

Earnings before tax 46667000

less: tax 120000

Earnings After tax 46547000

preference share dividend 1330000

Earnings after tax and ps dividends 47877000

Interpretation: On the basis of above mentioned Profit and loss account of Rita plc the

organisation has favourable earning at the year ended on 31 December 2016 for 47877000. The

gross profit to be earned by industry for amount of 93400000 which is the positive sign of that

the organization is earning adequately as compared to the cost of goods sold. There has been

analysis based on the earning before tax with deducting all the expenses and adding the income

through rental property and trade receivable. Further it can be said that business has to pay tax of

4

P 3 Interpretation of profit and loss, cash flow and balance sheets

Profit and loss account of Rita Plc

PARTICULARS AMOUNT

Revenue 285100000

opening inventory 177700000

add: purchase 0

less: closing inventory 14000000

COGS 191700000

Gross profit 93400000

Income

Trade receivable 18000000

Rental income (investment property) 1600000

operating income 19600000

EXPENSES

Trade payable 15700000

bank interest 1030000

operating expense 39500000

investment property revaluation 180000

revaluation of land and property 840000

depreciation on plant and equipments 6000000

revaluation reserve 280000

redeemable preference share 133000

ordinary dividend 2670000

Total expenses 66333000

Earnings before tax 46667000

less: tax 120000

Earnings After tax 46547000

preference share dividend 1330000

Earnings after tax and ps dividends 47877000

Interpretation: On the basis of above mentioned Profit and loss account of Rita plc the

organisation has favourable earning at the year ended on 31 December 2016 for 47877000. The

gross profit to be earned by industry for amount of 93400000 which is the positive sign of that

the organization is earning adequately as compared to the cost of goods sold. There has been

analysis based on the earning before tax with deducting all the expenses and adding the income

through rental property and trade receivable. Further it can be said that business has to pay tax of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1200000 which bring earning of 43547000. After adding the preference share dividend, the

earning is 47877000.

cash flow statement of Rita plc

PARTICULARS AMOUNT

Earnings after tax and Pref.Sh

dividend 47877000

Bank 1200000

investment property revaluation 180000

revaluation of land and property 840000

depreciation on plant and equipments 6000000

revaluation reserve 280000

Deferred tax 6900000

increase in inventory 600000

cash flow 34277000

Interpretation: on the basis of above measured cash flow statement of Rita plc, as per

inflow and outflow of the cash during this assessment year, which in turn helps in bringing the

favourable cash flow of 34277000.

Financial position of Rita plc

Particulars AMOUNT AMOUNT

Current assets

bank 1200000

cash 34277000

trade receivable 1800000

total current assets 37277000

fixed assets

Land and property 84000000

less: depreciation 840000 83160000

investment property 21300000

less: depreciation 180000 21120000

plant and equipments 4800000

less: depreciation 600000 4200000

suspense account 1067000

Total fixed assets 109547000

Total assets 146824000

Current liabilities

Retained earning 23300000

5

earning is 47877000.

cash flow statement of Rita plc

PARTICULARS AMOUNT

Earnings after tax and Pref.Sh

dividend 47877000

Bank 1200000

investment property revaluation 180000

revaluation of land and property 840000

depreciation on plant and equipments 6000000

revaluation reserve 280000

Deferred tax 6900000

increase in inventory 600000

cash flow 34277000

Interpretation: on the basis of above measured cash flow statement of Rita plc, as per

inflow and outflow of the cash during this assessment year, which in turn helps in bringing the

favourable cash flow of 34277000.

