Financial Accounting and Reporting: Analysis of Financial Statements

VerifiedAdded on 2020/01/21

|16

|4247

|68

Report

AI Summary

This report delves into the realm of financial accounting and reporting, commencing with an exploration of the diverse users of financial statements, including investors, employees, customers, government entities, suppliers, and shareholders, and their respective information needs. It then elucidates the legal and regulatory influences shaping financial statements, encompassing the Companies Act 2006, UK accounting standards, GAAP, IFRS, and IAS, and assesses the implications of these frameworks for various stakeholders. The report further examines the ways different laws and regulations are addressed by accounting and reporting standards. It differentiates the information needs of various user groups, and prepares financial statements for publication by sole traders, partnerships, and limited companies. The report also includes the calculation and interpretation of accounting ratios to assess the performance and position of a company, along with suitable comparisons. The document concludes by providing a summary of the key findings and insights gained throughout the analysis.

Financial Accounting

and Reporting

and Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

1.1 Describing the different users of financial statement and their needs...................................3

1.2 Explaining the legal and regulatory framework influences on financial statements.............4

1.3 Assessing the implications for users......................................................................................5

1.4 Explaining different laws/regulations are dealt with by accounting and reporting standards

......................................................................................................................................................6

3.1 Explaining the information needs of different groups vary ..................................................6

3.2 Preparing financial statements for publication by a sole trader, partnership and limited

company.......................................................................................................................................7

Task 2...............................................................................................................................................8

Task 3...............................................................................................................................................8

4.1 Calculating accounting ratios to assess the performance and position of the ABC Ltd........8

4.2 Preparing a report incorporating and interpreting accounting ratios, including suitable

comparisons.................................................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................12

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

1.1 Describing the different users of financial statement and their needs...................................3

1.2 Explaining the legal and regulatory framework influences on financial statements.............4

1.3 Assessing the implications for users......................................................................................5

1.4 Explaining different laws/regulations are dealt with by accounting and reporting standards

......................................................................................................................................................6

3.1 Explaining the information needs of different groups vary ..................................................6

3.2 Preparing financial statements for publication by a sole trader, partnership and limited

company.......................................................................................................................................7

Task 2...............................................................................................................................................8

Task 3...............................................................................................................................................8

4.1 Calculating accounting ratios to assess the performance and position of the ABC Ltd........8

4.2 Preparing a report incorporating and interpreting accounting ratios, including suitable

comparisons.................................................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................12

INDEX OF TABLES

Table 1: Fundamental principles towards preparing Financial statements......................................8

Table 2: Format of income statement..............................................................................................9

Table 3: Format of profit and loss statement.................................................................................10

Table 4: Format of Cash flow statement........................................................................................10

Table 5: Format of Balance sheet..................................................................................................11

Table 6: Calculation of Ratios.......................................................................................................12

Table 1: Fundamental principles towards preparing Financial statements......................................8

Table 2: Format of income statement..............................................................................................9

Table 3: Format of profit and loss statement.................................................................................10

Table 4: Format of Cash flow statement........................................................................................10

Table 5: Format of Balance sheet..................................................................................................11

Table 6: Calculation of Ratios.......................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is a specialized branch of accounting and it is concerned with the

summary, analysis and reporting of monetary transactions for decision makers (Macve, 2015).

This involves preparation of the monetary statements for those people, who interested in

receiving such information. Financial statement is a process in which statements are produced,

which discloses the economic position of company to management, investors, stakeholders and

to the government (Francis and et.al., 2015). This report is based on the different cases, users of

financial statements and their needs are described. The legal and regulatory influences on these

statements and the implication for the users are explained. Format of the monetary statements for

a variety of businesses and a consolidated balance sheet and profit and loss a/c for a single group

of company is prepared. Incorporating and interpreting of accounting ratios are covered in this

report.

TASK 1

1.1 Describing the different users of financial statement and their needs

There are many users of financial statements which are produced by the company (Users

of Financial Statements, 2015). As it provides useful information to the users, some of these are:

Investors- They are more interested to know the company's profits and also the security

of their investments. With the help of the company's past financial statements, investor can

estimate the future returns (Armstrong and et.al., 2015). By this they can determine whether to

invest or not and can also access the ability of the firm to pay good returns.

Employees- They also need to know the stability and profitability of the company and

the ability of the company to provide remunerations, employment opportunities, retirement

benefits etc in the future (Weygandt, Kimmel and Kieso, 2015). The major interest of employees

is to know the current financial position of the company so they can plan their future in the

organization.

Customers- As customers are dependent on the company for specialized supplies and for

this they need to know whether company will continue supply them in the future or not (Barth,

2015). They need information of the profitability and the sales of the company to know the

continuance of the business.

Financial accounting is a specialized branch of accounting and it is concerned with the

summary, analysis and reporting of monetary transactions for decision makers (Macve, 2015).

This involves preparation of the monetary statements for those people, who interested in

receiving such information. Financial statement is a process in which statements are produced,

which discloses the economic position of company to management, investors, stakeholders and

to the government (Francis and et.al., 2015). This report is based on the different cases, users of

financial statements and their needs are described. The legal and regulatory influences on these

statements and the implication for the users are explained. Format of the monetary statements for

a variety of businesses and a consolidated balance sheet and profit and loss a/c for a single group

of company is prepared. Incorporating and interpreting of accounting ratios are covered in this

report.

TASK 1

1.1 Describing the different users of financial statement and their needs

There are many users of financial statements which are produced by the company (Users

of Financial Statements, 2015). As it provides useful information to the users, some of these are:

Investors- They are more interested to know the company's profits and also the security

of their investments. With the help of the company's past financial statements, investor can

estimate the future returns (Armstrong and et.al., 2015). By this they can determine whether to

invest or not and can also access the ability of the firm to pay good returns.

Employees- They also need to know the stability and profitability of the company and

the ability of the company to provide remunerations, employment opportunities, retirement

benefits etc in the future (Weygandt, Kimmel and Kieso, 2015). The major interest of employees

is to know the current financial position of the company so they can plan their future in the

organization.

Customers- As customers are dependent on the company for specialized supplies and for

this they need to know whether company will continue supply them in the future or not (Barth,

2015). They need information of the profitability and the sales of the company to know the

continuance of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Government- The main user of financial statement is government; they require this to

determine the correctness of the tax declared in the tax returns (Martin and Roychowdhury,

2015). They need information that, need information of the profitability, sales of the company

and whether firm is paying tax or not, the contribution of the firm towards the society, and did

they follow the government regulations.

Suppliers and other trade creditors- Suppliers are those who supply the products and

services of the company (Hirtle and et.al., 2015). They need financial statement to know the

credit worthiness of the firm and to know whether they supply goods on credit.

Shareholders- They are the owner of the shares which is issued by the organization, they

use financial statement to assess the risk and return of their investment in the company. With the

help of the financial statement, they can determine whether to purchase shares or not and by this

they can also access the ability of firm to pay good dividends.

1.2 Explaining the legal and regulatory framework influences on financial statements

There are different legal and regulatory influences which are to be determined at the time

of preparing financial statements. In UK, accounting regulations are divided into three main

regulatory authorities and governance which must be abide by all the entities whether sole trade

partnership or limited companies while preparing their financial year end (Martínez‐Ferrero,

Garcia‐Sanchez and Cuadrado‐Ballesteros, 2015). The three regulatory bodies are the Companies

act 2006, UK accounting standards board and the international accounting standards. They need

financial statement to know the credit worthiness of the firm

GAAP (Generally accepted accounting principles) are the framework which includes the

guidelines of general accounting. It includes rules, which are to be followed by a

business/financial manager while recording, summarizing and preparing the financial statements.

The rules and guidelines are to be considered while preparing financial reports (Greenbaum,

Thakor and Boot, 2015).

IFRS (International Financial Reporting Standards) are designed as a common language

for business affairs, so that across the international boundaries company accounts are

understandable and comparable. These are important for those companies that have dealing in

determine the correctness of the tax declared in the tax returns (Martin and Roychowdhury,

2015). They need information that, need information of the profitability, sales of the company

and whether firm is paying tax or not, the contribution of the firm towards the society, and did

they follow the government regulations.

Suppliers and other trade creditors- Suppliers are those who supply the products and

services of the company (Hirtle and et.al., 2015). They need financial statement to know the

credit worthiness of the firm and to know whether they supply goods on credit.

Shareholders- They are the owner of the shares which is issued by the organization, they

use financial statement to assess the risk and return of their investment in the company. With the

help of the financial statement, they can determine whether to purchase shares or not and by this

they can also access the ability of firm to pay good dividends.

1.2 Explaining the legal and regulatory framework influences on financial statements

There are different legal and regulatory influences which are to be determined at the time

of preparing financial statements. In UK, accounting regulations are divided into three main

regulatory authorities and governance which must be abide by all the entities whether sole trade

partnership or limited companies while preparing their financial year end (Martínez‐Ferrero,

Garcia‐Sanchez and Cuadrado‐Ballesteros, 2015). The three regulatory bodies are the Companies

act 2006, UK accounting standards board and the international accounting standards. They need

financial statement to know the credit worthiness of the firm

GAAP (Generally accepted accounting principles) are the framework which includes the

guidelines of general accounting. It includes rules, which are to be followed by a

business/financial manager while recording, summarizing and preparing the financial statements.

The rules and guidelines are to be considered while preparing financial reports (Greenbaum,

Thakor and Boot, 2015).

IFRS (International Financial Reporting Standards) are designed as a common language

for business affairs, so that across the international boundaries company accounts are

understandable and comparable. These are important for those companies that have dealing in

several countries (Hirtle and et.al., 2015). All listed and grouped EU companies are required to

use IFRS since 2005.

IAS (International Accounting Standards), this is the accounting standards issued by the

IASB and the IASC. All the UK listed and sometimes unlisted companies are required to present

their financial statements by using international standards.

Company’s act 2005, 'Accounts and reports' are structured so that provisions which apply

to different companies are easily identifiable. Companies Act 2006 implements relevant

requirement of EU laws (Macve, 2015). This act is wide ranging and all the laws applicable to

companies are covered. This required compulsory audit of balance sheet and profit and loss a/c.

The role of UK accounting standard board is to issue accounting standards; it influences the

development of international standards. The IASB was formed to replace the IASC.

1.3 Assessing the implications for users

There are different legal and regulatory frameworks which are to be determined by all the

entities (Lang and Stice-Lawrence, 2015). Whether sole trade partnership or limited companies

at the time of preparing their financial statements like profit and loss a/c, balance sheet and cash

flow statements. While determining this framework, there are great impacts on users, such as:

The applications of legal and regulatory framework have a positive impact on the users,

with the help of the financial statement they can get the accurate information about the

company on which investors are interested to invest.