Financial position of Rita plc

Particulars AMOUNT AMOUNT

Current assets

bank 1200000

cash 34277000

trade receivable 1800000

total current assets 37277000

fixed assets

Land and property 84000000

less: depreciation 840000 83160000

investment property 21300000

less: depreciation 180000 21120000

plant and equipments 4800000

less: depreciation 600000 4200000

suspense account 1067000

Total fixed assets 109547000

Total assets 146824000

Current liabilities

Retained earning 23300000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ordinary share capital 26700000

preference share capital 1330000

LESS: 10% redemption 133000 1197000

total current liabilities 51197000

bank interest 1030000

EATD 47877000

deferred taxation 6900000

tax 120000

accumulated depreciation 22400000 22400000

trade payable 15700000

rental income 1600000

total liabilities 146824000

Interpretation: Above listed financial position of Rita Plc indicates assets and liability as

well as ability of the organisation in paying their shareholders. Hence, there will be calculations

over depreciation charged to various fixed assets such as Land and property, plant and machinery

etc. Which helps in finding favourable values of such assets. Thus, the balance lies between total

assets and liabilities is for 146824000.

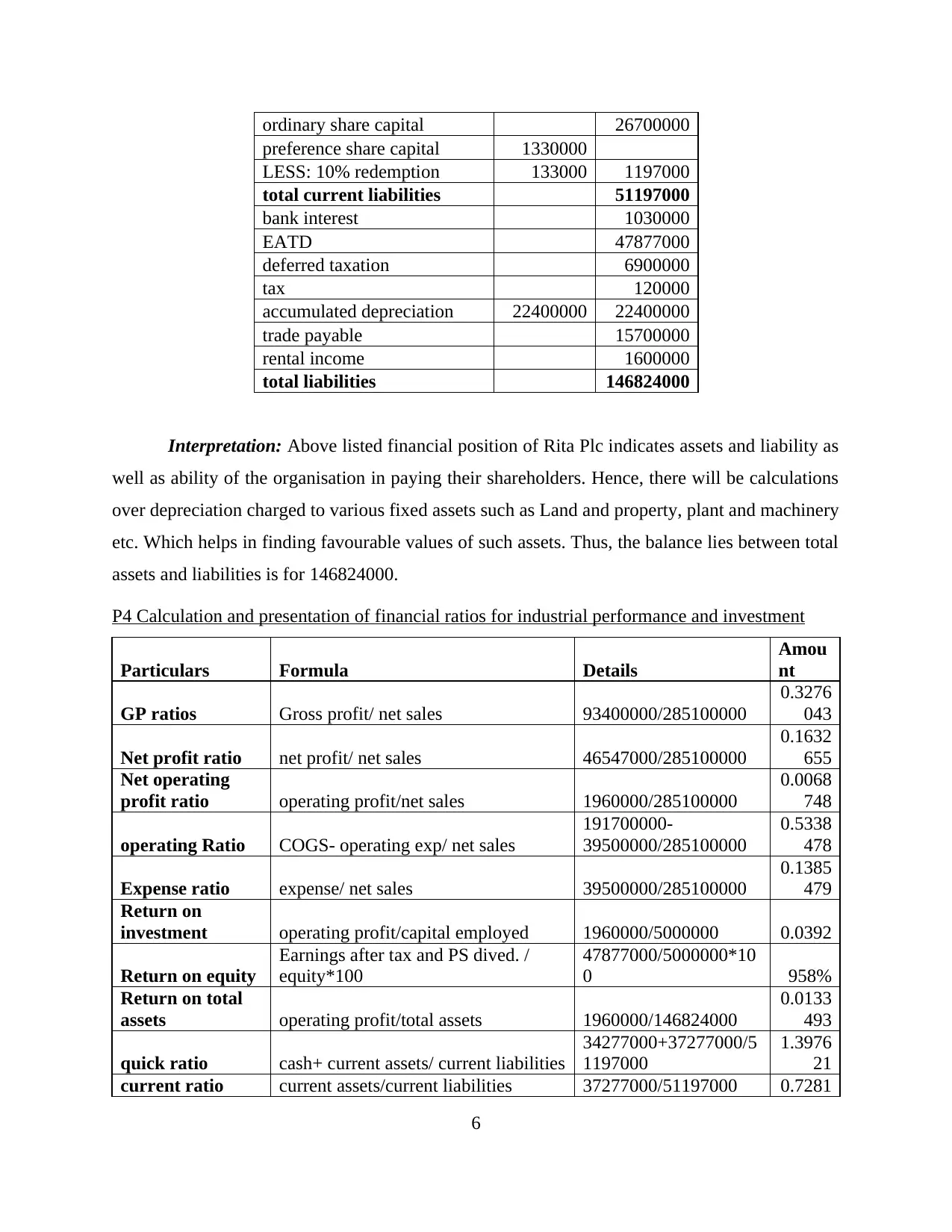

P4 Calculation and presentation of financial ratios for industrial performance and investment

Particulars Formula Details

Amou

nt

GP ratios Gross profit/ net sales 93400000/285100000

0.3276

043

Net profit ratio net profit/ net sales 46547000/285100000

0.1632

655

Net operating

profit ratio operating profit/net sales 1960000/285100000

0.0068

748

operating Ratio COGS- operating exp/ net sales

191700000-

39500000/285100000

0.5338

478

Expense ratio expense/ net sales 39500000/285100000

0.1385

479

Return on

investment operating profit/capital employed 1960000/5000000 0.0392

Return on equity

Earnings after tax and PS dived. /

equity*100

47877000/5000000*10

0 958%

Return on total

assets operating profit/total assets 1960000/146824000

0.0133

493

quick ratio cash+ current assets/ current liabilities

34277000+37277000/5

1197000

1.3976

21

current ratio current assets/current liabilities 37277000/51197000 0.7281