By applying these guidelines it is easier way to understand the financial statements of the

company, from which we can acquire the information related to the profits or losses from

the profit and loss a/c (Weygandt, Kimmel and Kieso, 2015).

This helps the investors in getting the proper information of the financial position of the

company. By this, risk and return are analyzed, they are more interested to know the

company's profits and also the security of their investments and it helps to make effective

investment decisions (Users of Financial Statements, 2015).

It also helps in determining the exact position of the company in the market. With these

employees can compare the financial position with the other companies.

use IFRS since 2005.

IAS (International Accounting Standards), this is the accounting standards issued by the

IASB and the IASC. All the UK listed and sometimes unlisted companies are required to present

their financial statements by using international standards.

Company’s act 2005, 'Accounts and reports' are structured so that provisions which apply

to different companies are easily identifiable. Companies Act 2006 implements relevant

requirement of EU laws (Macve, 2015). This act is wide ranging and all the laws applicable to

companies are covered. This required compulsory audit of balance sheet and profit and loss a/c.

The role of UK accounting standard board is to issue accounting standards; it influences the

development of international standards. The IASB was formed to replace the IASC.

1.3 Assessing the implications for users

There are different legal and regulatory frameworks which are to be determined by all the

entities (Lang and Stice-Lawrence, 2015). Whether sole trade partnership or limited companies

at the time of preparing their financial statements like profit and loss a/c, balance sheet and cash

flow statements. While determining this framework, there are great impacts on users, such as:

The applications of legal and regulatory framework have a positive impact on the users,

with the help of the financial statement they can get the accurate information about the

company on which investors are interested to invest.

By applying these guidelines it is easier way to understand the financial statements of the

company, from which we can acquire the information related to the profits or losses from

the profit and loss a/c (Weygandt, Kimmel and Kieso, 2015).

This helps the investors in getting the proper information of the financial position of the

company. By this, risk and return are analyzed, they are more interested to know the

company's profits and also the security of their investments and it helps to make effective

investment decisions (Users of Financial Statements, 2015).

It also helps in determining the exact position of the company in the market. With these

employees can compare the financial position with the other companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This have positive impact on the investors, by the help of financial statement they can

evaluate the performance of the management by this they can determine the risk associate

with their investment (Robinson and et.al., 2015).

It helps in evaluating the financial strength and staying power of the company for the

customers and the suppliers.

It also helps the Board of directors, to review the financial performance of company

through financial statements.

1.4 Explaining different laws/regulations are dealt with by accounting and reporting standards

There are different laws and regulations are dealt, some of these are:

International Accounting Standards (IASs) - It was found on 1st April, 2001. They are

accounting standards which is issued by the International Accounting Standard Board (Macve,

2015). It is an older set of standards which reflect particular types of transaction and other events

in financial statement. Earlier, it was issued by the Board of International Accounting Standard

Committee.

IASB also reissue standards some of them are IAS 1 presentation of financial statements,

IAS 3- consolidated financial statements, IAS 7- statements of cash flows, etc.

International Financial Reporting Standards (IFRS) - This is designed in a common

global language for business affairs so that company's accounts are easily understandable and

comparable across the international boundaries (Armstrong and et.al., 2015). Standards which

are issued by IASC are still within use today and go by the name International Accounting

Standards. IFRS are the rules, which are followed by the company to maintain books of

accounts, which are understandable, comparable for the users.

Accounting Standards Board (ASB) - It was taken from the Accounting Standard

committee (ASC) in 1990. The role of ASB is to issue accounting standards. It was recognized

for the purpose, under the companies Act 1985. The ASB have 10 Board Members in which 2

were full-time and rest is for part-time. Votes of seven Board members were required, under the

ASB's constitution (Martin and Roychowdhury, 2015). They have the power to issue new

accounting standards. It provides a framework to solve the financial accounting and corporate

reporting issues.

evaluate the performance of the management by this they can determine the risk associate

with their investment (Robinson and et.al., 2015).

It helps in evaluating the financial strength and staying power of the company for the

customers and the suppliers.

It also helps the Board of directors, to review the financial performance of company

through financial statements.

1.4 Explaining different laws/regulations are dealt with by accounting and reporting standards

There are different laws and regulations are dealt, some of these are:

International Accounting Standards (IASs) - It was found on 1st April, 2001. They are

accounting standards which is issued by the International Accounting Standard Board (Macve,

2015). It is an older set of standards which reflect particular types of transaction and other events

in financial statement. Earlier, it was issued by the Board of International Accounting Standard

Committee.

IASB also reissue standards some of them are IAS 1 presentation of financial statements,

IAS 3- consolidated financial statements, IAS 7- statements of cash flows, etc.

International Financial Reporting Standards (IFRS) - This is designed in a common

global language for business affairs so that company's accounts are easily understandable and

comparable across the international boundaries (Armstrong and et.al., 2015). Standards which

are issued by IASC are still within use today and go by the name International Accounting

Standards. IFRS are the rules, which are followed by the company to maintain books of

accounts, which are understandable, comparable for the users.

Accounting Standards Board (ASB) - It was taken from the Accounting Standard

committee (ASC) in 1990. The role of ASB is to issue accounting standards. It was recognized

for the purpose, under the companies Act 1985. The ASB have 10 Board Members in which 2

were full-time and rest is for part-time. Votes of seven Board members were required, under the

ASB's constitution (Martin and Roychowdhury, 2015). They have the power to issue new

accounting standards. It provides a framework to solve the financial accounting and corporate

reporting issues.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.1 Explaining the information needs of different groups vary.

Information needed is varied according to the different users. Some of this information

that needed by users are:

Shareholders- They are the individuals, group that owns one or more shares in a

company. They have the potential to earn dividend if company does well (Users of Financial

Statements, 2015). To purchase the shares of the company, firstly they have to focus on the

profitability and the performance of the company. This information can be accessed from the

Profit and loss a/c of financial statements. It helps in making decision whether to invest funds in

company or not.

Government- They need information that the company is paying tax or not and this

information can be accessed from the income statements of company.

Investors- They are interested to know the company's profits and losses and also the

security of their investments. They require the information like return on investment,

creditworthiness, profitability etc, which can be evaluate from the Profit and loss a/c and also

from Balance Sheet (Hirtle and et.al., 2015).

Employees- The information which they want is to know the stability, position,

profitability as well as the sales of the company. The entire information can be acquired from the

income statements and also from Balance Sheet (Lang and Stice-Lawrence, 2015).

Suppliers and other trade creditors- They need information to know the credit

worthiness and also the numbers of creditors and short term liabilities of the company which can

be accessed from the Balance Sheet of company.

3.2 Preparing financial statements for publication by a sole trader, partnership and limited

company

There are different types of business like sole trader, partnership and limited company

(Weygandt, Kimmel and Kieso, 2015). Each business has different fundamental principles

towards preparing financial statements, which are:

Table 1: Fundamental principles towards preparing financial statements

Types of business Formats

Information needed is varied according to the different users. Some of this information

that needed by users are:

Shareholders- They are the individuals, group that owns one or more shares in a

company. They have the potential to earn dividend if company does well (Users of Financial

Statements, 2015). To purchase the shares of the company, firstly they have to focus on the

profitability and the performance of the company. This information can be accessed from the

Profit and loss a/c of financial statements. It helps in making decision whether to invest funds in

company or not.

Government- They need information that the company is paying tax or not and this

information can be accessed from the income statements of company.

Investors- They are interested to know the company's profits and losses and also the

security of their investments. They require the information like return on investment,

creditworthiness, profitability etc, which can be evaluate from the Profit and loss a/c and also

from Balance Sheet (Hirtle and et.al., 2015).

Employees- The information which they want is to know the stability, position,

profitability as well as the sales of the company. The entire information can be acquired from the

income statements and also from Balance Sheet (Lang and Stice-Lawrence, 2015).

Suppliers and other trade creditors- They need information to know the credit

worthiness and also the numbers of creditors and short term liabilities of the company which can

be accessed from the Balance Sheet of company.

3.2 Preparing financial statements for publication by a sole trader, partnership and limited

company

There are different types of business like sole trader, partnership and limited company

(Weygandt, Kimmel and Kieso, 2015). Each business has different fundamental principles

towards preparing financial statements, which are:

Table 1: Fundamental principles towards preparing financial statements

Types of business Formats

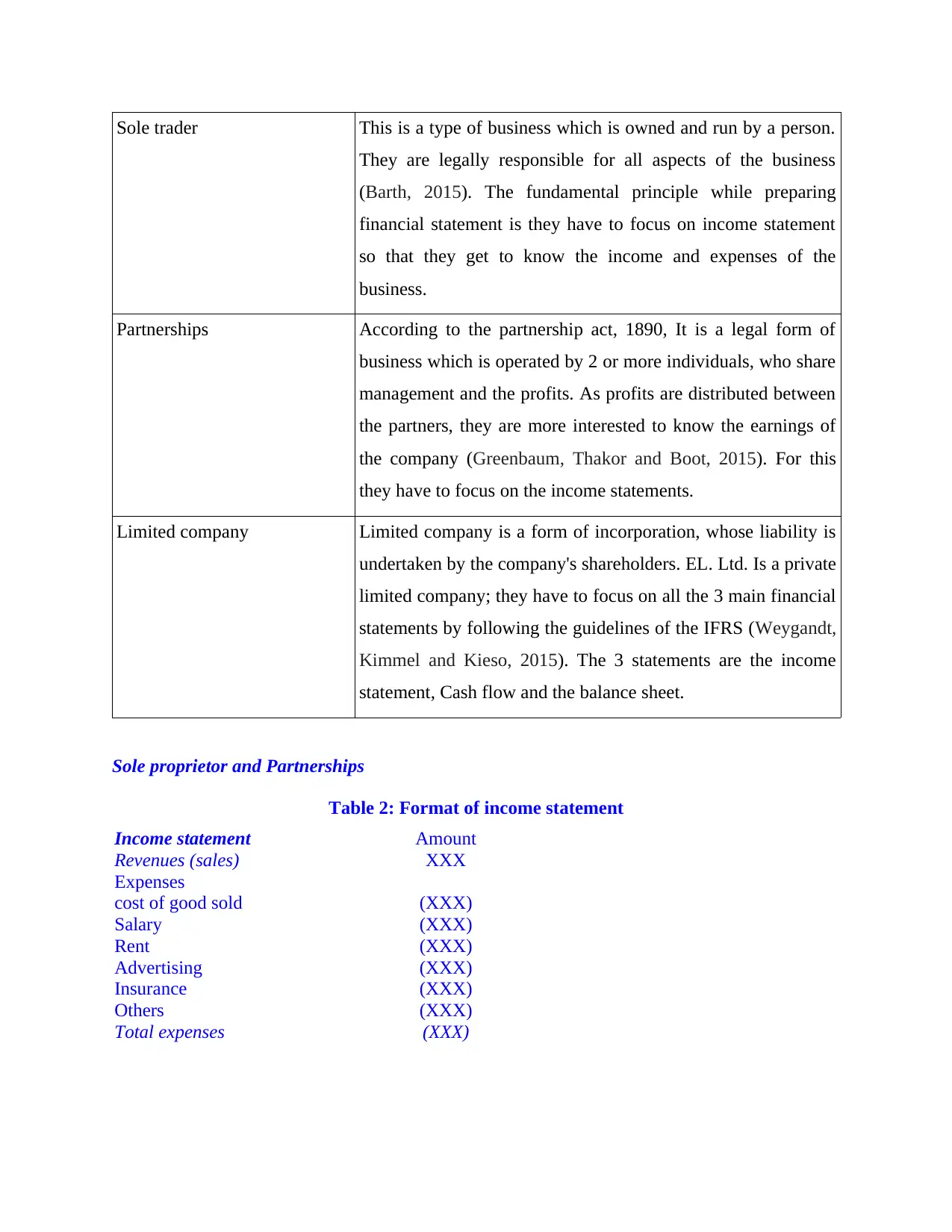

Sole trader This is a type of business which is owned and run by a person.

They are legally responsible for all aspects of the business

(Barth, 2015). The fundamental principle while preparing

financial statement is they have to focus on income statement

so that they get to know the income and expenses of the

business.

Partnerships According to the partnership act, 1890, It is a legal form of

business which is operated by 2 or more individuals, who share

management and the profits. As profits are distributed between

the partners, they are more interested to know the earnings of

the company (Greenbaum, Thakor and Boot, 2015). For this

they have to focus on the income statements.

Limited company Limited company is a form of incorporation, whose liability is

undertaken by the company's shareholders. EL. Ltd. Is a private

limited company; they have to focus on all the 3 main financial

statements by following the guidelines of the IFRS (Weygandt,

Kimmel and Kieso, 2015). The 3 statements are the income

statement, Cash flow and the balance sheet.

Sole proprietor and Partnerships

Table 2: Format of income statement

Income statement Amount

Revenues (sales) XXX

Expenses

cost of good sold (XXX)

Salary (XXX)

Rent (XXX)

Advertising (XXX)

Insurance (XXX)

Others (XXX)

Total expenses (XXX)

They are legally responsible for all aspects of the business

(Barth, 2015). The fundamental principle while preparing

financial statement is they have to focus on income statement

so that they get to know the income and expenses of the

business.

Partnerships According to the partnership act, 1890, It is a legal form of

business which is operated by 2 or more individuals, who share

management and the profits. As profits are distributed between

the partners, they are more interested to know the earnings of

the company (Greenbaum, Thakor and Boot, 2015). For this

they have to focus on the income statements.

Limited company Limited company is a form of incorporation, whose liability is

undertaken by the company's shareholders. EL. Ltd. Is a private

limited company; they have to focus on all the 3 main financial

statements by following the guidelines of the IFRS (Weygandt,

Kimmel and Kieso, 2015). The 3 statements are the income

statement, Cash flow and the balance sheet.

Sole proprietor and Partnerships

Table 2: Format of income statement

Income statement Amount

Revenues (sales) XXX

Expenses

cost of good sold (XXX)

Salary (XXX)

Rent (XXX)

Advertising (XXX)

Insurance (XXX)

Others (XXX)