6

preference share capital 1330000

LESS: 10% redemption 133000 1197000

total current liabilities 51197000

bank interest 1030000

EATD 47877000

deferred taxation 6900000

tax 120000

accumulated depreciation 22400000 22400000

trade payable 15700000

rental income 1600000

total liabilities 146824000

Interpretation: Above listed financial position of Rita Plc indicates assets and liability as

well as ability of the organisation in paying their shareholders. Hence, there will be calculations

over depreciation charged to various fixed assets such as Land and property, plant and machinery

etc. Which helps in finding favourable values of such assets. Thus, the balance lies between total

assets and liabilities is for 146824000.

P4 Calculation and presentation of financial ratios for industrial performance and investment

Particulars Formula Details

Amou

nt

GP ratios Gross profit/ net sales 93400000/285100000

0.3276

043

Net profit ratio net profit/ net sales 46547000/285100000

0.1632

655

Net operating

profit ratio operating profit/net sales 1960000/285100000

0.0068

748

operating Ratio COGS- operating exp/ net sales

191700000-

39500000/285100000

0.5338

478

Expense ratio expense/ net sales 39500000/285100000

0.1385

479

Return on

investment operating profit/capital employed 1960000/5000000 0.0392

Return on equity

Earnings after tax and PS dived. /

equity*100

47877000/5000000*10

0 958%

Return on total

assets operating profit/total assets 1960000/146824000

0.0133

493

quick ratio cash+ current assets/ current liabilities

34277000+37277000/5

1197000

1.3976

21

current ratio current assets/current liabilities 37277000/51197000 0.7281

6

091

Interpretation: As per the above analysis of various financial ratios of organisation

which describes efficiency of firm in meeting long term or short-term debts, that the firm is

capable of paying its shareholders on required time. Gross profit ratios is around 0.32, net profit

is 0.16, operating profit is 0.006 and operating ratio is 0.53 which explains that firm has better or

positive earning throughout the year. Thus, the cost of selling an article is lower than profit

generated through sales of such goods. The current ratio of firm is 0.72 which says,company has

ability to meet its debts on time.

M 2 Interpretation of Financial ratios and statements in context with better decision making

On the basis of Rita Plc’s financial statements and ratios, this describes that the

organisation has made favourable earning throughout the years and has better gains in

millions. Hence, on the basis of above listed financial ratios the firm has ability to meet the

debts as well as has the better capital structure which in turn fruitful in paying shareholders

(Fraser, Ormiston and Fraser, 2010). Thus, it will be beneficial of the firm to gain the large

numbers of stakeholders or investors. There is need to expand the operational activities in

the industry as to maximises the sales or reduces the costs than it will be more profitable.

D 2 Suggesting organisations as per theories and models in context with solving the financial

problem

Theories of models has been used by various organisation in favour with making the suitable

financial decisions which in turn helps them in having better organisational control. Thus, it

can be suggested to Rita plc that they should introduce the current new techniques of

disclosing the financial statements such as integrated reports, CSR, sustainability reporting

(Daske and et.al., 2013). Hence, these techniques will be fruitful for the organisation in

having better cost control as well as generate the capital gains.

TASK 3

P 5 Explaining benefits of IAS and IFRS

To understand the better techniques for presenting the financial reports there has been

influence of International Accounting Standards as well as International financial reporting

standards (Mankin, Jewell and Rivas, 2017). Thus, such reporting techniques will help the

7

Interpretation: As per the above analysis of various financial ratios of organisation

which describes efficiency of firm in meeting long term or short-term debts, that the firm is

capable of paying its shareholders on required time. Gross profit ratios is around 0.32, net profit

is 0.16, operating profit is 0.006 and operating ratio is 0.53 which explains that firm has better or

positive earning throughout the year. Thus, the cost of selling an article is lower than profit

generated through sales of such goods. The current ratio of firm is 0.72 which says,company has

ability to meet its debts on time.

M 2 Interpretation of Financial ratios and statements in context with better decision making

On the basis of Rita Plc’s financial statements and ratios, this describes that the

organisation has made favourable earning throughout the years and has better gains in

millions. Hence, on the basis of above listed financial ratios the firm has ability to meet the

debts as well as has the better capital structure which in turn fruitful in paying shareholders

(Fraser, Ormiston and Fraser, 2010). Thus, it will be beneficial of the firm to gain the large

numbers of stakeholders or investors. There is need to expand the operational activities in

the industry as to maximises the sales or reduces the costs than it will be more profitable.

D 2 Suggesting organisations as per theories and models in context with solving the financial

problem

Theories of models has been used by various organisation in favour with making the suitable

financial decisions which in turn helps them in having better organisational control. Thus, it

can be suggested to Rita plc that they should introduce the current new techniques of

disclosing the financial statements such as integrated reports, CSR, sustainability reporting

(Daske and et.al., 2013). Hence, these techniques will be fruitful for the organisation in

having better cost control as well as generate the capital gains.

TASK 3

P 5 Explaining benefits of IAS and IFRS

To understand the better techniques for presenting the financial reports there has been

influence of International Accounting Standards as well as International financial reporting

standards (Mankin, Jewell and Rivas, 2017). Thus, such reporting techniques will help the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

professionals, accountants, auditor to make the favourable statements. There have been

various benefits such standards which are as follows:

International Accounting Standards (IAS): The motive behind introducing such

financial statements which in turns facilitating an internationally accepted financial

reporting standard (Ashraf, Rizwan and L’Huillier, 2016). Thus, know a day’s these

accounting standards have been adopted by various countries as well as many small-scale

industries are also using it. It helps the accounting professionals in the preparation of

financial statements with the help of internationally fixed framework. There have been

various benefits of such accounts which are as follows:

It will be fruitful in improving capital flow as well as brings the transparency in

accounting process.

It has been adopted by various countries so it becomes beneficial for organisation

to have international investors, so which in turn helps firm in having better capital

structure. It encourages the business interest as well as motivates the industries to make the

fruitful use of financial reporting.

International Financial Reporting Standards (IFRS): It was developed by the IAS board

in context with making a fix standard to be followed by every nation’s companies to

disclose financial statements with the help of principles (Salam, 2016). There have been

various benefits of these financial standards which are as follows:

It helps in improving he corporate governance as well as encouraging the free cash

capital flows across the national boundaries.