Total expenses (XXX)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

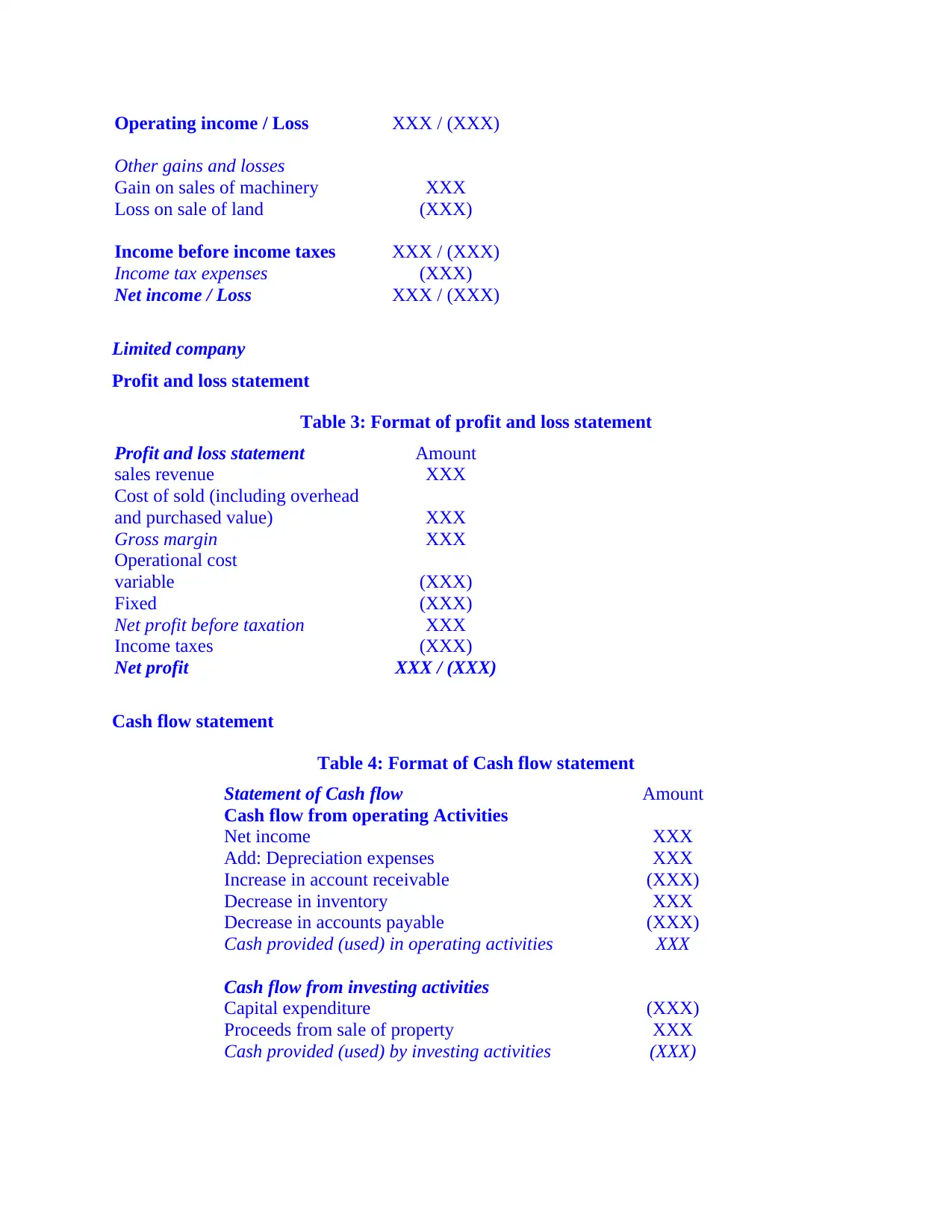

Operating income / Loss XXX / (XXX)

Other gains and losses

Gain on sales of machinery XXX

Loss on sale of land (XXX)

Income before income taxes XXX / (XXX)

Income tax expenses (XXX)

Net income / Loss XXX / (XXX)

Limited company

Profit and loss statement

Table 3: Format of profit and loss statement

Profit and loss statement Amount

sales revenue XXX

Cost of sold (including overhead

and purchased value) XXX

Gross margin XXX

Operational cost

variable (XXX)

Fixed (XXX)

Net profit before taxation XXX

Income taxes (XXX)

Net profit XXX / (XXX)

Cash flow statement

Table 4: Format of Cash flow statement

Statement of Cash flow Amount

Cash flow from operating Activities

Net income XXX

Add: Depreciation expenses XXX

Increase in account receivable (XXX)

Decrease in inventory XXX

Decrease in accounts payable (XXX)

Cash provided (used) in operating activities XXX

Cash flow from investing activities

Capital expenditure (XXX)

Proceeds from sale of property XXX

Cash provided (used) by investing activities (XXX)

Other gains and losses

Gain on sales of machinery XXX

Loss on sale of land (XXX)

Income before income taxes XXX / (XXX)

Income tax expenses (XXX)

Net income / Loss XXX / (XXX)

Limited company

Profit and loss statement

Table 3: Format of profit and loss statement

Profit and loss statement Amount

sales revenue XXX

Cost of sold (including overhead

and purchased value) XXX

Gross margin XXX

Operational cost

variable (XXX)

Fixed (XXX)

Net profit before taxation XXX

Income taxes (XXX)

Net profit XXX / (XXX)

Cash flow statement

Table 4: Format of Cash flow statement

Statement of Cash flow Amount

Cash flow from operating Activities

Net income XXX

Add: Depreciation expenses XXX

Increase in account receivable (XXX)

Decrease in inventory XXX

Decrease in accounts payable (XXX)

Cash provided (used) in operating activities XXX

Cash flow from investing activities

Capital expenditure (XXX)

Proceeds from sale of property XXX

Cash provided (used) by investing activities (XXX)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

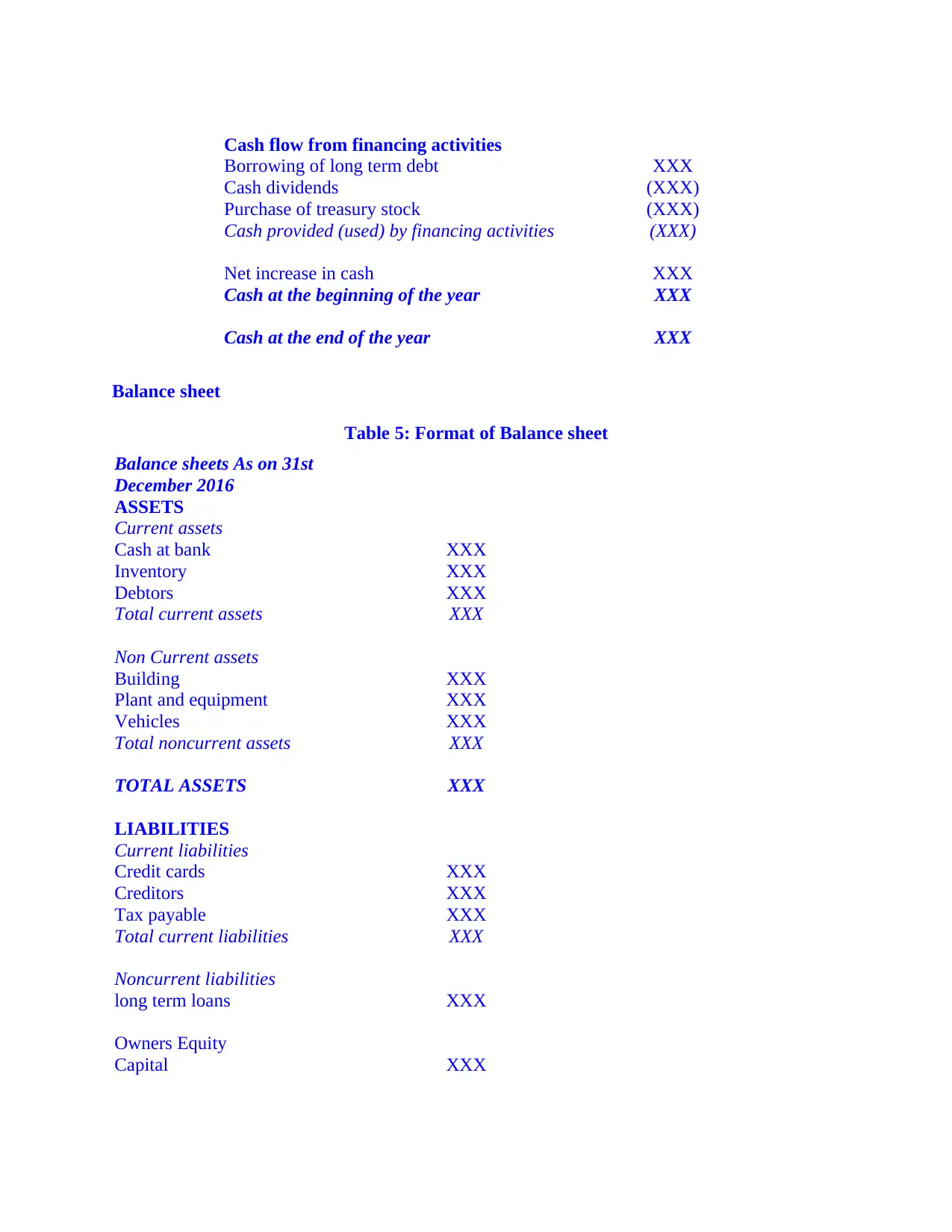

Cash flow from financing activities

Borrowing of long term debt XXX

Cash dividends (XXX)

Purchase of treasury stock (XXX)

Cash provided (used) by financing activities (XXX)

Net increase in cash XXX

Cash at the beginning of the year XXX

Cash at the end of the year XXX

Balance sheet

Table 5: Format of Balance sheet

Balance sheets As on 31st

December 2016

ASSETS

Current assets

Cash at bank XXX

Inventory XXX

Debtors XXX

Total current assets XXX

Non Current assets

Building XXX

Plant and equipment XXX

Vehicles XXX

Total noncurrent assets XXX

TOTAL ASSETS XXX

LIABILITIES

Current liabilities

Credit cards XXX

Creditors XXX

Tax payable XXX

Total current liabilities XXX

Noncurrent liabilities

long term loans XXX

Owners Equity

Capital XXX

Borrowing of long term debt XXX

Cash dividends (XXX)

Purchase of treasury stock (XXX)

Cash provided (used) by financing activities (XXX)

Net increase in cash XXX

Cash at the beginning of the year XXX

Cash at the end of the year XXX

Balance sheet

Table 5: Format of Balance sheet

Balance sheets As on 31st

December 2016

ASSETS

Current assets

Cash at bank XXX

Inventory XXX

Debtors XXX

Total current assets XXX

Non Current assets

Building XXX

Plant and equipment XXX

Vehicles XXX

Total noncurrent assets XXX

TOTAL ASSETS XXX

LIABILITIES

Current liabilities

Credit cards XXX

Creditors XXX

Tax payable XXX

Total current liabilities XXX

Noncurrent liabilities

long term loans XXX

Owners Equity

Capital XXX

Retained earning XXX

Current earnings XXX

Total owner Equity XXX

TOTAL LIABILITIES XXX

TASK 2

Note: To be completed.