Encourages growth of international business with in turns increase the economic

efficiency of organisations.

Data set of an industry prepared on international fixed standard which in turn helps

international investors to understand such information as well as enhances the

investment opportunities to a firm.

8

various benefits such standards which are as follows:

International Accounting Standards (IAS): The motive behind introducing such

financial statements which in turns facilitating an internationally accepted financial

reporting standard (Ashraf, Rizwan and L’Huillier, 2016). Thus, know a day’s these

accounting standards have been adopted by various countries as well as many small-scale

industries are also using it. It helps the accounting professionals in the preparation of

financial statements with the help of internationally fixed framework. There have been

various benefits of such accounts which are as follows:

It will be fruitful in improving capital flow as well as brings the transparency in

accounting process.

It has been adopted by various countries so it becomes beneficial for organisation

to have international investors, so which in turn helps firm in having better capital

structure. It encourages the business interest as well as motivates the industries to make the

fruitful use of financial reporting.

International Financial Reporting Standards (IFRS): It was developed by the IAS board

in context with making a fix standard to be followed by every nation’s companies to

disclose financial statements with the help of principles (Salam, 2016). There have been

various benefits of these financial standards which are as follows:

It helps in improving he corporate governance as well as encouraging the free cash

capital flows across the national boundaries.

Encourages growth of international business with in turns increase the economic

efficiency of organisations.

Data set of an industry prepared on international fixed standard which in turn helps

international investors to understand such information as well as enhances the

investment opportunities to a firm.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P 6 Evaluating models of financial reporting and auditing

Models and various theories are designed as to have the better framework in regulating the

favourable financial functioning of the organisation. There has been implementation of

various standards as to form the better use or measurement of financial statement. Thus, in

turns with having the profitable outcomes hic will result in generating the large numbers of

stakeholders to the industry (Ioannou and Serafeim, 2016). Various models have been

implementing in force by GAAP with IFRS which in turn helps the organisation to fetch

the adequate knowledge relevant to financial reporting and its framework. Thus, such

reporting techniques help the accounting professionals to make beneficial auditing in

context with achieving the organisational profit.

M 3 Critically evaluating Financial reporting with Judgements and Conclusion

Coherent application of theories and models may be beneficial for the organisation in

having better or adequate financial reporting techniques but currently the concept of presenting a

report is totally changed. Thus, main focus is paid on having favourable numbers of stakeholders

of organisation in context with having better capital gains (Padachi, Ramsurrun and Ramen,

2017). Thus, it will be fruitful that, industry should have better capital structure but there will be

reduction in the operational performance of the firm. The corporate social responsibility is now

on existence that the value of employees is being replaced with various machineries and robotic

arms.

D 3 Criticised evaluation of IFRS and its application in various countries

Implication of these financial techniques is done as to make the better reporting with the use

of authenticated data and the favourable information. Thus, with adequate knowledge of the

financial position of an organisation there will be generation of favourable numbers of

stakeholders as well as helps in internal management (Bonetti, Magnan and Parbonetti,

2016). Various countries such as USA, UK, European countries as well as Asian countries

has adopted these concepts and they are making profitable efforts as to have better

operational functioning of the organisation.

9

Models and various theories are designed as to have the better framework in regulating the

favourable financial functioning of the organisation. There has been implementation of

various standards as to form the better use or measurement of financial statement. Thus, in

turns with having the profitable outcomes hic will result in generating the large numbers of

stakeholders to the industry (Ioannou and Serafeim, 2016). Various models have been

implementing in force by GAAP with IFRS which in turn helps the organisation to fetch

the adequate knowledge relevant to financial reporting and its framework. Thus, such

reporting techniques help the accounting professionals to make beneficial auditing in

context with achieving the organisational profit.

M 3 Critically evaluating Financial reporting with Judgements and Conclusion

Coherent application of theories and models may be beneficial for the organisation in

having better or adequate financial reporting techniques but currently the concept of presenting a

report is totally changed. Thus, main focus is paid on having favourable numbers of stakeholders

of organisation in context with having better capital gains (Padachi, Ramsurrun and Ramen,

2017). Thus, it will be fruitful that, industry should have better capital structure but there will be

reduction in the operational performance of the firm. The corporate social responsibility is now

on existence that the value of employees is being replaced with various machineries and robotic

arms.

D 3 Criticised evaluation of IFRS and its application in various countries

Implication of these financial techniques is done as to make the better reporting with the use

of authenticated data and the favourable information. Thus, with adequate knowledge of the

financial position of an organisation there will be generation of favourable numbers of

stakeholders as well as helps in internal management (Bonetti, Magnan and Parbonetti,

2016). Various countries such as USA, UK, European countries as well as Asian countries

has adopted these concepts and they are making profitable efforts as to have better

operational functioning of the organisation.

9

TASK 4

P 7 Evaluating the financial reporting across different countries

There has been evaluation of financial reporting techniques in early 1999 which in turn

access the requirements of the managers as well as stakeholders in the organisation. These

can be started with the use of four financial tools such as balance sheet, income statements,

cash flows and the equity calculations for owners (Leuz and Wysocki, 2016). Various rules

and standards are developed for the organisation for having better accounting techniques to

be used by organisational professionals such as Security Exchange Commission,

Extensible Business Reporting Language which in turn facilitate better organisational

communication between various companies. Thus, it helps firms in having better

investments as well as better goodwill in context with satisfying requirements of the

stakeholders.

M 4 Analysing the factors which influence reporting

There have been various factors with influence the use of IFRS standards in

presenting the reports. The influence of government and various stakeholders which in turn

affects the use of such techniques or methods presented by IFRS (Daske and et.al., 2013).

Various perceptions have been be made by big MNCs that the use of such methods is very

time consuming as well as it did not affect much in attaining the organisational growth.

CONCLUSION

As per above discussed report or study, it can be concluded that the financial reporting is a

technique or method through which a company can analyse the overall performance in the

assessment year. Thus, it facilitates better communication between organisations as well as

stakeholders. Hence, as per the financial findings of Rita Plc it can be said that the entity is

operating on the favourable state as well as having better operational growth. Further, it can

be said that, due to implication of various standards such as IAS and IFRS which in turn

helps accounting professional in preparing such data sets by facilitating the framework.

10

P 7 Evaluating the financial reporting across different countries

There has been evaluation of financial reporting techniques in early 1999 which in turn

access the requirements of the managers as well as stakeholders in the organisation. These

can be started with the use of four financial tools such as balance sheet, income statements,

cash flows and the equity calculations for owners (Leuz and Wysocki, 2016). Various rules

and standards are developed for the organisation for having better accounting techniques to

be used by organisational professionals such as Security Exchange Commission,

Extensible Business Reporting Language which in turn facilitate better organisational

communication between various companies. Thus, it helps firms in having better

investments as well as better goodwill in context with satisfying requirements of the

stakeholders.

M 4 Analysing the factors which influence reporting

There have been various factors with influence the use of IFRS standards in

presenting the reports. The influence of government and various stakeholders which in turn

affects the use of such techniques or methods presented by IFRS (Daske and et.al., 2013).

Various perceptions have been be made by big MNCs that the use of such methods is very

time consuming as well as it did not affect much in attaining the organisational growth.

CONCLUSION

As per above discussed report or study, it can be concluded that the financial reporting is a

technique or method through which a company can analyse the overall performance in the

assessment year. Thus, it facilitates better communication between organisations as well as

stakeholders. Hence, as per the financial findings of Rita Plc it can be said that the entity is

operating on the favourable state as well as having better operational growth. Further, it can

be said that, due to implication of various standards such as IAS and IFRS which in turn

helps accounting professional in preparing such data sets by facilitating the framework.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.