TASK 3

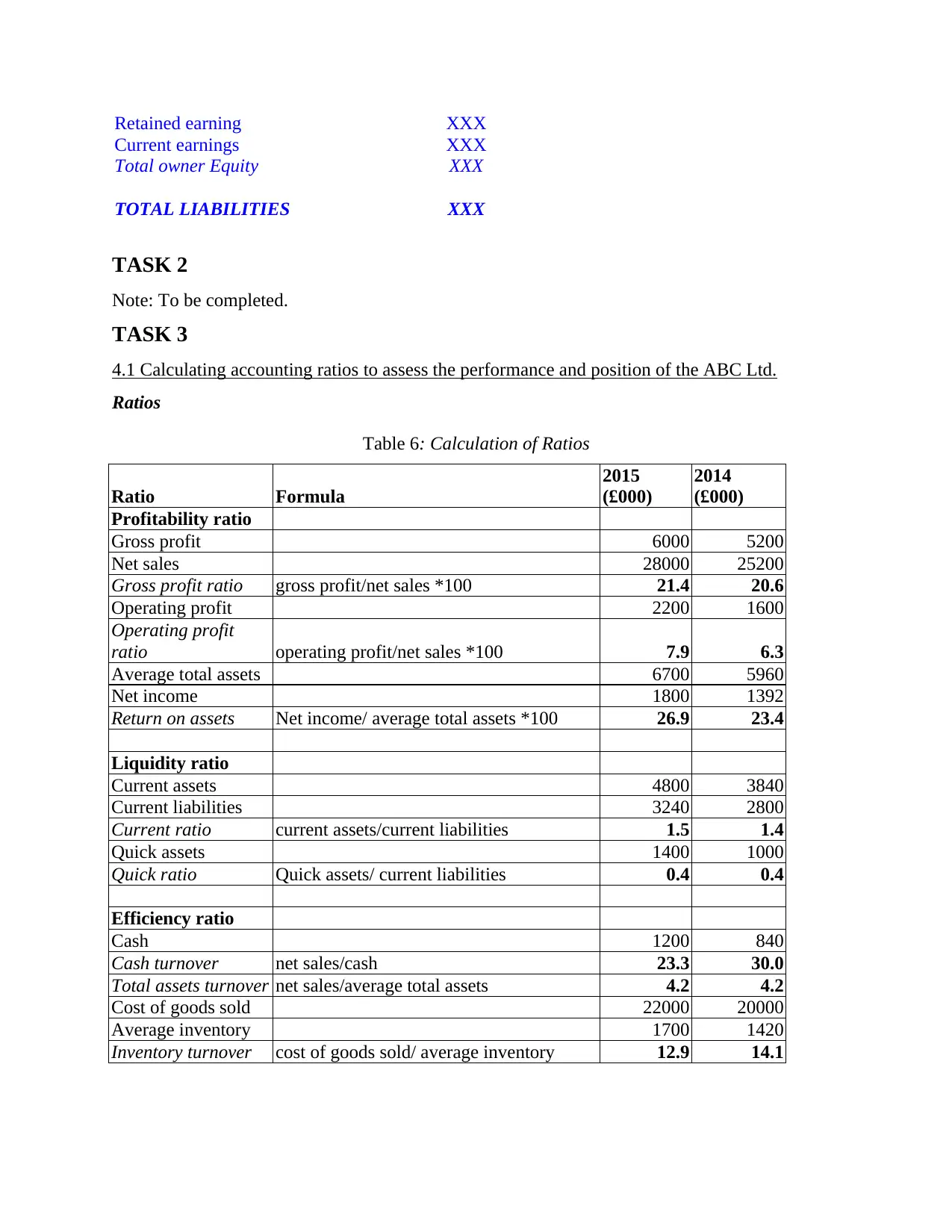

4.1 Calculating accounting ratios to assess the performance and position of the ABC Ltd.

Ratios

Table 6: Calculation of Ratios

Ratio Formula

2015

(£000)

2014

(£000)

Profitability ratio

Gross profit 6000 5200

Net sales 28000 25200

Gross profit ratio gross profit/net sales *100 21.4 20.6

Operating profit 2200 1600

Operating profit

ratio operating profit/net sales *100 7.9 6.3

Average total assets 6700 5960

Net income 1800 1392

Return on assets Net income/ average total assets *100 26.9 23.4

Liquidity ratio

Current assets 4800 3840

Current liabilities 3240 2800

Current ratio current assets/current liabilities 1.5 1.4

Quick assets 1400 1000

Quick ratio Quick assets/ current liabilities 0.4 0.4

Efficiency ratio

Cash 1200 840

Cash turnover net sales/cash 23.3 30.0

Total assets turnover net sales/average total assets 4.2 4.2

Cost of goods sold 22000 20000

Average inventory 1700 1420

Inventory turnover cost of goods sold/ average inventory 12.9 14.1

Current earnings XXX

Total owner Equity XXX

TOTAL LIABILITIES XXX

TASK 2

Note: To be completed.

TASK 3

4.1 Calculating accounting ratios to assess the performance and position of the ABC Ltd.

Ratios

Table 6: Calculation of Ratios

Ratio Formula

2015

(£000)

2014

(£000)

Profitability ratio

Gross profit 6000 5200

Net sales 28000 25200

Gross profit ratio gross profit/net sales *100 21.4 20.6

Operating profit 2200 1600

Operating profit

ratio operating profit/net sales *100 7.9 6.3

Average total assets 6700 5960

Net income 1800 1392

Return on assets Net income/ average total assets *100 26.9 23.4

Liquidity ratio

Current assets 4800 3840

Current liabilities 3240 2800

Current ratio current assets/current liabilities 1.5 1.4

Quick assets 1400 1000

Quick ratio Quick assets/ current liabilities 0.4 0.4

Efficiency ratio

Cash 1200 840

Cash turnover net sales/cash 23.3 30.0

Total assets turnover net sales/average total assets 4.2 4.2

Cost of goods sold 22000 20000

Average inventory 1700 1420

Inventory turnover cost of goods sold/ average inventory 12.9 14.1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.